Programmable Logic Controller (PLC) Market Size, Share, Trends and Forecast by Type, End Use Industry, and Region, 2026-2034

Global Programmable Logic Controller (PLC) Market Size, Share, Trends & Forecast (2026-2034)

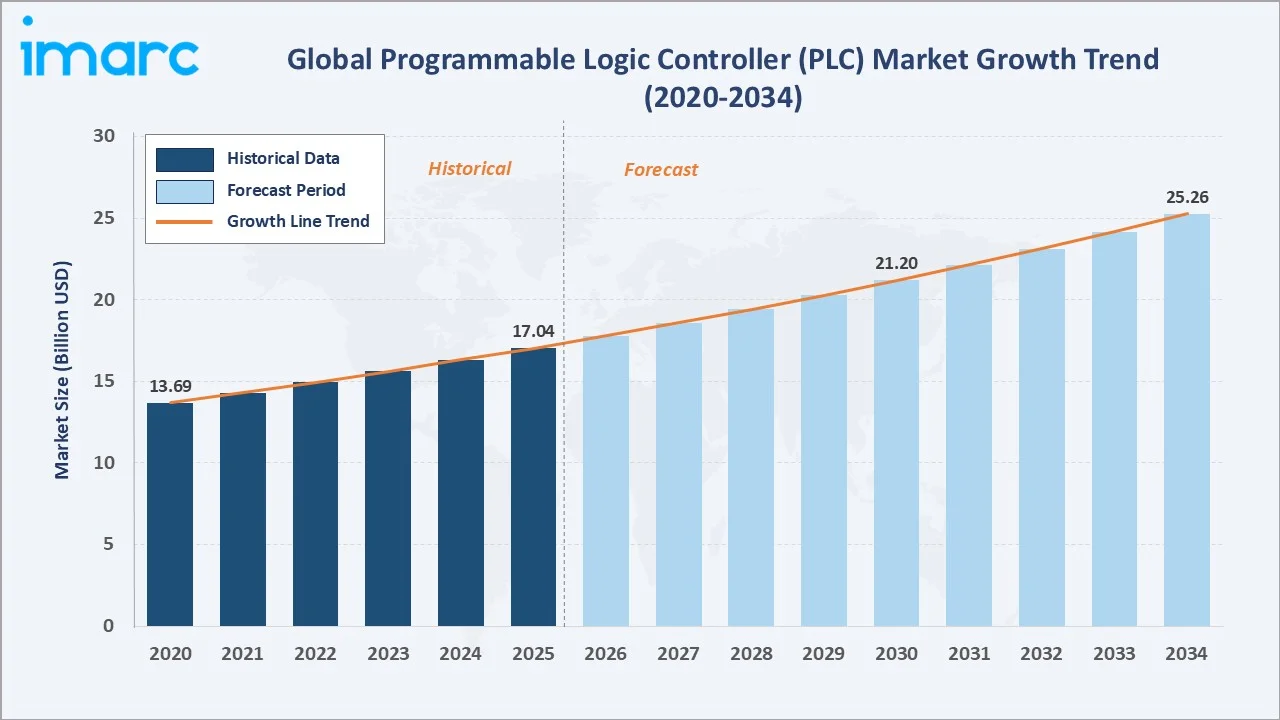

The global programmable logic controller (PLC) market size was valued at USD 17.00 Billion in 2025 and is projected to reach USD 25.26 Billion by 2034, exhibiting a CAGR of 4.47% during the forecast period 2026-2034. Accelerating Industry 4.0 adoption, smart factory rollouts, the integration of edge AI and IIoT into discrete and process automation, and rising investment in software-defined automation are driving the programmable logic controller market growth. Hardware and Software lead the type segment with a 68.0% share in 2025, while Automotive dominates end-use industries at 18.0%. Asia-Pacific accounts for 41.0% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 17.00 Billion |

|

Forecast Market Size (2034) |

USD 25.26 Billion |

|

CAGR (2026-2034) |

4.47% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (41.0% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Type |

Hardware and Software (68.0%, 2025) |

|

Leading End-Use Industry |

Automotive (18.0%, 2025) |

The global programmable logic controller market growth trajectory from 2020 through 2034 contrasts a steady historical expansion base against a sustained forecast curve powered by Industry 4.0 build-out, EV manufacturing automation, and the migration to software-defined controllers.

