Diaper Market Size, Share, Trends and Forecast by Product Type, Product Type, Distribution Channel, and Region, 2026-2034

Global Diaper Market Size, Share, Trends & Forecast (2026-2034)

The global diaper market reached a value of USD 97.2 Billion in 2025 and is projected to reach USD 168.5 Billion by 2034, exhibiting a CAGR of 6.30% during the forecast period (2026-2034). Growth is driven by rising birth rates in developing nations, an aging global population fueling adult incontinence product demand, increasing hygiene awareness, and rapid e-commerce penetration. Asia Pacific dominates with a 35.4% revenue share in 2025, underpinned by large infant populations in China, India, and Southeast Asia. The market is expected to reach USD 131.93 Billion by 2030. Key players include Procter & Gamble (Pampers), Kimberly-Clark (Huggies), Unicharm, Essity (TENA), and Ontex Group.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 97.2 Billion |

|

Market Size (2030) |

USD 131.93 Billion |

|

Forecast Market Size (2034) |

USD 168.5 Billion |

|

CAGR (2026-2034) |

6.30% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (35.4%, 2025) |

|

Fastest Growing Region |

Asia Pacific |

The market's growth from USD 71.6 Billion in 2020 to USD 97.2 Billion in 2025 reflects a robust historical CAGR of approximately 6.3%, a pace sustained through the forecast period, representing an incremental value addition of USD 71.3 Billion by 2034.

Figure 1: Global Diaper Market Growth Trend (2020–2034)

The 6.30% CAGR over 2026–2034 positions the diaper market among the faster-growing consumer goods categories globally. Biodegradable and eco-friendly product innovation, combined with e-commerce accessibility, is accelerating market penetration particularly in underserved rural and emerging-market geographies.

Figure 2: CAGR Comparison – Diaper Market Segments (2026–2034)

Executive Summary

The global diaper market stood at USD 97.2 Billion in 2025, sustained by the interplay of demographic expansion, rising hygiene consciousness, and product innovation across both the baby and adult segments. The market is projected to reach USD 168.5 Billion by 2034 at a CAGR of 6.30%, reflecting broad structural demand resilience. Asia Pacific leads with a 35.4% revenue share, driven by large infant populations, increasing disposable incomes, and growing urban middle-class adoption of premium baby care products.

Key growth catalysts include rising birth rates in developing markets, a rapidly expanding elderly population globally requiring adult incontinence products, and the surge in e-commerce and subscription-based diaper services. In February 2025, Ontex Group launched its Dreamshields technology for baby diapers in Europe, enhancing leakage protection and sustainability by reducing CO2 emissions and plastic use. This underscores the market's accelerating trajectory toward eco-friendly and high-performance product formats.

By distribution channel, pharmacies lead at 44.7% (2025), followed by supermarkets and hypermarkets (26.3%), online stores (16.7%), and convenience stores (10.6%). North America (23.7%) and Europe (22.3%) complete the regional picture. Investment in biodegradable materials, smart diaper technology, and direct-to-consumer subscription models are the critical themes shaping competitive positioning through 2034.

Key Market Insights

|

Insight |

Data |

|

Market Size (2025) |

USD 97.2 Billion |

|

Market Size (2030) |

USD 131.93 Billion |

|

Market Forecast (2034) |

USD 168.5 Billion |

|

CAGR (2026–2034) |

6.30% |

|

Largest Adult Diaper Segment |

Pad Type – 52.5% (2025) |

|

Leading Distribution Channel |

Pharmacies – 44.7% (2025) |

|

Fastest Growing Channel |

Online Stores (2026–2034) |

|

Leading Region |

Asia Pacific – 35.4% (2025) |

|

Top Companies |

P&G (Pampers), Kimberly-Clark, Unicharm, Essity, Ontex |

|

Key Market Opportunity |

Adult incontinence segment – fastest growing product category |

Key analytical observations supporting the above data points:

- Asia Pacific's 35.4% share (2025) is driven by high birth rates in India and Southeast Asia, a large infant base in China, and accelerating penetration of premium disposable diapers over traditional cloth alternatives.

