Power Tool Accessories Market Size, Share, Trends and Forecast by Type, Application, End-Use Sector, and Region 2026-2034

Global Power Tool Accessories Market Size, Share, Trends & Forecast (2026-2034)

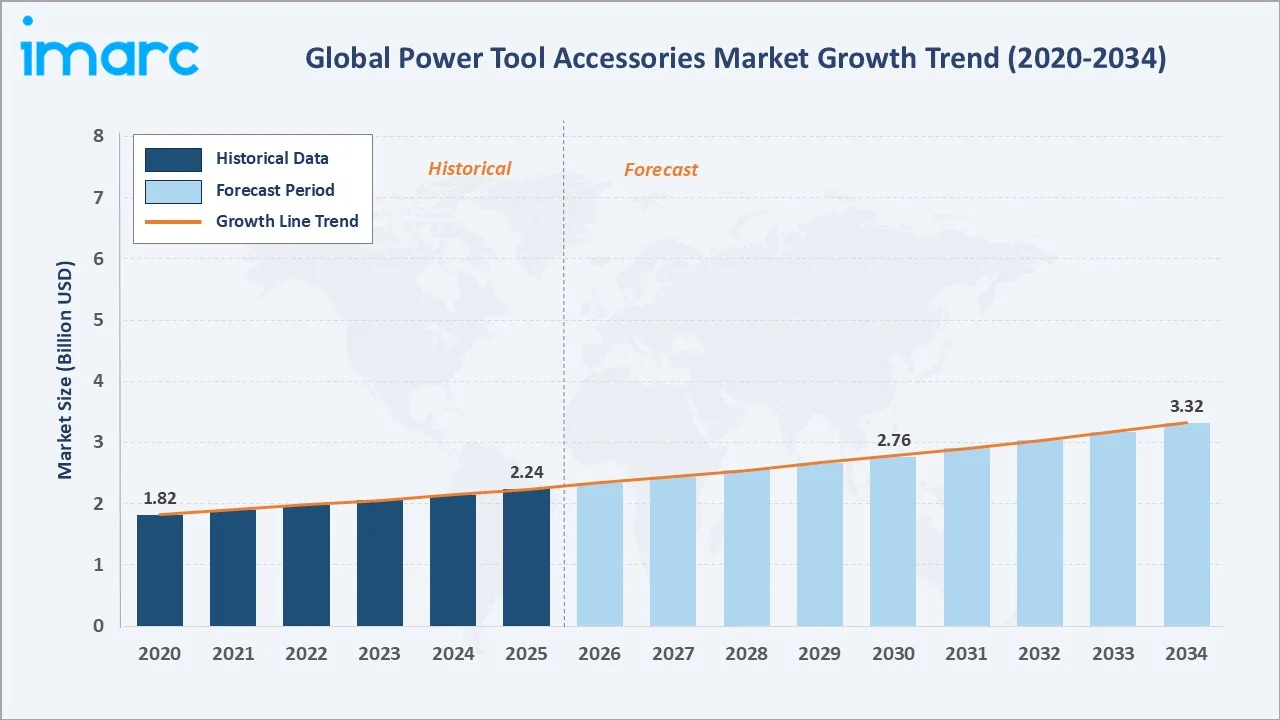

The global power tool accessories market size reached USD 2.24 Billion in 2025 and is projected to reach USD 3.32 Billion by 2026-2034, exhibiting a CAGR of 4.26% during 2026-2034.

