Preclinical CRO Market Size, Share, Trends, and Forecast by Service, End Use, and Region, 2026-2034

Global Preclinical CRO Market Size, Share, Trends & Forecast (2026-2034)

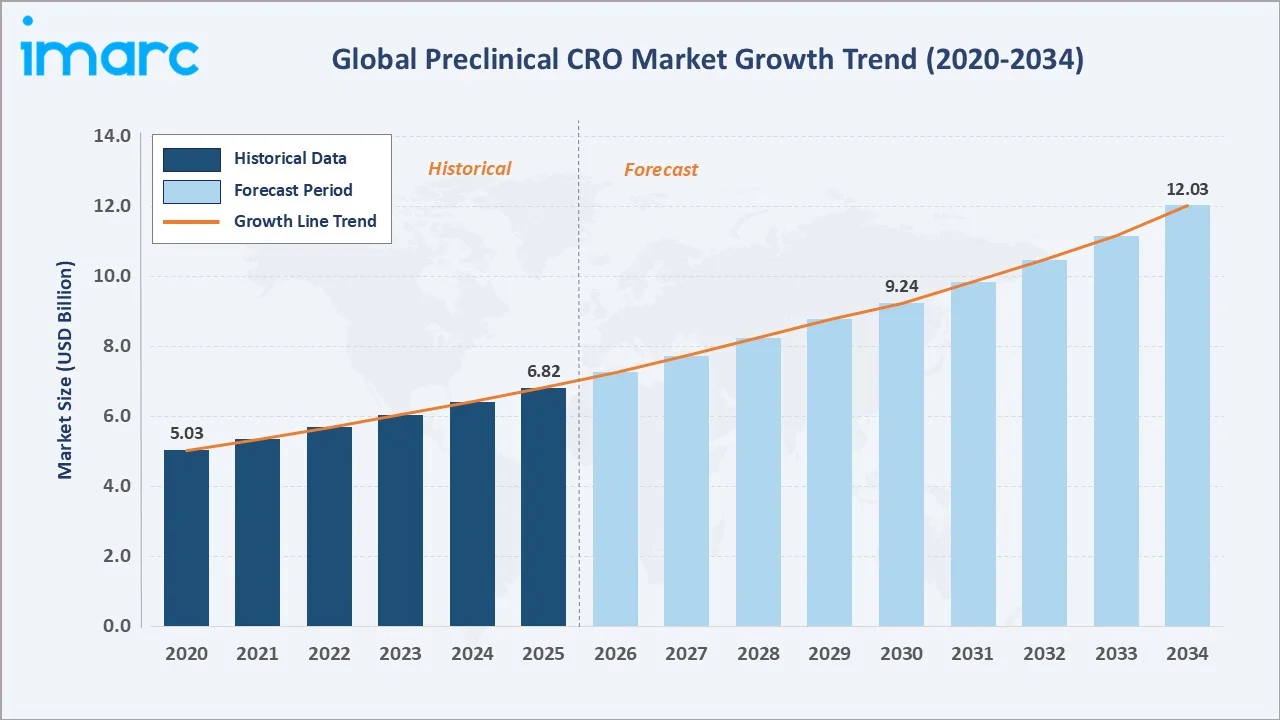

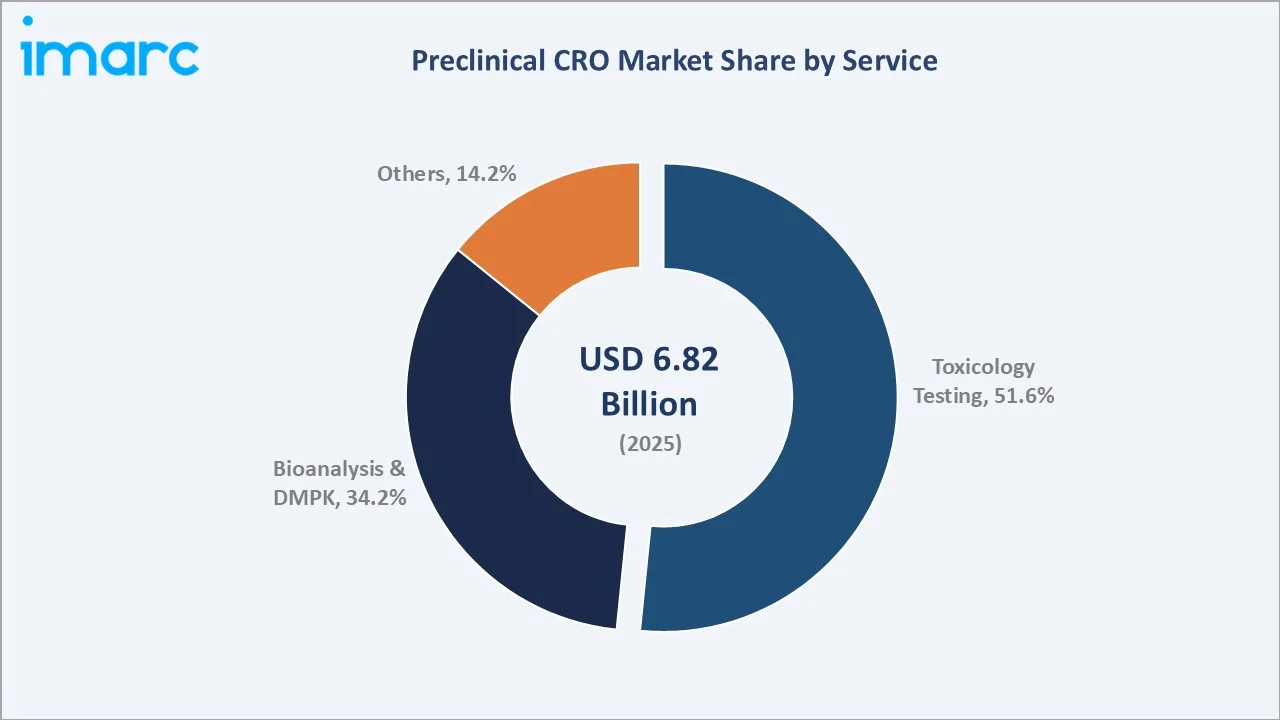

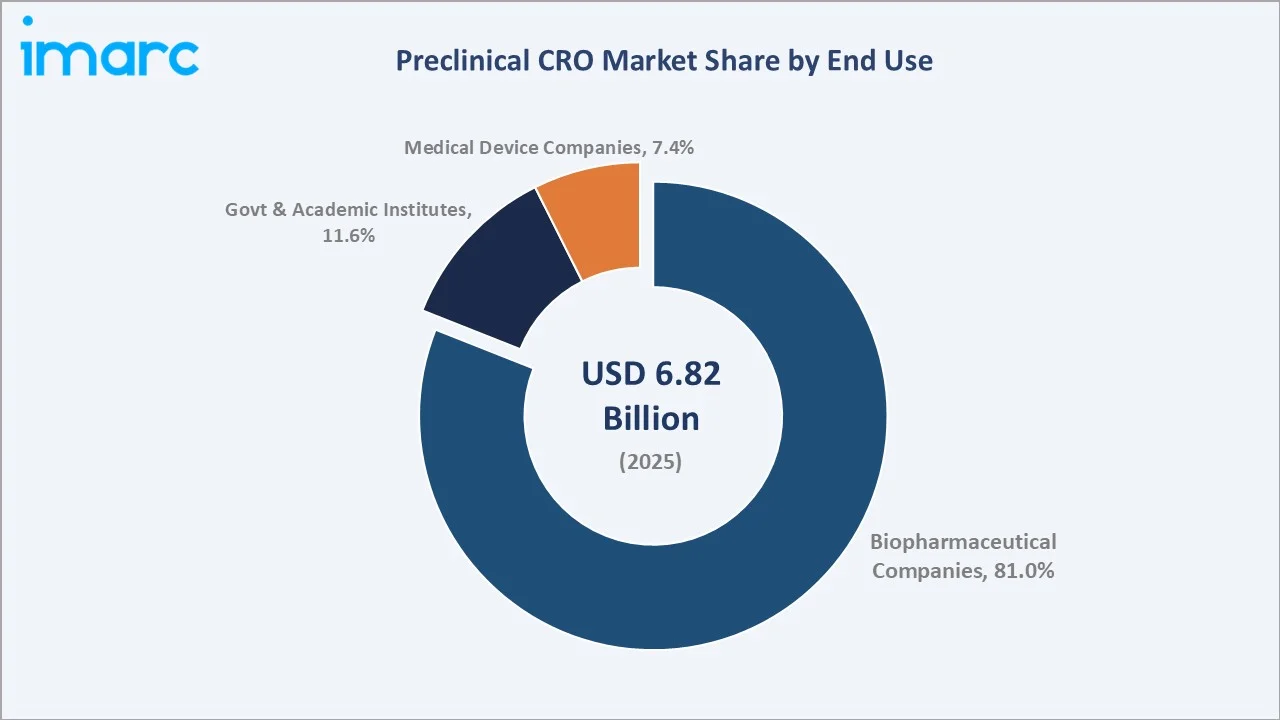

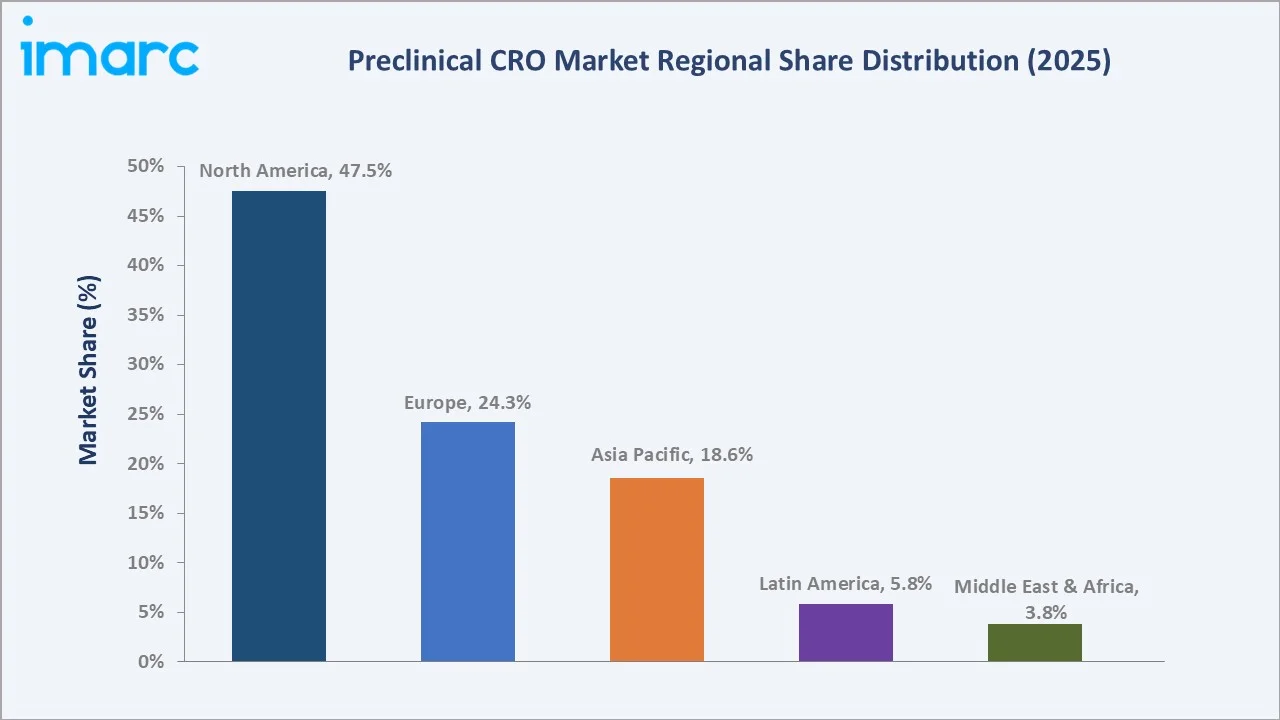

The global preclinical CRO market size was valued at USD 6.82 Billion in 2025 and is projected to reach USD 12.03 Billion by 2034, exhibiting a CAGR of 6.28% during the forecast period 2026-2034. Rising pharmaceutical R&D expenditure, the growing complexity of regulatory requirements, and the accelerating adoption of outsourcing models by biopharmaceutical companies are the primary catalysts driving the market. Toxicology Testing leads the service mix at 51.6% in 2025, while Biopharmaceutical Companies account for 81.0% of end-use demand. North America dominates with a 47.5% revenue share in 2025, underpinned by a dense FDA-regulated drug pipeline and deep CRO infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.82 Billion |

|