- Pad type leads adult diapers at 52.5% (2025), favored for its discreet form factor and suitability for light to moderate incontinence, while pant type (25.5%) is gaining ground for active elderly users valuing comfort.

- Pharmacies dominate distribution at 44.7% (2025), but online stores (16.7%) are the fastest-growing channel, driven by subscription services, competitive pricing, and home delivery convenience.

- The adult incontinence segment is the fastest-growing product category, supported by global aging demographics, the U.S. population aged 65+ is projected to rise from 58 million (2022) to 82 million by 2050 (Population Reference Bureau, 2024).

- Biodegradable and eco-friendly diapers represent a high-growth niche, with brands including Ontex, Bambo Nature, and Seventh Generation accelerating sustainable product launches across European and North American markets.

- E-commerce penetration is reshaping the competitive landscape, with online platforms offering subscription models, bulk discounts, and algorithm-driven replenishment alerts that increase purchase frequency and brand loyalty.

Global Diaper Market Overview

The diaper market encompasses disposable and reusable absorbent hygiene products designed for infants, toddlers, and adults with incontinence conditions. The global ecosystem spans raw material suppliers (pulp, superabsorbent polymers, polypropylene), component manufacturers, branded diaper producers, distributors, and retail channels. As of 2025, the market is valued at USD 97.2 Billion and serves billions of consumers across all income segments globally. Macroeconomic drivers including urbanization, rising per capita incomes in developing markets, and aging demographics in developed economies are creating parallel growth trajectories across both the baby and adult product categories. UNICEF projects the number of children in urban areas will rise significantly, with 60% of children globally expected to reside in urban settings by 2050, directly expanding the addressable diaper market.

Figure 3: Diaper Industry Value Chain

Market Dynamics

Figure 4: Diaper Market Drivers & Restraints – Impact Analysis (2025)

Market Drivers

- Rising Birth Rates and Urbanization: Increasing birth rates in developing markets, particularly across Africa, South Asia, and Southeast Asia, are directly expanding the infant diaper consumer base. UNICEF data projects 60% of children globally will reside in urban areas by 2050, where disposable diaper adoption rates are significantly higher than rural areas.

- Aging Global Population - Adult Incontinence Growth: The global population aged 65+ is expanding rapidly. In the U.S. alone, the elderly population is projected to rise from 58 million in 2022 to 82 million by 2050. This demographic shift is creating sustained demand for adult incontinence diapers, pads, and pant-type products.

- E-commerce and Subscription Model Expansion: Online diaper sales are growing at an estimated CAGR of 8-9%, driven by platforms offering subscription-based replenishment, bulk pricing, and home delivery. E-commerce platforms such as Amazon, Flipkart, and Lazada are significantly lowering purchase friction across all consumer segments.

- Product Innovation and Premiumization: Ontex Group's February 2025 launch of Dreamshields technology for baby diapers, featuring enhanced leakage protection, reduced CO2 emissions, and lower plastic content exemplifies the market's trajectory toward high-performance, eco-responsible product formats that command premium price points.

Market Restraints

- Environmental and Sustainability Concerns: Traditional disposable diapers contribute approximately 3.5 million tons of waste annually to global landfills. Growing regulatory pressure and consumer environmental awareness are creating cost and reformulation headwinds for conventional diaper manufacturers.

- Raw Material Price Volatility: Fluctuations in pulp, superabsorbent polymer (SAP), and polypropylene prices, key diaper inputs, directly impact production costs and margin structures. SAP prices have experienced significant volatility of prices of year-on-year in recent periods.

- Low Penetration in Rural Markets: Despite strong urban demand, rural penetration in Sub-Saharan Africa, South Asia, and parts of Latin America remains limited due to affordability barriers and cultural preferences for traditional cloth alternatives.

