Private Tutoring Market Size, Share, Trends and Forecast by Learning Method, Course Type, Application, End User, and Region, 2026-2034

Private Tutoring Market Size, Share, Trends & Forecast (2026-2034)

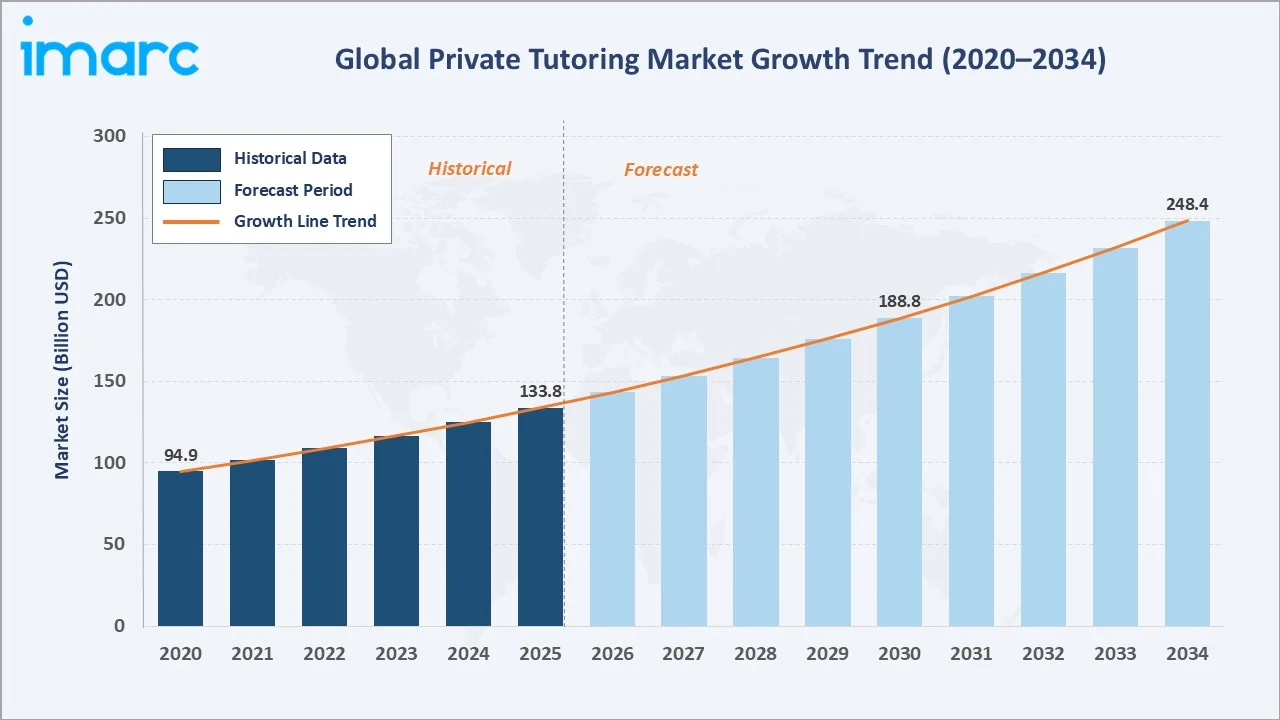

The global private tutoring market size was valued at USD 133.8 Billion in 2025 and is projected to reach USD 248.4 Billion by 2034, growing at a CAGR of 7.12% during 2026-2034. Intensifying academic competition, rising parental investment in supplemental education, and the accelerating adoption of AI-powered and online tutoring platforms are the primary forces underpinning robust market expansion across all major regions globally.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 133.8 Billion |

