Qatar Affordable Housing Market Size, Share, Trends and Forecast by Provider, Income Category, Unit Size, Location Type, and Region, 2026-2034

Qatar Affordable Housing Market Summary:

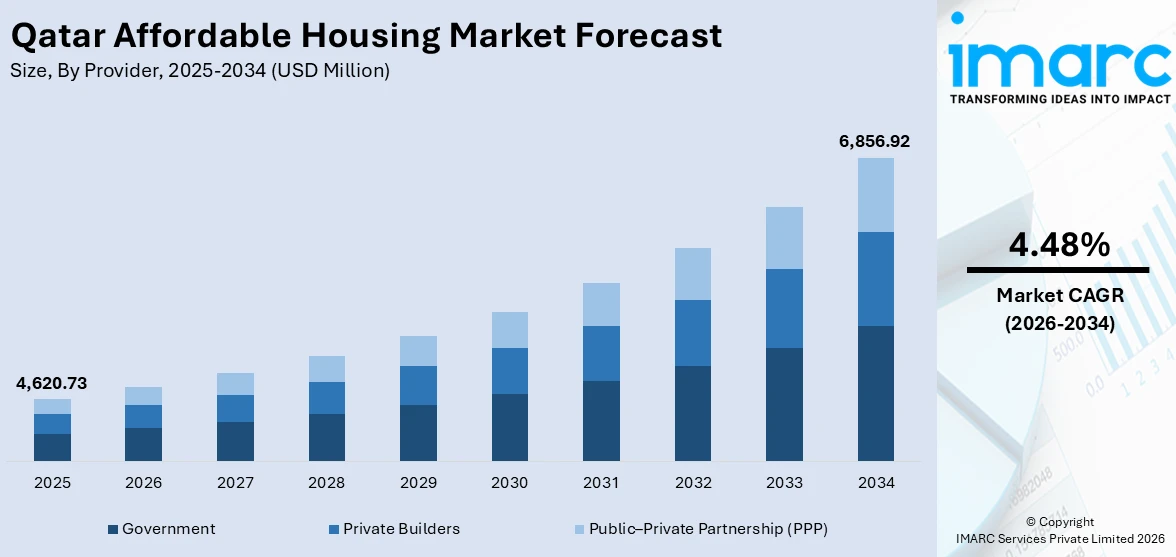

The Qatar affordable housing market size was valued at USD 4,620.73 Million in 2025 and is projected to reach USD 6,856.92 Million by 2034, growing at a compound annual growth rate of 4.48% from 2026-2034.

The Qatar affordable housing market is expanding as the government intensifies efforts to address the growing housing needs of middle-income residents and expatriates through strategic urban planning and targeted housing programs aligned with Qatar National Vision 2030. Rapid population growth, driven predominantly by an influx of expatriate workers across energy, construction, and services sectors, is creating sustained demand for cost-effective residential units in metropolitan areas. In May 2025, Ashghal announced a QR 81 Billion five-year infrastructure plan spanning 2025 to 2029 that includes the development of infrastructure for over 5,500 residential plots through public-private partnership frameworks. The increasing adoption of sustainable building practices, digital construction technologies, and modular housing solutions is further strengthening the supply pipeline while reducing development costs. Additionally, liberalized property ownership regulations and competitive mortgage financing options are broadening buyer accessibility, encouraging first-time homeownership, and attracting domestic and international investment into the Qatar affordable housing market share.

Key Takeaways and Insights:

- By Provider: Government dominates the market with a share of 48.7% in 2025, owing to its comprehensive national housing programs that prioritize affordable residential solutions for Qatari citizens and eligible residents. Sustained public investment in large-scale community developments and subsidized land allocation schemes continue to reinforce government leadership in affordable housing provision.

