Precision Gearbox Market Size, Share, Trends and Forecast by Axis of Orientation, Gear Technology, End Use Industry, and Region, 2026-2034

Precision Gearbox Market Size, Share, Trends & Forecast (2026-2034)

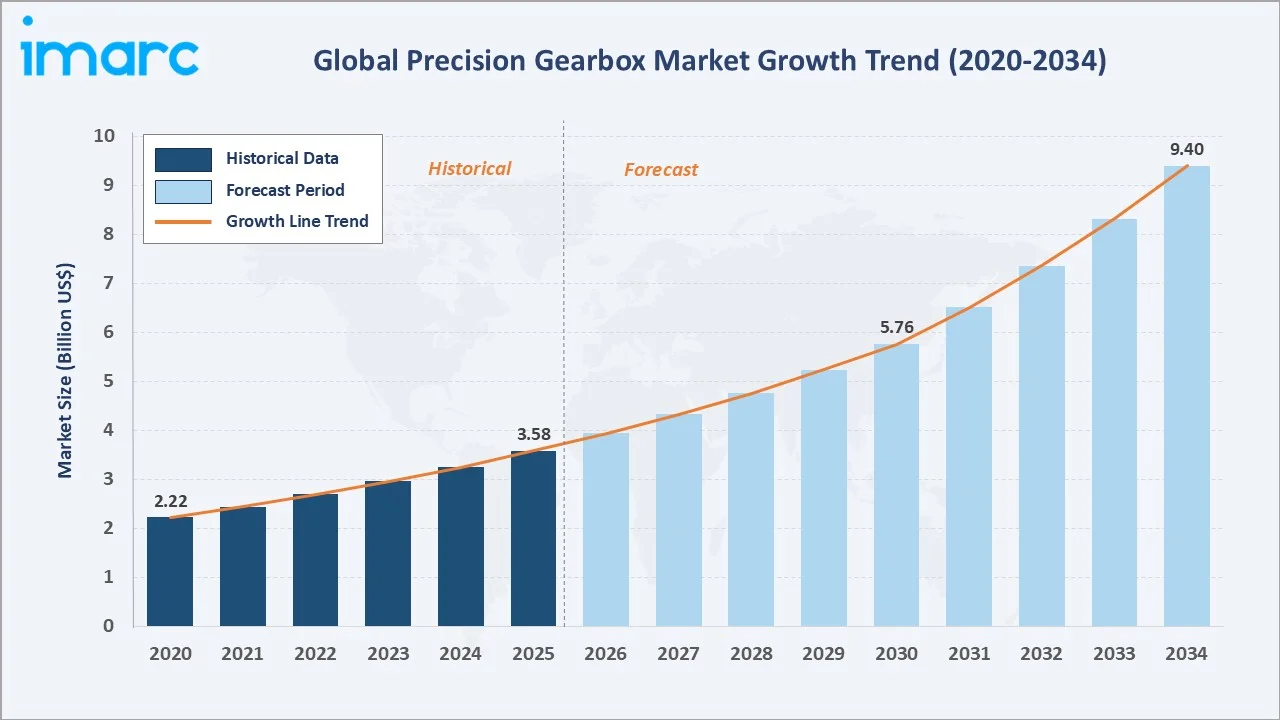

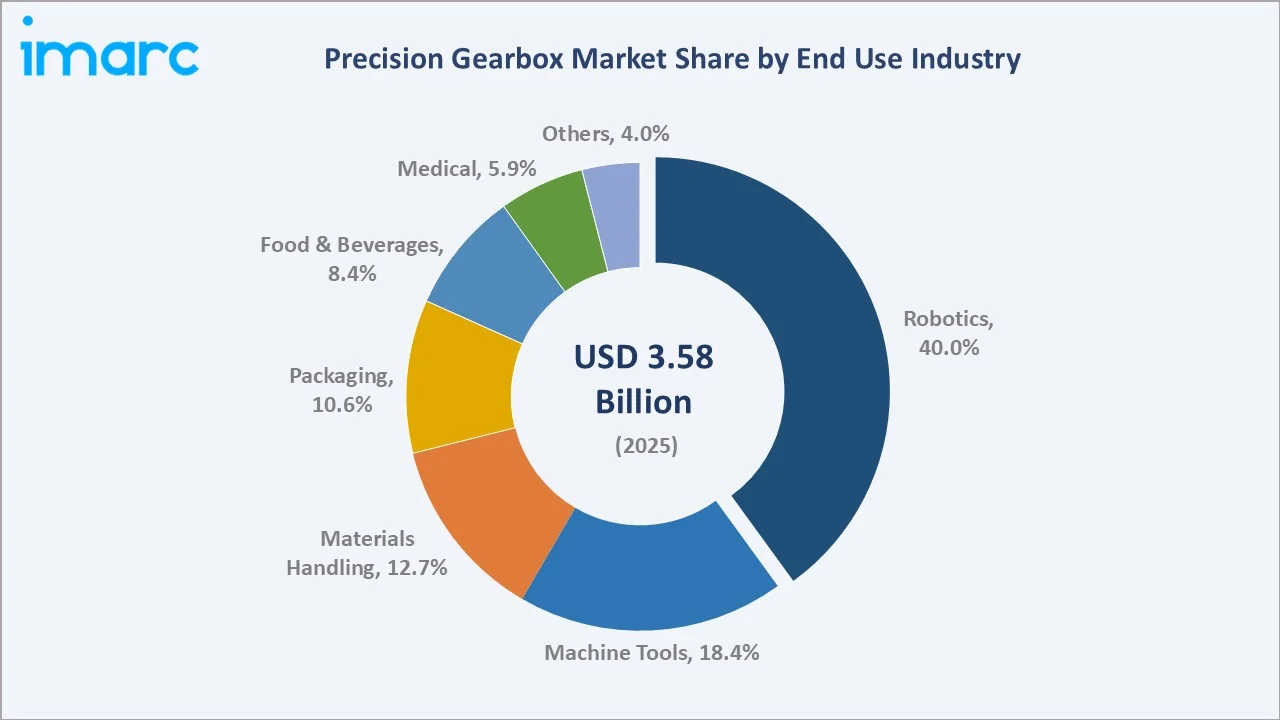

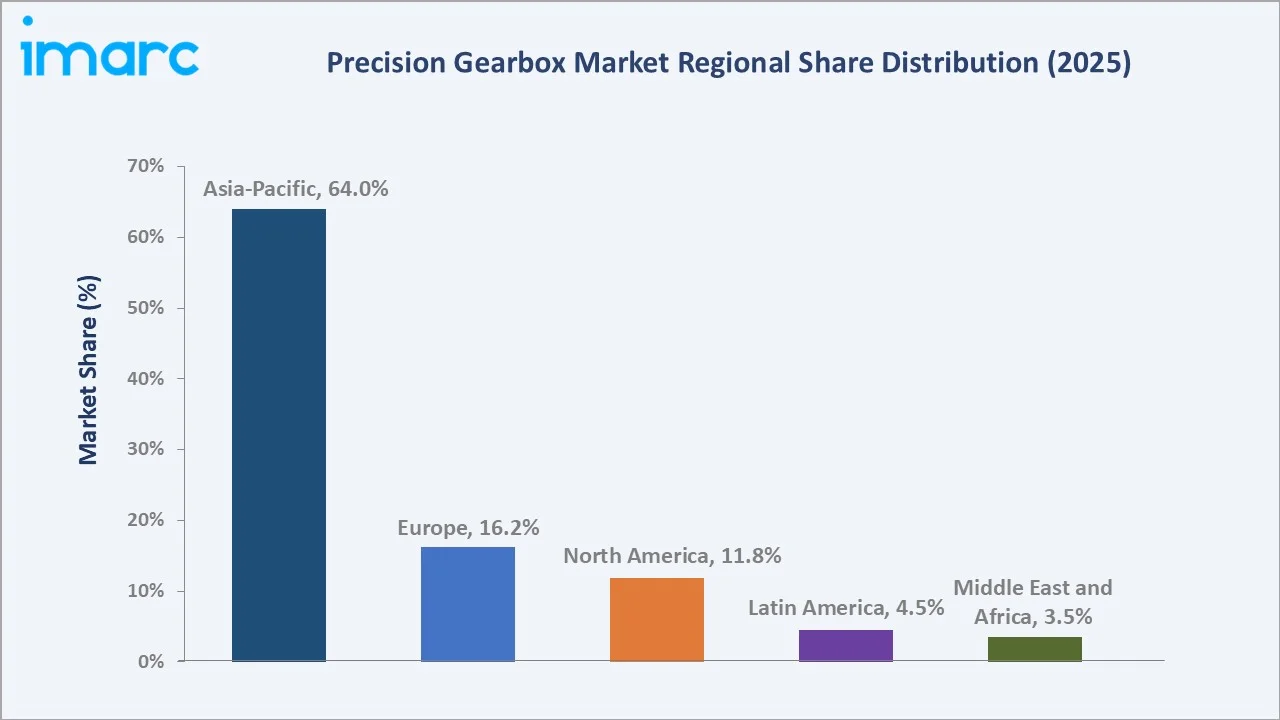

The global precision gearbox market reached USD 3.58 Billion in 2025 and is projected to reach USD 9.40 Billion by 2034, growing at a CAGR of 9.98% during 2026-2034. The market is driven by the rising adoption of industrial automation, robotics, and precision motion control systems across manufacturing industries. Growing demand for high-accuracy, high-torque transmission solutions in sectors such as automotive, electronics, and aerospace is further supporting market growth. World Robotics 2025 reported that 542,000 industrial robots were installed in 2024, more than twice the level recorded a decade earlier. This rapid growth in robot deployment is driving the precision gearbox market, as robotic arms and automation systems require high-accuracy gearboxes for precise motion control, torque transmission, and repeatable performance. Planetary gearboxes dominate at 50.0%. Robotics leads end use at 40.0%. Asia-Pacific commands 64.0% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.58 Billion |

|

Forecast Market Size (2034) |

USD 9.40 Billion |

|

CAGR (2026-2034) |

9.98% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Gear Technology |

Planetary (50.0%, 2025) |

|

Dominant End Use Industry |

Robotics (40.0%, 2025) |

|

Leading Region |

Asia-Pacific (64.0%, 2025) |

The market expanded from USD 2.22 Billion in 2020 to USD 3.58 Billion in 2025, anchored at USD 5.76 Billion in 2030, and forecast to reach USD 9.40 Billion by 2034. The COVID-19 pandemic paradoxically accelerated precision gearbox demand. The manufacturing sector's response to pandemic-driven labour availability uncertainty and social distancing requirements in factories created a structural pull forward of automation investment that sustained precision gearbox demand above the pre-pandemic trajectory from 2021 onward.

