Probiotic Dietary Supplement Market Size, Share, Trends and Forecast by Form, Distribution Channel, Application, and Region, 2026-2034

Probiotic Dietary Supplement Market Size, Share, Trends & Forecast (2026-2034)

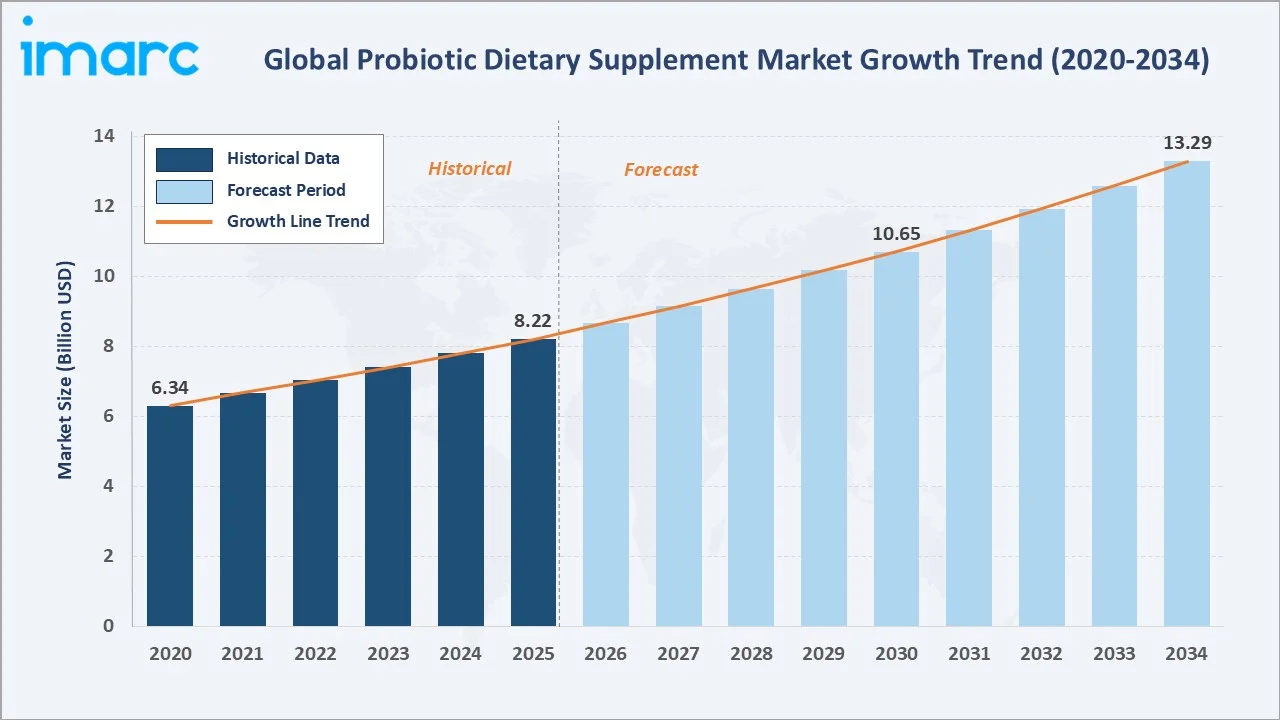

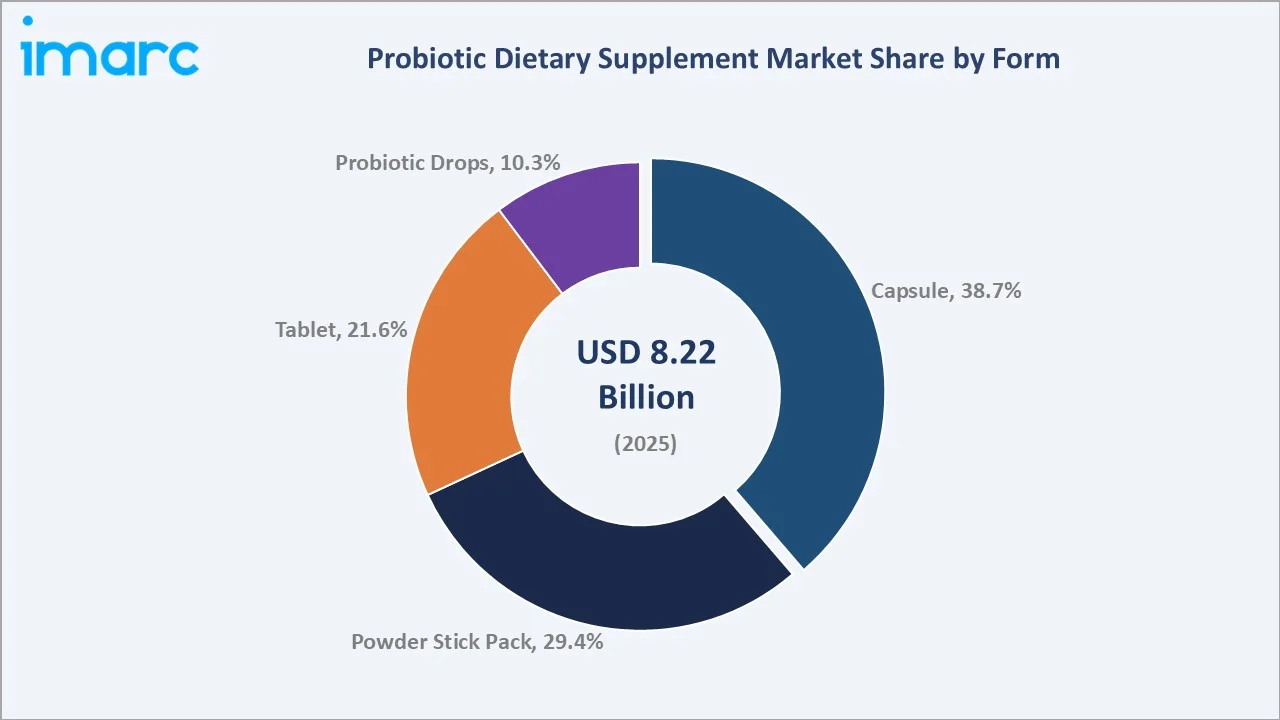

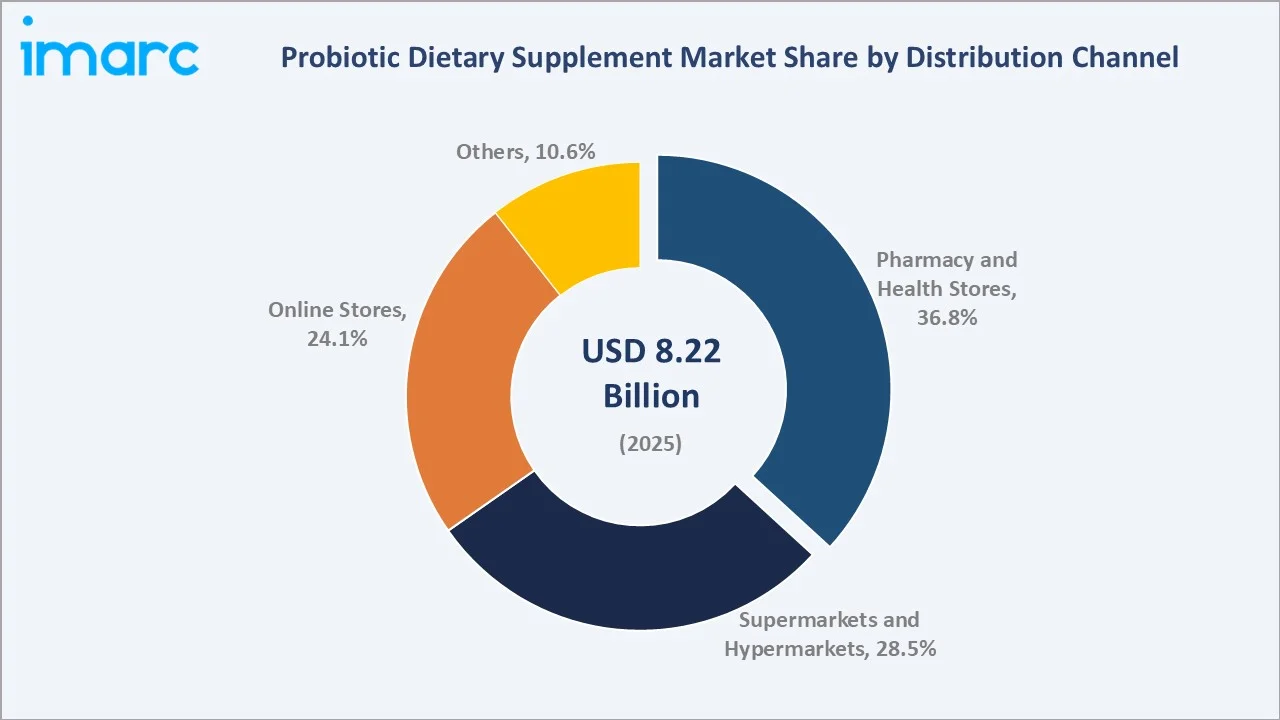

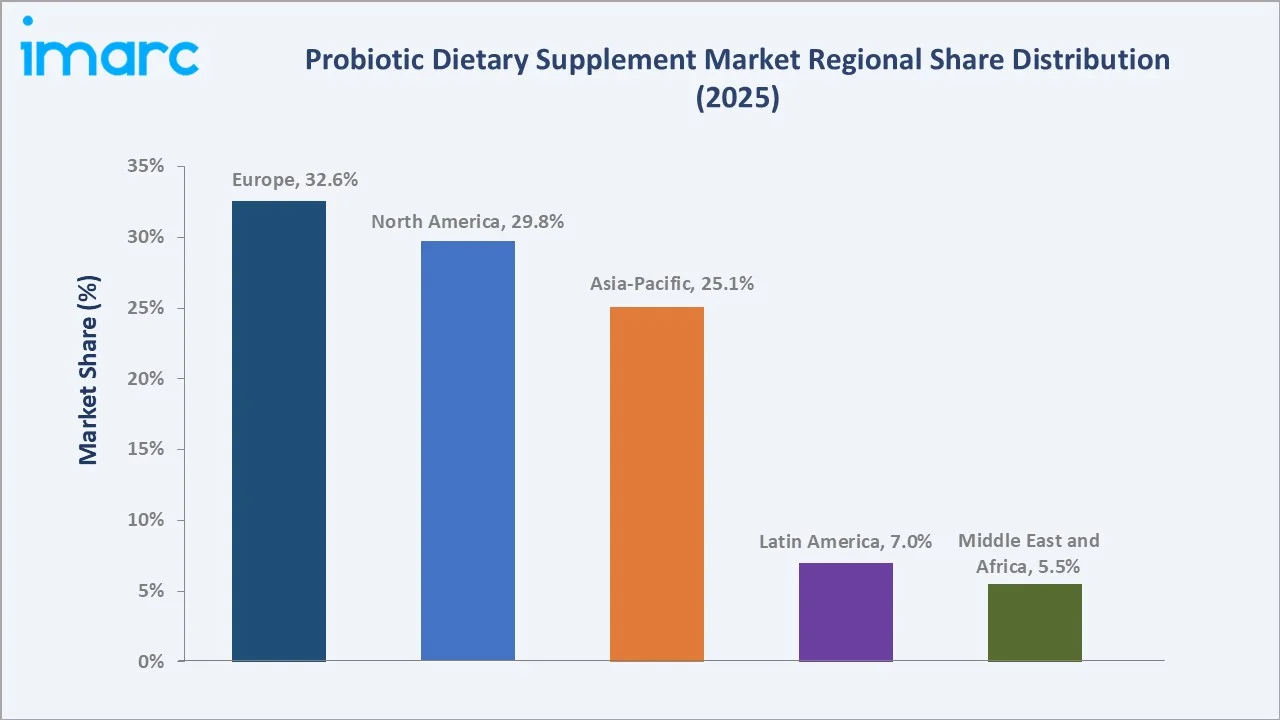

The global probiotic dietary supplement market reached USD 8.22 Billion in 2025 and is projected to reach USD 13.29 Billion by 2034, growing at a CAGR of 5.33% during 2026-2034. The market is driven by growing consumer awareness of gut health, digestive wellness, and immunity support. Americans show strong adoption of digestive health supplements in 2025, with 53% using probiotics and 44% using prebiotics, both higher than global averages of 49% and 41%, respectively. Higher supplement penetration also encourages brands to expand probiotic product formats, personalized formulations, and targeted digestive and immunity-focused offerings. Capsule leads form at 38.7%. Pharmacy and health stores lead distribution at 36.8%. Europe leads regionally at 32.6%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.22 Billion |

|

Forecast Market Size (2034) |

USD 13.29 Billion |

|

CAGR (2026-2034) |

5.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Form |

Capsule (38.7%, 2025) |

|

Dominant Distribution Channel |

Pharmacy and Health Stores (36.8%, 2025) |

|

Leading Region |

Europe (32.6%, 2025) |

The global probiotic dietary supplement market has grown steadily from USD 6.34 Billion in 2020 to USD 8.22 Billion in 2025, supported by rising consumer focus on gut health, immunity, and preventive wellness. The market is expected to reach USD 10.65 Billion by 2030, reflecting wider adoption of probiotics across capsules, tablets, gummies, powders, and functional supplement formats. By 2034, the market is forecast to reach USD 13.29 Billion, driven by microbiome-focused nutrition, personalized health solutions, and increasing demand for digestive and immune support products.