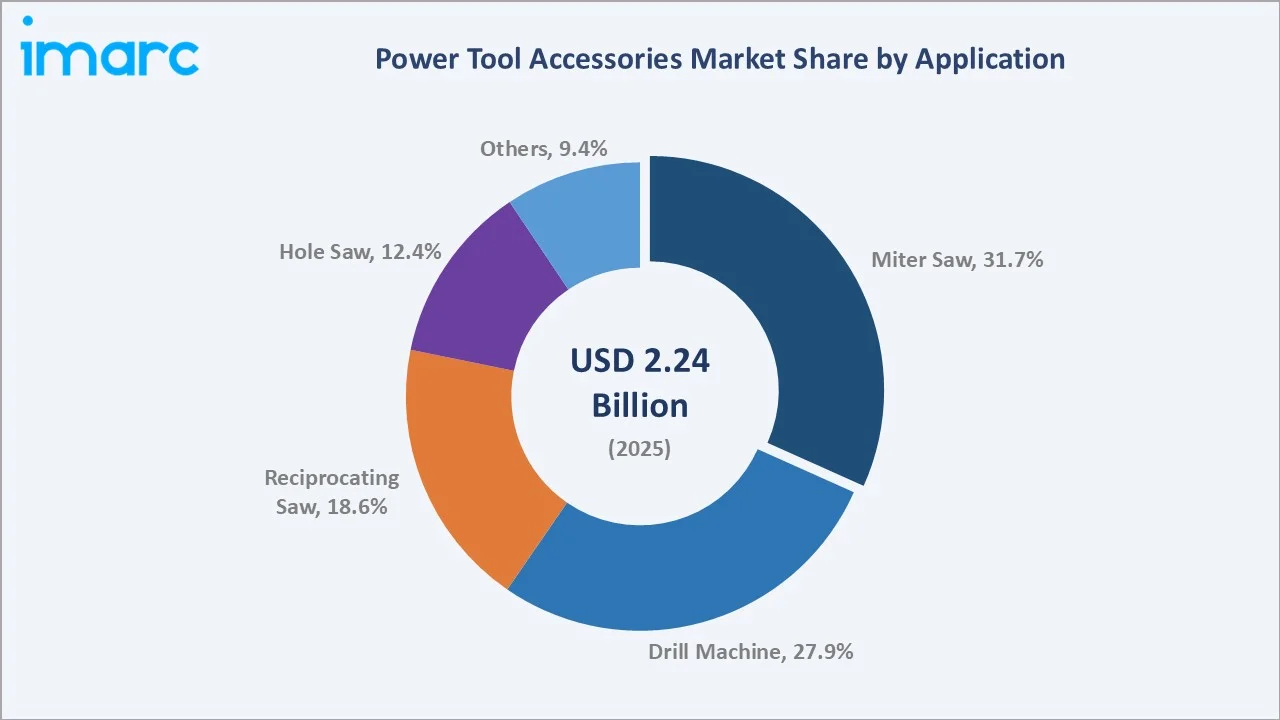

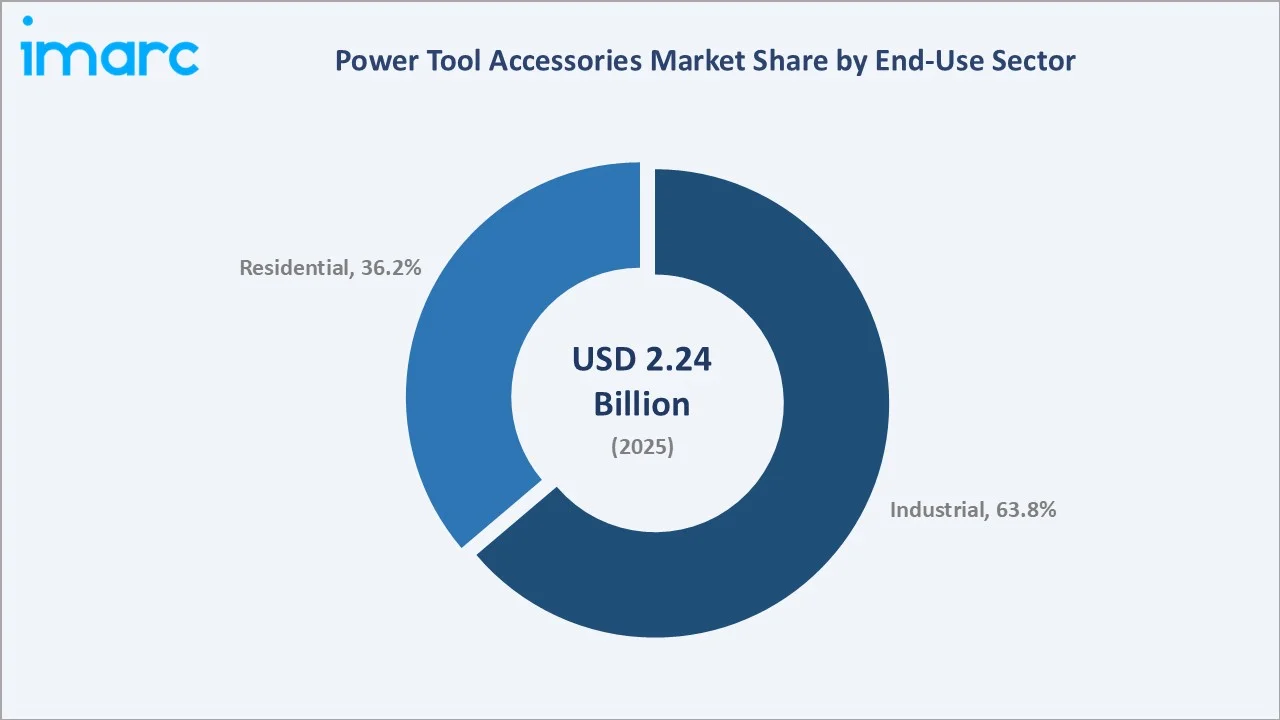

Rising construction spending, expanding DIY culture, and industrial automation are the primary forces driving growth. Miter saw applications dominate at 31.7% in 2025, while industrial end-use leads at 63.8%.

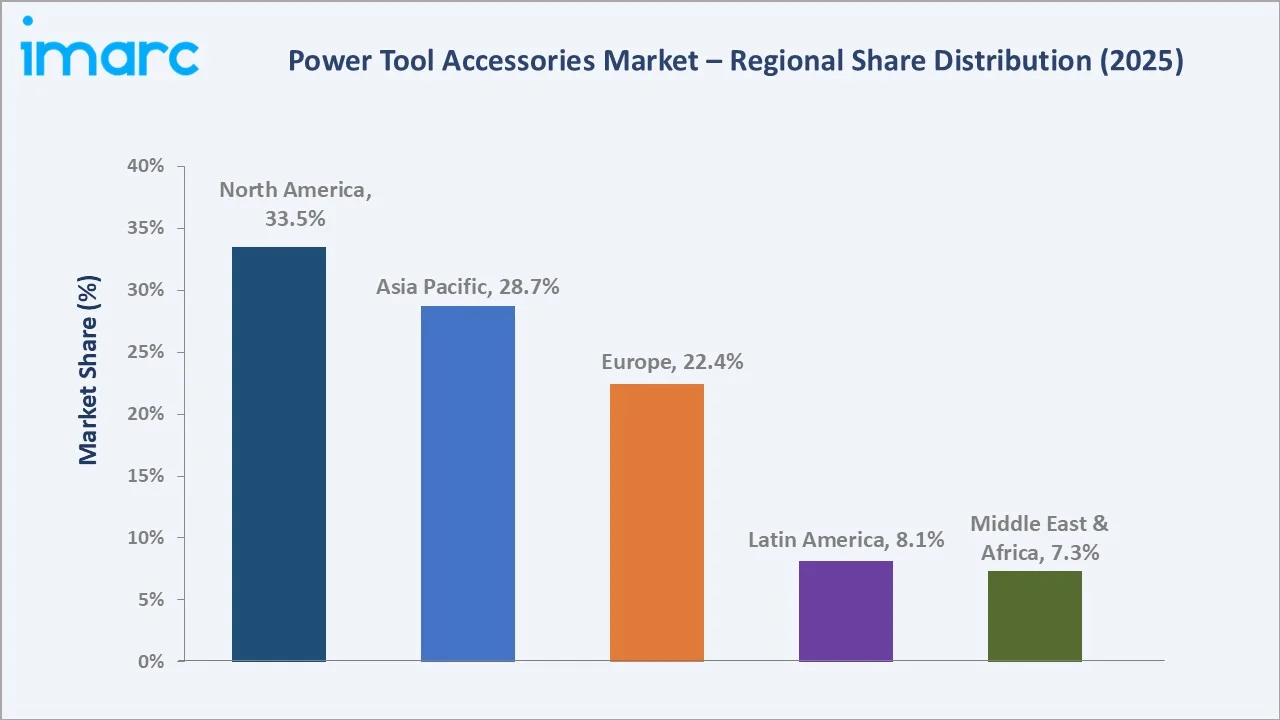

North America commands a 33.5% regional share in 2025, reflecting robust residential construction, nearshoring, and mature retail distribution networks absorbing large accessory replacement volumes annually.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.24 Billion |

|

Forecast Market Size (2034) |

USD 3.32 Billion |

|

CAGR (2026-2034) |

4.26% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (33.5% share, 2025) |

|

Second Largest Region |

Asia Pacific (28.7% share, 2025) |

|

Leading Application |

Miter Saw (31.7%, 2025) |

|

Leading End-Use Sector |

Industrial (63.8%, 2025) |

The global power tool accessories market growth trajectory from 2020 through 2034, with historical expansion to USD 2.24 Billion in 2025, reflects consistent construction and DIY demand. The forecast to USD 3.32 Billion captures accelerating cordless-tool adoption, nearshoring-linked industrial reinvestment, and e-commerce-led residential accessory demand across emerging economies.

To get more information on this market, Request Sample

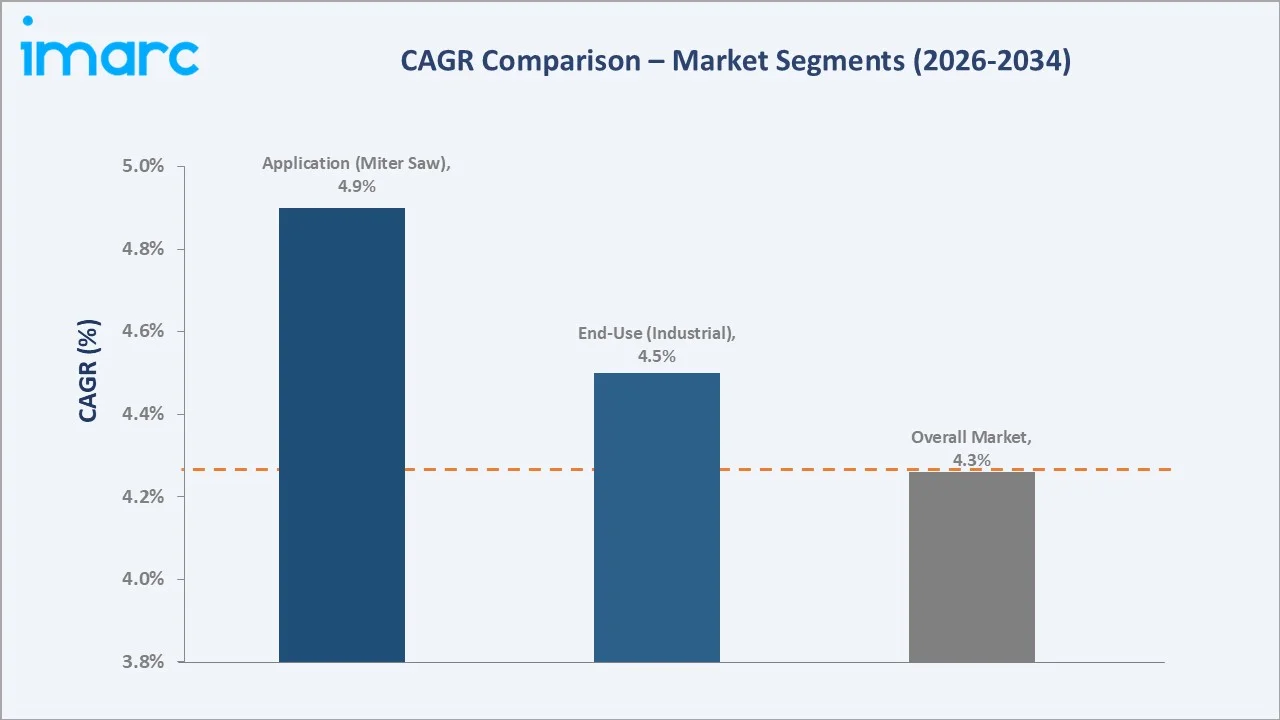

The CAGR trajectories across key application, end-use, and regional sub-segments, with Miter saw accessories at ~4.9% CAGR and industrial end-use at ~4.5% CAGR, represent the fastest-growing categories through 2034.

Executive Summary

The global power tool accessories market is on a sustained growth trajectory from USD 2.24 Billion in 2025 to USD 3.32 Billion by 2034. Accessories span drill bits, saw blades, abrasive wheels, and router bits that remain consumables.

Miter saw accessories dominate application share at 31.7% in 2025, driven by widespread use in carpentry, cabinetry, and framing workflows. Drill machine accessories follow at 27.9%, covering bits and chucks for metal, concrete, and wood drilling.

Reciprocating saw (18.6%) and Hole saw (12.4%) accessories serve remodelling, demolition, and plumbing trades where fast blade replacement cycles drive repeat purchase demand. The others category (9.4%) aggregates grinding wheels and specialty attachments.

Industrial end-use leads at 63.8% in 2025, reflecting procurement by automotive, construction, aerospace, energy, and marine contractors. Residential (36.2%) is the fastest-growing sector, lifted by DIY culture and cordless tool penetration.

North America dominates regional distribution at 33.5% in 2025, followed by Asia Pacific (28.7%) and Europe (22.4%). Latin America (8.1%) and Middle East & Africa (7.3%) accelerate on construction and mining investment.

Key Market Insights

|

Insight |

Data |

|

Leading Application |

Miter Saw - 31.7% share (2025) |

|

Leading End-Use Sector |

Industrial - 63.8% share (2025) |

|

Leading Region |

North America - 33.5% revenue share (2025) |

|

Second Largest Region |

Asia Pacific - 28.7% revenue share (2025) |

|

Top Companies |

Apex Tool Group, LLC, Emerson Electric Co., Makita U.S.A., Inc., Robert Bosch Tool Corporation, Stanley Black & Decker, Inc. |

Key Analytical Observations Expanding On The Above Data:

- Miter saw accessories, with 31.7% in 2025, dominate applications because circular blades and miter fences are high-turnover consumables in carpentry and framing, where blade wear cycles drive recurring purchases across residential and commercial construction.

- Drill machine accessories, with 27.9% in 2025, hold the second-largest share because drill bits are the single most widely consumed accessory SKU across industrial maintenance, construction, and residential DIY use globally.

- Industrial end-use, at 63.8% in 2025, reflects procurement scale from automotive OEMs, construction contractors, aerospace facilities, energy operators, and marine fabricators purchasing accessories in volume on recurring replacement contracts.

- North America, with 33.5% in 2025, benefits from the Bipartisan Infrastructure Law, CHIPS Act construction, robust housing repair/remodel spend, and a mature home-improvement retail channel anchored by Home Depot, Lowe’s, and Amazon.

Global Power Tool Accessories Market Overview

Power tool accessories are interchangeable consumable attachments, including drill bits, screwdriver bits, router bits, circular saw blades, jig saw blades, band saw blades, abrasive wheels, and reciprocating saw blades, that convert corded and cordless power tools into task-specific cutting, drilling, grinding, and fastening equipment.

The global ecosystem integrates raw material suppliers (tool steel, tungsten carbide, diamond, abrasives), OEM accessory producers, private-label manufacturers, power tool OEMs bundling accessories with platforms, specialised distributors, big-box retailers, online marketplaces, and end-users spanning industrial plants and residential consumers.

Market Dynamics

To evaluate market opportunities, Request Sample

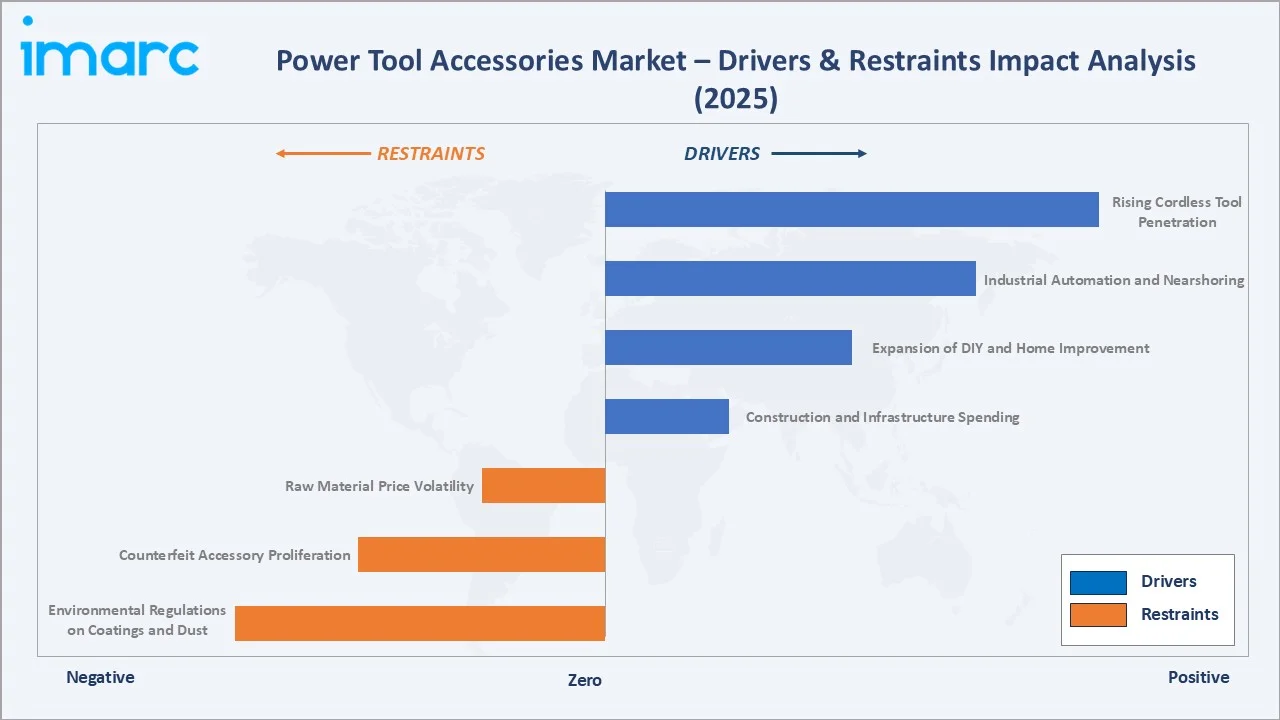

Market Drivers

- Construction and Infrastructure Spending: The US Bipartisan Infrastructure Law’s USD 1.2 Trillion allocation, global housing demand, and non-residential commercial build-out are generating sustained procurement of saw blades, drill bits, and abrasive wheels across contractor fleets.

- Expansion of DIY and Home Improvement: Post-pandemic residential renovation spending has remained elevated. US home improvement retail sales exceeded USD 600 Billion by 2027, generating strong pull-through for accessory replacement SKUs through Home Depot, Lowe’s, and Amazon.

- Industrial Automation and Nearshoring: Manufacturing reshoring in North America, Mexico, and Eastern Europe is driving capital-equipment spending that generates corresponding accessory demand for production maintenance, tooling changeovers, and in-plant fabrication activity.

- Rising Cordless Tool Penetration: Cordless power tools exceed 70% of new professional tool sales, expanding the installed base and multiplying the attach-rate opportunity for platform-specific drill bits, saw blades, and impact-rated accessory kits.

Market Restraints

- Raw Material Price Volatility: Tool steel, tungsten carbide, and industrial diamond feedstock prices experience significant swings tied to tungsten ore supply from China, cobalt prices, and steel index movements, compressing accessory manufacturer margins unpredictably.

- Counterfeit Accessory Proliferation: Low-quality counterfeit drill bits, saw blades, and abrasive wheels sold through informal online channels undercut branded accessory pricing, damage OEM brand reputation, and create safety risks that erode buyer trust in aftermarket purchases.

- Environmental Regulations on Coatings and Dust: Tightening EPA and EU REACH restrictions on solvent-based coatings, hexavalent chromium plating, and crystalline silica dust from abrasive accessories are raising compliance costs and forcing reformulation across legacy product lines.

- Tool Platform Longevity and Extended Replacement Cycles: Longer-lasting brushless motors and premium carbide-tipped accessories are stretching replacement intervals, softening volume growth for commodity HSS bit and blade SKUs in professional channels.

Market Opportunities

- Cordless Tool Ecosystem Accessory Bundling: Branded accessory kits designed for 18V and 20V cordless battery platforms from Bosch, DeWalt, Makita, and Milwaukee unlock attach-rate revenue by capturing consumers locked into specific battery ecosystems and voltage architectures.

- E-commerce and Direct-to-Consumer Channels: Amazon, Home Depot online, and OEM direct sites are converting accessory purchases from impulse retail to planned online reorder behaviour, creating subscription-style reorder opportunities and richer SKU-level analytics for manufacturers.

- Emerging-Market DIY Retail Penetration: Rising modern-trade home-improvement formats in India, Southeast Asia, and Latin America are unlocking a fast-growing residential consumer base, previously underserved by informal hardware channels, for branded power tool accessory SKUs.

- Diamond-Tipped and PCD Premium Accessory Lines: Polycrystalline diamond router bits, diamond-tipped hole saws, and PCD saw blades command 3-5x price premiums over carbide equivalents, opening rich margin corridors in aerospace composite machining and fibre-cement applications.

