Protein Bar Market Size, Share, Trends and Forecast by Source, Type, Distribution Channel, and Region, 2026-2034

Global Protein Bar Market Size, Share, Trends & Forecast (2026-2034)

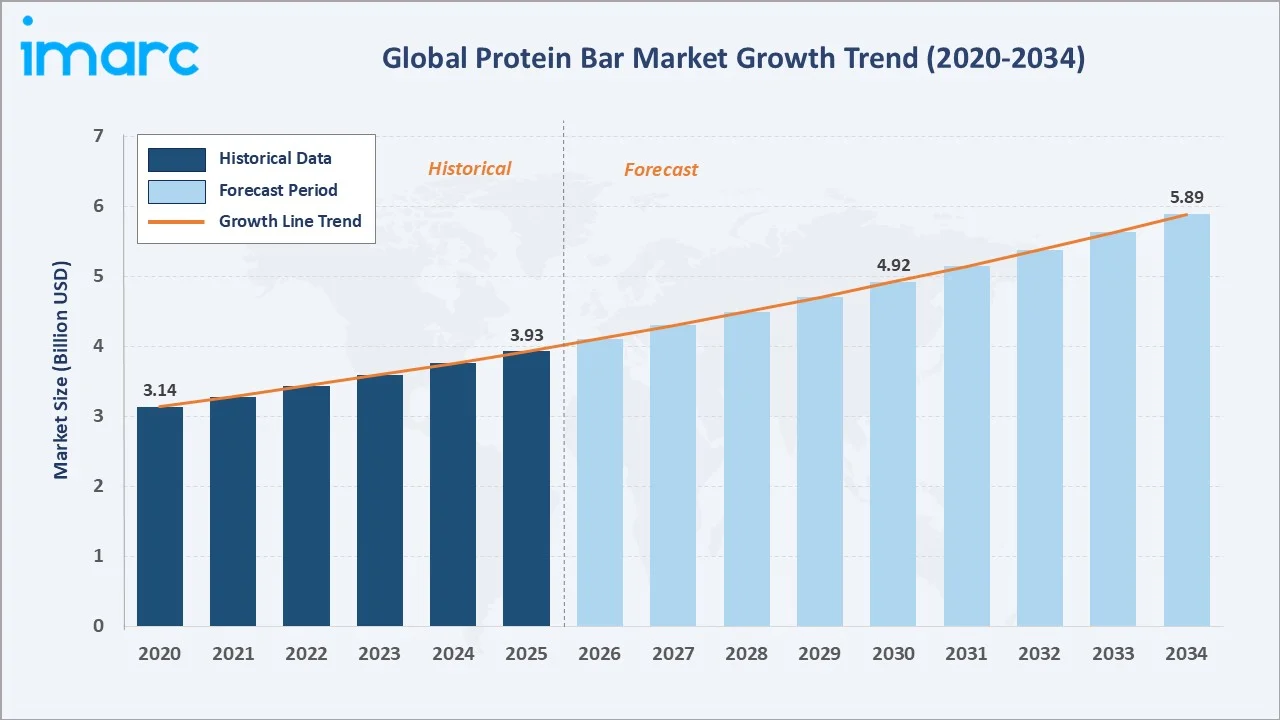

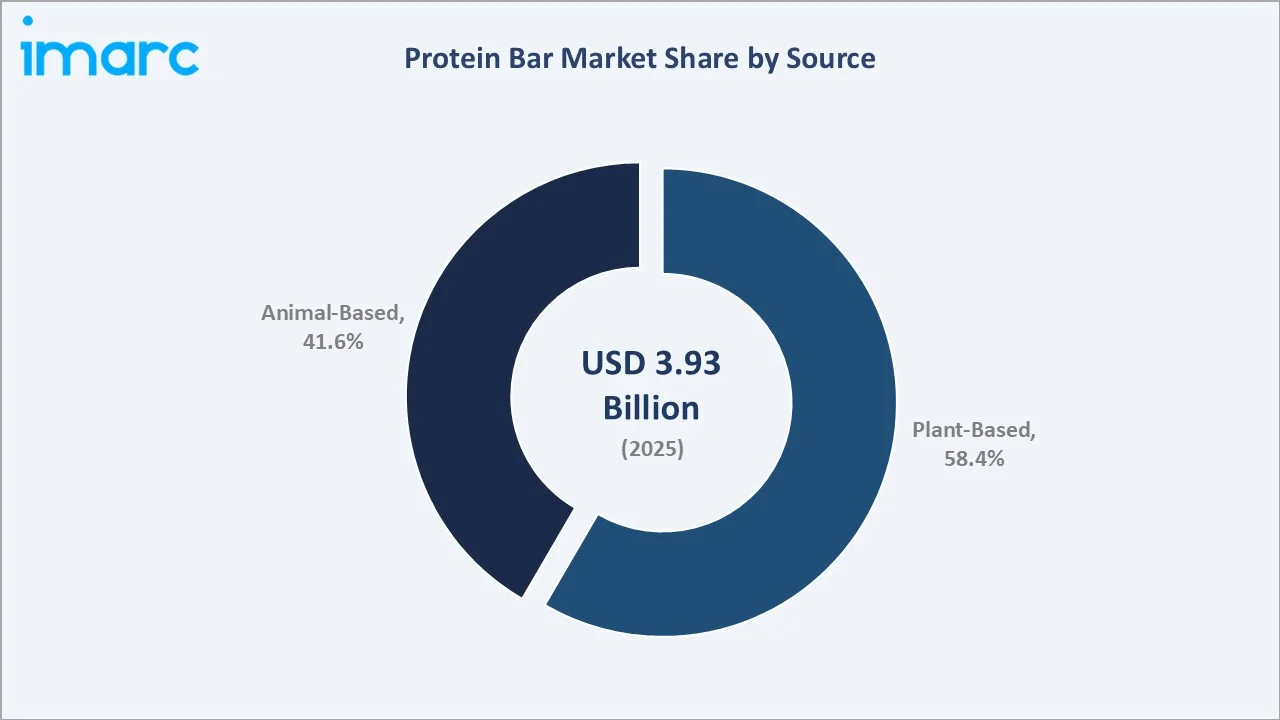

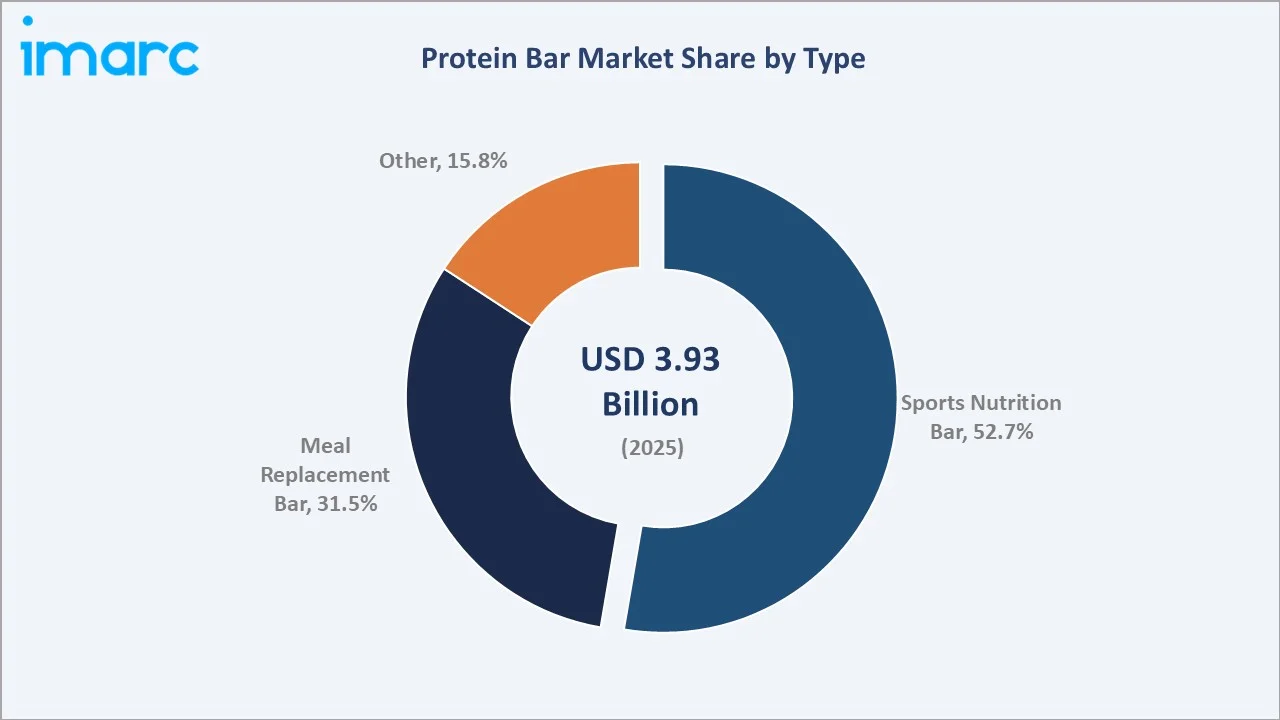

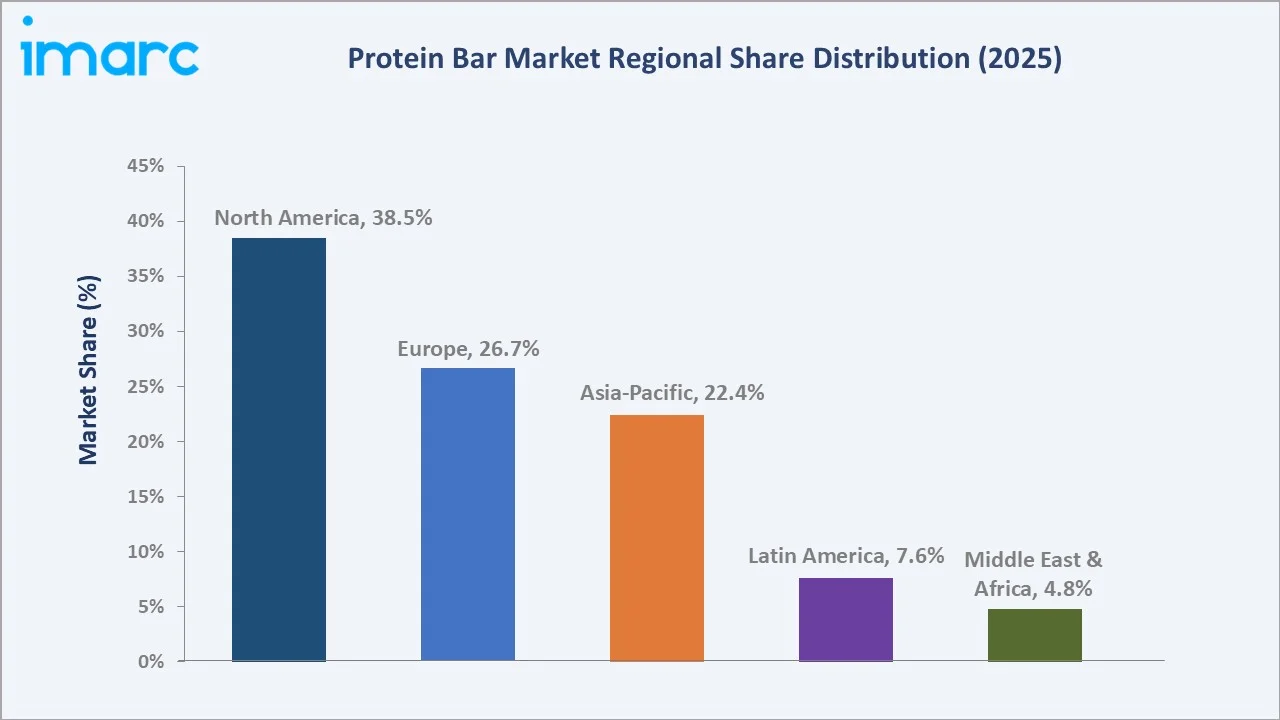

The global protein bar market size was valued at USD 3.93 Billion in 2025 and is projected to reach USD 5.89 Billion by 2034, exhibiting a CAGR of 4.6% during 2026-2034. Rising consumer health awareness, accelerating demand for plant-based nutrition, expanding sports and active-lifestyle populations, and growing on-the-go snacking trends are collectively driving protein bar market growth. Plant-Based bars dominate with a 58.4% share in 2025, while Sports Nutrition Bars account for 52.7% of the global market. North America leads regional demand with a 38.5% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.93 Billion |

|

Forecast Market Size (2034) |

USD 5.89 Billion |

|

CAGR (2026-2034) |

4.6% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.5% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Source Segment |

Plant-Based (58.4%, 2025) |

|

Leading Type Segment |

Sports Nutrition Bar (52.7%, 2025) |

The chart below illustrates the global protein bar market trajectory from 2020 to 2034, with strong post-2020 demand recovery driving historical growth and steady forecast momentum supported by health and fitness adoption.

To get more information on this market, Request Sample

CAGR analysis identifies Plant-Based bars and Sports Nutrition formats as the fastest-growing segments in the global protein bar market through 2034.

Executive Summary

The global protein bar market is transforming rapidly due to rising health consciousness, growing fitness participation, and evolving snacking preferences. Valued at USD 3.93 Billion in 2025, the market is projected to reach USD 5.89 Billion by 2034, expanding at a 4.60% CAGR. Increasing demand for clean-label, high-protein, and functional snacks is accelerating new product launches across mainstream and specialty channels.

Plant-based protein bars lead the market with a 58.4% share in 2025, supported by surging vegan, flexitarian, and lactose-intolerant consumer bases. Sports Nutrition Bars hold 52.7% of revenue, reflecting strong demand from gym-goers, athletes, and active-lifestyle consumers. Key trends include reduced sugar formulations, plant-protein innovation, functional ingredients such as collagen and adaptogens, and rapid online channel expansion.

North America leads the global protein bar market with a 38.5% share in 2025, driven by mature fitness culture, premium retail penetration, and innovation by U.S. brands. Europe holds 26.7%, supported by health-led snacking growth in the UK, Germany, and France. Asia-Pacific accounts for 22.4% and is the fastest-growing region, fuelled by rising urban incomes, fitness uptake, and accelerating modern retail in China and India.

Key Market Insights

|

Insight |

Data |

|

Largest Source Segment |

Plant-Based - 58.4% share (2025) |

|

Second Source Segment |

Animal-Based - 41.6% share (2025) |

|

Leading Type Segment |

Sports Nutrition Bar - 52.7% share (2025) |

|

Second Type Segment |

Meal Replacement Bar - 31.5% share (2025) |

|

Leading Region |

North America - 38.5% (2025) |

|

Second Region |

Europe - 26.7% (2025) |

|

Top Companies |

Mondelēz International, Mars, General Mills, and Nestlé |

|

Market Opportunity |

Plant-protein, functional ingredients, e-commerce expansion |

Key Analytical Observations Supporting the Above Data:

- Plant-Based dominance at 58.4% in 2025 reflects the structural shift toward vegan, flexitarian, and dairy-free diets, with pea, soy, and brown rice proteins becoming preferred replacements for whey-based formulations across global brands.

- Animal-Based bars at 41.6% in 2025 continue to anchor the high-performance and post-workout segments, where whey and casein remain preferred for their complete amino acid profile and superior muscle-recovery efficacy.

- Sports Nutrition Bars at 52.7% in 2025 validate the strong link between rising gym memberships, fitness app adoption, and protein supplementation, particularly across North America and Europe.

- Meal Replacement Bars at 31.5% in 2025 are expanding rapidly due to busy urban lifestyles, weight-management diets, and premium positioning by brands like Atkins, Slim-Fast, and IsaLean.

- North America's 38.5% global dominance in 2025 is supported by a deep retail ecosystem, high disposable income, and dense innovation pipelines from companies like Mondelez, Kellanova, and The Simply Good Foods Company.

- Asia-Pacific is the fastest-growing region, driven by rising fitness participation in India and China, expanding modern trade, and rapid e-commerce penetration through platforms such as Tmall, Amazon India, and Flipkart.

Global Protein Bar Market Overview

Protein bars are nutrition-focused snacks formulated with concentrated protein sources, fiber, and functional ingredients designed to support fitness, weight management, and on-the-go nutrition. The ecosystem includes whey, soy, pea, and brown rice protein suppliers, ingredient innovators, contract manufacturers, brand owners, distributors, and modern retail and online channels collectively shaping product flow from formulation to consumer.

Applications span sports nutrition, meal replacement, weight management, women's wellness, kids' nutrition, and clean-label everyday snacking. Growth is supported by rising fitness participation, increasing protein-deficiency awareness, premium product launches, expanding e-commerce, and continued investment in plant-based and functional formulations across mature and emerging markets.

