Qatar E-Mobility Market Size, Share, Trends and Forecast by Product, Voltage, Battery, and Region, 2026-2034

Qatar E-Mobility Market Summary:

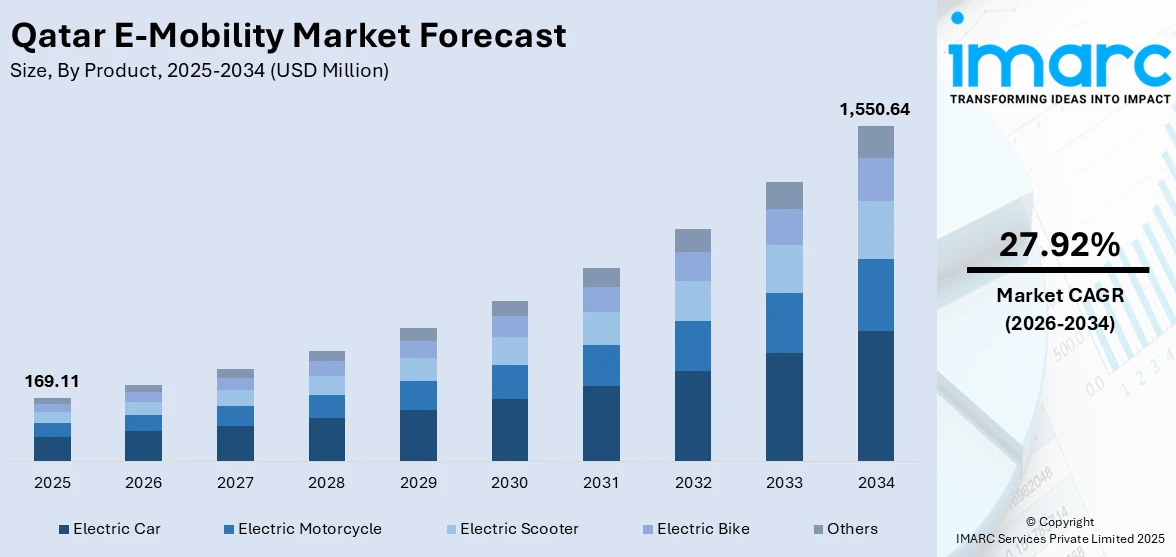

The Qatar e-mobility market size was valued at USD 169.11 Million in 2025 and is projected to reach USD 1,550.64 Million by 2034, growing at a compound annual growth rate of 27.92% from 2026-2034.

The Qatar e-mobility market is experiencing robust momentum as the nation accelerates its transition toward sustainable transportation solutions. Increasing government focus on clean energy, rapid infrastructure development, and growing consumer interest in electric mobility are strengthening adoption across passenger and commercial segments. Strategic investments in charging ecosystems, fleet electrification, and advanced vehicle technologies are reshaping the transportation landscape, positioning Qatar as an emerging regional hub for next-generation electric mobility and Qatar e-mobility market share.

Key Takeaways and Insights:

- By Product: Electric car dominates the market with a share of 46% in 2025, driven by rising consumer preference for zero-emission passenger vehicles, expanding model availability from global automakers, and supportive government policies promoting personal electric vehicle ownership across Qatar.

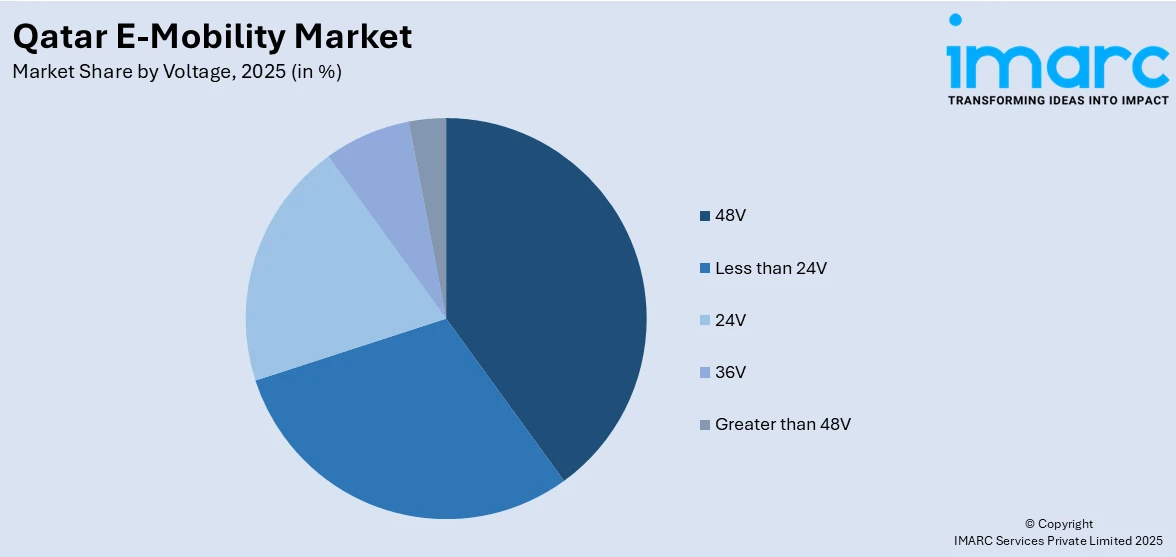

- By Voltage: 48V leads the market with a share of 38% in 2025, owing to its widespread application in electric cars and light electric vehicles that require efficient power delivery, regenerative braking capabilities, and enhanced energy management for urban commuting.

- By Battery: Li-ion exhibits a clear dominance in the market with 71% share in 2025, reflecting strong industry reliance on lithium-ion technology for its superior energy density, longer cycle life, lighter weight, and fast-charging capabilities essential for modern electric mobility.

- By Region: Ad Dawhah represents the largest region with 52% share in 2025, driven by the concentration of commercial activity, high-income demographics, dense charging infrastructure, and the presence of major automotive dealerships in Qatar’s capital city.

- Key Players: Key players in the Qatar e-mobility market are strengthening their presence by expanding electric vehicle portfolios, investing in charging infrastructure, enhancing battery performance technologies, and forming strategic partnerships to accelerate adoption and ensure consistent availability across diverse consumer and commercial segments.

To get more information on this market Request Sample

The Qatar e-mobility market is advancing steadily as government initiatives, industry investments, and evolving consumer preferences converge to support cleaner transportation solutions. A key factor shaping this trajectory is the nation’s comprehensive electric vehicle strategy, which targets electrification of public transport and broader adoption of electric vehicles across private and commercial fleets. Qatar’s commitment to sustainability is further reinforced by its National Vision 2030, which prioritizes environmental stewardship and economic diversification. For instance, according to the Ministry of Transport, approximately 73% of Qatar’s public buses are already electric, representing one of the highest electrification rates for public transit fleets in the Middle East. Expanding charging networks, growing availability of diverse electric vehicle models, and increasing interest from international automakers are creating a more accessible and competitive market landscape. Rising environmental consciousness, coupled with favorable fiscal policies and infrastructure development, is contributing to a more supportive ecosystem for sustainable mobility across Qatar’s urban and suburban corridors.

Qatar E-Mobility Market Trends:

Rapid Expansion of Smart Charging Infrastructure

Qatar is accelerating the deployment of smart electric vehicle charging infrastructure to support growing e-mobility adoption. The national utility Kahramaa, through its Tarsheed conservation program, has been expanding public charging stations across urban and highway corridors. For instance, in March 2025, the Ministry of Communications and Information Technology and Kahramaa launched the second version of the Tarsheed Smart EV Charging Platform, connecting over 135 charging points and recording more than 3,561 active transactions since its December 2023 launch. This digital infrastructure is improving accessibility and reducing range anxiety for electric vehicle users.

Accelerating Public Transport Electrification

Qatar is making significant progress in electrifying its public transportation system, reinforcing the Qatar e-mobility market growth. The country’s state-owned transport operator has been expanding its electric bus fleet in collaboration with global manufacturers. For example, in December 2024, the Minister of Transport laid the foundation stone for a Yutong electric bus assembly plant at Um Al Houl Free Zone, covering 53,000 square meters with an initial production capacity of 300 buses per year. This initiative supports the government’s target of achieving 100% electric public buses by 2030.

Growing Entry of International Electric Vehicle Brands

Qatar’s premium consumer market and favorable policy environment are attracting increasing numbers of international electric vehicle manufacturers. Brands are expanding their presence through dedicated showrooms, service networks, and diverse model offerings tailored to the local market. For instance, in October 2024, GAC AION officially launched its brand in Qatar with the introduction of the AION Y Plus all-electric SUV at its Doha showroom, marking the brand’s first entry into the Qatari market. The expanding model variety is broadening consumer choice and accelerating private electric vehicle adoption.

Market Outlook 2026-2034:

Qatar's e-mobility market is well-placed for continued growth during the forecast period, with a strong policy framework, expanding charging ecosystems, and increasing consumer demand for greener transportation. The Electric Vehicle Strategy 2021 of the government is in line with Qatar National Vision 2030 and has been acting as a strategic direction for fleet electrification and infrastructure development. Accelerated electrification of public transport fleets, building domestic electric vehicle manufacturing capabilities, and strategic placement of high-power charging stations along key urban corridors are expected to contribute toward sustained revenue growth. Declining battery costs, expanding model options from international carmakers, and further supportive fiscal incentives continue to expand market access. Strategic investments by Qatar in renewable energy infrastructure, including large-scale solar power, will underpin the long-term sustainability of its electric mobility ecosystem while further consolidating the country's position as a regional leader in clean transport. The market generated a revenue of USD 169.11 Million in 2025 and is projected to reach a revenue of USD 1,550.64 Million by 2034, growing at a compound annual growth rate of 27.92% from 2026-2034.

Qatar E-Mobility Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Electric Car |

46% |

|

Voltage |

48V |

38% |

|

Battery |

Li-ion |

71% |

|

Region |

Ad Dawhah |

52% |

Product Insights:

- Electric Car

- Electric Motorcycle

- Electric Scooter

- Electric Bike

- Others

Electric car dominates with a market share of 46% of the total Qatar e-mobility market in 2025.

Electric cars represent the largest product category in Qatar's e-mobility landscape, supported by the country's high per capita income and strong consumer preference for premium zero-emission passenger vehicles. The government's commitment to replacing conventional vehicles with electric alternatives under Qatar National Vision 2030 is accelerating adoption across private and fleet segments. Leading international automakers are actively competing in the market with diverse model offerings tailored to local driving conditions and consumer expectations.

The expansion of electric car availability is being supported by government procurement mandates and private sector investments. Regulatory directives requiring public agencies to prioritize electric or hybrid vehicles in their fleet acquisitions are creating guaranteed institutional demand and signaling strong governmental commitment to electrification. This regulatory push, combined with incentives such as import tax benefits and access to expanding charging networks, is strengthening the case for electric car ownership. The compact geographic size of Qatar further reduces range anxiety, making electric cars particularly well-suited for urban commuting and intercity travel within the country.

Voltage Insights:

Access the comprehensive market breakdown Request Sample

- Less than 24V

- 24V

- 36V

- 48V

- Greater than 48V

48V leads with a share of 38% of the total Qatar e-mobility market in 2025.

The 48V segment holds the largest voltage share in Qatar’s e-mobility market, driven by its widespread application across electric cars, mild hybrid systems, and light electric vehicles that require efficient energy management. The 48V architecture supports critical functions including regenerative braking, electric power steering, and advanced driver-assistance systems. Its adoption is increasing as automakers integrate mild-hybrid and full-electric powertrains into vehicles designed for Qatar’s urban commuting environment. According to PwC’s eMobility Outlook 2025 for Qatar, the total cost of ownership for commercial battery electric vehicles is now only 0.8% higher than internal combustion engine vehicles, encouraging broader fleet adoption of 48V and higher-voltage electric platforms.

The preference for 48V systems is further supported by their ability to balance performance requirements with energy efficiency in Qatar’s demanding climate conditions. Manufacturers are increasingly offering vehicles with 48V-based electrical architectures that can manage thermal regulation, cabin cooling, and battery management more effectively in high-temperature environments. The growing deployment of electric scooters, bikes, and light commercial vehicles in urban areas also contributes to the segment’s strength. As Qatar continues to expand its charging infrastructure with both AC and DC fast-charging options, the 48V segment is well-positioned to benefit from improved charging accessibility and expanding consumer demand for versatile electric mobility solutions.

Battery Insights:

- Sealed Lead Acid

- Li-ion

- NiMH

The Li-ion exhibits a clear dominance with a 71% share of the total Qatar e-mobility market in 2025.

Lithium-ion batteries are the predominant energy storage solution in Qatar's e-mobility market, driven by their superior energy density, lightweight construction, longer cycle life, and compatibility with fast-charging systems. The technology underpins the majority of electric cars, buses, and light electric vehicles operating in the country. As global battery production scales and costs decline, lithium-ion solutions are becoming increasingly accessible for Qatar's price-sensitive commercial fleet operators. The Qatar Investment Authority has been strategically investing in the global EV battery supply chain, including backing prominent manufacturers, strengthening Qatar's role in the broader e-mobility ecosystem.

Advancements in lithium-ion battery technology, including improvements in thermal management and energy retention under extreme heat conditions, are particularly relevant for Qatar’s arid climate. Battery manufacturers are developing specialized solutions that maintain performance and safety in high-temperature environments, addressing one of the key consumer concerns in the region. The integration of advanced battery management systems in electric vehicles sold in Qatar ensures optimized charging cycles and extended battery longevity. In March 2025, the country continues to expand its renewable energy capacity through projects such as the 800 MW Al Kharsaah solar power plant, lithium-ion batteries are well-positioned to serve as a critical link between clean energy generation and electric vehicle adoption.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah represents the leading region with a 52% share of the total Qatar e-mobility market in 2025.

Ad Dawhah holds a commanding share in the e-mobility market in Qatar due to its nature as the capital and financial hub of the country. It boasts the maximum footprint of vehicular movement, business activity, and charging infrastructure. It has a high standard demographics profile, coupled with high-end automotive showrooms and being central to all government offices. It also serves as a major center in terms of public transportation electrification since the majority of electric buses and metro operations are located in this vicinity.

The region's dominance is further reinforced by ongoing investments in charging accessibility across key commercial and transportation nodes. In January 2026, Hamad International Airport in Doha partnered with Kahramaa to install public EV charging stations under the Tarsheed sustainability program, expanding charging convenience for residents and visitors alike. The concentration of smart city developments, corporate fleet electrification initiatives, and government-led infrastructure projects continues to position Ad Dawhah as the epicenter of Qatar's e-mobility transition.

Market Dynamics:

Growth Drivers:

Why is the Qatar E-Mobility Market Growing?

Strong Government Policy Framework and National Vision 2030

Qatar's government is playing a central role in driving the e-mobility transition through comprehensive policy support, ambitious electrification targets, and strategic investment in clean transportation infrastructure. The regulatory environment is further strengthened by procurement mandates requiring public agencies to prioritize electric or hybrid vehicles in their fleet acquisitions. Fleet electrification requirements for new vehicle purchases are also encouraging broader private sector participation in the transition toward cleaner mobility. These procurement directives create guaranteed demand and signal strong institutional commitment to electrification. Import tax benefits, preferential registration processes, and access to free public charging further incentivize adoption. The government's proactive coordination between ministries, utilities, and free zone authorities is creating a streamlined ecosystem that supports manufacturers, consumers, and infrastructure providers alike.

Expanding Charging and Renewable Energy Infrastructure

The accelerated development of charging infrastructure and renewable energy generation capacity is easing important hindrances to the adoption of e-mobility in Qatar. Kahramaa, through its National Program for Conservation and Energy Efficiency (Tarsheed), is increasingly deploying more public charging infrastructure in urban clusters and along highways. The Tarsheed Smart EV Charging Platform, designed in partnership with the Ministry of Communications and Information Technology, offers motorists real-time information about charging infrastructure, remote control features, and payment systems. Renewable energy developments are adding to the already-green attributes of the e-mobility system in Qatar. The Al Kharsaah solar power plant is the first large-scale photovoltaic power project in Qatar, contributing a substantial amount of required peak power generation as well as the country’s carbon emission reduction targets. Additional renewable energy generation projects have been commissioned at Ras Laffan and Mesaieed Industrial Cities. QatarEnergy aims to substantially scale its renewable power generation portfolio over the coming decade, ensuring that the growing electricity demand from electric vehicles can be met through clean energy sources, further reducing the overall carbon footprint of the transportation sector.

Increasing Participation of Global Automakers and Domestic Innovation

The entry and expansion of international electric vehicle manufacturers have increased the scope of Qatari consumers to choose from and helped fuel market competition. Famous electric vehicle manufacturers across the world are entering the Qatari market, putting in place dedicated infrastructure such as exclusive showrooms. Qatari market consumers, with the higher GDP per capita, offer great potential for both luxurious and mass-market segment electronic vehicles. So far, Qatari consumers have access to different electronic vehicle models, which cover everything from smaller electronic vehicles to luxurious cars. Moreover, domestic innovation is also on the rise, with Qatar-based startup firms like EcoTranzit unveiling prototypes for its electronic vehicles under the ‘VIM’ brand, which promises to be the first electronic vehicle-specific marque with exclusive intellectual property in Qatar. The firm reportedly claimed to be establishing assembly units and electronic vehicle production lines. Additionally, the collaboration between Mowasalat and Yutong to establish an electric bus assembly plant at Um Al Houl Free Zone further demonstrates Qatar’s commitment to building domestic production capabilities, reducing import dependence, and positioning itself as a regional hub for electric vehicle manufacturing and innovation.

Market Restraints:

What Challenges the Qatar E-Mobility Market is Facing?

High Upfront Vehicle Costs

The purchase price of electric vehicles in Qatar remains significantly higher than comparable internal combustion engine alternatives, creating a substantial barrier to mass-market adoption. While Qatar’s high per capita income supports premium vehicle purchases, the elevated cost of electric vehicles limits penetration among price-sensitive consumer segments and small fleet operators. The absence of substantial direct purchase subsidies or consumer rebates further constrains affordability. Although total cost of ownership over the vehicle’s lifetime can be competitive, many potential buyers are deterred by the higher initial investment, particularly in the absence of accessible financing solutions tailored specifically to electric vehicle acquisition.

Extreme Climate Impact on Battery Performance

Qatar’s harsh summer temperatures, which frequently exceed 45 degrees Celsius, pose significant challenges for electric vehicle battery performance and longevity. Extreme heat accelerates battery degradation, reduces driving range, and increases the energy demand for cabin cooling systems, diminishing overall vehicle efficiency. These climate-related performance concerns contribute to consumer hesitancy and range anxiety, particularly during peak summer months. While manufacturers are developing improved thermal management systems, the additional engineering requirements for heat-resistant battery configurations can increase vehicle costs and limit model availability in the regional market.

Insufficient Charging Coverage in Peripheral Areas

Despite substantial progress in deploying charging infrastructure within Doha and major urban centers, coverage in outlying and peripheral areas of Qatar remains limited. Regions beyond the capital and its immediate suburbs experience lower charging station density, creating accessibility gaps that discourage electric vehicle adoption in these areas. The concentration of charging infrastructure in central locations leaves industrial zones, suburban communities, and intercity corridors underserved. Addressing this uneven distribution requires significant capital investment and coordinated planning between utilities, municipalities, and private operators to ensure comprehensive geographic coverage across the entire country.

Competitive Landscape:

The Qatar e-mobility industry has a highly competitive environment with established international automakers and local new entrants competing to find their footing in the domestic marketplace. The industry is looking to expand their portfolios of EVs and focus on upgrading the overall battery efficiency and developing a strong distribution infrastructure to capitalize on the increasing demand for such products and services by consumers in Qatar. Strategic partnerships are playing a crucial role in molding the competitive environment between government agencies, international companies, and organizations related to infrastructure development and provision of expertise to the market with respect to EVs. The local industry is looking to transition from a traditionally import-driven environment to a highly diversified one with respect to the provision of assembly and manufacturing capabilities to cater to the needs of the EV market.

Qatar E-Mobility Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products Covered |

Electric Car, Electric Motorcycle, Electric Scooter, Electric Bike, Others |

|

Voltages Covered |

Less than 24V, 24V, 36V, 48V, Greater than 48V |

|

Batteries Covered |

Sealed Lead Acid, Li-ion, NiMH |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar E-Mobility Market Report

The Qatar e-mobility market size was valued at USD 169.11 Million in 2025.

The Qatar e-mobility market is expected to grow at a compound annual growth rate of 27.92% from 2026-2034 to reach USD 1,550.64 Million by 2034.

Electric car dominated the market with a share of 46%, driven by rising consumer preference for zero-emission passenger vehicles, expanding model availability from global automakers, and government mandates supporting personal electric vehicle ownership across Qatar.

Key factors driving the Qatar e-mobility market include strong government policy support aligned with National Vision 2030, expanding charging infrastructure through the Tarsheed program, growing participation of international automakers, and increasing consumer environmental awareness.

Major challenges include high upfront vehicle costs, extreme summer temperatures affecting battery performance, insufficient charging coverage in peripheral areas, limited model availability, and consumer concerns about long-term battery replacement costs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)