Qatar Hydropower Market Size, Share, Trends and Forecast by Size, Application, and Region, 2026-2034

Qatar Hydropower Market Summary:

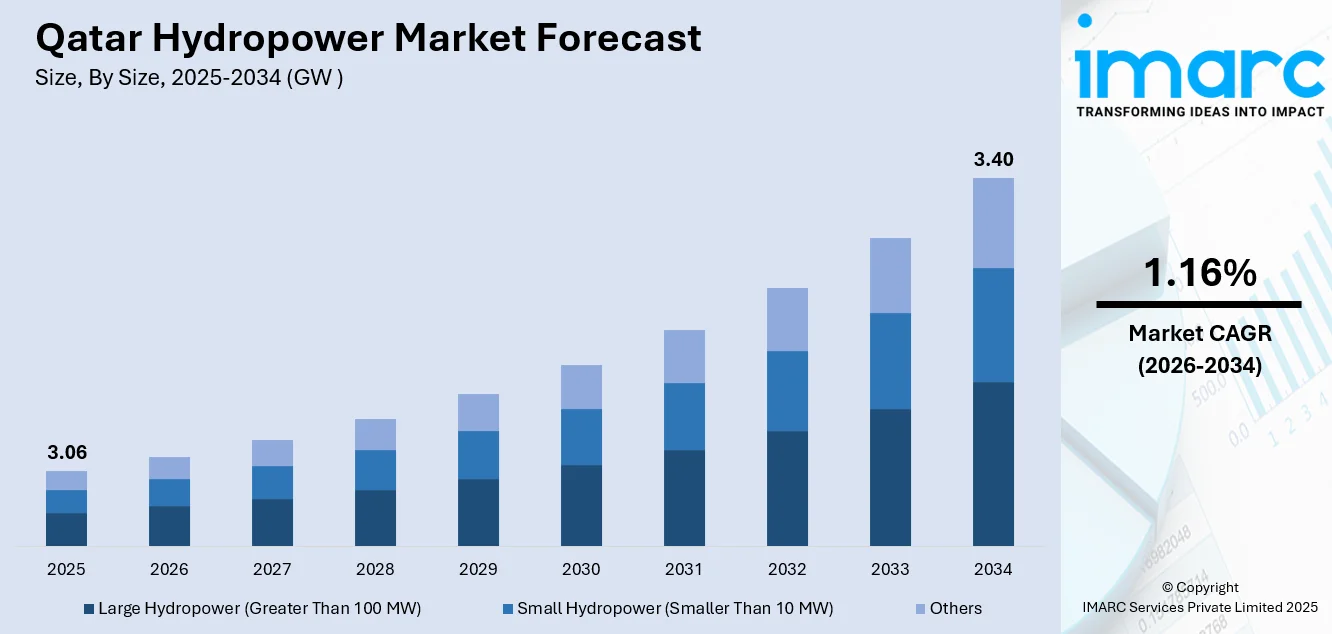

The Qatar hydropower market size reached 3.06 GW in 2025 and is projected to reach 3.40 GW by 2034, growing at a compound annual growth rate of 1.16% from 2026-2034.

Qatar is advancing innovative hydropower solutions to address geographic and water limitations within its arid environment, integrating micro-hydropower systems with water recycling infrastructure and desalination facilities. The market benefits from strategic government initiatives under the Qatar National Vision 2030 and the Qatar National Renewable Energy Strategy, which emphasize sustainable energy diversification and carbon reduction objectives. These developments complement the nation's broader renewable energy portfolio, supporting long-term energy security while enhancing the Qatar hydropower market share.

Key Takeaways and Insights:

- By Size: Large hydropower (greater than 100 MW) dominates the market with a share of 52% in 2025, driven by the concentration of utility-scale installations supporting industrial facilities and water desalination complexes in Qatar's primary energy hubs, enabling efficient baseload power generation for high-demand operations.

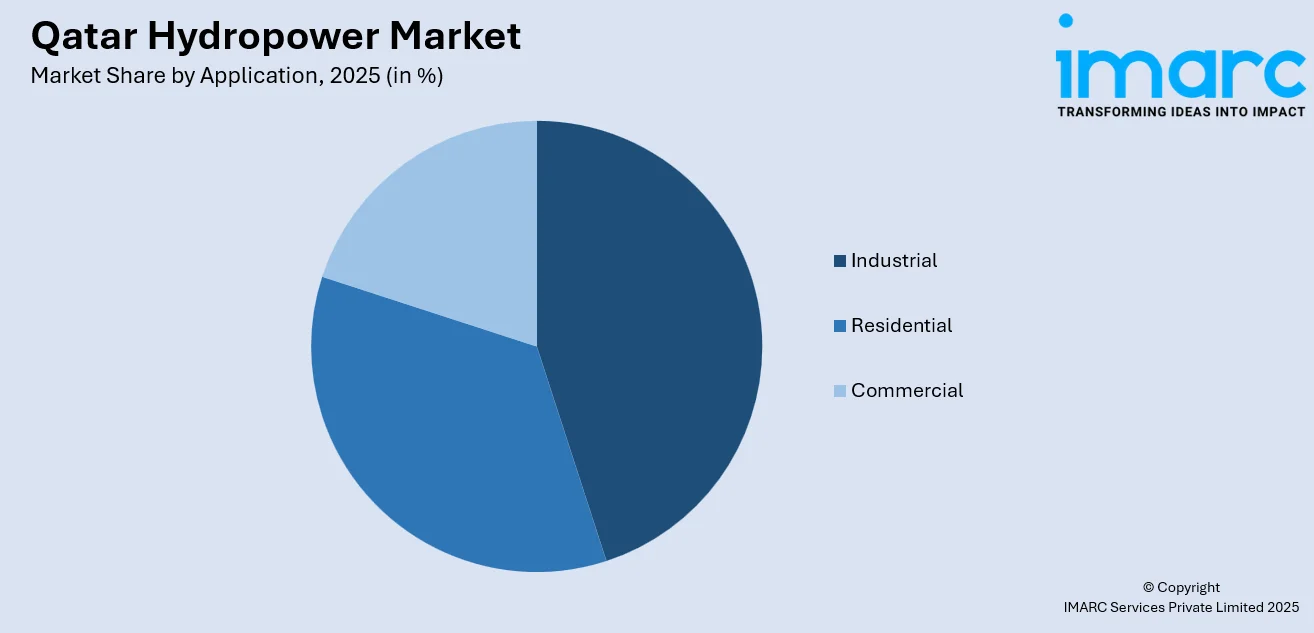

- By Application: Industrial leads the market with a share of 45% in 2025, owing to the significant energy requirements of Qatar's manufacturing, petrochemical processing, and water desalination operations concentrated in key industrial zones across Ras Laffan and Mesaieed.

- By Region: Ad Dawhah represents the largest segment with a market share of 40% in 2025, reflecting the capital region's role as the primary hub for electricity and water infrastructure, housing major desalination facilities and grid interconnection points serving the metropolitan population.

- Key Players: The Qatar hydropower market is characterized by a highly consolidated structure, with strong institutional involvement and collaborative approaches to infrastructure development. Centralized planning and public–private partnerships play a key role in advancing renewable capacity, supported by long-term energy strategies and coordinated investment frameworks.

To get more information on this market Request Sample

The Qatar hydropower market is experiencing strategic development driven by the nation's commitment to energy diversification and sustainable resource management. Despite geographic constraints inherent to arid environments, Qatar is pioneering innovative approaches to harness hydropower potential through integration with existing water infrastructure. The market is characterized by growing investments in micro-hydropower technologies and energy recovery systems within desalination facilities. For instance, in May 2025, KAHRAMAA contracted 3.1 billion Qatari riyals for power infrastructure expansion, including seven high-voltage substations and 212 kilometers of transmission lines, demonstrating the government's commitment to modernizing energy infrastructure. These investments align with Qatar's broader sustainability objectives, supporting the transition toward a diversified energy portfolio while maintaining a reliable power supply for industrial and residential consumers across the nation.

Qatar Hydropower Market Trends:

Emergence of Micro-Hydropower Technologies

Micro-hydropower technology development represents a significant trend driving the Qatar hydropower market as the country incorporates renewable energy solutions adapted to its desert environment. These technologies enable effective power generation from controlled watercourses and water recycling systems, maximizing resource efficiency within limited freshwater supplies. The Qatar Environment and Energy Research Institute (QEERI), under Qatar Foundation, conducts cutting-edge research to improve energy generation efficiency and develop sustainable solutions for water applications. Higher turbine efficiency and smart grid compatibility provide robust performance across diverse applications, aligning with national sustainability targets.

Hydropower Integration with Desalination Infrastructure

A leading development driving Qatar hydropower market growth involves integrating hydropower systems with desalination processes to generate power while addressing critical water supply demands. This integrated design utilizes energy potential within water flows at desalination facilities to produce renewable power, achieving maximum resource efficiency. Qatar's desalinated potable water capacity reached approximately 538 million gallons per day in 2024 following the Umm Al Houl expansion, with capacity expected to climb to 648 million gallons once the new Ras Abu Fontas plant becomes operational in 2028. Technological advancements in turbine systems and computerized controls further enhance production efficiency and operational stability.

Policy Support and Strategic Renewable Diversification

Strong policy programs and strategic development initiatives are at the forefront of Qatar's hydropower market advancement, with government-sponsored programs supporting the utilization of innovative hydropower solutions alongside other renewable resources. The Qatar National Renewable Energy Strategy (QNRES), launched by KAHRAMAA, establishes frameworks for renewable energy integration targeting increased renewable contribution to the national energy mix. Policy incentives, research grants, and pilot implementations facilitate the adaptation of hydropower technologies to Qatar's specific geographic and climatic conditions. For instance, in November 2024, KAHRAMAA's Tarsheed program achieved financial savings of approximately 840 million QAR while reducing carbon emissions by 1.2 million tons, demonstrating effective conservation initiatives.

Market Outlook 2026-2034:

The Qatar hydropower market outlook remains positive as strategic investments in water-energy infrastructure continue accelerating through the forecast period. Government commitment to Qatar National Vision 2030 and the Third National Development Strategy 2024-2030 ensures a sustained focus on sustainable energy solutions. Qatar's electricity demand is projected to increase by 58% by 2040 compared to 2021, intensifying efforts to diversify generation sources and enhance grid stability through innovative hydropower applications. The market size was estimated at 3.06 GW in 2025 and is expected to reach 3.40 GW by 2034, reflecting compound annual growth rate of 1.16% over the forecast period 2026-2034.

Qatar Hydropower Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Size | Large Hydropower Greater Than 100 MW) | 52% |

| Application | Industrial | 45% |

| Region | Ad Dawhah | 40% |

Size Insights:

- Large Hydropower (Greater Than 100 MW)

- Small Hydropower (Smaller Than 10 MW)

- Others

Large hydropower (greater than 100 MW) dominates with a market share of 52% of the total Qatar hydropower market in 2025.

Large hydropower installations maintain market dominance through their capacity to deliver substantial baseload power, supporting Qatar's energy-intensive industrial operations and water desalination infrastructure. These utility-scale systems offer economies of scale in power generation, providing reliable energy output essential for maintaining grid stability across the national electricity network. The segment benefits from concentrated deployment in major industrial zones where high electricity demand justifies significant capital investments in generation infrastructure.

Integration with Qatar's extensive water infrastructure creates synergies enabling large hydropower systems to capture energy from controlled water flows within desalination facilities and distribution networks. Strategic government investments in modernizing energy infrastructure support continued deployment of utility-scale installations, with KAHRAMAA leading initiatives to enhance generation capacity while advancing sustainability objectives aligned with Qatar National Vision 2030.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Industrial

- Residential

- Commercial

Industrial leads with a share of 45% of the total Qatar hydropower market in 2025.

The industrial application segment commands market leadership driven by Qatar's substantial manufacturing, petrochemical processing, and water desalination requirements concentrated in key industrial zones. Ras Laffan Industrial City and Mesaieed Industrial City serve as primary hubs housing major energy production and desalination facilities requiring consistent, reliable power supply. Industrial operations benefit from hydropower's capacity for baseload generation, ensuring uninterrupted energy availability essential for continuous manufacturing processes and critical infrastructure operations.

Growing industrialization under Qatar's economic diversification initiatives drives expanding energy demand from manufacturing and processing operations. The segment continues benefiting from strategic infrastructure investments, including the November 2024 consortium agreement for the Facility E Independent Water and Power Project, a $3.7 billion initiative that will produce 2,400 MW of electricity and 110 million gallons of desalinated water daily, representing a huge share of Qatar's total electricity output upon completion in 2029.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah exhibits clear dominance with a 40% share of the total Qatar hydropower market in 2025.

Ad Dawhah (Doha) maintains regional market leadership as Qatar's capital and primary economic center, housing the nation's largest concentration of population, commercial establishments, and critical infrastructure. The metropolitan region serves as the hub for electricity distribution and water supply networks, with KAHRAMAA's National Control Center managing all network demand and data acquisition from generation facilities. The region's dominant position reflects its role as the administrative and commercial heart of Qatar, with electricity consumption patterns driven by substantial residential, commercial, and institutional demand.

Strategic infrastructure investments continue strengthening Ad Dawhah's position, with major facilities including the Ras Abu Fontas power and water complex located approximately 25 kilometers south of the capital. The water distribution network expanded from 900 kilometers in 2015 to approximately 7,900 kilometers by mid-2025, with plans to reach 8,200 kilometers by 2028, demonstrating the region's central role in Qatar's energy and water infrastructure development.

Market Dynamics:

Growth Drivers:

Why is the Qatar Hydropower Market Growing?

Government Initiatives and Policy Support for Renewable Energy

Strong government support for renewable energy under national development strategies is providing significant momentum for hydropower market growth in Qatar. Comprehensive frameworks guide the integration of renewable energy, creating a conducive environment for adopting innovative hydropower solutions tailored to local conditions. Policy incentives, regulatory measures, and strategic investment programs encourage research, development, and deployment of sustainable energy technologies. This commitment is reinforced through funding for implementation and collaboration with research institutions, highlighting the government’s focus on advancing clean energy infrastructure and promoting long-term sustainability across the country’s power sector.

Integration with Water Desalination Infrastructure

Qatar’s substantial investment in water desalination infrastructure presents key opportunities for integrating hydropower, allowing energy recovery within water treatment and distribution systems. Expanding desalination capacity and modernizing facilities create potential for coupling hydropower solutions with existing operations, enhancing energy efficiency and supporting sustainable water and electricity management across the country. Major facilities, including Umm Al Houl, producing over 600,000 cubic meters of water daily alongside electricity generation, exemplify integrated approaches optimizing energy use. Such integrated systems not only improve operational efficiency but also demonstrate Qatar’s commitment to innovative, sustainable solutions that balance energy production with critical water resource management.

Rising Electricity Demand and Infrastructure Modernization

Escalating electricity demand driven by population growth, urbanization, and industrial expansion necessitates diversified generation sources, including hydropower applications. Qatar's electricity consumption increased at an average rate of 6.5% annually since 2020, reaching 56 TWh in 2024, primarily due to rising air conditioning loads and water desalination industry growth. Rising electricity demand in Qatar is driving the need for expanded generation capacity and modernized infrastructure. Ongoing grid enhancement initiatives, including the development of new substations and extensive transmission networks, are strengthening the power system and enabling the integration of diverse energy sources, including potential hydropower solutions, to ensure a reliable and resilient electricity supply across the country.

Market Restraints:

What Challenges is the Qatar Hydropower Market Facing?

Limited Natural Water Resources and Hyper-Arid Climate

Qatar's classification as a hyper-arid environment with extremely limited freshwater resources presents fundamental constraints for conventional hydropower development. Average rainfall of approximately 50-80 millimeters annually and the absence of permanent river bodies restrict opportunities for traditional large-scale hydropower installations requiring consistent natural water flows. These geographic limitations necessitate innovative approaches focused on micro-hydropower and energy recovery systems rather than conventional dam-based generation.

High Infrastructure Investment Requirements

The development of specialized hydropower infrastructure and adjustments to the peculiarities of Qatar create market constraints and demand substantial capital investments. The implementation of hydropower systems in any water infrastructure requires a considerable amount of engineering skills and bespoke implementation, making them more expensive than traditional systems to install. The development process can take time, and the intricate technical specifications can restrict it to well-financed organizations that can handle massive infrastructure developments.

Competition from Alternative Renewable Energy Sources

Solar energy is dominant in the Qatari renewable energy arena, and this makes it difficult to expand the hydropower market. Large-scale solar projects are economically good and thus attract a lot of investment and attention due to the availability of solar resources. Its increased focus on solar generation is also increasing its contribution to the renewable power generation mix of the country, thereby reducing the number of resources and focus on the development of hydropower and other renewable alternative solutions.

Competitive Landscape:

The Qatar hydropower market is highly consolidated, with collaboration between domestic institutions and international partners driving infrastructure development. The market is centrally coordinated, with a single authority overseeing transmission, distribution, and integrated electricity and water networks. Competition focuses on technological proficiency, project execution capabilities, and financial strength to undertake large-scale, capital-intensive infrastructure projects. Significant entry barriers exist due to stringent regulatory requirements, high investment costs, and the specialized engineering needed to implement hydropower solutions in arid and resource-constrained environments. Strategic partnerships and expertise are critical for market participation and successful project delivery.

Recent Developments:

- August 2025: A significant agreement was finalized in Dushanbe between the Ministry of Finance of Tajikistan and the Qatar Development Fund. Under the deal, Qatar will extend a concessional loan of $50 million to support the construction of the Rogun Hydropower Plant, Tajikistan’s largest energy initiative, often regarded as the cornerstone of the nation’s long-term energy strategy.

Qatar Hydropower Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | GW |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sizes Covered | Large Hydropower (Greater Than 100 MW), Small Hydropower (Smaller Than 10 MW), Others |

| Applications Covered | Industrial, Residential, Commercial |

| Regions Covered | Ad Dawhah, Al Rayyan, Al Wakrah, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Hydropower Market Report

The Qatar hydropower market size reached 3.06 GW in 2025.

The Qatar hydropower market is expected to grow at a compound annual growth rate of 1.16% from 2026-2034 to reach 3.40 GW by 2034.

Large hydropower (greater than 100 MW) dominated the market with a 52% share in 2025, driven by utility-scale installations supporting industrial facilities and water desalination infrastructure in Qatar's primary energy hubs.

Key factors driving the Qatar hydropower market include government initiatives under Qatar National Vision 2030 and QNRES, integration opportunities with extensive water desalination infrastructure, and rising electricity demand requiring diversified generation sources.

Major challenges include limited natural water resources in Qatar's hyper-arid environment, high infrastructure investment requirements for specialized installations, and competition from solar energy which benefits from abundant solar resources exceeding 2,000 kWh per square meter annually.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)