To get more information on this market, Request Sample

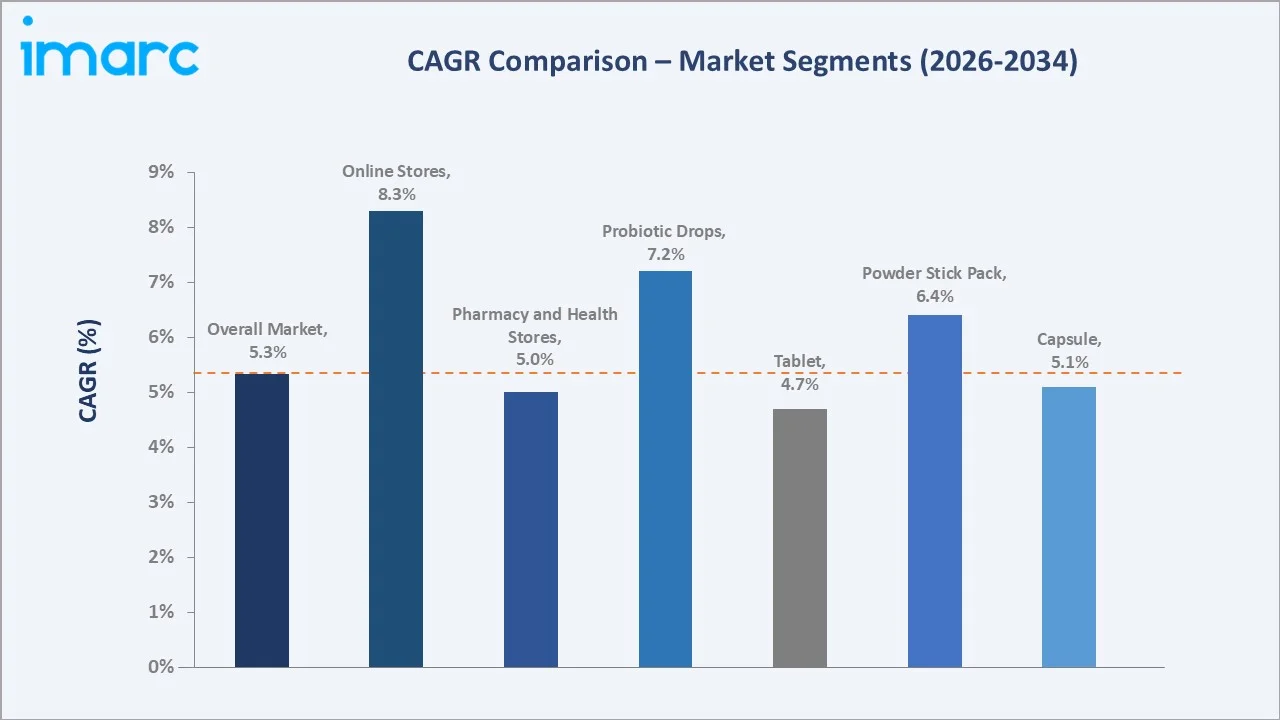

Online stores grow fastest at ~8.3% CAGR through D2C probiotic subscription platforms, Amazon Subscribe & Save auto-replenishment, and personalized microbiome DTC brand. Probiotic drops grow at ~7.2% CAGR through infant drops, pediatric probiotics, and liquid adult probiotics.

Executive Summary

The global probiotic dietary supplement market reached USD 8.22 Billion in 2025, driven by rising awareness of gut health, digestive wellness, immunity support, and preventive healthcare. Consumers are increasingly adopting probiotics in capsules, gummies, powders, tablets, and personalized nutrition formats. Growth is further supported by microbiome research, e-commerce expansion, and demand for natural wellness products. The market is projected to reach USD 13.29 Billion by 2034.

Capsule at 38.7% leads through enteric-coated delayed-release consumer preference. Pharmacy and health stores at 36.8% leads through pharmacist recommendation trust. Europe leads at 32.6% through regional brand dominance.

Key Market Insights

|

Insight |

Data |

|

Dominant Form |

Capsule - 38.7% share (2025) |

|

Dominant Distribution Channel |

Pharmacy and Health Stores - 36.8% market share (2025) |

|

Leading Region |

Europe - 32.6% share (2025) |

|

Market Opportunity |

Psychobiotic gut-brain axis supplements; precision microbiome personalized probiotics; pediatric drops; postbiotic and synbiotic combination; online subscription auto-replenishment probiotics |

Key Analytical Observations Supporting the Above Data:

- Capsule at 38.7%: The capsule segment dominates due to its convenience, accurate dosage, longer shelf life, and strong consumer acceptance. Capsules also protect probiotic strains better than some formats, helping maintain potency and effectiveness.

- Pharmacy and Health Stores at 36.8%: The pharmacy and health stores dominate because consumers trust these channels for safe, authentic, and expert-recommended probiotic supplements. These stores also offer better product visibility, brand credibility, and access to health-focused buyers seeking digestive and immunity support.

- Europe at 32.6%: Europe dominates regionally due to high consumer awareness of gut health, strong preventive healthcare habits, and widespread acceptance of probiotic supplements. The region also benefits from mature pharmacy/health retail channels, strict quality standards, and strong demand for digestive wellness and immunity-support products.

Probiotic Dietary Supplement Market Overview

The global probiotic dietary supplement market operates within the broader dietary supplement market as a multi-benefit gut and immune probiotic supplement category. The market is classified by probiotic genus (Lactobacillus, Bifidobacterium, Saccharomyces, and Bacillus coagulans spore-forming), CFU count, and form.

The probiotic dietary supplement ecosystem integrates probiotic strain fermentation and R&D, ingredient formulation and blending, contract manufacturing and packaging, multi-channel retail and distribution, regulatory bodies and standards, and general wellness, clinical, pediatric, and geriatric end consumers. Macroeconomic factors include rising healthcare expenditure, growing disposable incomes, and increasing consumer spending on preventive health and wellness products.