To get more information on this market, Request Sample

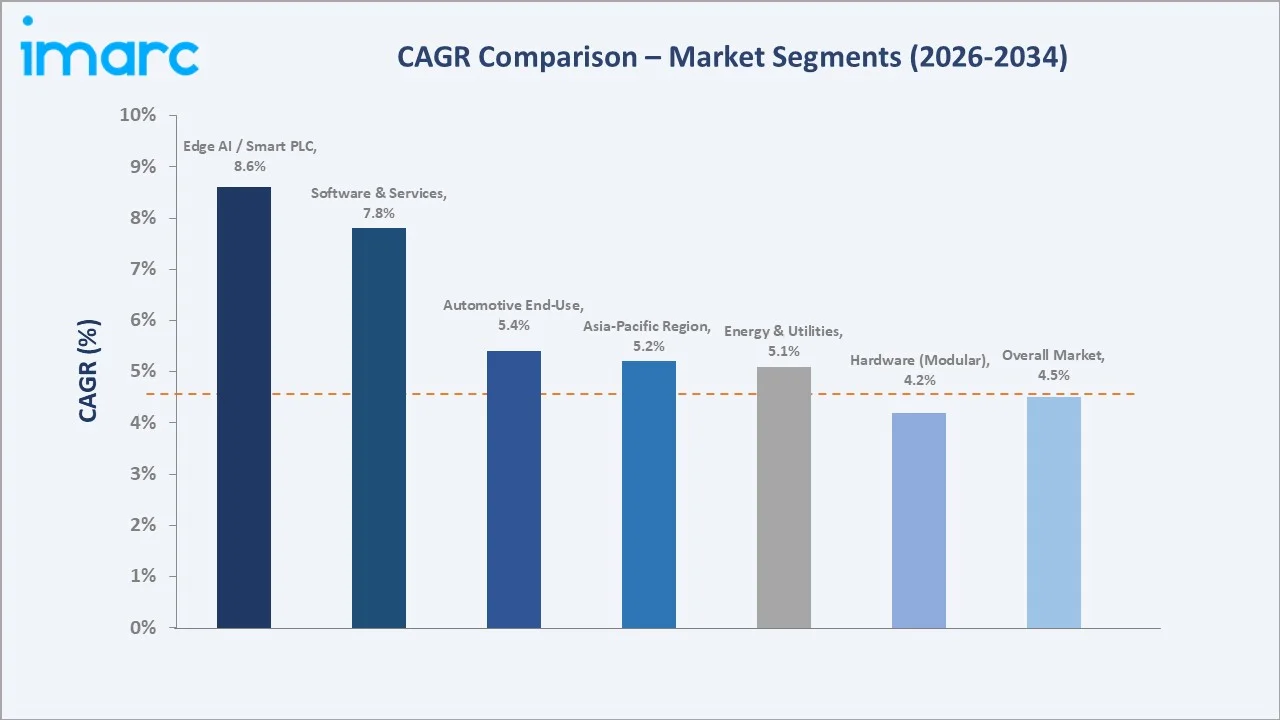

Segment-level CAGR comparisons highlight Edge AI / Smart PLC and Software & Services as the two fastest-growing technology sub-categories within the global programmable logic controller (PLC) industry analysis through 2034.

Executive Summary

The global programmable logic controller (PLC) market is undergoing a structural shift driven by Industry 4.0 adoption, software-defined automation, and the convergence of operational technology with information technology. Valued at USD 17.00 Billion in 2025, the market is projected to reach USD 25.26 Billion by 2034 at a CAGR of 4.47%. Demand is anchored in factory modernization, EV battery line build-out, and renewable energy plant automation, with edge analytics and cybersecurity becoming standard PLC capabilities.

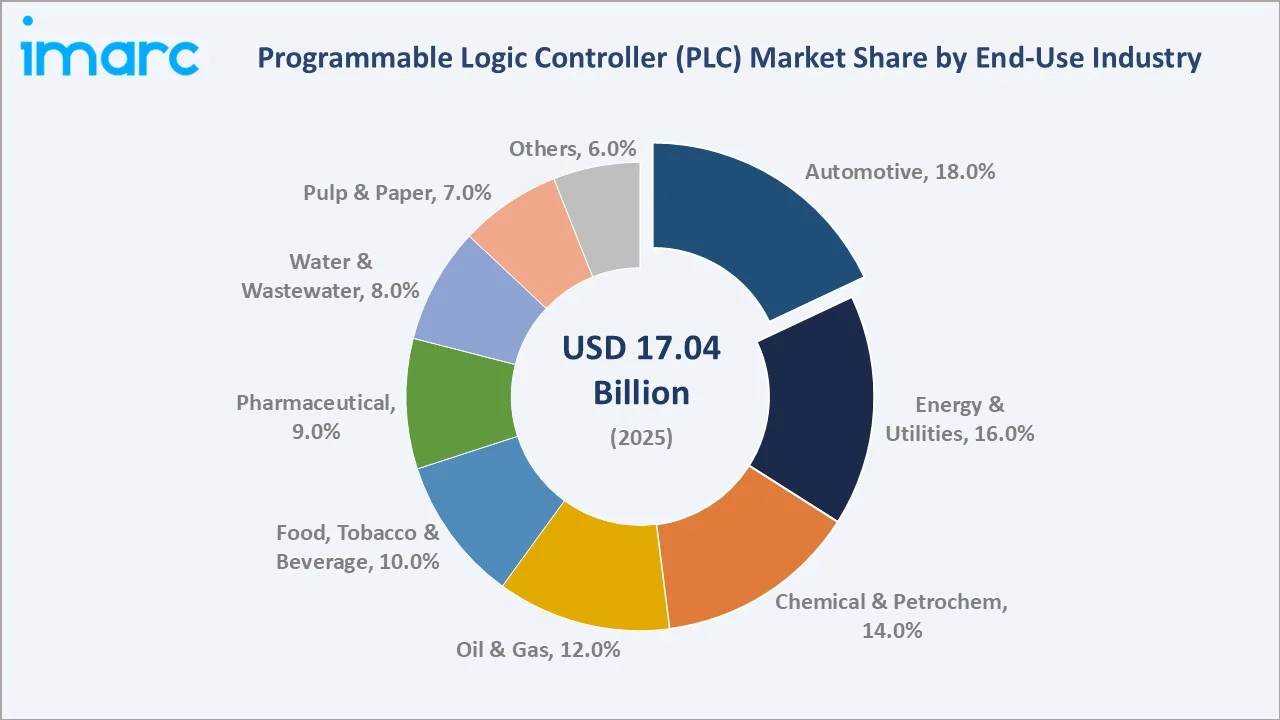

Hardware and Software collectively command 68.0% share in 2025, reflecting the indispensable role of compact, modular, and rack-mounted controllers in discrete and process industries. Services account for 32.0%, supported by rising demand for system integration, predictive maintenance, and PLC programming expertise as control architectures grow more complex. Automotive leads end-use industries at 18.0%, followed by Energy and Utilities at 16.0% and Chemical and Petrochemical at 14.0%.

