Qatar Freight and Logistics Market Size, Share, Trends and Forecast by Logistics Function, End-Use Industry, and Region, 2026-2034

Qatar Freight and Logistics Market Summary:

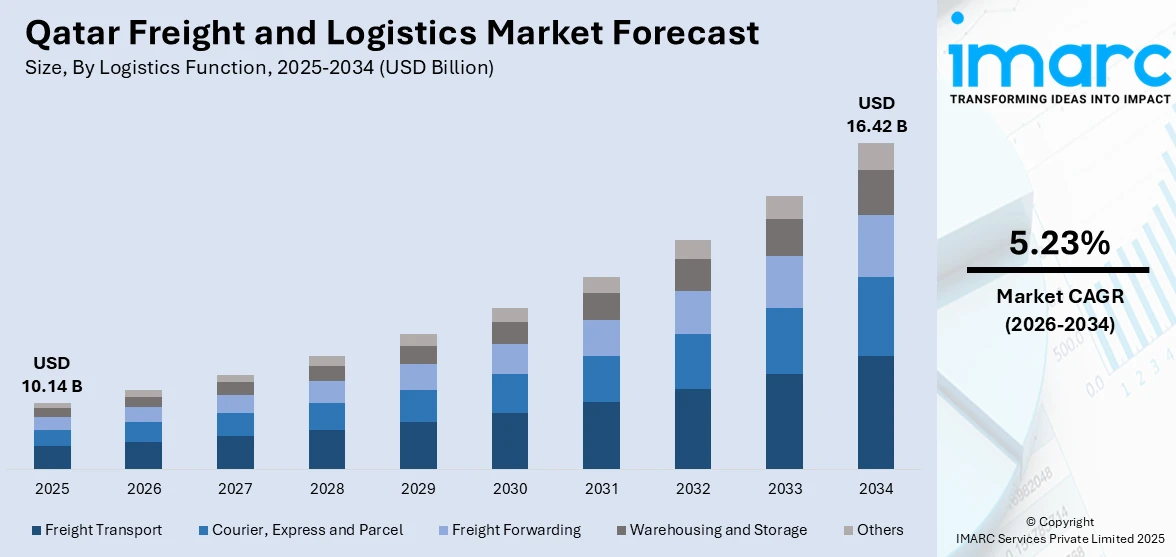

The Qatar freight and logistics market size was valued at USD 10.14 Billion in 2025 and is projected to reach USD 16.42 Billion by 2034, growing at a compound annual growth rate of 5.23% from 2026-2034.

The Qatar freight and logistics market is expanding steadily, driven by the country’s strategic geographic positioning as a trade gateway connecting Asia, Europe, and Africa. Ongoing infrastructure modernization, diversification efforts under the national economic vision, and the growing prominence of maritime and air cargo operations are strengthening logistics capabilities. Rising demand from energy, construction, and retail sectors continues to reinforce Qatar freight and logistics market share.

Key Takeaways and Insights:

- By Logistics Function: Freight transport dominates the market with a share of 38.9% in 2025, driven by the extensive movement of goods through advanced maritime and air cargo infrastructure supporting Qatar’s energy exports and import requirements across multiple trade corridors.

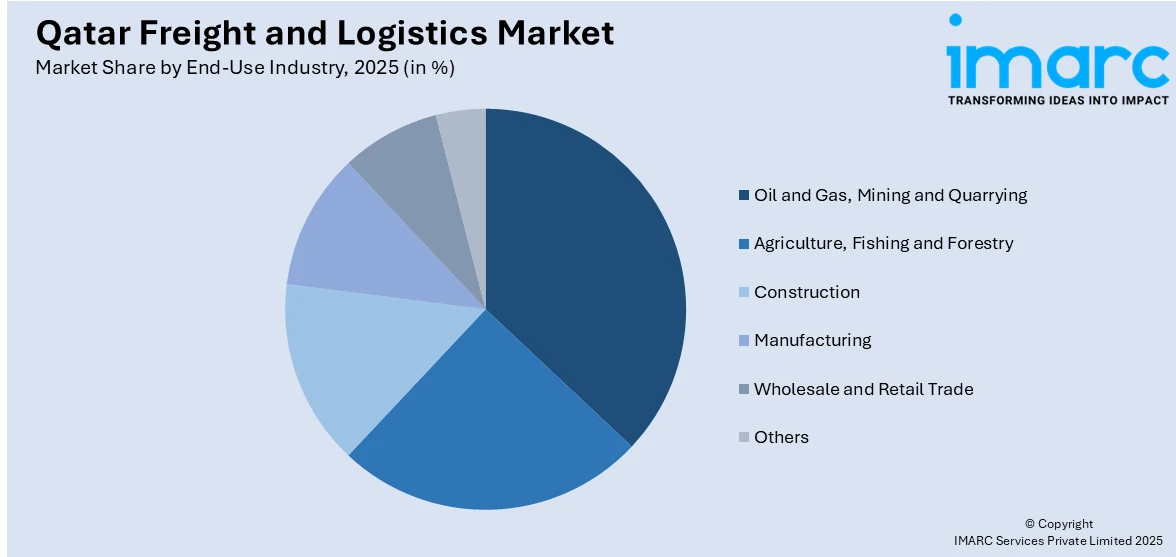

- By End-Use Industry: Oil and gas, mining and quarrying leads the market with a share of 34.2% in 2025, reflecting Qatar’s position as a leading global energy exporter with substantial logistics requirements for liquefied natural gas transportation, offshore supply, and upstream resource distribution.

- By Region: Ad Dawhah represents the largest region with 52.3% share in 2025, underpinned by the concentration of Qatar’s primary port, international airport, free-zone facilities, and the majority of logistics service providers within the capital metropolitan area.

- Key Players: Key players in the Qatar freight and logistics market are strengthening operations by expanding fleet capacities, investing in digital supply chain solutions, broadening warehousing infrastructure, and forging strategic partnerships to enhance service delivery and reinforce their competitive positioning.

To get more information on this market Request Sample

The Qatar freight and logistics market is moving forward as the country is increasing the pace of its infrastructure development initiatives and accelerating the process of economic diversification, moving away from hydrocarbons. The government-driven initiatives for port development, airport development, and road development are helping to build a more robust and optimized supply chain infrastructure. The country’s geographical position gives it direct connectivity to the global trade routes, making it an essential redistribution point for the entire Gulf and Middle East region. The development of free-zone logistics infrastructure, the adoption of digital customs clearance systems, and the increasing presence of global logistics companies are further enhancing the trade facilitation infrastructure of Qatar. At the same time, the growing demand from the construction, manufacturing, wholesale, and retail sectors is keeping the logistics momentum.

Qatar Freight and Logistics Market Trends:

Accelerating Digital Transformation in Customs and Trade Facilitation

Qatar is undergoing a significant shift toward digitalized customs and logistics operations, aiming to streamline trade processes and reduce clearance timelines. Government initiatives focused on integrating electronic single-window platforms with international transport systems are enhancing data exchange, improving transparency, and strengthening operational control across border crossings. The adoption of technologies such as artificial intelligence, Internet of Things, and advanced data analytics in cargo management is enabling real-time tracking and more efficient inventory handling. These efforts are positioning Qatar as a technology-driven trade gateway, supporting faster goods movement and reinforcing Qatar freight and logistics market growth. For instance, in May 2025, the General Authority of Customs announced the successful integration of its Al Nadeeb Customs Clearance System with the International Road Transport Union's (IRU) Digital TIR Carnet Service, enabling instant and secure exchange of data related to international road shipments. These efforts are positioning Qatar as a technology-driven trade gateway, supporting faster goods movement and reinforcing Qatar freight and logistics market growth.

Rising Prominence of Transshipment and Maritime Connectivity

The maritime industry in Qatar is also gaining recognition for its transshipment facilities, with the main port in the country continually developing its worldwide shipping links. Upgraded port facilities, deep draft routes, and sophisticated automated handling systems are making it possible to handle larger ships and increased cargo volumes. The ever-expanding list of direct shipping routes between Qatar and various countries in Asia, Africa, and Europe is further enhancing Qatar’s position as a regional redistribution hub. These developments in the maritime industry are matched by ongoing efforts to develop intermodal links between port operations and inland distribution networks.

Expansion of Free-Zone Logistics Ecosystems

Qatar’s free-zone authorities are actively attracting global logistics operators by offering streamlined customs processes, modern infrastructure, and proximity to key air and sea transport hubs. The development of specialized logistics parks within free zones is creating integrated platforms for warehousing, freight forwarding, and value-added services. International logistics providers are establishing operational bases in these zones to capitalize on Qatar’s connectivity advantages and access to regional markets. This trend is strengthening supply chain resilience and positioning free zones as catalysts for trade growth and logistics innovation in the country. In October 2025, Qatar Free Zones Authority and Qatar Airways signed a collaboration agreement to establish an aviation cluster at Ras Bu Fontas Free Zone, including a Maintenance, Repair and Overhaul facility and a customs-free corridor connecting the free zone to Hamad International Airport and Hamad Port. This trend is strengthening supply chain resilience and positioning free zones as catalysts for trade growth and logistics innovation in the country.

Market Outlook 2026-2034:

The Qatar freight and logistics market is set to grow steadily during the forecast period, driven by ongoing infrastructure development, growing trade, and increasing economic diversification. The development of sea capacity, airport cargo handling capacity, and logistics parks will provide further capacity in the freight market. Qatar’s geographical location at the intersection of Asia, Europe, and Africa will continue to encourage global logistics companies and facilitate transshipment growth. The expansion of Qatar’s energy industry, especially in the production of liquefied natural gas, will continue to fuel demand for specialized freight and sea transport services. Furthermore, the development of the e-commerce industry and changing consumer behavior will accelerate the adoption of last-mile delivery and express logistics solutions, leading to a diversified freight market in Qatar. The market generated a revenue of USD 10.14 Billion in 2025 and is projected to reach a revenue of USD 16.42 Billion by 2034, growing at a compound annual growth rate of 5.23% from 2026-2034.

Qatar Freight and Logistics Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Logistics Function |

Freight Transport |

38.9% |

|

End-Use Industry |

Oil and Gas, Mining and Quarrying |

34.2% |

|

Region |

Ad Dawhah |

52.3% |

Logistics Function Insights:

- Courier, Express and Parcel

- Destination Type

- Domestic

- International

- Destination Type

- Freight Forwarding

- Mode of Transport

- Air

- Sea and Inland Waterways

- Others

- Mode of Transport

- Freight Transport

- Mode of Transport

- Air

- Pipelines

- Rail

- Road

- Sea and Inland Waterways

- Mode of Transport

- Warehousing and Storage

- Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- Temperature Control

- Others

Freight transport dominates with a market share of 38.9% of the total Qatar freight and logistics market in 2025.

Freight transport forms the foundation of Qatar's logistics ecosystem, covering goods movement across road, sea, air, and pipeline networks. The segment's dominance stems from the country's extensive maritime operations and the pivotal role of energy exports in sustaining freight demand. Qatar's deep-water port infrastructure facilitates the handling of high-volume shipments, including containerized cargo, bulk commodities, and specialized energy products. Ongoing investments in port capacity and multimodal connectivity further reinforce freight transport's leading position within the national logistics landscape.

The freight transport segment further benefits from Qatar’s advanced air cargo capabilities, with the country’s primary international airport offering capacity of cargo handling per year. Road freight remains essential for domestic distribution, connecting industrial zones, free-trade areas, and urban consumption centers across the country. The government’s long-term transport planning framework continues to support infrastructure improvements, including road network upgrades and logistics corridor development, that strengthen multimodal freight operations and enhance the efficiency of goods movement across all transport modes within Qatar.

End-Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Agriculture, Fishing and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

Oil and gas, mining and quarrying leads with a share of 34.2% of the total Qatar freight and logistics market in 2025.

The oil and gas, mining and quarrying sector represents the largest end-use category in Qatar’s freight and logistics market, reflecting the country’s status as one of the world’s leading liquefied natural gas producers. The transportation of LNG, condensates, liquefied petroleum gas, and related petrochemical products requires specialized maritime and pipeline logistics infrastructure. Qatar’s state-owned energy entities are executing a major production expansion that aims to increase national LNG output capacity from 77 million metric tons per annum (mtpa) to 142 mtpa by 2030, generating sustained demand for specialized freight services.

Supporting this expansion, Qatar's flagship LNG shipping entity has rapidly scaled its fleet, signing long-term charter agreements for a substantial number of newbuild LNG carriers, including both conventional-size vessels and the largest class of carriers ever constructed. The energy sector's logistics requirements extend beyond maritime transport to include offshore supply services, pipeline operations, and industrial warehousing at dedicated facilities near production hubs. As upstream and midstream activities intensify, the demand for integrated logistics solutions serving the oil and gas value chain is expected to remain a cornerstone of Qatar's overall freight market growth.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah exhibits a clear dominance with a 52.3% share of the total Qatar freight and logistics market in 2025.

Ad Dawhah serves as the commercial and logistical heart of Qatar, hosting the country’s primary trade infrastructure, including the main international airport and the principal seaport that connects to over 100 maritime destinations worldwide through more than 30 direct shipping lines. [RG4] The capital region concentrates the majority of logistics service providers, freight forwarders, and customs brokerage operations, creating a dense ecosystem that facilitates both import and export activities. The presence of free-zone facilities adjacent to key transport hubs enables streamlined goods processing and reduces transit times for international shipments.

The region's logistics infrastructure continues to benefit from ongoing government investments in road connectivity, digital trade facilitation, and urban distribution networks. Leading global logistics providers have established regional facilities at Ras Bufontas Free Zone adjacent to Hamad International Airport, offering integrated warehousing, freight forwarding, and end-to-end supply chain solutions for retail, automotive, and technology industries. Ad Dawhah's concentration of corporate headquarters, retail centers, and industrial zones ensures that it remains the primary demand center for warehousing, last-mile delivery, and express logistics services across the country.

Market Dynamics:

Growth Drivers:

Why is the Qatar Freight and Logistics Market Growing?

Massive Energy Sector Expansion Driving Specialized Freight Demand

Qatar’s ongoing energy sector expansion represents one of the most significant growth catalysts for the freight and logistics market. The country is undertaking a historic multi-phase development program at its principal natural gas field, which is designed to substantially increase production output over the coming years. This expansion necessitates a corresponding scale-up in maritime transport capabilities, offshore supply logistics, and industrial warehousing capacity to support the movement of liquefied natural gas, condensates, and associated petrochemical products to global markets. The sheer magnitude of new production volumes requires dedicated fleet expansion programs, advanced vessel construction, and the development of enhanced loading and discharge terminal capacities. The energy expansion is also generating substantial secondary logistics demand through the procurement and transportation of construction materials, specialized heavy equipment, and industrial components required for building new liquefaction trains and supporting infrastructure. Dedicated shipping programs are being developed to ensure uninterrupted transportation of expanded production volumes, while ancillary logistics services, including bunker supply, vessel agency, and port handling, are scaling accordingly. The cumulative effect of these energy-driven logistics requirements is creating a sustained long-term demand foundation that reinforces freight market expansion across multiple transport modes and encourages new market entrants to develop specialized capabilities aligned with energy sector needs.

Strategic Infrastructure Investments Enhancing Logistics Capabilities

Qatar’s government continues to channel substantial resources into developing world-class transport and logistics infrastructure as part of its long-term national economic vision. Major road construction programs, port expansion initiatives, and airport capacity upgrades are collectively enhancing the country’s ability to handle growing freight volumes with greater efficiency. These investments are creating modern, high-capacity logistics corridors that connect production zones, free-trade areas, and distribution centers to global trade routes. The government’s focus on building intermodal transport networks ensures seamless connectivity between maritime, air, and land-based freight channels. The development of advanced customs clearance systems, integrated electronic trade platforms, and smart logistics technologies is further reducing processing times and lowering transaction costs for businesses operating within Qatar. The establishment and expansion of free zones with dedicated logistics infrastructure are attracting international operators, strengthening the competitive positioning of Qatar as a regional trade facilitation hub. Ongoing improvements in multimodal connectivity, linking maritime, air, and road transport networks, are enabling more seamless cargo movement and supporting the diversification of logistics services beyond traditional freight handling into value-added activities such as cold chain management, inventory optimization, and e-commerce fulfillment operations across the country.

Growing Trade Volumes and Economic Diversification Broadening Logistics Demand

Qatar’s commitment to economic diversification is generating new and expanding sources of freight and logistics demand beyond the traditional hydrocarbon sector. Growth in construction, manufacturing, wholesale and retail trade, and food import activities is driving increased requirements for warehousing, distribution, and express delivery services. The country’s high import dependency, particularly for consumer goods, food products, and industrial materials, sustains robust inbound freight volumes that support logistics market expansion. Government initiatives aimed at promoting local manufacturing and value-added industries are further creating new logistics service requirements across the supply chain. The emergence of e-commerce as a significant retail channel is creating additional demand for last-mile delivery, parcel handling, and fulfillment logistics. Rising consumer expectations for faster and more reliable delivery services are prompting logistics providers to invest in technology-enabled distribution capabilities and urban delivery networks. Furthermore, Qatar’s increasing integration into global supply chains through bilateral trade agreements, expanded shipping connectivity, and enhanced free-zone offerings is broadening the scope of logistics activities. The growing tourism and hospitality sectors also contribute to rising demand for specialized cold chain logistics and food service distribution. These diversification-driven trends are supporting more balanced and sustainable growth across all segments of the freight and logistics market.

Market Restraints:

What Challenges the Qatar Freight and Logistics Market is Facing?

Heavy Dependence on Hydrocarbon Sector for Logistics Demand

A significant portion of Qatar’s freight and logistics activity remains closely tied to the oil and gas sector, making the market vulnerable to fluctuations in global energy prices and production cycles. Any sustained downturn in hydrocarbon revenues or delays in energy expansion projects could reduce logistics volumes and investment flows. While economic diversification efforts are underway, the transition to a more balanced demand structure requires continued policy support and sustained growth in non-energy sectors to reduce concentration risk.

Limited Domestic Workforce and Rising Operational Costs

Qatar’s logistics sector faces challenges related to a limited domestic labor pool, necessitating significant reliance on expatriate workers for operational, technical, and managerial roles. Evolving immigration regulations, rising wage expectations, and increased compliance requirements contribute to higher operational costs for logistics service providers. Additionally, fuel subsidy reforms and changing regulatory frameworks for commercial transport are adding cost pressures that can affect pricing competitiveness and profitability, particularly for smaller and mid-sized logistics operators attempting to maintain service quality.

Intensifying Competition from Regional Logistics Hubs

Qatar is increasingly being subjected to competitive pressures from other logistics hubs in the region, which are investing heavily in port development, free zones, and trade facilitation capabilities. These competing logistics hubs have extensive warehousing capacity, well-developed shipping networks, and attractive incentive packages to lure global logistics companies and cargo to their locations. This scenario forces Qatar to make continuous investments in service differentiation, efficiency, and technology to sustain and enhance its position as a preferred logistics location within the Middle Eastern trade route.

Competitive Landscape:

The Qatar freight and logistics market has a moderately consolidated competitive environment, with a mix of domestic and global logistics companies competing for market share. The competitive environment is fueled by infrastructure ownership, capacity, service offerings, and the capability to provide end-to-end supply chain solutions. The major players in the market are using their large warehousing capacity, sea freight capabilities, and partnerships to cater to major industries such as energy, construction, and retail. The market is experiencing an increasing focus on digitalization, with players investing in automated warehouses, real-time tracking of cargo, and data analytics to enhance efficiency. Sustainability initiatives, such as the use of cleaner transport technologies and environmental certifications, are becoming a differentiator in the market. The presence of global logistics companies in Qatar’s free zones is increasing competition and enhancing service quality in the market.

Recent Developments:

- In September 2025, FedEx Logistics, in partnership with Qatar Free Zones Authority, officially opened a new regional logistics facility at Ras Bufontas Free Zone. The 1,249 square meter facility offers integrated warehousing, storage, and freight forwarding capabilities, serving as a key gateway for goods movement between Asia, Europe, and North America through the FedEx global network.

- In July 2025, Qatar Navigation (Milaha) signed a five-year agreement with Qatar Airways Group to deliver comprehensive warehousing and logistics services. Under the agreement, Milaha will provide end-to-end supply chain solutions, including warehousing, inventory management, and distribution support, powered by advanced logistics technologies and real-time visibility tools.

Qatar Freight and Logistics Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Logistics Functions Covered |

|

|

End-Use Industries Covered |

Agriculture, Fishing and Forestry; Construction; Manufacturing; Oil and Gas, Mining and Quarrying; Wholesale and Retail Trade; Others |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Freight and Logistics Market Report

The Qatar freight and logistics market size was valued at USD 10.14 Billion in 2025.

The Qatar freight and logistics market is expected to grow at a compound annual growth rate of 5.23% from 2026-2034 to reach USD 16.42 Billion by 2034.

Freight transport dominated the market with a share of 38.9%, driven by extensive maritime cargo operations, energy export logistics, and multimodal transport capabilities connecting Qatar to global trade corridors.

Key factors driving the Qatar freight and logistics market include massive energy sector expansion programs, strategic infrastructure investments, growing trade volumes, economic diversification efforts, and the development of advanced digital customs and logistics platforms.

Major challenges include heavy dependence on the hydrocarbon sector for logistics demand, limited domestic workforce availability, rising operational costs, intensifying competition from regional logistics hubs, and the need for sustained non-energy sector growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)