Market Opportunities

- Biodegradable and Eco-Friendly Diapers: The global sustainable baby care market is expanding rapidly, with consumers in Europe and North America willing to significantly high price premiums for certified eco-friendly diapers. Brands investing in plant-based materials, compostable structures, and reduced plastic content are well-positioned.

- Emerging Market Expansion: Asia Pacific, Africa, and Latin America represent substantial untapped potential. India's diaper market is growing at approximately 6.3% annually, driven by rising middle-class incomes and government hygiene awareness programs.

- Smart Diaper Technology: IoT-enabled diapers with wetness sensors and connected health monitoring capabilities are in commercial pilot phases. These products address parent convenience and healthcare provider needs, particularly in neonatal care and elderly care settings, unlocking premium segment revenue.

Market Challenges

- Regulatory Compliance Complexity: Evolving chemical safety regulations governing diaper materials including restrictions on formaldehyde, phthalates, and certain fragrances, across the EU and North America require continuous product reformulation and compliance investment.

- Intense Price Competition: Market saturation in developed markets has intensified price competition, particularly in the mid-tier baby diaper segment. Private-label retailers gaining share in supermarkets are compressing margins for branded manufacturers.

- Supply Chain Vulnerabilities: Geopolitical disruptions and logistics bottlenecks affecting SAP and pulp supply chains, materials sourced primarily from Asia and South America, create production continuity risks for global diaper manufacturers.

Emerging Market Trends

The global diaper market is being reshaped by five converging trends that are redefining product innovation, distribution strategies, and competitive positioning across both the baby and adult segments.

Figure 5: Diaper Market Trend Timeline (2020–2034)

1. Biodegradable and Sustainable Diaper Adoption

Consumer demand for eco-friendly diapers made from plant-based materials, organic cotton, and biodegradable superabsorbent polymers is accelerating. European markets are leading adoption, with regulatory frameworks incentivizing low-plastic and compostable product development. Brands including Bambo Nature, Dyper, and Ontex are scaling sustainable lines, with this segment projected to grow at over more than 10% CAGR through 2034.

2. Smart Diaper Technology and Connected Health

IoT-enabled diapers incorporating moisture sensors, temperature monitoring, and wireless connectivity to parent smartphones are transitioning from pilot to commercial deployment. Manufacturers including P&G and start-ups such as Pampers Smart Diapers are targeting the premium segment and neonatal healthcare market, representing a high-margin growth avenue.

3. E-commerce and Subscription-Based Distribution

Online stores are the fastest-growing distribution channel. Subscription-based replenishment models, pioneered by platforms including Amazon Subscribe & Save, are driving brand loyalty, increasing basket sizes, and reducing consumer switching behavior across both baby and adult product categories.

4. Adult Incontinence Market Surge

The adult diaper segment is growing faster than the baby segment, driven by rapid aging demographics in Japan, Germany, the U.S., and China. Pant-type adult diapers are gaining consumer acceptance as discreet, comfortable, everyday-wear products, with Essity (TENA) and Unicharm investing heavily in product design improvements targeting active elderly lifestyles.

5. Premiumization and Skin-Health-Focused Products

Parents and caregivers are increasingly prioritizing skin-friendly, hypoallergenic, and fragrance-free diaper formulations. Estimated spending on premium baby care products and raising a baby in India for children aged 0–3 has reached between 1 lakh to 3 lakh, reflecting the willingness to invest in superior product quality. Brands offering dermatologist-tested, organic-certified options are capturing disproportionate share in high-income markets.

Industry Value Chain Analysis

The diaper industry value chain spans seven interconnected stages from raw material sourcing to end-consumer delivery. Each stage contributes distinct value and involves specialized operators whose efficiency directly influences product quality, safety compliance, and cost competitiveness.

|

Stage |

Key Activities |

Representative Players |

|

Raw Material Procurement |

Pulp fiber, SAP (superabsorbent polymer), polypropylene, elastics |

Weyerhaeuser, Nippon Shokubai, ExxonMobil, Braskem |

|

Component Manufacturing |

Absorbent core production, elastic components, back sheet films |

Fitesa, PGI (Berry Global), Avgol Nonwovens |

|

Diaper Manufacturing |

Diaper assembly, quality control, product differentiation |

P&G, Kimberly-Clark, Unicharm, Essity, Ontex Group |

|

Quality & Regulatory Testing |

Absorbency, skin safety, chemical compliance testing |

SGS, Intertek, Bureau Veritas |

|

Distribution & Logistics |

Warehousing, 3PL logistics, cold-chain (medical diapers) |

DHL, XPO Logistics, Kuehne+Nagel, DB Schenker |

|

Retail Channels |

Supermarkets, pharmacies, online platforms, convenience stores |

Walmart, CVS, Amazon, Carrefour, Flipkart |

|

End Consumers |

Infants, toddlers, elderly adults, medical facilities |

Households, hospitals, nursing homes, care facilities |

The SAP and pulp raw material stages are the most critical cost drivers, collectively accounting for approximately 40–75% of total diaper production costs. Technology disruptions in bio-based SAP synthesis and recycled-fiber pulp sourcing are creating new cost reduction pathways for leading manufacturers investing in sustainable supply chain transformation.

Technology Landscape in the Diaper Industry

Advanced Absorbent Materials

Superabsorbent polymer technology continues to evolve, with next-generation SAP formulations offering higher absorption capacity at lower gram weights, enabling thinner and lighter diaper constructions. Bio-based SAP derived from renewable agricultural feedstocks is in advanced development, with commercial launches expected by 2027 from suppliers including Nippon Shokubai and BASF.

Smart and Connected Diaper Technology

IoT-integrated diapers embedding wetness sensors, temperature monitors, and Bluetooth connectivity are entering the premium commercial market. P&G's Pampers Smart Diapers, developed in collaboration with Lumi by Pampers, exemplify this trend. Healthcare applications in neonatal intensive care and elderly nursing facilities represent the highest near-term commercial potential for smart diaper technology.

Sustainable Material Innovation

Plant-based nonwoven fabrics, compostable back-sheet films, and reduced-plastic outer cover technologies are being adopted by brands across Europe and North America. Dyper and Bambo Nature have achieved third-party compostability certifications, while P&G and Kimberly-Clark have committed to reducing virgin plastic in diaper products by 50% by 2030.

Automated Manufacturing and Industry 4.0

High-speed automated diaper production lines operating at over 1,000 units per minute are now standard in large-scale facilities. AI-driven quality control systems using computer vision are reducing defect rates and material waste. Manufacturers investing in smart factory infrastructure are achieving significant production cost reductions versus legacy manual processes.

Market Segmentation Analysis

By Product Type - Adult Diaper

The adult diaper segment is segmented into three primary product formats, each serving distinct user needs and incontinence severity levels:

The pant type segment’s 25.5% share (2025) reflects the significant consumer preference shift among elderly users toward discreet, underwear-like incontinence products that support independence and active daily living. This segment is expected to grow its share within the forecast period.

Figure 6: Adult Diaper Market Share by Product Type (2025)

By Product Type - Baby Diaper

The baby diaper segment is dominated by disposable diapers, which account for approximately 61.6% of baby diaper revenues in 2025. Training diapers, cloth diapers, biodegradable diapers, and swim pants complete the product landscape.

The biodegradable diaper sub-segment (10.8%, 2025) is the fastest-growing baby diaper format. Regulatory incentives in the EU and increasing consumer willingness to pay sustainability premiums in North America and Oceania are primary demand catalysts.

Figure 7: Baby Diaper Market Share by Product Type (2025)

By Distribution Channel

Pharmacies remain the dominant channel at 44.7% (2025), offering trusted healthcare positioning and professional product guidance. Online stores at 16.7% represent the fastest-growing channel, fundamentally reshaping how consumers discover, compare, and replenish diaper products.