To get more information on this market, Request Sample

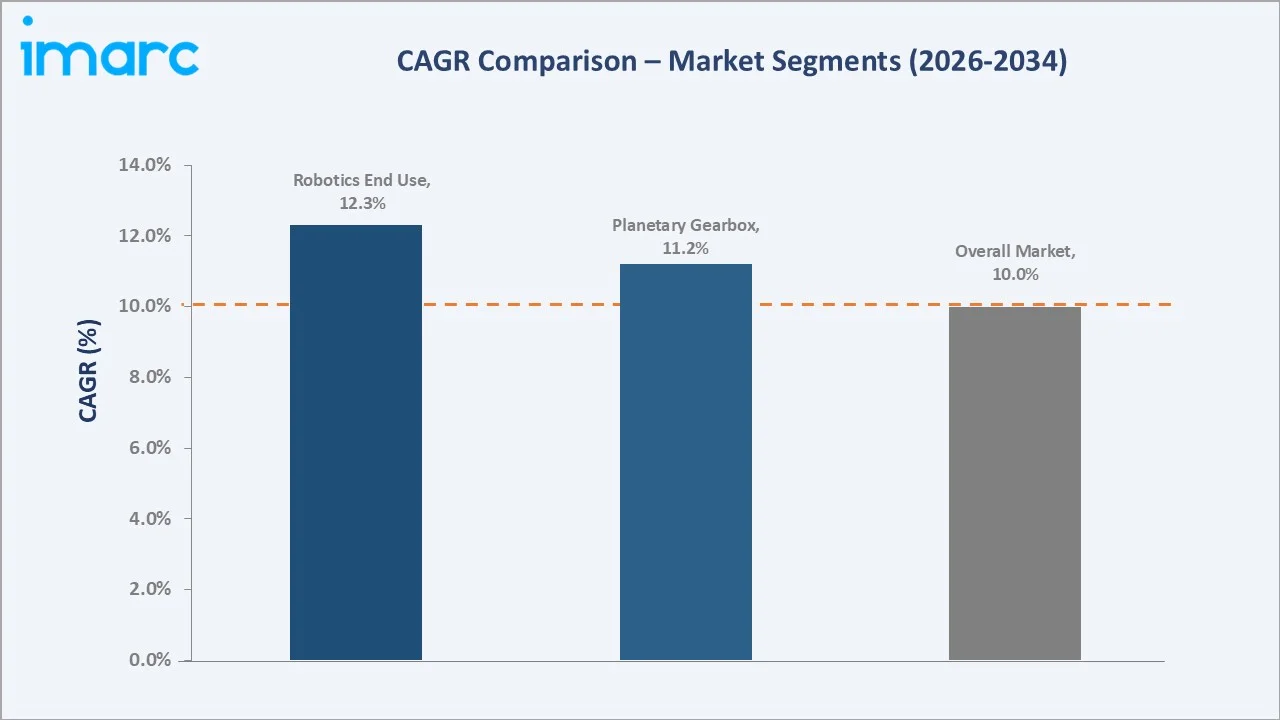

Planetary gearboxes grow fastest at ~11.2% CAGR through collaborative robot joint demand, industrial robot RV cycloidal gearbox scale-up, and humanoid robot joint actuator requirements. Robotics end use at ~12.3% CAGR reflects the compound growth of industrial robots, collaborative robots, and emerging humanoid robot commercial production, each requiring 4-6 precision gearboxes per robot unit.

Executive Summary

The global precision gearbox market reached USD 3.58 Billion in 2025, representing one of the industrial automation sector's most technically demanding and strategically important component categories. A precision gearbox is the enabling torque transmission component for every servo-driven precision motion application in industrial robotics, machine tools, packaging, medical devices, and advanced automation. The market encompasses planetary gearboxes, helical precision gearboxes, bevel and bevel-planetary right-angle precision drives, spur precision gearboxes, and strain wave gearboxes as the primary product categories. The market is projected to reach USD 9.40 Billion by 2034.

Planetary gearboxes at 50.0% dominate through their universal deployment in industrial robot joint axes. Robotics at 40.0% leads end-use demand through global robot installations, each consuming 4-6 precision gearboxes, the cobot expansion creating demand for zero-backlash strain wave gears, and emerging humanoid robot commercial production. Asia-Pacific at 64.0% commands market dominance through Japan's precision gearbox manufacturing leadership and China's world-record annual robot installation volumes.

Key Market Insights

|

Insight |

Data |

|

Dominant Gear Technology |

Planetary - 50.0% revenue share (2025) |

|

Dominant End Use Industry |

Robotics - 40.0% market share (2025) |

|

Leading Region |

Asia-Pacific - 64.0% market share (2025) |

|

Market Opportunity |

Humanoid robot joint actuator gearboxes; collaborative robot cobot growth; medical surgical robot gearboxes; EV actuator precision drives; smart gearbox with integrated sensing |

Key Analytical Observations Supporting the Above Data:

- Planetary at 50.0%: The planetary segment dominates due to its compact design, high torque density, low backlash, and excellent load distribution. These features make it widely preferred in robotics, automation, CNC machinery, and high-precision motion control applications.

- Robotics at 40.0%: Robotics requires highly accurate, compact, and low-backlash gearboxes for smooth motion control and repeatable positioning. Rising industrial robot installations across manufacturing, electronics, automotive, and logistics sectors further boost gearbox demand.

- Asia-Pacific at 64.0%: The Asia-Pacific region dominates due to rapid growth in industrial automation, robotics, electronics manufacturing, and automotive production. Strong robot adoption in China, Japan, South Korea, and India is driving high demand for precision motion control gearboxes.

Precision Gearbox Market Overview

The global precision gearbox market encompasses the design, manufacture, and supply of all precision torque reduction gearboxes used in servo-driven automation, robotics, machine tools, packaging, material handling, food processing, medical devices, and aerospace applications where positioning accuracy, torque density (Nm/kg), torsional rigidity, operational lifetime, and NVH characteristics significantly exceed standard industrial gearbox specifications. Primary product categories include planetary precision gearboxes, helical precision gearboxes, bevel precision gearboxes, spur precision gearboxes, and harmonic drive strain wave gears.

The ecosystem integrates precision gearbox manufacturers, raw material and gear blank suppliers, gear manufacturing equipment providers, quality metrology companies, robot and automation OEMs integrating precision gearboxes, and end-use industries deploying precision automation. Macroeconomic factors include industrial automation growth, rising labor costs, manufacturing modernization, and the expansion of robotics-intensive industries.

Market Dynamics

To evaluate market opportunities, Request Sample

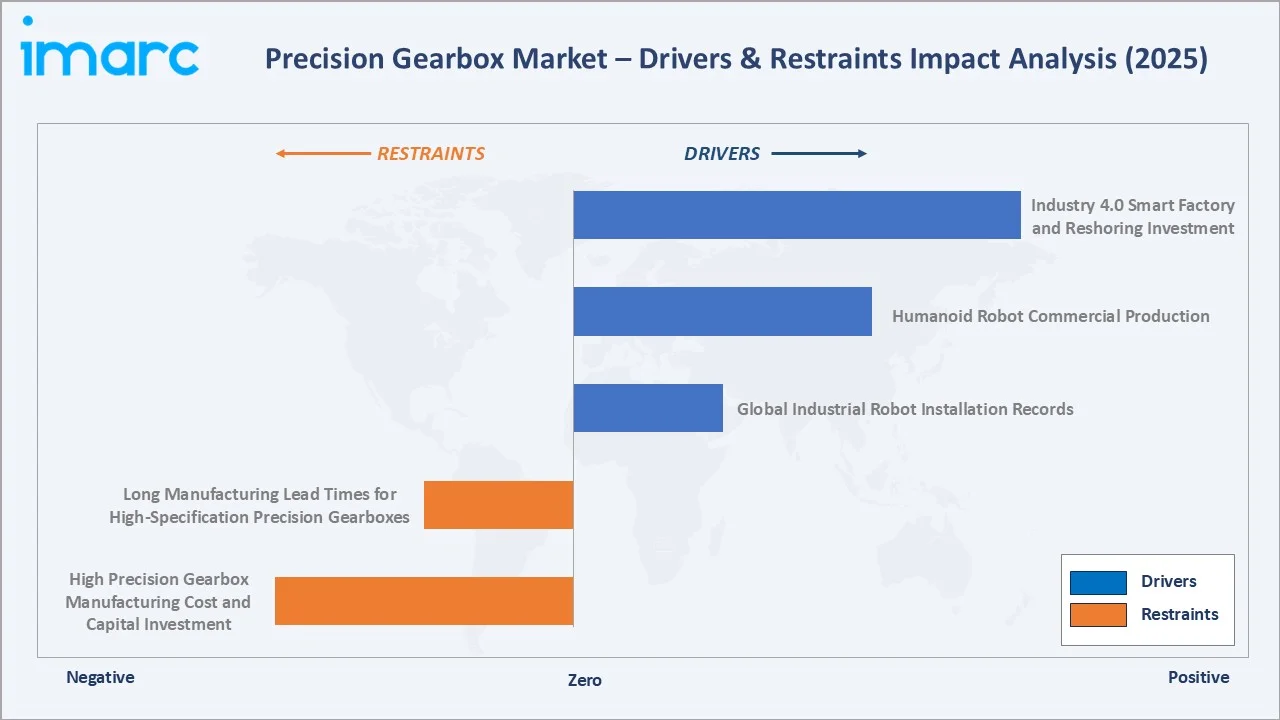

Market Drivers

- Global Industrial Robot Installation Records: The World Robotics 2025 report recording 542,000 robots installed in 2024, with annual installations topped 500,000 units for the fourth straight year, created the highest annual precision gearbox procurement volume in the market's history. Robotic arms require precision gearboxes to deliver high torque, low backlash, smooth rotation, and repeatable positioning. As robot deployment expands across automotive, electronics, logistics, and manufacturing sectors, the need for planetary, harmonic, and cycloidal precision gearboxes continues to grow.

- Humanoid Robot Commercial Production: Humanoid robot commercial production creates demand for compact, lightweight, and high-torque motion control systems. Humanoid robots require multiple precision gearboxes in joints such as arms, legs, shoulders, hips, and wrists for smooth and accurate movement. As production scales, demand for low-backlash gearboxes with high durability and repeatable positioning is expected to increase significantly.

- Industry 4.0 Smart Factory and Reshoring Investment: Industry 4.0 smart factory and reshoring investments are increasing demand for automated, high-precision production systems. Smart factories use robotics, CNC machines, conveyors, and motion control equipment that require low-backlash gearboxes for accurate and reliable operation. Reshoring initiatives are further boosting automation adoption, creating stronger demand for precision gearboxes across manufacturing industries.

Market Restraints

- High Precision Gearbox Manufacturing Cost and Capital Investment: High precision gearbox manufacturing cost and capital investment increase production expenses for advanced machining, heat treatment, precision grinding, and quality testing. These gearboxes require tight tolerances, specialized equipment, and skilled labor, raising entry barriers for manufacturers. Higher costs can limit mass adoption among price-sensitive industries and slow capacity expansion.

- Long Manufacturing Lead Times for High-Specification Precision Gearboxes: Long manufacturing lead times for high-specification precision gearboxes are delaying equipment deployment and project execution timelines. Advanced precision gearboxes require complex machining, high-accuracy assembly, and extensive quality testing, increasing production cycles. Longer delivery periods can disrupt automation projects, limit supply availability, and affect end-user procurement decisions.

Market Opportunities

- Medical and Surgical Robot Precision Gearbox: Medical and surgical robot precision gearboxes present a significant opportunity due to the growing adoption of robotic-assisted healthcare systems. These robots require ultra-precise, low-backlash, and compact gearboxes to enable accurate movement and positioning during surgical procedures. Rising investments in medical automation and minimally invasive surgeries are expected to increase demand for high-performance precision gearboxes.

- Integrated Smart Precision Gearbox with Embedded Sensing: Integrated smart precision gearboxes with embedded sensing enable real-time monitoring of torque, temperature, vibration, load, and wear conditions. This supports predictive maintenance, improves machine uptime, and reduces unexpected failures in robotics and automation systems. As Industry 4.0 adoption grows, demand is increasing for intelligent gearbox solutions that combine precision motion control with data-driven performance monitoring.

Market Challenges

- Chinese Domestic Precision Gearbox Development Progressively Reducing Japanese Import Dependency in China's Robot Market: Chinese domestic precision gearbox development is progressively reducing China’s reliance on imported Japanese gearbox suppliers. Local manufacturers are improving product quality, cost competitiveness, and supply reliability for robotics applications. This increases pricing pressure on established international players and may reduce their market share in China’s fast-growing robot industry.

- Precision Gearbox Intellectual Property Concentration: Precision gearbox intellectual property concentration is challenging because key designs, patents, and manufacturing know-how are often controlled by a limited number of established players. This creates entry barriers for new manufacturers and restricts technology access. It can also increase licensing costs, limit product differentiation, and slow innovation among smaller or emerging gearbox suppliers.

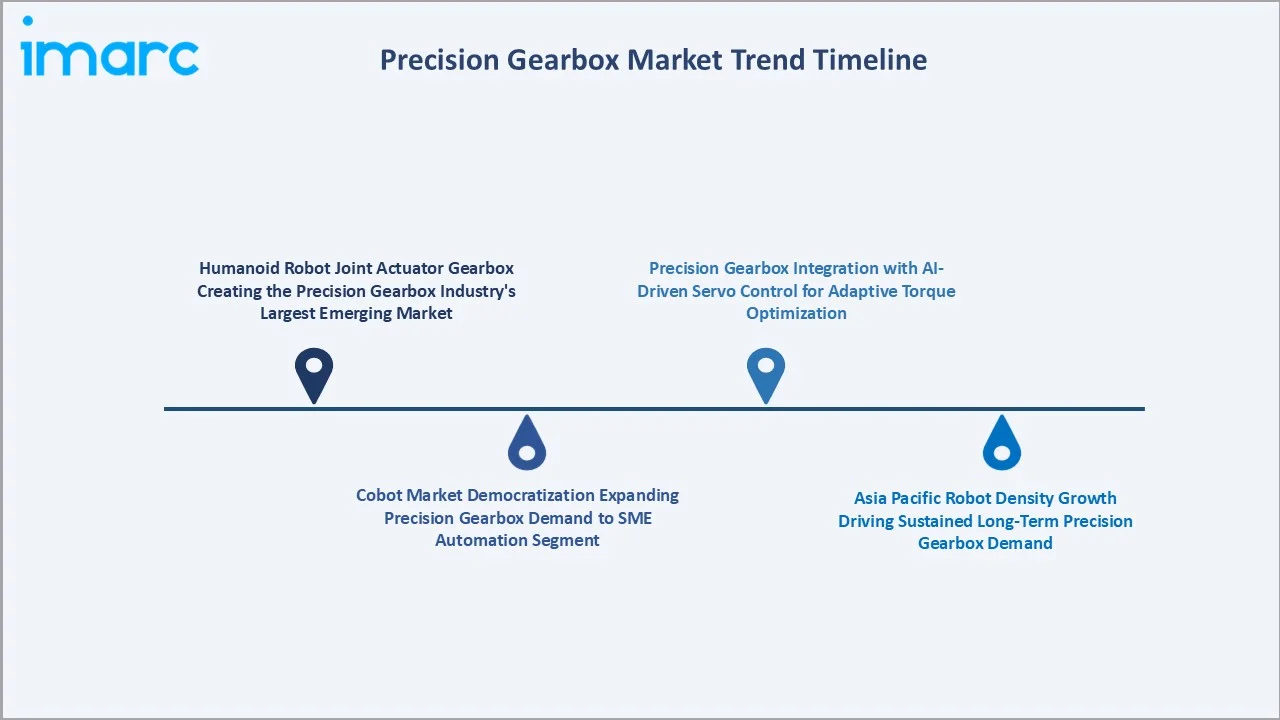

Emerging Market Trends

1. Humanoid Robot Joint Actuator Gearbox Creating the Precision Gearbox Industry's Largest Emerging Market

Humanoid robot joint actuator gearboxes are emerging as humanoid robots require multiple compact, high-torque, and low-backlash gearboxes for arms, legs, hands, hips, and shoulders. Each robot uses several precision joints, creating significant volume demand as commercial production scales. This is positioning humanoid robotics as one of the largest future growth areas for the precision gearbox market. In April 2026, Schaeffler entered a strategic partnership with VinDynamics to support humanoid robotics development through the supply of planetary gearboxes. These gearboxes are key actuator components that act like robot muscles and joints, while both companies also use robot and application data to improve actuator performance and enable future services such as predictive maintenance. As partnerships like this scale commercial humanoid robot development, demand for advanced precision gearboxes is expected to increase significantly.

2. Cobot Market Democratization Expanding Precision Gearbox Demand to SME Automation Segment

Cobot market democratization is emerging as affordable, easy-to-program collaborative robots are making automation accessible to small and medium-sized enterprises. Cobots require compact, low-backlash precision gearboxes for safe, accurate, and repeatable motion. As SME automation adoption expands across assembly, packaging, electronics, and light manufacturing, demand for cost-efficient precision gearboxes is expected to grow.

3. Asia Pacific Robot Density Growth Driving Sustained Long-Term Precision Gearbox Demand

Asia-Pacific robot density growth is emerging as manufacturers in China, Japan, South Korea, and India rapidly increase automation across factories. Higher robot density means more robotic joints and motion systems are deployed, creating sustained demand for precision gearboxes. World Robotics 2025 reported that 542,000 industrial robots were installed in 2024, with Asia accounting for 74% of new deployments. As rapid automation growth across China, Japan, South Korea, and other regional manufacturing hubs is increasing the use of robotic joints and motion systems, thereby driving sustained long-term demand for precision gearboxes.

4. Precision Gearbox Integration with AI-Driven Servo Control for Adaptive Torque Optimization

Precision gearbox integration with AI-driven servo control is emerging as automation systems increasingly require adaptive torque, speed, and positioning performance. AI-enabled servo systems can analyze load conditions in real time and optimize gearbox operation for higher efficiency, smoother motion, and reduced wear. This supports predictive maintenance, improves robotic accuracy, and increases demand for intelligent precision gearbox solutions.

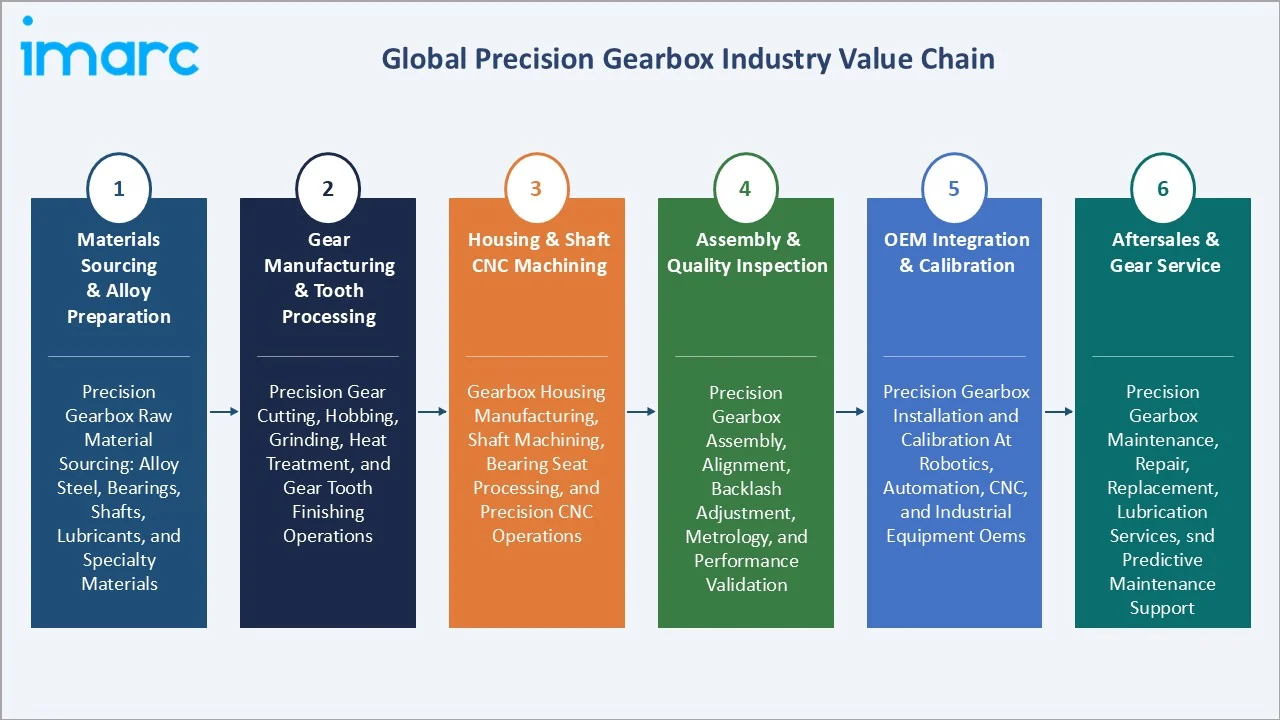

Industry Value Chain Analysis

The precision gearbox value chain integrates precision alloy materials sourcing, gear manufacturing & tooth processing, housing and shaft precision CNC machining, assembly and quality inspection, OEM integration and calibration, and after-sales gear service.

|

Stage |

Key Participants |

|

Materials Sourcing & Alloy Preparation |

Precision gearbox raw material sourcing, including alloy steel, bearings, shafts, lubricants, and specialty materials |

|

Gear Manufacturing & Tooth Processing |

Precision gear cutting, hobbing, grinding, heat treatment, and gear tooth finishing operations |

|

Housing & Shaft Precision CNC Machining |

Gearbox housing manufacturing, shaft machining, bearing seat processing, and precision CNC operations |

|

Assembly & Quality Inspection |

Precision gearbox assembly, alignment, backlash adjustment, metrology, and performance validation |

|

OEM Integration & Calibration |

Precision gearbox installation and calibration at robotics, automation, CNC, and industrial equipment OEMs |

|

Aftersales & Gear Service |

Precision gearbox maintenance, repair, replacement, lubrication services, and predictive maintenance support |

The gear tooth grinding stage is the value chain's most capital-intensive and quality-critical step. The assembly and quality inspection stage is uniquely critical in precision gearbox value chains because backlash specification achievement requires 100% unit-by-unit measurement and selective assembly, a labour and metrology-intensive process that cannot be shortcut without backlash specification non-conformances.

