Qatar LNG Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Qatar LNG Market Summary:

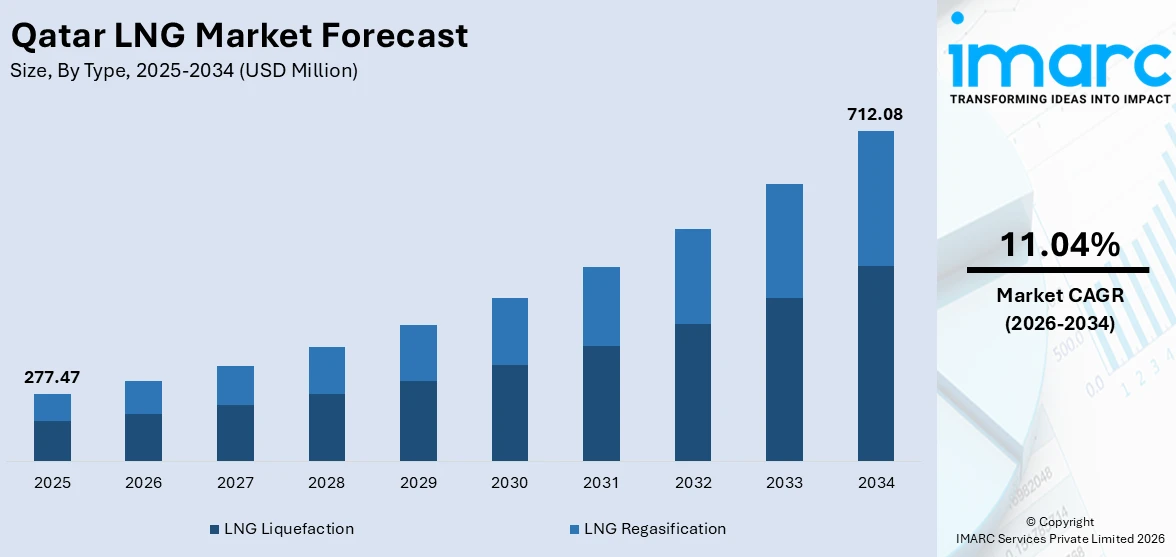

The Qatar LNG market size was valued at USD 277.47 Million in 2025 and is projected to reach USD 712.08 Million by 2034, growing at a compound annual growth rate of 11.04% from 2026-2034.

The Qatar LNG market is expanding rapidly, propelled by the nation’s strategic investments in liquefaction infrastructure and growing international demand for cleaner fossil fuels. The government’s commitment to maximizing natural gas output, coupled with long-term supply agreements across Asia and Europe, strengthens the country’s position as a premier global LNG supplier, supporting sustained market growth and economic diversification aligned with Qatar National Vision 2030.

Key Takeaways and Insights:

- By Type: LNG liquefaction dominates the market with a share of 88.9% in 2025, owing to Qatar’s massive North Field expansion program and the nation’s strategic priority of maximizing LNG export volumes through advanced cooling technologies.

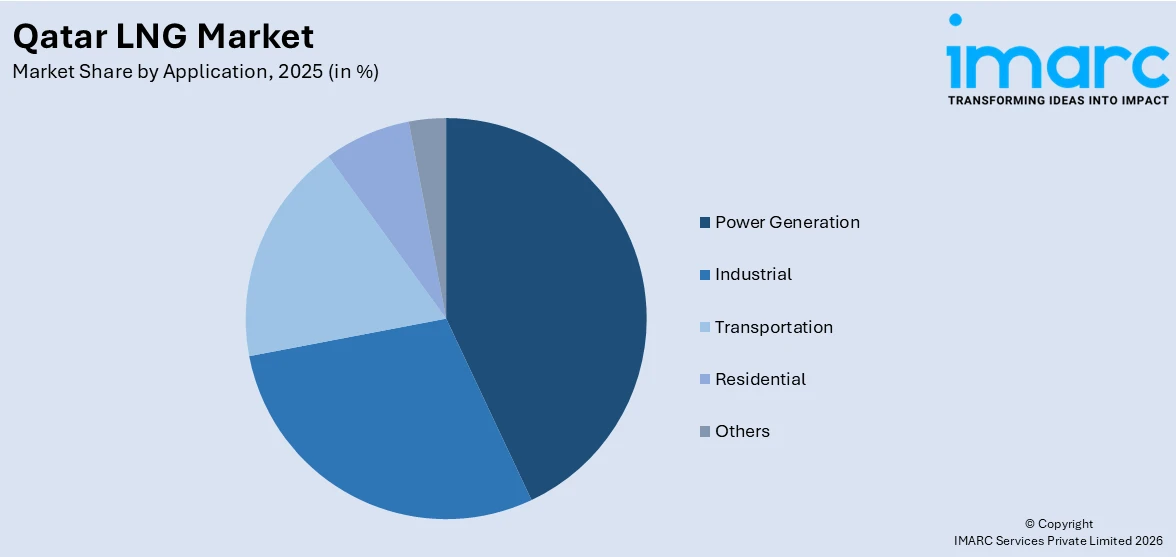

- By Application: Power generation leads the market with a share of 42.7% in 2025. This dominance is driven by the country’s reliance on natural gas-fired power plants for electricity production, expanding desalination requirements, and rising cooling demand from urbanization and infrastructure development projects.

- By Region: Ad Dawhah represents the largest region with 64.2% share in 2025, driven by the concentration of administrative headquarters, decision-making centers, and key energy sector corporate offices in the capital, coupled with proximity to major industrial facilities and port infrastructure supporting LNG operations.

- Key Players: Key players drive the Qatar LNG market by investing in mega-scale liquefaction expansions, deploying carbon capture technologies, building advanced LNG carrier fleets, and forging long-term supply partnerships with Asian and European buyers to strengthen global energy security and market positioning.

To get more information on this market Request Sample

The Qatar LNG market is experiencing a transformative growth phase, driven by large-scale capacity expansion initiatives and sustained investment across the LNG value chain. In February 2024, QatarEnergy announced an initiative to further develop its extensive North Field, which would boost the country's LNG output capacity by a minimum of 16 Million Tons annually. The country’s strategy to significantly increase liquefaction capacity is attracting capital into upstream gas processing, LNG shipping, and downstream distribution infrastructure. The commissioning of large solar photovoltaic facilities at Ras Laffan and Mesaieed reflects a growing focus on lowering the environmental footprint of LNG operations. Continued integration of sustainability measures, carbon capture initiatives, and expanded maritime logistics capabilities is further strengthening the competitiveness of the Qatar LNG sector.

Qatar LNG Market Trends:

Mega-Scale Liquefaction Capacity Broadening

Qatar is undertaking a major expansion of its LNG liquefaction infrastructure, positioning the country to sustain long-term leadership in global LNG supply. Large-scale investments in new liquefaction capacity are focused on deploying advanced cooling, processing, and efficiency-enhancing technologies to improve output reliability and reduce unit costs. This strategic buildout is designed to support rising LNG demand from established and emerging importing markets while strengthening competitiveness through economies of scale. Enhanced operational efficiency across upstream processing, liquefaction, and export logistics is reinforcing Qatar’s ability to deliver stable, long-term LNG supplies. Qatar continued to rank within the top 3 LNG exporters around the world in October 2025.

Integration of Carbon Capture and Storage Technologies

Qatar is embedding carbon capture and storage infrastructure directly into its LNG expansion projects, establishing one of the most ambitious decarbonization programs in the global energy sector. These initiatives are designed to significantly reduce greenhouse gas emissions associated with gas processing and liquefaction activities. By capturing and permanently storing carbon dioxide generated during production, LNG facilities can lower lifecycle emissions and improve environmental performance. The integration of carbon capture technologies also supports compliance with tightening global climate regulations and aligns with buyer preferences for lower-carbon LNG.

Historic Fleet Expansion and Maritime Logistics Modernization

Qatar is building one of the largest LNG carrier fleets in maritime history to support its expanded production and global delivery commitments. In September 2024, QatarEnergy finalized an agreement with China State Shipbuilding Corporation (CSSC) for building 6 more advanced QC-Max vessels, increasing the total LNG vessels ordered in its fleet expansion initiative to 128, which included 24 QC-Max mega vessels. The QC-Max ships are the biggest LNG vessels ever constructed, each having a capacity of 271,000 cubic meters. The latest advanced carriers are expected to arrive between 2028 and 2031. This fleet modernization ensures reliable transportation logistics, reduces per-unit shipping costs, and supports the growing volume of spot market transactions alongside long-term contract deliveries to key Asian and European markets.

Market Outlook 2026-2034:

The Qatar LNG market is poised for robust expansion throughout the forecast period, driven by the sequential commissioning of new liquefaction trains, deepening global demand for cleaner transitional fuels, and the country’s strategic positioning as a reliable long-term energy partner. The market generated a revenue of USD 277.47 Million in 2025 and is projected to reach a revenue of USD 712.08 Million by 2034, growing at a compound annual growth rate of 11.04% from 2026-2034. Growing emphasis on carbon capture integration, fleet modernization, and long-term supply agreements with Asian and European economies will further strengthen market fundamentals, while rising LNG adoption in power generation and industrial applications supports sustained demand across Qatar’s domestic and export-oriented value chains.

Qatar LNG Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

LNG Liquefaction |

88.9% |

|

Application |

Power Generation |

42.7% |

|

Region |

Ad Dawhah |

64.2% |

Type Insights:

- LNG Liquefaction

- LNG Regasification

LNG liquefaction dominates with a market share of 88.9% of the total Qatar LNG market in 2025.

LNG liquefaction holds commanding dominance in the Qatar LNG market, demonstrating the country's strategic emphasis on optimizing capacity for export-oriented gas processing. At Ras Laffan Industrial City, Qatar runs one of the biggest integrated liquefaction complexes in the world. It has several mega-trains that transform enormous amounts of natural gas from the North Field into liquefied form for shipping throughout the world. Advanced liquefaction technology and continuous efficiency improvements greatly increase throughput dependability and cost competitiveness throughout LNG export plants.

The well-connected infrastructure of Qatar benefits the LNG liquefaction sector by integrating facilities for gas processing, storage, and maritime export into a single industrial ecosystem. Handling losses are reduced, operational downtime is reduced, and a faster response to shifts in global market demand is made possible by this relationship. Operational resilience is being improved and unit production costs are being decreased by ongoing investments in automation, predictive maintenance, and energy efficiency improvements. As the demand for LNG increases globally, liquefaction remains the cornerstone of Qatar's LNG value chain, allowing long-term supply guarantees, flexible contract terms, and continued competitiveness in international energy markets.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Power Generation

- Industrial

- Transportation

- Residential

- Others

Power generation leads with a share of 42.7% of the total Qatar LNG market in 2025.

Power generation represents the leading application in the Qatar LNG market, propelled by the nation's heavy reliance on natural gas for district cooling, water desalination, and electricity generation. Gas-fired power plants make up the majority of Qatar's electrical infrastructure, with combined-cycle gas turbines accounting for a major portion of installed generation capacity. Throughout the projected period, the domestic power generation ecosystem will continue to consume a significant amount of LNG-derived gas, due to the fast growing population, accelerated urbanization, and large-scale infrastructure development projects that are driving up peak energy demand.

Qatar's power mix is changing due to the incorporation of renewable energy sources, which strengthens the fundamental role of gas-fired generation. Since intermittent solar output necessitates dependable gas-based backup systems to ensure grid stability, the country's plan to expand its solar capacity to 4 GW by 2030 complements natural gas rather than replaces it. As a result, LNG-based gas generation continues to serve as the backbone of Qatar’s power system, providing flexible load balancing and reliable baseload support alongside the growing share of renewable energy.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah represents the leading region with a 64.2% share of the total Qatar LNG market in 2025.

Ad Dawhah holds an overwhelming share of the Qatar LNG market, driven by its role as the nation’s capital and primary commercial hub where the headquarters of major energy sector entities are located. The municipality’s concentration of corporate decision-making centers, financial institutions, and government regulatory bodies facilitates the coordination of large-scale LNG project investments and procurement activities. Additionally, Doha’s proximity to the Ras Laffan Industrial City, which serves as the operational heart of Qatar’s liquefaction and export operations, strengthens this regional dominance.

The capital region benefits from a vast logistical and transportation network that links it to important facilities for shipping and LNG production. Strong pipeline networks extending from Ras Laffan, strategic marine terminals, and state-of-the-art port infrastructure facilitate the effective transportation of LNG volumes destined for global markets. A comprehensive ecosystem supporting all phases of LNG project development, from preliminary feasibility studies through construction and long-term operational management, is created by the presence of specialized engineering consultancies, technology service providers, and financial advisory firms in Ad Dawhah.

Market Dynamics:

Growth Drivers:

Why is the Qatar LNG Market Growing?

Expanding Demand for Cleaner Transitional Energy

The growing emphasis on reducing carbon emissions from power generation and industrial processes is driving sustained demand for LNG as a cleaner-burning transitional fuel. Countries across Asia, Europe, and emerging markets are increasingly incorporating natural gas into their energy mix as they phase out coal-fired power plants and seek reliable alternatives to intermittent renewable energy sources. Qatar has capitalized on this structural shift by securing an extensive portfolio of long-term supply agreements with major importing nations. As low-carbon power systems are being adopted, LNG is ideally positioned to support energy security due to its reduced emissions profile, operational flexibility, and scalability. To lower geopolitical risks and guarantee supply stability, importing nations are likewise giving varied LNG sourcing top priority. Qatar's position as a key provider in the changing global energy market is being strengthened by these trends, which also increase the long-term demand visibility for its LNG shipments.

Rising LNG Demand from Industrial and Petrochemical Applications

Beyond power generation, the thriving petrochemical and industrial sectors are becoming significant hubs for LNG consumption. As per IMARC Group, the Qatar petrochemicals market size reached USD 1,370.39 Million in 2025. Because of the efficiency and operational dependability of natural gas, it is becoming a more important feedstock and energy source for industries, including chemical, fertilizer, metal, and refining. LNG promotes industrial growth and diversification by providing gas access in areas with poor pipeline infrastructure. Higher gas consumption for petrochemical manufacturing, hydrogen production, and process heating is being driven by developing nations' expanding industrial output. LNG's position as a vital component of industrial value chains is reinforced by this fundamental demand rise. Serving big, long-term industrial buyers helps Qatar maintain broad end use exposure and improve demand stability.

Expansion of LNG Use in Shipping and Marine Fuel Markets

The maritime sector is increasingly adopting LNG as a marine fuel in response to tightening emissions regulations and fuel efficiency requirements. LNG-powered vessels, including container ships, bulk carriers, and tankers, are gaining traction due to lower sulfur emissions and improved operational performance compared to conventional marine fuels. Ports and shipping operators are investing in LNG bunkering infrastructure, supporting wider adoption across major trade routes. This transition is creating a new, structurally growing demand segment for LNG beyond traditional power and industrial uses. As global shipping fleets modernize, LNG demand linked to marine fuel applications is expected to rise steadily. Qatar benefits from this trend as shipping companies seek reliable LNG suppliers capable of supporting long-term fuel contracts and consistent delivery schedules across international maritime corridors.

Market Restraints:

What Challenges the Qatar LNG Market is Facing?

Potential Global LNG Oversupply and Price Pressure

The market faces a growing risk of oversupply as multiple major producers, including the United States, Australia, and emerging exporters in Africa and Southeast Asia, simultaneously expand their liquefaction capacity. This convergence of new supply entering the market could depress spot prices and weaken the incentive for importing nations to commit to long-term purchase agreements at premium pricing levels, potentially affecting Qatar’s revenue projections from uncontracted volumes.

Intensifying Competition from Alternative Energy Sources

The accelerating deployment of renewable energy technologies, particularly solar, wind, and battery storage systems, poses a structural challenge to long-term LNG demand growth. Major importing nations are progressively increasing the share of renewables in their power generation mix, reducing dependence on fossil fuel imports. As the cost of renewable energy continues to decline and grid-scale storage solutions mature, the window for natural gas as a transitional fuel may narrow, potentially limiting future LNG consumption growth in Qatar.

Geopolitical Uncertainties and Regional Security Risks

The Qatar LNG market operates within a geopolitically complex region where tensions between neighboring states, maritime security concerns in key shipping corridors, and broader geopolitical rivalries can create uncertainty for long-term investment planning. Disruptions to shipping routes, diplomatic conflicts, and evolving international sanctions regimes affecting regional energy flows pose risks to the uninterrupted execution of expansion projects and the reliable delivery of contracted LNG volumes to global customers.

Competitive Landscape:

The Qatar LNG market exhibits a highly concentrated competitive structure, dominated by the state-owned energy apparatus operating through strategic partnerships with leading international energy corporations. The market’s competitive dynamics are shaped by massive capital requirements for liquefaction infrastructure, advanced technological capabilities needed for cryogenic processing, and the critical importance of long-term supply contract portfolios. International joint venture partners contribute specialized engineering expertise, financial co-investment, and access to downstream distribution networks in key importing regions. The evolving competitive landscape is further influenced by the integration of sustainability technologies, fleet modernization programs, and the development of LNG trading capabilities that enable participation in both long-term contracted and spot market transactions across global energy exchanges.

Recent Developments:

- In February 2026, QatarEnergy signed 20-year long-term LNG supply agreements with Japan and Malaysia during the LNG 2026 conference held in Doha. The deal with Japan covers up to three Million Tons per year starting in 2028, while the agreement with Malaysia’s Petronas involves two million Tons annually, reinforcing Qatar’s strategic partnerships with key Asian markets.

Qatar LNG Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

LNG Liquefaction, LNG Regasification |

|

Applications Covered |

Power Generation, Industrial, Transportation, Residential, Others |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar LNG Market Report

The Qatar LNG market size was valued at USD 277.47 Million in 2025.

The Qatar LNG market is expected to grow at a compound annual growth rate of 11.04% from 2026-2034 to reach USD 712.08 Million by 2034.

LNG Liquefaction dominated the market with a share of 88.9%, driven by Qatar’s world-class liquefaction infrastructure at Ras Laffan, the North Field expansion program, and the nation’s strategic priority on export-oriented gas processing.

Key factors driving the Qatar LNG market include the growing global demand for cleaner transitional energy, strategic long-term supply agreements with Asian and European economies, and the integration of carbon capture technologies.

Major challenges include potential global LNG oversupply from competing producers, intensifying competition from renewable energy sources, geopolitical uncertainties in the region, evolving environmental regulations on methane emissions, and the operational complexity of executing mega-scale expansion projects on schedule.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)