Qatar Automotive Market Size, Share, Trends and Forecast by Vehicle Type, Propulsion Type, Application, Ownership Model, Sales Channel, and Region, 2026-2034

Qatar Automotive Market Summary:

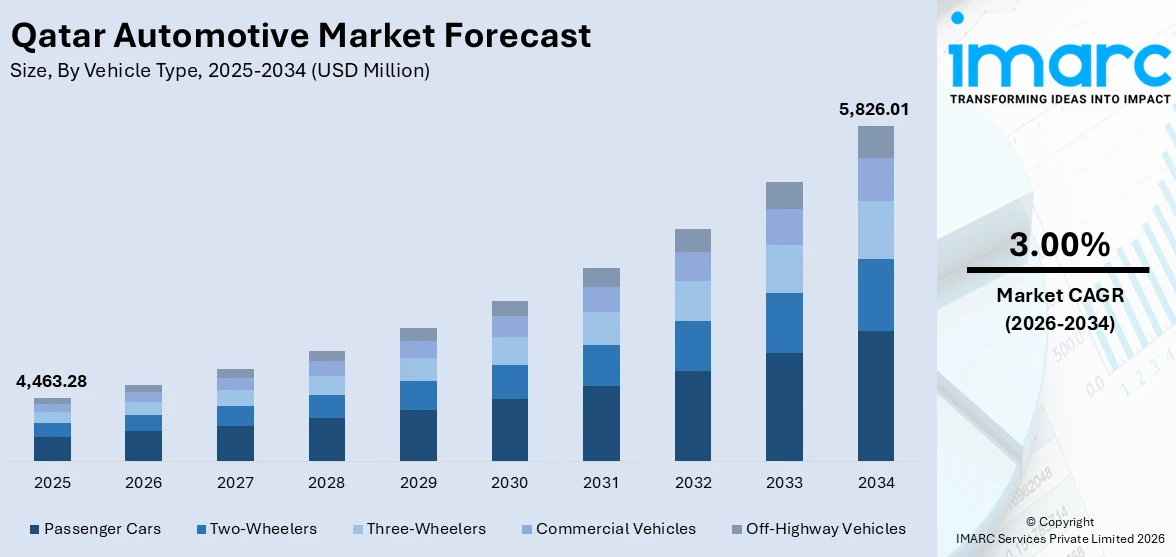

The Qatar automotive market size was valued at USD 4,463.28 Million in 2025 and is projected to reach USD 5,826.01 Million by 2034, growing at a compound annual growth rate of 3.00% from 2026-2034.

The country's strong economic diversification strategy, growing population, and expanding consumer spending power are all contributing to the steady growth of the Qatari automobile industry. A favorable climate for the demand for automobiles is being created by government investments in top-notch road infrastructure, smart city projects like Lusail, and the growth of public transit networks. The rise of new international and Chinese automakers, together with consumers' growing desire for SUVs and premium cars, is increasing competition and expanding product selection. New markets are also being stimulated by the government's dedication to sustainable transportation through the implementation of charging infrastructure and its Electric Vehicle Strategy. A strong post-World Cup economy, internet retail platforms, and alluring financing alternatives continue to boost customer confidence and increase Qatar's market share in the automobile industry.

Key Takeaways and Insights:

- By Vehicle Type: Passenger cars dominate the market with a share of 52.3% in 2025, because of consumers' strong need for personal mobility, growing disposable incomes, and the growing selection of sedan and SUV models that appeal to both the premium and budget markets in Qatar.

- By Propulsion Type: Internal combustion engine (ICE) leads the market with a share of 83.5% in 2025, demonstrating the ongoing accessibility and affordability of cars that run on conventional gasoline, which is bolstered by low fuel costs and a robust nationwide fuelling network.

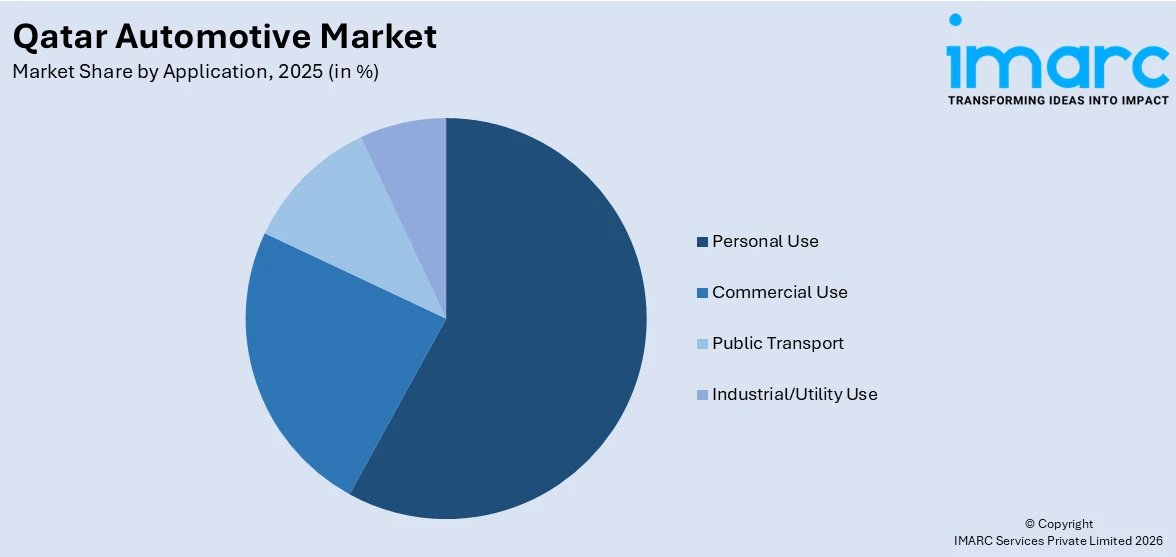

- By Application: Personal use represents the biggest segment with a market share of 57.8% in 2025, driven by an increasing number of expatriates who need daily commute solutions, high per capita income levels, and cultural attitudes that encourage private car ownership for family mobility.

- By Ownership Model: Individual ownership exhibits a clear dominance in the market with 69.4% share in 2025, supported by easily available auto finance programs, affordable insurance choices, and the social value of owning a car in Qatari culture as a symbol of individual prestige and freedom of movement.

- By Sales Channel: OEM/authorized dealers lead the market with a share of 61.7% in 2025, fueled by customer confidence in after-sales service networks, manufacturer-backed warranty programs, and the availability of the newest model releases through well-established dealership infrastructure.

- By Region: Ad Dawhah is the largest region with 60.5% share in 2025, spurred by the fact that the capital municipality and the surrounding metropolitan region house the majority of Qatar's population, business activity, financial services, and large networks of car dealerships.

- Key Players: By increasing model portfolios, improving dealership networks, investing in digital sales platforms, and fortifying after-sales service capabilities, major companies propel the Qatari automotive market. Adoption is accelerated and product accessibility is ensured by their emphasis on premium products, SUV lines, affordable pricing, and collaborations with finance institutions.

To get more information on this market Request Sample

Growing brand variety, increased car sales, and strategic government efforts in line with Qatar National Vision 2030 are all signs of a transitional period in the country's automotive industry. Consumer demand for new and luxury cars is being maintained by the country's solid macroeconomic foundations, which are reinforced by significant public investment and economic diversification. With commerce, financial services, and tourism expanding the customer base with a wider range of vehicle tastes, the non-hydrocarbon industry has become a crucial development driver. A steady rebound in car sales, supported by increasing consumer spending power and population inflows, indicates rekindled market confidence as the automotive industry gets closer to pre-downturn levels. With competitively priced, feature-rich vehicles that appeal to a wide range of consumer categories, new multinational and regional manufacturers are rapidly entering the market and upending established brand hierarchies. At the same time, the government's initiatives for smart transportation, electric mobility, and sustainable urban development are creating new opportunities for innovation and expansion throughout the automotive value chain.

Qatar Automotive Market Trends:

Rapid Rise of Chinese Automotive Brands

Chinese automakers are making significant inroads into Qatar’s automotive landscape, challenging the long-standing dominance of Japanese and Korean manufacturers. Brands such as Jetour, Geely, and Chery are gaining consumer acceptance through competitively priced, technology-rich SUV offerings that resonate with local buyer preferences. The entry of new Chinese brands is accelerating competition and expanding vehicle options for cost-conscious consumers. In 2025, Jetour recorded over 70,000 vehicle sales across the Middle East, representing more than 80% year-on-year growth, and captured an 8.5% share of the Middle East SUV segment, ranking third behind only Toyota and Nissan, underscoring its growing influence in Qatar automotive market growth.

Growing Adoption of Digital Sales Platforms and Online Retail Channels

With customers depending more and more on online platforms for research, comparison, and transactions, the automobile industry in Qatar is undergoing a noticeable change toward digitalized car purchase. Transparency is being improved by digital retail channels, which make it possible to configure vehicles, take virtual showroom tours, and apply for financing easily. Younger, tech-savvy customers who value the ease of internet interaction are especially affected by this trend. Buyer confidence in cross-border transactions is being strengthened by streamlined customs processes and enhanced vehicle tracing systems, which is also hastening the nationwide adoption of digital automotive retail ecosystems.

Expansion of Premium and Luxury Vehicle Segment

Qatar’s high per capita income and affluent consumer base continue to fuel demand for premium and luxury vehicles, with buyers seeking advanced technology, superior comfort, and prestige-oriented models. The strong preference for SUVs and luxury crossovers is reshaping product offerings from both established and emerging brands. Dealership networks are investing in state-of-the-art showroom experiences to cater to this discerning clientele. In June 2025, Škoda Auto announced Q-Auto as its exclusive distributor in Qatar, with plans to open a brand-new showroom and service centre, introducing five models including the flagship Kodiaq SUV, reflecting growing brand diversification in the premium segment.

Market Outlook 2026-2034:

The Qatar automotive market is poised for sustained expansion over the forecast period, underpinned by the nation’s accelerating economic diversification agenda, robust public infrastructure investments, and the government’s strategic commitment to sustainable mobility under Qatar National Vision 2030. The market generated a revenue of USD 4,463.28 Million in 2025 and is projected to reach a revenue of USD 5,826.01 Million by 2034, growing at a compound annual growth rate of 3.00% from 2026-2034. Rising population inflows, increasing consumer sophistication, and the continued expansion of dealership networks and financing solutions are expected to sustain vehicle sales momentum. Additionally, the government’s ambitious targets for electric vehicle adoption, including reaching 10% of total vehicle sales by 2030 and deploying over 1,000 charging stations, will open new market segments. The growing penetration of Chinese automotive brands, development of smart city projects such as Lusail, and advancements in connected vehicle technologies are further expected to reshape the competitive landscape and create diverse growth opportunities across vehicle categories.

Qatar Automotive Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Vehicle Type |

Passenger Cars |

52.3% |

|

Propulsion Type |

Internal Combustion Engine (ICE) |

83.5% |

|

Application |

Personal Use |

57.8% |

|

Ownership Model |

Individual Ownership |

69.4% |

|

Sales Channel |

OEM/Authorized Dealers |

61.7% |

|

Region |

Ad Dawhah |

60.5% |

Vehicle Type Insights:

- Two-Wheelers

- Three-Wheelers

- Passenger Cars

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Off-Highway Vehicles

Passenger cars dominate with a market share of 52.3% of the total Qatar automotive market in 2025.

Because of Qatar's high per capita income and robust demand for personal mobility solutions, the passenger vehicle category continues to hold its dominant position in the country's automotive industry. The expanding selection of vehicles, which includes luxury SUVs, mid-range crossovers, and economical sedans, serves Qatar's diversified population, which includes both wealthy citizens and a sizable expat population. While a prolonged economic recovery continues to boost consumer confidence and propel strong registration numbers throughout the passenger car category, competitive financing programs from banks and dealers have reduced obstacles to vehicle ownership.

Cultural choices that highlight private vehicle ownership as crucial for everyday commute and family mobility in Qatar's climate further support the ongoing dominance of passenger automobiles. SUVs continue to be quite popular in the passenger car market because they provide a blend of comfort, luxury, and functionality that is appropriate for the local terrain and lifestyle choices. Rapid brand diversity is also occurring in this category, as new domestic and foreign manufacturers are gaining headway with feature-rich, competitively priced vehicles that are upending established brand hierarchies and giving consumers more options in the passenger car market.

Propulsion Type Insights:

- Internal Combustion Engine (ICE)

- Hybrid Vehicles (HEV/PHEV)

- Electric Vehicles (BEV)

Internal combustion engine (ICE) leads with a share of 83.5% of the total Qatar automotive market in 2025.

The country's affordable gasoline prices, substantial fueling infrastructure, and long-standing customer preference for conventional powertrains all contribute to the internal combustion engine segment's continued dominance of the Qatari automobile industry. From cheap to luxury, ICE vehicles are widely available and reasonably priced, which guarantees their continued dominance. Despite increased interest in alternative powertrains, the segment's established market position is reinforced by Qatar's hot climate and lengthy intercity distances, which also favor ICE cars as buyers continue to be wary about battery performance and charging logistics.

Although internal combustion engines continue to dominate the market, the sector is progressively changing as manufacturers release lower-emission and more fuel-efficient ICE models to meet more stringent regional regulations. For Qatari consumers who desire performance and dependability, the value proposition of ICE cars is being improved by the adoption of turbocharged engines and sophisticated transmission systems. Even while ICE remains dominant in the medium future, the government's electric vehicle policy points to a gradual transition ahead, with growing interest in hybrid and battery electric options suggesting that the propulsion landscape will vary over time.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Personal Use

- Commercial Use

- Public Transport

- Industrial/Utility Use

Personal use is the largest segment with 57.8% share of the total Qatar automotive market in 2025.

The market for cars in Qatar is dominated by personal usage due to the country's high levels of disposable income, hot environment that demands air-conditioned private transportation, and significant focus on individual mobility. Personal automobiles are becoming increasingly necessary for everyday commuting due to the growing number of expatriates. By providing easily accessible Sharia-compliant and traditional auto financing options, banks and other financial institutions further assist this market, reducing obstacles to car ownership and maintaining high private vehicle registration volumes that demonstrate the persistently high demand for personal vehicles.

The well-established road system in Qatar helps the personal usage sector by enabling pleasant and easy private car travel across the small country. Automakers are being compelled to improve their personal-use car lineups in response to growing consumer demands for connected technologies, cutting-edge safety features, and upscale interiors. The market also shows the rising desire for family-friendly automobiles such crossovers and mid-size SUVs that blend elegance and functionality. It is anticipated that sustained economic expansion and national development plans centered on sustainable prosperity would maintain consumer spending power and increase demand for personal automobiles across a range of price points.

Ownership Model Insights:

- Individual Ownership

- Fleet Ownership

- Subscription-Based Ownership

- Shared Mobility (Ride-hailing, Car-sharing)

The individual ownership exhibits a clear dominance with 69.4% share of the total Qatar automotive market in 2025.

The most common ownership model in the Qatari automobile industry is still individual ownership, which reflects both the practical need for private mobility in an area with harsh weather conditions and ingrained cultural preferences for owning a personal car. Barriers to purchasing a personal automobile have been greatly lowered by the availability of competitive auto finance options, such as Sharia-compliant contracts with adjustable terms and easily accessible down payment plans. This ownership model is the foundation of the larger automotive ecosystem as the country's high level of consumer spending power guarantees a steady demand for privately owned automobiles in the luxury, mid-range, and economy categories.

Favorable government regulations, such as low registration fees, no yearly property taxes on cars, and affordable insurance rates, further encourage private ownership. Strong individual acquisition patterns are further supported by the societal significance of automobile ownership in Qatari society, where cars are used as status and family prestige indicators. Dealership networks provide extended warranty plans, loyalty rewards, and trade-in programs to individual customers. In order to increase market penetration across both client categories, dealers implement targeted promotions while maintaining a balance between fleet and individual ownership channels.

Sales Channel Insights:

- OEM/Authorized Dealers

- Independent/Used Vehicle Dealers

- Online Platforms

- Direct-to-Consumer (D2C)

OEM/authorized dealers represent the leading segment with 61.7% share of the total Qatar automotive market in 2025.

OEM/authorized dealers dominate the Qatar automotive market's sales channel landscape, benefiting from strong consumer trust in manufacturer-backed warranty programs, certified service centers, and access to the latest model launches. The Qatari market's emphasis on brand prestige and after-sales reliability makes authorized dealership networks the preferred point of purchase for both national and expatriate consumers. Dealership groups continue to invest in state-of-the-art showroom facilities and integrated service centers, consolidating multiple customer offerings under one roof to enhance service convenience and strengthen long-term brand loyalty.

The authorized dealer channel further benefits from exclusive distribution agreements that guarantee brand representation and model availability. Dealers leverage integrated financing partnerships with leading banks to offer attractive purchase packages directly at the point of sale. The channel is also evolving through digital integration, with dealers deploying virtual showrooms, online booking systems, and home delivery services to complement traditional in-person experiences. The entry of new international and regional brands into Qatar's market continues to expand the authorized dealer landscape, reinforcing this channel's dominant position through diversified product portfolios and enhanced customer engagement strategies.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah holds the largest share with 60.5% of the total Qatar automotive market in 2025.

Ad Dawhah, encompassing Qatar's capital city Doha, commands the largest share of the automotive market owing to its position as the nation's demographic, economic, and commercial hub. The municipality accommodates the majority of Qatar's residential, financial, and administrative centers, creating the highest concentration of vehicle demand in the country. The Doha Metropolitan Area is home to the largest cluster of automotive dealerships, service centers, and financing institutions, ensuring extensive vehicle accessibility and consumer choice across all segments and price points. The presence of major corporate headquarters, government ministries, and international organizations within the municipality generates sustained demand for both personal and commercial vehicles.

The region's well-developed road infrastructure, including modern highways, ring roads, and expressways, facilitates convenient private vehicle travel and supports high vehicle ownership rates among residents. The concentration of premium residential districts, luxury retail destinations, and smart city developments further drives demand for high-end and technologically advanced vehicles. Ad Dawhah also serves as the primary gateway for new automotive brand launches and showroom openings, with dealership groups establishing flagship facilities to attract the municipality's affluent and diverse consumer base. The ongoing expansion of metro connectivity and urban development projects continues to enhance the region's attractiveness, reinforcing its dominant position within the broader Qatar automotive market landscape.

Market Dynamics:

Growth Drivers:

Why is the Qatar Automotive Market Growing?

Robust Economic Diversification and Rising Consumer Purchasing Power

Qatar's ambitious economic diversification strategy is creating a favorable macroeconomic environment that sustains and accelerates automotive demand. The government's strategic focus on expanding non-hydrocarbon sectors including tourism, financial services, logistics, and technology is generating new employment opportunities and attracting a growing expatriate workforce that contributes directly to vehicle demand. Rising disposable incomes and consumer confidence are translating into higher vehicle acquisition rates across luxury, mid-range, and economy segments. The stable currency environment provides importers and consumers with predictable cost structures, facilitating smoother transaction planning. Robust public investment and strong progress in economic diversification continue to bolster consumer spending power, with the non-hydrocarbon sector emerging as a vital growth engine that is broadening the consumer base and creating sustained demand for vehicles across all price categories and vehicle types throughout the country.

Strategic Government Investment in Transportation Infrastructure

The Qatar government's sustained investment in world-class transportation infrastructure is fundamentally enhancing the environment for automotive market growth. The development of modern highway networks, ring roads, expressways, and smart city projects creates improved driving conditions that encourage vehicle ownership and usage. The integration of metro systems, tram networks, and intercity road links further supports a multi-modal transportation ecosystem where private vehicles play a central role. Qatar's ambitious infrastructure agenda, stemming from Qatar National Vision 2030 and the Third National Development Strategy, positions transportation as a vital enabler of economic growth and diversification. Specialized government initiatives aimed at enhancing public transportation efficiency, logistics performance, digital transformation, and smart mobility innovation are further strengthening the institutional framework supporting automotive sector expansion and long-term sustainable mobility across the nation.

Intensifying Brand Competition and Expanding Vehicle Accessibility

The Qatar automotive market is benefiting from an unprecedented wave of new brand entries, dealership expansions, and diversified product offerings that are broadening vehicle accessibility and consumer choice. Both established international manufacturers and emerging regional automakers are investing heavily in local dealership infrastructure, after-sales networks, and marketing campaigns to capture growing demand. This intensifying competition is driving innovation in pricing, financing, and service delivery, making vehicles more accessible to a wider consumer base including mid-income expatriate segments. The diversification of available brands and models ensures that consumer preferences across luxury, performance, and value segments are comprehensively addressed. The country's strategic importance as a gateway market for new automotive brand launches continues to attract global manufacturers seeking to establish regional footholds, further enriching the competitive landscape and strengthening consumer access to diverse mobility solutions.

Market Restraints:

What Challenges the Qatar Automotive Market is Facing?

Limited Electric Vehicle Charging Infrastructure and High EV Costs

Despite government commitments to sustainable mobility, the Qatar automotive market faces challenges from insufficient electric vehicle charging infrastructure and high EV price points. The current network of fast chargers remains far below projected future requirements, creating range anxiety among potential buyers. The high upfront cost of electric vehicles compared to conventional alternatives, combined with consumer concerns about battery performance in extreme summer temperatures, continues to limit EV adoption and constrain the growth of emerging powertrain segments.

Volatility in Global Supply Chains and Import Dependencies

Qatar’s automotive market is entirely dependent on vehicle imports, making it vulnerable to disruptions in global supply chains, shipping logistics, and international trade policies. Fluctuations in shipping costs, semiconductor shortages, and delays in vehicle production at overseas manufacturing plants can impact model availability, increase waiting times, and elevate vehicle prices. This import dependency also means that sudden changes in trade tariffs, sanctions, or geopolitical tensions can directly affect the cost and availability of vehicles and spare parts, creating uncertainty for dealers and consumers.

Consumer Hesitancy Toward New and Unfamiliar Brands

While new automotive brands, particularly from China, are gaining market share, a significant portion of Qatari consumers remains cautious about unfamiliar brands due to concerns about long-term vehicle reliability, resale value retention, spare parts availability, and after-sales service quality. The established dominance of Toyota, Nissan, and other legacy brands reflects deep-rooted consumer trust built over decades. Overcoming these trust barriers requires sustained investment in service networks, warranty programs, and brand-building efforts, which remains a challenge for newer entrants.

Competitive Landscape:

The Qatar automotive market features a dynamic competitive environment shaped by the presence of established global manufacturers alongside rapidly emerging brands. Competition is driven by dealership network expansion, product portfolio diversification, technology integration, and customer service excellence. Market participants are increasingly differentiating through digital retail capabilities, integrated financing solutions, premium showroom experiences, and comprehensive after-sales support. The entry of Chinese automakers has intensified price competition, pushing established brands to enhance value propositions. Strategic partnerships between international manufacturers and local distributors are strengthening brand accessibility, while investments in electric vehicle infrastructure and sustainable mobility solutions are positioning forward-thinking market players for long-term competitive advantage in Qatar’s evolving automotive landscape.

Qatar Automotive Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Vehicle Types Covered |

|

|

Propulsion Types Covered |

Internal Combustion Engine (ICE), Hybrid Vehicles (HEV/PHEV), Electric Vehicles (BEV) |

|

Applications Covered |

Personal Use, Commercial Use, Public Transport, Industrial/Utility Use |

|

Ownership Models Covered |

Individual Ownership, Fleet Ownership, Subscription-Based Ownership, Shared Mobility (Ride-hailing, Car-sharing) |

|

Sales Channels Covered |

OEM/Authorized Dealers, Independent/Used Vehicle Dealers, Online Platforms, Direct-to-Consumer (D2C) |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Automotive Market Report

The Qatar automotive market size was valued at USD 4,463.28 Million in 2025.

The Qatar automotive market is expected to grow at a compound annual growth rate of 3.00% from 2026-2034 to reach USD 5,826.01 Million by 2034.

Passenger cars dominated the market with a share of 52.3%, driven by high consumer purchasing power, growing population, diverse model availability, and strong preference for SUVs and personal mobility solutions across both national and expatriate demographics.

Key factors driving the Qatar automotive market include robust economic diversification, rising consumer incomes, strategic government infrastructure investments, expanding dealership networks, intensifying brand competition, and increasing vehicle financing accessibility.

Major challenges include limited EV charging infrastructure, high electric vehicle costs, global supply chain vulnerabilities affecting vehicle imports, extreme climate conditions impacting battery technology, and consumer hesitancy toward newer automotive brands.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)