Market Dynamics

To evaluate market opportunities, Request Sample

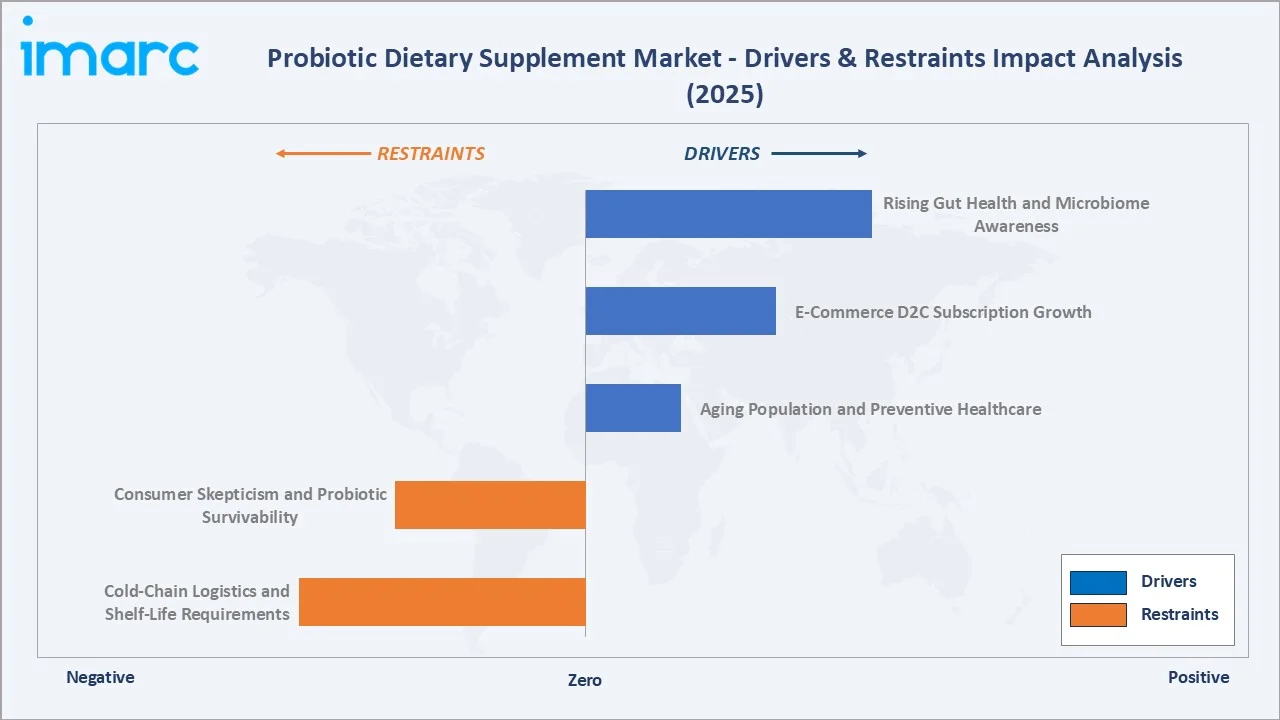

Market Drivers

- Rising Gut Health and Microbiome Awareness: Rising gut health and microbiome awareness are driving the market as consumers increasingly link digestive balance with immunity, metabolism, mood, and overall wellness. Growing education around the gut microbiome is encouraging daily probiotic use as part of preventive healthcare routines. Yakult Danone India launched a multi-platform awareness campaign during World Digestive Health Week, held in May 2026, to bring greater attention to digestive wellness and preventive healthcare. The campaign spans digital media, radio, podcasts, public relations, and the company’s website, aiming to educate consumers that gut health affects more than digestion. This rising health awareness is expanding demand for probiotic supplements.

- E-Commerce D2C Subscription Growth: E-commerce and D2C subscription growth are making products more accessible through online platforms, brand websites, and auto-refill models. Subscription services encourage repeat purchases and improve customer retention, especially for daily-use probiotic products. Digital channels also allow brands to offer personalized recommendations, bundled wellness packs, and targeted formulations. This is helping expand consumer reach and accelerate probiotic supplement adoption.

- Aging Population and Preventive Healthcare: By 2030, one in six people globally will be aged 60 years or above, with this population rising from 1 billion in 2020 to 1.4 billion. By 2050, the number of people aged 60 and older is expected to double to 2.1 billion, while the population aged 80 years and above is projected to triple to 426 million between 2020 and 2050. This aging population is driving the market as older adults increasingly seek solutions to support digestive health, immunity, and overall well-being. Age-related changes in gut microbiota and the rising prevalence of chronic health conditions are encouraging the use of probiotics as part of daily wellness routines. Consumers are also becoming more proactive about preventive healthcare to reduce future medical costs and maintain quality of life.

Market Restraints

- Consumer Skepticism and Probiotic Survivability: Consumers question whether probiotic strains remain alive and effective until consumption. Concerns around clinical proof, strain-specific benefits, dosage accuracy, and shelf stability can reduce trust in product claims. Probiotics are also sensitive to heat, moisture, stomach acid, and storage conditions, which may affect potency. These issues create a need for stronger labeling, scientific validation, and advanced delivery technologies to improve consumer confidence.

- Cold-Chain Logistics and Shelf-Life Requirements: Many probiotic strains require controlled temperature conditions during storage and transportation to maintain viability. Maintaining refrigeration throughout the supply chain increases operational costs and complexity for manufacturers, distributors, and retailers. Exposure to heat, humidity, or improper handling can reduce the number of live microorganisms, affecting product efficacy and consumer trust. These challenges are particularly significant in emerging markets with limited cold-chain infrastructure.

Market Opportunities

- Personalized Probiotic Supplements: Personalized probiotic supplements create a strong opportunity as consumers increasingly seek gut health solutions tailored to their age, lifestyle, diet, health goals, and microbiome profile. Brands can use quizzes, microbiome testing, and AI-driven recommendations to offer customized probiotic strains and dosages. This improves consumer engagement, product relevance, and repeat purchases. As demand for personalized nutrition grows, targeted probiotic formulations are expected to gain wider adoption.

- Synbiotic Probiotic Combination Supplements: Synbiotic probiotic combination supplements combine probiotics with prebiotics that help nourish and support beneficial gut bacteria. This synergistic approach can improve probiotic survival, colonization, and overall effectiveness in the digestive system. In April 2026, Olly introduced Precise Probiotics, a new product range aimed at supporting the gut microbiome and overall wellness. The line extends beyond basic digestive health, offering targeted formulas for stress support, metabolism support, and skin support. Each product includes clinically studied probiotic strains along with the Synbio blend Howaru Bi-07 to promote digestive and immune health. Growing consumer interest in comprehensive gut health and microbiome optimization is driving demand for synbiotic formulations.

Market Challenges

- Strain Stability and Product Potency Maintenance: Strain stability and product potency maintenance are major challenges because probiotic microorganisms can lose viability during manufacturing, storage, transportation, and shelf life. Exposure to heat, moisture, oxygen, and stomach acid can reduce live cell counts, affecting product effectiveness. Manufacturers must invest in advanced encapsulation, protective packaging, and stability testing to maintain claimed CFU levels. These requirements increase production costs and make quality assurance more complex.

