Qatar Digital Banking Market Size, Share, Trends and Forecast by Services, Deployment Type, Technology, Industries, and Region, 2026-2034

Qatar Digital Banking Market Summary:

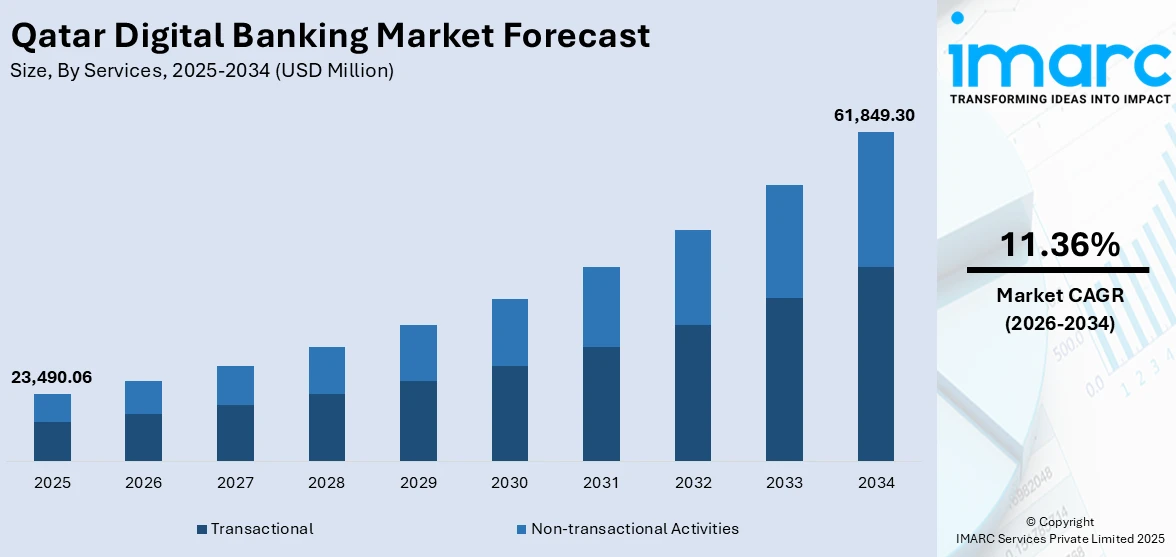

The Qatar digital banking market size was valued at USD 23,490.06 Million in 2025 and is projected to reach USD 61,849.30 Million by 2034, growing at a compound annual growth rate of 11.36% from 2026-2034.

The Qatar digital banking market is advancing rapidly as the nation accelerates its transition toward a fully digitalized financial ecosystem. Growing consumer preference for seamless, real-time banking experiences, coupled with supportive regulatory frameworks and robust digital infrastructure, is driving widespread adoption. Increasing smartphone penetration, rising demand for contactless transactions, and strategic fintech collaborations are reshaping the financial services landscape, positioning Qatar as an emerging digital banking hub in the Gulf region.

Key Takeaways and Insights:

- By Services: Transactional dominates the market with a share of 64% in 2025, spurred by the rise of digital financial transfers, cash management made possible by mobile devices, and automated debit and credit services that improve daily banking ease for Qatar's tech-savvy populace.

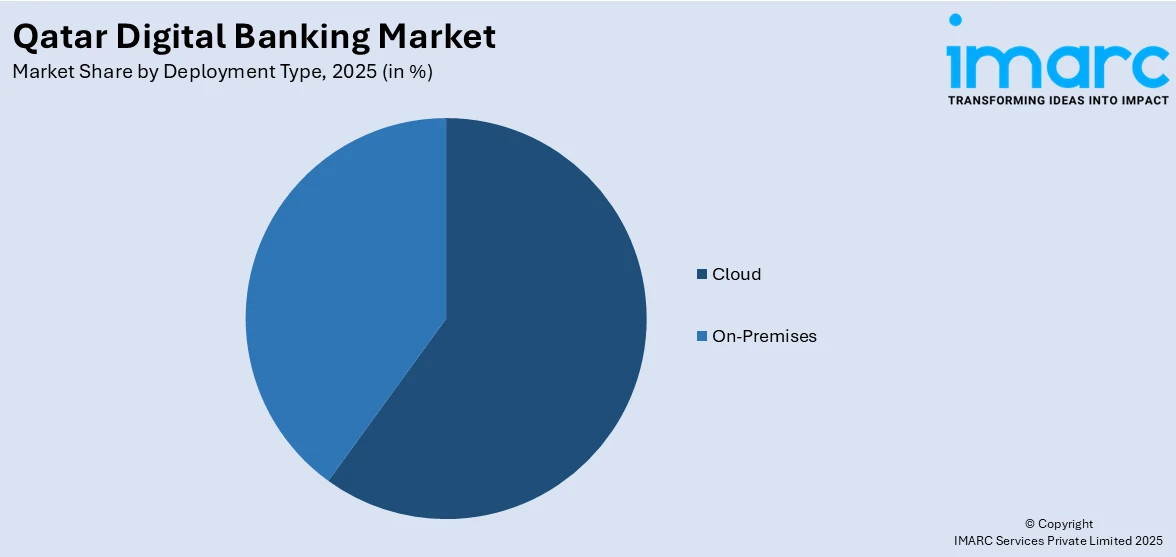

- By Deployment Type: Cloud leads the market with a share of 72% in 2025, because cloud-based systems give financial institutions the flexibility, cost-effectiveness, and quick deployment capabilities they need to modernize operations and provide clients with seamless digital experiences.

- By Technology: Mobile banking exhibits a clear dominance in the market with 46% share in 2025, demonstrating the broad use of smartphone-based banking apps that give tech-savvy customers fast payments, real-time account access, and customized financial management features.

- By Industries: Banking is the biggest segment with 38% share in 2025, driven by significant investments made by commercial and retail banking institutions in digital transformation projects, such as automated loan services, open banking platforms, and AI-powered client interaction.

- By Region: Ad Dawhah represents the largest region with 55% share in 2025, driven by the concentration of major financial institutions, a highly urbanized and tech-savvy population, and advanced digital infrastructure that supports widespread adoption of digital banking solutions.

- Key Players: Key players drive the Qatar digital banking market by expanding digital platforms, investing in AI and cloud-based solutions, strengthening cybersecurity frameworks, and forging strategic fintech partnerships. Their focus on open banking, mobile-first strategies, and regulatory compliance accelerates digital adoption and ensures consistent service delivery across diverse consumer and enterprise segments.

To get more information on this market Request Sample

The Qatar digital banking market is gaining robust momentum as the country pursues an ambitious digital transformation agenda anchored in the Qatar National Vision 2030 and the Third Financial Sector Strategy. Financial institutions are increasingly leveraging artificial intelligence, blockchain technology, and cloud computing to deliver enhanced customer experiences, streamline operations, and expand financial inclusion. The regulatory environment has become increasingly supportive, with the Qatar Central Bank issuing the Regulatory Framework for Digital Banks in December 2024, establishing comprehensive guidelines for digital-only lenders to operate through online and mobile platforms. This framework mandates that licensed digital banks comply with stringent cybersecurity, data protection, and anti-money laundering requirements while supporting both conventional and Islamic digital banking models. The nation's internet penetration rate stands at approximately 99.7%, creating a highly conducive environment for digital banking adoption. Rising demand for personalized financial services, expanding contactless payment ecosystems, and strategic collaborations between traditional banks and fintech firms are further reinforcing the Qatar digital banking market share.

Qatar Digital Banking Market Trends:

Accelerating Adoption of Open Banking Ecosystems

Qatar is witnessing a significant shift toward open banking frameworks as financial institutions embrace API-driven collaboration to foster innovation and improve customer engagement. Banks are progressively opening their core financial services to fintechs and third-party providers through secure digital interfaces, enabling seamless data sharing and payment facilitation across organizations. This collaborative approach is supporting the Qatar digital banking market growth. Regulatory encouragement, evolving consumer expectations, and rising fintech partnerships are creating a more interconnected, transparent, and customer-centric financial ecosystem across the country.

Rising Integration of Artificial Intelligence in Banking Operations

Artificial intelligence is reshaping how financial institutions in Qatar deliver services, manage risk, and engage customers. AI-powered chatbots, predictive analytics, and robo-advisory tools are enabling hyper-personalized banking experiences while reducing operational costs. According to a PwC survey, 90% of CEOs in Qatar adopted generative AI over the past year, surpassing the global average of 83%. Banks are increasingly deploying machine learning algorithms for credit scoring, fraud detection, and automated customer support to enhance operational efficiency and service delivery.

Expansion of Instant Payment Infrastructure

Qatar is rapidly expanding its real-time payment capabilities to support its transition toward a cashless economy. Instant payment platforms are gaining widespread traction, enabling consumers and businesses to execute transfers within seconds using simplified identification methods such as mobile numbers instead of traditional account details. This shift is significantly reducing transaction processing times and enhancing the convenience of digital financial interactions. The ongoing modernization of payment infrastructure, supported by growing registered user bases and rising transaction volumes, is reinforcing consumer confidence in digital payment channels across the country.

Market Outlook 2026-2034:

The Qatar digital banking market is poised for sustained expansion, underpinned by continuous regulatory support, advancing digital infrastructure, and an increasingly tech-savvy consumer base. Financial institutions are accelerating investments in cloud-native platforms, mobile-first solutions, and AI-driven services to meet evolving customer expectations. The market generated a revenue of USD 23,490.06 Million in 2025 and is projected to reach a revenue of USD 61,849.30 Million by 2034, growing at a compound annual growth rate of 11.36% from 2026-2034. The issuance of the Digital Banks Regulatory Framework by the Qatar Central Bank, coupled with the nation's near-universal internet penetration and growing fintech ecosystem, is expected to attract new digital banking entrants and stimulate product innovation. Strategic partnerships between established banks and technology providers, rising adoption of open banking and embedded finance solutions, and the expansion of real-time payment networks are anticipated to drive higher revenue streams and foster a more competitive, inclusive, and technologically advanced digital banking landscape across Qatar.

Qatar Digital Banking Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Services |

Transactional |

64% |

|

Deployment Type |

Cloud |

72% |

|

Technology |

Mobile Banking |

46% |

|

Industries |

Banking |

38% |

|

Region |

Ad Dawhah |

55% |

Services Insights:

- Transactional

- Cash Deposits and Withdrawals

- Fund Transfers

- Auto-Debit/Auto-Credit Services

- Loans

- Non-transactional Activities

- Information Security

- Risk Management

- Financial Planning

- Stock Advisory

Transactional dominates with a market share of 64% of the total Qatar digital banking market in 2025.

The transactional services segment leads the Qatar digital banking market, driven by the growing demand for real-time fund transfers, automated payment processing, and mobile-enabled cash management solutions. Consumers and businesses increasingly prefer digital channels for everyday banking operations, including bill payments, peer-to-peer transfers, and auto-debit services. The sustained growth in digital transaction volumes across the country demonstrates the expanding scale and depth of transactional banking activity, reinforcing the segment's dominant market position within the broader digital banking landscape.

The expansion of real-time payment infrastructure is further strengthening transactional banking services. Financial institutions are integrating advanced payment gateways, contactless solutions, and instant settlement mechanisms to enhance transaction speed and reliability. The adoption of simplified identification-based transfers has streamlined payment processes, enabling consumers to execute transfers using mobile numbers rather than traditional account details. Rising e-commerce activity, growing merchant acceptance of digital payments, and increasing corporate adoption of automated treasury management tools are contributing to sustained demand for transactional digital banking services across Qatar.

Deployment Type Insights:

Access the comprehensive market breakdown Request Sample

- On-Premises

- Cloud

Cloud leads with a share of 72% of the total Qatar digital banking market in 2025.

The highest market share in Qatar's digital banking industry is held by the cloud deployment segment, which reflects the financial sector's rapid transition to cloud-native banking solutions. Cloud infrastructure is being adopted by banks and fintech companies in order to provide seamless digital experiences while increasing scalability, operational agility, and cost effectiveness. Cloud-native platforms and API-based architectures are becoming more and more popular among financial institutions worldwide. In Qatar, this trend is especially noticeable as banks change their operational models to become data-driven and cloud-augmented, enabling quicker product deployment and improved customer engagement across a range of consumer segments.

Financial institutions can handle increasing transaction volumes, connect third-party apps, and quickly expand services with cloud-based deployment without having to make large capital investments in physical infrastructure. Institutions have been encouraged to move key banking functions to the cloud by the Qatar Central Bank's benevolent regulatory approach, which includes its fintech sandbox program and digital banking architecture. Cloud-based architectures that provide real-time data interchange and interoperability throughout the financial ecosystem are also required due to the increased focus on open banking, API-driven collaboration, and embedded finance solutions.

Technology Insights:

- Internet Banking

- Digital Payments

- Mobile Banking

Mobile banking is the largest segment, accounting for 46% of the total Qatar digital banking market in 2025.

Mobile banking dominates the technology segment of Qatar's digital banking market, driven by the country's exceptionally high smartphone penetration rate and a young, tech-savvy population that prioritizes convenience and real-time access to financial services. Banks are investing heavily in feature-rich mobile applications that offer personalized dashboards, biometric authentication, instant payments, and wealth management tools. In December 2024, AlRayan Bank launched its new mobile banking application, AlRayan Go, built on the Backbase platform, offering Sharia-compliant services including account access, transfers, card management, bill payments, and telecom top-ups.

The mobile-first banking approach is being further reinforced by consumer demand for contactless and on-the-go financial services. With approximately 96% of all in-store digital transactions in Qatar now conducted via contactless methods, mobile banking applications serve as the primary interface for managing payments, transfers, and account operations. Financial institutions are integrating AI-powered analytics within mobile platforms to deliver tailored product recommendations, spending insights, and predictive financial guidance, enhancing user engagement and driving the adoption of mobile banking solutions across diverse customer segments.

Industries Insights:

- Media and Entertainment

- Manufacturing

- Retail

- Banking

- Healthcare

Banking holds the largest share at 38% of the total Qatar digital banking market in 2025.

Since commercial and retail banks are still making significant investments in digital transformation to improve service delivery and customer retention, the banking sector is the largest end-user category in Qatar's digital banking market. To save expenses and optimize operations, traditional banks are using cloud-based platforms, incorporating AI-driven analytics, and updating their basic infrastructure. The nation's top financial institutions are driving innovation in digital banking through mobile-first design, open banking APIs, and strategic fintech partnerships that increase service accessibility and enhance the general customer experience for both corporate and retail customers.

In the banking industry, the regulatory environment has grown more receptive to digital innovation. Banks can now employ sandbox-tested solutions, investigate embedded finance models, and create new digital products thanks to the Qatar Central Bank's Third Financial Sector Strategy and National Fintech Strategy. In order to safeguard digital assets and foster customer confidence, banks are also investing in cybersecurity infrastructure, growing their digital lending platforms, and automating credit evaluations using machine learning algorithms. These actions are all contributing to the banking sector's dominant position in the Qatari digital banking market.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah represents the leading region with a 55% share of the total Qatar digital banking market in 2025.

As the nation's capital and main economic center, Ad Dawhah controls the majority of the digital banking business in Qatar. Strong demand for digital banking services is fueled by the concentration of important financial institutions, such as the main offices of top banks and fintech firms, as well as by the population's high level of urbanization and digital literacy. Advanced telecommunications infrastructure, broad merchant adoption of digital payment systems, and close proximity to important political and regulatory entities that influence the financial technology environment are all advantages for the town. Increased use of digital wallets, contactless payment methods, and mobile banking is also a result of high consumer purchasing power, a thriving business community, and an expanding foreign labor force.

Ad Dawhah's fintech incubators, innovation centers, and technology accelerators provide a vibrant atmosphere that encourages cooperation between financial institutions and technology suppliers. Prior to wider nationwide implementation, the area acts as the main testing ground for new open banking connectors, digital banking products, and AI-driven financial services. Rapid adoption of breakthrough financial technology is made possible by strong connections between private sector innovation hubs and public sector efforts. The region's dominant position in the market is further strengthened by the concentration of corporate headquarters and international corporations in Ad Dawhah, which creates a steady demand for enterprise-grade banking platforms, automated payroll systems, and sophisticated digital treasury management.

Market Dynamics:

Growth Drivers:

Why is the Qatar Digital Banking Market Growing?

Supportive Regulatory Framework and Government Initiatives

The use of financial technology and innovation in digital banking are actively promoted by the extensive regulatory environment that the Qatar Central Bank has set up. A significant advancement has been made with the creation of specific legal frameworks for lenders that solely operate online. These frameworks offer unambiguous operating standards pertaining to cybersecurity, data protection, anti-money laundering compliance, and capital needs. These frameworks increase the opportunities for new market entrants by supporting both traditional and Islamic digital banking models. The regulatory actions are in line with more comprehensive national financial sector plans that give the digital transformation of Qatar's financial services industry top priority. In order to speed up the time to market for new digital goods, the central bank has also implemented sandbox programs that allow fintech companies to test and implement creative ideas in regulated settings. Additionally, by establishing a more open and innovative environment that draws in both domestic and foreign digital banking players, government-backed initiatives are boosting institutional trust. Long-term stability and continuity are ensured when regulatory policies are in line with national economic diversification objectives. This promotes consistent investment in the nation's digital banking infrastructure and technological advancements.

High Digital Infrastructure Readiness and Smartphone Penetration

The spread of digital banking services throughout the nation is well-supported by Qatar's top-notch digital infrastructure. One of the quickest and most dependable communication settings in the Middle East is provided by extensive broadband access, a strong fiber-optic backbone, and statewide coverage of next-generation mobile networks. Financial institutions can create, implement, and grow complex digital banking products with efficiency and low latency thanks to our fast infrastructure. A youthful, tech-savvy populace that increasingly favors mobile-first banking services is contributing to the nation's constantly rising smartphone penetration rate. The trend toward digital financial services is being accelerated by a tech-savvy populace, which is driving up demand for contactless payment methods, digital wallets, and user-friendly mobile applications. Adoption of digital banking is significantly encouraged by the combination of favorable customer demographics and sophisticated telecommunications infrastructure. In order to improve customer engagement and achieve greater market penetration, financial institutions are using this connection advantage to launch cutting-edge services like personalized financial management tools, biometric verification, and real-time notifications.

Growing Fintech Ecosystem and Strategic Collaborations

With the help of focused incubation programs, smart alliances, and increasing investor activity, Qatar's fintech ecosystem is expanding quickly. Fintech hubs supported by the government are essential for fostering companies and speeding up the adoption of financial technology through financing support mechanisms, mentorship programs, and specialized accelerator programs. Growing investor confidence in the industry's potential for expansion is drawing in both foreign and domestic capital, which is fostering the creation of creative financial solutions suited to the demands of regional markets. Through the combination of institutional knowledge and entrepreneurial agility, strategic partnerships between well-established banks and Internet companies are propelling market development even further. These collaborations are accelerating the adoption of innovative financial technology, expanding support for high-potential entrepreneurs, and opening up new avenues for venture capital investment. Qatar is becoming known as a regional center for fintech innovation because to cooperation between financial institutions, development banks, and international technological networks. These ecosystem-level efforts are enhancing the overall competitiveness and resilience of Qatar's digital banking sector by creating an atmosphere where cutting-edge technical solutions and conventional banking skills meet.