The online channel’s 16.7% share (2025) is projected to grow steadily as subscription-based diaper services and algorithm-driven replenishment become mainstream consumer behavior across both developed and emerging markets.

Figure 8: Diaper Market Share by Distribution Channel (2025)

Regional Market Insights

The global diaper market exhibits significant regional variation in growth rates, product preferences, and competitive dynamics. Asia Pacific leads in revenue share, while North America and Europe represent the highest premium product penetration markets.

|

Region |

Share (2025) |

Key Growth Drivers |

Notable Players |

|

Asia Pacific |

35.4% |

High birth rates (India, Indonesia), urbanization, rising incomes, aging Japan |

Unicharm, P&G, Kimberly-Clark, Kao Corporation |

|

North America |

23.7% |

Aging population (adult diapers), premium baby care, e-commerce growth |

P&G (Pampers), Kimberly-Clark (Huggies), Drylock |

|

Europe |

22.3% |

Sustainability mandates, biodegradable product adoption, aging demographics |

Essity (TENA), Ontex, Hartmann, Paul Hartmann AG |

|

Middle East & Africa |

10.4% |

Young population, rising birth rates, improving retail infrastructure |

P&G, Kimberly-Clark, Hayat Kimya, Nobel Hygiene |

|

Latin America |

8.2% |

Rising middle class, birth rates, informal market formalization |

P&G, Kimberly-Clark, Hypermarcas, Softys |

Asia Pacific's 35.4% dominance (2025) reflects the region's position as the world's largest infant consumer base. India alone is expected to become the world's most populous nation, with its diaper market growing at approximately 13% CAGR through 2034. Japan, conversely, represents the world's largest adult incontinence market, where Unicharm and Kao compete fiercely in a premium segment. Europe's 22.3% share is shaped by stringent sustainability regulations and high consumer receptiveness to certified eco-friendly products.

Figure 9: Regional Diaper Market Share Distribution (2025)

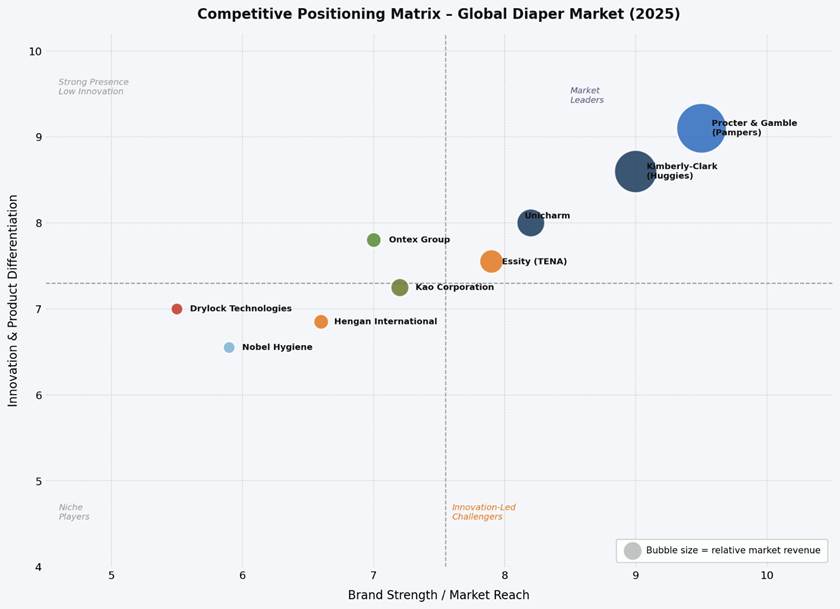

Competitive Landscape

The global diaper market is moderately concentrated at the top end, with Procter & Gamble (Pampers) and Kimberly-Clark (Huggies) collectively commanding more than 35–40% of global baby diaper revenues. The adult incontinence sub-segment is led by Essity (TENA) and Unicharm, with growing competition from European specialists including Ontex and Paul Hartmann.