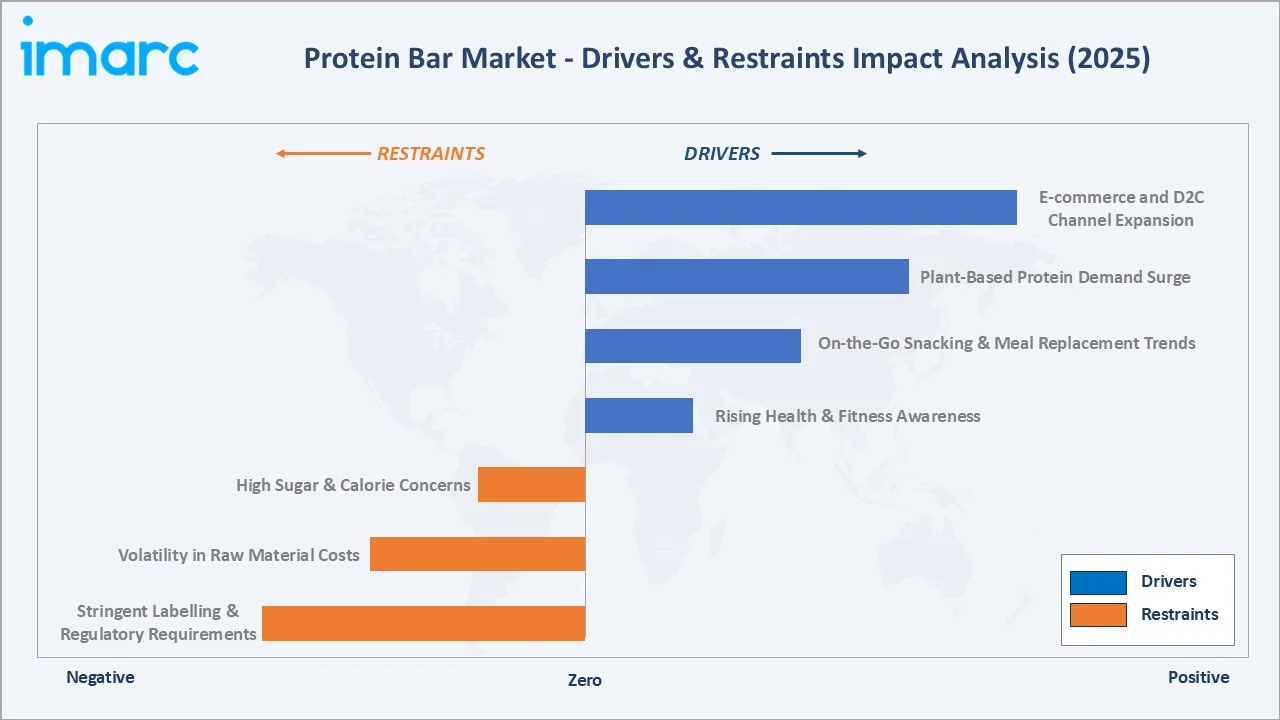

Market Dynamics

Multiple structural and consumer-led forces are shaping the protein bar industry, balancing strong demand drivers against cost, regulatory, and competitive pressures across global geographies.

To evaluate market opportunities, Request Sample

Market Drivers

- Rising Health and Fitness Awareness: Surging gym memberships, fitness-app pulled in 345 million users in 2024, and growing protein-intake awareness are propelling protein bar demand across active and lifestyle consumer segments.

- Plant-Based Protein Demand Surge: Plant-based protein bar innovation is accelerating due to rising vegan and flexitarian diets and lactose intolerance. While exact global launch growth varies, industry reports confirm strong expansion driven by sustainability and health preferences.

- On-the-Go Snacking and Meal Replacement Trends: Busy lifestyles are boosting demand for convenient nutrition, with many consumers replacing meals with snacks. Around 40% of U.S. adults snack multiple times a daily, supporting growth in protein bars as portable meal alternatives.

- E-commerce and Direct-to-Consumer Channel Expansion: E-commerce is a key growth channel for protein bars, driven by platforms like Amazon, Tmall, and iHerb. Online retail expansion and subscription models are improving product accessibility and global reach.

Market Restraints

- High Sugar and Calorie Concerns: Many protein bars still contain notable added sugars, prompting scrutiny from health-conscious consumers and regulators. Authorities such as the World Health Organization recommend limiting free sugar intake, pushing brands toward reformulation and increasing product development costs.

- Volatility in Raw Material Costs: Prices of key inputs such as whey protein, cocoa, nuts, and plant proteins have shown volatility due to supply chain disruptions, climate impacts, and global demand shifts, increasing production costs and pressuring margins for protein bar manufacturers.

- Stringent Labelling and Regulatory Requirements: FDA, EFSA, and FSSAI regulations on protein content claims, allergen disclosure, and nutrition labelling have raised compliance complexity for manufacturers selling across multiple jurisdictions.

Market Opportunities

- Functional and Specialty Bar Innovation: Protein bars with added functional ingredients such as collagen, probiotics, and adaptogens are gaining traction in premium segments. While exact global growth varies, industry evidence confirms rising demand for functional snacks driven by health, wellness, and personalized nutrition trends.

- Emerging Market Expansion: Asia-Pacific and Latin America present strong growth opportunities due to rising fitness awareness and disposable incomes. Markets like India and China are witnessing expanding sports nutrition demand, supported by urbanization and increasing participation in active lifestyles.

- Sustainable and Upcycled Ingredient Adoption: Brands using upcycled fruit fibers, regenerative-agriculture oats, and recyclable wrappers are capturing ESG-conscious consumers, particularly among Millennials and Gen Z buyers in Europe and North America.

Market Challenges

- Intense Brand Competition and Shelf Crowding: The protein bar category is highly fragmented, with numerous SKUs competing for limited retail shelf space, increasing competition, pricing pressure, and making differentiation difficult for both new entrants and established brands.

- Taste and Texture Limitations of Plant Proteins: Plant-based bars often face palatability challenges due to chalky textures and bitter notes, requiring sustained R&D investment in flavor masking and processing technology.

- Greenwashing and Clean-Label Scrutiny: Regulators such as the European Commission and Federal Trade Commission are increasing scrutiny of misleading “natural” and “clean label” claims, raising compliance risks and requiring transparent labeling practices.

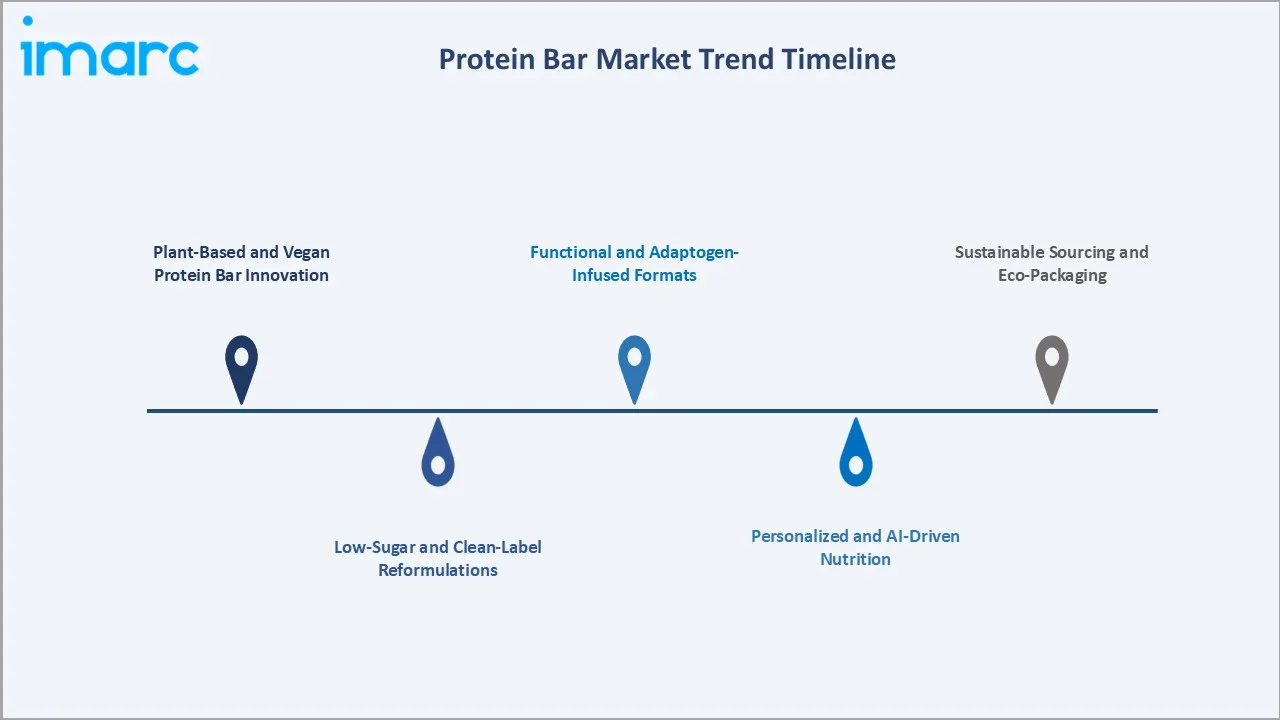

Emerging Market Trends

Five transformative trends are redefining the global protein bar market, blending science-led nutrition with sustainability and personalization.

1. Plant-Based and Vegan Protein Bar Innovation

Manufacturers are increasingly using plant proteins such as pea, soy, and rice to meet vegan and lactose-free demand. Companies like Mondelez International, Nestlé, and General Mills are expanding plant-based snack portfolios globally.

2. Low-Sugar and Clean-Label Reformulations

Protein bar brands are reducing sugar and simplifying ingredients to align with health trends. Growing global diabetes prevalence over 500 million adults supports demand for low-sugar options and clean-label products.

3. Functional and Adaptogen-Infused Formats

Functional protein bars with added ingredients such as probiotics, botanicals, and adaptogens are gaining traction. Rising consumer focus on immunity, energy, and holistic wellness is driving innovation in premium, value-added snack segments.

4. Personalized and AI-Driven Nutrition

Direct-to-consumer brands such as Gainful and HUEL are pioneering subscription-based, personalized protein bars formulated using AI-driven body, fitness, and dietary inputs to deliver tailored nutrition at scale.

5. Sustainable Sourcing and Eco-Packaging

Sustainability is becoming a key differentiator, with brands adopting recyclable or compostable packaging and responsibly sourced ingredients. Increasing environmental awareness among consumers is pushing companies toward eco-friendly product development and transparent supply chains.

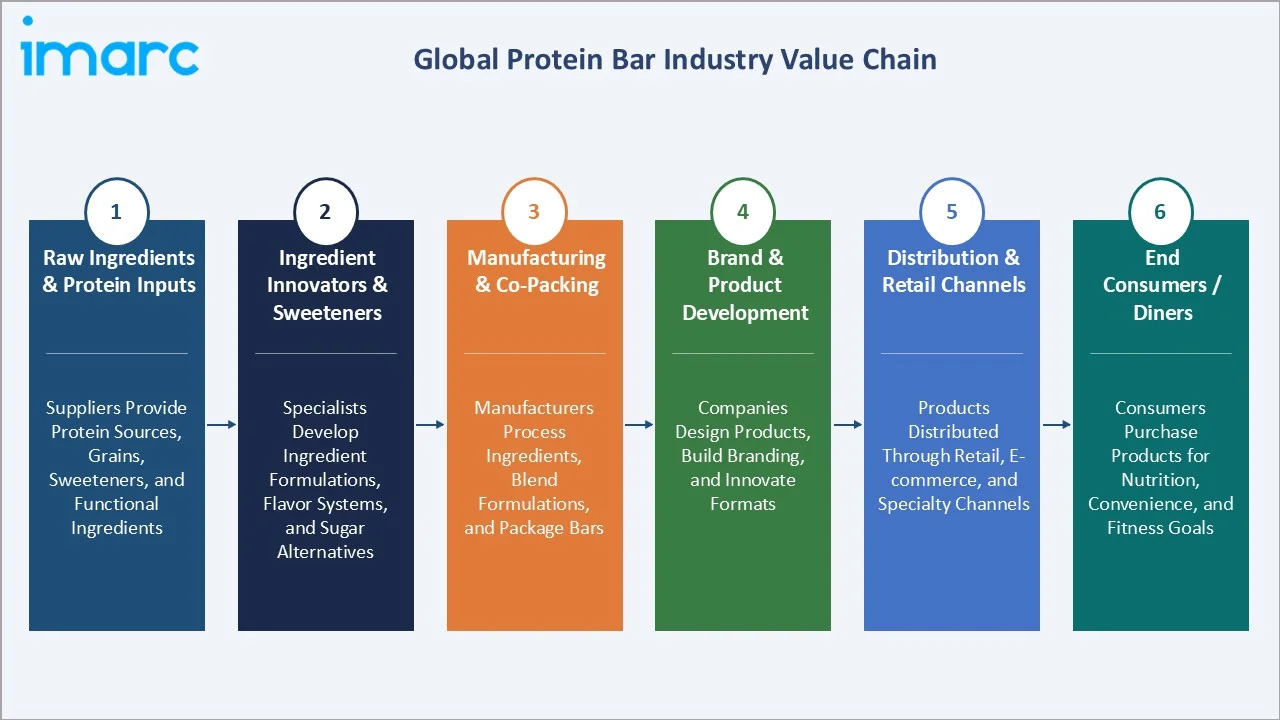

Industry Value Chain Analysis

The protein bar value chain spans six stages, from raw ingredients to end consumers, each shaping cost, quality, and innovation dynamics across the global industry.