|

Forecast Market Size (2034) |

USD 248.4 Billion |

|

CAGR (2026-2034) |

7.12% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

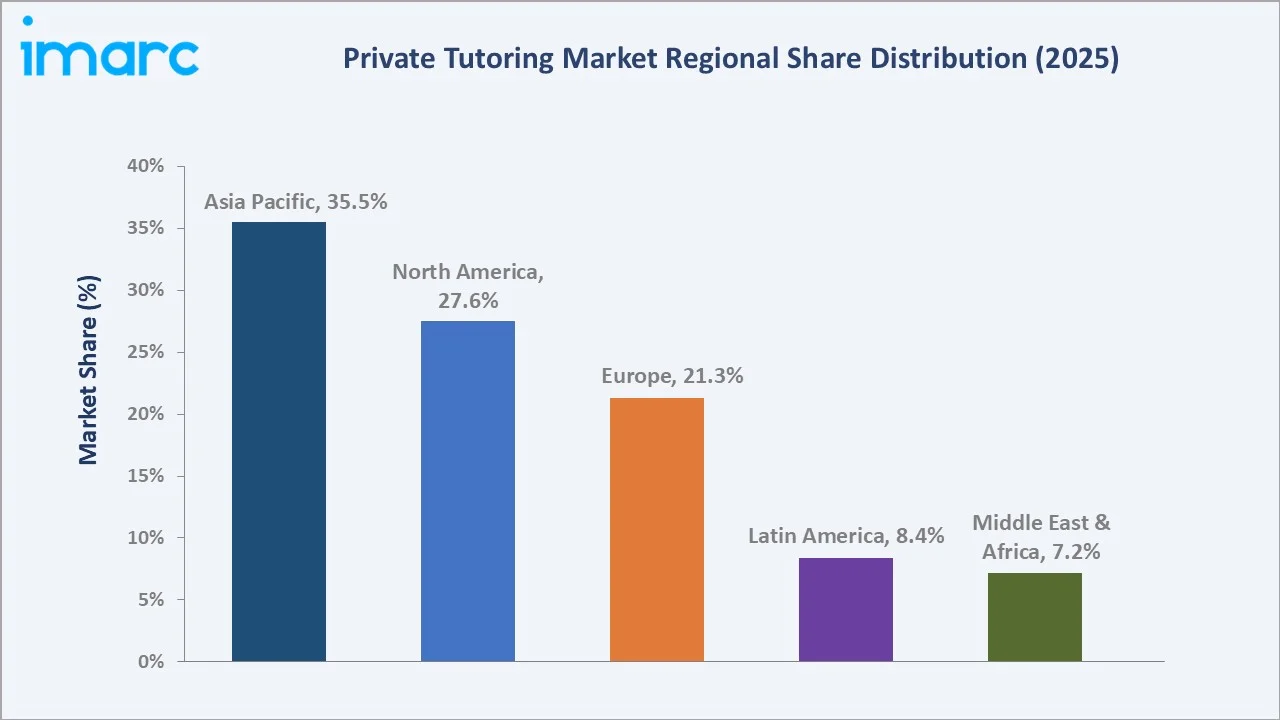

Asia Pacific (35.5% share, 2025) |

|

Largest Learning Method |

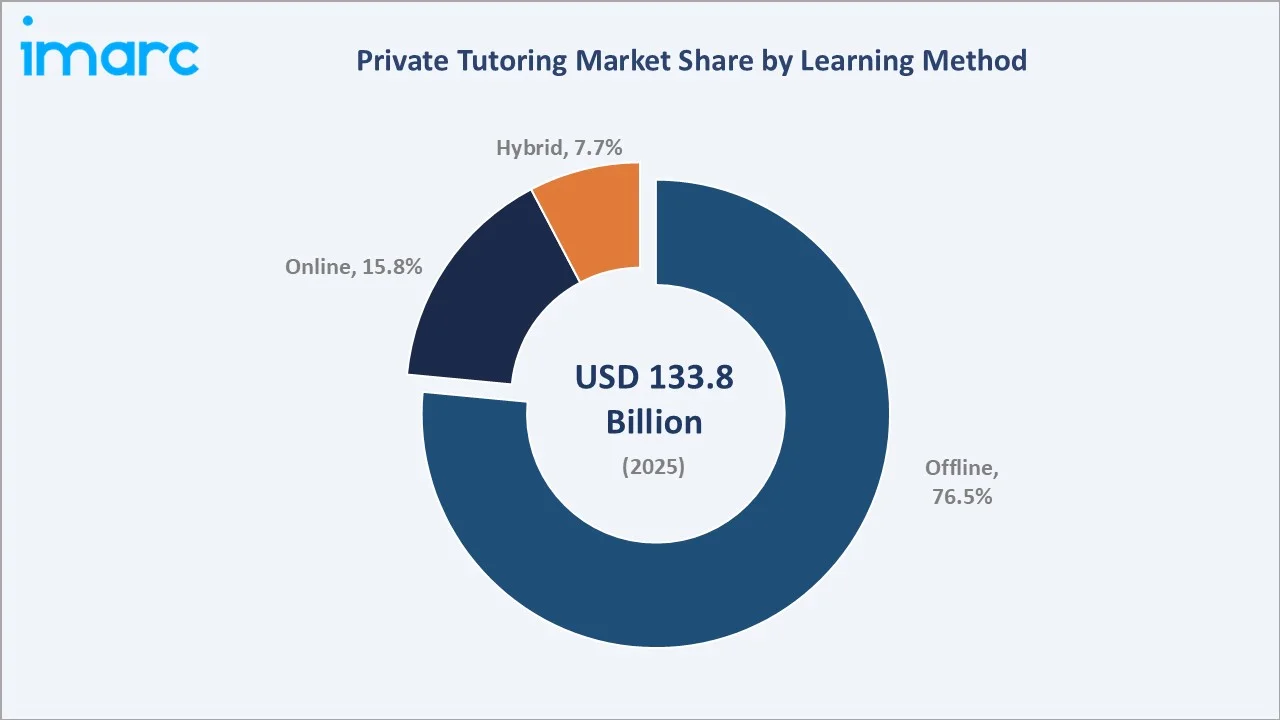

Offline (76.5% share, 2025) |

|

Dominant Application |

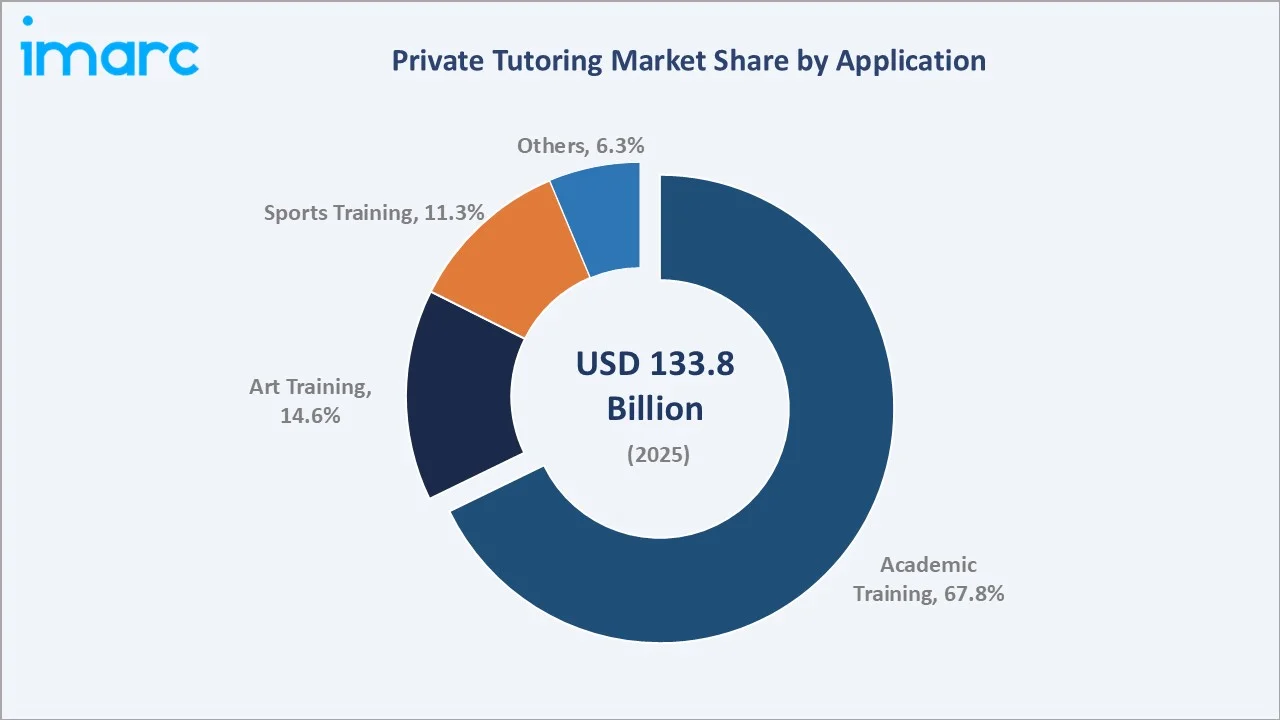

Academic Training (67.8% share, 2025) |

Private tutoring providers such as New Oriental Education & Technology Group, TAL Education Group, and Chegg Inc. enable students to access personalized academic instruction, standardized test preparation, and skill-based training across offline, online, and hybrid delivery formats. The market continues to expand due to increasing demand for personalized learning pathways, real-time academic performance analytics, and the integration of advanced technologies such as AI-driven adaptive assessments and mobile-first tutoring interfaces.