Technology Landscape in the Precision Gearbox Industry

RV Cycloidal Gearbox Technology

RV cycloidal gearbox technology provides high torque capacity, excellent rigidity, low backlash, and superior positioning accuracy. These gearboxes are widely used in industrial robots and heavy-duty automation systems due to their ability to handle high loads with stable performance. Their durability and precision are driving adoption in next-generation robotics and advanced motion control applications.

Strain Wave Gearing Technology

Strain wave gearing technology enables compact, lightweight, and high-reduction-ratio gearboxes with very low backlash. It is widely used in robotic arms, collaborative robots, medical robots, and semiconductor equipment, where precise motion and repeatability are critical. Its high torque accuracy and space-saving design are driving adoption in advanced automation and next-generation robotics. In May 2025, ECM PCB Stator Tech launched a new servo motor featuring integrated 50:1 gear ratio strain wave gearing, designed to deliver high torque density, precise motion control, and a compact form factor. Such innovations improve positioning accuracy, reduce system size, and strengthen adoption in robotics, automation, and high-precision motion applications.

Precision Planetary Gearbox Technology

Precision planetary gearbox technology offers high torque density, compact design, low backlash, and excellent positioning accuracy. These gearboxes are widely used in robotics, CNC machinery, servo systems, and automation equipment due to their efficient load distribution and reliable motion control. Their versatility and compatibility with advanced automation systems are driving broader adoption across industrial applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Axis of Orientation |

🔒 |

🔒 |

2025 |

|

Gear Technology |

Planetary |

50.0% |

2025 |

|

End Use Industry |

Robotics |

40.0% |

2025 |

|

Region |

Asia Pacific |

64.0% |

2025 |

By Gear Technology

Planetary gearboxes lead at 50.0% (2025). This category encompasses the most technically diverse precision gearbox segment. The planetary segment's ~11.2% CAGR is driven by three concurrent demand vectors: industrial robot RV cycloidal, collaborative robot strain wave, and humanoid robot joint actuators.

To access detailed market analysis, Request Sample

Helical at 21.8% serves the industrial machine and continuous-duty automation segment through inline helical, helical-bevel, and helical-worm configurations for conveyor, packaging, and machine tool main drive applications. Bevel at 14.6% captures the right-angle precision transmission segment for machine tool rotary tables, robot wrist axes, and aerospace actuators. Spur at 8.7% serves cost-sensitive light-duty servo applications. Others at 4.9% primarily encompasses harmonic drive strain wave gears for cobots, medical, and space applications.

By End Use Industry

Robotics leads at 40.0% (2025). The robotics segment's above-market ~12.3% CAGR reflects the convergence of industrial robot installation records, cobot market expansion, and emerging humanoid robot commercial production. Machine tools at 18.4% captures the precision gearbox market's highest-specification application segment. Materials handling at 12.7% includes automated warehouse, AGV (automated guided vehicle), and conveyor precision drives.

Packaging at 10.6% reflects precision servo packaging machine drives requiring precision gearboxes for high-cycle-rate servo axes. Food and beverage at 8.4% emphasise hygiene-rated stainless steel housing and wash-down resistant precision gearboxes for food processing automation. Medical at 5.9% is the highest-margin precision gearbox application with surgical robots, rehabilitation exoskeletons, and medical imaging precision drives, commanding a 3-5x industrial pricing premium for precision gearbox supply.

Regional Market Insights

|

Region |

Share (2025) |

Key Precision Gearbox Market Drivers & Characteristics |

|

Asia-Pacific |

64.0% |

Driven by strong industrial automation growth, high robot deployment, expanding electronics manufacturing, and rising adoption of smart factories |

|

Europe |

16.2% |

Driven by advanced robotics adoption, automotive automation, Industry 4.0 initiatives, and demand for high-precision manufacturing systems |

|

North America |

11.8% |

Supported by increasing factory automation, investments in robotics, and the growing deployment of collaborative robots across industries |

|

Latin America |

4.5% |

Driven by manufacturing modernization, automation investments, and expanding industrial production activities |

|

Middle East and Africa |

3.5% |

Emerging with increasing industrial automation initiatives, infrastructure development, and the adoption of advanced manufacturing technologies |

Asia-Pacific, at 64.0%, dominates through Japan's precision gearbox manufacturing leadership and China's record of robot installations. Europe, at 16.2%, reflects German precision gearbox technology excellence and industrial robot density leadership.

North America, at 11.8%, reflects US manufacturing reshoring, automation investment and the world's largest surgical robot installed base. Latin America, at 4.5%, reflects Brazil and Mexico's growing manufacturing automation. MEA, at 3.5%, captures GCC industrial automation and Israeli aerospace precision gearbox applications.

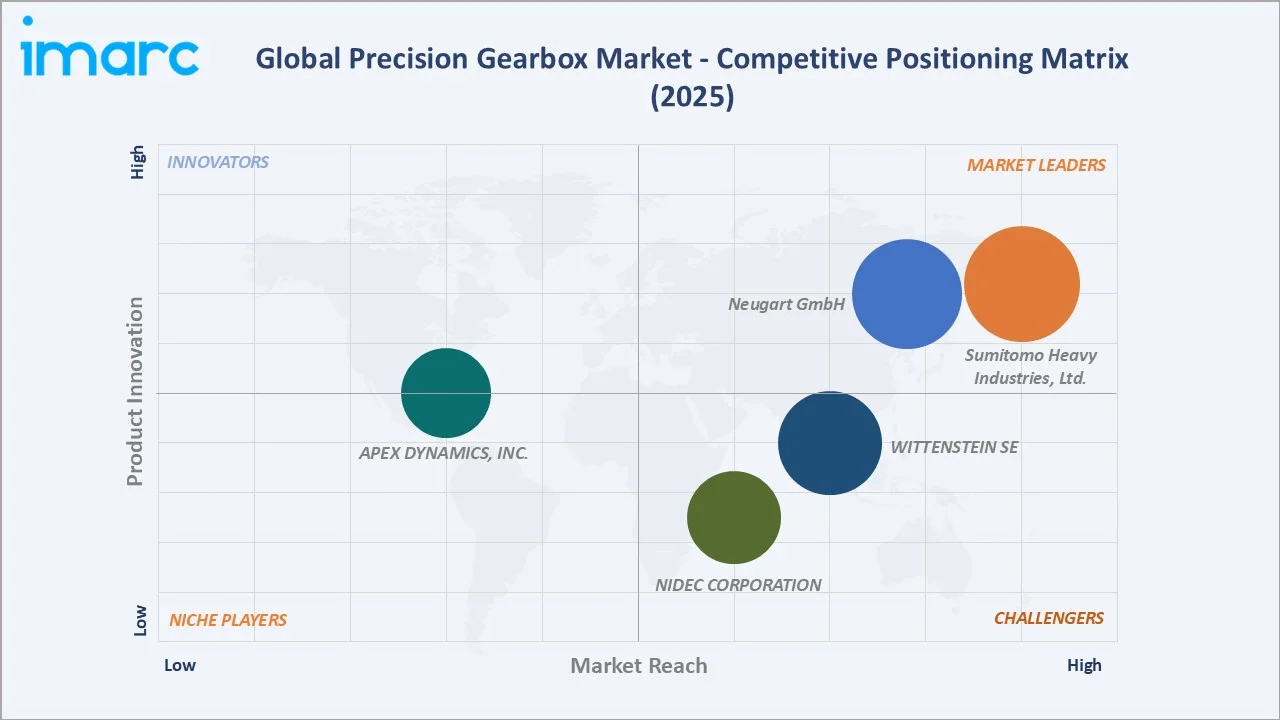

Competitive Landscape

The global precision gearbox market is highly concentrated at the robotic precision cycloidal gearbox tier. At the precision planetary tier for servo automation, market share is more distributed among regional specialists.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Sumitomo Heavy Industries, Ltd. |

Fine CYCLO DA, UA, E-Cyclo |

Market Leader |

Sumitomo Heavy Industries, Ltd., through its Sumitomo Drive Technologies division, plays a leading role in the global precision gearbox market, particularly as a pioneer and major manufacturer of cycloidal speed reducers. |

|

Neugart GmbH |

PSNpro, PSFNpro, PSBNpro, WPLN, WPSFN, PSFN, PSN, PLN, PLFN |

Market Leader |

Neugart GmbH specializes in high-precision planetary and right-angle gearboxes for robotics, automation, and industrial applications. |

|

WITTENSTEIN SE |

Galaxie G, Miniaturized Galaxie, Galaxie GS, Galaxie GH, XPC+ |

Strong Challenger |

WITTENSTEIN SE is recognized as a pioneer in low-backlash planetary and right-angle gearboxes and a key innovator in mechatronic drive systems. |

|

NIDEC CORPORATION |

EVB Series, EVL Series, VRB Series, VRL Series |

Strong Challenger |

Nidec Corporation, primarily through its subsidiary Nidec Drive Technology Corporation (formerly Shimpo), is a dominant global player in the precision gearbox market, specializing in high-precision power transmission systems and servo gearboxes for robotics and industrial automation. |

|

APEX DYNAMICS, INC. |

MG-SERIES, MGK-SERIES, MGH-SERIES, MGHK-SERIES, MGHC-SERIES, MGHCK-SERIES |

Established Player |

Apex Dynamics, Inc. is a global leader in the manufacturing of high-precision planetary gearboxes, focusing on servomotor-driven applications. |

The competitive landscape is being actively disrupted by two forces: the humanoid robot commercial launch, creating entirely new precision gearbox requirements where no established incumbent has a dominant position, and Chinese domestic precision gearbox quality improvement, progressively qualifying Chinese manufacturers for cost-sensitive Chinese domestic robot applications.

Key Company Profiles

Sumitomo Heavy Industries, Ltd.

Sumitomo Heavy Industries, Ltd. is a Japan-based industrial machinery and power transmission company with a strong presence in the precision gearbox market through its cycloidal reducers, planetary gear systems, and precision motion control solutions.

- Key Products: Fine CYCLO DA, UA, E-Cyclo

- Recent Developments: In January 2025, Sumitomo Heavy Industries, Ltd. introduced its new zero-backlash DA Series gear head for servo motors under the Fine CYCLO high-precision gearbox lineup. The product is designed for easy mounting and high-precision positioning, making it suitable for machine tools, semiconductor manufacturing equipment, and other precision applications.

- Strategic Focus: Expanding high-precision, zero-backlash gearbox solutions for robotics, servo motors, machine tools, and semiconductor equipment.

Neugart GmbH

Neugart GmbH is a Germany-based manufacturer specializing in precision planetary gearboxes and drive technology solutions with a strong presence in the precision gearbox market. The company focuses on developing planetary gearboxes, right-angle gearboxes, and customized drive systems used in robotics, automation, machine tools, packaging equipment, and material handling applications.

- Key Products: PSNpro, PSFNpro, PSBNpro, WPLN, WPSFN, PSFN, PSN, PLN, PLFN.

- Recent Developments: In November 2025, Neugart launched a new performance class above its current precision gearbox range with the PSNpro, PSFNpro, and PSBNpro series. These gearboxes use innovative gear technologies and advanced materials, with improved tooth flank quality that reduces load peaks and allows higher torque transmission while maintaining the same service life.

- Strategic Focus: Advancing high-performance precision planetary gearboxes with higher torque capacity, improved materials, and optimized gear technology.

Market Concentration Analysis

The precision gearbox market exhibits extraordinary concentration at the robotic precision gearbox tier. This concentration reflects both the technical difficulty of achieving performance specifications from competitive equipment and the long-term OEM qualification relationships that keep robot OEMs certified on existing precision gearbox suppliers rather than continuously re-qualifying alternatives. At the precision planetary gearbox tier for servo automation (non-robot applications), market concentration is significantly lower. The Chinese domestic precision gearbox development is progressively increasing the market concentration disruption risk.