Market Challenges

- Skilled Labour Shortage in Trades: Declining carpentry, electrician, and construction workforce pipelines in the US and Europe limit growth of professional end-user accessory consumption, despite continued demand from DIY and residential channels offsetting parts of the gap.

- Cordless Platform Lock-in and Fragmentation: Competing battery platforms fragment the accessory market into ecosystem-specific SKUs, increasing inventory complexity for distributors and making cross-brand accessory compatibility a recurring friction point for end-users.

- Price Competition from Chinese Accessory Manufacturers: Low-cost accessory imports from Zhejiang and Jiangsu-based manufacturers continue pressuring branded pricing in commodity drill bit and saw blade segments, especially across e-commerce marketplaces and emerging-market retail channels.

- Supply Chain and Logistics Cost Volatility: Container freight volatility, tungsten and cobalt export controls, and geopolitical trade friction between the US, EU, and China are raising landed costs and working capital requirements for global accessory supply networks.

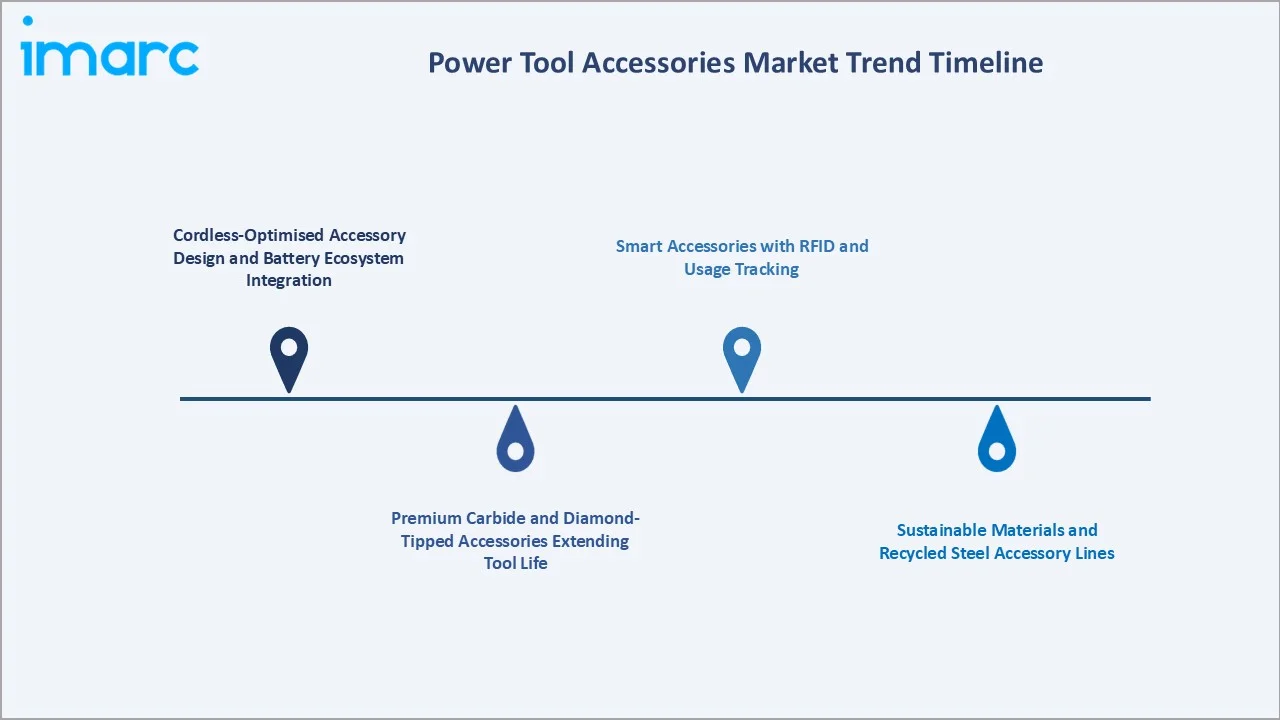

Emerging Market Trends

1. Cordless-Optimised Accessory Design and Battery Ecosystem Integration

Cordless tool penetration now exceeds 70% of new professional power tool sales globally, pushing accessory manufacturers to redesign bits and blades for lower torque, higher RPM profiles, and extended runtime per battery cycle that cordless platforms demand.

2. Premium Carbide and Diamond-Tipped Accessories Extending Tool Life

Tungsten carbide-tipped saw blades, polycrystalline diamond router bits, and industrial diamond hole saws are gaining specification share in professional segments, offering 3-5x longer service life than high-speed steel equivalents despite per-unit premiums.

3. Smart Accessories with RFID and Usage Tracking

Enterprise fleet buyers are piloting RFID-tagged drill bits and saw blades that enable tool-room inventory tracking, automatic reorder triggers, and usage analytics tied to specific machine operators in industrial maintenance and fabrication environments.

4. Sustainable Materials and Recycled Steel Accessory Lines

Major OEMs are introducing accessory lines manufactured from recycled tool steel and responsibly sourced tungsten, targeting LEED procurement credits, EU Green Deal compliance, and sustainability-linked industrial buyer specifications growing across public works contracts.

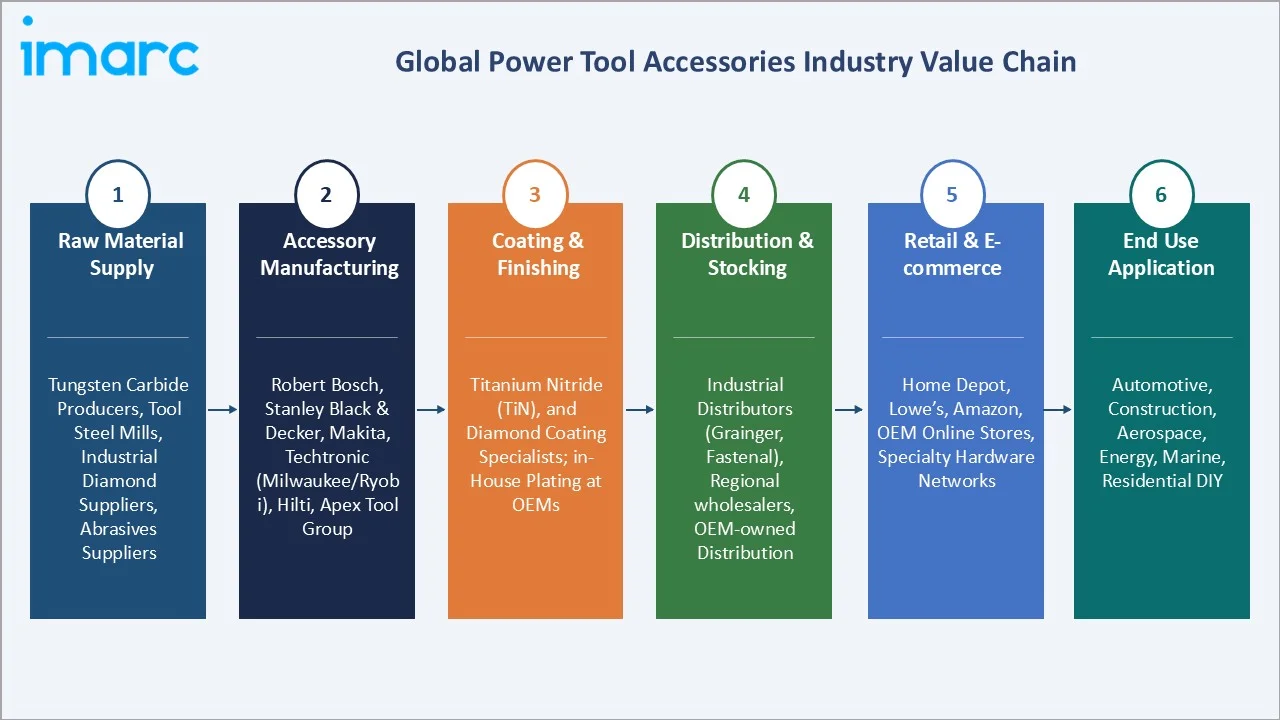

Industry Value Chain Analysis

The power tool accessories value chain spans six stages from raw material input to end-use application. Accessory manufacturing and coating capture the highest value-add margins, while distribution and retail generate working capital demand that favours well-capitalised, branded OEM accessory suppliers.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Tungsten carbide producers, tool steel mills, industrial diamond suppliers, abrasives suppliers |

|

Accessory Manufacturing |

Robert Bosch, Stanley Black & Decker, Makita, Techtronic (Milwaukee/Ryobi), Hilti, Apex Tool Group |

|

Coating & Finishing |

Titanium nitride (TiN), and diamond coating specialists; in-house plating at OEMs |

|

Distribution & Stocking |

Industrial distributors (Grainger, Fastenal), regional wholesalers, OEM-owned distribution |

|

Retail & E-commerce |

Home Depot, Lowe’s, Amazon, OEM online stores, specialty hardware networks |

|

End Use Application |

Automotive, Construction, Aerospace, Energy, Marine, Residential DIY |

Integrated power tool OEMs with captive accessory production (Bosch, Stanley Black & Decker, Techtronic) capture margin across tool and accessory attach sales, while standalone accessory specialists compete through distribution breadth, coating innovation, and professional segment certification.

Technology Landscape in the Power Tool Accessories Industry

Cutting Edge Technology: Carbide, Diamond, and Bimetal Innovation

Tungsten carbide-tipped teeth dominate premium circular saw blades and router bits, providing 3-5x wear life over high-speed steel. Polycrystalline diamond (PCD) tipping is expanding into router bits and hole saws cutting abrasive composites and cured concrete.

Coating Innovation: TiN, TiAlN, and Multi-Layer Coatings

Titanium nitride (TiN) and titanium aluminium nitride (TiAlN) coatings on drill bits extend service life by 2-3x through reduced friction and heat build-up. Advanced multi-layer coatings are gaining adoption across aerospace and automotive machining.

Material Innovation: High-Speed Steel and Cobalt Alloys

Cobalt-enriched M35 and M42 high-speed steel grades retain dominance in twist drill production for stainless steel and hardened metal drilling. Powder metallurgy HSS variants are capturing share in premium bit segments for industrial fabrication.

Digital Accessory Catalogues and OEM Configurator Tools

Accessory manufacturers are investing in digital configurators, AR-enabled selection apps, and battery-platform compatibility matrices integrated into OEM mobile tool apps to simplify specification and reduce returns from mismatched accessory purchases.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Drill Bits | 🔒 | 2025 |

| Application | Miter Saw | 31.7% | 2025 |

| End-Use Sector | Industrial | 63.8% | 2025 |

| Region | North America | 33.5% | 2025 |

By Application

Miter saw accessories command a 31.7% majority share in 2025, driven by widespread deployment in carpentry, cabinetry, framing, and finish trim workflows. Circular blade consumption scales directly with residential and light-commercial construction activity across North America, Europe, and emerging Asia Pacific markets.

To access detailed market analysis, Request Sample

Drill machine accessories at 27.9% in 2025 cover twist bits, masonry bits, spade bits, and hole cutters consumed across industrial maintenance, construction, and residential DIY at very high unit volumes. Reciprocating saw accessories (18.6%) serve demolition, remodelling, and emergency-response trades.

Hole saw accessories (12.4%) are specified for plumbing, electrical rough-in, and HVAC installation work. The others category (9.4%) captures specialty attachments including grinding wheels, flap discs, sanding pads, wire brushes, and oscillating tool blades.

By End-Use Sector

Industrial end-use dominates the sector segment at 63.8% in 2025, representing the highest-volume consumption channel across automotive assembly plants, construction contractor fleets, aerospace fabrication, energy infrastructure maintenance, and marine/shipbuilding operations that treat accessories as recurring consumables.

Residential end-use, at 36.2% in 2025, is the fastest-growing sector segment, driven by post-pandemic home improvement spending, expanding DIY demographics, and cordless tool adoption in households. E-commerce penetration is reshaping residential accessory reorder behaviour toward planned online purchases.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

33.5% |

Bipartisan Infrastructure Law; CHIPS Act construction; mature home improvement retail; DIY culture |

|

Asia Pacific |

28.7% |

China manufacturing hub; India infrastructure pipeline; ASEAN urbanisation; residential construction |

|

Europe |

22.4% |

Industrial maintenance cycles; EU Green Deal construction; premium DIY retail; renovation activity |

|

Latin America |

8.1% |

Brazil housing deficit reduction; Mexico nearshoring; mining equipment maintenance |

|

Middle East & Africa |

7.3% |

GCC Vision 2030 mega-projects; African mining fleet expansion |

North America’s 33.5% market leadership in 2025 reflects robust housing repair/remodel spending, nearshoring-led manufacturing reinvestment, and a mature home-improvement retail channel anchored by Home Depot and Lowe’s that absorbs accessory replacement volumes at scale.

Asia Pacific, with 28.7% in 2025, benefits from China’s manufacturing scale, India’s National Infrastructure Pipeline, and ASEAN residential construction. Europe (22.4%) is driven by renovation cycles, EU Green Deal construction, and Germany’s industrial maintenance base.

Latin America (8.1%) grows on Brazil housing deficit reduction and Mexico nearshoring-linked manufacturing. Middle East & Africa (7.3%), the fastest-growing region, is powered by Saudi NEOM construction, UAE industrial zones, and African mining-fleet expansion.

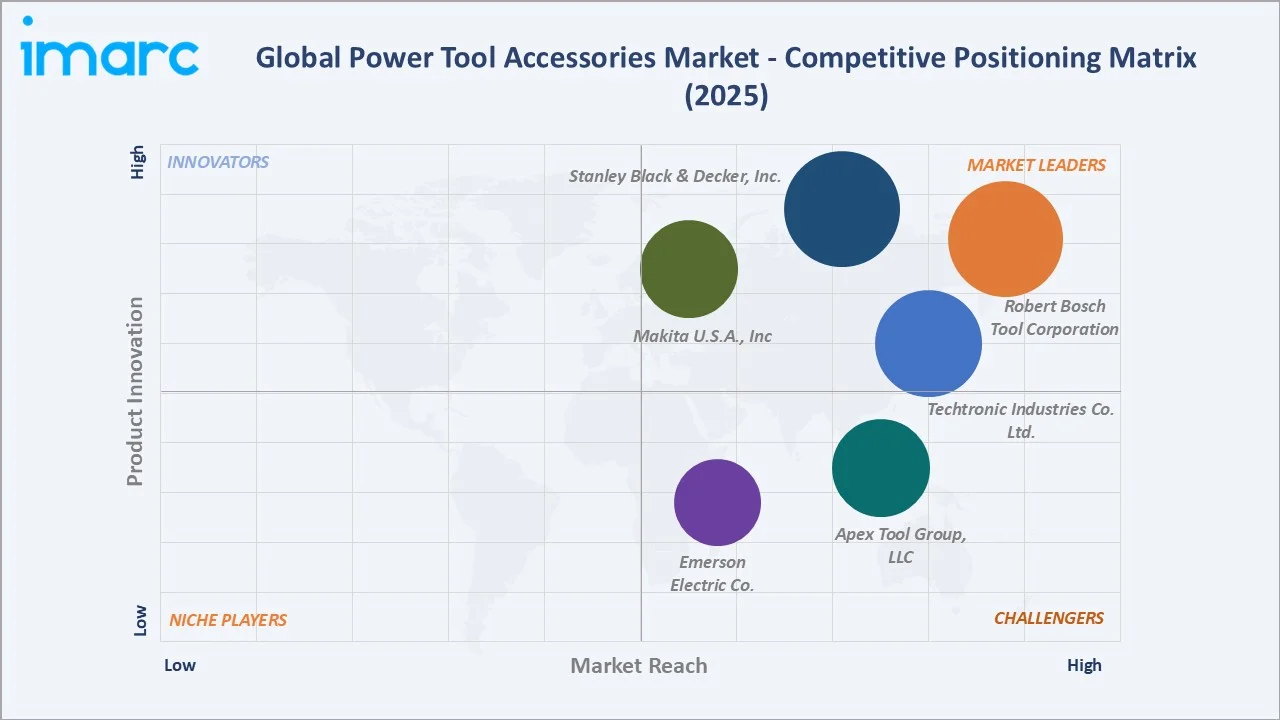

Competitive Landscape

The global power tool accessories market is moderately consolidated, with integrated power tool OEMs holding strong positions through accessory bundling into their battery platforms, while specialist accessory firms compete across distribution breadth, coating technology, and professional-segment certification.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Apex Tool Group, LLC |

Drill bits, screwdriver bits, impact sockets |

Challenger |

US multi-brand portfolio; GearWrench, Crescent; industrial channel focus |

|

Emerson Electric Co. |

Electrical conduit and wire tools, crimping and cutting tools |

Challenger |

North America; trades and industrial; pro-grade differentiation |

|

Makita U.S.A., Inc. |

Drill bits, saw blades, screwdriver bits, accessories kits |

Leader |

Global; cordless-first accessory integration; trades & industrial |

|

Robert Bosch Tool Corporation |

Drill bits, saw blades, router bits, abrasive accessories |

Leader |

Global leader; integrated cordless platform; widest accessory range |

|

Stanley Black & Decker, Inc. |

DeWalt, LENOX, Irwin, Craftsman, Black+Decker accessory brands |

Leader |

Global; multi-brand portfolio; trades, industrial & residential |

|

Techtronic Industries Co. Ltd. |

Milwaukee, Ryobi, AEG accessory lines |

Leader |

Global; Milwaukee professional focus; cordless ecosystem leadership |

Key players include Apex Tool Group, LLC, Emerson Electric Co., Makita U.S.A., Inc., Robert Bosch Tool Corporation, Stanley Black & Decker, Inc., Techtronic Industries Co. Ltd., and others.

Key Company Profiles

Robert Bosch Tool Corporation

Robert Bosch Tool Corporation is a subsidiary of the Robert Bosch Group, a leading global supplier of power tools and accessories. Bosch’s integrated strategy leverages cordless battery platforms, global distribution, and premium brand positioning across professional and DIY segments.

- Product Portfolio: Offers drill bits, saw blades, router bits, and abrasive accessories for power tools.

- Recent Developments: In October 2025, Bosch expanded its 18V power tools portfolio with a new lineup of cordless and corded solutions designed to enhance performance, precision, and ease of use for professional applications. The launch includes tools such as a brushless pin nailer, compact reciprocating saw, and high-torque right-angle drill, all engineered to improve productivity, reduce user fatigue, and support demanding jobsite tasks.

- Strategic Focus: Bosch emphasises accessory integration with its 18V cordless (with ProCore battery technology) platform, continuous innovation in carbide and diamond-tipped lines, and captive distribution to capture attach-rate revenue.

Stanley Black & Decker, Inc.

Stanley Black & Decker, Inc. is a global leader in hand tools, power tools, and accessories, operating DeWalt, Black+Decker, and Irwin accessory brands. Its diversified portfolio covers professional trades, industrial channels, and residential DIY at varied price points.

- Product Portfolio: Offers LENOX (cutting accessories: saw blades, hole saws, reciprocating blades), DeWalt drill bits and saw blades, Black+Decker residential accessory kits, and Irwin professional bit/blade ranges.

