Qatar Fintech Market Size, Share, Trends and Forecast by Deployment Mode, Technology, Application, End User, and Region, 2026-2034

Qatar Fintech Market Overview:

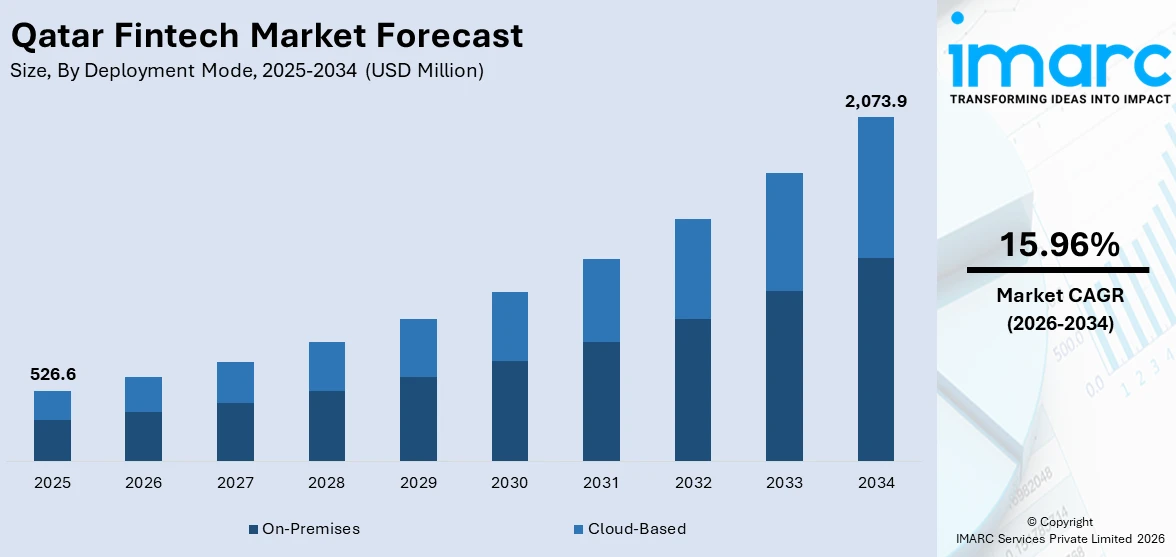

The Qatar fintech market size reached USD 526.6 Million in 2025. The market is projected to reach USD 2,073.9 Million by 2034, exhibiting a growth rate (CAGR) of 15.96% during 2026-2034. The market is progressing rapidly, with firm infrastructure and pervasive digital uptake. The nation is adopting new payment infrastructure, mobile wallets, contactless payments, and blockchain technology, coupled with regulatory changes defining open banking and Islamic fintech frameworks. Public-private efforts such as the Qatar FinTech Hub are fueling startup development, and the central bank is promoting innovation through sandboxes and licensing arrangements. These initiatives are building momentum and increasing Qatar fintech market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 526.6 Million |

| Market Forecast in 2034 | USD 2,073.9 Million |

| Market Growth Rate 2026-2034 | 15.96% |

Qatar Fintech Market Trends:

Surge in Digital Payment Adoption

The adoption of digital payments in Qatar has accelerated sharply, supported by consumer demand for convenience and continued investment in payment infrastructure. In March 2024, Point‑of‑Sale (POS) transaction volumes reached over 32 million, reflecting elevated use of card and mobile payment solutions as customers and merchants shift towards contactless and online options. QR‑code, eWallet, and instant transfer systems are gaining ground, complementing traditional card channels. The Qatar Central Bank’s push to enhance digital payment platforms, including mobile payments, has made it easier for consumers to perform day‑to‑day transactions without reliance on cash. Retailers, transportation services, and small merchants are increasingly installing systems that accept contactless and digital methods, driven both by consumer preferences and regulatory encouragement. These shifts are improving financial inclusion and simplifying commerce, reducing transaction bottlenecks and paving the way for innovations in payments. The momentum in payment platform adoption is central to Qatar fintech market trends, showing how evolving payment habits are reshaping how financial services are used across the country.

To get more information on this market Request Sample

Expansion of Fintech Ecosystem Through SME‑Focused Services

Qatar is expanding its fintech ecosystem with growing attention to serving small and medium‑sized enterprises (SMEs) through specialized financial services and partnerships. Government agencies are partnering with fintech firms to provide tools such as commercial wallets, bulk payment platforms, and streamlined account services designed for business users. These initiatives aim to ease administrative processes, improve cash flow management, and support cross‑border remittances and trade for SME operators. Digital payment infrastructure upgrades and regulatory support are enabling service providers to reach underserved segments, including smaller enterprises that traditionally faced higher barriers. Enhanced digital identity systems, integrated regulatory oversight, and financial incentives are also helping to reduce friction in SME financial operations. Traditional banking channels are being complemented by these fintech‑enabled solutions, which offer more responsive, automated, and accessible financial tools. This trend supports broader inclusivity and efficiency in the financial sector. These developments contribute meaningfully to Qatar fintech market by bolstering supply of SME‑oriented fintech services and reinforcing the market’s capacity to deliver tailored financial solutions.

Regulatory Structures Facilitating Digital Banks

Qatar is building its financial sector with robust regulatory frameworks meant to promote financial innovation and digital banking. The Qatar Central Bank released its Digital Banks Regulatory Framework in December 2024, reaffirming its vision for empowering digital banks that can provide services through online platforms and mobile apps. The framework prioritizes financial inclusion, compelling digital banks to adhere to capital and customer protection requirements while operating with efficacy and security. This policy harmonizes with the Third Financial Sector Strategy and with the national fintech strategy, with regulatory clarity and support for innovation. Digital banks will make it possible for people and businesses to access banking services more conveniently, with lower friction in everyday transactions. These regulations also prompt institutions to develop new products levergaing technology, including real-time payments, digital wallets, and embedded finance. The developing regulatory clarity is facilitating trust in fintech services, both locally and internationally. This enhanced policy landscape is a major factor in Qatar fintech market growth, emphasizing how regulation is facilitating transformation and deepening access to digital financial services.

Qatar Fintech Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on deployment mode, technology, application, and end user.

Deployment Mode Insights:

- On-Premises

- Cloud-Based

The report has provided a detailed breakup and analysis of the market based on the deployment mode. This includes on-premises and cloud-based.

Technology Insights:

- Application Programming Interface

- Artificial Intelligence

- Blockchain

- Robotic Process Automation

- Data Analytics

- Others

The report has provided a detailed breakup and analysis of the market based on the technology. This includes application programming interface, artificial intelligence, blockchain, robotic process automation, data analytics, and others.

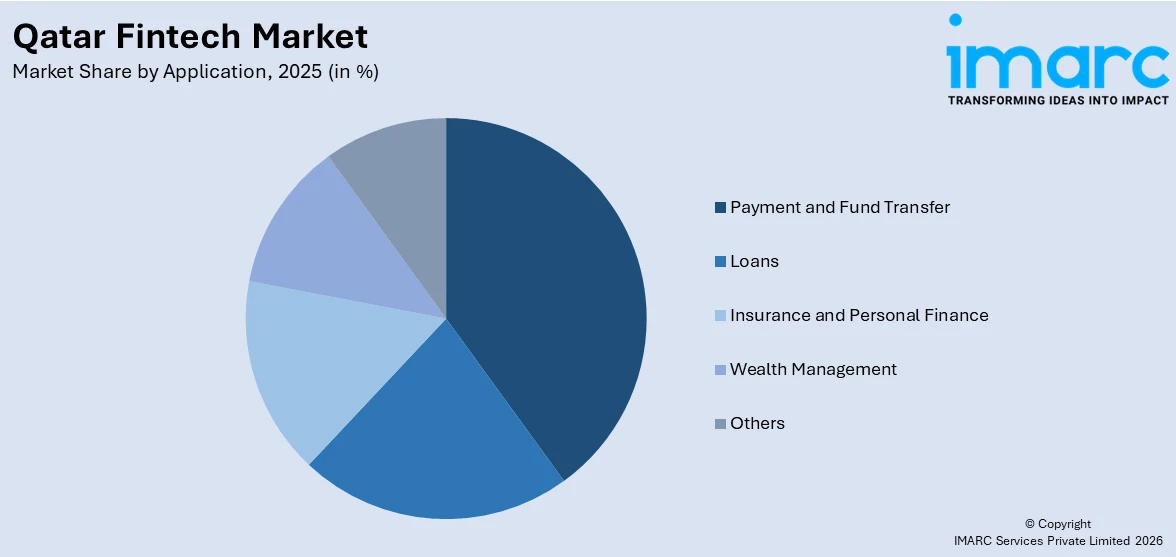

Application Insights:

Access the comprehensive market breakdown Request Sample

- Payment and Fund Transfer

- Loans

- Insurance and Personal Finance

- Wealth Management

- Others

A detailed breakup and analysis of the market based on the application has also been provided in the report. This includes payment and fund transfer, loans, insurance and personal finance, wealth management, and others.

End User Insights:

- Banking

- Insurance

- Securities

- Others

A detailed breakup and analysis of the market based on the end user has also been provided in the report. This includes banking, insurance, securities, and others.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

The report has also provided a comprehensive analysis of all the major regional markets, which include Ad Dawhah, Al Rayyan, Al Wakrah, and others.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Qatar Fintech Market News:

- January 2025: Qatari-based AlRayan Bank recently launched a new mobile banking app, AlRayan Go, built using Backbase. AlRayan Go is Sharia-compliant and features services like access to accounts, transfers, managing cards, paying bills, and top-ups for local telecommunication plan subscriptions. AlRayan Go's purpose is to upgrade digital banking experience with added security and convenience for users. The launch reflects Qatar's move towards modernizing its financial sector as well as enhancing its digital banking.

Qatar Fintech Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Deployment Modes Covered | On-Premises, Cloud-Based |

| Technologies Covered | Application Programming Interface, Artificial Intelligence, Blockchain, Robotic Process Automation, Data Analytics, Others |

| Applications Covered | Payment and Fund Transfer, Loans, Insurance and Personal Finance, Wealth Management, Others |

| End Users Covered | Banking, Insurance, Securities, Others |

| Regions Covered | Ad Dawhah, Al Rayyan, Al Wakrah, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Qatar fintech market performed so far and how will it perform in the coming years?

- What is the breakup of the Qatar fintech market on the basis of deployment mode?

- What is the breakup of the Qatar fintech market on the basis of technology?

- What is the breakup of the Qatar fintech market on the basis of application?

- What is the breakup of the Qatar fintech market on the basis of end user?

- What is the breakup of the Qatar fintech market on the basis of region?

- What are the various stages in the value chain of the Qatar fintech market?

- What are the key driving factors and challenges in the Qatar fintech market?

- What is the structure of the Qatar fintech market and who are the key players?

- What is the degree of competition in the Qatar fintech market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Qatar fintech market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Qatar fintech market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Qatar fintech industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)