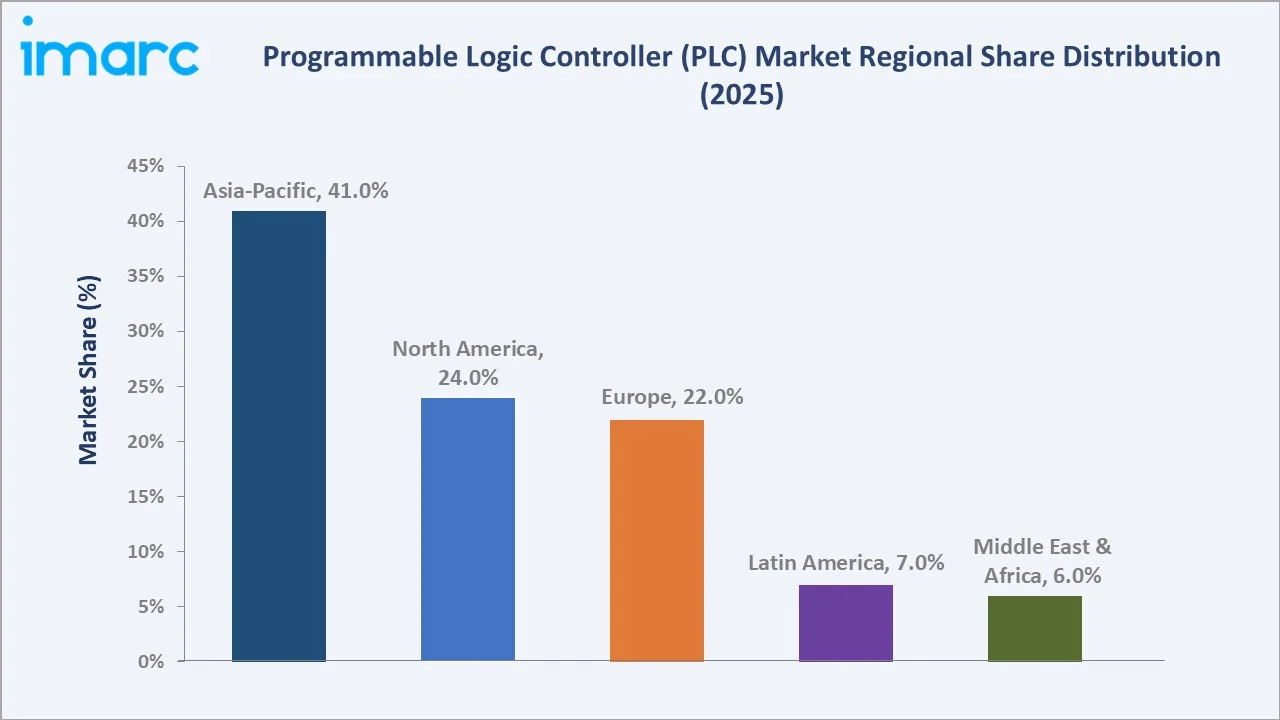

Asia-Pacific dominates with 41.0% of global revenue in 2025, propelled by China's manufacturing scale, India's industrial corridor program, and Japan's deterministic control technology leadership. North America (24.0%) and Europe (22.0%) anchor demand through advanced regulatory frameworks, software-defined automation pilots, and reshoring initiatives. Latin America (7.0%) and Middle East and Africa (6.0%) remain emerging but high-potential markets driven by oil and gas, water treatment, and infrastructure investment.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Hardware and Software – 68.0% share (2025) |

|

Leading End-Use Industry |

Automotive – 18.0% share (2025) |

|

Leading Region |

Asia-Pacific – 41.0% revenue share (2025) |

|

Second Region |

North America – 24.0% revenue share (2025) |

|

Top Companies |

Siemens, Rockwell Automation, Schneider Electric, Mitsubishi Electric Corporation, ABB, OMRON Corporation |

|

Market Opportunity |

Software-defined automation, vPLC, edge AI |

Key Analytical Observations Supporting The Data Above:

- Hardware and Software command 68.0% share in 2025 due to the dominance of modular and compact PLC architectures across automotive, energy, and discrete manufacturing applications worldwide.

- The Automotive segment leads end-use at 18.0% in 2025, fuelled by EV battery manufacturing build-out, robotic assembly automation, and the ongoing transition toward software-defined production lines.

- Asia-Pacific's 41.0% global dominance reflects China's vehicle production scale of over 27 million units in 2024, India's PLI scheme rollout, and concentrated Tier-1 automation supply in Japan and South Korea.

- Software-defined PLC platforms, including Siemens' virtual PLC and Rockwell's Logix Edge, are emerging as the most disruptive opportunity area, decoupling control logic from proprietary hardware.

Global Programmable Logic Controller (PLC) Market Overview

Programmable logic controllers are ruggedized industrial computers designed to monitor sensor inputs, execute programmed control logic, and deliver real-time outputs to actuators, motors, valves, and machines on the factory floor. Modern PLC architectures span compact, modular, and rack-mounted formats, with rising integration of IIoT connectivity, OPC UA over TSN, edge analytics, and cybersecurity-by-design protocols compliant with IEC 62443.

Applications span the full industrial value chain, including automotive assembly, oil and gas extraction, chemical processing, food and beverage packaging, water and wastewater treatment, pharmaceutical batching, pulp and paper, and renewable energy plant control. Macroeconomic enablers include the global Industry 4.0 transition, the reshoring of manufacturing in North America and Europe, the EV revolution, and aggressive smart-factory build-out across the Asia-Pacific.

Market Dynamics

To evaluate market opportunities, Request Sample

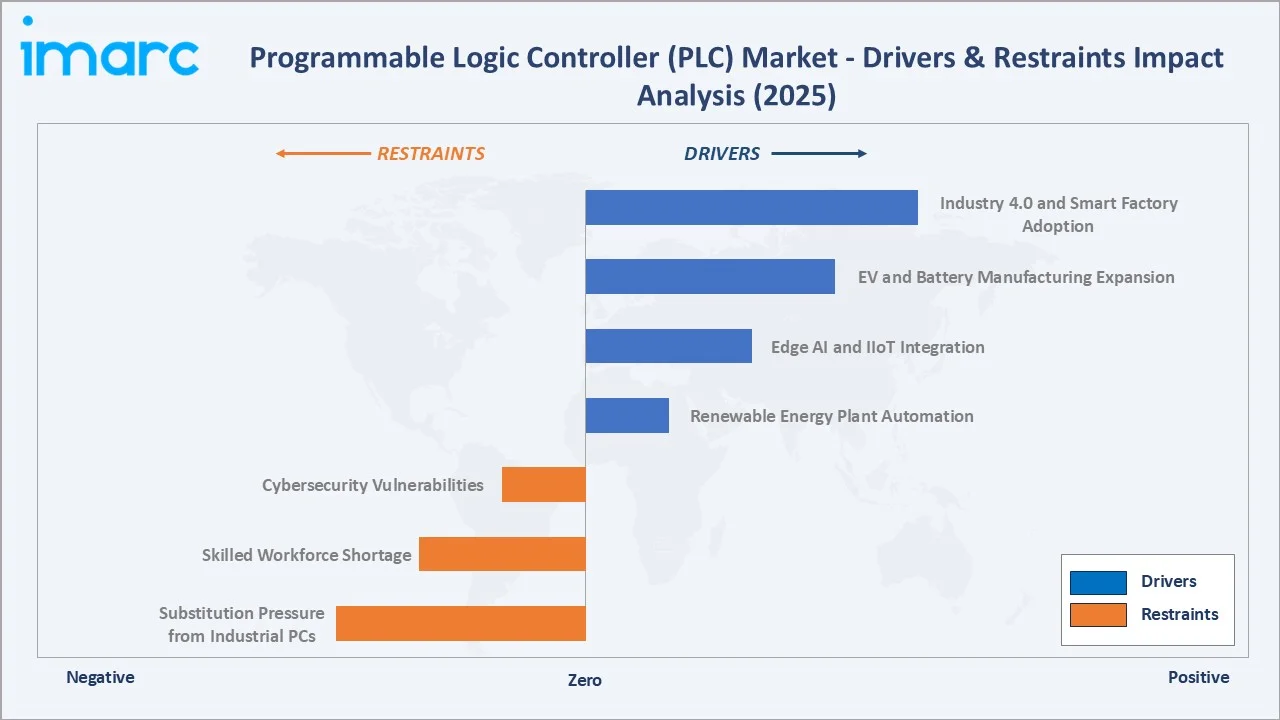

Market Drivers

- Industry 4.0 and Smart Factory Adoption: Industrial automation deployment is accelerating across discrete and process manufacturing, with global smart manufacturing reaching USD 175 Billion in 2025 (IoT Analytics), creating sustained PLC demand for interconnected machine control and real-time data exchange.

- EV and Battery Manufacturing Expansion: Global electric car sales topped 17 million in 2024 (IEA), and EV gigafactories require dense PLC deployment for cell stacking, formation, packaging, and high-precision robotic assembly across new and retrofit lines.

- Edge AI and IIoT Integration: PLCs are evolving from fixed-function controllers into edge analytics nodes, enabling anomaly detection, predictive maintenance, and direct cloud connectivity through OPC UA and MQTT protocols at the machine level.

Market Restraints

- Cybersecurity Vulnerabilities: As PLCs are integrated into IIoT and cloud systems, attack surfaces expand. The EU Cyber Resilience Act of 2024 requires OEMs to certify security-by-design, raising compliance costs for legacy PLC vendors.

- Skilled Workforce Shortage: Advanced PLC programming, particularly in IEC 61131-3 structured text and Codesys-based environments, faces a persistent talent gap, lengthening project deployment cycles.

Market Opportunities

- Software-Defined Automation (SDA) and Virtual PLCs: The shift from proprietary hardware-locked controllers to virtualised PLC runtimes hosted on industrial PCs represents the most disruptive opportunity area, allowing OEMs to deploy and update control logic flexibly.

- Renewable Energy Plant Automation: Wind, solar, and battery storage projects globally are creating new PLC demand for grid-tied control, inverter management, and SCADA integration in distributed energy assets.

Market Challenges

- Substitution Pressure from Industrial PCs and DCS: PC-based control systems and distributed control systems are gaining share in mid-complexity applications, compressing PLC pricing in select segments.

- Supply Chain and Tariff Volatility: Semiconductor input cost swings and 2025 tariff uncertainty have introduced project deferral risk in price-sensitive emerging markets.

Emerging Market Trends

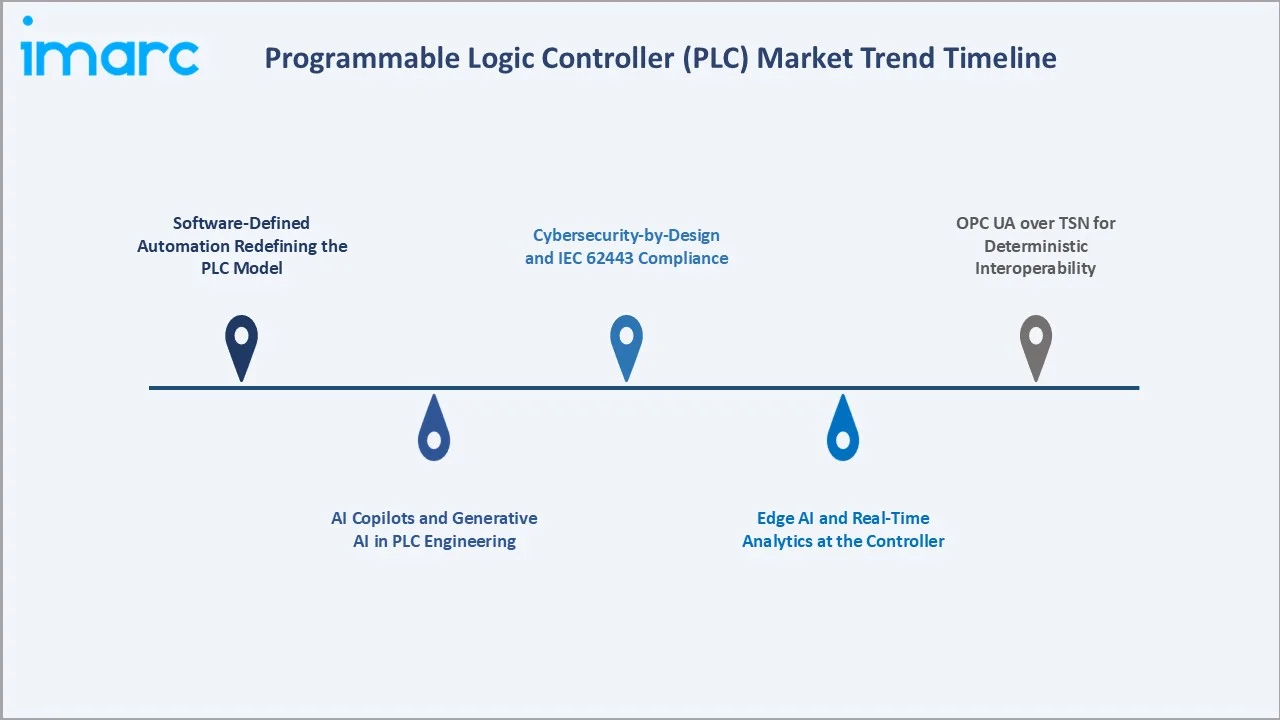

1. Software-Defined Automation Redefining the PLC Model

The PLC market is undergoing a fundamental shift from hardware-locked controllers to software-defined automation platforms. At SPS 2025, Siemens unveiled two new virtual PLC versions running on its Industrial Edge platform, while Rockwell Automation announced its Logix Edge software-defined controller targeted for Q4 2026. This decoupling of control logic from proprietary hardware enables OEMs to flexibly deploy, update, and manage automation workloads across industrial PCs.

2. AI Copilots and Generative AI in PLC Engineering

Industrial AI is being embedded directly into PLC engineering workflows. Siemens has committed over EUR 1 billion to industrial AI capabilities over the next three years and released over 20 industrial copilots, including the Siemens Engineering Copilot, which helps engineers generate and debug PLC code. Generative AI is accelerating commissioning time and bridging the OT skills gap.

3. Cybersecurity-by-Design and IEC 62443 Compliance

The 2024 EU Cyber Resilience Act and NIS2 Directive are reshaping PLC product roadmaps. Phoenix Contact's PLCnext Technology platform achieved IEC 62443 certification in 2025, and Rockwell's new ControlLogix 5590 ships with built-in cybersecurity. Security-by-design is moving from a premium feature to a baseline requirement across all PLC tiers.

4. Edge AI and Real-Time Analytics at the Controller

PLCs are increasingly hosting edge AI workloads for anomaly detection, predictive maintenance, and quality inspection. Mitsubishi Electric's Maisart AI platform and Siemens' Simatic AI offerings illustrate the convergence of deterministic control with machine learning, reducing latency and bandwidth dependency on cloud infrastructure.

5. OPC UA over TSN for Deterministic Interoperability

Time-Sensitive Networking with OPC UA is enabling vendor-agnostic, deterministic communication across PLCs, drives, and HMIs. As OPC UA over TSN matures in 2025-2026, hardware commoditisation accelerates, shifting differentiation toward software toolchains, ecosystem partners, and lifecycle support.

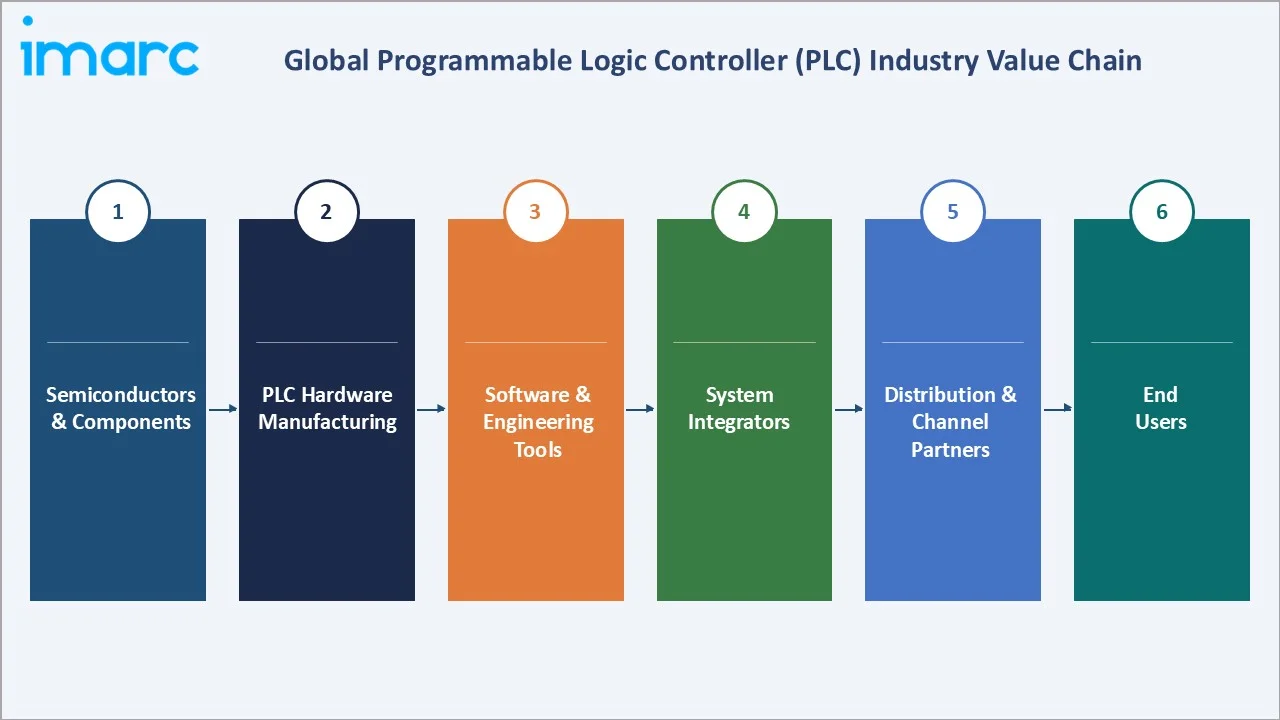

Industry Value Chain Analysis

The programmable logic controller (PLC) value chain spans semiconductor input through end-user deployment, with each stage exhibiting distinct margin and competitive dynamics.

