Qatar Fertilizers Market Size, Share, Trends and Forecast by Product Type, Product, Product Form, Crop Type, and Region, 2026-2034

Qatar Fertilizers Market Summary:

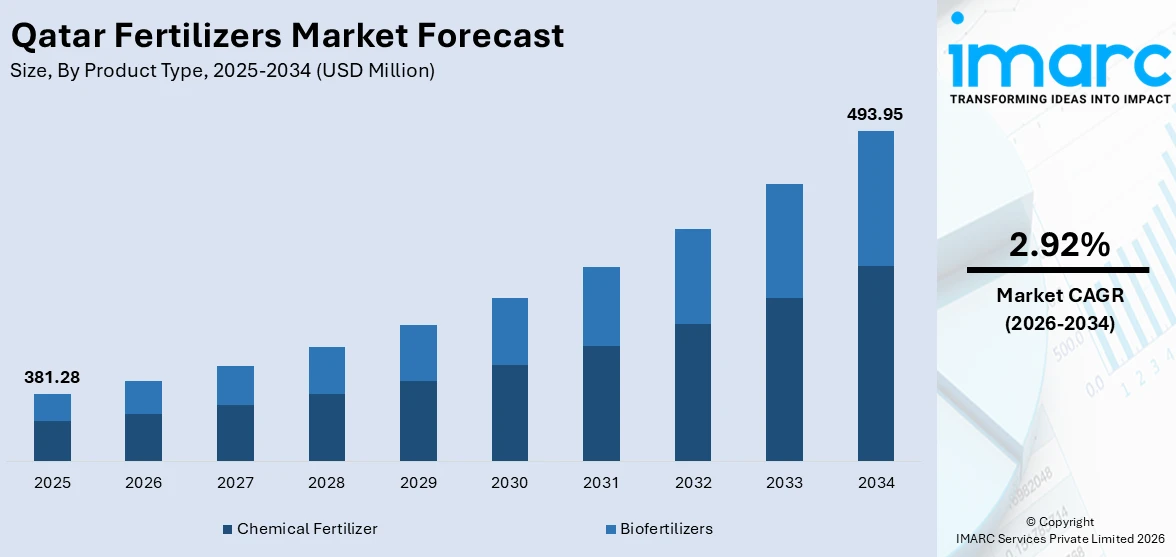

The Qatar fertilizers market size was valued at USD 381.28 Million in 2025 and is projected to reach USD 493.95 Million by 2034, growing at a compound annual growth rate of 2.92% from 2026-2034.

The Qatar fertilizers market is expanding steadily as the government’s food security priorities, agricultural modernization initiatives, and rising domestic crop production drive sustained demand for chemical and biological nutrient solutions. Controlled environment farming expansion, growing adoption of precision agriculture technologies, and investments in sustainable nutrient management are reinforcing the deployment of advanced fertilizer formulations to support crop yield optimization across the Qatar fertilizers market share.

Key Takeaways and Insights:

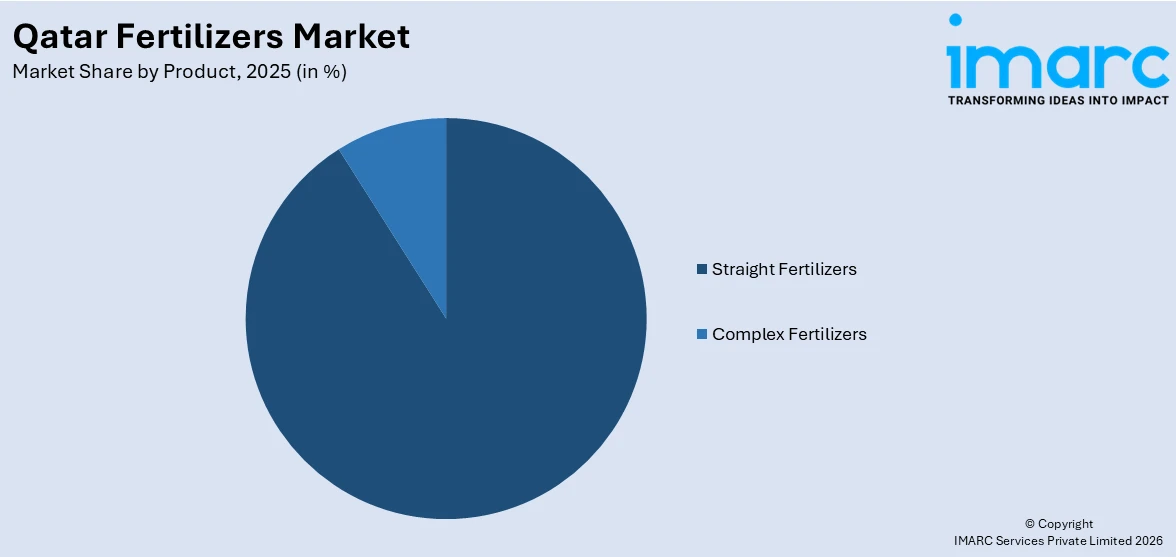

- By Product Type: Chemical fertilizer dominates the market with a share of 91.4% in 2025, owing to the established dependence on synthetic nitrogen, phosphorus, and potassium formulations for crop production.

- By Product: Straight fertilizers lead the market with a share of 63.8% in 2025. This dominance is driven by the widespread application of nitrogenous fertilizers, particularly urea, in grain and cereal cultivation, and the availability of domestically produced nitrogen-based nutrient products.

- By Product Form: Dry represents the largest segment with a market share of 88.6% in 2025, reflecting the practical advantages of granular and prilled fertilizer formulations in terms of storage stability, ease of transport, and compatibility with conventional broadcasting and mechanical application methods.

- By Crop Type: Grains and cereals exhibit a clear dominance in the market with 44.9% share in 2025, driven by Qatar’s strategic emphasis on increasing domestic cereal production capacity and reducing reliance on imported grain supplies as part of national food security objectives.

- By Region: Ad Dawhah comprises the largest region with 39.7% share in 2025, driven by the concentration of agricultural distribution networks, government agricultural support offices, proximity to major import terminals, and the highest population density generating significant food production demand.

- Key Players: The market is led by major integrated producers competing on feedstock access, production efficiency, and export reach. State-linked and private firms vie for global market share, leveraging advantaged natural gas, cost competitiveness, and logistics infrastructure, while rising regional capacity and evolving trade dynamics intensify rivalry.

To get more information on this market Request Sample

The Qatar fertilizers market is strengthening as the country implements its National Food Security Strategy 2030, which encompasses 17 targeted initiatives designed to achieve sustainable food self-sufficiency. Qatar’s agricultural sector has expanded steadily, supported by a rising number of productive farms and stronger domestic supply chains. The country’s arid climate and limited arable land require intensive fertilizer use to optimize yields and maintain soil productivity. Nitrogen based fertilizers, particularly urea, remain central to grain, cereal, and vegetable cultivation. Domestic production capacity, led by established manufacturers, provides a solid supply base largely focused on export markets, while local consumption is gradually increasing alongside agricultural growth. The adoption of controlled environment farming, hydroponics, and smart irrigation systems is also driving demand for specialized, water soluble, and precision applied fertilizer products.

Qatar Fertilizers Market Trends:

Expansion of controlled-environment agriculture

Qatar is increasingly adopting controlled-environment agriculture technologies, including hydroponics, vertical farming, and greenhouse cultivation, to overcome the constraints of its arid desert climate. These advanced farming systems require specialized fertilizer formulations with precise nutrient ratios optimized for soilless growing media. In April 2025, the government launched the National Food Security Strategy 2030, which prioritizes sustainable agricultural technologies and aims to increase local production efficiency by 50%, driving demand for tailored liquid and water-soluble fertilizer products suited to high-technology farming environments.

Growing integration of biofertilizers into agricultural practices

Qatar’s agricultural sector is witnessing increasing adoption of biofertilizers as part of the country’s transition toward sustainable nutrient management. The area dedicated to organic farming doubled in 2024 according to the National Food Security Strategy report, reflecting growing interest in biological soil amendment approaches that reduce dependence on synthetic chemical inputs. Biofertilizer adoption is being supported by government agricultural extension programs that promote microbial inoculants and organic nutrient solutions as complementary tools for improving soil health and crop resilience in arid conditions.

Rising demand for water-soluble and liquid fertilizer formulations

The proliferation of drip irrigation and fertigation systems across Qatar’s farms is creating growing demand for water-soluble and liquid fertilizer products that enable precise nutrient delivery with minimal water consumption. Qatar’s farms increasingly deploy smart irrigation technologies that integrate fertilizer application directly into water distribution systems. With Qatari produce covering approximately 70% of the domestic vegetable market needs in 2024, the continued expansion of irrigated cultivation is accelerating the shift toward liquid formulations that optimize nutrient uptake efficiency in water-scarce environments.

Market Outlook 2026-2034:

The Qatar fertilizers market is positioned for steady growth, underpinned by the government’s strategic commitment to food security, agricultural modernization, and sustainable farming practices. The National Food Security Strategy 2030 is expected to drive increased agricultural activity and consequently expand domestic fertilizer consumption throughout the forecast period. Continued expansion of controlled-environment farming, greenhouse cultivation, and precision agriculture technologies will sustain demand for both chemical and biological fertilizer products. Meanwhile, Qatar’s massive investment in doubling urea production capacity to 12.4 million tons per annum by the end of the decade is expected to reinforce the domestic supply ecosystem and strengthen the country’s position as a global fertilizer production hub, creating positive spillover effects for the local fertilizer distribution and application markets. The market generated a revenue of USD 381.28 Million in 2025 and is projected to reach a revenue of USD 493.95 Million by 2034, growing at a compound annual growth rate of 2.92% from 2026-2034.

Qatar Fertilizers Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Chemical Fertilizer |

91.4% |

|

Product |

Straight Fertilizers |

63.8% |

|

Product Form |

Dry |

88.6% |

|

Crop Type |

Grains and Cereals |

44.9% |

|

Region |

Ad Dawhah |

39.7% |

Product Type Insights:

- Chemical Fertilizer

- Biofertilizers

Chemical fertilizer dominates with a market share of 91.4% of the total Qatar fertilizers market in 2025.

Chemical fertilizers constitute the dominant product type in Qatar’s fertilizer market, driven by the country’s intensive agricultural practices that require high-concentration synthetic nutrient inputs to compensate for poor natural soil fertility in arid desert conditions. Qatar’s agricultural sector relies heavily on nitrogen, phosphorus, and potassium-based chemical formulations to sustain crop production across grains, vegetables, and fodder cultivation. The country’s domestic chemical fertilizer production infrastructure is anchored by the Qatar Fertiliser Company, which operates six world-class plants with a combined annual urea production capacity of 5.6 million metric tons, making it the world’s largest single-site urea exporter with approximately 14% of global supply.

The strategic expansion of Qatar's chemical fertilizer production base provides the market segment which leads the market with increased strength. QatarEnergy will establish a major urea production facility which will double national output capacity in Mesaieed Industrial City. The project will include several ammonia plants which will operate together with new urea production facilities to achieve better operational performance through increased vertical integration. This expansion will elevate Qatar's position in global fertilizer trade while also creating stronger chemical fertilizer supply chains which will endure through time.

Product Insights:

Access the comprehensive market breakdown Request Sample

- Straight Fertilizers

- Nitrogenous Fertilizers

- Urea

- Calcium Ammonium Nitrate

- Ammonium Nitrate

- Ammonium Sulfate

- Anhydrous Ammonia

- Others

- Phosphatic Fertilizers

- Mono-Ammonium Phosphate (MAP)

- Di-Ammonium Phosphate (DAP)

- Single Super Phosphate (SSP)

- Triple Super Phosphate (TSP)

- Others

- Potash Fertilizers

- Muriate of Potash (MoP)

- Sulfate of Potash (SoP)

- Secondary Macronutrient Fertilizers

- Calcium Fertilizers

- Magnesium Fertilizers

- Sulfur Fertilizers

- Micronutrient Fertilizers

- Zinc

- Manganese

- Copper

- Iron

- Boron

- Molybdenum

- Others

- Nitrogenous Fertilizers

- Complex Fertilizers

Straight fertilizers lead with a share of 63.8% of the total Qatar fertilizers market in 2025.

Straight fertilizers represent the largest product segment in Qatar’s fertilizer market, driven predominantly by the widespread use of nitrogenous fertilizers, particularly urea, in domestic crop production. Urea accounts for approximately 60% of global nitrogen fertilizer demand and serves as the primary nutrient input for grain, cereal, and vegetable cultivation in Qatar. The country’s strong domestic production base in straight nitrogen fertilizers, supported by abundant natural gas feedstock for ammonia synthesis, ensures competitive pricing and reliable supply. Straight fertilizer products offer farmers simplified nutrient application with predictable crop response characteristics, making them the preferred choice for conventional agricultural operations.

The continued dominance of straight fertilizers is further supported by Qatar’s strategic investments in expanding urea production capacity. The Qatar Fertiliser Company currently operates the world’s largest single-site urea production facility in Mesaieed Industrial City, with six plants producing a combined annual capacity of 3.8 million metric tons of ammonia and 5.6 million metric tons of urea. This production infrastructure ensures a robust supply base for straight nitrogen fertilizers that serve both export markets and growing domestic agricultural consumption. The availability of domestically manufactured urea at competitive prices reinforces the preference for straight fertilizer products among Qatari farmers.

Product Form Insights:

- Dry

- Liquid

The dry segment exhibits a clear dominance with an 88.6% share of the total Qatar fertilizers market in 2025.

Dry fertilizers dominate Qatar’s fertilizer market, reflecting the practical advantages of granular and prilled formulations for agricultural application in arid desert environments. Dry fertilizer products offer superior storage stability, extended shelf life, and resistance to degradation under extreme heat conditions that characterize Qatar’s climate, where summer temperatures regularly exceed 45 degrees Celsius. The country’s fertilizer distribution infrastructure is primarily designed for handling dry products, with Mesaieed Industrial City serving as one of the largest fertilizer export facilities in the Middle East and North Africa region, equipped with specialized dry bulk storage and handling systems.

The dry fertilizer segment benefits from the predominance of urea in Qatar’s fertilizer production and consumption landscape. Qatar’s urea output, which constitutes the majority of domestic fertilizer production, is manufactured in both prilled and granular forms, with approximately 96% of industrial urea production utilized as a nitrogen-release fertilizer for crop yield enhancement. The established logistics chain for dry fertilizer products, from production facilities to agricultural distribution points, supports efficient supply chain management. Conventional broadcasting and mechanical spreading methods commonly employed on Qatari farms are optimally suited for dry granular fertilizer application, further reinforcing this segment’s market position.

Crop Type Insights:

- Grains and Cereals

- Pulses and Oilseeds

- Fruits and Vegetables

- Flowers and Ornamentals

- Others

Grains and cereals represent the leading segment with a 44.9% share of the total Qatar fertilizers market in 2025.

Grains and cereals represent the largest segment of fertilizer consumption in Qatar, reflecting the country’s focus on strengthening domestic cereal production as part of its broader food security agenda. Although imports continue to meet a significant share of demand, national policy places priority on improving local output through higher productivity and better land utilization. The National Food Security Strategy emphasizes advanced cultivation methods and optimized nutrient management, positioning grain and cereal farming as a key driver of sustained fertilizer demand.

The fertilizer-intensive nature of grain and cereal cultivation in Qatar’s challenging arid environment ensures sustained demand for high-nitrogen chemical fertilizer products. Wheat, barley, and animal fodder crops require significant nitrogenous fertilizer inputs to achieve economically viable yields in Qatar’s desert soils, which are naturally deficient in organic matter and essential macronutrients. Over 950 productive farms are operational nationwide according to the National Food Security Strategy report, with a substantial proportion dedicated to grain and fodder production that supports the country’s livestock population of 1.4 million animals including sheep, goats, camels, and cattle.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah holds the largest share at 39.7% of the total Qatar fertilizers market in 2025.

Ad Dawhah, encompassing Qatar’s capital city Doha and its surrounding metropolitan area, commands the largest regional share in the fertilizers market. The region serves as the primary hub for agricultural input distribution, hosting major import terminals and government agricultural support offices that coordinate fertilizer procurement and allocation. Ad Dawhah’s high population density generates the strongest food production demand, while proximity to Hamad Port facilitates efficient handling of fertilizer imports from Jordan, the Netherlands, and Saudi Arabia.

In addition, the region benefits from well-developed logistics networks, warehousing facilities, and access to financial and regulatory institutions that streamline trade and distribution processes. As such, in September 2025, Bin Yousef Cargo opened a new warehouse at Ras Bufontas Free Zone, enhancing logistics connectivity near Hamad International Airport and Hamad Port. The facility offers streamlined customs, duty exemptions, and cost efficiencies, supporting Qatar’s strategy to strengthen its regional trade hub position. Agricultural suppliers, cooperatives, and retail distributors are concentrated around the metropolitan area, ensuring efficient last-mile delivery to farms across the country. The presence of research institutions and extension services further supports the adoption of modern nutrient management practices, reinforcing Ad Dawhah’s central role in shaping fertilizer demand and market coordination nationwide.

Market Dynamics:

Growth Drivers:

Why is the Qatar Fertilizers Market Growing?

National food security strategy driving agricultural expansion and fertilizer consumption

Qatar’s government is advancing comprehensive food security initiatives that are expanding domestic agricultural output and supporting higher fertilizer demand. The National Food Security Strategy focuses on strengthening local production efficiency, building resilient supply chains, and improving adaptation to climate related challenges. The plan builds on earlier progress that increased cultivated areas and enhanced production capacity nationwide. By prioritizing sustainable farming practices and productivity gains, the strategy is reinforcing long term growth in agricultural inputs, including fertilizers. Qatar has already made substantial progress, with over 950 productive farms operational nationwide and local vegetable production exceeding 26 million kilograms marketed by Mahaseel Company in 2024. The strategy’s emphasis on increasing agricultural land productivity through modern technologies and optimized nutrient management is creating direct incremental demand for fertilizer products across all crop segments.

Massive expansion of domestic fertilizer production infrastructure

Qatar is undertaking unprecedented investments in expanding its fertilizer production capacity, strengthening both the domestic supply ecosystem and the country’s global market position. In September 2024, QatarEnergy announced the construction of a new world-scale urea production complex in Mesaieed Industrial City that will more than double the country’s urea output from approximately 6 million tons per annum to 12.4 million tons per annum by the end of the decade. This mega project involves building three ammonia production lines and four new urea production trains, positioning Qatar as the world’s largest urea producer. Additionally, the Ammonia-7 blue ammonia project, with an investment of approximately QAR 4.4 Billion and a production capacity of 1.2 million tonnes per annum, commenced construction in November 2024 at Mesaieed Industrial City. These capacity expansion initiatives strengthen the broader fertilizer supply chain and create positive spillover effects for domestic market availability.

Adoption of controlled-environment agriculture increasing specialized fertilizer demand

The rapid expansion of controlled-environment agriculture in Qatar, including hydroponics, vertical farming, and greenhouse cultivation, is creating growing demand for specialized fertilizer formulations. Qatar’s challenging climate, characterized by extreme summer temperatures exceeding 45 degrees Celsius and annual rainfall below 80 millimeters, has driven farmers to adopt advanced indoor cultivation systems that require precision nutrient solutions. Qatari produce currently covers the domestic vegetable market needs, with this growth primarily driven by high-technology farming methods that demand tailored water-soluble, liquid, and controlled-release fertilizer products. The government actively supports this agricultural modernization through targeted initiatives, agricultural extension programs, and financial incentives that encourage farmers to adopt smart irrigation and fertigation systems compatible with advanced fertilizer application technologies.

Market Restraints:

What Challenges the Qatar Fertilizers Market is Facing?

Arid climate and limited arable land constraining agricultural expansion

Qatar’s harsh desert climate, characterized by extreme temperatures, chronic water scarcity, and minimal annual rainfall, severely limits the availability of productive arable land for conventional agriculture. The country’s poor natural soil fertility, dominated by sandy and saline substrates with minimal organic matter content, restricts the types of crops that can be cultivated and increases the complexity of fertilizer management. These environmental constraints inherently cap the potential scale of domestic fertilizer consumption growth despite government efforts to expand agricultural production.

Heavy dependence on imported fertilizer products for domestic consumption

Despite being a major fertilizer producer, Qatar’s domestic market remains reliant on imported products to meet the varied nutrient requirements of local agriculture. A significant share of specialty and blended fertilizers is sourced from international suppliers to support different crop types and soil conditions. This reliance exposes the market to potential supply chain disruptions, global price fluctuations, and logistical constraints. Such external dependencies can influence product availability, input costs, and planning certainty for farmers across the country.

Environmental regulations on synthetic fertilizer usage and production

Increasing environmental awareness and regulatory pressures regarding the ecological impact of synthetic chemical fertilizers present growing constraints for the Qatar fertilizers market. Concerns about groundwater contamination from nutrient runoff, soil salinization from excessive chemical input application, and greenhouse gas emissions from nitrogen fertilizer manufacturing are driving stricter environmental compliance requirements. These regulations add operational complexity and costs for fertilizer producers and distributors, potentially constraining consumption growth and accelerating the transition toward more expensive biological alternatives.

Competitive Landscape:

The Qatar fertilizers market features a competitive landscape shaped by a combination of large-scale domestic producers, international chemical companies, and regional agricultural input distributors. Market participants compete through product portfolio diversification, pricing strategies, distribution network expansion, and technical advisory services for farmers. Competition increasingly centers on developing specialized fertilizer formulations tailored to Qatar’s unique agricultural conditions, including heat-resistant formulations, water-soluble products compatible with drip irrigation systems, and slow-release nutrient technologies designed for arid-climate cultivation.

Recent Developments:

- In February 2026, QAFCO partnered with Baker Hughes to implement an AI based operational framework to optimize ammonia production and predictive maintenance. Since 2023, the program raised daily output by 0.8% and saved 566 operating hours, strengthening reliability and supporting expansion toward enterprise-wide optimization.

- In September 2025, Mekdam Holding secured a QAR 203.9 Million contract from Qatar Fertiliser Company to supply Tier 1 manpower for major projects, including carbon capture and the QatarEnergy Urea Project. The five-year agreement strengthens support for national industrial and decarbonization initiatives.

Qatar Fertilizers Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

Chemical Fertilizer, Biofertilizers |

|

Products Covered |

|

|

Product Forms Covered |

Dry, Liquid |

|

Crop Types Covered |

Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, Flowers and Ornamentals, Others |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Fertilizers Market Report

The Qatar fertilizers market size was valued at USD 381.28 Million in 2025.

The Qatar fertilizers market is expected to grow at a compound annual growth rate of 2.92% from 2026-2034 to reach USD 493.95 Million by 2034.

Chemical fertilizer dominated the market with a share of 91.4%, driven by the established dependence on synthetic nitrogen, phosphorus, and potassium formulations for crop production in Qatar’s arid agricultural environment and the country’s strong domestic urea production base.

Key factors driving the Qatar fertilizers market include the National Food Security Strategy 2030, massive domestic urea production expansion, growing adoption of controlled-environment agriculture, and increasing government support for agricultural modernization and self-sufficiency.

Major challenges include arid climate and limited arable land constraining agricultural expansion, heavy dependence on imported fertilizer products for diverse nutrient requirements, environmental regulatory pressures on synthetic fertilizer usage, and water scarcity limiting conventional farming practices.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)