|

Company Name |

Key Brand(s) |

Market Position |

Primary Strategy |

|

Procter & Gamble |

Pampers, Luvs |

Market Leader – Baby Diapers |

Digital innovation, smart diapers, sustainable product lines |

|

Kimberly-Clark |

Huggies, Pull-Ups, Depend |

Leader – Baby & Adult |

Premium positioning, eco-innovation, emerging market expansion |

|

Unicharm Corporation |

MamyPoko, Lifree |

Leader – Asia Pacific |

Asia-first expansion, adult incontinence growth, cost leadership |

|

Essity AB |

TENA, Libero |

Leader – Adult Incontinence |

Healthcare channel dominance, elderly care market growth |

|

Ontex Group |

Ontex, Dreamshields |

Challenger – Eco Segment |

Sustainability tech (Dreamshields 2025), European market focus |

|

Kao Corporation |

Merries, Laurier |

Challenger – Premium Baby |

Ultra-premium positioning, Japan-first, skin-care technology |

|

Hengan International |

Anerle |

Challenger – China |

Domestic China market leadership, value segment dominance |

|

Nobel Hygiene |

Friends Adult Diapers |

Emerging – India/MEA |

Fast-growing India adult market, affordable positioning |

|

Drylock Technologies |

Private Label Manufacturing |

B2B Private Label |

Retailer private label supply, European contract manufacturing |

Competitive differentiation in the diaper market is increasingly driven by sustainability credentials, smart product technology investment, and speed of penetration into high-growth emerging markets. P&G's Pampers and Kimberly-Clark's Huggies maintain global leadership through brand equity, innovation investment, and extensive distribution infrastructure.

Figure 10: Competitive Positioning Matrix – Global Diaper Market (2025)

Key Company Profiles

Procter & Gamble (Pampers)

P&G is the global market leader in baby diapers through its Pampers brand, with a presence across 100+ countries and estimated diaper segment revenues exceeding USD 10 Billion annually. Pampers commands more than 30% global baby diaper market share.

- Product Portfolio: Pampers Swaddlers, Pampers Baby-Dry, Pampers Pure Protection (eco-line), Pampers Easy Ups (training), Luvs (value), Pampers Splashers (swim).

- Recent Developments: Pampers launched Pampers AMORE™ in 2026, Pampers’ most premium and most absorbent1 diaper yet! Pampers AMORE has been designed for parents who seek superior comfort for their little ones without any compromise whatsoever.

- Strategic Focus: Digital and smart product innovation, sustainability commitments (30% plastic reduction by 2030), premium segment expansion, and e-commerce subscription growth.

Kimberly-Clark (Huggies)

Kimberly-Clark operates the Huggies, Depend, and Pull-Ups brands across the baby and adult categories, generating approximately USD 7.0 Billion in diaper-related revenues annually.

- Product Portfolio: Huggies Special Delivery (premium), Huggies Natural Care, Pull-Ups training pants, Depend (adult), GoodNites (youth bedwetting).

- Recent Developments: Expanded Huggies Special Delivery natural/organic line; launched biodegradable packaging initiatives across North America in 2024.

- Strategic Focus: Premium baby and adult care expansion, sustainability packaging transition, e-commerce channel investment, and Asia Pacific market penetration.

Unicharm Corporation

Unicharm is the dominant diaper brand in Asia, particularly Japan, Southeast Asia, China, and India, with its MamyPoko brand among the most recognized baby diaper brands in the region. Global revenues exceeded USD 6 Billion in fiscal 2025.

- Product Portfolio: MamyPoko Pants, MamyPoko Standard, Lifree (adult incontinence), Sofy (feminine hygiene).

- Recent Developments: Accelerated MamyPoko premium tier expansion in India and Indonesia in 2023–2024; invested in biodegradable material research through Japanese government-funded R&D programs.

- Strategic Focus: Asian market dominance, adult incontinence segment growth (Lifree), sustainable product innovation, and premium product mix improvement.

