Qatar 3PL Market Size, Share, Trends and Forecast by Transport, Service Type, End Use, and Region, 2026-2034

Qatar 3PL Market Summary:

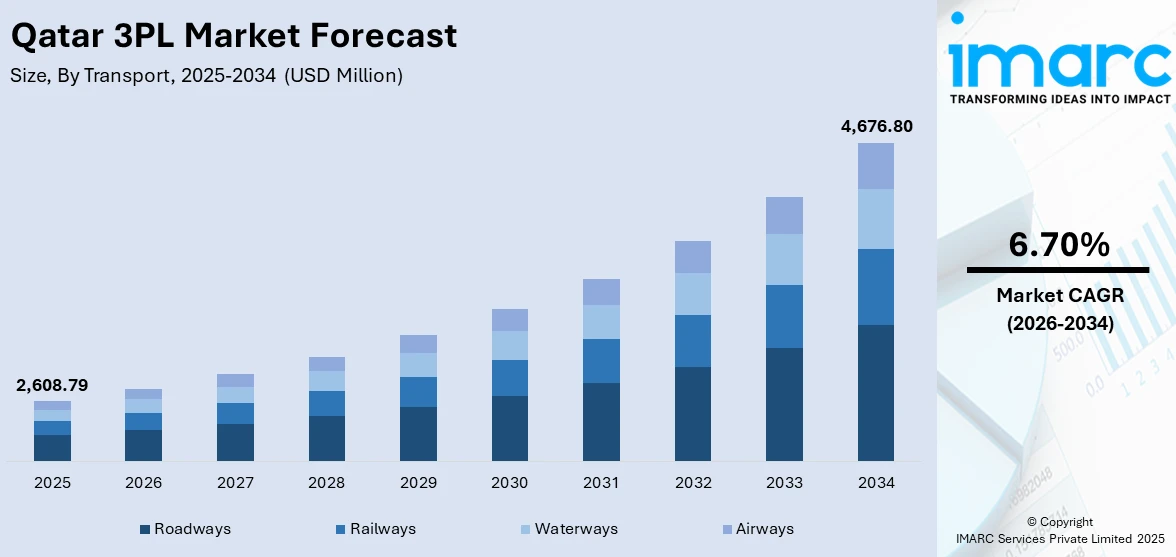

The Qatar 3PL market size was valued at USD 2,608.79 Million in 2025 and is projected to reach USD 4,676.80 Million by 2034, growing at a compound annual growth rate of 6.70% from 2026-2034.

The Qatar 3PL market is experiencing robust growth driven by government-led infrastructure development initiatives that are significantly expanding logistics capacity and connectivity throughout the country. The rapid expansion of e-commerce is fueling demand for advanced third-party logistics services, including warehousing, order fulfillment, and last-mile delivery solutions. The digital transformation of the logistics sector through adoption of smart technologies, automation, and artificial intelligence is enhancing operational efficiency and expanding the Qatar 3PL market share.

Key Takeaways and Insights:

- By Transport: Roadways dominate the market with a share of 54% in 2025, driven by Qatar's extensive road network development and domestic freight distribution requirements connecting industrial zones to ports.

- By Service Type: Domestic transportation management leads the market with a share of 30% in 2025, owing to increasing demand for efficient inland logistics coordination and supply chain optimization services.