- Intense Competition from Functional Foods and Beverages: Intense competition from functional foods and beverages is challenging as consumers increasingly obtain probiotics through yogurts, fermented drinks, kefir, kombucha, and other fortified food products. These products offer a convenient and familiar way to support gut health without requiring separate supplement purchases. Major food and beverage companies are also investing heavily in probiotic product innovation and marketing, increasing competitive pressure. As a result, supplement manufacturers must differentiate through higher-potency formulations, strain-specific benefits, and clinically validated health claims.

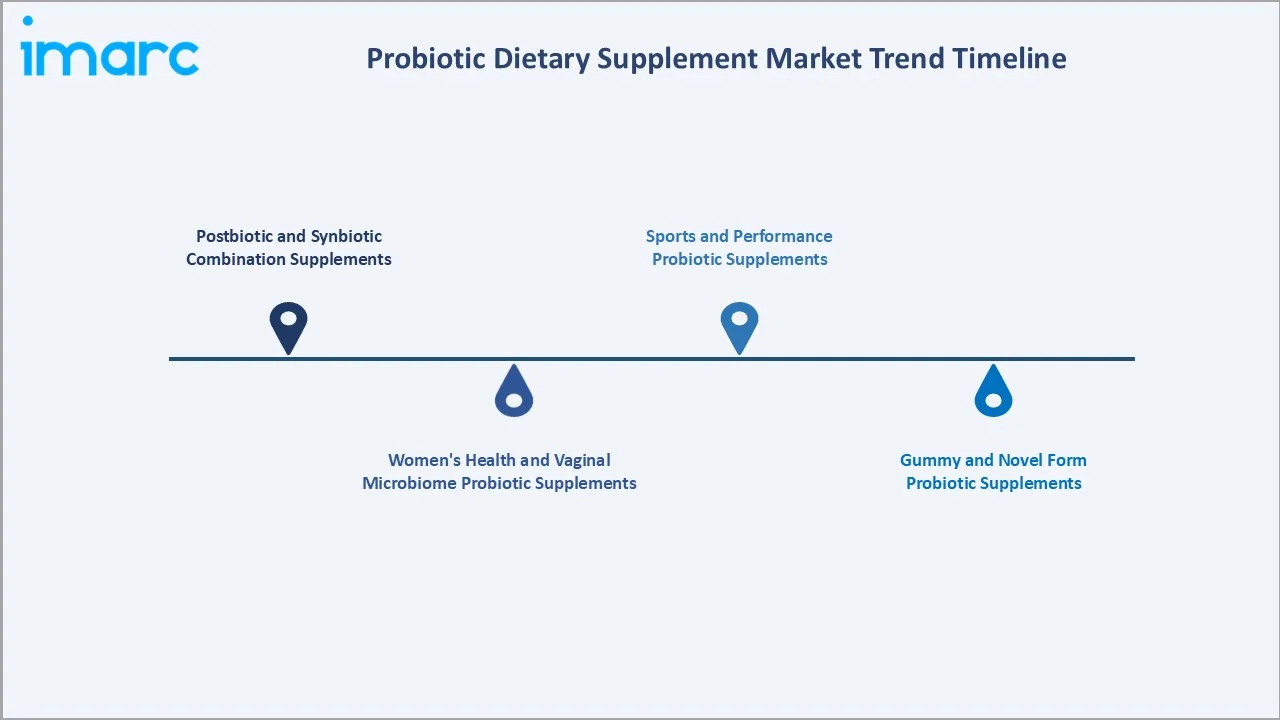

Emerging Market Trends

1. Postbiotic and Synbiotic Combination Supplements

Postbiotic and synbiotic combination supplements are emerging as consumers seek more complete gut health solutions. Synbiotics combine probiotics with prebiotics to improve bacterial survival and effectiveness, while postbiotics provide beneficial compounds produced by probiotics. These combinations offer broader digestive, immune, skin, metabolism, and wellness benefits. In March 2025, TopGum launched Gummiotics, a sugar-free synbiotic gummy supplement. The three-in-one formula combines prebiotics, probiotics, and postbiotics to support gut health and immune function. As brands focus on targeted and science-backed formulations, demand for multi-benefit microbiome supplements is expected to grow.

2. Women's Health and Vaginal Microbiome Probiotic Supplements

Women's health and vaginal microbiome probiotic supplements are emerging as awareness of feminine health, hormonal balance, and microbiome wellness continues to grow. Consumers are increasingly seeking targeted probiotic strains that support vaginal health, urinary tract health, pregnancy wellness, and menopause-related concerns. In June 2026, Daré Bioscience announced the commercial launch of Flora Sync LF5, a vaginal probiotic capsule designed to help restore microbiome balance and support long-lasting vaginal comfort. These novel product launches and advances in microbiome research are enabling the development of strain-specific formulations tailored to women's health needs.

3. Gummy and Novel Form Probiotic Supplements

Gummy and novel-form probiotic supplements are emerging as consumers seek convenient, enjoyable, and easy-to-consume alternatives to traditional capsules and tablets. Formats such as gummies, chewables, melts, sticks, powders, and liquid shots improve product appeal among children, adults, and first-time supplement users. These forms also support better brand differentiation and daily-use compliance. As wellness brands focus on taste, convenience, and lifestyle-based nutrition, demand for innovative probiotic supplement formats is expected to rise.

4. Sports and Performance Probiotic Supplements

Sports and performance probiotic supplements are emerging as athletes and active consumers increasingly link gut health with energy, recovery, immunity, and nutrient absorption. Targeted probiotic strains are being developed to support exercise recovery, reduce digestive discomfort, and improve overall performance resilience. These products are gaining traction in sports nutrition formats such as capsules, powders, sachets, and functional blends. As fitness-focused consumers seek holistic wellness solutions, demand for performance-oriented probiotics is expected to grow.

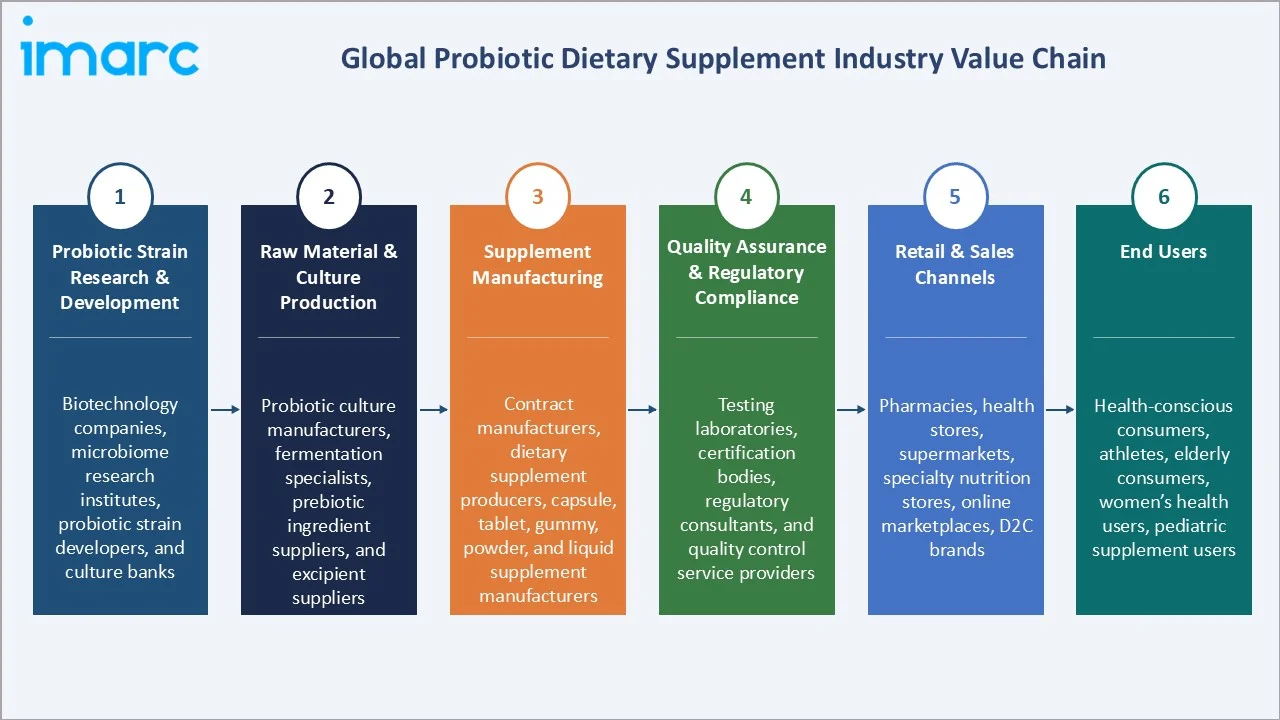

Industry Value Chain Analysis

The probiotic dietary supplement value chain integrates probiotic strain research & development, raw material & culture production, supplement manufacturing, quality assurance & regulatory compliance, retail & sales channels, and end users.

|

Stage |

Key Participants |

|

Probiotic Strain Research & Development |

Biotechnology companies, microbiome research institutes, probiotic strain developers, and culture banks |

|

Raw Material & Culture Production |

Probiotic culture manufacturers, fermentation specialists, prebiotic ingredient suppliers, and excipient suppliers |

|

Supplement Manufacturing |

Contract manufacturers, dietary supplement producers, capsule, tablet, gummy, powder, and liquid supplement manufacturers |

| Quality Assurance & Regulatory Compliance |

Testing laboratories, certification bodies, regulatory consultants, and quality control service providers |

|

Retail & Sales Channels |

Pharmacies, health stores, supermarkets, specialty nutrition stores, online marketplaces, D2C brands |

|

End Users |

Health-conscious consumers, athletes, elderly consumers, women’s health users, pediatric supplement users |

The supplement manufacturing stage is the most value-added segment in the probiotic dietary supplement value chain. It is where probiotic strains are formulated into capsules, tablets, gummies, powders, and other delivery formats using proprietary encapsulation, stability, and dosage technologies. This stage creates the greatest product differentiation, brand value, and margin potential through formulation expertise and consumer-focused innovation.

Technology Landscape in the Probiotic Dietary Supplement Industry

Probiotic Strain Technology and CFU Optimization

Probiotic strain technology and CFU optimization enable the development of more effective and targeted formulations. Advances in strain selection, genetic characterization, and fermentation techniques help improve probiotic stability, survivability, and health benefits. Manufacturers are also optimizing colony-forming unit (CFU) levels to ensure adequate potency throughout shelf life and delivery to the gut. These innovations enhance product efficacy, consumer confidence, and differentiation in an increasingly competitive market.

Microbiome Analytics and Personalization Technology

Microbiome analytics and personalization technology enable customized nutrition solutions based on individual gut microbiome profiles. Advances in microbiome sequencing, AI-driven analytics, and health data platforms help identify specific microbial imbalances and recommend targeted probiotic strains. These technologies improve product precision, consumer engagement, and health outcomes. As personalized wellness gains popularity, microbiome-based supplement recommendations are becoming a major differentiator for probiotic brands.

ProBioAct Technology

ProBioAct technology improves the adhesion of probiotic strains to the intestinal lining, which enhances their survival and effectiveness in the gut. The technology helps beneficial bacteria remain active for longer periods, improving digestive and immune health outcomes. In August 2025, ecosupp launched an advanced next-generation probiotic range focused on stability, targeted action, and clinical performance. The series includes three formulas: REBALANCE for post-antibiotic recovery, BASE-IT for daily microbiome balance, and ZEN for gut–brain axis support during stress. The range uses ProBioAct technology, which helps probiotic bacteria survive digestive conditions, reach the intestine in active form, and deliver improved stability and effectiveness. As manufacturers seek to maximize probiotic efficacy, advanced delivery technologies such as ProBioAct are becoming increasingly important for product differentiation and clinical performance.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Form |

Capsule |

38.7% |

2025 |

|

Distribution Channel |

Pharmacy and Health Stores |

36.8% |

2025 |

|

Application |

Nutritional Supplements |

🔒 |

2025 |

|

Region |

Europe |

32.6% |

2025 |

By Form

Capsule leads at 38.7% (2025), through enteric-coated delayed-release consumer preference, high-CFU concentration, and multi-strain capsule formulation.

To access detailed market analysis, Request Sample

Powder stick pack at 29.4% grows at ~6.4% CAGR through D2C probiotic subscription stick pack, functional drink powder probiotic, and children's flavored powder. Tablet at 21.6% reflects a chewable probiotic supplement. Probiotic drops at 10.3% grows fastest at ~7.2% CAGR through infant drops, pediatric liquids, and adult oil-based drops.

By Distribution Channel

Pharmacy and health stores lead at 36.8% (2025), through pharmacist-recommended probiotic trust, pharmacy dominance, and clinical probiotic brands.

Supermarkets and hypermarkets at 28.5% offering strong product visibility, easy accessibility, and trusted retail availability for probiotic supplements. Online stores at 24.1% grow fastest at ~8.3% CAGR through D2C subscription, Amazon, and personalized microbiome DTC. Others at 10.6% include direct sales and practitioner dispensing.

Regional Market Insights

|

Region |

Share (2025) |

Key Probiotic Dietary Supplement Market Drivers & Characteristics |

|

Europe |

32.6% |

Driven by strong consumer awareness of gut health, preventive healthcare practices, and widespread adoption of probiotic supplements. |

|

North America |

29.8% |

Reflects high consumer spending on dietary supplements, increasing interest in digestive health, and strong adoption of personalized nutrition solutions. |

|

Asia-Pacific |

25.1% |

Supported by a large consumer base, rising health awareness, growing disposable incomes, and the long-standing cultural acceptance of fermented and probiotic products. |

|

Latin America |

7.0% |

Driven by increasing awareness of digestive wellness, improving access to dietary supplements, and a growing middle-class population seeking preventive health solutions. |

|

Middle East and Africa |

5.5% |

Reflects growing health consciousness, rising demand for immunity and digestive health products, and increasing availability of probiotic supplements through pharmacies, health stores, and online platforms. |

Europe's 32.6% supported by strong gut health awareness, preventive healthcare habits, and mature pharmacy and health retail channels. North America's 29.8% due to high supplement spending, strong e-commerce adoption, and demand for personalized microbiome solutions.

Asia-Pacific's 25.1% driven by rising disposable incomes, health consciousness, and cultural familiarity with fermented products. Latin America's 7.0% and Middle East & Africa’s 5.5% supported by expanding retail access, growing wellness awareness, and increasing demand for digestive and immunity-support supplements.

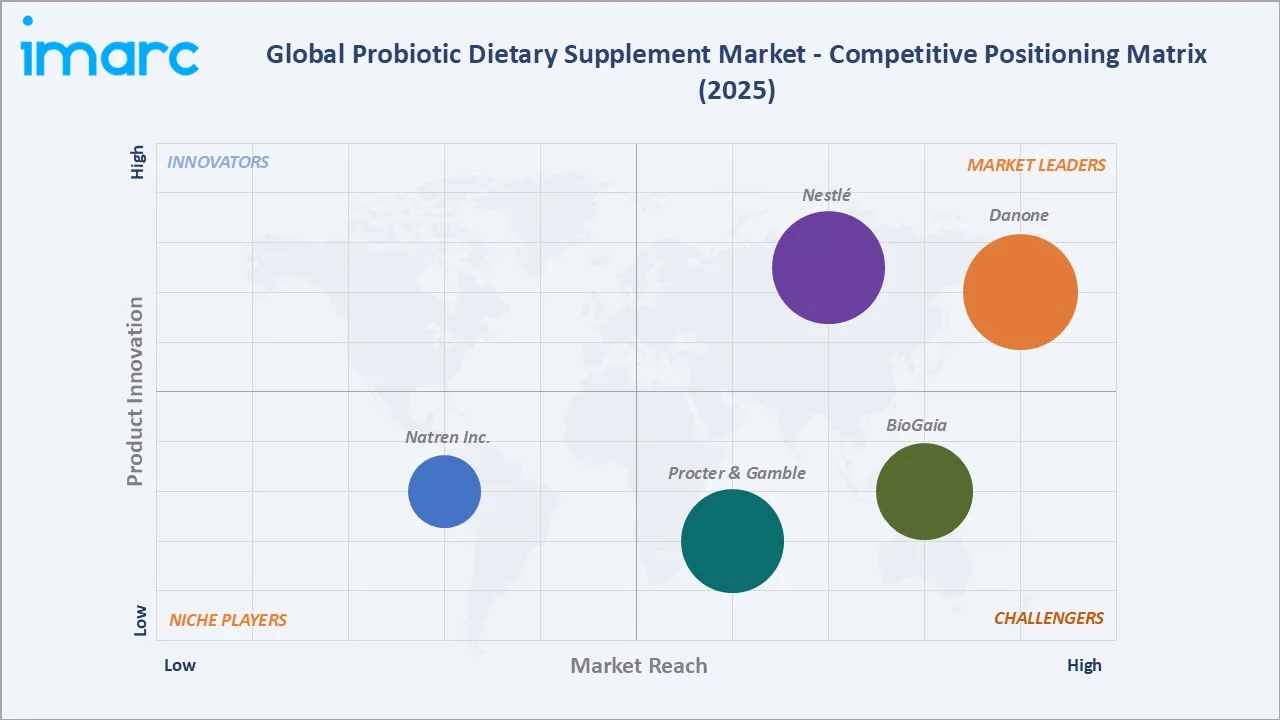

Competitive Landscape

The global probiotic dietary supplement market is highly competitive, characterized by the presence of multinational nutrition companies, specialty probiotic manufacturers, and emerging microbiome-focused brands. Competition is centered on strain efficacy, clinical validation, product stability, delivery technologies, and targeted health benefits such as digestive, immune, women's, and sports health.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

Danone |

Actimel, Activia |

Market Leader |

Danone plays a pioneering, market-leading role by integrating clinically backed probiotics, prebiotics, and postbiotics into everyday functional foods, specialized clinical nutrition, and early-life products. |

|

Nestlé |

Garden of Life |

Market Leader |

Nestlé plays a major role in the probiotic and dietary supplement industry through its medical and scientific branch, Nestlé Health Science. |

|

BioGaia |

BioGaia |

Strong Challenger |

BioGaia is a pioneering Swedish healthcare company and global leader in probiotic research. Its primary role in the dietary supplement industry is to develop and supply scientifically validated, single-strain probiotics designed to restore and maintain the natural microbial balance in the human body. |

|

Procter & Gamble |

Align Probiotic |

Strong Challenger |

Procter & Gamble operates as a major player in the probiotic dietary supplement market primarily through its flagship digestive health brand, Align. |

|

Natren Inc. |

Natren |

Niche Player |

Natren, Inc. is a pioneering leader in the probiotic dietary supplement industry, recognized for introducing the term "probiotics" and popularizing it globally. |

Companies are investing heavily in personalized nutrition, microbiome research, synbiotic formulations, and innovative formats such as gummies, powders, and sachets. Strategic partnerships, acquisitions, direct-to-consumer channels, and e-commerce expansion are key growth strategies. Continuous product innovation and scientifically backed health claims remain critical factors for maintaining market share and brand differentiation.

Key Company Profiles

Danone

Danone is a global food and nutrition company with a strong presence in the probiotic and gut health segment through its science-based nutrition and health-focused product portfolio. The company is widely recognized for leveraging probiotic research, microbiome science, and clinically studied bacterial strains across its digestive health offerings.

- Key Brands: Actimel, Activia.

- Strategic Focus: Advancing gut health, microbiome science, and preventive nutrition through research-backed probiotic solutions.

Nestlé

Nestlé is one of the world's largest nutrition, health, and wellness companies, with a significant presence in the probiotic dietary supplement market through its science-driven nutrition and health businesses. The company leverages extensive expertise in microbiome research, functional nutrition, and clinical science to develop products supporting digestive health, immunity, and overall wellness.

- Key Brands: Garden of Life.

- Strategic Focus: Centered on microbiome science, personalized nutrition, and preventive healthcare solutions.

Market Concentration Analysis

The probiotic dietary supplement market is moderately fragmented, with global nutrition companies, pharmaceutical firms, specialty probiotic players, and D2C wellness brands competing across formats and health claims. Large companies such as Danone, Nestlé, BioGaia, Procter & Gamble, and Natren Inc. benefit from strong brand recognition, R&D capabilities, and wide distribution networks. Smaller microbiome-focused brands compete through targeted formulations, personalized probiotics, synbiotics, women’s health products, and gummy formats. Competition is increasingly based on strain validation, CFU stability, delivery technology, clinical evidence, and digital sales channels.

Investment & Growth Opportunities

Highest Growth Segments

Online stores (~8.3% CAGR), probiotic drops (~7.2% CAGR), powder stick pack (~6.4% CAGR), Asia-Pacific (~6.5% CAGR through China and India), psychobiotic mental health (~10-12% CAGR from emerging segment), and women's vaginal health probiotic (~8-10% CAGR) represent probiotic dietary supplement highest-growth investment vectors through 2034.

Investment Themes

- D2C personalized microbiome probiotic subscription: This is an attractive investment theme because consumers are increasingly seeking personalized wellness solutions based on gut microbiome profiles, lifestyle, and health goals. Subscription-based models create recurring revenue streams, improve customer retention, and enable brands to deliver tailored probiotic formulations through direct-to-consumer channels.

- Infant and pediatric probiotic drops: This is a promising investment theme due to growing parental awareness of the role of gut health in infant digestion, immunity, and overall development. Rising demand for clinically validated, easy-to-administer probiotic drops for newborns and young children is creating opportunities for specialized pediatric nutrition and healthcare brands.

Future Market Outlook (2026-2034)

The global probiotic dietary supplement market is projected to grow from USD 8.22 Billion in 2025 to USD 13.29 Billion by 2034, delivering a 5.33% CAGR over the forecast period through microbiome science mainstreaming, psychobiotic gut-brain axis research, D2C personalized probiotic subscription, infant and pediatric drops clinical expansion, and Asia-Pacific gut health awareness. The market's anchor value of USD 10.65 Billion in 2030 represents probiotic supplements at clinical and digital inflection.

Three structural forces define probiotic dietary supplement growth through 2034: rising consumer awareness of gut health and the microbiome, increasing demand for preventive healthcare and immunity support, and rapid innovation in personalized nutrition. Growth is further supported by D2C subscriptions, novel formats such as gummies and drops, and expanding use of probiotics across women’s health, pediatric care, sports nutrition, and healthy aging.

Research Methodology

Primary Research

Primary research comprised interviews with probiotic supplement manufacturers, microbiome researchers, nutrition experts, healthcare professionals, distributors, and retail channel participants. Discussions focused on consumer preferences, strain selection, formulation trends, pricing, distribution strategies, and emerging health applications.

Secondary Research

Secondary research encompassed company websites, annual reports, product brochures, investor presentations, industry publications, and regulatory databases. It also included reviewing scientific papers, microbiome research studies, supplement trade data, retail channel insights, and government health statistics.

Forecasting Models

Forecasting models combined historical sales performance, supplement consumption trends, healthcare expenditure patterns, and probiotic adoption rates to estimate future market growth. Quantitative techniques such as CAGR analysis, demand forecasting, and market penetration modeling were integrated with qualitative assessments of microbiome research, product innovation, and consumer wellness trends. Scenario analysis and expert validation were applied to ensure robust projections through 2034.

Probiotic Dietary Supplement Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Forms Covered | Powder Stick Pack, Capsule, Tablet, Probiotic Drops |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Pharmacy and Health Stores, Online Stores, Others |

| Applications Covered | Food Supplement, Nutritional Supplements, Specialty Nutrients, Infant Formula, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Danone, Nestlé, BioGaia, Procter & Gamble, Natren Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the probiotic dietary supplement market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global probiotic dietary supplement market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the probiotic dietary supplement industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Probiotic Dietary Supplement Market Report

The global probiotic dietary supplement market reached USD 8.22 Billion in 2025, driven by rising consumer awareness of gut health, digestive wellness, immunity support, and preventive healthcare. Growth is further supported by increasing demand for microbiome-based nutrition, personalized probiotic formulations, and synbiotic products. Expanding e-commerce, D2C subscriptions, and novel formats such as gummies, powders, and drops are also accelerating market adoption.

The global probiotic dietary supplement market grows at 5.33% CAGR during 2026-2034, reaching USD 13.29 Billion by 2034. The CAGR reflects microbiome science mainstreaming, psychobiotic gut-brain axis, D2C personalized subscription, infant drops clinical, and Asia-Pacific awareness.

Capsule leads at 38.7% due to their convenience, accurate dosage, and strong consumer acceptance. They help protect probiotic strains from moisture, oxygen, and stomach acid, improving survivability and potency. Capsules also offer better shelf stability and are widely preferred by adults seeking daily digestive and immunity support.

Pharmacy and health stores lead at 36.8% due to strong consumer trust, product authenticity, and access to expert recommendations. These channels are preferred for health-focused purchases, especially digestive, immunity, women’s health, and pediatric probiotic supplements. Their wide product availability and credibility help drive repeat purchases and brand loyalty.

Europe leads at 32.6% due to high consumer awareness of gut health, digestive wellness, and preventive healthcare. The region benefits from mature pharmacy and health store channels, strong product quality standards, and widespread acceptance of probiotic supplements. Rising demand for immunity support, microbiome-based nutrition, and clinically validated formulations further strengthens Europe’s market leadership.

Leading companies include Danone, Nestlé, BioGaia, Procter & Gamble, and Natren Inc., among others.

The market is projected to reach approximately USD 10.65 Billion by 2030, reflecting steady growth in gut health, immunity, and preventive wellness demand. Growth will be supported by wider adoption of capsules, gummies, powders, and personalized probiotic formulations. Expanding pharmacy, health store, e-commerce, and D2C channels will further strengthen market penetration.

Three priority investment opportunities include D2C personalized microbiome probiotic subscriptions, which leverage microbiome analytics and recurring revenue models to improve customer retention. Infant and pediatric probiotic drops represent a high-growth segment driven by increasing parental focus on digestive and immune health from an early age. Additionally, synbiotic and postbiotic combination supplements offer strong potential as consumers seek science-backed, multi-functional solutions for gut health, immunity, and overall wellness.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade