Qatar Combined Cycle Power Plant Market Size, Share, Trends and Forecast by Fuel Type, Application, End User, and Region, 2026-2034

Qatar Combined Cycle Power Plant Market Summary:

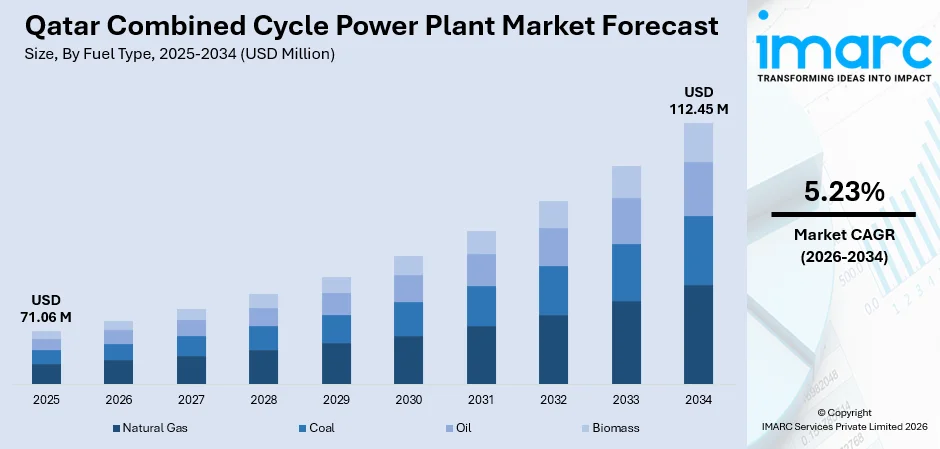

The Qatar combined cycle power plant market size was valued at USD 71.06 Million in 2025 and is projected to reach USD 112.45 Million by 2034, growing at a compound annual growth rate of 5.23% from 2026-2034.

The Qatar combined cycle power plant market is expanding steadily as rising electricity consumption, large-scale infrastructure development, and national energy security priorities drive sustained investment in high-efficiency gas-fired generation. Government-led modernization of the power sector, combined with growing industrial and residential demand, is reinforcing the deployment of advanced combined cycle systems to ensure reliable baseload power supply across the Qatar combined cycle power plant market share.

Key Takeaways and Insights:

- By Fuel Type: Natural gas dominates the market with a share of 91.4% in 2025, owing to Qatar’s abundant domestic reserves, established pipeline infrastructure, and the superior thermal efficiency of gas-fired combined cycle systems. Continuous investments in gas production are fueling the market expansion.

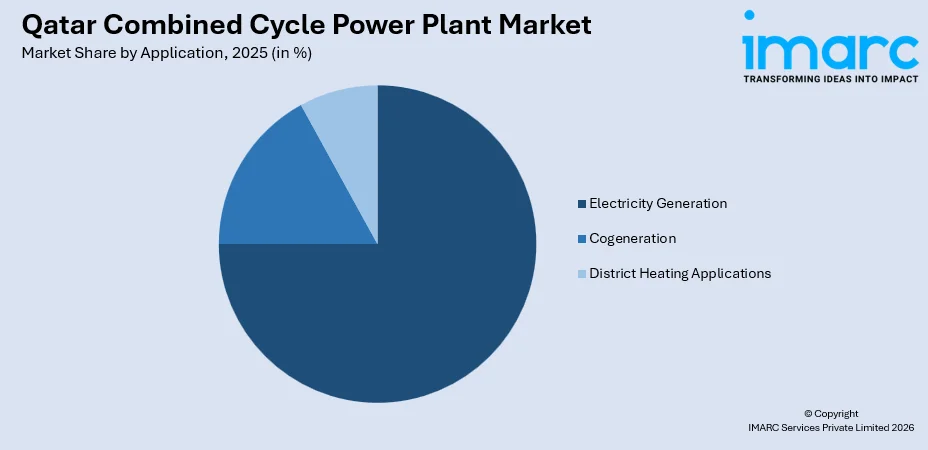

- By Application: Electricity generation leads the market with a share of 74.6% in 2025. This dominance is driven by rapidly growing power demand, the need for reliable baseload generation capacity, and ongoing investments in new combined cycle facilities to meet projected electricity consumption increases across the country.

- By End User: Utilities represent the largest segment with a market share of 68.9% in 2025, reflecting Kahramaa’s central role in commissioning and managing national power generation infrastructure, and the government’s strategic reliance on utility-scale combined cycle plants for grid stability and energy security.

- By Region: Ad Dawhah comprises the biggest region with 46.8% share in 2025, driven by the concentration of population, commercial activity, government infrastructure, and proximity to major power generation and water desalination facilities in the Ras Abu Fontas industrial zone.

- Key Players: The market is characterized by competition among international EPC contractors, turbine manufacturers, and regional energy firms partnering with state utilities. Players compete on efficiency, project delivery capability, financing strength, and long-term service agreements, with government backed tenders shaping contract awards and market positioning.

To get more information on this market Request Sample

The Qatar combined cycle power plant market is strengthening as the country pursues comprehensive energy infrastructure development aligned with the Qatar National Vision 2030 and the Third National Development Strategy 2024–2030. Rising electricity consumption, which reached 56 terawatt-hours in 2024 according to Enerdata, growing at 6.5% annually since 2020, is creating sustained demand for efficient baseload power generation. Combined cycle gas turbine plants currently account for majority of Qatar’s generation capacity, serving as the backbone of the national power system due to their superior fuel efficiency and compatibility with abundant natural gas resources. The government’s strategy to retire aging open-cycle gas turbine facilities and replace them with modern high-efficiency combined cycle plants is driving significant capital investment. Simultaneously, the integration of renewable energy into the power mix necessitates flexible combined cycle infrastructure capable of complementing intermittent solar generation and maintaining grid reliability during demand fluctuations across the forecast period.

Qatar Combined Cycle Power Plant Market Trends:

Deployment of high-efficiency H-class gas turbine technology

Qatar is increasingly adopting advanced H-class gas turbine technology for its combined cycle power plants, achieving substantial thermal efficiency levels. The Facility E project in Ras Abu Fontas, awarded in November 2024, will deploy high-efficiency gas turbines within a 2,400-megawatt combined cycle configuration that consumes less natural gas and produces lower emissions compared to existing plants. This technology transition reflects Qatar’s commitment to maximizing power output per unit of fuel consumed while aligning with national decarbonization objectives and the Qatar combined cycle power plant market growth.

Integration of combined cycle plants with desalination infrastructure

Qatar continues to develop integrated water and power projects that combine combined cycle power generation with seawater desalination, optimizing resource utilization and capital efficiency. For instance, in January 2026, Ras Abu Fontas Power secured USD 990 Million from JBIC within a USD 2.97 Billion package to expand a 2,400 MW gas-fired combined cycle plant and 110 MIGD desalination facility, supplying Kahramaa under a 25-year agreement. This co-generation approach leverages waste heat from power generation for desalination processes, enhancing overall system efficiency.

Grid modernization and transmission capacity expansion

Qatar is investing substantially in grid modernization to accommodate expanding combined cycle generation capacity. As such, in May 2025, Kahramaa signed four strategic contracts valued at approximately 3.1 Billion Qatari Riyals for the construction of seven high-voltage substations and 212 kilometers of underground cables and overhead transmission lines. This infrastructure expansion ensures efficient power evacuation from new combined cycle plants and enhances grid reliability across the national electricity network.

Market Outlook 2026-2034:

The Qatar combined cycle power plant market is poised for continued growth, supported by robust electricity demand projections, ambitious infrastructure investment programs, and the government’s commitment to deploying high-efficiency gas-fired generation capacity. Qatar’s electricity demand is projected to increase by approximately 58% by 2040 compared to 2021 levels, necessitating substantial additions to combined cycle generation infrastructure. Strategic investments in new combined cycle facilities, grid modernization programs, and the replacement of aging generation assets are expected to sustain market momentum. The growing role of combined cycle plants as flexible partners to expanding renewable capacity further reinforces their long-term strategic importance within Qatar’s evolving energy landscape. The market generated a revenue of USD 71.06 Million in 2025 and is projected to reach a revenue of USD 112.45 Million by 2034, growing at a compound annual growth rate of 5.23% from 2026-2034.

Qatar Combined Cycle Power Plant Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Fuel Type |

Natural Gas |

91.4% |

|

Application |

Electricity Generation |

74.6% |

|

End User |

Utilities |

68.9% |

|

Region |

Ad Dawhah |

46.8% |

Fuel Type Insights:

- Natural Gas

- Coal

- Oil

- Biomass

Natural gas dominates with a market share of 91.4% of the total Qatar combined cycle power plant market in 2025.

Natural gas is the foundational fuel for combined cycle power generation in Qatar, leveraging the country’s position as one of the world’s largest natural gas producers with proven reserves of approximately 843 trillion cubic feet. Qatar’s gas-fired combined cycle plants benefit from domestically sourced fuel at competitive prices through QatarEnergy, eliminating import dependency and ensuring stable input costs. The country’s extensive gas pipeline infrastructure and established fuel procurement frameworks further reinforce natural gas as the most economically viable and strategically secure fuel source for baseload power generation across the market.

The strategic importance of natural gas in Qatar’s combined cycle fleet is further strengthened by advancing turbine technologies that maximize fuel conversion efficiency. In 2024, natural gas accounted for 12 gigawatts of installed power generation capacity according to Climatescope, generating approximately 58.87 terawatt-hours of electricity and reinforcing the fuel’s near-total dominance in the country’s power generation landscape. Modern high-efficiency gas turbines deployed in new projects such as Facility E consume less gas and emit lower pollutants compared to older generation equipment, supporting Qatar’s decarbonization efforts while maintaining natural gas primacy.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Electricity Generation

- Cogeneration

- District Heating Applications

Electricity generation leads with a share of 74.6% of the total Qatar combined cycle power plant market in 2025.

Electricity generation remains the main application for combined cycle power plants in Qatar, supported by rising power demand and the government’s commitment to maintaining reliable supply across residential, commercial, and industrial segments. Rapid urban growth, expanding desalination capacity, and heavy air conditioning requirements continue to place sustained pressure on the national grid. Combined cycle facilities provide high efficiency and dependable baseload output, making them central to the country’s generation mix. Their operational flexibility also supports grid stability as energy demand patterns evolve.

The electricity generation segment is supported by continued investment in new combined cycle capacity to replace aging assets and accommodate future demand growth. Kahramaa has partnered with QatarEnergy, Qatar Electricity and Water Company, and Sumitomo Corporation to develop the Ras Abu Fontas Power and Water Facility, reinforcing long term supply planning. The project highlights the strategic importance of combined cycle plants in safeguarding national energy security, ensuring stable baseload generation, and sustaining Qatar’s industrial expansion and urban development objectives.

End User Insights:

- Utilities

- Manufacturing

- Oil and Gas

- Others

The utilities segment exhibits a clear dominance with a 68.9% share of the total Qatar combined cycle power plant market in 2025.

The utilities sector represents the largest end-user segment for combined cycle power plants in Qatar, reflecting the government’s centralized approach to power generation and distribution through Kahramaa and Qatar Electricity and Water Company. Utility-scale combined cycle facilities provide the majority of Qatar’s grid-connected generation capacity, operating under long-term power purchase agreements that ensure revenue stability and support sustained infrastructure investment. In February 2025, Kahramaa and QEWC signed a power purchase agreement valued at approximately 1.6 Billion Qatari Riyals for 511 megawatts of peak generation capacity at Ras Abu Fontas, reinforcing the utility sector’s dominant procurement role.

Utilities remain the primary drivers of combined cycle power plant deployment in Qatar through centralized planning, capacity procurement, and long-term infrastructure development aligned with national energy objectives. Kahramaa oversees an extensive generation and grid network that enables the integration of new combined cycle projects. With exclusive control over transmission and distribution systems, the utility sector determines investment priorities and project timelines. This centralized structure positions utilities as the main force sustaining combined cycle expansion and long-term market growth.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah holds the largest share at 46.8% of the total Qatar combined cycle power plant market in 2025.

Ad Dawhah, which includes Doha and its surrounding metropolitan area, holds the largest regional share in Qatar’s combined cycle power plant market. Its proximity to the Ras Abu Fontas industrial zone, home to major power and desalination facilities, strengthens its position within the national generation network. The region’s dense population, extensive commercial activity, and concentration of government institutions create the highest electricity demand in the country, reinforcing the need for reliable large scale thermal generation capacity.

Ongoing urban expansion, transport infrastructure development, and growth in mixed use real estate projects continue to elevate baseload requirements in the capital region. As such, Qatar invested USD 70 Billion in transport infrastructure under National Vision 2030, with Doha at the center through the Expressway Programme, Lusail Expressway, and advanced ITS systems, expanding road networks and smart mobility to support rapid urban growth and major events. As the administrative and economic center of Qatar, Ad Dawhah remains the focal point for capacity additions, grid upgrades, and long term thermal generation planning to ensure stable electricity supply.

Market Dynamics:

Growth Drivers:

Why is the Qatar Combined Cycle Power Plant Market Growing?

Surging electricity demand driven by urbanization and industrial expansion

Qatar’s rapidly growing electricity consumption is a fundamental driver of combined cycle power plant investment. The country’s electricity demand has been expanding, driven by increasing air conditioning usage, expanding water desalination operations, and accelerating urbanization. The residential sector accounts for 47% of total electricity consumption, followed by services at 29% and industry at 24%, reflecting diversified demand across all economic segments that requires reliable baseload generation. Looking forward, Qatar’s electricity demand is projected to increase, creating a sustained need for additional generation capacity. Combined cycle gas turbine plants are uniquely positioned to address this demand through their superior fuel efficiency, operational flexibility, and ability to deliver reliable baseload power generation at scale.

Strategic government investment in power infrastructure modernization

The Qatari government is committing significant capital toward upgrading and expanding the country’s power generation and transmission infrastructure, reinforcing a supportive environment for combined cycle power plant development. Through strategic agreements led by Kahramaa, the electricity network is being strengthened with new substations, expanded transmission corridors, and grid reinforcement projects designed to improve reliability and accommodate future capacity additions. These upgrades are critical for integrating new thermal generation assets and maintaining stable power distribution across industrial, commercial, and residential demand centers. In parallel, the government continues to advance large scale combined cycle power and desalination projects that rank among the most prominent energy investments in the country. Such developments highlight the central role of efficient gas fired generation in supporting long term energy security, economic expansion, and national infrastructure growth.

Need for flexible generation to complement expanding renewable capacity

Qatar’s growing renewable energy portfolio is creating complementary demand for flexible combined cycle power plants capable of balancing intermittent solar generation and maintaining grid stability. The country’s solar capacity reached 1,675 megawatts in 2025 following the inauguration of the Ras Laffan and Mesaieed plants, with plans to scale to over 4,000 megawatts by 2030 through additional projects including the 2,000-megawatt Dukhan solar plant. As solar generation introduces variability into the power mix, combined cycle plants provide essential ramping capability and reliable backup generation. The Qatar National Renewable Energy Strategy envisions a power mix where combined cycle gas turbine generation maintains approximately 72% of total generation by 2030, declining from 80% as renewables expand but continuing to provide the flexible foundation upon which solar and other clean energy sources can be reliably integrated.

Market Restraints:

What Challenges the Qatar Combined Cycle Power Plant Market is Facing?

High capital expenditure requirements for large-scale combined cycle projects

The development of combined cycle power plants in Qatar involves high upfront capital commitments, complex engineering requirements, and extended construction timelines. Large scale facilities demand advanced turbines, heat recovery systems, grid interconnection works, and supporting desalination infrastructure, all of which increase financial exposure. These projects often rely on structured financing models involving international lenders and export credit agencies. The scale and cost intensity can slow new capacity additions and require careful coordination between sponsors, contractors, and government stakeholders.

Growing competition from renewable energy alternatives

The rapid expansion of renewable energy, particularly solar photovoltaic generation, is creating stronger competition for investment allocation and grid access. As solar technology becomes more cost competitive and national targets prioritize cleaner energy sources, gas fired generation faces gradual pressure within the power mix. Policy direction increasingly supports diversification, which may reduce the long-term share of combined cycle plants in future capacity planning and influence procurement strategies across the sector.

Environmental regulatory pressures and decarbonization mandates

Environmental regulations and national decarbonization commitments are adding operational and compliance pressures to gas fired combined cycle plants. International sustainability standards and emissions reporting requirements are tightening expectations for environmental performance, especially in export linked energy systems. At the same time, domestic carbon reduction initiatives and carbon capture programs introduce additional technical and financial obligations. These evolving requirements may raise lifecycle costs and encourage efficiency upgrades or integration with emissions mitigation technologies.

Competitive Landscape:

The Qatar combined cycle power plant market is characterized by a concentrated competitive landscape dominated by leading international engineering, procurement, and construction firms alongside established gas turbine original equipment manufacturers. Major players compete for large-scale government-commissioned projects through strategic consortia that combine engineering expertise, equipment supply capabilities, and project financing capacity. Competition centers on technological differentiation through higher efficiency turbines, hydrogen-ready combustion systems, and integrated power-plus-desalination solutions. Long-term service agreements and operations and maintenance contracts represent additional revenue streams that strengthen competitive positioning within the market.

Recent Developments:

- In December 2025, Doosan Enerbility secured a KRW 130 Billion (approximately USD 88.5 Million) equipment supply contract from Samsung C&T for the Facility E combined cycle power plant in Qatar. Under the agreement, Doosan Enerbility will supply two 430-megawatt-class steam turbines, generators, and auxiliary equipment for the 2,400-megawatt plant in Ras Abu Fontas, with deliveries scheduled for completion by 2029.

- In November 2025, Syria signed concession agreements with a consortium led by Qatar’s Urbacon Holding to develop eight power plants totaling 5 GW, including four gas-fired combined cycle plants and four solar projects. The public-private partnership aims to double national output within three years for gas and two years for solar.

Qatar Combined Cycle Power Plant Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Fuel Types Covered |

Natural Gas, Coal, Oil, Biomass |

|

Applications Covered |

Electricity Generation, Cogeneration, District Heating Applications |

|

End Users Covered |

Utilities, Manufacturing, Oil and Gas, Others |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Combined Cycle Power Plant Market Report

The Qatar combined cycle power plant market size was valued at USD 71.06 Million in 2025.

The Qatar combined cycle power plant market is expected to grow at a compound annual growth rate of 5.23% from 2026-2034 to reach USD 112.45 Million by 2034.

Natural gas dominated the market with a share of 91.4%, driven by Qatar’s abundant domestic reserves, established fuel supply infrastructure, superior thermal efficiency of gas-fired combined cycle systems, and strategic alignment with national energy policy.

Key factors driving the Qatar combined cycle power plant market include surging electricity demand, strategic government investments in power infrastructure modernization, the need for flexible generation to complement expanding renewable energy capacity, and retirement of aging generation assets.

Major challenges include high capital expenditure requirements for large-scale projects, growing competition from renewable energy alternatives, environmental regulatory pressures, decarbonization mandates, and the need for complex international consortia to execute large-scale combined cycle developments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)