Forecast Market Size (2034) |

USD 12.03 Billion |

|

CAGR (2026-2034) |

6.28% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (47.5% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~8.0%) |

|

Leading Service Segment |

Toxicology Testing (51.6%, 2025) |

|

Leading End-Use Segment |

Biopharmaceutical Companies (81.0%, 2025) |

The global preclinical CRO market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by biopharmaceutical outsourcing, expanding clinical pipelines, and AI-integrated drug discovery services.

To get more information on this market, Request Sample

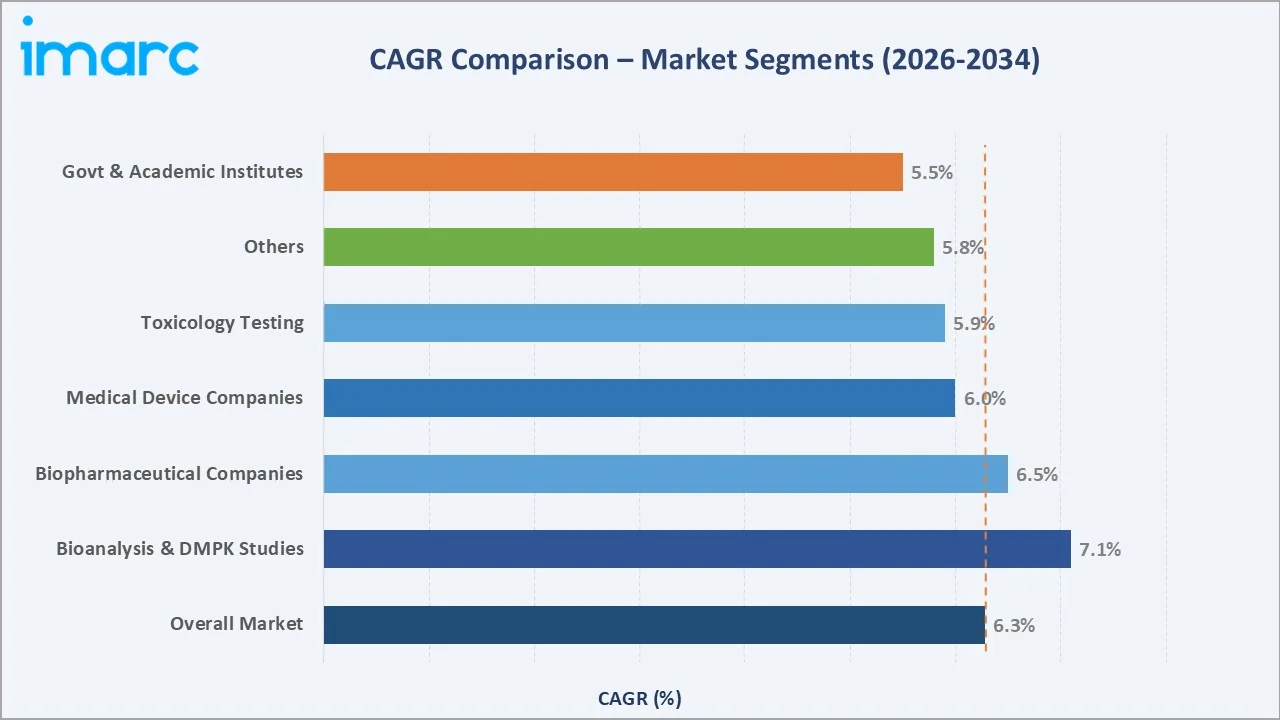

Segment-level CAGR comparisons highlighting Bioanalysis and DMPK Studies and Biopharmaceutical end use as the fastest-growing categories within the global preclinical CRO industry analysis through 2034.

Executive Summary

The global preclinical CRO market is experiencing sustained structural expansion, driven by the convergence of escalating drug development complexity and the accelerating outsourcing trend within the pharmaceutical and biotechnology industries. Valued at USD 6.82 Billion in 2025, the market is forecast to reach USD 12.03 Billion by 2034 at a CAGR of 6.28%.

Toxicology Testing commands the largest service share at 51.6% in 2025, reflecting the non-negotiable requirement for GLP-compliant safety data packages ahead of IND submissions to the U.S. FDA and the European Medicines Agency (EMA). Bioanalysis and DMPK Studies represent 34.2%, a proportion expanding as drug developers invest more heavily in metabolite identification and pharmacokinetic profiling for complex modalities, including biologics, oligonucleotides, and gene therapies.

Biopharmaceutical Companies account for an overwhelming 81.0% of end-use demand in 2025. The chronic disease burden, with the U.S. Centers for Disease Control and Prevention reporting that six in ten American adults live with at least one chronic condition, sustains a high-value drug pipeline. North America commands 47.5% of the global market. Asia Pacific, at 18.6%, is the fastest-growing region driven by cost-competitive laboratory infrastructure in India and China.

Key Market Insights

|

Insight |

Data |

|

Largest Service Segment |

Toxicology Testing – 51.6% share 2025 |

|

Leading End-Use Segment |

Biopharmaceutical Companies – 81.0% share 2025 |

|

Leading Region |

North America – 47.5% revenue share 2025 |

|

Fastest Growing Region |

Asia Pacific (CAGR ~8.0%) |

|

Top Companies |

Charles River Laboratories International, Inc., Fortrea, ICON plc, and WuXi AppTec Co., Ltd. |

Key Analytical Observations Supporting The Above Data:

- Toxicology Testing's 51.6% dominance in 2025 reflects mandatory GLP safety testing requirements ahead of every IND filing, making this segment structurally insulated from R&D budget cycles.

- Bioanalysis and DMPK Studies at 34.2% are growing faster than the blended market rate, driven by the increasing prevalence of biologics, gene therapies, and RNA-based modalities requiring sophisticated metabolic profiling.

- Biopharmaceutical companies at 81.0% of end use demonstrate their deep structural dependence on CRO partnerships; for most mid-size biotechs, outsourcing is the default operating model for all preclinical work.

- North America's 47.5% share is anchored by the United States, which contributes approximately 93.7% of regional revenue, fuelled by the world's highest per-capita pharmaceutical R&D investment.

- Asia Pacific is the fastest growing geography, with India's preclinical CRO market valued at USD 183.3 Million in 2023 and expanding at a CAGR of 11.4% through 2030, driven by Syngene International and Jubilant Pharmova Limited.

Global Preclinical CRO Market Overview

Preclinical contract research organizations (CROs) provide specialized scientific services that pharmaceutical, biotechnology, and medical device companies require before advancing a candidate compound into human clinical trials. Core service offerings include in vitro and in vivo toxicology testing, bioanalytical method development, pharmacokinetics and pharmacodynamics profiling, drug metabolism and DMPK studies, efficacy testing, and safety pharmacology. All studies supporting regulatory submissions must be conducted under Good Laboratory Practice (GLP) standards defined by the U.S. FDA (21 CFR Part 58) and the OECD Principles of GLP.

Applications span the full biopharmaceutical pipeline: small molecule drugs, biologics, gene therapies, cell therapies, ADCs, and mRNA therapeutics. The market serves multinational pharmaceutical corporations, virtual biotechs, academic spinouts, and government agencies, including the National Institutes of Health (NIH). Macroeconomic tailwinds include rising global R&D expenditure, an expanding advanced-modality therapeutic pipeline, and a chronic disease burden that sustains high commercial pressure for new drug approvals.

The global preclinical CRO industry is underpinned by strong macroeconomic fundamentals. Over 6,000 drugs are in active clinical development worldwide. The FDA approved a record number of novel drugs in 2023-2024, each representing preclinical CRO work completed years prior.

Market Dynamics

To evaluate market opportunities, Speak to Analyst

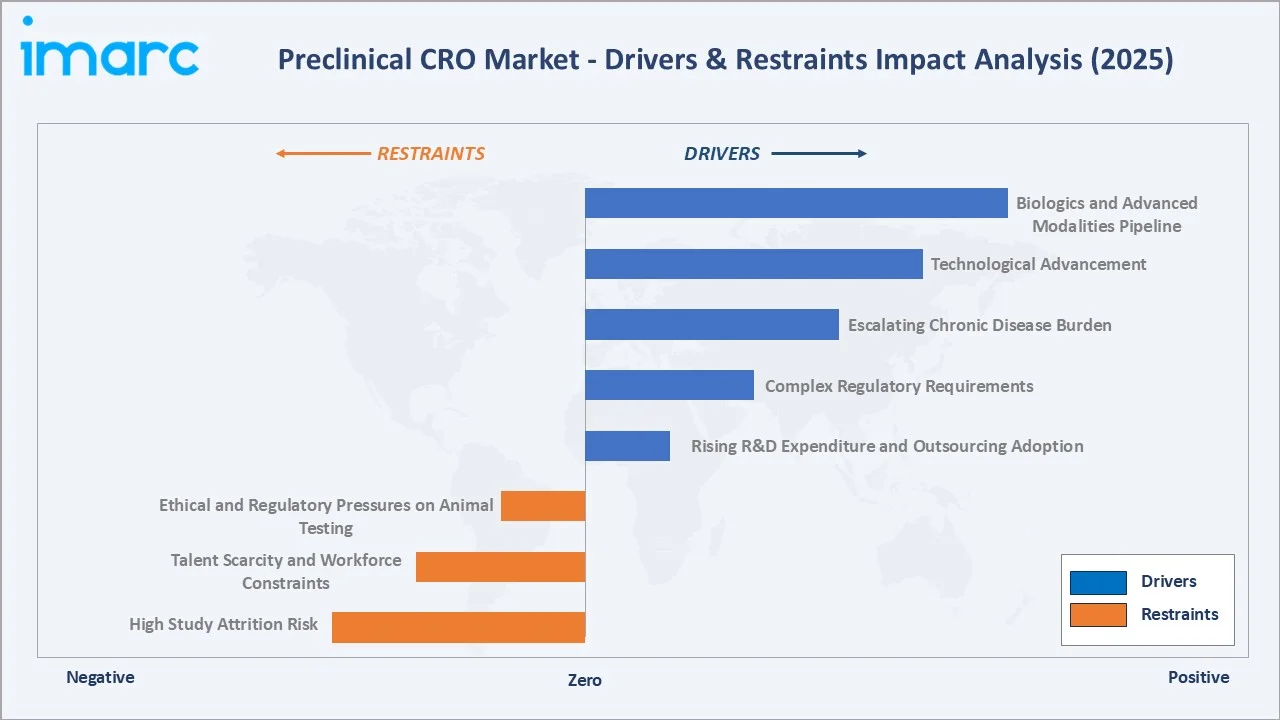

Market Drivers

- Rising R&D Expenditure and Outsourcing Adoption: Global pharmaceutical R&D spending surpassed USD 250 billion in 2024, according to industry estimates (e.g., PhRMA, Evaluate Pharma). Drug developers are increasingly shifting toward asset-light operating models, retaining core discovery capabilities while outsourcing capital-intensive preclinical functions to CROs. This model enables 30–40% cost efficiencies, improved scalability, and faster study execution timelines.

- Complex Regulatory Requirements: The U.S. FDA, EMA, and other agencies mandate extensive GLP-compliant preclinical data packages before any IND or CTA approval. The NCATS notes that a new drug journey from the lab to the clinic can take up to 15 years, with preclinical testing constituting a significant portion.

- Escalating Chronic Disease Burden: According to the Centers for Disease Control and Prevention, 6 in 10 U.S. adults suffer from at least one chronic disease, with cardiovascular diseases and cancer accounting for ~40% of annual mortality. This epidemiological burden continues to drive robust drug discovery pipelines across oncology, neurology, metabolic, and cardiovascular segments.

- Technological Advancement: Advancements in AI-driven toxicology, organ-on-chip systems, and high-content screening technologies are improving the efficiency, predictability, and throughput of preclinical studies. Initiatives by organizations like the National Center for Advancing Translational Sciences are further strengthening translational research capabilities.

Market Restraints

- High Study Attrition Risk: Drug development remains inherently high-risk, with a significant proportion of candidates failing in later stages despite extensive preclinical evaluation. This creates challenges in demonstrating predictive accuracy and managing client expectations.

- Talent Scarcity and Workforce Constraints: The specialized skill set required for GLP toxicology, DMPK, and bioanalytical work remains scarce. High demand for credentialed study directors and analytical chemists is inflating labour costs across North America and Europe.

- Ethical and Regulatory Pressures on Animal Testing: Growing regulatory encouragement for 3R (Replace, Reduce, Refine) methodologies is adding complexity to in vivo study designs, potentially increasing per-study cost and timelines.

Market Opportunities

- Biologics and Advanced Modalities Pipeline: The FDA approved a record volume of biologics licenses in 2023-2024. Gene therapies, cell therapies, and mRNA vaccines require entirely new preclinical characterization paradigms. CROs developing specialized biosafety and immunotoxicology capabilities are positioned to capture premium pricing.

- Asia Pacific Market Expansion: India and China offer cost-effective capacity expansion for global pharmaceutical companies. Government-backed pharmaceutical parks in Hyderabad, Pune, and Chengdu are attracting incremental outsourcing contracts from North American and European drug developers.

- Digital Biomarker and Companion Diagnostic Development: The co-development of precision medicine diagnostics with new therapeutic candidates is creating adjacent preclinical testing demand for companion biomarker validation services.

Market Challenges

- Data Integrity and Regulatory Scrutiny: FDA Warning Letters related to GLP data integrity violations issued to CRO facilities in emerging markets have heightened client due diligence requirements and can result in costly repeat studies.

- Competitive Pricing Pressure: As the CRO market consolidates and overcapacity emerges in certain service lines, price compression is squeezing margins at mid-tier operators while benefiting large platforms such as Charles River Laboratories International, Inc. and Fortrea.

Emerging Market Trends

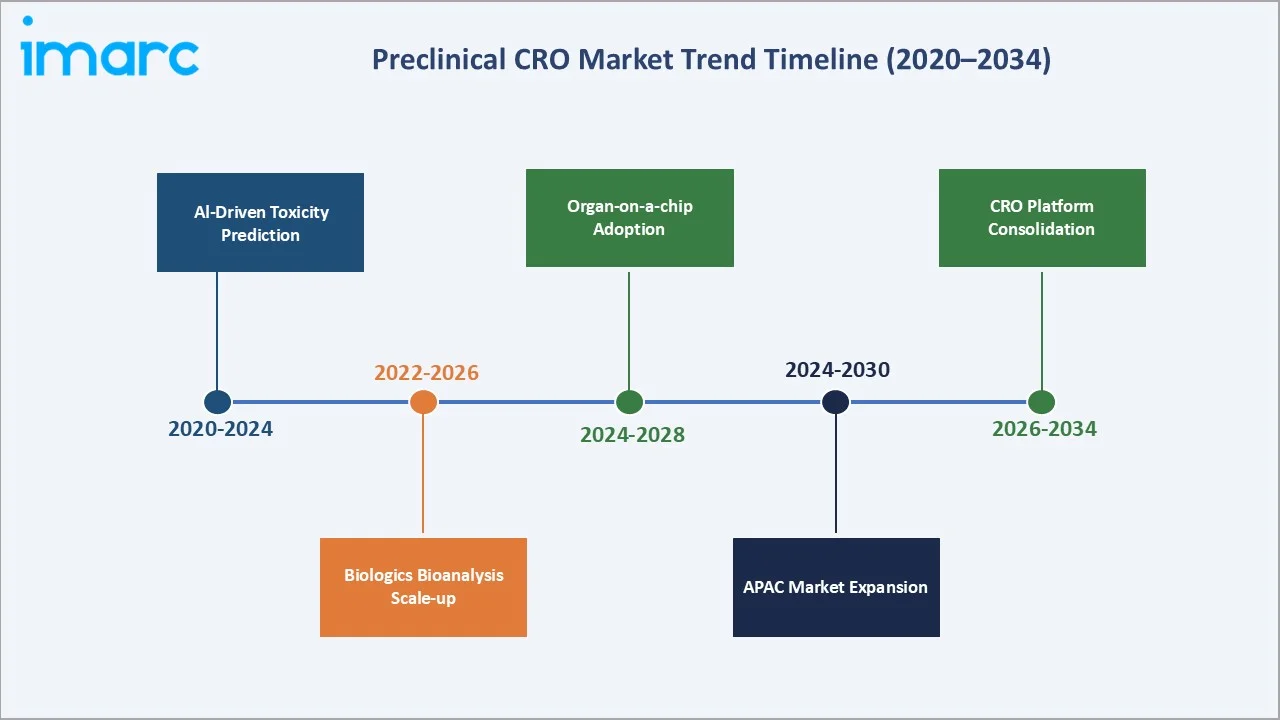

1. AI-Driven Predictive Toxicology Replacing Traditional Animal Testing Panels

Machine learning models trained on historical toxicology datasets are enabling CROs to provide in silico toxicity predictions with measurable accuracy. This trend aligns with the FDA 2023 guidance encouraging non-animal alternatives where scientifically justified. CROs embedding AI tools reduce per-study cost and can predict DILI risk before committing to costly in vivo studies.

2. Expansion of Bioanalytical Capabilities for Complex Biologics

Bioanalytical CROs are investing heavily in LC-MS/MS, immunogenicity testing, and cell-based assay platforms to support the characterization of mAbs, ADCs, bispecifics, and mRNA therapeutics at every preclinical stage.

3. Integration of Organ-on-a-Chip and 3D Culture Models

Microphysiological systems, referred to as organ-on-a-chip, replicate human tissue microenvironments with greater physiological fidelity than standard 2D cell cultures. Leading CROs, including Charles River Laboratories International, Inc. and Evotec, are partnering with organ-on-a-chip developers to offer human-relevant toxicity testing that reduces animal usage while providing translatable pharmacological data.

4. Geographic Diversification into the Asia Pacific and Latin America

Syngene International and Jubilant Pharmova Limited are capturing global outsourcing demand with GLP-accredited facilities. Brazil and Mexico are emerging as cost-effective alternatives for Latin American pharmaceutical companies seeking regulatory-compliant preclinical support.

5. Strategic Consolidation Reshaping the Competitive Landscape

The preclinical CRO sector is experiencing significant M&A activity as global CRO conglomerates acquire niche specialists to broaden service portfolios. WuXi AppTec's expansion, ICON's acquisition strategy, and Charles River Laboratories' targeted bolt-on purchases are reshaping the landscape, creating fully integrated preclinical-to-clinical service platforms.

Industry Value Chain Analysis

The preclinical CRO value chain spans five integrated stages from drug discovery through regulatory submission. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Drug Discovery & Target ID |

Pharma / Biotech companies, NIH-funded academic labs, spinouts |

|

Preclinical CRO Services |

Charles River Laboratories International, Inc., Fortrea, ICON plc, WuXi AppTec Co., Ltd. |

|

Bioanalysis & DMPK Testing |

Evotec, SGS SA, Pacific BioLabs |

|

Regulatory Package Preparation |

ICON plc, specialist GLP consultants |

|

End Users |

Biopharmaceutical companies, medical device firms, government bodies, and academic institutes |

Preclinical CRO services occupy the most critical strategic position in this value chain. CROs that offer vertically integrated services, from target-based toxicology screening through full GLP safety packages, command meaningful premiums over single-service providers. The value chain is increasingly characterized by strategic partnerships rather than transactional project engagements.

Technology Landscape in the Preclinical CRO Industry

AI and Machine Learning in Toxicity Prediction

Machine learning models combined with QSAR (quantitative structure-activity relationship) architectures trained on proprietary toxicology databases are enabling CROs to provide pre-screen safety assessments within hours rather than weeks. The FDA 2023 guidance on alternative methods signals regulatory acceptance of AI-based toxicity tools as complements to traditional in vivo testing.

High-Resolution Mass Spectrometry and Bioanalytical Platforms

High-resolution LC-MS/MS platforms now enable quantification of drug metabolites at sub-nanogram concentrations, critical for DMPK studies supporting first-in-human dosing decisions. Automation in GLP bioanalytical laboratories through robotic liquid-handling systems and LIMS-integrated workflows reduces human error and improves data traceability, directly addressing regulatory data integrity requirements.

Next-Generation In Vitro Models and 3D Biology

iPSC-derived hepatocytes, cardiomyocytes, and neural organoids provide human-relevant biological substrates for toxicity and efficacy profiling. These technologies represent a convergence of translational science and regulatory compliance, enabling CROs to generate more predictive preclinical data while simultaneously reducing animal study requirements in line with 3R principles.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service |

Toxicology Testing |

51.6% |

2025 |

|

End Use |

Biopharmaceutical Companies |

81.0% |

2025 |

|

Region |

North America |

47.5% |

2025 |

By Service

The preclinical CRO market segments by service into Toxicology Testing, Bioanalysis and DMPK Studies, and Others. Each segment reflects distinct regulatory requirements, client demand profiles, and technology investment patterns.

To access detailed market analysis, Request Sample

Toxicology Testing commands the largest share at 51.6% in 2025. This segment encompasses acute, subacute, subchronic, and chronic toxicity studies as well as genotoxicity and carcinogenicity assessments. Every drug candidate requires a GLP-compliant toxicology package before IND submission, making this service line structurally non-discretionary. The expanding biopharmaceutical pipeline, with over 6,000 drugs in active clinical development globally, sustains consistently high demand.

Bioanalysis and DMPK Studies represent 34.2% of the 2025 service mix and are growing above the blended market average. This acceleration is driven by the increasing complexity of new drug modalities. Biologics, ADCs, oligonucleotides, and gene therapies each require customized bioanalytical method development and metabolite identification strategies.

By End Use

The market segments by end use into Biopharmaceutical Companies, Government and Academic Institutes, and Medical Device Companies.

Biopharmaceutical Companies constitute the dominant end-use category at 81.0% in 2025. This concentration reflects the structural reality that drug development economics make in-house preclinical infrastructure uneconomical for the majority of biotechs.

Government and Academic Institutes account for 11.6% of 2025 revenue. NIH-funded translational science programmes and academic drug discovery centres represent a stable end-use base.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

47.5% |

Dense biopharmaceutical R&D cluster; FDA-mandated GLP preclinical packages; US contributes ~93.7% |

|

Europe |

24.3% |

EMA ICH guideline compliance; leading CRO infrastructure in the UK, Germany, and Switzerland |

|

Asia Pacific |

18.6% |

Fastest growing; China and India are driving cost-competitive outsourcing capacity expansion. |

|

Latin America |

5.8% |

Emerging CRO hub: Brazil and Mexico are building GLP-compliant laboratory infrastructure. |

|

Middle East & Africa |

3.8% |

Nascent market; government-backed pharmaceutical investment programmes |

North America dominates the global preclinical CRO market with a 47.5% revenue share in 2025, the largest of any region. The United States contributes approximately 93.7% of regional revenue, fuelled by the FDA's rigorous IND submission requirements and the chronic disease burden driving a high-value pharmaceutical pipeline. Major CRO campuses operated by Charles River Laboratories International, Inc. and Fortrea are concentrated in Massachusetts, New Jersey, and California.

Europe holds a 24.3% share in 2025, anchored by the UK, Germany, and Switzerland. The EMA's stringent requirements for non-clinical safety data packages under ICH S2-S9 guidelines drive substantial CRO expenditure. Evotec (Germany), SGS SA (Switzerland), and MRC (UK) represent established European CRO infrastructure with global reach.

Asia Pacific, at 18.6% of 2025 revenue, is the fastest-growing region with an estimated regional CAGR approaching 8.0%. India's preclinical CRO market was valued at USD 183.3 Million in 2023, expanding at 11.4% CAGR through 2030, driven by Syngene International, Jubilant Pharmova Limited, and international CRO subsidiaries. China's WuXi AppTec Co., Ltd. operates one of the world's largest GLP-certified preclinical testing platforms.

Latin America commands 5.8% of the 2025 market. Brazil, as the region's largest pharmaceutical market, is building GLP-accredited CRO capacity to support domestic biotechs and attract global outsourcing. The Middle East and Africa region holds 3.8%, with growth driven by government pharmaceutical investment programmes in the UAE and Saudi Arabia under national economic diversification strategies.

Competitive Landscape

|

Company Name |

Key Platform / Focus |

Market Position |

Core Strength |

|

Charles River Laboratories International, Inc. |

Safety Assessment, Discovery Services |

Leader |

Integrated discovery-to-preclinical platform; 100+ global sites |

|

Fortrea |

Clinical Development Services (Phase I–IV), Decentralized Trials, Patient Access Solutions |

Leader |

CRO) Strong global clinical trial execution; deep therapeutic expertise; agile, CRO-focused model post-spin-off |

|

ICON plc |

Preclinical-to-Phase III services |

Leader |

Scale from PRA merger; integrated study management |

|

WuXi AppTec Co., Ltd. |

GLP Tox, DMPK, Bioanalysis |

Challenger |

World-class GLP campus in Shanghai; cost-competitive |

|

Evotec SE |

Discovery alliances, rare disease |

Challenger |

European discovery-preclinical integration |

|

Syngene International Ltd |

GLP Tox, DMPK, Bioanalysis |

Emerging |

India-based GLP facility; 11.4% CAGR domestic market |

|

Jubilant Pharmova Limited |

Toxicology, Safety Pharmacology |

Emerging |

India CRO; growing global outsourcing contracts |

|

Pacific BioLabs |

Bioanalysis, DMPK |

Emerging |

US West Coast specialty DMPK and bioanalytical niche |

The global preclinical CRO market exhibits moderate-to-high concentration among the top platforms. Charles River Laboratories International, Inc., Fortrea, and ICON plc collectively account for a significant proportion of global revenue in 2025. The competitive landscape is characterized by a small number of global platforms commanding substantial OEM relationships, alongside mid-tier specialists competing across niche service lines and geographic markets.

Key Company Profiles

Charles River Laboratories International, Inc.

Charles River Laboratories is the global leader in preclinical CRO services, operating across 100+ sites worldwide. Its integrated platform spans early drug discovery, in vivo and in vitro safety assessment, GLP toxicology, bioanalysis, and manufacturing support.

- Product & Platform Portfolio: Safety Assessment, Discovery Services, Manufacturing Support

- Recent Developments: In January 2026, Charles River Laboratories International, Inc. announced the proposed acquisition of PathoQuest, a next-generation sequencing (NGS)-based biologics testing firm, to strengthen its biologics testing and alternative (non-animal) methods platform.

- Strategic Focus: Integration of AI-assisted toxicity prediction tools and organ-on-a-chip platforms to accelerate study timelines while reducing animal usage.

Fortrea

Fortrea is a leading pure-play clinical contract research organization (CRO) focused exclusively on clinical development services following its spin-off from Labcorp. The company operates across 90+ countries, supporting biopharma clients with end-to-end clinical trial execution from early-phase studies through post-marketing support, with strong capabilities in decentralized and hybrid trial models.

- Product & Platform Portfolio: Clinical Development (Phase I–IV), Clinical Pharmacology, Decentralized Clinical Trials (DCT), Patient Access & Recruitment, Real-World Evidence (RWE)

- Recent Developments: In April 2026, Fortrea unveiled Fortrea Intelligent Technology (FIT), an AI-powered suite designed to enhance clinical trial operations by automating workflows, improving data insights, and enabling faster, more efficient trial execution across global studies.

- Strategic Focus: Strengthening its position as a standalone CRO by investing in technology-enabled clinical trials, including AI-driven study design, remote monitoring solutions, and data analytics platforms, while deepening therapeutic expertise in oncology, rare diseases, and complex biologics.

WuXi AppTec Co., Ltd.

WuXi AppTec Co., Ltd. operates one of the world's largest GLP-certified preclinical testing campuses in Shanghai, offering cost-competitive toxicology and DMPK services that attract global biotech and pharma clients seeking Asia-based study execution.

- Product & Platform Portfolio: GLP Toxicology, DMPK, Bioanalysis, Chemistry Services

- Recent Developments: In December 2024, WuXi AppTec announced the sale of its Advanced Therapies (cell & gene therapy) unit to a U.S. private equity firm amid regulatory pressures, signaling portfolio restructuring.

- Strategic Focus: Positioning as the preferred preclinical partner for global biotech companies seeking cost-efficient, high-quality GLP studies executed in Asia-Pacific.

Market Concentration Analysis

The global preclinical CRO market exhibits moderate-to-high concentration among the top Tier-1 CRO platforms. Charles River Laboratories International, Inc., Fortrea, and ICON plc collectively account for approximately 30-40% of global preclinical CRO revenue in 2025.

The market is experiencing a bifurcated structural dynamic. At the premium end, consolidation is occurring as complex integrated preclinical services require massive R&D investment that only the largest CROs can sustain. Simultaneously, the Asia Pacific market is generating new challengers, with Indian and Chinese CROs demonstrating technical competitiveness at significantly lower price points.

Investment & Growth Opportunities

Fastest-Growing Segments

Bioanalysis and DMPK Studies are the highest-growth service segment at approximately 7.1% CAGR through 2034. The deployment of advanced LC-MS/MS platforms and immunogenicity testing capabilities for biologics is transforming this segment from a commodity service to a high-value, specialized offering. Biopharmaceutical end-use is growing at 6.5% CAGR, driven by the sustained expansion of the global biologics pipeline.

Emerging Market Expansion

Asia Pacific represents the highest-potential geographic growth opportunity. The combination of cost-competitive infrastructure, improving GLP regulatory compliance, and strong government support for pharmaceutical manufacturing creates a compelling growth case.

Technology Investment Trends

AI-integrated drug discovery platforms represent the most significant near-term investment opportunity within the CRO sector. CROs embedding machine-learning tools for toxicity prediction and DMPK modelling are achieving measurable reductions in study turnaround time and per-compound testing cost. Strategic partnerships with organ-on-a-chip and microphysiological system developers are also attracting venture investment.

Future Market Outlook (2026-2034)

The global preclinical CRO market forecast projects steady value expansion from USD 6.82 Billion in 2025 to USD 12.03 Billion by 2034 at a CAGR of 6.28%, a near-doubling of market value underpinned by expanded biopharmaceutical outsourcing, advanced modality adoption, and geographic capacity expansion in the Asia Pacific through the forecast period.

Three structural dynamics are most likely to reshape the preclinical CRO market through 2034. AI integration will progressively reduce the cost of in silico screening, shifting preclinical CRO value from commodity assay execution to data interpretation and regulatory strategy. Biologics and advanced therapy medicinal products (ATMPs) will constitute a growing share of drug pipelines, demanding specialized bioanalytical and immunogenicity capabilities.

By 2034, the preclinical CRO industry is forecast to have completed its transition from a primarily fee-for-service model to a platform-based partnership model where CROs co-invest in drug development programmes in exchange for milestone and royalty-based revenue sharing, fundamentally altering the competitive landscape.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with preclinical CRO industry stakeholders, including study directors at Tier-1 CRO platforms, pharmaceutical R&D outsourcing leads, biotech CMC directors, regulatory affairs consultants, and institutional investors in life science services. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include U.S. FDA Drug Approvals Database, EMA EPAR database, NCATS Translational Research publications, NIH Research Portfolio Online Reporting Tools, IQVIA pharmaceutical R&D pipeline data, company annual reports, and trade publications, including CRO Forum reports, Drug Discovery Today, and Pharmaceutical Technology journals.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating pharmaceutical R&D expenditure growth rates, drug pipeline conversion rates, outsourcing adoption indices, and historical CRO market evolution patterns. Scenario analysis was performed to account for macroeconomic uncertainty and regulatory environment variations.

Preclinical CRO Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Services Covered | Bioanalysis and DMPK Studies, Toxicology Testing, Others |

| End Uses Covered | Biopharmaceutical Companies, Government and Academic Institutes, Medical Device Companies |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Charles River Laboratories International, Inc., Fortrea, ICON plc, WuXi AppTec Co., Ltd., Evotec SE, Syngene International Ltd, Jubilant Pharmova Limited, Pacific BioLabs, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the preclinical CRO market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global preclinical CRO market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the preclinical CRO industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Preclinical CRO Market Report

The global preclinical CRO market was valued at USD 6.82 Billion in 2025, driven by rising pharmaceutical R&D expenditure and growing biopharmaceutical outsourcing demand.

The market is projected to reach USD 12.03 Billion by 2034 growing at a CAGR of 6.28% during 2026 to 2034, driven by biopharmaceutical outsourcing, advanced modality pipeline growth, and Asia Pacific expansion.

Toxicology Testing leads with a 51.6% share in 2025, driven by mandatory GLP safety study requirements for every new drug candidate before IND filing.

Biopharmaceutical Companies lead with an 81.0% share in 2025, reflecting their deep structural dependence on CRO partnerships due to the cost-prohibitive nature of maintaining in-house preclinical infrastructure.

North America leads with a 47.5% share in 2025, driven by FDA-regulated drug pipeline density, high per-capita pharmaceutical R&D investment, and established CRO infrastructure in the United States.

Key drivers include rising pharmaceutical R&D expenditure exceeding USD 250 Billion in 2024, complex regulatory requirements mandating GLP preclinical packages, escalating chronic disease burden sustaining drug pipelines, and AI-driven technological advancements accelerating CRO capabilities.

Bioanalysis and DMPK Studies are the fastest-growing service segment, driven by the increasing complexity of biologics and advanced modalities requiring sophisticated pharmacokinetic profiling and metabolite identification.

Leading companies include Charles River Laboratories International, Inc., Fortrea, ICON plc, WuXi AppTec Co., Ltd., Evotec SE, Syngene International Ltd, Jubilant Pharmova Limited, and Pacific BioLabs.

AI-driven predictive toxicology platforms are enabling CROs to provide in silico safety assessments within hours, reducing animal study requirements and per-compound testing costs. The FDA 2023 guidance on alternative testing methods further accelerates AI adoption across the preclinical CRO industry.

Good Laboratory Practice (GLP) compliance is a mandatory requirement for all regulatory-grade preclinical safety studies. GLP certification differentiates credible CROs and provides pharmaceutical clients with assurance of data integrity, reproducibility, and regulatory acceptability across FDA, EMA, and ICH guideline requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)