Qatar Industrial Gases Market Size, Share, Trends and Forecast by Type, Application, Supply Mode, and Region, 2026-2034

Qatar Industrial Gases Market Summary:

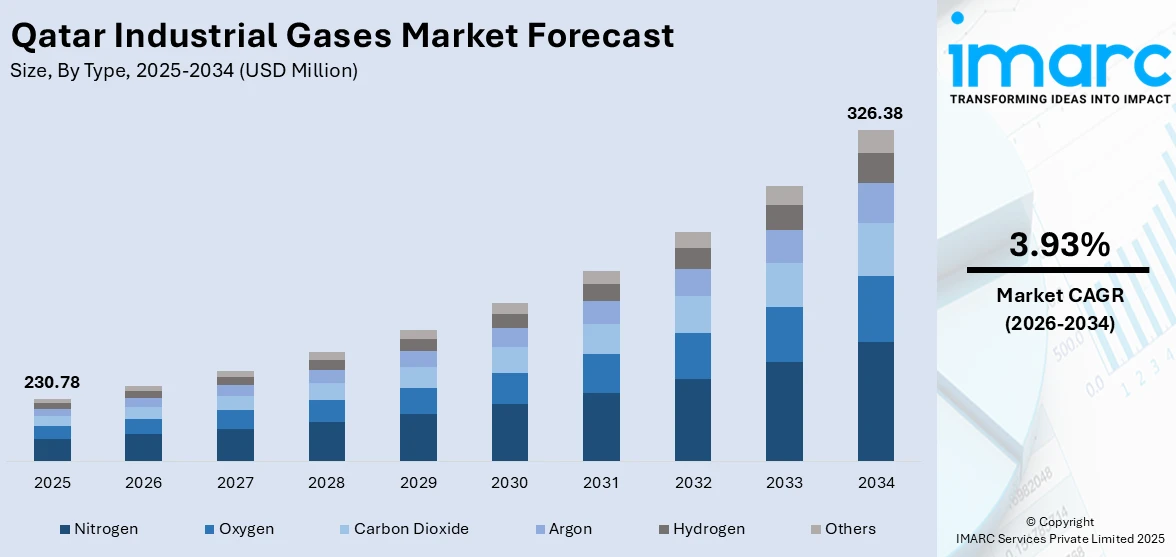

The Qatar industrial gases market size was valued at USD 230.78 Million in 2025 and is projected to reach USD 326.38 Million by 2034, growing at a compound annual growth rate of 3.93% from 2026-2034.

The market is fueled by the fast-paced industrialization process, the development of energy infrastructure, and the nation’s strategic emphasis on economic diversification based on its National Vision 2030 initiative. The increasing demand from the oil and gas, manufacturing, healthcare, and chemical industries remains a major driver for the consumption of the major industrial gases. Moreover, the development of massive infrastructure projects and the expansion of downstream petrochemical operations are also driving the Qatar industrial gases market share.

Key Takeaways and Insights:

-

By Type: Nitrogen dominates the market with a share of 36.7% in 2025, driven by its extensive use in LNG inerting, purging operations, enhanced oil recovery, and food packaging applications.

-

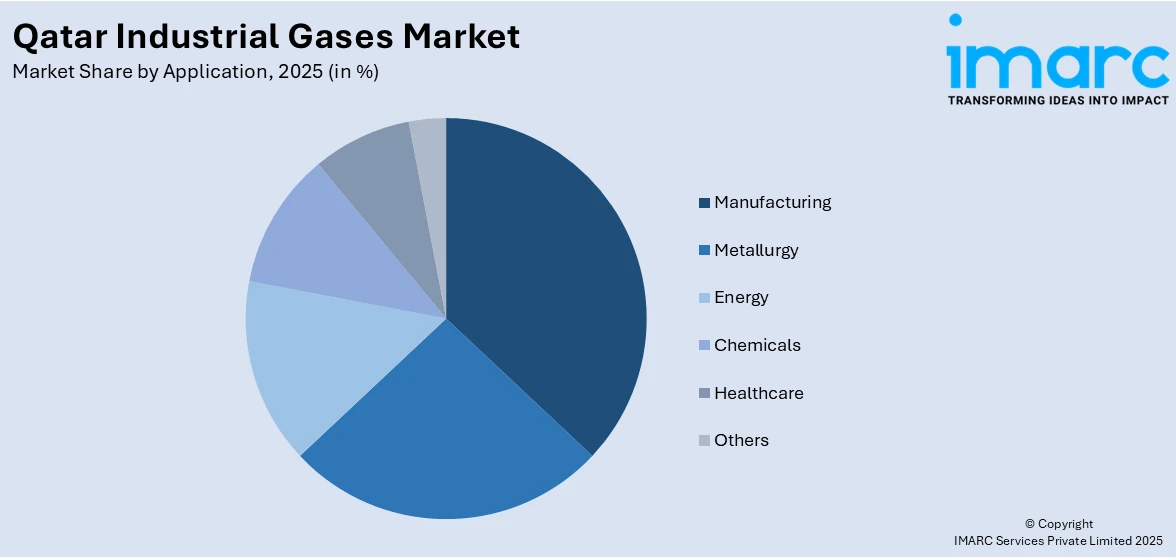

By Application: Manufacturing leads the market with a share of 34.9% in 2025, owing to expanding downstream petrochemical complexes, rising welding and metal fabrication demand, and growing polymer production activities.

-

By Supply Mode: Bulk represents the largest segment with a market share of 48.5% in 2025, driven by its cost-effectiveness for high-volume consumers and efficient cryogenic delivery ensuring uninterrupted industrial supply.

-

By Region: Ad Dawhah leads the market with a share of 42.1% in 2025, owing to the concentration of industrial facilities, healthcare institutions, and manufacturing operations around the capital region.

-

Key Players: The Qatar industrial gases market exhibits a moderately consolidated competitive landscape, with global industrial gas suppliers competing alongside regional manufacturers through long-term supply agreements, on-site generation capabilities, and strategic partnerships with major energy operators.

To get more information on this market Request Sample

The Qatar industrial gases market is experiencing robust growth, underpinned by the nation's strategic investments in energy infrastructure, economic diversification, and industrial modernization. The country's ambitious LNG expansion programs are driving significant demand for nitrogen, hydrogen, and other process gases used in liquefaction, purification, and inerting operations. In September 2025, Messer signed a long-term agreement with QatarEnergy to source approximately three million cubic meters of high-purity helium annually from Ras Laffan, supporting global industrial and medical applications. Simultaneously, the rapid development of downstream petrochemical facilities, integrated polymer complexes, and specialty chemical plants is generating sustained demand for oxygen, argon, and carbon dioxide across manufacturing and processing applications. The healthcare sector is emerging as a key growth driver, with increasing investments in hospital infrastructure and medical facilities boosting demand for medical-grade oxygen and specialty gases. Qatar's National Vision 2030 framework, which emphasizes non-hydrocarbon economic growth, is further catalyzing industrial diversification and expanding the addressable market for industrial gas suppliers.

Qatar Industrial Gases Market Trends:

Rising Adoption of On-Site Gas Generation Technologies

A significant trend shaping the Qatar industrial gases market is the increasing preference for on-site gas generation systems among large industrial consumers. Major energy and petrochemical operators are transitioning from traditional bulk delivery models toward dedicated air separation units and pressure swing adsorption systems installed directly at their facilities. In October 2025, Qatar Shell GTL and Gasal Q.S.C. signed an expanded oxygen supply agreement to support operations at the Pearl GTL gas‑to‑liquids plant in Ras Laffan Industrial City, reinforcing secure, high‑purity gas delivery for continuous industrial processes. This shift is driven by the need for uninterrupted gas supply, reduced logistics dependencies, and greater operational control over gas purity levels.

Growing Integration of Hydrogen in Clean Energy Applications

The emergence of hydrogen as a pivotal element in Qatar's energy transition strategy is reshaping the industrial gases landscape. The country is actively investing in blue hydrogen production capabilities, leveraging its abundant natural gas reserves and carbon capture infrastructure to develop low-carbon hydrogen value chains. In November 2024, QatarEnergy broke ground on a $1.2 billion blue ammonia plant in Mesaieed Industrial City, with 1.2 mtpa capacity, integrating carbon capture and scheduled to begin production in 2026. Moreover, this strategic pivot is creating new demand corridors for hydrogen across industrial applications, including refinery processes, ammonia production, and potential export-oriented supply chains.

Expansion of Healthcare-Driven Demand for Medical Gases

Qatar's healthcare sector is undergoing rapid expansion, with substantial government investments in new hospitals, specialized medical centers, and primary healthcare facilities. This growth trajectory is generating significant demand for medical-grade industrial gases, particularly oxygen for respiratory therapy, surgical applications, and intensive care units, as well as nitrogen for cryogenic medical procedures. In November 2025, Qatar’s Minister of Public Health inaugurated The Pearl International Hospital in Doha, adding a state-of-the-art facility with advanced diagnostics, operating rooms, and specialized clinics to strengthen national healthcare infrastructure.

Market Outlook 2026-2034:

The Qatar industrial gases market is poised for sustained revenue growth over the forecast period, driven by the convergence of energy sector expansion, industrial diversification, and healthcare infrastructure development. Revenue generation will be significantly supported by the commissioning of new LNG production trains, the expansion of petrochemical downstream operations, and the development of blue hydrogen and ammonia production facilities. The country's commitment to non-hydrocarbon economic growth under its National Vision 2030 framework is expected to catalyze new demand across manufacturing, construction, and technology sectors, creating additional revenue streams for industrial gas suppliers. The market generated a revenue of USD 230.78 Million in 2025 and is projected to reach a revenue of USD 326.38 Million by 2034, growing at a compound annual growth rate of 3.93% from 2026-2034.

Qatar Industrial Gases Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Nitrogen |

36.7% |

|

Application |

Manufacturing |

34.9% |

|

Supply Mode |

Bulk |

48.5% |

|

Region |

Ad Dawhah |

42.1% |

Type Insights:

- Nitrogen

- Oxygen

- Carbon Dioxide

- Argon

- Hydrogen

- Others

Nitrogen dominates with a market share of 36.7% of the total Qatar industrial gases market in 2025.

Nitrogen holds the largest share in the Qatar industrial gases market by type, primarily driven by its critical role in the oil and gas sector. The gas is extensively used for inerting, purging, and blanketing operations across LNG production facilities, refineries, and petrochemical plants. As per sources, in November 2025, QatarEnergy confirmed first LNG from its North Field Expansion will be produced in the second half of 2026, with full capacity reaching 126 million metric tons annually by 2027.

In addition to the energy industry, the consumption of nitrogen is also increasing in the food processing and packaging industry, where it is used in modified atmosphere packaging to extend the shelf life of products. The growing food and beverage sector in Qatar, driven by population and consumer demand, is also opening up new avenues for consumption. Moreover, the use of nitrogen in electronics production, metal heat treatment, and chemical synthesis is also on the rise, as Qatar is diversifying its economy.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Manufacturing

- Metallurgy

- Energy

- Chemicals

- Healthcare

- Others

Manufacturing leads with a share of 34.9% of the total Qatar industrial gases market in 2025.

The manufacturing leads the Qatar industrial gases market by application, reflecting the sector's integral role in the nation's economic diversification strategy. Industrial gases such as oxygen, nitrogen, and argon are indispensable in welding, cutting, and metal fabrication processes that underpin manufacturing operations. As per sources, QatarEnergy and Chevron Phillips Chemical began building a $6bn Ras Laffan polymers complex, featuring the Middle East’s largest ethane cracker, reinforcing industrial gas demand across manufacturing and petrochemical operations.

Qatar's national manufacturing strategy aims to strengthen the sector's contribution to gross domestic product and boost non-hydrocarbon exports, driving the establishment of new manufacturing facilities across industrial zones. The integration of advanced manufacturing technologies, including additive manufacturing and precision engineering, is further expanding the range of industrial gas applications. The growing emphasis on smart and green manufacturing practices is also promoting the adoption of high-purity specialty gases in quality assurance and environmental monitoring processes, reinforcing manufacturing's leading position within the industrial gases market.

Supply Mode Insights:

- Packaged

- Bulk

- On-site

Bulk exhibits a clear dominance with a 48.5% share of the total Qatar industrial gases market in 2025.

The bulk supply commands the largest share in the Qatar industrial gases market, driven by the requirements of large-scale industrial consumers in the energy, petrochemical, and manufacturing sectors. Bulk delivery via cryogenic tankers and pipeline networks provides the most cost-effective and reliable solution for facilities with high-volume, continuous gas consumption needs. Major industrial complexes in Ras Laffan and Mesaieed Industrial City rely on bulk supply arrangements to ensure uninterrupted operations across their processing activities.

The predominance of bulk supply is further supported by the small geographical size of Qatar, which ensures that the distance between gas production and consumption points is small. This has reduced the cost of gas transportation and improved the efficiency of the supply chain. On the other hand, the establishment of new industrial areas and the expansion of the existing petrochemical plants are promoting bulk supply agreements between gas companies and industrial enterprises, while integrated supply schemes are further strengthening the leading position of the sector.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah dominates with a market share of 42.1% of the total Qatar industrial gases market in 2025.

Ad Dawhah holds the largest regional share in the Qatar industrial gases market, attributable to its position as the country's primary economic and administrative center. The capital city and its surrounding metropolitan area host the highest concentration of industrial, commercial, and healthcare facilities, generating substantial demand for various industrial gases. The presence of major hospitals, research institutions, and medical centers drives consumption of medical-grade oxygen and specialty gases, while dense commercial and construction activity requires gases for welding, cutting, and fabrication applications across ongoing development projects.

The region's dominance is further supported by its well-developed transportation infrastructure and proximity to key industrial zones, which facilitate efficient gas distribution and delivery networks. Ad Dawhah's role as a hub for financial services, technology, and professional services also generates demand for specialty gases used in laboratory and research applications. The ongoing urban development projects, including commercial complexes, residential developments, and public infrastructure initiatives, continue to sustain demand for industrial gases in construction-related applications, reinforcing the region's leading position within the overall market.

Market Dynamics:

Growth Drivers:

Why is the Qatar Industrial Gases Market Growing?

Massive LNG Expansion Programs Driving Process Gas Demand

Qatar's ambitious LNG expansion initiatives represent one of the most significant growth drivers for the industrial gases market. The country is undertaking large-scale development of new liquefaction trains at its primary production facilities, which will substantially increase its LNG output capacity over the coming years. In February 2024, QatarEnergy awarded major EPC contracts for the North Field South expansion, adding two LNG trains and advancing onshore processing infrastructure at Ras Laffan, strengthening long-term operational intensity. Moreover, these expansion programs require enormous quantities of nitrogen for inerting and purging operations, oxygen for combustion and processing applications, and hydrogen for refining processes.

Strategic Economic Diversification and Industrial Modernization

Qatar's concerted efforts toward economic diversification are creating new and expanding demand channels for industrial gases across multiple sectors. The country's national development strategy emphasizes the growth of non-hydrocarbon industries, including advanced manufacturing, food processing, pharmaceuticals, and technology, all of which are significant consumers of industrial gases. The establishment of new industrial zones, free trade areas, and special economic zones is attracting both domestic and international manufacturers who require reliable industrial gas supply for their operations and production processes.

Rapid Healthcare Infrastructure Expansion

The significant expansion of Qatar's healthcare sector is emerging as a powerful growth driver for the industrial gases market, particularly for medical-grade oxygen and specialty gases. The country is investing heavily in new hospital facilities, specialized medical centers, and primary healthcare infrastructure to meet the needs of its growing population and achieve world-class healthcare standards. In November 2025, Qatar Medicare 2025 convened 100 local and international healthcare companies in Doha, highlighting digital health innovation, smart hospitals, and public-private collaboration under the Ministry of Public Health.

Market Restraints:

What Challenges the Qatar Industrial Gases Market is Facing?

High Capital Investment Requirements for Gas Production Infrastructure

The establishment and expansion of industrial gas production facilities, including air separation units and hydrogen generation plants, require substantial capital investment that can limit market entry and slow capacity expansion. The specialized nature of cryogenic equipment, high-purity gas processing systems, and storage infrastructure demands significant upfront financial commitment, creating barriers for smaller operators and constraining supply growth.

Volatility in Energy Prices Affecting Industrial Activity

Fluctuations in global energy prices can significantly impact Qatar's industrial activity levels and consequently the demand for industrial gases. As the economy remains substantially linked to hydrocarbon revenues, periods of depressed oil and gas prices can lead to reduced capital expenditure across energy and petrochemical sectors, delaying expansion projects and curbing industrial gas consumption.

Logistical and Safety Complexities in Gas Transportation

The transportation and distribution of industrial gases involve inherent logistical complexities and safety considerations that can restrain market growth. High-pressure cylinders, cryogenic liquid tanks, and specialized transport vehicles require trained personnel and stringent safety protocols, increasing operational costs. The extreme climate conditions in Qatar add additional challenges to storage and transportation of temperature-sensitive gases.

Competitive Landscape:

The Qatar industrial gases market features a moderately consolidated competitive structure, characterized by the presence of established global industrial gas suppliers alongside regional producers. Market participants compete on the basis of supply reliability, gas purity specifications, long-term contract offerings, and technical service capabilities. The competitive landscape is shaped by the prevalence of long-term supply agreements with major energy and petrochemical operators, which create significant customer retention advantages for incumbent suppliers. On-site gas generation contracts, where suppliers install and operate production facilities within customer premises, represent a key competitive strategy that enhances supply security and deepens customer relationships.

Recent Developments:

-

In June 2025, OEG signed a long-term partnership with Al Nasr Holding in Qatar, strengthening support for oil, gas, petrochemical, and industrial sectors. The agreement expands logistics capacity through ISO cryogenic nitrogen transport tanks, reinforcing local supply chains, enhancing operational reliability, and supporting Qatar’s expanding energy and industrial infrastructure programs nationwide.

Qatar Industrial Gases Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Nitrogen, Oxygen, Carbon Dioxide, Argon, Hydrogen, Others |

|

Applications Covered |

Manufacturing, Metallurgy, Energy, Chemicals, Healthcare, Others |

|

Supply Modes Covered |

Packaged, Bulk, On-site |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Industrial Gases Market Report

The Qatar industrial gases market size was valued at USD 230.78 Million in 2025.

The Qatar industrial gases market is expected to grow at a compound annual growth rate of 3.93% from 2026-2034 to reach USD 326.38 Million by 2034.

Nitrogen held the largest Qatar industrial gases market share, driven by its extensive utilization in LNG inerting and purging operations, enhanced oil recovery applications, food packaging and preservation processes, and expanding manufacturing sector requirements across the country.

Key factors driving the Qatar industrial gases market include massive LNG expansion programs, strategic economic diversification under National Vision 2030, rapid healthcare infrastructure development, expanding downstream petrochemical operations, and growing demand from manufacturing and construction sectors.

Major challenges include high capital investment requirements for gas production infrastructure, volatility in global energy prices affecting industrial activity levels, logistical and safety complexities in gas transportation, specialized workforce requirements, and the cyclical nature of demand linked to hydrocarbon sector performance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)