|

Stage |

Key Players / Examples |

|

Semiconductors and Components |

Capital-intensive and consolidated, with margins protected by scale but exposed to cyclicality and geopolitical supply risk. Automation-grade chips increasingly dictate PLC performance benchmarks. |

|

PLC Hardware Manufacturing |

The highest-value and most concentrated stage, dominated by a few global OEMs. Margins are protected by long lifecycles, certification barriers, and ecosystem lock-in, with differentiation shifting toward edge computing and IIoT-native designs. |

|

Software and Engineering Tools |

A rapidly appreciating layer offering recurring revenue and the stickiest customer lock-in. Margins exceed those of hardware, though open, hardware-agnostic platforms like Codesys are pressuring proprietary incumbents. |

|

System Integrators |

A fragmented, services-driven segment where value comes from domain expertise and project execution rather than IP. Margins are moderate and project-based, with consolidation accelerating around multinational contracts. |

|

Distribution and Channel Partners |

Volume-driven and relatively low-margin, providing geographic reach and technical support. Channel economics are under pressure from direct sales and digital procurement, shifting differentiation toward value-added services. |

|

End Users |

The demand-side anchor spans discrete and process industries. Automotive, energy, and oil & gas drive volume, while pharma and food & beverage grow fastest, with end-user specifications increasingly reshaping upstream product design. |

PLC hardware manufacturers occupy the highest-value position in the chain due to their control of platform architecture, ecosystem integration, and long-cycle OEM relationships. However, value is migrating toward software toolchains and engineering services as software-defined automation accelerates.

Technology Landscape in the Programmable Logic Controller Industry

Hardware Architecture Innovation

Modular PLCs anchor large-plant deployments due to I/O scalability and field-replaceable expansion modules. Compact PLCs serve stand-alone machines and packaging lines, while distributed PLCs deliver fault-tolerant control in oil refineries and power generation.

Software-Defined and Virtualized Control

The transition to software-defined architectures is being led by Siemens' virtual PLC running on Industrial Edge, Rockwell's Logix Edge platform announced for Q4 2026, and the Codesys ecosystem. Hypervisor-based runtimes deliver deterministic performance on standard industrial PCs.

Connectivity, Edge AI, and Cybersecurity

OPC UA over TSN, MQTT, and 5G are converging to enable seamless OT-IT data exchange. Edge AI in next-generation PLCs allows on-device analytics for predictive maintenance, while IEC 62443 and the EU Cyber Resilience Act 2024 are driving baseline cybersecurity integration.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the global programmable logic controller (PLC) market, with forecasts at the global, regional, and country levels for 2026-2034. The market has been categorized based on type and end-use industry.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Hardware and Software | 68.0% | 2025 |

| End Use Industry | Automotive | 18.0% | 2025 |

| Region | Asia-Pacific | 41.0% | 2025 |

By Type

To evaluate market opportunities, Request Sample

Hardware and Software hold a 68.0% share of the global programmable logic controller (PLC) market in 2025. The dominance reflects the indispensable role of physical control hardware paired with engineering software across modular, compact, and rack-mounted architectures. Demand is anchored in discrete manufacturing automation, particularly in automotive assembly, electronics, and food and beverage packaging, where deterministic real-time control is mission-critical. Modular PLCs, supported by their scalability across complex multi-cell production environments, continue to drive a substantial portion of this segment. Services account for the remaining 32.0% and represent the fastest evolving sub-segment, supported by demand for system integration, retrofit modernization, predictive maintenance contracts, and PLC programming expertise. The skilled workforce shortage and growing complexity of cybersecurity-compliant deployments are extending services revenue per project, particularly in regulated process industries.

By End-Use Industry

Automotive leads the end-use industry segment with an 18.0% share in 2025, supported by EV battery gigafactory build-out, robotic assembly automation, and software-defined production lines. Global vehicle production exceeded 92.5 million units in 2024, with EV sales contributing over 17 million units (IEA), each requiring denser PLC deployment than ICE platforms. Energy and Utilities follows at 16.0%, driven by renewable plant automation, smart grid integration, and substation control modernization. Chemical and Petrochemical accounts for 14.0%, anchored in continuous batch process control and safety instrumented systems. Oil and Gas (12.0%) deploys PLCs across upstream extraction, midstream pipeline control, and downstream refining. Food, Tobacco, and Beverage (10.0%), Pharmaceutical (9.0%), Water and Wastewater Treatment (8.0%), and Pulp and Paper (7.0%) round out the remaining major end-use industries, with Others contributing 6.0%.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

41.0% |

China NEV manufacturing scale, India PLI scheme, Japan deterministic control leadership, ASEAN smart factory build-out |

|

North America |

24.0% |

Reshoring, USD 13M DoE smart manufacturing investment 2025, Industry 4.0 retrofits, software-defined automation pilots |

|

Europe |

22.0% |

EU Cyber Resilience Act 2024, German automotive automation, sustainability, and energy efficiency mandates |

|

Latin America |

7.0% |

Brazil and Mexico nearshoring, oil and gas projects, food and beverage packaging modernization |

|

Middle East and Africa |

6.0% |

Saudi Vision 2030 smart industry pillar, GCC water and wastewater investment, and mining sector automation |

Asia-Pacific commands a 41.0% share in 2025, the most dominant regional position globally. China is the single most important national market, combining the world's largest vehicle production volume of over 27 million units in 2024 with aggressive subsidy-backed factory automation upgrades. India's PLI scheme and industrial corridor build-outs are driving first-time PLC deployment, while Japan's Quality 4.0 initiatives sustain demand for nano-second-deterministic controllers.

North America (24.0%) is led by U.S. reshoring momentum and software-defined automation pilots, supported by USD 13 million in DoE smart manufacturing investment in 2025. Europe (22.0%) is shaped by the EU Cyber Resilience Act, German automotive Tier-1 demand, and decarbonization-driven energy management investments.