To get more information on this market, Request Sample

Asia Pacific dominates, holding a market share of 35.5% in 2025. Academic training leads application demand at 67.8%, while offline tutoring commands a dominant 76.5% share, reflecting the entrenched preference for face-to-face instruction in high-stakes examination markets across Asia. The market reflects deepening digital integration, rising household education spending, and the accelerating convergence of traditional and technology-enabled tutoring models.

Executive Summary

The global private tutoring market is experiencing sustained expansion, propelled by structural demand forces that are demographic, technological, and competitive. Intensifying academic pressure in exam-oriented education systems across the Asia Pacific, particularly China, India, South Korea, and Japan, alongside standardized test preparation demand in North America and Europe, continues to generate robust enrolment growth. The market reached USD 133.8 Billion in 2025 and is forecast to surpass USD 248.4 Billion by 2034, representing a compelling CAGR of 7.12% over the forecast period.

Offline tutoring holds the largest share at 76.5% in 2025, driven by longstanding parental preference for in-person instruction, tutor accountability, and the established tutoring center model that dominates markets across the Asia Pacific. Online tutoring accounts for 15.8%, having demonstrated accelerated growth as AI-driven platforms, video-conferencing tools, and adaptive learning algorithms lower barriers to accessing high-quality tutors globally.

Hybrid tutoring captures the remaining 7.7% share, with growth prospects strengthening as educational institutions invest in blended delivery capabilities. Academic training dominates application demand at 67.8%, driven by the structural imperative to perform well in high-stakes examinations and university admissions globally. Asia Pacific leads regionally at 35.5%, supported by a deeply embedded culture of shadow education, high parental spending, and rapid platform digitalization across the region.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Learning Method) |

Offline – 76.5% share (2025) |

|

Second Largest (Learning Method) |

Online – 15.8% share (2025) |

|

Dominant Application |

Academic Training – 67.8% share (2025) |

|

Leading Region |

Asia Pacific – 35.5% share (2025) |

|

Fastest Growing Region |

North America (rising EdTech investment + AI platform growth) |

|

Top Companies |

New Oriental Education & Technology Group, TAL Education Group, Chegg Inc., EF (Education First), and Ambow Education Holding Ltd. |

Key Analytical Observations Supporting The Above Data:

- Offline tutoring accounts for 76.5% of the global private tutoring market in 2025, anchored by established tutoring center networks in the Asia Pacific and parental preference for structured, in-person accountability. Markets such as South Korea, Japan, and China sustain among the highest per-student tutoring expenditures globally, predominantly through offline center-based delivery models.

- Online tutoring (15.8%) is the fastest-growing modality, as schools reporting that they provide on‑demand online tutoring, which includes chat‑based tutoring models, increased from 8% in 2024 to 11% in June 2025, based on a U.S. federal survey of public schools conducted by the National Center for Education Statistics.

- Academic training (67.8%) dominates application demand, reflecting the structural role of private supplemental education in high-stakes test preparation globally. The 2025 SAT Suite of Assessments Annual Report reveals that over 2 million students in the high school class of 2025 took the SAT at least once, an increase from 1.97 million in the class of 2024.

- Asia Pacific leads with 35.5% of global market revenue in 2025, driven by intense academic competition, with over 55% of students in India engaging with private tutoring services according to a report by Cambridge International, supported by rising middle-class household incomes and government digital education investment.

Private Tutoring Market Overview

The global private tutoring market encompasses all instructional services provided outside the formal education system, including one-on-one academic tutoring, group coaching sessions, test preparation services, online tutoring platforms, language instruction, and non-academic skill training in arts and sports. The ecosystem spans independent tutors, institutional tutoring centers, EdTech companies, curriculum developers, assessment tool providers, and digital content aggregators serving students from pre-school through post-graduate levels across all major global markets.

Macroeconomic tailwinds, including expanding middle-class household incomes in Asia and Latin America, elevated government education expenditure, and the growing recognition of supplemental education as a standard investment in human capital, create structural demand for private tutoring services. The private tutoring market growth is further amplified by the widespread adoption of AI, real-time performance analytics, and personalized adaptive learning capabilities that reduce the cost of high-quality instruction and extend meaningful access to geographically underserved student populations worldwide.

Market Dynamics

To evaluate market opportunities, Request Sample

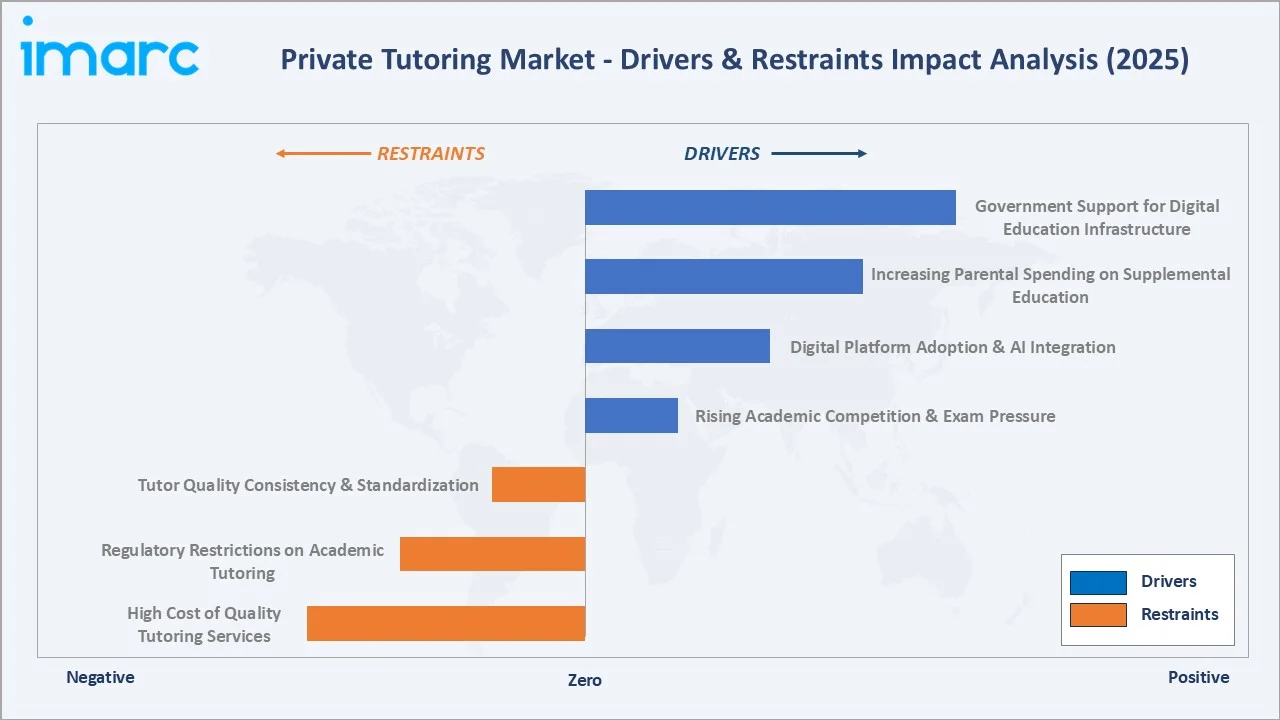

Market Drivers

- Rising Academic Competition & Exam Pressure: The intensification of academic competition across major economies, particularly university entrance examinations in China, India, South Korea, and standardized tests (SAT, ACT, GRE, GMAT) in North America, is a primary demand driver. Students seek specialized coaching to secure admission to elite institutions, sustaining high per-student tutoring expenditure.

- Digital Platform Adoption & AI Integration: In October 2024, FEV Tutor announced results from a study with Stanford University demonstrating that its AI-powered Tutor CoPilot improved K–12 math tutoring outcomes by an average of 9 percentage points for less-experienced tutors. AI-driven adaptive learning engines, machine learning-powered diagnostics, and intelligent content personalization are accelerating platform scalability and instructional efficacy at reduced cost per student.

- Increasing Parental Spending on Supplemental Education: Rising disposable incomes, particularly across Asia Pacific and North America, are enabling higher household allocations toward private tutoring. In FY2024, the U.S. Department of Education (ED) allocated USD 180.0 billion for K-12 and postsecondary education, reflecting substantial investment in supplemental learning services.

- Government Support for Digital Education Infrastructure: Under the National Education Policy (NEP) in India, DIKSHA offers over 19,698 courses with 182.3 million enrolments and 145.7 million completions in 2025–26, while SWAYAM provides 18,500+ courses and has recorded 6.1 crore enrolments and 53.7 lakh certifications.

Market Restraints

- High Cost of Quality Tutoring Services: Premium one-on-one tutoring remains unaffordable for lower-income household segments, particularly in emerging markets where educational access disparities are pronounced. Rising tuition costs and increasing platform subscription fees create adoption barriers, disproportionately affecting rural and economically disadvantaged student populations.

- Regulatory Restrictions on Academic Tutoring: China's 2021 "double reduction" policy banning for-profit academic tutoring for K–9 students imposed significant structural disruption on the world's largest tutoring market. Similar regulatory considerations in South Korea and other markets create uncertainty, requiring providers to diversify strategically into non-academic program verticals to sustain revenue growth.

- Tutor Quality Consistency & Standardization: Maintaining consistent pedagogical quality across large networks of independent tutors poses operational challenges for platform-based tutoring companies, leading to variable student outcomes that erode platform trust, increase churn rates, and complicate quality assurance investment at scale.

Market Opportunities

- Emerging Market Expansion: Southeast Asia, Sub-Saharan Africa, and Latin America represent substantially under-penetrated private tutoring markets with rapidly expanding youth populations, improving internet connectivity, and growing middle-class household formation. These regions offer significant greenfield growth opportunities for EdTech platforms and institutional providers capable of localizing content and pricing models to regional education contexts.

- Gamification, VR & Immersive Learning Integration: In January 2025, Prodigy Learning collaborated with Minecraft Education to launch an AI Credential Product teaching students AI literacy through gamified environments. The integration of virtual reality and augmented reality into tutoring sessions is demonstrating materially superior learner engagement and knowledge retention.

Market Challenges

- Content Quality Standardization Across Platforms: The proliferation of AI-generated tutoring content and automated assessment tools raises concerns about educational accuracy, pedagogical soundness, and quality assurance, requiring significant human editorial oversight and curriculum validation investment that adds operational cost complexity for platform operators.

- Student Engagement & Retention in Digital Formats: Maintaining sustained learner motivation and completion rates in asynchronous online tutoring formats remains a persistent challenge. Dropout rates in digital tutoring programs significantly exceed those of in-person alternatives, necessitating sophisticated behavioral engagement mechanisms, personalized nudge systems, and progress gamification to sustain enrolment and revenue.

Emerging Market Trends

1. Artificial Intelligence Transforming Personalized Tutoring

At the 2025 World Artificial Intelligence Conference in Shanghai, TAL Education Group’s Xueersi launched its “MathGPT AI Learning” intelligent learning companion, showcasing an AI‑driven virtual tutoring system with multimodal interaction and personalized support comparable to one‑on‑one instruction. Machine learning algorithms enable platforms to identify knowledge gaps, predict learning trajectories, and surface hyper-relevant content with a precision that traditional tutors cannot replicate.

2. Expansion of Hybrid Tutoring Models

In October 2024, Ambow Education announced a USD 1.3 million licensing agreement with Singapore-based Inspiring Futures Pte. Ltd. for its HybriU AI UniBox, demonstrating commercial momentum behind hybrid delivery innovation. The flexibility of hybrid models appeals particularly to high-income urban households prioritizing tutor relationship continuity while demanding scheduling flexibility that digital supplementation enables.