|

Stage |

Key Players / Examples |

|

Raw Ingredients & Protein Inputs |

Suppliers provide protein sources, grains, sweeteners, and functional ingredients forming the foundation of final products |

|

Ingredient Innovators & Sweeteners |

Specialists develop ingredient formulations, flavor systems, and sugar alternatives enhancing taste, nutrition, and product differentiation |

|

Manufacturing & Co-Packing |

Manufacturers process ingredients, blend formulations, and package bars while ensuring quality, safety, and consistency standards |

|

Brand & Product Development |

Companies design products, build branding, and innovate formats to meet evolving consumer preferences and demands |

|

Distribution & Retail Channels |

Products are distributed through retail, e-commerce, and specialty channels ensuring wide availability and consumer accessibility |

|

End Consumers / Diners |

Consumers purchase and consume products for nutrition, convenience, fitness goals, and lifestyle needs across segments |

Tier-1 multinationals dominate the value-add stages of brand building, R&D, and global distribution, leveraging scale to control margins and innovation pipelines unmatched by regional and emerging competitors.

Technology Landscape in the Protein Bar Industry

Advanced Plant Protein Processing

Advancements in plant protein extraction and processing are improving taste, texture, and solubility of pea and legume proteins, supporting wider use in protein bars and other foods as demand for plant-based nutrition increases.

Functional Ingredient Integration

Technologies such as microencapsulation enable stable incorporation of sensitive ingredients like probiotics and omega-3s into food products, supporting growth of functional snacks. These innovations help improve shelf life, bioavailability, and product differentiation in protein bars.

Smart Packaging and QR-Enabled Traceability

QR codes and digital packaging technologies are increasingly used to provide product traceability, ingredient sourcing, and sustainability information, enhancing transparency and consumer trust across food products, including protein bars.

AI-Driven Personalized Nutrition Platforms

Artificial intelligence and data analytics are enabling personalized nutrition solutions based on lifestyle and dietary preferences. Food and nutrition companies are increasingly adopting digital platforms to offer tailored product recommendations and customized formulations.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Source |

Plant-Based |

58.4% |

2025 |

|

Type |

Sports Nutrition Bar |

52.7% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

North America |

38.5% |

2025 |

By Source

Plant-based bars hold a 58.4% share in 2025, driven by rising vegan and flexitarian populations, lactose intolerance prevalence, and accelerating ESG-aligned consumer choices. The segment leads new product launches across North America and Europe, with pea, soy, and rice proteins emerging as key formulation pillars.

To access detailed market analysis, Request Sample

Animal-based bars account for 41.6% in 2025, retaining strong demand in performance nutrition where whey and casein deliver complete amino acid profiles, faster absorption, and superior muscle-recovery characteristics preferred by athletes and serious gym-goers.

By Type

Sports Nutrition Bars hold 52.7% of the global protein bar market in 2025, fuelled by rising fitness culture, expanding gym chains, and growing protein-supplementation awareness across North America, Europe, and emerging Asia-Pacific markets.

Meal Replacement Bars hold 31.5% in 2025, supported by busy urban lifestyles, weight-management programs, and premium positioning by brands such as Atkins, Slim-Fast, and IsaLean. Other formats hold 15.8%, including snack-style and kids' protein bar variants.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.5% |

Mature fitness culture, premium retail penetration, dense innovation pipeline (U.S. & Canada) |

|

Europe |

26.7% |

Health-led snacking, plant-based demand, leading brands in UK, Germany, France |

|

Asia-Pacific |

22.4% |

Rising fitness participation, urban income growth, e-commerce expansion in China, India, Japan |

|

Latin America |

7.6% |

Growing gym culture in Brazil and Mexico, rising premium snacking penetration |

|

Middle East & Africa |

4.8% |

GCC fitness investments, premium retail expansion, rising disposable incomes |

North America commands a 38.5% global in 2025, anchored by U.S. consumer leadership in fitness culture, premium snacking, and the strongest brand and retail ecosystem worldwide. Mondelez, Mars, and General Mills drive innovation, while specialty channels such as GNC and Vitamin Shoppe sustain category visibility.

Europe holds 26.7% of the global protein bar market in 2025, driven by health-led snacking trends, mature plant-based demand, and leading regional brands across the UK, Germany, and France. Asia-Pacific at 22.4% remains the fastest-growing regional market, supported by rising urban incomes, expanding fitness participation in India and China, and rapid e-commerce penetration through 2034.

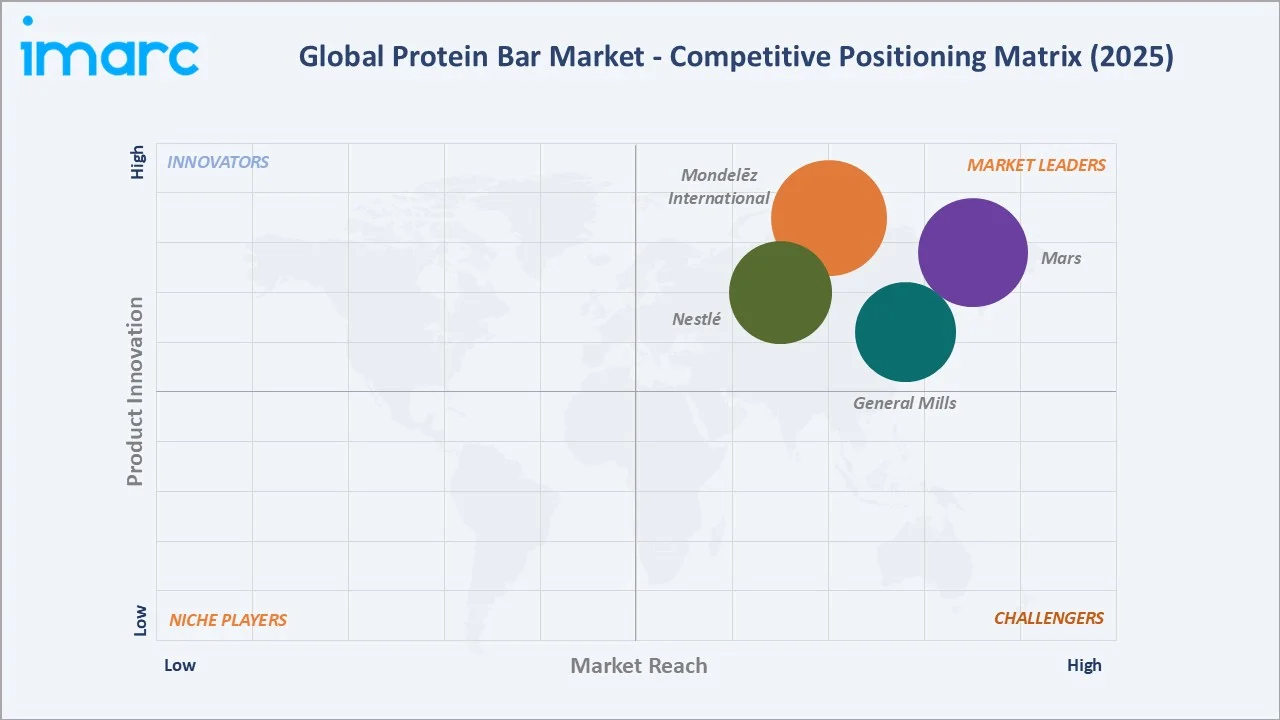

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Mondelēz International |

CLIF Bar , Grenade |

Leader |

Global scale, premium fitness brands, broad distribution |

|

Mars |

MARS Protein, SNICKERS Hi-Protein |

Leader |

Iconic confectionery DNA, mass-market reach |

|

General Mills |

Nature Valley |

Leader |

Strong U.S. retail presence, clean-label leadership |

|

Nestlé |

YES!, Fitness |

Leader |

Health & nutrition expertise, global footprint |

The protein bar market is led by major multinationals alongside specialty challenger brands that capture premium and niche segments. Mondelez International, with brands including CLIF Bar and Grenade, generated over USD 36 Billion in net revenue in 2024, supported by its broad snacking portfolio, global distribution scale, and strong R&D capabilities.

Key Company Profiles

Mondelēz International

Mondelēz International, headquartered in Chicago, is a global leader in snacks and nutrition, operating in over 150 countries. In 2024, it generated USD 36 billion in revenue, driven by biscuits, chocolate, and growing participation in the protein and energy bar segment through acquisitions like CLIF Bar and Grenade.

- Product & Service Portfolio: Mondelēz’s protein and nutrition bar portfolio includes CLIF Bar, CLIF Builders, CLIF Kid Zbar, and Grenade high-protein bars, focusing on sports nutrition, energy, and functional snacking categories

- Recent Developments: In 2025, Mondelēz International strengthened its “well-being snacking” strategy by expanding mindful, portion-controlled, and functional snack offerings. The company reported over 84% of revenue coming from mindful portion products and increased investment in healthier snacking formats, aligning with rising consumer demand for balanced, protein-oriented, and lifestyle-driven nutrition choices globally.

- Strategic Focus: Mondelez focuses on premium snacking expansion, plant-based product innovation, and continued growth in protein nutrition through acquisitions, distribution scale, and emerging-market penetration.

Mars

Mars, Incorporated, headquartered in McLean, Virginia, is a privately held global leader in confectionery, pet care, and food products, operating in over 80 countries. In 2024, the company generated estimated revenues above USD 50 billion, driven by strong brands like Snickers, KIND, and a growing focus on health-oriented snacking.

- Product & Service Portfolio: Snickers Hi-Protein, and MARS Protein functional bars across sports, wellness, and meal-replacement formats.

- Recent Developments: In August 2024, Mars, Incorporated announced a $35.9 billion agreement to acquire Kellanova at $83.50 per share, a 44% premium. The deal combines major snack brands like Pringles and Snickers, strengthening Mars’ global snacking leadership and expanding its footprint across confectionery, salty snacks, and health-oriented products.

- Strategic Focus: Mars is investing in protein-led product extensions, plant-based reformulations, and global expansion of premium wellness brands across mature and emerging markets.

General Mills

General Mills, headquartered in Minneapolis, is a leading global packaged food company with FY2024 net sales of about USD 19.9 billion. The company has a strong presence in the protein and nutrition bar segment through brands like Nature Valley, LÄRABAR, and EPIC, targeting mainstream, natural, and functional snacking consumers.

- Product & Service Portfolio: General Mills’ protein bar portfolio includes Nature Valley Protein bars, LÄRABAR (plant-based/clean-label fruit and nut bars), and EPIC Provisions (meat-based protein bars), covering mainstream, natural, and high-protein functional snacking segments.

- Recent Developments: In March 2026, General Mills introduced five new Nature Valley soft-baked bars, including PB&J variants and kids-focused flavors like Peanut Butter Brownie and S’mores. Each kids’ bar contains 5g protein, reflecting demand for functional snacks. The launch modernizes nostalgic formats into convenient, protein-enhanced bars for on-the-go consumption.

- Strategic Focus: General Mills is focused on clean-label expansion, low-sugar reformulation, and accelerating distribution in natural and specialty retail to capture growing health-conscious consumer demand.

Market Concentration Analysis

The global protein bar market is moderately consolidated at the top, with Mondelēz International, Mars, General Mills, and Nestlé collectively accounting for approximately 40-45% of global revenue in 2025, driven by global brand strength, broad distribution, and significant R&D investment.

Market fragmentation increases at the mid- and lower-tier levels, with a wide range of specialty brands targeting plant-based, women's wellness, weight management, low-sugar, and clean-label niches. This bifurcated structure is typical of premium snacking categories where mainstream multinationals coexist with disruptive challenger brands.

Consolidation continues through acquisition activity, with Mondelez's 2022 acquisition of CLIF Bar exemplifying how global leaders absorb premium specialty brands. Rising consumer focus on health, sustainability, and personalization is expected to drive further M&A through 2030 as multinationals seek capability gaps in plant-based, functional, and clean-label segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Plant-based protein bars are among the fastest-growing segments, supported by increasing adoption of vegan and flexitarian diets and rising demand for dairy-free, clean-label products across developed markets. Functional protein bars enriched with ingredients such as probiotics, collagen, and adaptogens are gaining traction as premium offerings. Sports nutrition bars continue to attract strong investment, driven by expanding global fitness participation, growing gym memberships, and increasing consumer focus on active lifestyles, recovery nutrition, and convenient high-protein snacking solutions.

Emerging Market Expansion

Asia-Pacific represents a high-growth region for protein bars, driven by rapid urbanization, rising disposable incomes, and increasing awareness of health and fitness in countries such as India and China. Expanding e-commerce channels and westernized dietary trends are further supporting demand. Meanwhile, Latin America and the Middle East & Africa are emerging as growth frontiers, supported by a young population base, increasing gym penetration, and rising interest in convenient nutrition products, particularly in key markets such as Brazil, Mexico, and GCC countries.

Venture & Strategic Investment Trends

Venture capital and strategic investments are increasingly directed toward plant-based nutrition companies, functional ingredient innovators, and personalized nutrition platforms. Food and beverage multinationals are actively investing in direct-to-consumer brands, sustainable packaging solutions, and digital health technologies. Investment activity has accelerated in recent years as companies aim to strengthen innovation pipelines and capture premium, health-focused segments, with partnerships, acquisitions, and minority investments playing a key role in expanding product portfolios and technological capabilities.

Future Market Outlook (2026-2034)

The global protein bar market forecast projects sustained value expansion from USD 3.93 Billion in 2025 to USD 5.89 Billion by 2034 at a CAGR of 4.60% - representing an incremental opportunity of nearly USD 1.96 Billion through the forecast period. Growth will be driven by health-led snacking, plant-based innovation, functional ingredient adoption, and expanding e-commerce.

Three transformational trends will reshape the protein bar industry through 2034. AI-enabled personalized nutrition will allow tailored protein bar formulations at scale, while sustainable sourcing and compostable packaging will become baseline requirements. Additionally, functional bars enriched with adaptogens, probiotics, and collagen will create premium-priced sub-segments redefining traditional category boundaries.

By 2034, protein bars are expected to evolve from generic high-protein snacks into highly personalized, functionally enriched, and sustainability-led nutrition products. Brands investing in plant-based innovation, clean-label reformulation, and direct-to-consumer ecosystems are likely to capture disproportionate share of forecast-period growth across both mature and emerging markets.

Research Methodology

Primary Research

Primary research encompassed structured interviews and surveys conducted in 2024-2025 with industry stakeholders including senior brand managers at leading protein bar companies, sports nutrition retailers, gym chain operators, ingredient supplier executives, dietitians, and end-consumer panels across North America, Europe, and Asia-Pacific.

Secondary Research

Secondary sources include company annual reports (Mondelez, Mars, General Mills, Nestle, Kellanova), trade association publications, industry trade media, retail audit data (Nielsen, Mintel), regulatory publications (FDA, EFSA, FSSAI), and global health and fitness participation reports from organizations such as IHRSA and WHO.

Forecasting Models

Market size estimations and growth projections were derived using both top-down and bottom-up forecasting models. The methodology incorporates GDP growth, fitness population trends, retail and e-commerce expansion data, historical category evolution, and scenario analysis under base, optimistic, and conservative macroeconomic assumptions.

Protein Bar Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sources Covered | Plant-Based and Animal-Based |

| Types Covered | Sports Nutrition Bar, Meal Replacement Bar, and Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online Stores, and Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Mondelēz International, Mars, General Mills, Nestlé, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the protein bar market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global protein bar market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the protein bar industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Protein Bar Market Report

The global protein bar market was valued at USD 3.93 Billion in 2025, driven by rising health awareness, sports nutrition demand, and growing on-the-go snacking trends across mature and emerging markets.

The market is projected to reach USD 5.89 Billion by 2034, growing at a CAGR of 4.60% during 2026-2034, supported by plant-based innovation, e-commerce expansion, and functional bar adoption.

Plant-based bars lead with a 58.4% share in 2025, driven by rising vegan and flexitarian populations, lactose intolerance prevalence, and ESG-aligned consumer choices in North America and Europe.

Sports Nutrition Bars dominate with a 52.7% share in 2025, supported by rising fitness participation, expanding gym memberships, and growing protein-supplementation awareness across global markets.

North America leads with a 38.5% share in 2025, anchored by mature fitness culture, premium retail penetration, and dense innovation pipelines from leading U.S. and Canadian protein bar brands.

Key drivers include rising health and fitness awareness, plant-based protein demand, on-the-go snacking trends, e-commerce expansion, functional ingredient innovation, and growing premium snacking culture.

Asia-Pacific is the fastest-growing region, supported by rising urban incomes, expanding fitness participation in India and China, accelerating modern retail, and rapid e-commerce penetration through 2034.

Leading companies include Mondelēz International, Mars, General Mills, and Nestlé and among others.

Animal-based bars hold 41.6% share in 2025, mainly serving performance nutrition where whey and casein proteins offer complete amino acids, faster absorption, and superior muscle-recovery efficacy.

Plant-based growth is driven by rising vegan and flexitarian diets, lactose intolerance, ESG-aligned consumer choices, and brand investment in pea, soy, and rice protein innovation across global markets.

Advanced plant protein processing, microencapsulation of functional ingredients, AI-driven personalized nutrition, and QR-enabled traceability are transforming product innovation, branding, and consumer engagement worldwide.

Supermarkets and hypermarkets remain the largest channel, while online stores are the fastest-growing, supported by Amazon, Tmall, iHerb, and brand-owned subscription platforms enabling rapid global reach.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)