Competitive Landscape

|

Company |

Brand / Offerings |

Position |

Core Strength |

|

Siemens |

SIMATIC Automation |

Leader |

Industrial AI, software-defined automation, Industrial Edge platform |

|

Rockwell Automation |

Allen‑Bradley |

Leader |

North America strength, integrated cybersecurity, FactoryTalk software |

|

Schneider Electric |

Modicon |

Leader |

Energy and infrastructure focus, sustainability, India footprint |

|

Mitsubishi Electric Corporation |

Programmable Controllers MELSEC |

Leader |

Japan and ASEAN dominance, CC-Link IE TSN ecosystem |

|

ABB |

AC500 / Automation Builder |

Leader |

Process industries, robotics integration, Europe presence |

|

OMRON Corporation |

NX / NJ Series |

Challenger |

Machine automation, vision integration, AI-enabled control |

|

Honeywell International Inc. |

ControlEdge PLC |

Challenger |

Process industries, oil and gas, and building automation |

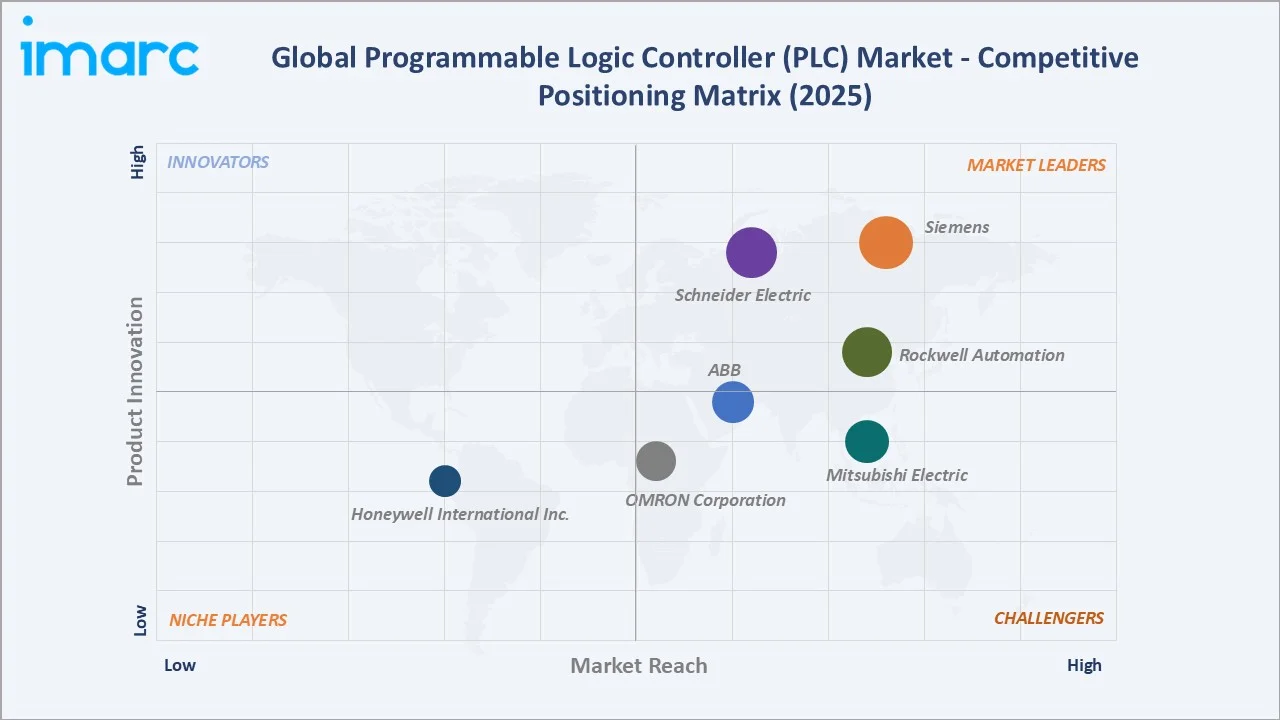

The global programmable logic controller (PLC) competitive landscape is moderately concentrated, with the top five vendors collectively accounting for an estimated 70-77% of global revenue in 2025. Siemens AG retained market leadership with over 20% share, supported by its SIMATIC platform breadth and TIA Portal ecosystem. Software-defined automation is reshaping competitive dynamics as Siemens, Rockwell, and Schneider invest heavily in virtualised PLC runtimes and AI-augmented engineering.

Key Company Profiles

Siemens

Germany-based Siemens is anchored by its SIMATIC controller portfolio and TIA Portal engineering platform, with EUR 1 billion in industrial AI investment through 2028.

- Product & Platform Portfolio: SIMATIC S7-1200 G2, S7-1500, virtual PLC (vPLC), TIA Portal, Industrial Edge platform, Simatic AX engineering.

- Recent Developments: In January 2026, Siemens and NVIDIA expanded their partnership to build the Industrial AI Operating System, reinventing the entire end-to-end industrial value chain through AI – from design and engineering to manufacturing, production, operations, and into supply chains.

- Strategic Focus: Siemens prioritises software-defined automation through vPLC and Industrial Edge, AI-augmented engineering via 20+ industrial copilots, and zero-trust OT security, converting hardware leadership into a recurring software platform business through Xcelerator.

Rockwell Automation

U.S.-based Rockwell Automation anchors the North American PLC market through its Allen-Bradley ControlLogix and CompactLogix families, with growing momentum in software-defined controllers and cybersecurity.

- Product & Platform Portfolio: Allen-Bradley ControlLogix 5590, CompactLogix, Micro800, Logix Edge software-defined controller, Studio 5000 engineering, FactoryTalk software suite.

- Recent Developments: In October 2025, Rockwell Automation, Inc. announced the highly anticipated launch of its newest controller, ControlLogix 5590, the powerhouse at the core of the Logix platform.

- Strategic Focus: Rockwell prioritises North American smart-factory leadership through FactoryTalk, software-defined controller migration via Logix Edge, and deep integration with hyperscaler cloud platforms for predictive maintenance and digital twin offerings.

Schneider Electric

France-based Schneider Electric delivers PLC solutions through its Modicon family and EcoStruxure platform, with strong positions in energy management and emerging market manufacturing build-out.

- Product & Platform Portfolio: Modicon M580, M340, M221, Momentum controllers, EcoStruxure Control Expert engineering, EcoStruxure Machine Expert.