Market Restraints:

What Challenges the Qatar Digital Banking Market is Facing?

Cybersecurity Threats and Data Privacy Concerns

The increasing digitalization of banking services exposes financial institutions to heightened cybersecurity risks, including data breaches, phishing attacks, and sophisticated fraud attempts. As digital banking platforms handle growing volumes of sensitive financial data, maintaining robust security frameworks becomes critical. The complexity of implementing advanced security measures, including biometric authentication, encryption protocols, and real-time threat monitoring systems, adds operational costs and technical challenges for financial institutions operating in the market.

Regulatory Compliance Complexities for New Entrants

Navigating Qatar's evolving regulatory landscape presents challenges for new digital banking entrants, particularly smaller fintech firms and international players. The Digital Banks Regulatory Framework mandates stringent requirements, including mandatory Qatar-based headquarters, resident board members, and compliance with anti-money laundering and financial crime prevention standards. These compliance obligations can create barriers to entry, increase operational costs, and extend the timeline for launching digital banking products, potentially limiting the pace of market expansion.

Limited Consumer Trust in Fully Digital Banking Platforms

Despite high digital literacy and widespread technology adoption, a segment of Qatar's population remains cautious about relying entirely on digital-only banking platforms for critical financial transactions. Concerns about the absence of physical branch access, potential system outages, and the perceived risks of fully digital wealth management deter some customers from transitioning away from traditional banking relationships. Building sustained consumer confidence in purely digital banking models requires ongoing education, transparent communication, and consistent service reliability.

Competitive Landscape:

The competitive environment of the digital banking sector in Qatar is marked by the active involvement of both new fintech companies and large established banks going through digital transformation. Well-known financial institutions are introducing cutting-edge digital platforms, open banking APIs, and mobile-first services by utilizing their large client bases, regulatory expertise, and brand trust. As banks make investments in cybersecurity, cloud infrastructure, and AI-driven analytics to set themselves apart from the competition, the market is becoming more competitive. Innovation, quicker product creation, and more service accessibility are all being made possible by strategic alliances between banks and fintech companies. A dynamic and innovative competitive environment is being created by the regulatory environment, which includes the fintech sandbox and digital banking framework, which are enticing both domestic and foreign players to enter the sector.

Qatar Digital Banking Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Services Covered |

|

|

Deployment Types Covered |

On-Premises, Cloud |

|

Technologies Covered |

Internet Banking, Digital Payments, Mobile Banking |

|

Industries Covered |

Media and Entertainment, Manufacturing, Retail, Banking, Healthcare |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Digital Banking Market Report

The Qatar digital banking market size was valued at USD 23,490.06 Million in 2025.

The Qatar digital banking market is expected to grow at a compound annual growth rate of 11.36% from 2026-2034 to reach USD 61,849.30 Million by 2034.

Transactional dominated the market with a share of 64%, driven by the increasing volume of digital fund transfers, mobile-enabled cash management, and automated payment processing services across Qatar's financial landscape.

Key factors driving the Qatar digital banking market include supportive regulatory frameworks, high internet and smartphone penetration, expanding fintech ecosystems, growing consumer demand for digital financial services, and strategic bank-fintech collaborations.

Major challenges include cybersecurity threats and data privacy concerns, regulatory compliance complexities for new entrants, limited consumer trust in fully digital banking platforms, high technology integration costs, and evolving data protection requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)