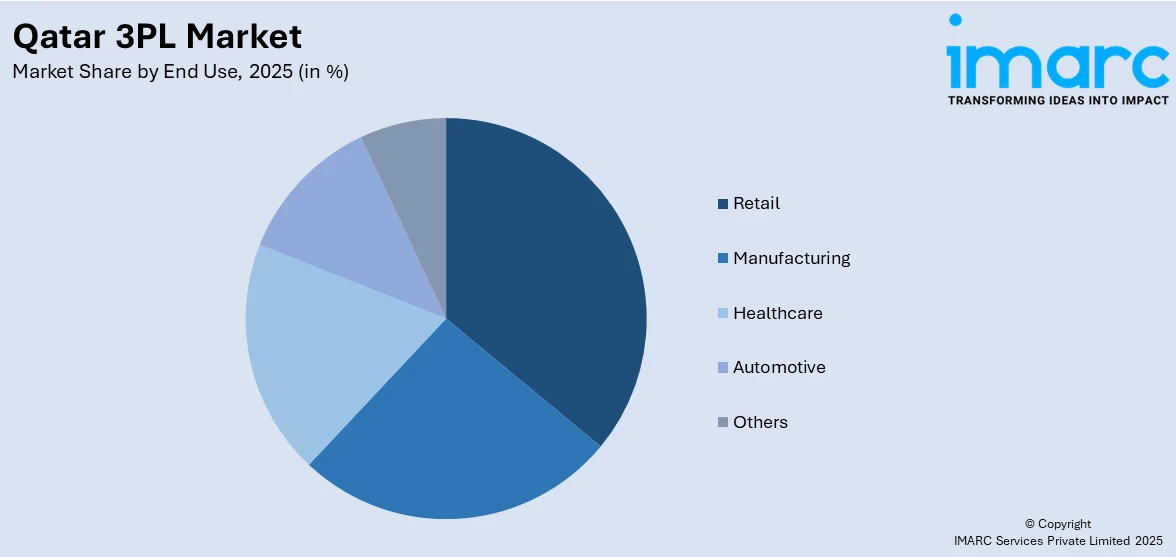

- By End Use: Retail represents the largest segment with a market share of 25% in 2025, driven by the swift growth of e-commerce platforms and increasing consumer expectations for quicker and more reliable delivery services. This surge in online shopping has intensified demand for efficient logistics solutions, making retail the dominant end-use segment in the industry.

- By Region: Ad Dawhah leads the market with a share of 46% in 2025, reflecting the capital's concentration of logistics infrastructure, commercial activity, and consumer markets.

- Key Players: The Qatar 3PL market exhibits moderate competitive intensity, featuring a mix of established regional logistics providers and international freight forwarding companies. The competitive landscape is characterized by strategic partnerships, technological innovation, and expanding service portfolios to capture growing e-commerce demand.

To get more information on this market Request Sample

Qatar's transformation into a regional logistics powerhouse is being accelerated by billions in infrastructure investment, strategic free zones, and advanced digital systems designed to capture a larger share of global trade. Hamad Port has been developed into one of the Middle East’s most sophisticated maritime hubs, equipped to manage a substantial volume of container traffic each year. The port achieved top ranking in the Gulf and placed eleventh globally in the 2024 Container Port Performance Index, jointly published by the World Bank and S&P Global. Additionally, Qatar's integrated air-sea logistics network now serves over 200 destinations, offering end-to-end value propositions including bonded warehousing, re-export capabilities, and advanced customs clearance. Logistics services play a significant role in Qatar’s economy, with expectations of continued growth in their contribution to the country’s overall economic output in the coming years.

Qatar 3PL Market Trends:

Growing Demand for E-Commerce Logistics

The exponential growth of e-commerce is profoundly reshaping Qatar's logistics landscape, with online retail platforms driving unprecedented demand for fulfillment and last-mile delivery services. Third-party logistics providers have become essential partners for managing inventory, processing orders, and ensuring rapid deliveries to meet consumer expectations. For instance, in September 2025, BSX Logistics expanded its fulfillment solutions in Doha to enhance order processing and last-mile delivery capabilities for Qatar's growing e-commerce market, incorporating advanced technology and inventory management systems to improve efficiency and customer satisfaction.

Digital Transformation and Technology Adoption

The Qatar 3PL sector is experiencing a major digital transformation, driven by the integration of artificial intelligence, IoT sensors, advanced warehouse management systems, and real-time tracking technologies. These innovations are enhancing operational visibility, improving efficiency, and enabling predictive analytics for optimized supply chain management. Strategic investments in AI and supporting infrastructure are fostering the adoption of automated logistics operations, predictive maintenance solutions, and intelligent warehouse management, positioning Qatar’s third-party logistics industry for greater efficiency, scalability, and responsiveness to evolving market demands.