- Recent Developments: In May 2023, Schneider Electric performed the groundbreaking ceremony of its new manufacturing plant at Prospace Industrial Park Pvt Ltd., in Kolkata. The plant would be spread over 9 acres and would involve an investment of INR 140 crores.

- Strategic Focus: Schneider's strategy is anchored in energy-and-sustainability-led automation, deep India market expansion, and convergence of power management and process control through EcoStruxure for renewable energy and grid-edge applications.

Market Concentration Analysis

The global programmable logic controller (PLC) market exhibits moderate-to-high concentration. The top five players, Siemens, Rockwell Automation, Schneider Electric, Mitsubishi Electric Corporation, and ABB, collectively held an estimated 70-77% of global revenue in 2025, with Siemens alone commanding over 20% market share.

The market is bifurcating along regional and architectural lines. At the global premium tier, consolidation is intensifying as software-defined automation requires sustained R&D investment that only the largest vendors can support. Concurrently, Chinese domestic suppliers and Codesys-based open-platform startups are creating new fragmentation pressure in mid-tier segments and emerging markets.

Investment & Growth Opportunities

Fastest-Growing Segments

Software and services represent the highest-growth sub-segment of the programmable logic controller (PLC) market, supported by virtual PLC platforms, predictive maintenance contracts, and cybersecurity compliance services. EV battery manufacturing automation and renewable energy plant control are the fastest-growing end-use sub-segments through 2034.

Emerging Market Expansion

India, ASEAN, the GCC, and Latin America offer the highest growth headroom. India's PLI scheme, ASEAN smart factory build-out, Saudi Vision 2030 industrial pillar, and Mexico nearshoring momentum each represent multi-year structural demand for first-time PLC deployment and modernization.

Venture and Strategic Investment Trends

Strategic investment activity in 2025-2026 includes Mitsubishi Electric's USD 120 million investment in Tulip Interfaces (January 2026), Schneider Electric's USD 167 million Kolkata plant (September 2024), and the Siemens-NVIDIA Industrial AI Operating System partnership announced at CES 2026.

Future Market Outlook (2026-2034)

The global programmable logic controller (PLC) market forecast projects steady value expansion from USD 17.00 Billion in 2025 to USD 25.26 Billion by 2034 at a CAGR of 4.47%. Growth is underpinned by Industry 4.0 build-out, EV manufacturing scale-up, software-defined automation adoption, and the integration of edge AI and cybersecurity-by-design capabilities.

Three structural shifts will reshape the competitive landscape through 2034. First, software-defined automation will progressively decouple control logic from proprietary hardware. Second, AI copilots and generative engineering tools will compress commissioning timelines and reduce the OT skills gap. Third, cybersecurity compliance under the EU Cyber Resilience Act and IEC 62443 will become baseline rather than premium, shifting differentiation toward platform openness.

By 2034, the programmable logic controller (PLC) industry is forecast to have transitioned from a hardware-centric controller market to a hybrid hardware-software platform economy, anchored in deterministic control, edge analytics, and ecosystem interoperability through OPC UA over TSN.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with PLC vendor product managers, system integrators, OEM automation leads, end-user plant engineering directors across automotive, energy, oil and gas, and chemical industries, and channel partners. Insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include vendor annual reports, IEA Global EV Outlook, ZVEI industry data, IoT Analytics Industrial Automation Reports, U.S. Department of Energy publications, EU Cyber Resilience Act 2024 documentation, IEC 62443 standards, OPC Foundation publications, and trade publications including Control Engineering, Automation World, and Industrial Ethernet Book.

Forecasting Models

Market sizing combined top-down and bottom-up approaches, incorporating industrial production indices, capex trends, and end-use industry build-out plans. Scenario analysis (base, optimistic, and conservative cases) accounted for tariff and macroeconomic uncertainty observed in 2025.

Programmable Logic Controller (PLC) Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered |

|

| End Use Industries Covered | Automotive, Energy and Utilities, Chemical and Petrochemical, Oil and Gas, Pulp and Paper, Pharmaceutical, Water and Wastewater Treatment, Food, Tobacco and Beverage, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Siemens, Rockwell Automation, Schneider Electric, Mitsubishi Electric Corporation, ABB, OMRON Corporation, Honeywell International Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the programmable logic controller (PLC) market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global programmable logic controller (PLC) market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the programmable logic controller (PLC) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Programmable Logic Controller (PLC) Market Report

The global programmable logic controller (PLC) market was valued at USD 17.00 Billion in 2025, supported by Industry 4.0 adoption, EV battery manufacturing automation, and software-defined controller deployment.

The market is projected to reach USD 25.26 Billion by 2034, growing at a CAGR of 4.47% during 2026-2034, driven by smart factory build-out, edge AI integration, and renewable energy plant automation.

Hardware and Software lead with a 68.0% share in 2025, anchored by modular and compact controller demand across automotive, energy, and discrete manufacturing applications. Services account for the remaining 32.0%.

Automotive leads with an 18.0% share in 2025, driven by EV battery gigafactories, robotic assembly automation, and software-defined production line build-out across global OEMs.

Asia-Pacific leads with a 41.0% share in 2025, driven by China's NEV manufacturing scale, India's PLI scheme rollout, Japan's deterministic control technology leadership, and ASEAN smart factory build-out.

Key drivers include Industry 4.0 adoption, EV battery manufacturing build-out (17M EVs sold globally in 2024 per IEA), edge AI and IIoT integration, and software-defined automation.

Software-defined automation is the fastest-growing trend.

Leading companies include Siemens, Rockwell Automation, Schneider Electric, Mitsubishi Electric Corporation, ABB, OMRON Corporation, and Honeywell International Inc.

Industrial AI copilots, including Siemens Engineering Copilot from a EUR 1 billion industrial AI investment, help engineers generate and debug PLC code, reducing commissioning timelines by 25-50% and bridging the persistent OT skills gap.

The 2024 EU Cyber Resilience Act and IEC 62443 are making cybersecurity-by-design a baseline requirement. Rockwell's ControlLogix 5590 with built-in IEC 62443 cybersecurity and Phoenix Contact's certified PLCnext platform exemplify this shift.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade