Power Semiconductor Market Size, Share, Trends and Forecast by Component, Material, End Use Industry, and Region 2026-2034

Global Power Semiconductor Market Size, Share, Trends & Forecast (2026-2034)

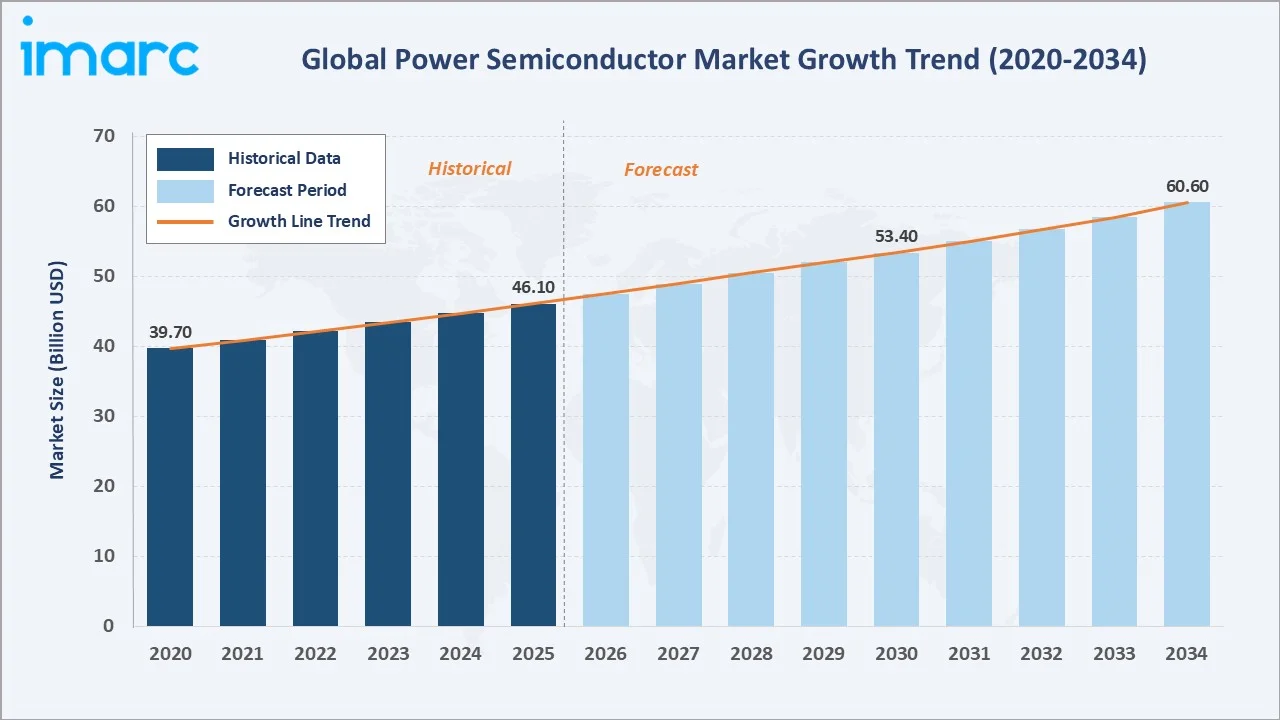

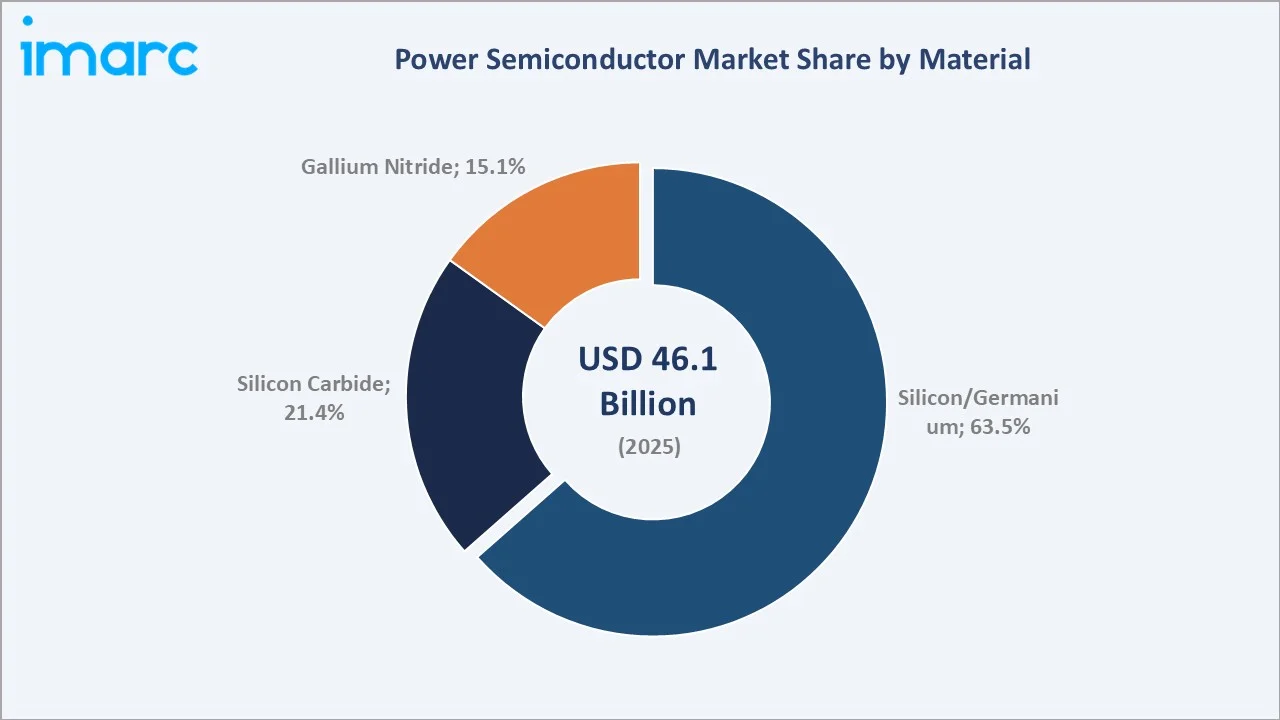

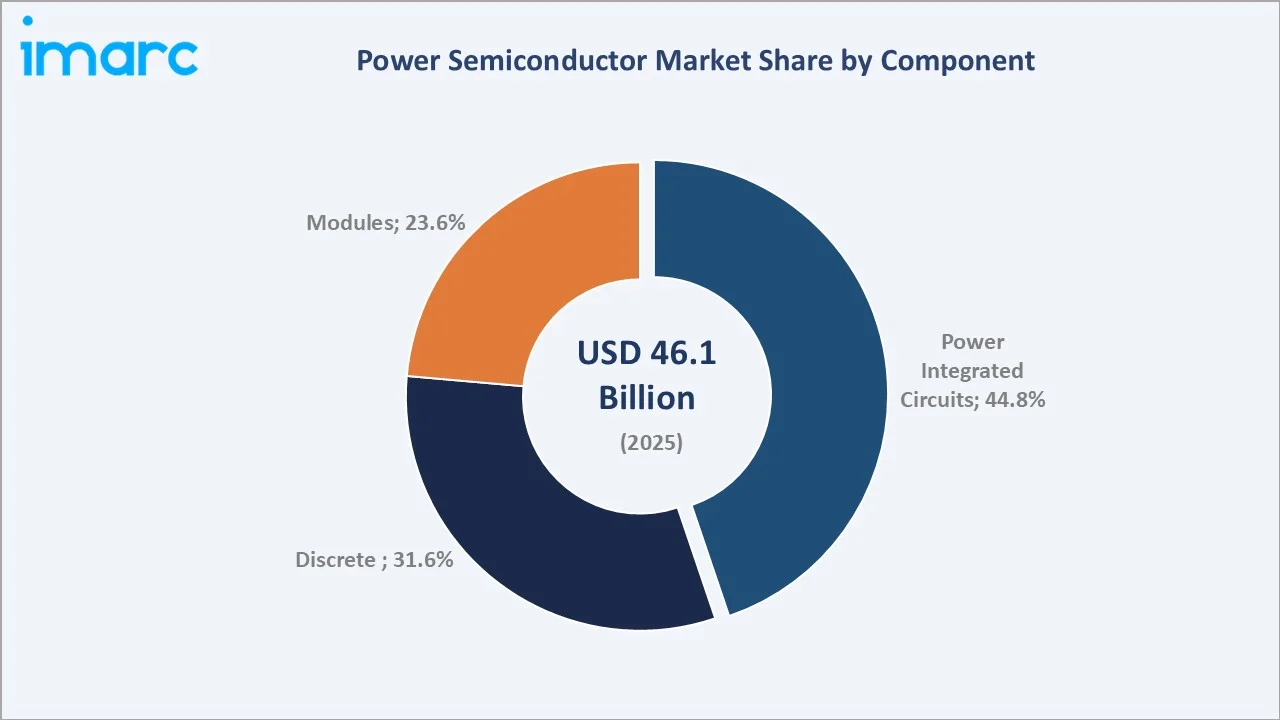

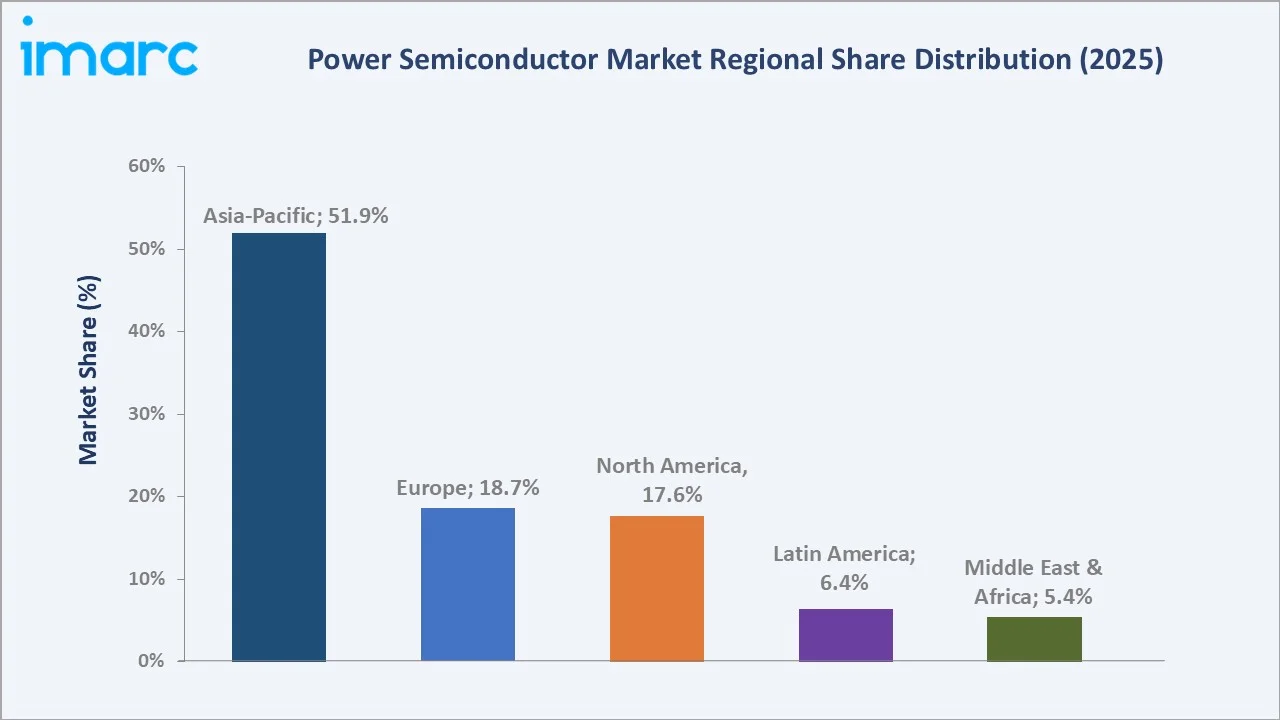

The global power semiconductor market size was valued at USD 46.1 Billion in 2025 and is projected to reach USD 60.6 Billion by 2034, exhibiting a CAGR of 3.00% during the forecast period 2026-2034. The power semiconductor market growth is propelled by surging electric-vehicle production, accelerating renewable-energy buildout, 5G network deployment, AI data-center power demand, and the accelerating adoption of wide-bandgap materials. Silicon/Germanium leads materials at 63.5% share in 2025, while Power Integrated Circuits dominate component demand at 44.8%. Asia-Pacific dominates with 51.9% of global revenue in 2025, anchored by China, Japan, South Korea, and Taiwan's electronics manufacturing scale.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 46.1 Billion |

|

Forecast Market Size (2034) |

USD 60.6 Billion |

|

CAGR (2026-2034) |

3.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (51.9% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR 4.2%) |

|

Leading Material |

Silicon/Germanium (63.5%, 2025) |

|

Leading Component |

Power Integrated Circuits (44.8%, 2025) |

The global power semiconductor market growth trajectory from 2020 through 2034 reflects a steady climb, supported by sustained demand from electric vehicles, renewable inverters, industrial motor drives, and next-generation data-center power delivery.

To get more information on this market, Request Sample

Segment-level CAGR benchmarks highlight Gallium Nitride and Silicon Carbide as the fastest-growing categories within the global power semiconductor market forecast through 2034, substantially outpacing the blended 3.00% industry growth rate.

Executive Summary

The global power semiconductor market is undergoing a structural shift as wide-bandgap (WBG) materials begin to capture share from mature silicon platforms. Valued at USD 46.1 Billion in 2025, the market is forecast to reach USD 60.6 Billion by 2034 at a CAGR of 3.00%. Electric-vehicle electrification, renewable-energy buildout, and data-center power delivery are the strongest multi-year growth anchors through 2034.

Silicon/Germanium commands 63.5% share of materials in 2025, reflecting its dominance across consumer, industrial, and legacy automotive applications. Silicon Carbide (21.4%) and Gallium Nitride (15.1%) are expanding rapidly, with SiC forecast to grow at approximately 8.4% CAGR and GaN at 11.6% CAGR through 2034, powered by EV powertrains, fast-charging infrastructure, and high-efficiency data-center power supplies.

Power Integrated Circuits lead component demand at 44.8% of global revenue, followed by Discrete devices (31.6%) and Modules (23.6%). Asia-Pacific anchors global demand with 51.9% revenue share in 2025, supported by China's electronics manufacturing scale, Japanese and Korean automotive semiconductors, and Taiwan's foundry base. Europe (18.7%) and North America (17.6%) follow, led by industrial and automotive electrification programs. The power semiconductor market outlook remains positive through 2034 despite near-term inventory cyclicality.

Key Market Insights

|

Insight |

Data |

|

Largest Material |

Silicon/Germanium - 63.5% share (2025) |

|

Fastest Growing Material |

Gallium Nitride (GaN) - 11.6% CAGR (2026-2034) |

|

Largest Component |

Power Integrated Circuits - 44.8% share (2025) |

|

Leading Region |

Asia-Pacific - 51.9% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific - 4.2% CAGR (2026-2034) |

|

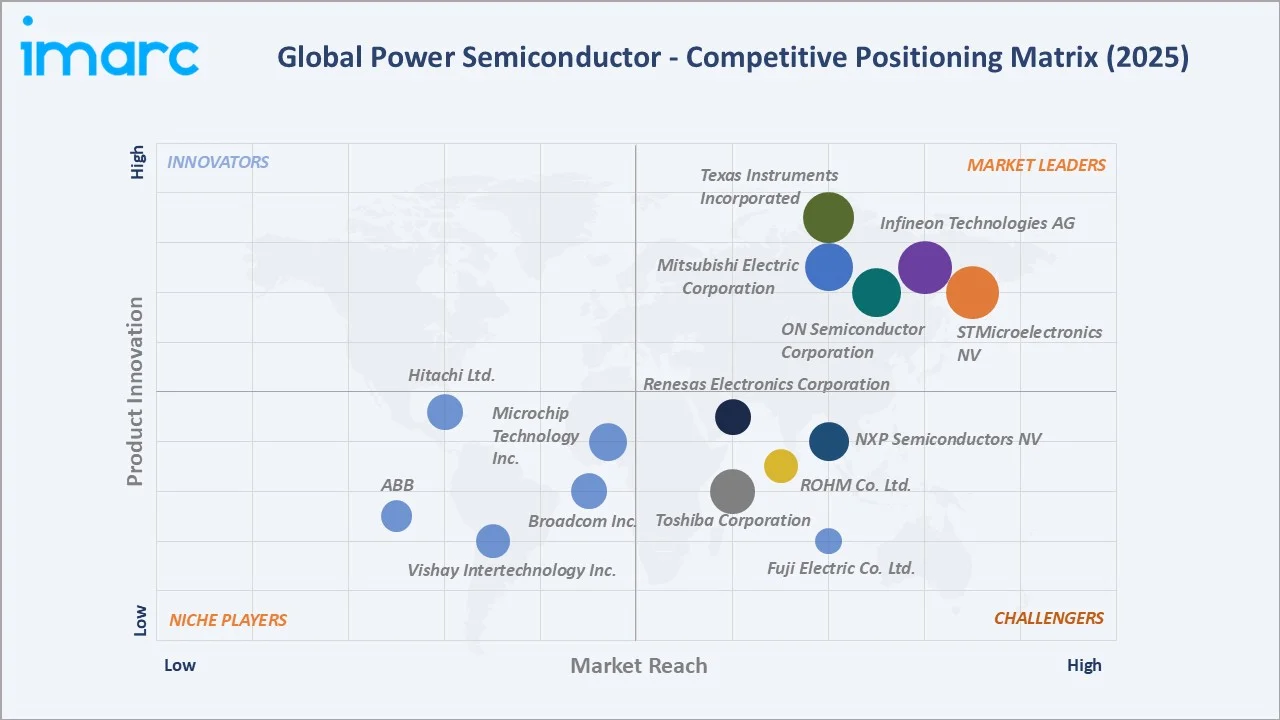

Top Companies |

Infineon Technologies AG, STMicroelectronics NV, ON Semiconductor Corporation, Texas Instruments Incorporated, Mitsubishi Electric Corporation |

Key Analytical Observations Supporting the Above Data:

- Silicon/Germanium's 63.5% dominance in 2025 reflects its cost-efficient maturity across consumer electronics, industrial motor drives, and legacy automotive platforms. Over 90% of installed power switching infrastructure globally still runs on silicon-based devices.

- SiC's 21.4% and GaN's 15.1% combined share: The global semiconductor industry is experiencing a strong growth cycle, with total sales reaching USD 791.7 billion in 2025, up from USD 630.5 billion in 2024, reflecting robust demand across key end markets. Quarterly momentum remained strong, with Q4 sales at USD 236.6 billion, while monthly sales reached USD 78.9 billion in December 2025. The industry is projected to approach USD 1 trillion in annual sales by 2026, underscoring a structural upcycle driven by advanced technologies and expanding applications.

- Power ICs' 44.8% share is underpinned by power management ICs (PMICs) and gate drivers shipping into smartphones, laptops, automotive ECUs, and industrial controllers. Global PMIC shipments reached multi-billion-unit scale in 2024, driven by strong demand across consumer electronics, automotive, and industrial applications, with Asia-Pacific accounting for a significant share of global production and consumption.

- Asia-Pacific's 51.9% global dominance reflects China's EV manufacturing leadership, Japan's automotive semiconductor scale (Toshiba, Mitsubishi, ROHM, Renesas), South Korea's consumer electronics base, and Taiwan's wafer foundry dominance (TSMC, Vanguard, PSMC).

- Automotive is the fastest-growing end-use industry accounting for over 30% of power semiconductor demand in 2025. Global plug-in electric-vehicle sales crossed 17 million units in 2024 per IEA, requiring 5-10x more power semiconductor content than conventional ICE vehicles.

- Top 5 vendor concentration (Infineon, STMicroelectronics, onsemi, Texas Instruments, Mitsubishi Electric) is estimated at almost half of global power semiconductor revenue in 2024, indicating a moderately concentrated competitive structure.

Global Power Semiconductor Market Overview

Power semiconductors are specialized electronic devices designed to switch, convert, and control electrical power efficiently across a wide range of voltages, currents, and frequencies. The global market spans discrete devices (MOSFETs, IGBTs, diodes, thyristors), power modules, and power integrated circuits (PMICs, gate drivers, regulators). Product materials include traditional silicon and germanium as well as emerging wide-bandgap substrates such as silicon carbide (SiC) and gallium nitride (GaN). Applications extend across automotive, industrial, consumer electronics, power and energy, IT and telecommunications, military and aerospace, and other segments.

The industry operates at the convergence of energy efficiency, electrification, and digital transformation. Macroeconomic drivers include accelerating EV adoption (17+ million plug-in EVs sold globally in 2024), renewable-energy installations exceeding 560 GW added in 2024 per IRENA, 5G rollout covering more than 2.2 billion connections in 2024, and data-center power density growth driven by AI compute. Policy tailwinds such as the U.S. CHIPS and Science Act, the EU Chips Act, and China's semiconductor self-sufficiency programs are reshaping global capacity investment through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

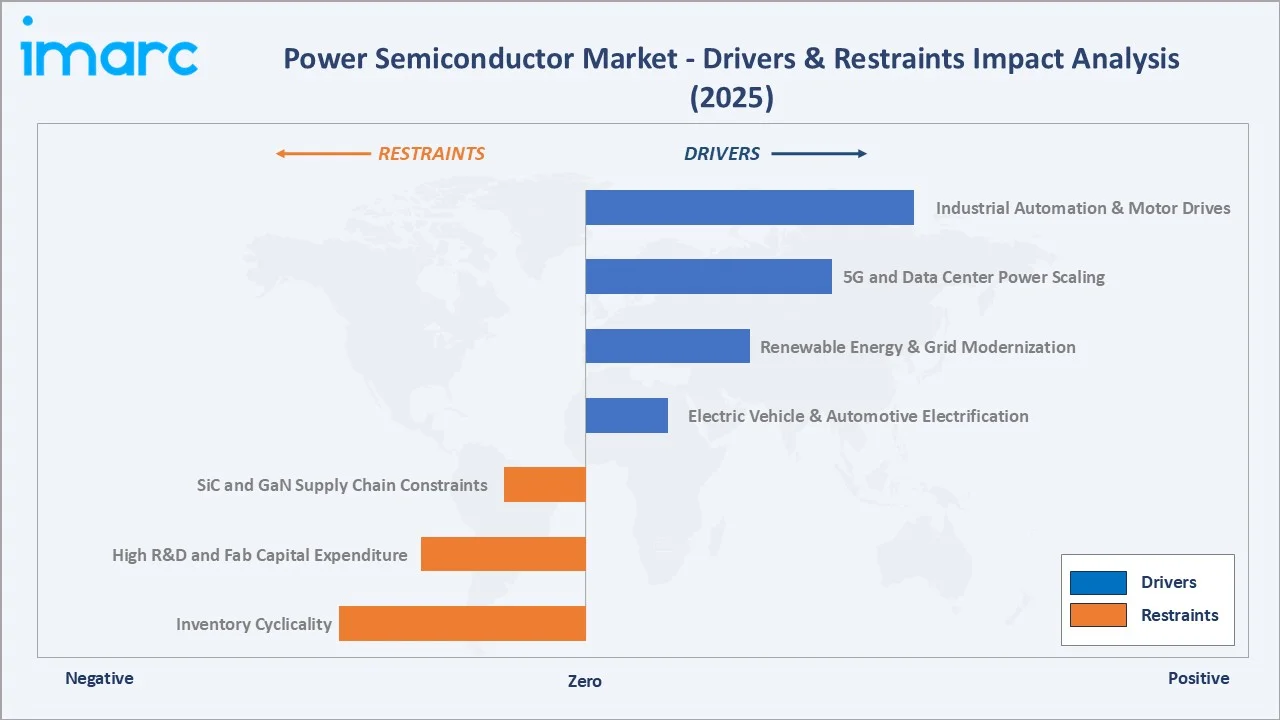

Market Drivers

- Electric Vehicle and Automotive Electrification: Global plug-in EV sales exceeded 17 million units in 2024 per IEA. Each EV requires USD 450-750 of power semiconductor content versus USD 80-100 for a conventional ICE vehicle, making automotive the single largest growth anchor through 2034.

- Renewable Energy and Grid Modernization: Global renewable capacity additions topped 560 GW in 2024 per IRENA. Solar inverters, wind converters, and grid-scale energy storage systems are driving sustained high-voltage power semiconductor demand.

- 5G and Data Center Power Scaling: AI server deployments are driving data-center rack power densities above 50 kW, compared to 8-12 kW legacy ranges. High-efficiency power delivery using GaN and SiC devices is becoming critical, with data-center power semiconductor revenue growing in the high-teens CAGR through 2030.

- Industrial Automation and Motor Drives: Global industrial motor drive shipments have reached significant scale, reflecting strong demand across manufacturing and energy-intensive industries. At the same time, IGBTs and silicon carbide–based modules are increasingly replacing legacy silicon platforms, enabling more energy-efficient operation in line with tightening regulations such as the EU Ecodesign Directive and standards from the U.S. Department of Energy.

Consumer electronics, USB-PD fast chargers, and wireless-charging applications add incremental demand. Integrated GaN power stages are becoming mainstream in high-wattage (65W-140W) fast chargers shipping with premium smartphones and laptops from leading OEMs through 2025.

Market Restraints

- SiC and GaN Supply Chain Constraints: SiC substrate availability remains tight, with leading wafer suppliers Wolfspeed, Coherent, and SiCrystal running multi-quarter lead times. The 200mm SiC wafer transition is not yet fully scaled, limiting device cost-down curves through 2026.

- High R&D and Fab Capital Expenditure: Semiconductor fabrication costs vary significantly by wafer size, with 200mm fabs typically requiring lower capital investment, while 300mm facilities demand substantially higher upfront spending due to advanced equipment, automation, and process complexity. This sharp increase in capital intensity creates high entry barriers and longer payback cycles, limiting participation to large, well-capitalized players.

- Inventory Cyclicality: The 2023-2024 automotive and industrial inventory correction compressed vendor revenues temporarily. Infineon, STMicroelectronics, and onsemi all reported near-term revenue pressure in Q4 2024 and H1 2025 as customers worked down elevated channel inventories.

- Export Controls and Geopolitical Compliance: U.S., EU, and Japanese export controls on advanced semiconductors, including select power device technologies, have increased compliance burden. Export licensing requirements for shipments to mainland China affect supply planning for leading global vendors.

Market Opportunities

- 800V EV Architectures: OEM shift to 800V EV platforms (Porsche Taycan, Hyundai E-GMP, Kia EV6, Lucid Air) is accelerating SiC adoption. 800V powertrains enable faster charging, lower cabling mass, and improved efficiency, driving a premium SiC device opportunity through 2030.

- GaN in Data-Center and AI Power: GaN FETs in 48V-to-12V and 48V-direct point-of-load converters for AI servers represent an emerging multi-billion-dollar opportunity. Leading hyperscalers including Microsoft, Google, and AWS are validating GaN designs for next-generation rack architectures.

Market Challenges

- Design-In Cycle Complexity: Transitioning from silicon IGBTs to SiC MOSFETs requires redesign of gate drivers, thermal management, and packaging. Design-in cycles can extend 18-30 months, slowing broad adoption even where performance advantages are clear.

- Reliability and Qualification Standards: Automotive AEC-Q101 qualification for new SiC and GaN devices remains rigorous, with Tier-1 suppliers requiring field-proven reliability before large-scale production commitments. This extends commercialization timelines for new products.

- Talent and Engineering Bottlenecks: SEMI estimates a global semiconductor workforce gap of 300,000+ engineers by 2030. Power electronics design talent is particularly constrained, limiting vendor capacity to scale SiC and GaN product roadmaps as quickly as end-market demand permits.

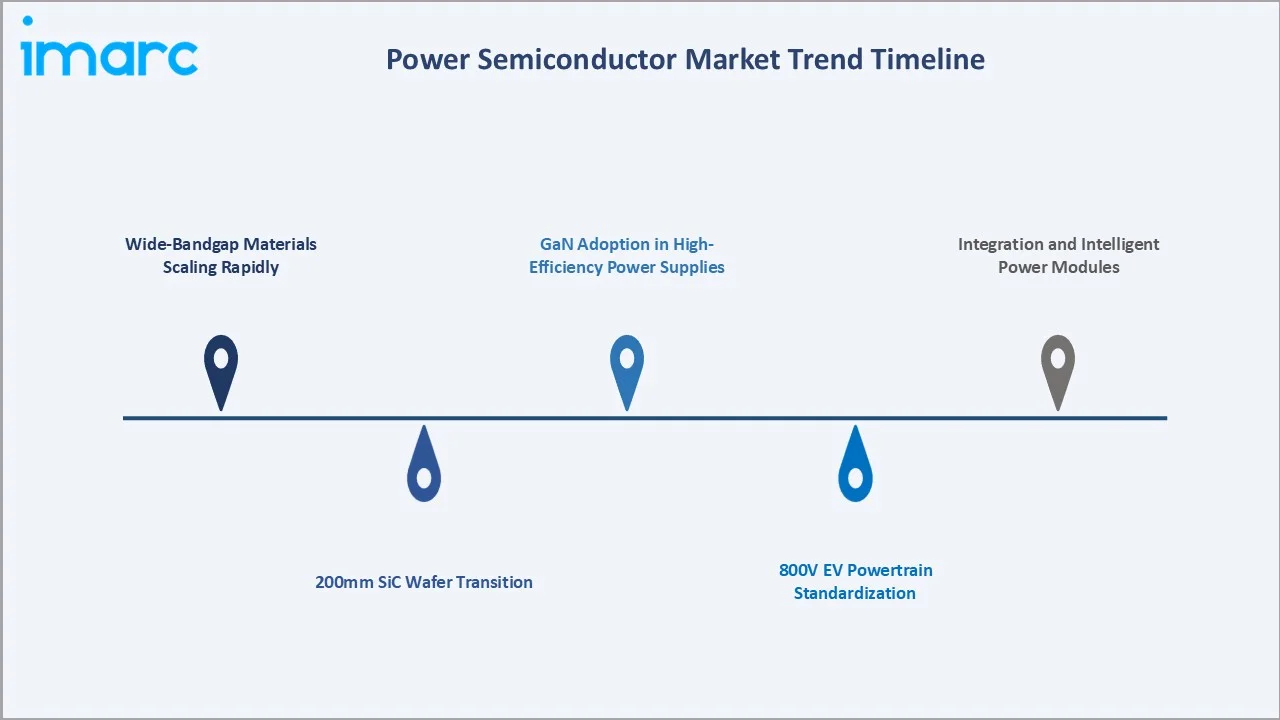

Emerging Market Trends

1. Wide-Bandgap Materials Scaling Rapidly

Silicon carbide continues to scale rapidly as a core wide-bandgap technology, with market momentum expected to drive substantial expansion through the end of the decade. At the same time, GaN power devices are witnessing strong year-on-year growth, driven by applications such as fast-charging adapters and high-frequency power electronics. Overall, wide-bandgap materials are transitioning from early adoption to broader commercial deployment, particularly across automotive electrification and advanced power supply applications.

2. 200mm SiC Wafer Transition

The industry is transitioning from 150mm to 200mm SiC substrates. Wolfspeed's Mohawk Valley fab in New York and STMicroelectronics-Soitec partnership in France are flagship 200mm capacity builds targeting commercial ramp during 2025-2027.

3. 800V EV Powertrain Standardization

Leading global OEMs are standardizing on 800V electrical architectures, including Porsche, Hyundai-Kia, Lucid, and emerging Chinese EV brands. 800V platforms reduce charging time, improve efficiency, and fully leverage SiC's voltage advantages, driving premium-segment device ASPs and multi-year volume commitments.

4. GaN Adoption in High-Efficiency Power Supplies

GaN FET adoption is accelerating across 65W-240W consumer fast chargers, 48V server power delivery, and solar microinverters. Navitas Semiconductor, GaN Systems (acquired by Infineon in 2023), and Innoscience are scaling GaN capacity aggressively, driving unit cost declines and commercial proliferation.

5. Integration and Intelligent Power Modules

Intelligent power modules (IPMs) and system-in-package (SiP) integration are capturing growing share. Combining gate drivers, protection, sensing, and power switching into a single module simplifies system design, reduces board space, and is gaining particular traction in industrial motor drives and EV auxiliary inverters.

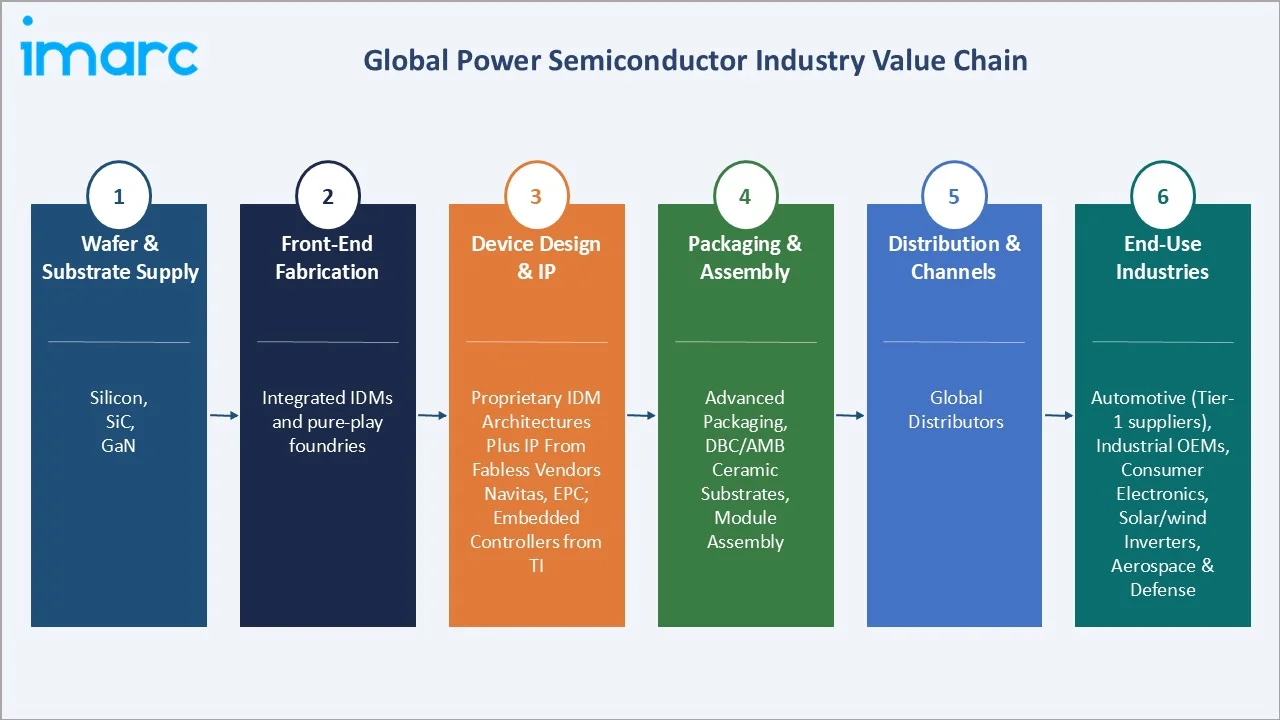

Industry Value Chain Analysis

The global power semiconductor value chain spans six integrated stages from wafer substrate supply through end-user product integration. Each stage presents distinct competitive dynamics, capital intensity, and margin profiles relevant to the overall power semiconductor market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Wafer & Substrate Supply |

Silicon (Shin-Etsu, SUMCO, GlobalWafers), SiC (Wolfspeed, Coherent, Resonac, SiCrystal), GaN (IQE) |

|

Front-End Fabrication |

Integrated IDMs (Infineon, STMicro, onsemi, Toshiba, Mitsubishi) and pure-play foundries (TSMC, Vanguard, GlobalFoundries) supporting power device wafers |

|

Device Design & IP |

Proprietary IDM architectures plus IP from fabless vendors including Navitas, EPC, and GaN-specialists; embedded controllers from TI, Microchip |

|

Packaging & Assembly |

Advanced packaging (ASE, Amkor, JCET), DBC/AMB ceramic substrates (Heraeus, Rogers), and module assembly at IDMs |

|

Distribution & Channels |

Global distributors Arrow, Avnet, Future Electronics, WPG, Digi-Key serving fragmented design-in customer base |

|

End-Use Industries |

Automotive (Tier-1 suppliers), industrial OEMs, consumer electronics, solar and wind inverter makers, and aerospace & defense contractors |

Integrated device manufacturers (IDMs) hold the highest strategic value through vertical integration across design, fabrication, packaging, and qualification. Meanwhile, substrate and wafer suppliers form the critical bottleneck in wide-bandgap device scaling, with leading SiC substrate makers commanding premium margins and multi-year customer commitments through 2028.

Technology Landscape in the Power Semiconductor Industry

Silicon IGBTs and Super-Junction MOSFETs

IGBTs and super-junction MOSFETs remain the workhorse technologies for medium-voltage (600V-1700V) power switching. Seventh-generation IGBTs from Infineon, Mitsubishi, and Fuji Electric deliver lower switching losses and higher current density, sustaining competitiveness against SiC in cost-sensitive applications. Super-junction MOSFETs dominate in the 500V-900V industrial and server power supply range.

Silicon Carbide (SiC) MOSFETs and Schottky Diodes

SiC MOSFETs offer 3-5x lower switching losses and 5-10x faster switching frequencies versus silicon equivalents. Automotive qualified 1200V and 1700V SiC devices are standard in EV traction inverters, onboard chargers, and DC fast-charging. Wolfspeed, STMicroelectronics, Infineon, onsemi, and ROHM are the leading SiC device suppliers in 2025.

Gallium Nitride (GaN) FETs

GaN-on-silicon and GaN-on-SiC platforms enable switching speeds above 1 MHz, with strong momentum in consumer fast chargers, data-center 48V power delivery, and lidar. Infineon's 2023 acquisition of GaN Systems, combined with STMicroelectronics' France-based GaN fab, signal accelerated capacity investment through 2027.

Intelligent Power Modules and Packaging

Intelligent power modules integrate gate drivers, protection circuits, and sensing alongside power switches. Advanced packaging technologies such as direct bonded copper (DBC), active metal brazing (AMB), and silver sintering are enabling higher thermal performance, critical for SiC and high-current IGBT module designs in automotive and industrial applications.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the global power semiconductor market, along with forecasts at the global, regional, and country levels from 2026 to 2034. The market has been categorized based on material and component.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Component | Power Integrated Circuits | 44.8% |

2025 |

| Material | Silicon/Germanium | 63.5% |

2025 |

| End Use Industry | Consumer Electronics |

🔒 |

2025 |

| Region | Asia-Pacific | 51.9% |

2025 |

By Material

Silicon/Germanium leads the global power semiconductor market material segment with a 63.5% share in 2025. Silicon remains the dominant platform across consumer electronics, legacy automotive, industrial motor drives, and general-purpose switching applications due to its mature supply base, cost efficiency, and wide design-in footprint. Seventh-generation IGBTs and super-junction MOSFETs continue to extend silicon's competitive life against wide-bandgap alternatives in the 600V-1700V range.

To access detailed market analysis, Request Sample

Silicon Carbide (SiC) accounts for 21.4% of global materials demand and is the second-fastest growing material segment, advancing at an estimated 8.4% CAGR through 2034. SiC market is expected to exceeded USD 14 billion in 2031 per Yole Group, with onboard chargers, and DC fast-charging stations. Gallium Nitride (GaN) holds 15.1% share and is the overall fastest-growing material at 11.6% CAGR, driven by adoption in high-efficiency power supplies, consumer fast chargers, and 48V data-center power architectures.

By Component

Power Integrated Circuits dominate the component segmentation at 44.8% of global revenue in 2025. Power management ICs (PMICs), gate drivers, DC-DC regulators, and embedded power controllers form the bulk of this segment, shipping across smartphones, notebooks, automotive ECUs, industrial controllers, and IoT devices. Global PMIC shipments reached multi-billion unit scale in 2024, driven by strong demand across consumer electronics, automotive, and industrial applications, with Asia-Pacific accounting for a significant share of global volume.

Discrete devices account for 31.6% of global demand, encompassing MOSFETs, IGBTs, diodes, thyristors, and rectifiers. Discrete demand is anchored by consumer fast-charging adapters, industrial SMPS, and automotive body electronics. Modules represent 23.6% of the market and are the fastest-growing component category at an estimated 3.5% CAGR through 2034. IGBT and SiC-based modules are scaling rapidly in EV traction inverters, solar inverters, wind power converters, and industrial motor drives, where integrated module architecture deliver superior thermal and reliability performance.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

51.9% |

China EV scale, Japan/Korea IDMs, Taiwan foundries, India semiconductor policy |

|

Europe |

18.7% |

Germany automotive, EU Chips Act, renewable-energy buildout, industrial automation |

|

North America |

17.6% |

US CHIPS Act, data-center AI power, EV growth, military & aerospace |

|

Latin America |

6.4% |

Mexico nearshoring, Brazil industrial automation, automotive assembly hubs |

|

Middle East & Africa |

5.4% |

Saudi Arabia industrial diversification, UAE data centers, South Africa mining |

Asia-Pacific commands 51.9% global revenue share in 2025, by far the largest of any region. China anchors the market with its world-leading EV production (over 11 million NEVs sold in 2024 per CAAM), expanding solar manufacturing (over 80% of global PV module supply), and state-backed semiconductor self-sufficiency programs. Japan's IDMs (Toshiba, Mitsubishi Electric, Fuji Electric, ROHM, Renesas) lead global IGBT and SiC module supply, while South Korea's consumer electronics and Taiwan's foundry base (TSMC, Vanguard) complete the regional ecosystem.

Asia-Pacific is also forecast to be the fastest-growing region at an estimated 4.2% CAGR through 2034. India's semiconductor push under the Semicon India Programme, with over 1.6 Lakh Crore in approved fab and ATMP investments by 2024, is adding a new national growth engine. Micron's Sanand ATMP facility and Tata Electronics' Dholera fab are flagship projects scheduled for phased commissioning through 2027.

Europe holds 18.7% of global revenue, anchored by Germany's automotive semiconductor leadership (Infineon, Bosch), STMicroelectronics' multi-country footprint, and NXP's automotive processor base. The EU Chips Act, approved in September 2023 with EUR 43 billion of public-private funding, is accelerating regional capacity expansion, including ESMC's Dresden fab (TSMC-led) and Infineon's Kulim, Malaysia + Villach, Austria investments.

North America accounts for 17.6% of global revenue, anchored by U.S. CHIPS Act funding (USD 52.7 billion program). Texas Instruments, onsemi, Wolfspeed, and Microchip are scaling U.S. manufacturing, with Wolfspeed's Mohawk Valley facility being the world's first fully automated 200mm SiC fab. Data-center AI power demand, EV growth, and military & aerospace applications sustain premium growth.

Latin America represents 6.4% of global demand, led by Mexico's automotive assembly hubs and Brazil's industrial electronics base. Nearshoring under USMCA is driving semiconductor demand in Mexican Tier-1 automotive suppliers. Middle East & Africa accounts for 5.4%, driven by Saudi Arabia's Vision 2030 industrial diversification, UAE data-center expansion (Khazna, G42), and emerging electronics manufacturing initiatives in South Africa, Egypt, and Morocco.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Infineon Technologies AG |

Infineon Technologies |

Leader |

Global #1 power semiconductor, strong SiC & automotive |

|

STMicroelectronics NV |

STMicroelectronics |

Leader |

SiC leadership, automotive & industrial breadth |

|

ON Semiconductor Corporation |

Onsemi |

Leader |

SiC vertical integration, automotive scale |

|

Texas Instruments Incorporated |

Texas Instruments |

Leader |

Power management ICs, analog & mixed-signal strength |

|

Mitsubishi Electric Corporation |

Mitsubishi Electric |

Leader |

Industrial & traction IGBT modules leadership |

|

Toshiba Corporation |

Toshiba Electronic Devices & Storage Corporation |

Challenger |

Discrete MOSFETs, IGBTs, Japan manufacturing base |

|

ROHM Co. Ltd. |

ROHM Semiconductor |

Challenger |

Early SiC innovator, automotive & industrial reach |

|

NXP Semiconductors NV |

NXP Semiconductors |

Challenger |

Automotive processors, integrated power platforms |

|

Renesas Electronics Corporation |

Renesas Electronics |

Challenger |

Automotive MCUs, integrated power management |

|

Fuji Electric Co. Ltd. |

Fuji Electric |

Challenger |

Industrial IGBTs, solar & wind inverter modules |

|

Hitachi Ltd. |

Hitachi Energy |

Emerging |

Rail traction, industrial and grid applications |

|

Microchip Technology Inc. |

Microchip |

Emerging |

Embedded controllers, SiC acquisition via Microsemi |

|

Broadcom Inc. |

Broadcom |

Emerging |

ICs for enterprise IT, specialty power |

|

Vishay Intertechnology Inc. |

Vishay Intertechnology |

Emerging |

Discrete MOSFETs, diodes, broad product catalog |

|

ABB |

ABB |

Emerging |

High-power modules for traction and grid systems |

The global power semiconductor market's competitive landscape is moderately concentrated, with European, Japanese, and U.S. IDMs leading through vertical integration across design, fabrication, packaging, and qualification. Infineon's 2023 acquisition of GaN Systems, STMicroelectronics' joint venture with Soitec for SiC substrates, and Wolfspeed's Mohawk Valley ramp represent defining competitive moves shaping wide-bandgap leadership through 2030. Onsemi's vertical SiC integration through the Hudson Fab in New Hampshire also underscores the shift toward owning the full SiC supply chain.

Key Company Profiles

Infineon Technologies AG

Infineon Technologies AG is the world's largest power semiconductor supplier, headquartered in Neubiberg, Germany. Founded in 1999 as a Siemens spinoff, Infineon operates across automotive, industrial, power & sensor systems, and connected secure systems divisions, with a presence in over 50 countries.

- Product & Platform Portfolio: Infineon's power portfolio spans CoolMOS super-junction MOSFETs, TrenchStop IGBTs, CoolSiC MOSFETs and diodes, and CoolGaN power HEMT devices. It also supplies gate drivers, power management ICs, and intelligent power modules for automotive, industrial, and consumer applications.

- Recent Developments: In February 2025, First 200mm SiC products shipped. Infineon began shipping its first power devices manufactured on 200mm silicon carbide wafers from its Villach, Austria fab, targeting high-voltage applications in renewable energy, rail, and EVs. Infineon positioned the move as a step toward improved cost efficiency and scaled capacity, with Kulim ramping in phases behind it

- Strategic Focus: Infineon's strategy centers on automotive electrification leadership, wide-bandgap scaling across SiC and GaN, and expansion of power management ICs serving data center, renewable, and industrial applications through 2034.

STMicroelectronics N.V.

STMicroelectronics is a Europe-based global semiconductor leader, headquartered in Geneva, Switzerland, with operations across 35+ countries. The company is a leading supplier of SiC power devices and serves automotive, industrial, personal electronics, and communications markets.

- Product & Platform Portfolio: ST's portfolio includes STPOWER SiC MOSFETs, STi2GaN power ICs, MDmesh super-junction MOSFETs, IGBTs, gate drivers, and power management ICs. Its Catania, Italy SiC fab is one of the world's largest integrated SiC manufacturing sites.

- Recent Developments: In July 2025, ST entered into an agreement to acquire NXP Semiconductors' MEMS sensor business for up to US$950 million (US$900 million upfront and up to US$50 million in milestone-contingent payments), targeting automotive safety and industrial sensing.

- Strategic Focus: ST's strategy emphasizes SiC vertical integration, expansion of automotive-qualified power devices, and GaN scaling through its joint manufacturing site in Tours, France. The company targets USD 20 billion in annual revenue by 2027-2030.

ON Semiconductor Corporation

ON Semiconductor Corporation is a leading U.S. semiconductor company, headquartered in Scottsdale, Arizona. The company has strategically repositioned intelligent power and sensing, with automotive and industrial customers forming over 80% of revenue in 2024.

- Product & Platform Portfolio: ON Semiconductor Corporation portfolio includes EliteSiC SiC MOSFETs, modules, and diodes, NCP family power management ICs, IGBTs, and intelligent power modules. Its vertical integration spans substrate, epitaxy, device fabrication, and module assembly.

- Recent Developments: In April 2025, onsemi terminated its pursuit of Allegro, citing the reluctance of Allegro's board to engage and explore the proposal, and redirected capital to its existing share repurchase program.

- Strategic Focus: ON Semiconductor Corporation strategy is built around SiC-led growth, vertical integration, and deep automotive customer relationships. The company targets sustained revenue expansion through 800V EV traction inverter design wins and industrial automation deployments.

Market Concentration Analysis

The global power semiconductor market exhibits moderate concentration. The top five players - Infineon, STMicroelectronics, onsemi, Texas Instruments, and Mitsubishi Electric - collectively account for an estimated 42-48% of global revenue in 2024 per industry estimates. The remaining share is distributed across Toshiba, ROHM, NXP, Renesas, Fuji Electric, Hitachi, Microchip, Broadcom, Vishay, ABB, and a broader set of regional and specialty vendors.

The market is experiencing a dual-track dynamic. At the silicon IGBT and super-junction MOSFET tier, consolidation continues around scale, qualification breadth, and channel distribution. Simultaneously, the wide-bandgap transition is reshaping competitive positioning, with Infineon's GaN Systems acquisition, STMicroelectronics' Soitec partnership, and onsemi's SiC vertical integration underscoring a race to own end-to-end capability. Chinese and Taiwanese players are also scaling rapidly, intensifying competition at the lower and mid voltage tiers through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Gallium Nitride is the highest-growth material segment, projected to expand to approximately 11.6% CAGR through 2034. Silicon Carbide follows at an estimated 8.4% CAGR. By end-use, electric vehicles remain the single largest growth anchor, with automotive power semiconductor spend per vehicle rising from ~USD 500 today to USD 700-1,000 as 800V platforms scale. Data center and AI server power delivery represent the second major premium growth segment.

Emerging Market Expansion

India represents the highest-potential emerging opportunity, supported by the Semicon India Programme with over USD 15 billion in approved fab and ATMP investments as of 2024. Mexico and Vietnam are emerging as key assembly and test (ATMP) hubs, while Saudi Arabia is building a nascent semiconductor industry under Vision 2030, supported by sovereign investment vehicles such as Alat and PIF.

Strategic and Financial Investment Trends

Strategic investment in SiC and GaN manufacturing capacity accelerated sharply in 2023-2024. Wolfspeed's Mohawk Valley 200mm SiC fab, STMicroelectronics' Catania Campus, Infineon's Kulim expansion, and onsemi's Hudson fab represent combined capex commitments exceeding USD 15 billion through 2027. Venture and strategic capital into GaN specialists (Navitas, Innoscience, Transphorm) also exceeded USD 1 billion during 2022-2024.

Future Market Outlook (2026-2034)

The global power semiconductor market forecast projects steady value expansion from USD 46.1 Billion in 2025 to USD 60.6 Billion by 2034 at a CAGR of 3.00%. Asia-Pacific will retain regional revenue leadership through 2034 while Europe and North America sustain premium growth through automotive electrification, renewable energy expansion, and CHIPS Act-enabled capacity additions.

Three key structural shifts will reshape the power semiconductor market through 2034. First, wide-bandgap materials will continue to capture share, with SiC and GaN collectively crossing 45-50% of materials revenue by 2032 from 36.5% in 2025. Second, 800V EV architectures will become the premium-segment standard, driving a large multi-year SiC device upgrade cycle. Third, integration and intelligent power modules will reshape value capture, with vendors combining gate drivers, sensing, and protection into higher-margin, system-level solutions through 2034.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with power semiconductor industry stakeholders, including product directors at leading IDMs, procurement managers at automotive Tier-1 suppliers, data-center power architects at hyperscale operators, and institutional investors covering the semiconductor sector. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include data from SEMI, SIA, WSTS, Yole Group, IEA electric vehicle outlook, IRENA renewable capacity reports, the U.S. CHIPS Program Office, European Commission Chips Act publications, company annual reports and SEC filings, and trade publications including EE Times, Semiconductor Digest, Power Electronics News, and Nikkei Asia.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating EV sales, renewable installation data, semiconductor wafer capacity, historical device ASP trajectories, and technology substitution curves. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic, geopolitical, and technology uncertainty.

Power Semiconductor Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Discrete, Module, Power Integrated Circuits |

| Materials Covered | Silicon/Germanium, Silicon Carbide (SiC), Gallium Nitride (GaN) |

| End Use Industries Covered | Automotivem, Consumer Electronics, Industrial, Power and Energy, IT and Telecommunication, Military and Aerospace, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Infineon Technologies AG, STMicroelectronics NV, ON Semiconductor Corporation, Texas Instruments Incorporated, Mitsubishi Electric Corporation, Toshiba Corporation, ROHM Co. Ltd., NXP Semiconductors NV, Renesas Electronics Corporation, Fuji Electric Co. Ltd., Hitachi Ltd., Microchip Technology Inc., Broadcom Inc., Vishay Intertechnology Inc., ABB, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Power Semiconductor Market Report

The global power semiconductor market was valued at USD 46.1 Billion in 2025, driven by electric-vehicle electrification, renewable-energy expansion, 5G rollout, AI data-center power demand, and sustained industrial automation investment across major global economies.

The market is projected to reach USD 60.6 Billion by 2034, growing at a CAGR of 3.00% during 2026-2034, supported by wide-bandgap scaling, 800V EV architectures, renewable buildout, AI server power growth, and sustained industrial automation demand globally.

ilicon/Germanium leads with a 63.5% share in 2025, driven by mature supply base, cost efficiency, and broad design-in footprint. Silicon Carbide (21.4%) and Gallium Nitride (15.1%) follow, with wide-bandgap materials growing significantly faster than silicon through 2034.

Power Integrated Circuits dominate at 44.8% of global revenue in 2025, led by PMICs, gate drivers, and DC-DC controllers shipping into smartphones, automotive ECUs, and industrial systems. Discrete devices follow at 31.6% and Modules at 23.6%, with Modules growing fastest.

Asia-Pacific dominates with a 51.9% share in 2025, led by China's EV manufacturing scale, Japan's automotive semiconductor leadership (Toshiba, Mitsubishi, ROHM, Renesas), South Korea's consumer electronics base, and Taiwan's wafer foundry infrastructure.

Asia-Pacific is the fastest-growing region, advancing at an estimated 4.2% CAGR through 2034. Growth is powered by Chinese EV expansion, India's Semicon India Programme, Japanese and Korean SiC capacity scaling, and ASEAN electronics manufacturing growth.

Key drivers include electric-vehicle electrification, renewable-energy buildout, 5G and AI data-center power delivery, industrial automation, consumer fast-charging adoption, and macro tailwinds from U.S. CHIPS Act, EU Chips Act, and China semiconductor self-sufficiency programs.

Major players include Infineon Technologies AG, STMicroelectronics NV, ON Semiconductor Corporation, Texas Instruments Incorporated, Mitsubishi Electric Corporation, Toshiba Corporation, ROHM Co. Ltd., NXP Semiconductors NV, Renesas Electronics Corporation, Fuji Electric Co. Ltd., Hitachi Ltd., Microchip Technology Inc., Broadcom Inc., Vishay Intertechnology Inc., ABB.

Gallium Nitride (GaN) is the fastest-growing material, projected at approximately 11.6% CAGR through 2034. Silicon Carbide (SiC) follows at approximately 8.4% CAGR, both significantly outpacing the overall market, driven by EV, data-center, and fast-charger applications.

Key challenges include SiC and GaN supply chain constraints, high R&D and fab capital expenditure, automotive qualification cycle length, export control compliance, inventory cyclicality, and the global semiconductor engineering talent shortage estimated at 300,000+ by 2030.

AI server power density is rising above 50 kW per rack, versus legacy 8-12 kW. This is driving adoption of 48V direct power architectures and GaN-based high-efficiency point-of-load converters, creating a multi-billion-dollar incremental revenue stream for leading vendors.

Key opportunities include SiC and GaN capacity expansion, 800V EV traction inverter design wins, AI data-center power delivery, India semiconductor fabs and ATMP, intelligent power modules, and vertical integration across substrate, wafer, device, and module stages through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)