Qatar Industrial Real Estate Market Size, Share, Trends and Forecast by Property Type, End Use, Size, Location Type, Sales Channel, and Region, 2026-2034

Qatar Industrial Real Estate Market Summary:

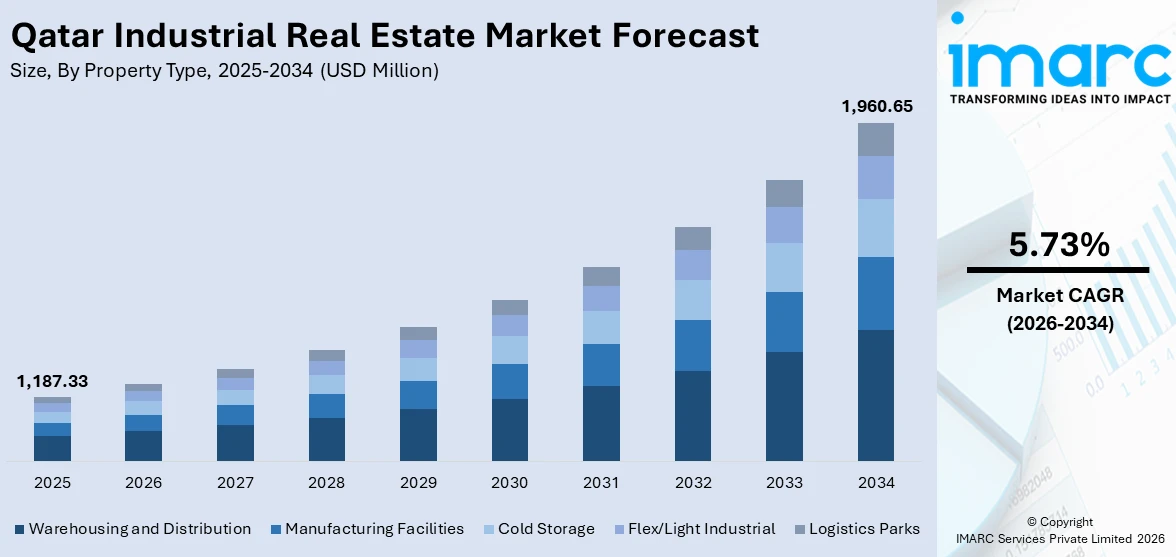

The Qatar industrial real estate market size was valued at USD 1,187.33 Million in 2025 and is projected to reach USD 1,960.65 Million by 2034, growing at a compound annual growth rate of 5.73% from 2026-2034.

The Qatar industrial real estate market is expanding steadily, driven by the nation’s economic diversification strategy and infrastructure modernization efforts. Rising demand for warehousing, logistics facilities, and manufacturing spaces is reshaping the industrial property landscape. Supportive government policies, free zone development, and growing trade activity are accelerating investment in purpose-built industrial assets, positioning Qatar as a competitive regional hub for industrial and logistics operations.

Key Takeaways and Insights:

- By Property Type: Warehousing and distribution dominate the market with a share of 34.9% in 2025, owing to rising import volumes, expanding e-commerce fulfillment requirements, and the strategic positioning of Qatar as a regional trade gateway. Growing investments in modern storage infrastructure are further fueling demand.

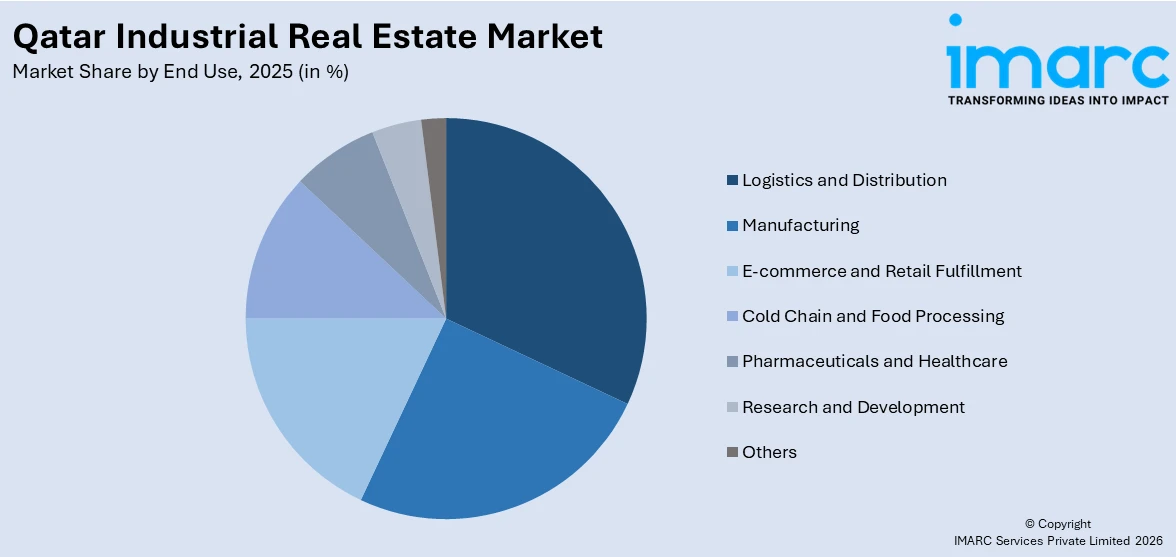

- By End Use: Logistics and distribution lead the market with a share of 31.7% in 2025. This dominance is driven by Qatar’s expanding port and airport infrastructure, rising freight volumes, and the government’s emphasis on establishing the country as a premier logistics hub connecting Asia, Europe, and Africa.

- By Size: Medium exhibits a clear dominance in the market with 42.5% share in 2025, reflecting strong demand from mid-scale logistics operators, manufacturing enterprises, and distribution companies seeking cost-effective industrial spaces with adequate capacity for diversified operations.

- By Location Type: Urban is the biggest segment with 54.8% share in 2025, driven by the concentration of commercial activity in and around Doha, proximity to major transportation networks, and strong tenant demand for accessible industrial facilities near key economic centers.

- By Sales Channel: OEM/authorized dealers represent the leading segment with a market share of 38.2% in 2025, reflecting the preference for professionally managed, standardized industrial property transactions that offer regulatory compliance assurance, after-sales support, and transparent pricing for institutional and corporate tenants.

- By Region: Ad Dawhah is the largest region with 57.3% share in 2025, driven by the capital’s established industrial infrastructure, deep-water port connectivity, proximity to Hamad International Airport, and concentration of government and corporate demand for logistics and warehousing facilities.

- Key Players: Key players drive the Qatar industrial real estate market by expanding logistics capabilities, investing in free zone infrastructure, enhancing warehousing technologies, and forming strategic partnerships with international logistics providers to strengthen supply chain efficiency, attract foreign investment, and ensure consistent availability of modern industrial facilities.

To get more information on this market Request Sample

The Qatar industrial real estate market is advancing as the government, institutional investors, and logistics operators embrace infrastructure modernization and economic diversification. A major driver shaping this progress is the nation's commitment to developing world-class free zones and industrial parks that attract both domestic and international businesses. Strategic reductions in industrial and logistics zone leasing rates by government authorities in collaboration with economic zone operators are lowering entry barriers and encouraging broader investor participation across key industrial corridors. Policy support under Qatar National Vision 2030, the expansion of major port and airport infrastructure, and the rising demand for temperature-controlled storage and e-commerce fulfillment facilities are contributing to a more favorable environment for industrial real estate development. Ongoing improvements in regulatory frameworks, foreign ownership provisions, and streamlined licensing processes are further enhancing the attractiveness of industrial properties for multinational tenants. Growing trade volumes, logistics sector investment, and corporate relocations into purpose-built facilities continue to strengthen Qatar industrial real estate market share.

Qatar Industrial Real Estate Market Trends:

Expansion of Smart Warehousing and Logistics Automation

Qatar is witnessing growing integration of automation, IoT-enabled monitoring, and AI-powered warehouse management systems across its industrial real estate portfolio. Modern facilities are incorporating automated racking, real-time inventory tracking, and predictive maintenance tools to enhance operational efficiency. Leading global logistics providers are establishing technologically advanced regional facilities within Qatar's free zones, featuring integrated warehousing, storage, and office spaces designed to serve as gateways for international freight forwarding operations. These technological upgrades are improving supply chain transparency, reducing operational costs, and supporting Qatar industrial real estate market growth.

Rising Demand for Cold Storage and Temperature-Controlled Facilities

The need for temperature-controlled industrial spaces is intensifying as Qatar expands its food security infrastructure and pharmaceutical distribution networks. National food security strategies are driving sustained investment in cold chain logistics at major ports and inland facilities. The government has prioritized the development of large-scale strategic food storage and processing facilities designed to secure essential commodity reserves for extended periods. The hospitality sector's growth, expanding pharmaceutical distribution requirements, and rising consumer preference for fresh imported foods are further accelerating demand for specialized cold storage industrial properties across key logistics corridors.

Development of Specialized Free Zone Industrial Clusters

Qatar is creating specialized industrial clusters within its free zones to attract sector-specific investment and streamline supply chain operations. Airport-adjacent and seaport-adjacent free zones offer tailored infrastructure for logistics, light manufacturing, and technology companies, providing full foreign ownership, competitive tax structures, and seamless customs integration. Government-operated economic zones are achieving consistently high occupancy levels across industrial, logistics, and commercial spaces, reflecting strong investor confidence. This clustering strategy facilitates knowledge exchange, operational synergies, and enhanced connectivity between complementary industries operating within shared infrastructure ecosystems.

Market Outlook 2026-2034:

Qatar’s industrial real estate market is positioned for sustained expansion, underpinned by strategic government initiatives, growing logistics infrastructure, and rising demand across warehousing, manufacturing, and distribution segments. The market generated a revenue of USD 1,187.33 Million in 2025 and is projected to reach a revenue of USD 1,960.65 Million by 2034, growing at a compound annual growth rate of 5.73% from 2026-2034. The Third National Development Strategy 2024-2030 and the National Manufacturing Strategy are directing substantial investment toward industrial zone modernization, free zone expansion, and supply chain digitalization. The government’s ongoing commitment to reducing reliance on hydrocarbons and fostering knowledge-based industries is expected to diversify tenant demand, attract foreign direct investment, and generate higher revenue streams across the industrial property landscape.

Qatar Industrial Real Estate Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Property Type |

Warehousing and Distribution |

34.9% |

|

End Use |

Logistics and Distribution |

31.7% |

|

Size |

Medium |

42.5% |

|

Location Type |

Urban |

54.8% |

|

Sales Channel |

OEM/Authorized Dealers |

38.2% |

|

Region |

Ad Dawhah |

57.3% |

Property Type Insights:

- Warehousing and Distribution

- Manufacturing Facilities

- Cold Storage

- Flex/Light Industrial

- Logistics Parks

Warehousing and distribution dominate with a market share of 34.9% of the total Qatar industrial real estate market in 2025.

The warehousing and distribution segment leads Qatar’s industrial real estate market, driven by the country’s heavy reliance on imports for consumer goods, food, and industrial materials, which necessitates extensive storage and distribution infrastructure. Qatar’s strategic position at the crossroads of Asia, Europe, and Africa enhances its attractiveness as a regional warehousing hub. In September 2025, FedEx Logistics, along with Qatar Free Zones Authority (QFZ), inaugurated a 1,249 square meter regional logistics facility at Ras Bufontas Free Zone featuring integrated warehousing, storage, and office spaces connected to the global FedEx network for end-to-end supply chain solutions.

Modern warehousing facilities in Qatar are increasingly incorporating automated storage and retrieval systems, advanced inventory management technologies, and energy-efficient building designs to meet the evolving requirements of logistics operators and distribution companies. The expansion of e-commerce and the growing volume of cross-border trade are intensifying demand for purpose-built distribution centers equipped with sorting, packing, and last-mile dispatch capabilities. The government’s focus on developing logistics parks near Hamad Port and Hamad International Airport is further strengthening this segment’s position within Qatar’s industrial property landscape.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Manufacturing

- E-commerce and Retail Fulfillment

- Logistics and Distribution

- Cold Chain and Food Processing

- Pharmaceuticals and Healthcare

- Research and Development

- Others

Logistics and distribution leads with a share of 31.7% of the total Qatar industrial real estate market in 2025.

The logistics and distribution segment commands the largest share of end-use demand in Qatar’s industrial real estate market, reflecting the country’s transformation into a critical regional logistics node. Hamad Port’s transshipment volumes accounted for nearly 50% of total container volumes handled between January to December 2025, underscoring the port’s expanding role as a regional redistribution center. The growth of third-party logistics services, freight forwarding operations, and integrated supply chain solutions is driving consistent demand for large-format distribution facilities across key industrial corridors.

Qatar’s logistics sector is benefiting from the government’s comprehensive investment in multimodal connectivity, including road networks, metro systems, and port and airport expansions. The increasing adoption of digital supply chain management tools, real-time cargo tracking, and automated dispatch systems is elevating the operational standards expected of industrial properties. Logistics operators are seeking modern, well-connected facilities that offer flexible configurations, adequate loading bays, and proximity to major transport corridors, reinforcing the segment’s leading position in shaping industrial real estate demand.

Size Insights:

- Small

- Medium

- Large

Medium is the largest segment, accounting for 42.5% of the Qatar industrial real estate market in 2025.

Medium-sized industrial properties represent the dominant size category in Qatar's market, catering to a broad spectrum of tenants including mid-scale logistics providers, light manufacturing units, and distribution companies. These properties offer an optimal balance between operational capacity and cost efficiency, making them attractive to both domestic enterprises and international firms establishing regional operations. Government-operated economic zones have achieved consistently high occupancy levels, with medium-scale facilities recording strong tenant absorption rates driven by growing industrial diversification and expanding non-hydrocarbon economic activities across the country.

The growing presence of small and medium enterprises in Qatar's industrial sector, supported by government financing initiatives and reduced leasing rates, is sustaining strong demand for medium-sized industrial spaces. These facilities typically accommodate warehousing operations, assembly workshops, spare parts storage, and value-added logistics services. The flexibility offered by medium-format properties in terms of layout customization, scalability, and lease terms makes them well-suited for businesses seeking operational agility without the capital commitment required for large-scale industrial complexes. Streamlined licensing procedures and enhanced investor support services are further encouraging tenant uptake in this segment.

Location Type Insights:

- Urban

- Suburban

- Rural/Peripheral

Urban holds the largest share at 54.8% of the Qatar industrial real estate market in 2025.

Urban industrial real estate dominates the Qatar market, driven by the concentration of commercial and logistics activity within and around the Greater Doha metropolitan area. Proximity to the nation's primary international airport, established road networks, and the metro system enhances the appeal of urban industrial locations for time-sensitive logistics and distribution operations. The capital municipality consistently accounts for the highest share of real estate transaction activity in the country, reinforcing the strong correlation between urban centrality and industrial property demand across warehousing, distribution, and light manufacturing categories.

Urban industrial properties benefit from strong infrastructure connectivity, reliable utility services, and access to a skilled labor pool, all of which are essential for high-frequency logistics and distribution operations. The development of airport-adjacent free zones provides businesses with modern, purpose-built industrial facilities that offer tax incentives, full foreign ownership, and seamless customs integration. Rising e-commerce activity and the demand for rapid last-mile delivery solutions are further concentrating industrial real estate investment in urban zones, while ongoing urban redevelopment initiatives are expanding the availability of functional industrial spaces within established commercial corridors.

Sales Channel Insights:

- OEM/Authorized Dealers

- Independent/Used Vehicle Dealers

- Online Platforms

- Direct-to-Consumer (D2C)

OEM/authorized dealers represent the leading category with 38.2% share of the total Qatar industrial real estate market in 2025.

The OEM and authorized dealer channel lead industrial real estate transactions in Qatar, reflecting the market's preference for professionally managed property acquisition and leasing processes that ensure regulatory compliance and quality assurance. This channel is particularly prominent for institutional tenants and multinational corporations seeking standardized facilities with clear legal frameworks. Free zone authorities are actively developing specialized logistics hubs within designated economic zones, featuring large-format automotive storage, climate-controlled facilities, pre-delivery inspection infrastructure, and integrated warehousing solutions that cater to premium corporate tenants and regional distribution operations.

Authorized dealers and OEM channels provide tenants with transparent pricing structures, comprehensive after-sales support, and access to premium industrial properties that meet international operational standards. The growing participation of government-backed entities in facilitating industrial property transactions through structured programs and investor support platforms further strengthens this channel. Corporate tenants increasingly prefer authorized channels for their ability to bundle property solutions with infrastructure services, licensing support, and customs facilitation. The alignment of these channels with national economic zone strategies enhances their credibility and reliability in attracting long-term institutional investment.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah dominates the Qatar industrial real estate market with 57.3% share in 2025.

Ad Dawhah commands the largest share of Qatar's industrial real estate market, benefiting from its position as the nation's capital and primary commercial center. The municipality's proximity to the country's main international airport and established road networks makes it the preferred location for logistics operators, distribution companies, and manufacturing enterprises. The capital consistently records the highest volume and value of real estate transactions in Qatar, reinforcing its position as the country's dominant industrial and commercial hub supported by deep institutional demand and robust infrastructure connectivity.

The concentration of free zone facilities, government institutions, and corporate headquarters in Ad Dawhah generates sustained demand for modern warehousing, distribution centers, and light industrial properties. Urban redevelopment projects and adaptive-reuse programs are converting underutilized commercial spaces into functional industrial facilities, expanding supply without requiring extensive greenfield development. The availability of skilled labor, reliable utilities, and advanced telecommunications infrastructure further enhances the municipality's attractiveness for industrial real estate investment. Ongoing government-led urban planning initiatives are ensuring that industrial property supply evolves in alignment with growing tenant requirements.

Market Dynamics:

Growth Drivers:

Why is the Qatar Industrial Real Estate Market Growing?

Economic Diversification Under Qatar National Vision 2030

Qatar's comprehensive economic diversification strategy under the National Vision 2030 is fundamentally reshaping demand for industrial real estate. The government's strategic pivot away from hydrocarbon dependence toward manufacturing, logistics, technology, and knowledge-based industries is generating strong demand for purpose-built industrial facilities, research laboratories, and light manufacturing spaces. National manufacturing strategies aim to substantially increase the industrial sector's contribution to the economy, expand non-hydrocarbon exports, and attract higher levels of industrial investment over the coming years. This policy framework is creating a stable and predictable environment for long-term industrial real estate investment. The government's simultaneous focus on regulatory simplification, foreign ownership liberalization, and infrastructure modernization is attracting multinational enterprises and institutional investors to Qatar's industrial property market, driving both greenfield development and adaptive-reuse projects across the country.

Expansion of Free Zones and Industrial Infrastructure

The rapid development of specialized free zones and modern logistics parks is a significant catalyst for Qatar's industrial real estate growth. The Qatar Free Zones Authority administers strategic free zones adjacent to the nation's primary airport and seaport, both offering full foreign ownership, competitive tax rates, and world-class infrastructure. Government authorities have collaborated with economic zone operators to implement substantial reductions in industrial and logistics zone leasing rates, lowering entry barriers for investors across multiple designated zones. These incentives reduce operational costs for industrial tenants and attract investment into warehousing, light manufacturing, and distribution activities. The ongoing development of new logistics parks near major port facilities and industrial cities is expanding the supply of serviced industrial land, enabling businesses of all scales to access modern facilities at competitive rates and strengthening Qatar's positioning as a leading regional industrial hub.

Growing E-Commerce and Logistics Sector Demand

The rapid expansion of e-commerce in Qatar is generating substantial demand for fulfillment centers, last-mile distribution hubs, and automated warehousing facilities. The country's digital commerce ecosystem is growing at an accelerated pace, driven by exceptionally high internet penetration, widespread smartphone adoption, and strong consumer purchasing power. This digital commerce expansion necessitates specialized industrial real estate configurations including sorting facilities, temperature-controlled storage, and quick-dispatch centers. The logistics sector's contribution to Qatar's economy is increasing progressively, with transport and storage activities strengthening their share of national output. Operators are seeking modern facilities near major transport nodes that offer flexible layouts, advanced loading infrastructure, and smart building management systems to support high-velocity distribution operations, further accelerating industrial real estate absorption across key logistics corridors.

Market Restraints:

What Challenges the Qatar Industrial Real Estate Market is Facing?

High Construction and Operational Costs in Extreme Climate

Developing and operating industrial facilities in Qatar’s desert climate demands significant investment in climate control systems, specialized insulation materials, and energy-intensive cooling infrastructure. Extreme summer temperatures substantially increase operational expenses for warehousing and manufacturing properties, particularly cold storage facilities that require continuous temperature regulation. These elevated construction and maintenance costs can deter smaller investors and create financial barriers for emerging industrial enterprises.

Post-World Cup Supply Adjustment in Select Property Segments

The substantial infrastructure development resulted in accelerated construction activity that, in certain commercial and industrial property categories, created temporary oversupply conditions. While adaptive-reuse programs and government-backed absorption strategies are addressing this imbalance, the adjustment period has moderated rental growth expectations in some segments and prompted tenants to negotiate more flexible leasing terms, slowing immediate revenue realization for property developers and investors.

Limited Skilled Workforce and Labor Market Constraints

Qatar’s industrial real estate market faces challenges related to workforce availability, as the country relies heavily on expatriate labor for construction, facility management, and operational activities. Visa regulations, housing requirements for workers, and competition for skilled professionals from neighboring Gulf states create constraints on the pace of industrial property development and facility operations. These labor market dynamics can extend project delivery timelines and increase long-term staffing costs for industrial tenants.

Competitive Landscape:

The Qatar industrial real estate market features a competitive landscape shaped by government-backed entities, established real estate developers, and international logistics providers. Market participants are focusing on developing specialized industrial facilities, enhancing sustainability credentials through green building certifications, and integrating smart building technologies to attract premium tenants. Competition is intensifying as free zone authorities expand incentive programs, reduce leasing rates, and offer customized infrastructure solutions. Strategic partnerships between government bodies and global logistics companies are accelerating the delivery of world-class warehousing and distribution facilities, raising operational standards across the market and strengthening Qatar’s positioning as a leading regional industrial hub.

Qatar Industrial Real Estate Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Property Types Covered |

Warehousing and Distribution, Manufacturing Facilities, Cold Storage, Flex/Light Industrial, Logistics Parks |

|

End Uses Covered |

Manufacturing, E-commerce and Retail Fulfillment, Logistics and Distribution, Cold Chain and Food Processing, Pharmaceuticals and Healthcare, Research and Development, Others |

|

Sizes Covered |

Small, Medium, Large |

|

Location Types Covered |

Urban, Suburban, Rural/Peripheral |

|

Sales Channels Covered |

OEM/Authorized Dealers, Independent/Used Vehicle Dealers, Online Platforms, Direct-to-Consumer (D2C) |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Industrial Real Estate Market Report

The Qatar industrial real estate market size was valued at USD 1,187.33 Million in 2025.

The Qatar industrial real estate market is expected to grow at a compound annual growth rate of 5.73% from 2026-2034 to reach USD 1,960.65 Million by 2034.

Warehousing and distribution dominated the market with a share of 34.9%, driven by rising import volumes, expanding e-commerce fulfillment requirements, and Qatar’s strategic positioning as a regional trade and logistics gateway.

Key factors driving the Qatar industrial real estate market include economic diversification under National Vision 2030, expansion of free zones and logistics infrastructure, growing e-commerce activity, government incentive programs, and rising foreign direct investment.

Major challenges include high construction and operational costs in extreme climate conditions, post-World Cup supply adjustments in select property segments, limited skilled workforce availability, regulatory complexities, and competition from neighboring Gulf states.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)