Essity AB (TENA)

Essity is the global leader in adult incontinence through its TENA brand and has been generating significant revenue. TENA is the #1 incontinence brand globally.

- Product Portfolio: TENA Pants, TENA Pads, TENA Slip (flat/tape style), TENA Flex (adult), Libero (baby, Europe).

- Recent Developments: Launched TENA Discreet Comfort with 50% less plastic in 2024; expanded hospital and care home supply partnerships across MEA.

- Strategic Focus: Adult incontinence leadership, healthcare channel deepening, sustainability-led product reformulation, and emerging-market adult care segment entry.

Ontex Group

Ontex is a leading European diaper manufacturer focused on private-label production and branded eco-products, generating approximately EUR 2.4 Billion in revenues in 2023.

- Product Portfolio: Dreamshields baby diapers (2025 launch), Lille Healthcare (adult), private-label diaper manufacturing for major European retailers.

- Recent Developments: Launched Dreamshields technology (February 2025) reducing CO2 and plastic use while improving leakage protection; strategic focus shift toward sustainability-led brand differentiation.

- Strategic Focus: Eco-product technology leadership, European market expansion, private-label retail supply, and adult healthcare segment growth.

Market Concentration Analysis

The global diaper market is moderately concentrated at the premium end, with Procter & Gamble, Kimberly-Clark, and Unicharm collectively commanding approximately 55–60% of global baby diaper revenues in 2025. The adult incontinence sub-segment is more fragmented, with Essity, Unicharm, and Kimberly-Clark (Depend) holding leading positions alongside strong regional players.

The private-label diaper segment is growing rapidly, with retailers including Walmart, Aldi, Lidl, and Amazon Basics capturing 18–22% of combined baby and adult diaper revenues in developed markets by 2025. This private-label expansion is compressing branded manufacturers' pricing power in the value and mid-tier segments, accelerating investment in premium and eco-differentiated product lines.

Consolidation trends include Ontex's portfolio rationalization toward higher margin branded eco-products, Essity's healthcare channel deepening through targeted M&A, and Unicharm's continued Asia Pacific market roll-up through joint ventures and minority stakes in regional diaper manufacturers. The market is expected to see 8-12 significant M&A or JV transactions annually through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

The adult incontinence segment (CAGR approximately 7–9%), biodegradable and eco-friendly baby diapers (CAGR above 12%), and online/subscription distribution represent the highest-growth investment vectors through 2034.

Emerging Market Expansion

India's diaper market is projected to grow at approximately 13% CAGR through 2034, driven by the world's largest birth cohort, rising middle-class incomes, and government hygiene awareness programs. Sub-Saharan Africa represents an incremental opportunity in this segment. Entry via local manufacturing partnerships, affordable product tiers, and government health program supply contracts are preferred strategies.

Technology and Innovation Investment Trends

- Smart diaper technology (IoT sensors, connected health monitoring) represents a premium-segment opportunity with applications in neonatal care, pediatric healthcare, and elderly nursing homes.

- Bio-based and compostable diaper material start-ups are attracting significant VC and corporate venture investment, with BASF, Nippon Shokubai, and TotalEnergies investing in next-generation SAP alternatives.

- Subscription-based e-commerce platforms including Dyper, Hello Bello, and The Honest Company are capturing millennial and Gen-Z parent segments with direct-to-consumer models combining sustainability credentials and personalized service.

- Diaper recycling infrastructure investment is gaining traction in the Netherlands, Japan, and the U.K., with pilot programs demonstrating commercial viability, creating circular economy opportunity for established manufacturers.

Future Market Outlook (2026-2034)

The global diaper market is positioned for sustained, above-average consumer goods growth through 2034, driven by demographic inevitability, infant populations in emerging markets and elderly populations in developed economies collectively ensure structural demand resilience. From USD 97.2 Billion in 2025, the market is forecast to reach USD 168.5 Billion by 2034, passing USD 131.93 Billion in 2030, an absolute value addition of USD 71.3 Billion across the forecast decade.