- Recent Developments: In January 2023, DEWALT, a brand of Stanley Black & Decker, showcased a new range of advanced tools, accessories, and storage solutions at the World of Concrete trade show, targeting professionals in the concrete and masonry sectors. The launch highlights a comprehensive, end-to-end jobsite ecosystem designed to enhance productivity, performance, and efficiency across demanding construction applications.

- Strategic Focus: Stanley Black & Decker leverages multi-brand positioning, global distribution, and accessory compatibility with DeWalt’s 20V MAX and FlexVolt platforms to capture professional, industrial, and residential share.

Makita U.S.A., Inc.

Makita U.S.A., Inc. is the US subsidiary of Makita Corporation, a Japan-headquartered global power tool and accessory manufacturer combining Japanese precision engineering with a broad cordless battery ecosystem for professional trades.

- Product Portfolio: Offers drill bits, saw blades, screwdriver bits, and accessory kits designed for Makita’s 18V LXT and 40V XGT cordless platforms.

- Recent Developments: In October 2025, Makita introduced new outdoor power equipment accessories specifically designed for arborists, aimed at improving efficiency in cutting, pruning, and tree maintenance applications. The additions expand Makita’s broader ecosystem of battery-powered tools, offering enhanced compatibility with its existing equipment lineup while supporting professional-grade performance.

- Strategic Focus: Makita focuses on cordless-first accessory design, professional trades distribution via independent specialists, and Japanese-engineered quality positioning that commands premiums in industrial channels.

Market Concentration Analysis

The global power tool accessories market is moderately consolidated at the global level, with the top five OEM-aligned players (Bosch, Stanley Black & Decker, Techtronic, Makita, Hilti) collectively accounting for an estimated 45-55% of branded professional revenue in 2025.

Consolidation is more advanced in the professional industrial channel than in residential DIY, where private-label and regional specialists capture material share via Amazon and retailer house brands. M&A activity continues through OEM bolt-on accessory acquisitions.

Investment & Growth Opportunities

Fastest-Growing Segments

Miter saw accessories at ~4.9% CAGR through 2034 are the highest-growth application segment, driven by carpentry activity and cordless miter saw penetration. Industrial end-use, growing at ~4.5% CAGR, represents the broadest-based growth opportunity.

Emerging Markets

Middle East & Africa, growing at the fastest regional CAGR, is lifted by Saudi NEOM construction, UAE industrial zones, and African mining-fleet demand. India and Southeast Asia offer structural residential DIY runway as retail modernisation deepens.

Venture & Investment Trends

Private equity interest in consolidating regional accessory specialists continues, while OEMs pursue bolt-on acquisitions in coating technology and diamond-tipped premium niches. Sustainability-linked lines and e-commerce-native private-label brands also attract meaningful investment.

Future Market Outlook (2026-2034)

The global power tool accessories market is forecast to expand from USD 2.24 Billion in 2025 to USD 3.32 Billion by 2034 at a CAGR of 4.26%, adding USD 1.08 Billion in incremental annual market value.

Three forces will shape the accessory industry through 2034. Cordless battery platform dominance will continue reshaping accessory design around high-RPM, brushless motor torque profiles. Premium carbide and diamond-tipped accessories will gain professional share.

Digital commerce and RFID-enabled smart accessories will transform industrial procurement, enabling tool-room inventory analytics, automatic reorder triggers, and usage tracking across fleet-operating industrial buyers.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews in 2024-2025 with power tool accessory industry stakeholders, including commercial managers at OEMs, industrial procurement specialists, home-improvement retail category managers, and distributor executives at Grainger, Fastenal, and specialist tool distributors.

Secondary Research

Key secondary sources include company annual reports of Bosch, Stanley Black & Decker, TTI, Makita, and Hilti, World Power Tool Manufacturers Association data, US Census Bureau retail trade data, home improvement retailer earnings transcripts, and industry trade publications including Pro Tool Reviews and Tool Manufacturer magazine.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, incorporating GDP growth, construction spending indices, cordless tool penetration rates, and historical accessory attach-rate patterns. Scenario analysis (base, optimistic, conservative) was performed to account for macroeconomic uncertainty.

Power Tool Accessories Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Drill Bits, Screwdriver Bits, Router Bits, Circular Saw Blades, Jig Saw Blades, Band Saw Blades, Abrasive Wheels, Reciprocating Saw Blades, Others |

| Applications Covered | Miter Saw, Drill Machine, Reciprocating Saw, Hole Saw, Others |

| End-Use Sectors Covered | Industrial, Residential |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Apex Tool Group, LLC, Emerson Electric Co., Makita U.S.A., Inc., Robert Bosch Tool Corporation, Stanley Black & Decker, Inc., Techtronic Industries Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Power Tool Accessories Market Report

The global power tool accessories market reached USD 2.24 Billion in 2025, reflecting steady demand from construction, industrial maintenance, and residential DIY activity.

The market is projected to reach USD 3.32 Billion by 2034, growing at a CAGR of 4.26% during 2026-2034, driven by cordless adoption and nearshoring-linked industrial demand.

Miter saw accessories lead with a 31.7% application share in 2025, driven by circular blade consumption in carpentry, cabinetry, framing, and finish trim workflows.

The industrial sector leads at 63.8% in 2025, driven by procurement from automotive, construction, aerospace, energy, and marine contractors consuming accessories as high-turnover consumables.

North America commands a 33.5% share in 2025, supported by infrastructure spending, nearshoring, mature home-improvement retail, and an entrenched DIY culture across US households.

Miter saw accessories are among the fastest-growing applications at ~4.9% CAGR through 2034, lifted by cordless miter saw platform penetration and residential carpentry activity.

Leading companies include Apex Tool Group, LLC, Emerson Electric Co., Makita U.S.A., Inc., Robert Bosch Tool Corporation, Stanley Black & Decker, Inc., Techtronic Industries Co. Ltd., and others.

Key applications include miter saw (cutting and trim work), drill machine (boring), reciprocating saw (demolition), hole saw (plumbing), and others covering grinding, sanding, and specialty attachments.

Cordless tool penetration above 70% of new professional sales is reshaping accessory design toward high-RPM, brushless-optimised bits and driving attach-rate revenue via platform-specific bundling.

Industrial accessories prioritise durability, carbide/diamond tipping, and bulk procurement. Residential accessories emphasise value pricing, starter-kit packaging, and retail availability through Home Depot, Lowe’s, and Amazon.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)