Investment & Growth Opportunities

Highest Growth Segments

Robotics end use (~12.3% CAGR), planetary gearboxes (~11.2% CAGR), medical precision gearbox (~10-12% CAGR from small premium base), humanoid robot joint gearbox (~25-40% CAGR from near-zero commercial base), collaborative robot strain wave (~15-18% CAGR), Asia Pacific market (~10.5% CAGR), and smart IoT-integrated precision gearbox (~15% CAGR from small base) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Humanoid robot joint actuator precision gearbox development represents the precision gearbox market's highest-risk, highest-reward emerging investment. Companies that achieve qualification as preferred precision gearbox suppliers for humanoid robot programmes by 2026-2027 position themselves for long-term high-volume supply relationships that transform their business scale.

Investment Themes

- Compact lightweight precision gearbox development for humanoid robot joint application at mass-production cost: Developing precision gearboxes that meet humanoid robot joint requirements requires a fundamental product design departure from current industrial robot RV gearboxes toward a new product optimized for mass-production humanoid joint economics. The first manufacturers to achieve this specification-cost intersection capture the humanoid robot joint gearbox market at its formative stage before incumbent industrial robot precision gearbox suppliers establish volume relationships with humanoid OEMs.

- Smart IoT-integrated precision gearbox platform for predictive maintenance as recurring service revenue: Precision gearbox manufacturers investing USD 20-50 Million in smart gearbox electronics integration and IIoT cloud platform development can capture 3-5x per-unit lifetime value above standard precision gearbox sale economics as industrial customers adopt condition-based maintenance strategies across their automation asset base.

Future Market Outlook (2026-2034)

The global precision gearbox market is projected to grow from USD 3.58 Billion in 2025 to USD 9.40 Billion by 2034, delivering a 9.98% CAGR over the forecast period. The market's anchor value of USD 5.76 Billion in 2030 represents a precision gearbox industry fundamentally shaped by three concurrent demand forces not previously operating simultaneously: industrial robot installation records, collaborative robot market mainstream commercialization, and humanoid robot commercial production entering its first significant volume phase.

Three structural forces define precision gearbox market growth through 2034 with exceptional confidence. The global manufacturing automation imperative is irreversible; labour cost inflation, demographic workforce declines in advanced economies, and competitive manufacturing efficiency requirements make industrial robot adoption fundamentally non-optional for manufacturers in cost-exposed product categories, creating sustained precision gearbox demand that is resistant to economic cycle variability. The compounding installed robot base creates a proportionally growing replacement precision gearbox market. The humanoid robot demand optionality creates a forecast upside scenario where market growth substantially exceeds the base CAGR.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025) including Chief Technology Officers; Precision Gearbox Division Directors; Robot OEM procurement leads; Precision gear manufacturing equipment specialists; Humanoid robot development engineering leads; precision gearbox distributor principals in North America, Europe, and Asia Pacific.

Secondary Research

Secondary research encompassed the International Federation of Robotics World Robotics 2025 Report; company annual reports; machine tool industry statistics 2024; European plastics and rubber machinery association data; Packaging Machinery Manufacturers Institute North America market data; Machinery Dealers National Association precision machine tool statistics; International Journal of Machine Tools and Manufacture precision gearbox technology publications; Gear Technology International precision gear manufacturing papers. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using application-based bottom-up model: (i) robotics sector: IFR robot installation forecast by year multiplied by average precision gearbox unit count per robot type multiplied by average unit price by gearbox type and volume tier; (ii) non-robotics sectors: machine tool production statistics multiplied by average precision gearbox content per machine; packaging and materials handling automation investment data multiplied by precision gearbox content factor; medical robot installed base growth multiplied by replacement and new gearbox events.

Precision Gearbox Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Axis of Orientations Covered | In-Line/Coaxial, Right Angle, Parallel |

| Gear Technologies Covered | Planetary, Bevel, Helical, Spur, Others |

| End Use Industries Covered | Food and Beverage, Machine Tools, Materials Handling, Packaging, Robotics, Medical, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Sumitomo Heavy Industries, Ltd., Neugart GmbH, WITTENSTEIN SE, NIDEC CORPORATION, APEX DYNAMICS, INC., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the precision gearbox market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global precision gearbox market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the precision gearbox industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Precision Gearbox Market Report

The global precision gearbox market reached USD 3.58 Billion in 2025, driven by planetary gearboxes at 50.0% market share from annual industrial robot installations each consuming 4-6 precision RV or cycloidal gearboxes, Robotics end use dominating at 40.0% through record robot installations and cobot market expansion, Asia-Pacific commanding 64.0% through Japan's precision gearbox manufacturing leadership and China's world-record annual robot deployment, and growing collaborative robot and emerging humanoid robot applications creating new demand pools above traditional industrial robot procurement.

The market grows at 9.98% CAGR during 2026-2034, reaching USD 9.40 Billion by 2034. This growth reflects IFR-projected industrial robot installation growth, collaborative robot market mainstream commercialization, creating high annual strain wave gearbox procurement events, and humanoid robot commercial production beginning to generate meaningful precision gearbox volume demand from 2027 onward.

Planetary gearboxes lead at 50.0%, this category encompasses both conventional precision epicyclic planetary and the commercially dominant RV cycloidal gearboxes, plus harmonic drive strain wave gears for collaborative robots. Planetary grows fastest at ~11.2% CAGR, driven by robot installation volume growth, cobot strain wave gearbox demand, and emerging humanoid robot joint actuator applications requiring miniaturized precision planetary or cycloidal gearboxes per joint.

Robotics leads at 40.0% and grows fastest at ~12.3% CAGR. Robotics' dominance reflects the high annual global industrial robot installations, each consuming 4-6 precision RV cycloidal gearboxes, plus high annual cobot installations each consuming 6 harmonic drive strain wave gearboxes, creating the world's highest-volume precision gearbox procurement category.

Asia-Pacific leads at 64.0%, by far the largest regional share, reflecting Japan's global leadership in precision gearbox manufacturing and China's high annual industrial robot installations, creating the world's highest-concentration precision gearbox demand market.

Leading companies include Sumitomo Heavy Industries, Ltd., Neugart GmbH, WITTENSTEIN SE, NIDEC CORPORATION, and APEX DYNAMICS, INC, among others.

The market is projected to reach approximately USD 5.76 Billion by 2030, with global industrial robot installations growth, collaborative robot annual installations creating high annual strain wave gearbox procurement events, and humanoid robot commercial production beginning to contribute 50,000-200,000 annual units of joint gearbox demand.

Three priority opportunities: humanoid robot joint actuator gearbox development and supplier qualification, medical precision gearbox certification and surgical robot OEM qualification, and smart IoT precision gearbox platform development for predictive maintenance recurring revenue.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)