Product innovation will be the primary competitive battleground. Brands investing in smart diaper technology, biodegradable materials, and subscription-based distribution models will capture disproportionate share of the incremental market value. The bifurcation between value and premium segments will intensify, private-label players will dominate price-sensitive emerging markets while branded manufacturers retreat to higher-margin premium, eco, and smart-product tiers.

By 2034, the adult incontinence segment is projected to represent over 35% of global diaper revenues, surpassing the baby diaper segment in growth rate if not absolute value. Manufacturers that achieve scale in both segments, leveraging shared distribution, retail relationships, and manufacturing infrastructure will have decisive competitive advantages in the next decade's competitive landscape.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 180 industry participants in 2024–2025, comprising diaper brand executives, retail buyers, healthcare procurement managers, pediatricians, geriatricians, and end consumers across North America, Europe, Asia Pacific, and MEA.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, UNICEF demographic data, Population Reference Bureau statistics, trade publications (Nonwovens Industry, Baby Care International), and industry databases (Euromonitor, Mintel, IRI). Over 350 secondary sources were reviewed and triangulated for data validation.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up and top-down forecasting models, incorporating birth rate projections, aging demographic indices, disposable income growth data, e-commerce penetration rates, and historical market evolution patterns. Scenario analysis across base, optimistic, and conservative cases accounts for macroeconomic uncertainty over the 2026–2034 forecast horizon.

Diaper Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Billion Units |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types (Baby Diaper) Covered | Disposable Diapers, Training Diapers, Cloth Diapers, Swim Pants, Biodegradable Diapers |

| Product Types (Adult Diapers) Covered |

Pad Type, Flat Type, Pant Type |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Pharmacies, Convenience Stores, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Procter & Gamble, Kimberly-Clark, Unicharm Corporation, Essity AB, Ontex Group, Kao Corporation, Hengan International, Nobel Hygiene, Drylock Technologies, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the diaper market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global diaper market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the diaper industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global diaper market was valued at USD 97.2 Billion in 2025 and is projected to reach USD 168.5 Billion by 2034.

The market is forecast to grow at a CAGR of 6.30% during 2026-2034, driven by rising birth rates, aging demographics, product innovation, and e-commerce expansion.

Asia Pacific is the leading region, holding a 35.4% market share in 2025. High birth rates in India and Southeast Asia, combined with Japan's large adult incontinence market, drive the region's dominance.

Asia Pacific is also the fastest-growing region with an estimated CAGR of approximately 7.5%, led by India's rapidly expanding middle class and government hygiene awareness initiatives.

Key drivers include rising birth rates in developing markets, an aging global population increasing adult incontinence demand, e-commerce growth, product premiumization, and increasing hygiene awareness.

Pad type leads the adult diaper market with a 52.5% share in 2025, favored for its discreet design suitable for light to moderate incontinence in both home and institutional settings.

Key trends include biodegradable diaper adoption, smart IoT-connected diaper technology, e-commerce subscription growth, adult incontinence product surge, and premiumization in skin-health-focused formulations.

Leading companies include Procter & Gamble (Pampers), Kimberly-Clark (Huggies), Unicharm (MamyPoko), Essity (TENA), Ontex Group, Kao Corporation, Hengan International, Nobel Hygiene, and Drylock technologies.

Pharmacies are the largest channel at 44.7% (2025), though online stores (16.7%) are the fastest-growing channel driven by e-commerce subscription services.

Online stores are growing at approximately 9.2% CAGR (2026–2034), driven by subscription-based replenishment models, home delivery convenience, and competitive pricing on platforms including Amazon, Flipkart, and Lazada.

High-growth opportunities exist in adult incontinence products, biodegradable diapers, smart diaper technology, emerging market expansion (India, Africa), and e-commerce direct-to-consumer subscription platforms.

Key challenges include environmental sustainability pressures, raw material (SAP, pulp) price volatility, regulatory chemical safety compliance, intense private-label competition, and low penetration in rural emerging markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)