3. Surge in STEM and Test Preparation Tutoring

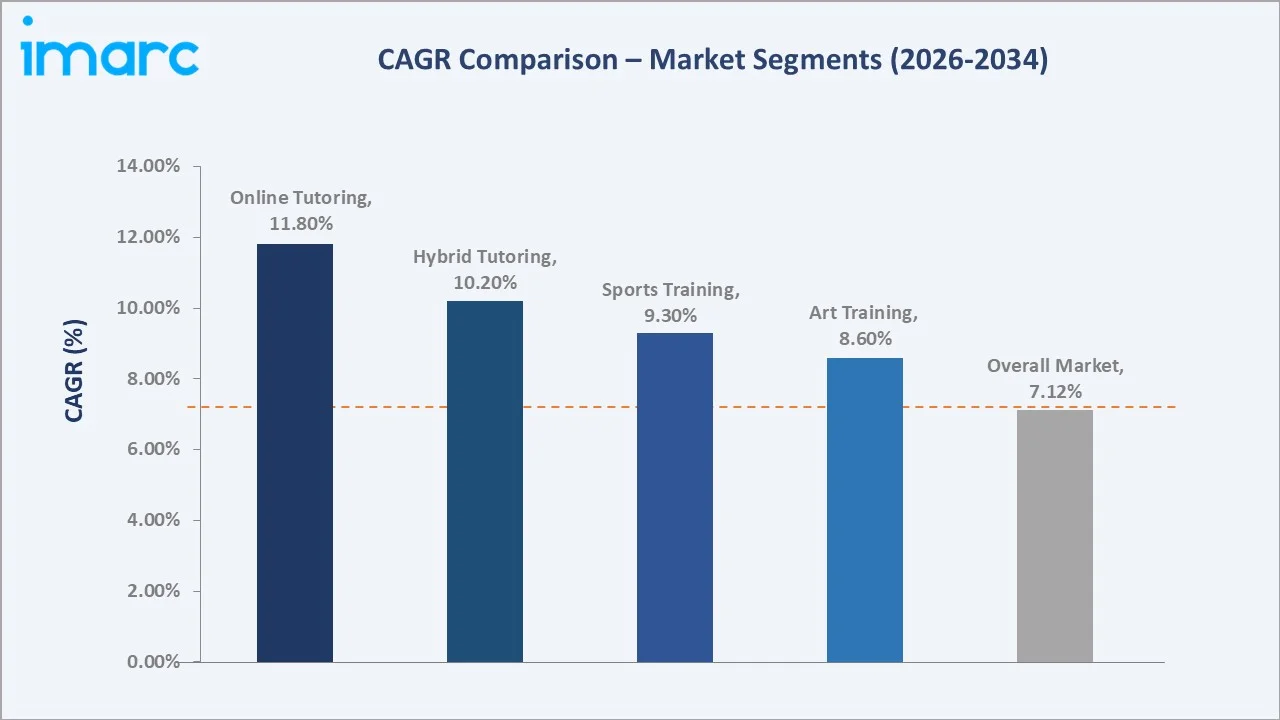

STEM-focused tutoring is gaining momentum as governments worldwide expand STEM curriculum mandates and employers increase preference for candidates with demonstrated technical competencies. Online STEM tutoring is projected to grow at approximately 11.8% CAGR through 2034, significantly above the overall market average, with test preparation services for engineering, medical, and management entrance examinations sustaining high per-student revenue potential across Asia Pacific and North America.

4. Rise of Non-Academic and Skills-Based Tutoring

The private tutoring market is experiencing meaningful segment diversification beyond traditional academic subjects, driven by growing demand for art training (14.6% share), sports coaching (11.3% share), music instruction, language learning, and professional certification preparation. New Oriental expanded its non-academic tutoring to over 60 cities, enrolling about 1.06 million students in creative and sports programs, effectively neutralizing the regulatory impact of K–12 academic bans.

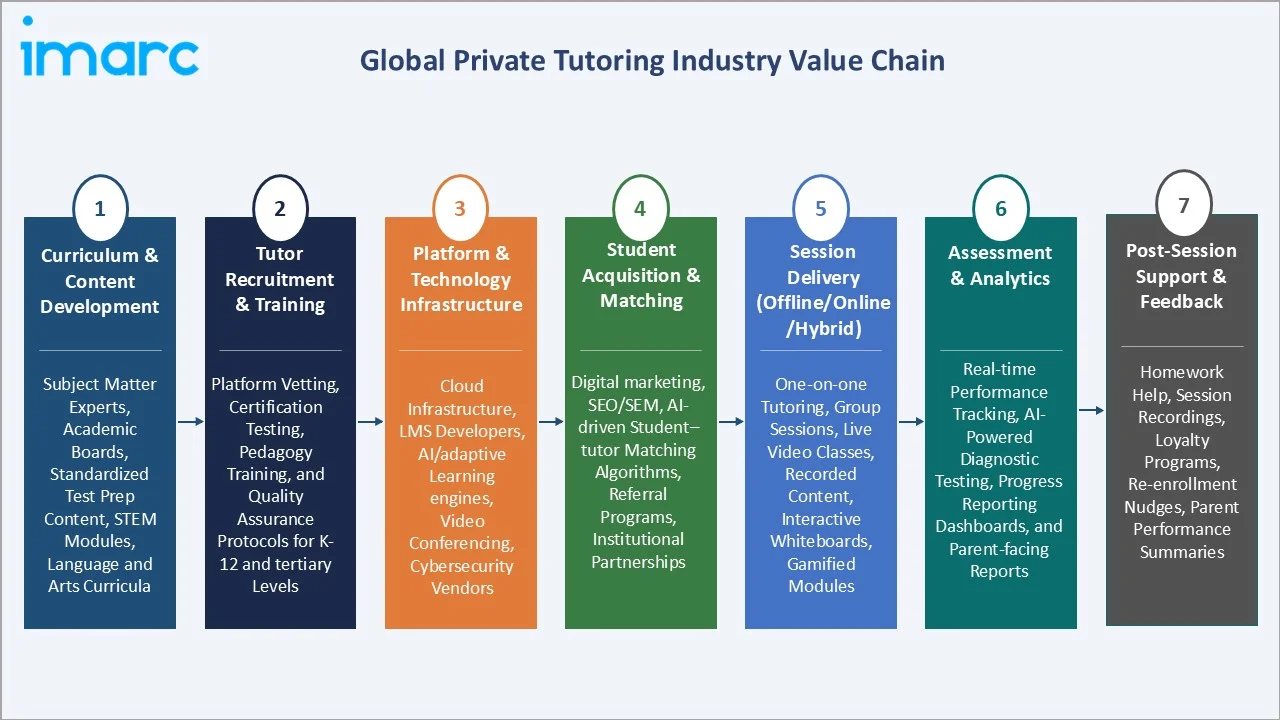

Industry Value Chain Analysis

The private tutoring value chain spans curriculum development through post-session support, with each stage populated by specialized operators whose performance directly influences learner satisfaction, platform economics, and competitive differentiation across the global market.

|

Stage |

Key Activities / Examples |

|

Curriculum & Content Development |

Subject matter experts, academic boards, standardized test prep content, STEM modules, language and arts curricula |

|

Tutor Recruitment & Training |

Platform vetting, certification testing, pedagogy training, and quality assurance protocols for K–12 and tertiary levels |

|

Platform & Technology Infrastructure |

Cloud infrastructure, LMS developers, AI/adaptive learning engines, video conferencing, cybersecurity vendors |

|

Student Acquisition & Matching |

Digital marketing, SEO/SEM, AI-driven student–tutor matching algorithms, referral programs, institutional partnerships |

|

Session Delivery (Offline/Online/Hybrid) |

One-on-one tutoring, group sessions, live video classes, recorded content, interactive whiteboards, gamified modules |

|

Assessment & Analytics |

Real-time performance tracking, AI-powered diagnostic testing, progress reporting dashboards, and parent-facing reports |

|

Post-Session Support & Feedback |

Homework help, session recordings, loyalty programs, re-enrollment nudges, parent performance summaries |

Technology Landscape in the Private Tutoring Industry

Artificial Intelligence & Adaptive Learning Engines

In April 2026, A digital education platform, My Learning, in Nigeria plans to launch with AI‑powered tools to connect students and families with qualified tutors, mentors, and tailored learning resources, aiming to address uneven access to quality education. Adaptive learning engines that dynamically adjust content difficulty, pacing, and format based on real-time performance signals are becoming standard capabilities among leading tutoring platforms, enabling scalable one-on-one-quality instructions.

Video Conferencing, Interactive Whiteboards & Virtual Classrooms

Tutor.com launched its LEO (Learner Engagements Online) platform, a 24/7 institutional tutoring solution with actionable analytics and scheduling tools centralizing academic support for both institutions and students. Real-time collaborative annotation, session recording, and integrated payment processing within tutoring platforms have enhanced the quality and accountability of digital tutoring sessions, contributing to growing student and parent acceptance of online delivery formats.

Gamification, VR & Immersive Learning Technologies

Virtual and augmented reality are at earlier deployment stages but represent a significant technology frontier, particularly for STEM subjects, where three-dimensional visualization materially enhances conceptual understanding. Platforms incorporating immersive learning technologies are demonstrating superior knowledge retention metrics and student satisfaction scores compared to traditional digital formats, positioning them for premium pricing and lower structural churn.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Learning Method | Offline | 76.5% | 2025 |

| Course Type | 🔒 | 🔒 | 2025 |

| Application | Academic Training | 67.8% | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Region | Asia-Pacific | 35.5% | 2025 |

By Learning Method

Offline tutoring dominates the learning method segment with a 76.5% share in 2025. This dominance reflects the entrenched preference for face-to-face instruction across Asia Pacific markets, the accountability and relationship quality of in-person tutoring, and the well-established infrastructure of tutoring centers in high-density urban environments.

To access detailed market analysis, Request Sample

Online tutoring represents 15.8% of the market, driven by rapid platform adoption in India, Southeast Asia, and North America, where AI-powered tutoring platforms enable high-quality academic support without geographic constraints. Hybrid tutoring accounts for 7.7%, representing the fastest-evolving modality as platforms and tutoring centers invest in blended delivery capabilities combining in-person relationship-building with digital practice tools.

By Application

Academic training dominates the application segment with a 67.8% share in 2025, driven by its foundational role in student performance and competitive examination preparation across all major global markets. The structural imperative to perform well in high-stakes national examinations, Gaokao in China, JEE/NEET in India, GCSE and A-level in the UK, and SAT/ACT in the U.S., ensures persistent, non-cyclical demand for academic tutoring.

Art training captures 14.6% of the market, reflecting growing parental investment in holistic child development and increasing recognition of creative skills as complementary to academic achievement. Sports training accounts for 11.3%, benefiting from the formalization of youth athletic coaching and aspirations of student-athletes targeting professional careers or collegiate athletic scholarships.

Regional Market Insights

Asia Pacific's market leadership (35.5%, 2025) reflects the world's most deeply embedded shadow education culture. Academically competitive national examination systems in China, India, Japan, and South Korea generate near-universal demand for private supplemental tutoring, with more than half of students in China (57%) and India (55%) receiving private tuition on average.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

35.5% |

Exam-oriented culture; high parental spending; rapid platform digitalization |

|

North America |

27.6% |

SAT/ACT/GRE test prep; AI EdTech investment; rising personalized learning demand; government digital funding |

|

Europe |

21.3% |

Multilingual tutoring; GCSE/A-level prep; growing online platform adoption; rising parental education spending |

|

Latin America |

8.4% |

Rising internet penetration, expanding middle class, EdTech investment, and youth population growth |

|

Middle East & Africa |

7.2% |

Government education investment; young demographics; improving digital infrastructure; STEM push |

North America represents 27.6% of the global private tutoring market in 2025, driven by standardized test preparation demand, personalized learning trends, and the rapid growth of AI-powered EdTech platforms. Europe's 21.3% share is sustained by multilingual tutoring needs, growing digital platform adoption, and expanding examination preparation demand in the UK, Germany, and France.

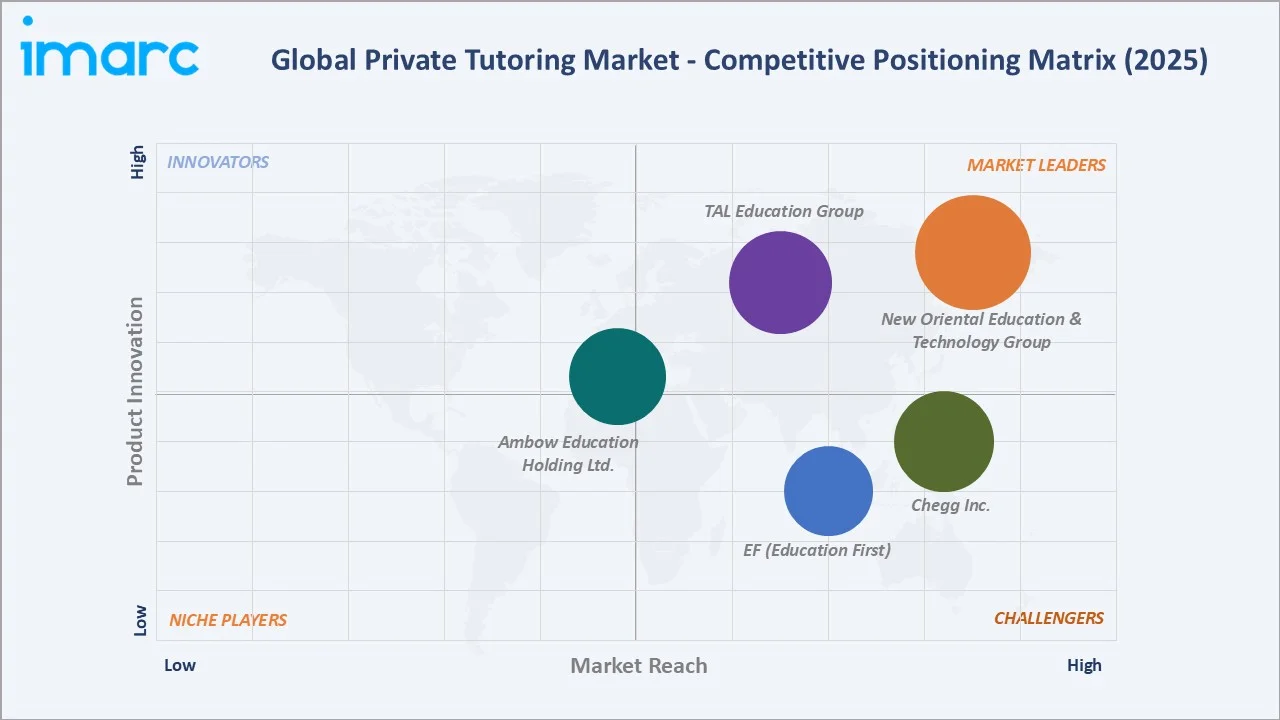

Competitive Landscape

The global private tutoring market exhibits a two-tier competitive structure at the top tier. New Oriental Education & Technology Group reported strong recovery momentum in 2025 following its non-academic diversification, enrolling about 1.06 million students across its arts and sports programs, reflecting resilient demand and successful regulatory navigation.

|

Company |

Brand / Platform/Programs |

Market Position |

Core Strength |

|

New Oriental Education & Technology Group |

New Oriental |

Market Leader |

Largest tutoring network in China; arts & sports pivot post-K12 academic ban |

|

TAL Education Group |

National Open Innovation Platform for Next Generation Artificial Intelligence, MathGPT |

Market Leader |

Proprietary MathGPT AI; live tutoring + analytics for K–12 students |

|

Chegg Inc. |

Chegg Study Help, Chegg Math Solver |

Strong Challenger |

AI-enhanced study tools; STEM homework help; 24/7 tutoring access |

|

EF (Education First) |

EF SET (EF Skills Evaluation Technology) |

Challenger |

Language learning; 50+ country presence; international student programs |

|

Ambow Education Holding Ltd. |

HybriU |

Technology Licensor |

Hybrid AI-powered learning platform licensed to universities globally |

The competitive landscape is characterized by innovation-driven strategies, accelerating AI platform investment, geographic diversification into non-academic verticals, and aggressive pricing to capture digital-native student populations across high-growth emerging markets globally.

Key Company Profiles

New Oriental Education & Technology Group

New Oriental Education & Technology Group, headquartered in Beijing, China, is one of the world's largest private educational services providers, operating a comprehensive network of schools, tutoring centers, and digital platforms.

- Product Portfolio: Language Training, Test Preparation, Int'l Study Consulting, Tourism-Related Business, Livestreaming Platform, and Education Content.

- Recent Developments: For the first fiscal quarter ended August 31, 2025, New Oriental Education & Technology Group Inc. reported net revenues of USD 1,523.0 million, up 6.1% year‑over‑year, and operating income of USD 310.8 million, up 6.0% YoY.

- Strategic Focus: Non-academic vertical diversification; overseas educational program expansion; AI-enhanced curriculum delivery; live-streaming content monetization through the Dongfang Zhenxuan platform.

TAL Education Group

TAL Education Group, headquartered in Beijing, China, operates a diversified portfolio of K–12 online and offline tutoring services, test preparation programs, and AI-powered learning tools across China and select international markets. TAL has invested heavily in proprietary AI and EdTech capabilities to differentiate its instructional offerings.

- Product Portfolio: K–12 subject tutoring, high-school and university entrance exam preparation, STEM education programs, AI-powered MathGPT tutoring system, and international curriculum tracks.

- Recent Developments: At the 2025 World Artificial Intelligence Conference in Shanghai, TAL Education Group showcased its MathGPT AI Learning tool, an AI‑powered learning companion. The system leverages multimodal interaction, customized problem practice, and 24/7 assistance to enhance students’ math learning experiences.

- Strategic Focus: AI and LLM investment for personalized STEM tutoring; small-group and 1-on-1 live tutoring expansion; international market penetration with locally adapted curriculum content.

Chegg Inc.

Chegg, Inc., headquartered in Santa Clara, California, operates one of the United States' largest digital student services platforms, offering AI-enhanced homework help, textbook solutions, and career readiness tools to higher education students across global markets.

- Product Portfolio: Chegg Study Help and Math Solver

- Recent Developments: In June 2024, Chegg selected Amazon Web Services (AWS) as its preferred cloud provider to support its next‑generation, AI‑powered, student‑focused learning solutions, leveraging AWS’s scalable infrastructure and AI technologies.

- Strategic Focus: Generative AI integration for personalized learning pathways; vocational and professional skills expansion; mobile-first product experience optimization; international student market penetration.

Market Concentration Analysis

The global private tutoring market exhibits moderate-to-high concentration in institutional terms, with a handful of large-scale providers in China, the United States, and South Korea commanding significant national market share. However, the structural fragmentation of the broader industry, comprising millions of individual tutors, regional centers, and localized platforms, ensures substantial competitive dynamism across the global market.

Consolidation activity is gaining momentum within the EdTech sub-segment. In May 2025, IXL Learning acquired MyTutor, expanding its institutional market reach in Europe. The Ambow Education–Inspiring Futures HybriU licensing agreement in October 2024 reflects a parallel trend toward technology licensing as a scalable growth model for platform providers seeking international expansion without the capital intensity of direct market entry. These transactions signal a strategic imperative among market leaders to deepen platform capabilities, extend geographic reach, and transition from commodity tutoring services to integrated learning ecosystems with superior retention economics.

Investment & Growth Opportunities

Fastest Growing Segments

Online tutoring (estimated 11.8% CAGR through 2034), AI-powered adaptive learning platforms (12%+ CAGR), and STEM-focused test preparation services (10–12% CAGR) represent the three highest-growth investment vectors within the global private tutoring market. Together, these niches address a total addressable market of approximately USD 75 Billion by 2030, with disproportionate margin potential versus traditional offline center-based tutoring.

Emerging Market Digital Expansion

Southeast Asia, Sub-Saharan Africa, and Latin America represent substantially under-penetrated private tutoring markets offering significant greenfield growth for EdTech-native platforms. Rising smartphone penetration, expanding mobile internet access, and growing middle-class aspirations for quality supplemental education create favorable conditions for mobile-first tutoring platform deployment.

Institutional and Corporate B2B Opportunities

- Key investment themes include AI-powered adaptive tutoring platforms with demonstrated engagement metrics, EdTech companies specializing in STEM and professional certification training, and corporate "Tutoring-as-a-Benefit" solutions targeting enterprise HR buyers.

- Private equity and venture capital interest is concentrated in mobile-first tutoring platforms with strong emerging market penetration, AI-native tutoring startups demonstrating superior learning outcome data, and EdTech marketplaces enabling high-volume tutor–student matching at low marginal cost.

Future Market Outlook (2026-2034)

The global private tutoring market is positioned for sustained, high-growth expansion through 2034. From a base of USD 133.8 Billion in 2025, the market is projected to reach USD 248.4 Billion by 2034, representing total incremental value creation of approximately USD 114.6 Billion over the forecast decade.

Platform evolution, particularly the transition from transactional tutoring sessions to AI-powered personalized learning companions capable of dynamically managing entire student academic trajectories, will redefine how value is captured in the ecosystem. Platforms that successfully integrate autonomous performance diagnostics and real-time curriculum adjustment will command sustainable competitive advantages and superior student retention rates in an increasingly contested market environment.

Long-term, the market trajectory is tied to three structural mega-themes: the democratization of high-quality tutoring through AI, reducing the cost and geographic constraints of expert instruction; the formalization of non-academic supplemental education as a recognized industry vertical with institutional-scale providers; and the emergence of lifelong learning as a cultural norm among millennial and Gen Z parents who allocate disproportionately higher household budget shares to their children's supplemental education.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including tutoring platform executives, academic institution administrators, EdTech technology vendors, financial analysts specializing in the education sector, and a representative consumer panel of 2,200 parents and students across Asia Pacific, North America, and Europe. Insights were gathered on tutoring demand drivers, platform usage patterns, parental spending behaviors, and tutor recruitment and quality assurance practices across all major regional markets.

Secondary Research

Secondary research encompassed a systematic review of company annual reports and investor presentations, government education expenditure databases (UNESCO, World Bank, national education ministries), EdTech industry trade publications, academic research on supplemental education efficacy, and publicly available platform enrolment and engagement data. Sources included IMARC proprietary databases, regulatory filings, and peer-reviewed educational research publications from 2024–2025.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches incorporating national education expenditure data, enrolment rates in supplemental tutoring programs, household income trends, and platform-reported revenue and enrolment data. A base-case CAGR of 7.12% reflects consensus analyst estimates validated against reported tutoring platform revenue growth rates and regional education demand indices, with sensitivity analysis performed across bullish (8.5%) and bearish (5.5%) demand scenarios for the 2026–2034 forecast period.

Private Tutoring Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Learning Methods Covered | Online, Blended, Others |

| Course Types Covered | Curriculum-Based Learning, Test Preparation, Others |

| Applications Covered | Academic Training, Sports Training, Art Training, Others |

| End Users Covered | Pre-School Children, Primary School Students, Middle School Students, High School Students, College Students, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | New Oriental Education & Technology Group, TAL Education Group, Chegg Inc., EF (Education First), Ambow Education Holding Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the private tutoring market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global private tutoring market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the private tutoring industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Private Tutoring Market Report

The global private tutoring market size was valued at USD 133.8 Billion in 2025 and is projected to reach USD 248.4 Billion by 2034.

The market is expected to grow at a CAGR of 7.12% during the forecast period from 2026-2034, driven by rising academic competition, parental investment in supplemental education, AI platform adoption, and expanding middle-class household incomes globally.

Asia Pacific leads the market with a 35.5% share in 2025, driven by exam-oriented education cultures, high parental spending on supplemental education, over 55% student tutoring participation in China and India, and rapid digital platform adoption across the region.

The offline segment holds the largest share at 76.5% in 2025 (approximately USD 102.4 Billion), driven by parental preference for face-to-face instruction, tutor accountability, and the established tutoring center model that dominates markets across the Asia Pacific.

Academic training dominates with a 67.8% share in 2025, reflecting the structural importance of private supplemental education in competitive examination preparation globally, including Gaokao (China), JEE/NEET (India), and SAT/ACT (United States).

Key drivers include rising academic competition and exam pressure, growing parental investment in supplemental education, accelerating adoption of AI-powered and online tutoring platforms, government support for digital education infrastructure, increasing STEM curriculum demand, and expanding middle-class household incomes across the Asia Pacific and Latin America.

Online tutoring is the fastest-growing modality, projected at approximately 11.8% CAGR through 2034. AI-powered adaptive learning platforms and STEM-focused test preparation services are also among the highest-growth investment vectors, driven by increasing internet penetration and government-backed digital education initiatives.

AI is transforming private tutoring by enabling personalized adaptive learning at scale, real-time student performance diagnostics, automated feedback systems, and 24/7 tutoring availability. In mid-2025, TAL Education's MathGPT demonstrated the commercial viability of generative AI in live tutoring, while FEV Tutor's Tutor CoPilot improved K–12 math outcomes by 9 percentage points for less-experienced tutors.

Some of the major players in the private tutoring market include New Oriental Education & Technology Group, TAL Education Group, Chegg Inc., EF (Education First), and Ambow Education Holding Ltd., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)