Qatar Dairy Market Size, Share, Trends and Forecast by Product Type and Region, 2026-2034

Qatar Dairy Market Summary:

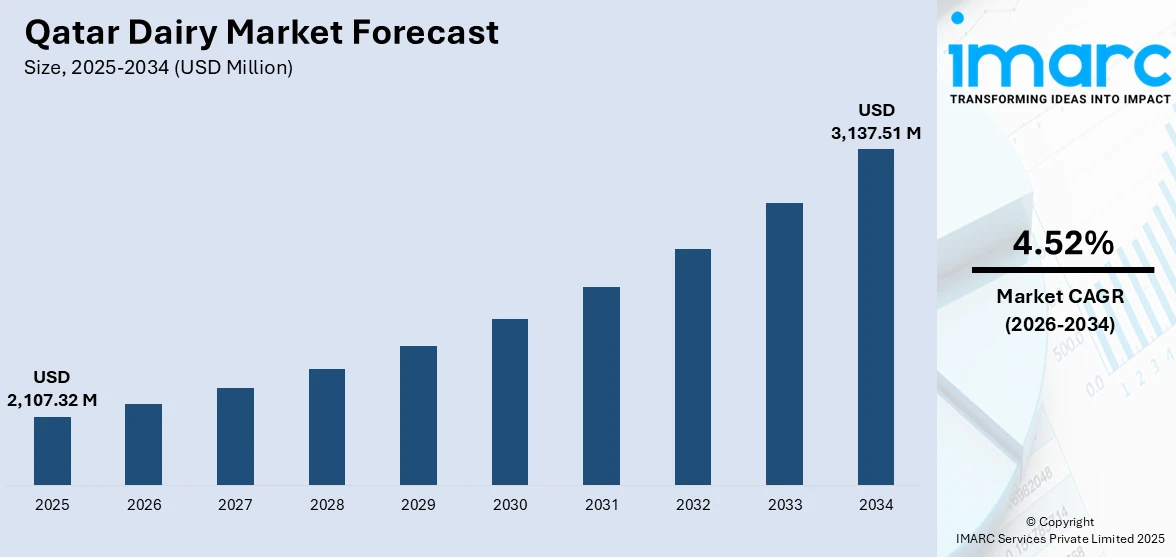

The Qatar dairy market size was valued at USD 2,107.32 Million in 2025 and is projected to reach USD 3,137.51 Million by 2034, growing at a compound annual growth rate of 4.52% from 2026-2034.

The Qatar dairy market is expanding steadily as the nation strengthens its domestic production capabilities and prioritizes food self-sufficiency. Growing consumer health awareness, rising demand for premium and functional dairy products, and an increasingly diverse expatriate population are accelerating consumption patterns. Government-led food security strategies, modernized farming infrastructure, and investments in advanced processing technologies are reinforcing production capacity, positioning Qatar as a resilient and evolving dairy market within the broader Gulf region and supporting the Qatar dairy market share.

Key Takeaways and Insights:

- By Product Type: Liquid milk dominates the market with a share of 34% in 2025, driven by high daily consumption rates, established local production infrastructure, and government support for fresh milk self-sufficiency across the nation.

- By Region: Ad Dawhah leads the market with a share of 50% in 2025, reflecting the capital's concentration of population, retail outlets, hospitality establishments, and institutional demand for dairy products.

- Key Players: The Qatar dairy market features a competitive landscape shaped by dominant local producers operating alongside established international brands, with companies competing through product innovation, supply chain integration, quality certifications, and strategic partnerships to capture a growing consumer base across diverse retail and institutional channels.

To get more information on this market Request Sample

The Qatar dairy market is undergoing a significant transformation driven by the convergence of food security imperatives, technological innovation, and evolving consumer preferences. The nation has achieved approximately 98% self-sufficiency in fresh dairy production, a milestone largely attributed to strategic public-private partnerships and substantial investments in climate-controlled farming infrastructure. Qatar’s dairy sector is being shaped by a strong national focus on food security and long-term sustainability. Policy direction emphasizes strengthening domestic production, building resilient supply chains, and reducing pressure on natural resources used in agriculture. Alongside these structural priorities, consumer preferences are shifting toward health-oriented dairy products, including organic and functional offerings. This change is encouraging producers to broaden their product ranges and invest in more advanced processing technologies. Together, sustainability objectives and evolving demand patterns are reshaping competitive dynamics and supporting the continued development of Qatar’s dairy market.

Qatar Dairy Market Trends:

Growing Demand for Premium and Functional Dairy Products

Consumers in Qatar are increasingly favoring premium and health-oriented dairy products such as organic milk, fortified drinks, high-protein yoghurts, and probiotic-rich options. Growing health awareness among affluent consumers, along with diverse preferences within the expatriate population, is driving demand for higher-quality and functionally enhanced dairy offerings. In response, producers are expanding and refining their product portfolios to address evolving tastes across multiple segments. This shift toward value-added dairy is stimulating ongoing product innovation and contributing to a more dynamic and differentiated dairy market in Qatar.

Adoption of Advanced Dairy Farming Technologies

Qatar is leveraging cutting-edge agricultural technologies to overcome the challenges posed by its arid climate and limited natural resources. Climate-controlled barns, automated milking parlours, and precision farming systems have become integral to the country's dairy operations. For instance, Baladna's facilities, spanning two million square metres across two farms with 40 barns equipped with state-of-the-art milking systems, exemplify this modernization. The country’s dairy productivity has improved significantly, reaching standards comparable to those of leading global producers. This progress highlights the impact of technology-driven farming practices in enhancing efficiency, consistency, and overall quality within the dairy sector.

Expansion of Value-Added Dairy Segments

The Qatar dairy market is increasingly shifting toward value-added products such as cheese, flavored milk, and specialty yoghurt varieties. Consumers are showing stronger preference for convenient, ready-to-consume options and diverse flavor profiles inspired by global tastes. This evolving demand is encouraging producers and retailers to expand beyond traditional dairy products and introduce more differentiated offerings. As product ranges become broader and more premium-oriented, competition within the market is intensifying. This diversification is supporting long-term market development while enhancing consumer choice and strengthening brand positioning across Qatar’s dairy sector.

Market Outlook 2026-2034:

The Qatar dairy market is positioned for sustained expansion over the forecast period, underpinned by continued government investment in food security infrastructure, growing consumer demand for diversified and premium dairy products, and the deepening integration of advanced production technologies. Rising urbanization, increasing per capita income, and an expanding hospitality sector are expected to drive higher consumption volumes across all product categories. Strategic initiatives targeting domestic capacity building and international trade diversification will further strengthen the market's resilience. The market generated a revenue of USD 2,107.32 Million in 2025 and is projected to reach a revenue of USD 3,137.51 Million by 2034, growing at a compound annual growth rate of 4.52% from 2026-2034.

Qatar Dairy Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Liquid Milk |

34% |

|

Region |

Ad Dawhah |

50% |

Product Type Insights:

- Liquid Milk

- Flavored Milk

- Cream

- Butter

- Cheese

- Yoghurt

- Ice Cream

- Anhydrous Milk Fat (AMF)

- Skimmed Milk Powder (SMP)

- Whole Milk Powder (WMP)

- Whey Protein

- Lactose Powder

- Curd

- Paneer

Liquid milk dominates with a market share of 34% of the total Qatar dairy market in 2025.

Liquid milk holds a dominant position in Qatar’s dairy sector due to its role as a daily staple consumed across households, institutions, and foodservice channels. Strong emphasis on domestic fresh milk production has encouraged the development of large, vertically integrated dairy operations supported by advanced climate-controlled systems. These investments have strengthened local supply capabilities, reduced reliance on imports, and ensured stable availability throughout the year. As a result, liquid milk remains widely accessible and trusted, reinforcing its importance within the country’s food security and everyday consumption patterns.

Consumer preferences within the liquid milk category are gradually shifting toward healthier and more specialized options. Growing interest in organic, fortified, and lactose-free variants reflects wider wellness trends and increased nutritional awareness. Improvements in processing and packaging technologies have enhanced shelf life and distribution efficiency, allowing products to reach a broader range of retail and institutional outlets. At the same time, continued investment in domestic processing capacity is supporting product diversification, strengthening the liquid milk value chain, and reinforcing Qatar’s commitment to a resilient and self-sufficient dairy sector.

Region Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah represent the largest share at 50% of the total Qatar dairy market in 2025.

Ad Dawhah, Qatar's capital and most densely populated municipality, accounts for the largest regional share of the dairy market, driven by its concentration of commercial establishments, hospitality outlets, institutional buyers, and a diverse consumer base comprising both nationals and expatriates. The municipality serves as the primary hub for retail distribution networks, including major supermarket chains and hypermarkets, which facilitate high-volume dairy product sales. The presence of international hotel chains, airline catering operations, and healthcare institutions generates significant institutional demand for a broad range of dairy products.

The capital benefits from a well-developed cold chain and efficient logistics networks that ensure smooth movement of dairy products from production facilities to retail shelves. This infrastructure supports the consistent availability of fresh products and enhances consumer access across the city. Strong demand is reinforced by a growing population, higher spending power, and an expanding food service sector, including institutional and hospitality consumption. Together, these factors strengthen the capital’s role as the primary hub for dairy distribution and consumption, maintaining its leading position within the national dairy market.

Market Dynamics:

Growth Drivers:

Why is the Qatar Dairy Market Growing?

Government-Led Food Security Initiatives and Self-Sufficiency Programs

The Qatar government has placed food security at the centre of its national development agenda, implementing comprehensive strategies and substantial investments to strengthen domestic dairy production capabilities. The National Food Security Strategy 2030, launched in December 2024 by the Ministry of Municipality, targets maintaining complete self-sufficiency in dairy and fresh poultry production while advancing sustainability goals across the agricultural sector. The strategy is structured around multiple initiatives aligned with key pillars that emphasize strengthening local production, building strategic reserves, and diversifying trade relationships. A strong focus on self-sufficiency has helped stabilize the fresh dairy supply over time. Ongoing government support through the distribution of advanced farming equipment, such as controlled-environment and water-efficient systems, is encouraging sustainable agricultural practices and improving long-term productivity across the sector.

Rapid Population Growth and Diverse Expatriate Demographics

Qatar’s growing population, supported by ongoing economic activity and infrastructure development, is a key driver of increasing dairy consumption. A large and diverse expatriate community contributes to varied dietary habits, creating demand for a broad spectrum of dairy products. Consumers seek everything from everyday fresh milk and yoghurt to international cheese styles, flavored drinks, and specialty dairy items. High purchasing power further supports this trend, allowing households to spend more on premium and value-added offerings. Together, demographic expansion, cultural diversity, and strong consumer spending capacity are reinforcing demand across multiple dairy categories and strengthening growth across retail and foodservice channels.

Investments in Advanced Production Infrastructure and Technology

The dairy sector in Qatar is absorbing massive investment in modern dairy production and processing that is enhancing capacity and efficiency in the sector. Improved solutions like climate regulation housing, automatized milking systems, and precision-based farming systems have helped the producers to be able to perform their functions despite the stringent environmental conditions. Mega facilities that are vertically integrated are contributing to a steady production, a better quality level, and better cost management. These enhancements are also promoting an increased product diversification and operational performance. Simultaneously, the implementation of internationally accepted food safety and quality systems is increasing industry standards. Combined, long-term capital investment and the modernization that is driven by technology are driving productivity, bolstering competitiveness, and contributing to the long-term stability of the domestic Qatar dairy industry.

Market Restraints:

What Challenges the Qatar Dairy Market is Facing?

High Dependence on Imported Animal Feed and Raw Materials

Qatar's dairy industry relies heavily on imported animal feed, including hay sourced from Asia, Europe, and Africa, which exposes producers to global commodity price fluctuations, supply chain disruptions, and elevated logistics costs. This dependence on external inputs constrains production cost management and limits the ability of dairy operators to maintain competitive pricing, particularly during periods of international trade volatility or geopolitical uncertainty.

Extreme Climatic Conditions Impacting Livestock Management

The extreme weather conditions in Qatar are a problem that presents difficulties to the livestock health, welfare, and productivity due to the harsh desert climate with temperatures that are above 45 degrees Celsius during summer. To ensure favorable working environments in dairy cattle production, a lot of money is necessary for climate-controlled buildings and cooling units, which increases the cost of operation. These environmental factors restrict the expansion of dairy farming activities and make it more expensive to attain comparable levels of productivity to temperate climatic areas.

Limited Agricultural Land and Water Resource Scarcity

Limited availability of arable land and freshwater supply in Qatar limits the possibilities of developing dairy farming businesses and increasing the production of animal fodder at home. Use of desalinated water to irrigate agricultural land raises the cost of production substantially, and there is also a lack of land to build new farming units. These resource limitations continue to pose constant problems in expanding domestic production capacity to satisfy rising demand caused by population growth and the changing consumption trends.

Competitive Landscape:

The Qatar dairy market features a concentrated competitive structure anchored by a dominant local producer that has achieved near-complete market coverage in fresh milk and related product categories. Competition is intensifying as international brands expand their presence through strategic partnerships with local distributors and retailers. Market participants are differentiating through product innovation, including the introduction of health-focused formulations, premium packaging formats, and expanded flavour portfolios. Investments in vertically integrated production models, advanced food safety certifications, and institutional supply contracts are shaping competitive strategies. Retail channel diversification, including expanded online availability and direct-to-consumer offerings, is further influencing market positioning among both domestic and imported dairy brands.

Recent Developments:

- In November 2025, Baladna Q.P.S.C. proposed a 24% capital increase through a rights issue to accelerate its international expansion strategy, following record nine-month financial performance with revenue of QAR 941 million and net profit of QAR 381 million. The company targets increasing EBITDA to QAR 1.4 billion by 2030 through international market entry and operational efficiency improvements.

- In February 2025, LuLu Qatar launched a dedicated showcase of British dairy products in collaboration with the Agriculture and Horticulture Development Board and the United Kingdom's Department of Business and Trade. The initiative expanded access to premium imported dairy offerings across LuLu's retail network in Qatar.

Qatar Dairy Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Million |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

Liquid Milk, Flavored Milk, Cream, Butter, Cheese, Yoghurt, Ice Cream, Anhydrous Milk Fat (AMF), Skimmed Milk Powder (SMP), Whole Milk Powder (WMP), Whey Protein, Lactose Powder, Curd, Paneer |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Dairy Market Report

The Qatar dairy market size was valued at USD 2,107.32 Million in 2025.

The Qatar dairy market is expected to grow at a compound annual growth rate of 4.52% from 2026-2034 to reach USD 3,137.51 Million by 2034.

Liquid milk, representing the largest market share of 34% in 2025, continues to be the leading product category in Qatar's dairy market, driven by high daily consumption, established local production infrastructure, and government support for fresh milk self-sufficiency across the nation.

Key factors driving the Qatar dairy market include government-led food security initiatives targeting dairy self-sufficiency, rapid population growth with diverse expatriate demographics, investments in advanced dairy farming and processing technologies, and rising consumer demand for premium and health-focused dairy products.

Major challenges include high dependence on imported animal feed and raw materials, extreme climatic conditions affecting livestock management costs, limited agricultural land availability, water resource scarcity constraining production scalability, and competitive pressure from established international dairy brands.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)