Qatar Meat Market Size, Share, Trends and Forecast by Type, Product, Distribution Channel, and Region, 2026-2034

Qatar Meat Market Summary:

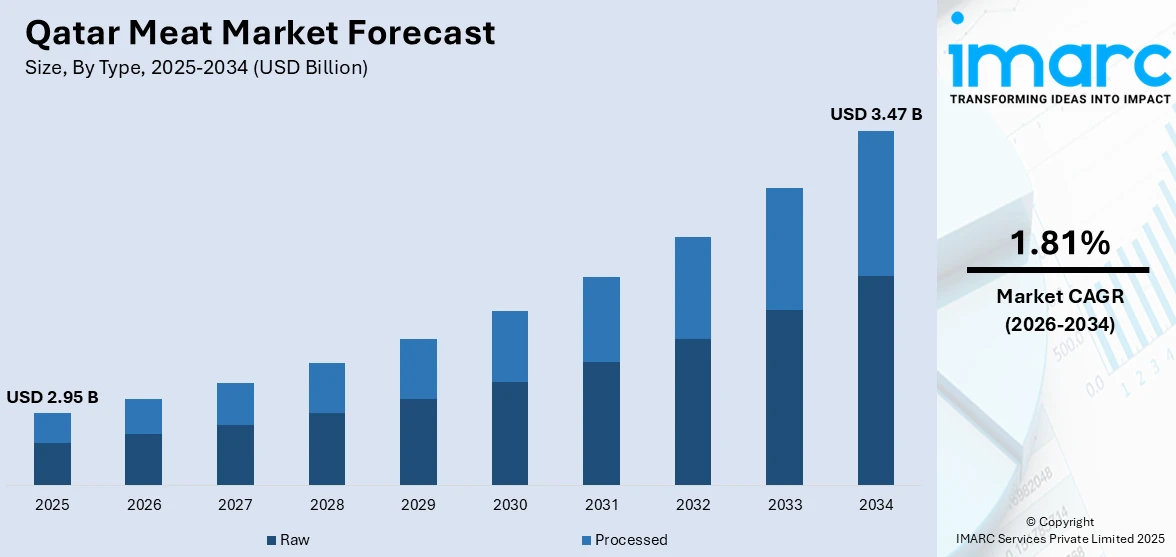

The Qatar meat market size was valued at USD 2.95 Billion in 2025 and is projected to reach USD 3.47 Billion by 2034, growing at a compound annual growth rate of 1.81% from 2026-2034.

The Qatar meat market is driven by rising population growth, increasing disposable incomes, and a shifting preference towards protein-rich diets. Government-led food security initiatives and expanding domestic production capabilities are strengthening supply chain resilience. Modernization of retail infrastructure, growing demand from the hospitality sector, and evolving consumer preferences for fresh, halal-certified meat products are collectively contributing to the sustained expansion of the market share.

Key Takeaways and Insights:

- By Type: Raw dominates the market with a share of 67% in 2025, owing to strong consumer preference for fresh, unprocessed cuts and a deeply rooted culinary tradition favoring home-prepared meals. Rising incomes and expanding retail channels are fueling the segment expansion.

- By Product: Chicken leads the market with a share of 43% in 2025. This dominance is driven by affordability, versatile culinary applications, and high nutritional value that align with the dietary preferences of Qatar’s diverse and growing population base.

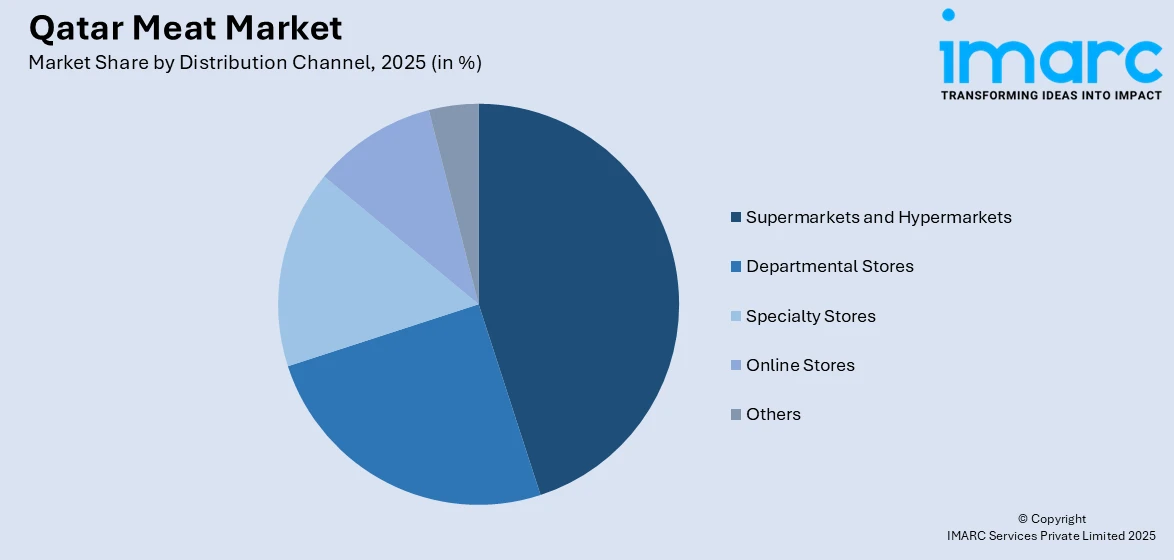

- By Distribution Channel: Supermarkets and hypermarkets prevail the market with a share of 45% in 2025. This leadership is driven by organized retail formats offering superior product variety, stringent hygiene standards, and convenient one-stop shopping experiences that appeal to modern consumers.

- By Region: Ad Dawhah represents the largest region with 53% share in 2025, driven by the concentration of Qatar’s population in the capital city, higher disposable incomes, a vibrant hospitality sector, and extensive retail infrastructure supporting diverse meat product availability.

- Key Players: Key players drive the Qatar meat market by expanding product portfolios, improving processing technologies, and strengthening nationwide distribution networks. Their investments in cold chain infrastructure, halal certification, and partnerships with retailers boost availability, accelerate adoption, and ensure consistent product quality across diverse consumer segments.

To get more information on this market Request Sample

The Qatar meat market is advancing, as government bodies, private enterprises, and consumers collectively prioritize food security, quality nutrition, and sustainable sourcing practices. A major driver shaping this progress is the nation’s strategic commitment to reducing import dependency and building domestic production capacity for essential food commodities. In 2024, Qatar’s Ministry of Municipality reported that the country’s livestock population had grown to 1.1 Million animals, comprising sheep, goats, and camels. Expanding modern retail formats and rising consumer demand for premium halal meat products are contributing to a more favorable environment for market expansion. The hospitality and tourism sectors are also playing a critical role in driving consumption, as hotels, restaurants, and catering services continue to expand their meat-based offerings. Increasing urbanization, a diverse expatriate population, and evolving dietary patterns further reinforce the growth trajectory of the market in Qatar.

Qatar Meat Market Trends:

Rising Demand for Halal-Certified and Premium Meat Products

Qatar is witnessing a growing consumer preference for halal-certified and premium-quality meat products, driven by heightened health consciousness and adherence to Islamic dietary principles. In 2023, the country ranked among the top ten nations on the Global Islamic Economy Indicator, reflecting its strong positioning within the global halal ecosystem. Consumers are increasingly seeking traceable, ethically sourced, and antibiotic-free meat options, pushing producers and retailers to adopt advanced quality assurance protocols. This rising preference is expanding the availability of premium cuts and organic meat across retail and foodservice channels.

Expansion of E-Commerce and Digital Food Retail Platforms

Digital transformation is reshaping how Qatari consumers access and purchase meat products. With 3.05 Million people accessing the internet in Qatar at the beginning of 2025, online grocery platforms and mobile delivery applications are experiencing rapid adoption. Major retailers have integrated meat delivery into their digital platforms, offering tracking, quality assurance, and same-day delivery options. This trend is supporting the Qatar meat market growth by improving accessibility and convenience for both urban and suburban consumers.

Modernization of Meat Processing and Cold Chain Infrastructure

Qatar is investing heavily in advanced meat processing technologies and cold chain logistics to enhance product quality and supply chain efficiency. As per IMARC Group, the Qatar cold chain logistics market size reached USD 584.12 Million in 2024. Automated slaughterhouses have been established across key locations, including Al Wakra, Umm Salal, Al Sheehaniya, Al Khor, and Al Shamal, ensuring consistent fresh meat supply. Blockchain-based traceability systems and artificial intelligence (AI)-driven quality control measures are being adopted to meet stringent food safety regulations and maintain halal compliance throughout the distribution network.

Market Outlook 2026-2034:

The Qatar meat market is positioned for sustained growth, underpinned by strategic government investments in food security, expanding domestic production capacity, and evolving consumer preferences for high-quality, halal-certified meat products. The market generated a revenue of USD 2.95 Billion in 2025 and is projected to reach a revenue of USD 3.47 Billion by 2034, growing at a compound annual growth rate of 1.81% from 2026-2034. Continued modernization of retail infrastructure, cold chain improvements, and technology-driven supply chain management are expected to strengthen distribution efficiency and product freshness. Rising contributions from the tourism and hospitality sectors, coupled with growing expatriate demand for diverse protein options, will further support revenue expansion.

Qatar Meat Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Raw |

67% |

|

Product |

Chicken |

43% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

45% |

|

Region |

Ad Dawhah |

53% |

Type Insights:

- Raw

- Processed

Raw dominates with a market share of 67% of the total Qatar meat market in 2025.

Raw maintains its commanding position in the Qatar meat market, driven by deep-rooted cultural preferences for fresh, unprocessed cuts used in traditional Qatari cuisine. Consumers prioritize quality and freshness, particularly for home cooking, where whole chickens, fresh lamb, and beef cuts are essential ingredients. The preference for freshly slaughtered meat, aligned with halal practices, further reinforces demand for raw formats. Seasonal festivals and family gatherings also boost household consumption of fresh meat, supporting consistent year-round demand.

The growth of structured retail channels, where specialized fresh meat counters with temperature-controlled display units guarantee product quality and customer confidence, is advantageous to the segment. A sizable client base is served by traditional wet markets and butcher shops, especially in residential areas where patrons value individualized attention and specialized cuts. Raw meat consumption is further fueled by the expanding hospitality industry, which includes lodging facilities, dining venues, and catering services. As per IMARC Group, the Qatar hospitality market size reached USD 3,794.08 Million in 2025. These businesses need to purchase large quantities of high-quality fresh cuts for their varied menus.

Product Insights:

- Chicken

- Beef

- Pork

- Mutton

- Others

Chicken leads with a share of 43% of the total Qatar meat market in 2025.

Chicken maintains its leadership in the Qatar meat market, owing to its affordability, nutritional profile, and versatility across diverse culinary applications. The product serves as the primary protein source for households, restaurants, and institutional buyers, reflecting its broad consumer appeal. Qatar achieved an impressive 98% self-sufficiency rate in fresh poultry meat production in 2024, supported by local producers who collectively delivered over 21,737 Tons of domestically produced poultry to meet national consumption demands. This strong domestic supply base reinforces chicken’s availability and affordability across retail and foodservice channels.

The market position of this segment is being further reinforced by the rising demand for processed chicken items, such as kebabs, sausages, nuggets, and marinated ready-to-cook choices. The quality of products and consumer confidence are being improved by modern production facilities with fully automated processing lines and strict halal certification requirements. In addition to increasing institutional procurement of chicken, the growing number of quick-service restaurants (QSRs) and informal dining outlets throughout Qatar is generating a steady demand cycle that supports both fresh and frozen product categories.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Departmental Stores

- Specialty Stores

- Online Stores

- Others

Supermarkets and hypermarkets exhibit a clear dominance with a 45% share of the total Qatar meat market in 2025.

Supermarkets and hypermarkets continue to be the primary distribution channel for meat products in Qatar, leveraging their extensive product assortment, standardized hygiene practices, and convenient shopping formats. Major retail chains have expanded their dedicated meat sections with temperature-controlled display units, halal-certified counters, and in-store butchery services that enhance the consumer experience. Extended operating hours and centralized sourcing models further improve product availability and pricing consistency for consumers.

The leadership of this channel is being strengthened by the ongoing development of organized retail infrastructure, which includes the launch of new hypermarkets and store renovations. To enhance in-store experiences, retailers are incorporating digital features, including click-and-collect services, online ordering, and delivery via mobile applications. Leading supermarket chains' private label meat brands are becoming more popular among consumers because they offer high-quality goods at affordable prices, solidifying the place of supermarkets and hypermarkets in Qatar’s meat distribution business.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah represents the leading region with a 53% share of the total Qatar meat market in 2025.

Ad Dawhah maintains its dominance in the Qatar meat market, driven by its position as the capital city with the highest population density, economic activity, and concentration of commercial establishments. The municipality hosts the majority of Qatar’s supermarkets, hypermarkets, specialty meat retailers, and foodservice establishments, ensuring extensive meat product availability across all categories. Well-developed cold chain infrastructure and efficient logistics networks also support consistent supply and quality across the municipality.

Demand for a broad range of meat variations, ranging from premium cuts and imported specialty meats to common poultry products, is driven by the region's wealthy and diversified consumer base, which includes both locals and a sizable expatriate community. Institutional meat procurement is greatly influenced by Doha's thriving tourism and hospitality industry, which includes five-star hotels, global restaurant chains, and catering services. Ad Dawhah's dominant position in the Qatar meat market is further strengthened by ongoing commercial expansions and urban development initiatives in the municipality, which draw in new foodservice operators and retail formats.

Market Dynamics:

Growth Drivers:

Why is the Qatar Meat Market Growing?

Government-Led Food Security and Domestic Production Initiatives

Qatar’s strategic focus on food security is a pivotal driver of the market, with the government implementing comprehensive programs to enhance self-sufficiency and reduce dependence on imports. The National Food Security Strategy 2030 sets ambitious targets, including achieving 30% self-sufficiency in sheep and goat meat production and maintaining existing poultry self-sufficiency levels. These government-backed initiatives are complemented by significant investments in agricultural technology, biosecurity protocols, and modern farming infrastructure. Public-private partnerships (PPPs) are further accelerating progress, with institutions coordinating livestock development programs and processing facility upgrades. In parallel, capacity expansion in local slaughterhouses and cold storage facilities is improving domestic processing efficiency. These collective efforts are building a more resilient meat supply ecosystem that supports long-term market expansion across Qatar.

Expanding Tourism and Hospitality Sector Driving Institutional Demand

Qatar’s rapidly growing tourism and hospitality sectors are generating substantial demand for meat products across institutional channels. Hotels, restaurants, catering companies, and airline kitchens require consistent, high-volume supplies of fresh and processed meat to serve diverse international clientele. In 2025, Qatar welcomed 5.1 Million foreign tourists, indicating a yearly increase of 3.7%, demonstrating the pace of tourism expansion. The hospitality industry’s demand spans a wide range of meat products, ranging from premium cuts for fine-dining establishments to standardized processed options for QSRs and catering operations. Ongoing investments in tourism infrastructure, including new hotel developments, entertainment venues, and sports facilities, are creating sustained procurement channels. As Qatar continues to position itself as a leading destination for business and leisure tourism, the institutional demand for quality meat products is expected to remain a significant growth contributor.

Rising Population and Evolving Dietary Preferences Towards Protein-Rich Foods

Qatar’s growing and increasingly diverse population is driving elevated demand for meat products as dietary preferences shift towards protein-rich food consumption. The country’s large expatriate community, representing multiple nationalities and culinary traditions, creates demand for varied meat types, including chicken, beef, mutton, and specialty cuts from different global cuisines. In 2024, expats comprised 88.4% of the total population, equating to approximately 2.76 Million. Higher disposable incomes and economic diversification are enabling more households to access premium and value-added meat products. The shift towards protein-enriched diets is further supported by rising health and wellness awareness, where consumers increasingly recognize the nutritional benefits of lean meats and quality protein sources. Modern retail formats are responding by expanding their fresh meat sections, introducing organic and antibiotic-free options, and providing greater product variety. These evolving consumption patterns, combined with population growth projections, are establishing a strong foundation for sustained meat market expansion in Qatar.

Market Restraints:

What Challenges the Qatar Meat Market is Facing?

Heavy Dependence on Meat Imports and Supply Chain Vulnerabilities

The Qatar meat market remains significantly reliant on imports to meet domestic consumption requirements. This heavy dependence exposes the market to global supply chain disruptions, fluctuating international commodity prices, and geopolitical uncertainties that can affect both availability and affordability. Climate-related challenges and limited arable land further constrain the expansion of local livestock production, making the country vulnerable to external supply shocks.

Rising Feed Costs and Production Input Constraints

Fluctuating prices of animal feed, which is predominantly imported, represent a persistent challenge for domestic meat producers in Qatar. These cost pressures directly impact production economics, particularly for poultry and livestock farming operations that depend on consistent and affordable feed supply. Volatile global grain markets, transportation costs, and storage requirements further add to operational burdens, potentially limiting the ability of local producers to scale output and maintain competitive pricing against imported alternatives.

Stringent Regulatory and Halal Compliance Requirements

Strict food safety regulations, halal certification standards, and import quality controls, while essential for consumer protection, impose significant compliance costs on market participants. Producers, importers, and retailers must invest heavily in quality assurance infrastructure, laboratory testing, and certification processes to meet regulatory requirements. These compliance demands can create entry barriers for smaller operators and increase operational costs across the value chain, potentially constraining market competitiveness and slowing the introduction of new product offerings.

Competitive Landscape:

The Qatar meat market features a moderately concentrated competitive structure, with a combination of established domestic producers, regional suppliers, and international food companies vying for market share. Companies are focusing on diversifying product offerings, enhancing processing capabilities, and strengthening distribution networks to capture a larger consumer base. Competition is also driven by investments in cold chain logistics, halal certification expansion, and technological adoption in production facilities. Strategic partnerships between local distributors and international meat suppliers are facilitating product innovation and improving supply chain efficiency. As consumer preferences evolve towards premium, organic, and convenience-oriented meat products, market players are continually refining their strategies to strengthen positioning and capitalize on emerging growth opportunities.

Recent Developments:

- In February 2025, the Ministry of Commerce and Industry launched a national initiative to encourage local production and subsidize red meat prices for the holy month of Ramadan. Widam Food Company was designated to provide local and imported sheep to citizens at subsidized prices of QR 1,000 per head through its slaughterhouses across Qatar, aiming to stabilize market prices and ensure affordable meat availability.

Qatar Meat Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Raw, Processed |

|

Products Covered |

Chicken, Beef, Pork, Mutton, Others |

|

Distribution Channels Covered |

Supermarkets and Hypermarkets, Departmental Stores, Specialty Stores, Online Stores, Others |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Meat Market Report

The Qatar meat market size was valued at USD 2.95 Billion in 2025.

The Qatar meat market is expected to grow at a compound annual growth rate of 1.81% from 2026-2034 to reach USD 3.47 Billion by 2034.

Raw dominated the market with a share of 67%, driven by strong consumer preference for fresh, unprocessed cuts used in traditional home cooking and widespread availability across organized retail channels and traditional butcheries.

Key factors driving the Qatar meat market include government food security initiatives, expanding domestic production capacity, rising population growth, increasing disposable incomes, growing hospitality sector demand, and evolving consumer preferences towards premium protein-rich diets.

Major challenges include heavy dependence on meat imports, supply chain vulnerabilities to global disruptions, rising animal feed costs, stringent regulatory and halal compliance requirements, limited arable land for livestock expansion, and production cost pressures facing domestic producers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)