Sustainability and Green Logistics Initiatives

Environmental sustainability is emerging as a central focus in Qatar’s third-party logistics sector, with providers increasingly implementing eco-friendly practices such as electric vehicle fleets, renewable energy-powered warehouses, and optimized routing systems. These initiatives align with the country’s long-term goals to reduce carbon emissions while improving operational efficiency. Investments in supporting infrastructure, including EV charging networks and cleaner public transport, are further promoting green logistics. Collectively, these efforts are helping Qatar’s 3PL industry transition toward more sustainable, energy-efficient, and environmentally responsible operations.

Market Outlook 2026-2034:

The Qatar 3PL market outlook remains strongly positive, driven by continued infrastructure investments, e-commerce expansion, and economic diversification initiatives under Qatar National Vision 2030. The Third National Development Strategy 2024-2030 identifies logistics as a key growth cluster, with plans to establish Qatar as a re-export center for high-value products and strengthen the country's transport competitiveness. The government's cumulative target of USD 100 billion in foreign direct investment by 2030 is expected to attract additional logistics operators and technology providers. The market generated a revenue of USD 2,608.79 Million in 2025 and is projected to reach a revenue of USD 4,676.80 Million by 2034, growing at a compound annual growth rate of 6.70% from 2026-2034.

Qatar 3PL Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Transport |

Roadways |

54% |

|

Service Type |

Domestic Transportation Management |

30% |

|

End Use |

Retail |

25% |

|

Region |

Ad Dawhah |

46% |

Transport Insights:

- Railways

- Roadways

- Waterways

- Airways

Roadways dominates with a market share of 54% of the total Qatar 3PL market in 2025.

Road transport forms the backbone of Qatar’s domestic logistics network, enabling efficient movement of goods between industrial zones, commercial centers, and consumer markets. The country’s well-developed road infrastructure connects key logistics hubs, including ports, airports, and free zone facilities, supporting smooth multimodal transportation. Strategic road and infrastructure initiatives have enhanced connectivity, improved safety, and facilitated the integration of pedestrian and cycling networks, contributing to more efficient and reliable logistics operations across urban and industrial areas.

The dominance of road transport is reinforced by long-term national transportation plans that focus on improving freight efficiency and reducing operational costs. It plays a crucial role in last-mile delivery services, particularly for the expanding e-commerce sector. Third-party logistics providers are leveraging advanced fleet management systems and route optimization technologies to enhance delivery speed, improve operational efficiency, and meet growing demand for timely, cost-effective logistics solutions across Qatar.

Service Type Insights:

- Dedicated Contract Carriage

- Domestic Transportation Management

- International Transportation Management

- Warehousing and Distribution

- Value Added Logistics Services

Domestic transportation management leads with a share of 30% of the total Qatar 3PL market in 2025.

Domestic transportation management services have emerged as the leading service type segment, driven by increasing demand for efficient inland logistics coordination across Qatar's compact yet economically dynamic geography. 3PL providers are offering comprehensive domestic transport solutions including freight consolidation, route planning, and real-time shipment tracking, to optimize supply chain performance. The segment benefits from Qatar's advanced road infrastructure and the growing need for integrated logistics services supporting retail, manufacturing, and construction sectors.

The rise of e-commerce has particularly accelerated demand for domestic transportation management services, with 3PL providers deploying technology-driven solutions to handle high-volume, time-sensitive deliveries. The Qatar e-commerce market size reached USD 3.8 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 10.1 Billion by 2033, exhibiting a growth rate (CAGR) of 10.27% during 2025-2033. Companies are investing in fleet modernization and digital platforms to provide end-to-end visibility and enhanced customer service capabilities.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Manufacturing

- Retail

- Healthcare

- Automotive

- Others

Retail represents the largest share of 25% of the total Qatar 3PL market in 2025.

Retail dominates the Qatar 3PL market due to the rapid expansion of e-commerce and modern retail chains across the country. Growing consumer demand for convenient, fast, and reliable delivery services has driven retailers to rely heavily on third-party logistics providers for warehousing, inventory management, and last-mile distribution. The integration of advanced technologies such as automated fulfillment centers, real-time order tracking, and data-driven supply chain solutions has further strengthened the role of 3PL providers in supporting retail operations efficiently.

In addition, retail’s diverse product range, from fast-moving consumer goods to electronics and fashion, requires specialized logistics handling and flexible transportation solutions. Third-party logistics providers offer scalable and customizable services, enabling retailers to optimize inventory, reduce delivery times, and manage seasonal demand fluctuations effectively. The sector’s continuous growth, fueled by urbanization, increasing digital adoption, and evolving consumer expectations, ensures that retail remains the leading contributor to the development and expansion of Qatar’s 3PL market.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah exhibits a clear dominance with a 46% share of the total Qatar 3PL market in 2025.

The Qatar 3PL market in Ad Dawhah is being driven by rapid urbanization and the expansion of commercial and industrial activities in the capital. Growing consumer demand for e-commerce and modern retail solutions is increasing the need for efficient warehousing, inventory management, and last-mile delivery services. Advanced infrastructure, including ports, airports, and road networks, facilitates smooth logistics operations, enabling 3PL providers to offer faster, more reliable, and cost-effective supply chain solutions to businesses operating across diverse sectors in the city.

Technological adoption is another key driver, with 3PL companies in Ad Dawhah implementing automated warehouse systems, real-time tracking, and data-driven logistics management to enhance operational efficiency. Government initiatives supporting trade, smart city development, and sustainable logistics practices are also contributing to market growth. Additionally, the increasing demand for specialized logistics services, such as temperature-controlled transport and cross-border shipments, is encouraging providers to expand capabilities, making Ad Dawhah a central hub for modern, flexible, and scalable 3PL solutions in Qatar.

Market Dynamics:

Growth Drivers:

Why is the Qatar 3PL Market Growing?

Government-Led Infrastructure Development

Qatar’s government is heavily investing in logistics infrastructure to position the country as a leading regional hub for trade and commerce. Major road projects, port expansions, and free zone developments are enhancing connectivity and freight movement efficiency. The creation of modern transportation corridors supports smoother domestic and international logistics operations. Meanwhile, the expansion of Hamad Port has established it as a highly advanced maritime gateway, linking Qatar to numerous global destinations. Its operational efficiency and state-of-the-art handling capabilities have strengthened the country’s position in regional and international trade networks.

Rapid E-Commerce Expansion

The rapid expansion of e-commerce in Qatar is driving strong demand for third-party logistics services, particularly in warehousing, order fulfillment, and last-mile delivery. Widespread internet access and high smartphone usage are fueling mobile commerce, making online shopping increasingly convenient. Investments in advanced network infrastructure have supported the growth of hyper-local logistics solutions, enabling faster deliveries across urban areas. The rise of online grocery and other retail segments is transforming consumer behavior, prompting 3PL providers to develop efficient, technology-driven logistics networks capable of meeting the evolving expectations of Qatar’s digital-first shoppers.

Strategic Geographic Location

Qatar's strategic position at the crossroads of Asia, Africa, and Europe provides significant competitive advantages for logistics operations. The country offers access to eighty percent of the world's population within eight hours by air and five days by sea, making it an attractive location for regional distribution centers and transshipment operations. Qatar ranked eighth out of fifty countries in the 2025 Agility Emerging Markets Logistics Index, reflecting its strong logistics infrastructure, business environment, and digital readiness. In 2024, Qatar attracted USD 2.7 billion in foreign direct investment across 241 projects, creating 9,348 jobs. The government has prioritized attracting foreign investment as part of its long-term economic diversification strategy, identifying logistics as a key sector to drive growth and support the goals of Qatar National Vision 2030.

Market Restraints:

What Challenges is the Qatar 3PL Market Facing?

Skilled Labor Shortage

The logistics sector in Qatar is facing the problem of a lack of professionals because the sector is growing faster than the number of trained specialists. This loophole may curtail the effectiveness of operations, slacken innovation, and impair the capacity of logistics enterprises to satisfy the increasing demand. The development of the logistics sector workforce and training is one of the most important issues that can be used to maintain the work performance and competitiveness.

High Operational Costs

Operational costs in the logistics industry in Qatar are influenced by the volatility in fuel prices, labor costs, and investment in new technologies, and thus are relatively high. Such financial strains may influence the profitability and put a strain on providers to ensure high service quality but compete. The cost management and the introduction of technology solutions are necessary to ensure the balance of expenses and performance, and efficiency in the work.

Regional Competition

Competition from neighboring countries with their own logistics ambitions presents challenges for Qatar's 3PL market. Regional rivals are investing heavily in port infrastructure, free zones, and technology capabilities to capture market share. To stay ahead, Qatar is focusing on specialized niches including pharmaceutical logistics, high-tech manufacturing supply chains, and green logistics solutions to differentiate its value proposition.

Competitive Landscape:

The Qatar 3PL market features a moderately competitive landscape characterized by a mix of established regional logistics providers and international freight forwarding companies. Leading domestic players leverage their extensive local infrastructure, understanding of regional business dynamics, and established relationships with key industries. International players bring global network capabilities, advanced technology solutions, and specialized expertise in areas such as cold chain logistics and e-commerce fulfillment. The market is witnessing increasing consolidation through strategic partnerships and joint ventures as companies seek to expand service portfolios and geographic coverage. Competition is intensifying around technology adoption, with providers investing in digital platforms, automation systems, and data analytics to enhance operational efficiency and customer experience.

Recent Developments:

- September 2025: Qatar Airways Cargo and Cainiao expanded their partnership to enhance cross-border e-commerce delivery. The agreement will double Cainiao's weekly charter flights on key China-Europe routes, improving connectivity and logistics capabilities to address the growing demand for fast international shipping in the evolving e-commerce landscape.

- September 2025: BSX Logistics expanded its fulfillment solutions in Doha to enhance order processing and last-mile delivery for Qatar's growing e-commerce market, incorporating advanced technology and inventory management systems to improve efficiency and customer satisfaction.

- May 2024: Qatar Free Zones Authority and FedEx Logistics signed a memorandum of understanding to establish a regional logistics facility in Qatar's free zones. The facility, part of FedEx's Trade Networks Transport and Brokerage division, will be in Ras Bufontas Free Zone and will include a modern logistics office.

Qatar 3PL Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Transports Covered | Railways, Roadways, Waterways, Airways |

| Service Types Covered | Dedicated Contract Carriage, Domestic Transportation Management, International Transportation Management, Warehousing and Distribution, Value Added Logistics Services |

| End Uses Covered | Manufacturing, Retail, Healthcare, Automotive, Others |

| Regions Covered | Ad Dawhah, Al Rayyan, Al Wakrah, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar 3PL Market Report

The Qatar 3PL market size was valued at USD 2,608.79 Million in 2025.

The Qatar 3PL market is expected to grow at a compound annual growth rate of 6.70% from 2026-2034 to reach USD 4,676.80 Million by 2034.

Roadways dominated the market with a 54% share in 2025, driven by Qatar's extensive road network development and domestic freight distribution requirements connecting industrial zones, ports, and consumer markets.

Key factors driving the Qatar 3PL market include government-led infrastructure development initiatives, rapid e-commerce expansion creating demand for fulfillment and last-mile delivery services, Qatar's strategic geographic location as a regional trade hub, and digital transformation through adoption of smart logistics technologies.

Major challenges include skilled labor shortages with approximately twenty-five percent of logistics positions unfilled, high operational costs impacting competitiveness, regional competition from neighboring countries with their own logistics ambitions, and the need for continuous technological innovation to maintain market position.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)