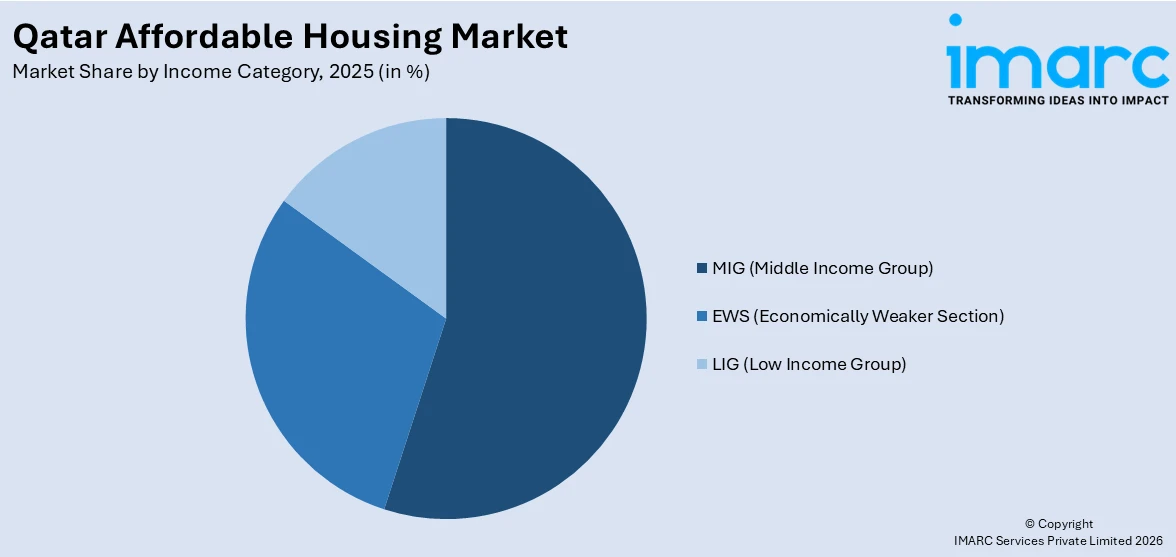

- By Income Category: MIG (Middle Income Group) leads the market with a share of 44.1% in 2025. This dominance is driven by the expanding middle-income expatriate workforce seeking quality housing at accessible price points, supported by favorable mortgage terms and integrated community developments offering modern amenities.

- By Unit Size: Above 800 sq. ft. exhibits a clear dominance in the market with 46.8% share in 2025, reflecting strong family-oriented demand for spacious residential units that accommodate multi-member households and align with cultural preferences for larger living spaces across Qatar.

- By Location Type: Metro represents the biggest segment with a market share of 63.4% in 2025, driven by the concentration of employment opportunities, commercial infrastructure, educational institutions, and healthcare facilities in Doha and its surrounding metropolitan areas.

- By Region: Ad Dawhah is the largest region with 58.6% share in 2025, underpinned by its position as Qatar's capital and primary economic hub, attracting the highest concentration of residential demand from both nationals and expatriates seeking proximity to workplaces and urban services.

- Key Players: Key players drive the Qatar affordable housing market by expanding residential portfolios, improving construction efficiency and sustainability standards, and strengthening distribution through strategic partnerships with government entities and financial institutions to boost accessibility and adoption.

To get more information on this market Request Sample

The Qatar affordable housing market is evolving as the nation accelerates its transition toward balanced urban development that caters to diverse income segments. Government-led initiatives under the Qatar National Vision 2030 framework are directing significant capital toward residential infrastructure, creating integrated communities that combine housing with essential social amenities. The rising expatriate population, which constitutes over 85% of Qatar's 2.7 Million residents, is generating sustained demand for affordable rental and ownership options across metropolitan centers. In Q2 2025, residential transactions in Qatar recorded a notable surge of 114%, reflecting renewed buyer confidence and growing interest in affordable and mid-tier housing segments. The integration of smart building technologies, energy-efficient designs, and Global Sustainability Assessment System certification into new affordable housing projects is enhancing livability standards while controlling operational costs. Public-private partnerships are increasingly central to the delivery model, enabling the government to leverage private sector expertise and capital while maintaining affordability targets. Developers are responding with innovative community-oriented projects that combine residential, retail, and recreational components, creating self-sufficient neighborhoods that reduce commuting burdens and improve quality of life for residents across all income brackets.

Qatar Affordable Housing Market Trends:

Integration of Sustainable Construction Practices in Affordable Housing

Qatar's affordable housing sector is increasingly embracing sustainability-driven construction methodologies aligned with the Global Sustainability Assessment System. Developers are incorporating energy-efficient insulation, solar panel installations, and water conservation systems into cost-effective residential projects, reducing long-term utility costs for residents. As of 2024, Qatar has 1,406 sustainability-certified buildings across public and private sectors, demonstrating the nation's commitment to environmentally responsible construction. This trend is reshaping the Qatar affordable housing market growth by enabling developers to deliver greener residential communities that meet both affordability targets and environmental standards.

Expansion of Transit-Oriented Affordable Residential Communities

The expansion of the Doha Metro network is reshaping residential demand patterns by enhancing connectivity between affordable housing areas and key employment centers. Areas near metro stations, including Al Wakra, Al Rayyan, and Education City, are witnessing increasing property demand as improved public transit accessibility makes suburban and peripheral locations more attractive for middle-income families. The planned Blue Line, targeted for completion between 2025 and 2026, will further extend the metro network to approximately 300 kilometers, connecting emerging residential neighborhoods and stimulating affordable housing development in newly accessible areas.

Rise of Community-Integrated Mixed-Use Affordable Developments

Qatar's affordable housing landscape is shifting toward integrated community developments that combine residential units with retail, healthcare, educational, and recreational facilities within self-contained neighborhoods. Projects such as Barwa City, spanning over 2.7 Million square meters and accommodating approximately 25,000 residents through a mix of apartments and studios, exemplify this model by offering comprehensive amenities alongside affordable housing. This approach addresses the holistic living needs of middle-income households, reducing commuting requirements while fostering stronger community engagement and social cohesion across the country.

Market Outlook 2026-2034:

The Qatar affordable housing market is poised for sustained expansion, underpinned by robust government investment in residential infrastructure, rising population growth, and the strategic diversification of the economy under Qatar National Vision 2030. The increasing focus on public-private partnerships for housing delivery, combined with regulatory reforms that broaden property ownership eligibility for foreign residents, is expected to attract greater domestic and international capital into the affordable segment. The market generated a revenue of USD 4,620.73 Million in 2025 and is projected to reach a revenue of USD 6,856.92 Million by 2034, growing at a compound annual growth rate of 4.48% from 2026-2034. Continued infrastructure development, including metro network expansion and new urban utility systems, will enhance the attractiveness of emerging residential zones. The adoption of modular construction techniques, sustainable building practices, and digital construction management tools is anticipated to improve delivery efficiency and reduce development costs, further supporting the market's growth trajectory throughout the forecast period.

Qatar Affordable Housing Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Provider |

Government |

48.7% |

|

Income Category |

MIG (Middle Income Group) |

44.1% |

|

Unit Size |

Above 800 sq. ft. |

46.8% |

|

Location Type |

Metro |

63.4% |

|

Region |

Ad Dawhah |

58.6% |

Provider Insights:

- Government

- Private Builders

- Public–Private Partnership (PPP)

Government dominates with a market share of 48.7% of the total Qatar affordable housing market in 2025.

The government sector leads Qatar's affordable housing landscape through comprehensive national housing programs that allocate subsidized land, provide interest-free loans, and deliver ready-built residential units to eligible citizens. The Ministry of Housing plays a pivotal role by overseeing housing applications, distributing units across designated communities, and ensuring that residential developments meet prescribed livability standards. Ongoing infrastructure development under public-private partnership frameworks is further strengthening the government's delivery capacity by expanding internal road networks, sewage systems, landscaping, and lighting across newly designated residential zones, reinforcing the state's commitment to sustainable and accessible housing provision.

Government-backed housing projects are strategically positioned in growing urban corridors to provide residents with proximity to essential services, employment centers, and public transportation networks. The alignment of housing programs with Qatar National Vision 2030 ensures long-term sustainability through the integration of energy-efficient building designs, green space allocation, and community-oriented planning. In 2024, the total residential stock in Qatar reached 399,542 units comprising 251,513 apartments and 148,029 villas, reflecting sustained governmental commitment to expanding housing supply across the country.

Income Category Insights:

Access the comprehensive market breakdown Request Sample

- EWS (Economically Weaker Section)

- LIG (Low Income Group)

- MIG (Middle Income Group)

MIG (Middle Income Group) leads with a share of 44.1% of the total Qatar affordable housing market in 2025.

The country's sizable expatriate population, which demands high-quality residential accommodations at reasonable prices, propels the MIG (Middle Income Group) sector to the top of Qatar's affordable housing market. Middle-class professionals working in the energy, finance, healthcare, and educational sectors make up a substantial portion of the demand for luxurious apartments and villas that provide contemporary conveniences without charging exorbitant prices. Increased homeownership among this group is being made possible by the growing mortgage market, which lowers obstacles to property acquisition through competitive financing options and expedited application procedures.

Developers are increasingly catering their residential developments to middle-class households' tastes by providing completely furnished apartments, flexible payment options, and integrated community features like shopping malls, gyms, and swimming pools. The market's responsiveness to MIG demand is demonstrated by the modern residential developments in well-connected metropolitan districts, which provide modern living spaces that strike a compromise between cost and high-quality lifestyle elements. Government initiatives that promote workforce expansion and economic diversification, which keep drawing skilled individuals to the nation, also contribute to this segment's growth. For middle-class families that want easy access to jobs, schools, and other necessities, the growing number of transit-oriented communities and mixed-use areas is also making cheap housing alternatives more alluring.

Unit Size Insights:

- Up to 400 sq. ft.

- 400–800 sq. ft.

- Above 800 sq. ft.

Above 800 sq. ft. exhibits a clear dominance with 46.8% share of the total Qatar affordable housing market in 2025.

The highest market share is held by the segment with unit sizes above 800 square feet, which reflects the strong cultural and demographic demand for roomy living arrangements that can support extended family structures, which is typical of Qatar's population. Larger apartments accommodate the changing lifestyle demands of both domestic and foreign households by offering specific areas for family activities, entertaining guests, and working from home. Larger units typically drive the highest occupancy rates throughout affordable housing projects in the nation, and family-sized layouts and complete facilities are available in community-oriented residential complexes that are ideally located close to key metropolitan centers.

Middle-class families, who value room without compromising budget, are especially drawn to apartments larger than 800 square feet. They look for apartments that strike a compromise between pleasant living quarters and easy access to healthcare services, schools, and recreational places. In order to meet this demand, developers are creating integrated community developments that include parks, shops, and social infrastructure in addition to bigger floorplans. Families are increasingly able to access roomy housing alternatives thanks to the expanding availability of flexible payment plans and reasonable financing options, which is supporting the ongoing demand for larger unit configurations throughout Qatar's affordable residential market.

Location Type Insights:

- Metro

- Non-Metro

Metro represents the leading segment with 63.4% share of the total Qatar affordable housing market in 2025.

The concentration of work possibilities, businesses, educational institutions, and healthcare facilities in and around Doha generates ongoing demand for inexpensive housing among budget-conscious households, which is why metropolitan regions dominate Qatar's affordable housing market. The operational Doha Metro network has greatly improved urban connections, increasing the accessibility and appeal of inexpensive home complexes in areas close to the metro for families and working professionals. Tenant activity is consistently highest in metro-connected locations because better public transportation lowers commute costs and travel times, which increases the allure of reasonably priced residential communities along transit corridors across the wider metropolitan area.

The metro area gains from ongoing infrastructure spending that raises living standards and property prices in residential urban areas. The demand for cheap housing in newly connected urban districts is anticipated to be further strengthened by the Doha Metro's planned extension, which includes the Blue Line and additional stations. In addition to supporting the construction of integrated, reasonably priced residential communities that cater to Qatar's expanding population and changing urban mobility needs, government investments in urban utilities, such as sophisticated sewage systems, treated water networks, and smart street lighting, are making metro areas more livable.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah holds the largest share with 58.6% of the total Qatar affordable housing market in 2025.

As the capital and main economic, administrative, and cultural center of Qatar, Ad Dawhah has the biggest concentration of government buildings, job hubs, and basic services, making it the dominant market for inexpensive housing in the country. Both domestic and foreign people looking for reasonably priced housing close to centers of employment and urban conveniences are most drawn to the municipality. Due to the capital's unparalleled concentration of social infrastructure, economic opportunities, and lifestyle options that appeal to a wide range of income levels nationwide, Doha and the surrounding areas routinely see the highest levels of residential transaction activity.

Affordable residential constructions are more easily accessible throughout the capital's many districts thanks to its well-developed transportation infrastructure, which includes the major interchange station of the Doha Metro and vast road networks. In addition to developing mixed-income housing alternatives that cater to a wide range of demographics, ongoing urban regeneration initiatives are reviving inner-city districts. The ongoing construction of neighborhood-focused amenities including parks, shopping malls, and medical facilities is making Ad Dawhah even more alluring to those looking for reasonably priced housing. Ad Dawhah's status as Qatar's main demand center for cheap housing is cemented by improved connection between the capital's residential areas and outlying job centers, which guarantees consistent demand.

Market Dynamics:

Growth Drivers:

Why is the Qatar Affordable Housing Market Growing?

Government-Led Housing Programs and Strategic Infrastructure Investment

The Qatari government's proactive approach to affordable housing delivery remains the primary catalyst for market expansion, encompassing subsidized land allocation, interest-free housing loans, and direct construction of residential communities for eligible citizens and residents. The Ministry of Housing administers a structured application process that ensures equitable distribution of housing units while maintaining quality standards aligned with national livability benchmarks. These programs are further reinforced by the government's substantial budgetary commitments directed toward infrastructure and development projects, including road construction, metro systems, and public facilities that directly support residential areas. The strategic deployment of public-private partnership models is accelerating housing delivery by leveraging private sector expertise and capital, with ongoing infrastructure development plans earmarking residential plot preparation across multiple locations nationwide. This comprehensive governmental approach is creating a robust pipeline of affordable residential units that addresses growing demand while enhancing the overall quality of life across Qatar's urban centers. The integration of sustainable construction standards and modern urban planning principles into government-led housing initiatives further ensures that new developments align with long-term national objectives for environmental stewardship and community wellbeing.

Rapid Population Growth and Expanding Expatriate Workforce

There is a continual need for inexpensive housing options in urban areas due to Qatar's steadily growing population, which is mostly caused by an ongoing migration of foreign workers from the energy, construction, finance, and services industries. Over the past ten years, the country's population has increased dramatically, and expatriates now make up a sizable portion of the overall population, which has supported the need for reasonably priced housing. In cities like Doha, Al Rayyan, and Al Wakrah, where accessibility to major job centers and basic amenities is a top factor when choosing a place to live, this population growth is more concentrated. The demand for housing is further increased by the government's economic diversification strategy under Qatar National Vision 2030, which continues to draw in highly qualified individuals from a variety of other countries. By drawing professionals from the hotel and service industries who need reasonably priced housing, the growing tourist sector is also boosting auxiliary residential demand. Long-term occupancy rates for affordable housing complexes are guaranteed by the trajectory of population growth, which also encourages ongoing investment in new residential projects by giving developers and investors predictable returns. The professional population looking for affordable housing options in Qatar is growing as a result of the country's economic base's diversification into technology, education, healthcare, and financial services.

Enhanced Urban Connectivity Through Metro and Transportation Infrastructure

Due to the growing accessibility and appeal of inexpensive housing in suburban and outlying areas, Qatar's public transportation network, anchored by the Doha Metro system, is radically altering patterns of residential demand. The feasibility of cheap housing developments in regions like Al Wakra, Al Rayyan, and Education City has been directly improved by the operating metro network, which has decreased commuters' costs and times. More metro lines are anticipated to be completed, expanding the network's reach into new residential areas and encouraging the development of new, reasonably priced homes along transportation routes. The nation's commitment to sustainable urban transportation is demonstrated by Qatar's substantial investment in metro and light rail infrastructure, which ranks among the greatest public transit pledges in the Gulf. A more integrated urban environment that fosters the expansion of affordable housing communities across the nation is also being created by continuous road development initiatives that are enhancing connectivity between residential areas and commercial hubs through improved expressways, bike lanes, and pedestrian pathways. In Qatar's growing urban landscape, the combination of improved public transportation, updated road systems, and pedestrian-friendly urban planning is changing the accessibility and appeal of reasonably priced residential neighborhoods.

Market Restraints:

What Challenges the Qatar Affordable Housing Market is Facing?

Elevated Construction Costs and Material Price Volatility

Development budgets for affordable housing projects in Qatar are still under pressure from rising costs for building materials including steel, cement, and specialty building components. Developers find it difficult to satisfy quality and sustainability criteria while maintaining affordability objectives due to rising input costs brought on by global supply chain disruptions, fluctuating commodity prices, and higher shipping costs. In the end, these cost constraints may slow the rate at which new affordable housing stock enters the market by causing project delays, decreased profit margins, and possible concessions on design criteria.

Limited Land Availability in Prime Metropolitan Locations

The growth of affordable housing in Qatar is severely hampered by the lack of developable land in Doha and other highly sought-after urban regions. Affordable housing projects are frequently redirected to outlying regions with less established infrastructure and worse connection as prime metropolitan locations are being given up to luxury, commercial, and mixed-use buildings that yield greater returns. For middle-class tenants who value being close to sources of employment, educational institutions, and medical services, this spatial displacement may make inexpensive apartments less appealing, which might diminish demand.

Post-World Cup Oversupply Concerns in Select Residential Segments

After the development boom, Qatar has a noticeable excess of residential units, which is putting pressure on prices and producing vacancy issues in some housing segments. In mid-tier apartment categories, where ongoing new unit deliveries are causing rental rates to fall, this overstock is most noticeable. In addition to compressing rental rates and slowing new building activity, the excess inventory might also raise doubts among investors assessing the future potential of the affordable housing market.

Competitive Landscape:

The competitive environment in Qatar's affordable housing industry is somewhat consolidated, with well-established private companies and government-affiliated developers holding a sizable market share. In order to distinguish their services, key players are concentrating on integrating sustainable design concepts, increasing construction efficiency through modular and prefabricated techniques, and growing residential portfolios through extensive community developments. By facilitating quicker delivery, wider geographic coverage, and improved pricing, strategic alliances between public and private developers are changing the competitive landscape. For appealing to budget-conscious purchasers and renters while upholding quality standards and adhering to national sustainability certification criteria, businesses are increasingly using digital construction management tools, smart home technology, and creative financing arrangements.

Qatar Affordable Housing Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Providers Covered |

Government, Private Builders, Public–Private Partnership (PPP) |

|

Income Categories Covered |

EWS (Economically Weaker Section), LIG (Low Income Group), MIG (Middle Income Group) |

|

Unit Sizes Covered |

Up to 400 sq. ft., 400–800 sq. ft., Above 800 sq. ft. |

|

Location Types Covered |

Metro, Non-Metro |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Affordable Housing Market Report

The Qatar affordable housing market size was valued at USD 4,620.73 Million in 2025.

The Qatar affordable housing market is expected to grow at a compound annual growth rate of 4.48% from 2026-2034 to reach USD 6,856.92 Million by 2034.

Government dominated the market with a share of 48.7%, driven by comprehensive national housing programs, subsidized land allocation, interest-free loans, and direct construction of residential communities aligned with Qatar National Vision 2030.

Key factors driving the Qatar affordable housing market include government-led housing programs, rapid population growth, expanding expatriate workforce, enhanced metro connectivity, public-private partnerships, and increasing adoption of sustainable construction practices.

Major challenges include elevated construction costs and material price volatility, limited land availability in prime metropolitan locations, post-World Cup oversupply concerns in select residential segments, and regulatory complexities affecting project timelines.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade