Qatar Mobile Payments Market Size, Share, Trends and Forecast by Payment Type, Application, and Region, 2026-2034

Qatar Mobile Payments Market Summary:

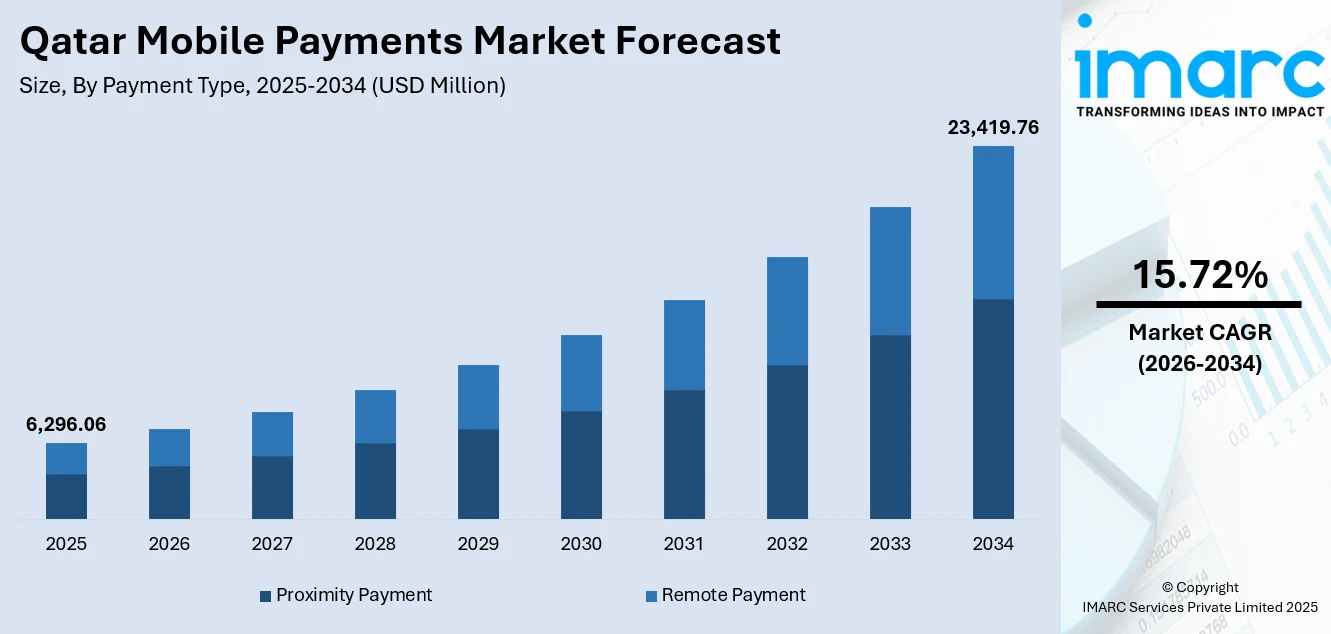

The Qatar mobile payments market size was valued at USD 6,296.06 Million in 2025 and is projected to reach USD 23,419.76 Million by 2034, growing at a compound annual growth rate of 15.72% from 2026-2034.

The Qatar mobile payments market is experiencing robust growth driven by rapid digital transformation, widespread smartphone adoption, and supportive government initiatives promoting cashless transactions. The country's modern financial infrastructure, enhanced by FIFA 2022 World Cup legacy investments in contactless payment terminals, continues to strengthen adoption rates. Rising e-commerce activities, integration of mobile payment solutions with retail platforms, and strategic fintech partnerships are accelerating the shift toward digital financial services. These developments are shaping payment behaviors across consumer and commercial segments, positively influencing the Qatar mobile payments market share.

Key Takeaways and Insights:

- By Payment Type: Proximity payment dominates the market with a share of 55% in 2025, driven by widespread NFC-enabled terminal coverage at retail outlets, fuel stations, and hospitality venues following infrastructure upgrades.

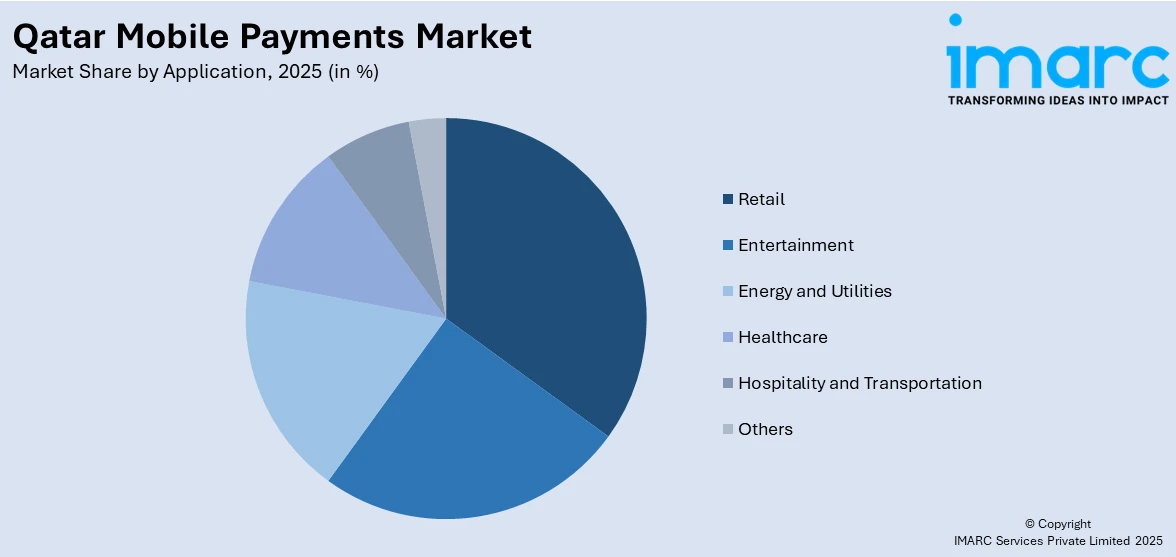

- By Application: Retail leads the market with a share of 28% in 2025, supported by high merchant adoption of mobile payment acceptance and integration with loyalty programs across shopping centers.

- By Region: Ad Dawhah represents the largest segment with a market share of 40% in 2025, attributed to its status as the capital with concentrated merchant density, financial institutions, and tech-savvy consumer population.

- Key Players: The Qatar mobile payments market exhibits a dynamic competitive landscape with major banks, telecommunications companies, and fintech providers competing through digital wallet innovations, strategic partnerships, and enhanced payment solutions to capture growing consumer demand for seamless mobile transactions.

To get more information on this market Request Sample

The Qatar mobile payments market is evolving rapidly as the country advances its digital financial transformation in line with national development objectives. Government-led initiatives have established a strong foundation for mobile payment adoption, providing the regulatory and technological frameworks needed for widespread use. The telecommunications sector plays a central role, offering integrated mobile wallet solutions that enable peer-to-peer transfers, bill payments, and retail transactions. Strategic collaborations with global payment platforms are further enhancing cross-border payment capabilities and strengthening Qatar’s position as a regional fintech hub. High smartphone adoption, robust digital infrastructure, and growing consumer preference for convenient, fast, and secure contactless payment methods are driving market growth. Together, these factors are fostering an ecosystem where mobile payments are increasingly embedded in everyday financial activities, supporting broader financial inclusion, digital innovation, and seamless transactional experiences for both consumers and businesses across the country.

Qatar Mobile Payments Market Trends:

Rising Digital Wallet Adoption and Financial Inclusion

Digital wallet adoption is accelerating across Qatar as consumers increasingly favor mobile-first banking solutions for everyday transactions. Recent regulatory measures enabling greater flexibility and interoperability within the mobile payment system are fostering broader wallet usage and promoting financial inclusion across diverse population segments. The trend toward cashless transactions is being supported by instant payment infrastructure, which allows seamless peer-to-peer transfers and merchant payments. These developments are driving the growth of the mobile payments market, reflecting a broader shift in consumer behavior toward convenient, secure, and efficient digital financial solutions.

Integration with E-Commerce and Retail Platforms

Mobile payments integration with retail and e-commerce platforms represents a significant market driver, with mobile devices generating approximately seventy percent of e-commerce revenue in 2024. Retailers are deploying mobile payment acceptance solutions to enhance customer engagement, streamline checkout processes, and implement loyalty programs. For instance, in April 2025, the Qatar Central Bank (QCB) reported that transactions processed via point-of-sale terminals and online commerce platforms amounted to QR 13.8 billion in March 2025, demonstrating strong consumer adoption. QR code-based payments, app-based solutions, and biometric authentication methods are gaining widespread acceptance across shopping centers, supermarkets, and service establishments, creating an interconnected payment ecosystem.

Contactless and NFC Payment Technology Expansion

Contactless and near-field communication (NFC) payment technologies are reshaping Qatar’s payment ecosystem, driving widespread adoption across retail, transportation, and service sectors. Infrastructure improvements following major events have strengthened tap-to-pay capabilities at merchants, fueling convenience and efficiency for consumers. NFC-enabled smartphones, wearables, and smart devices are increasingly used for everyday transactions, while global mobile wallet platforms integrate loyalty programs and secure authentication features. These developments are collectively enhancing digital payment accessibility, promoting cashless transactions, and supporting the ongoing growth of Qatar’s mobile payments market.

Market Outlook 2026-2034:

The outlook for Qatar’s mobile payments market remains very positive, driven by ongoing government investment in digital infrastructure, growing fintech collaborations, and increasing consumer preference for cashless transactions. The country’s instant payment system showcases strong demand for fast, seamless transfers, while strategic partnerships with global payment networks are enhancing cross-border capabilities. These developments are positioning Qatar as a regional hub for digital payments, supporting broader financial inclusion, facilitating efficient transactions, and reinforcing the adoption of mobile and wallet-based solutions across retail, services, and commercial sectors. The market generated a revenue of USD 6,296.06 Million in 2025 and is projected to reach a revenue of USD 23,419.76 Million by 2034, growing at a compound annual growth rate of 15.72% from 2026-2034.

Qatar Mobile Payments Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Payment Type | Proximity Payment | 55% |

| Application | Retail | 28% |

| Region | Ad Dawhah | 40% |

Payment Type Insights:

- Proximity Payment

- Near Field Communication (NFC)

- Quick Response (QR) Code

- Remote Payment

- Internet Payments

- Direct Operator Billing

- Digital Wallet

- SMS Payments

Proximity payment dominates with a market share of 55% of the total Qatar mobile payments market in 2025.

Proximity payments encompassing NFC and QR code transactions represent the largest payment type segment, driven by extensive merchant terminal coverage and consumer preference for quick, secure contactless transactions. The segment benefits from infrastructure investments made during the FIFA 2022 World Cup, which established near-universal terminal coverage at fuel stations, grocery stores, and pharmacies. Major financial institutions continue deploying advanced payment acceptance solutions including biometric authentication and tap-to-pay capabilities across retail networks.

NFC technology enables seamless transactions through smartphones and wearables, with global mobile wallets maintaining strong adoption through banking partnerships. QR code payments are gaining traction through the Qatar Mobile Payment system's standardized infrastructure, although fragmented adoption among small and medium enterprises remains a consideration. For instance, in February 2025, QNB collaborated with NPCI International Payments Limited (NIPL) to facilitate QR code-based Unified Payments Interface (UPI) transactions for merchants onboarded by the bank. This initiative enables Indian travelers to make seamless payments using UPI across QNB’s payment network, covering airports, hotels, tourist sites, restaurants, and retail outlets, enhancing convenience and promoting digital payment adoption within Qatar’s merchant ecosystem, facilitating reduced cash dependency among residents and visitors while demonstrating the segment's continued expansion.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Entertainment

- Energy and Utilities

- Healthcare

- Retail

- Hospitality and Transportation

- Others

Retail leads with a share of 28% of the total Qatar mobile payments market in 2025.

Retail is the leading segment in Qatar’s mobile payments market due to the high frequency of daily consumer transactions. Supermarkets, convenience stores, and specialty retailers increasingly adopt digital payment solutions to offer faster, more convenient checkout experiences. Contactless payments, QR codes, and mobile wallets enable seamless transactions, enhancing customer satisfaction. The integration of loyalty programs and promotions within retail mobile payment platforms further drives adoption, reinforcing retail’s dominant role in shaping Qatar’s digital payments ecosystem.

Retail’s leadership is also supported by widespread deployment of advanced payment infrastructure, including NFC-enabled terminals and e-commerce integration. Urban retail outlets and high-footfall commercial centers provide ideal environments for mobile wallet usage, while promotional campaigns and digital engagement initiatives encourage frequent use. Combined with consumer preference for cashless transactions, these factors make the retail sector the primary driver of mobile payment growth, ensuring consistent transaction volumes and sustained market expansion across Qatar.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah exhibits clear dominance with a 40% share of the total Qatar mobile payments market in 2025.

Ad Dawhah, as Qatar’s capital and largest urban center, is driving mobile payments adoption due to its dense population and high smartphone penetration. Residents increasingly prefer cashless and mobile-first solutions for daily transactions, from retail and dining to transportation services. Widespread digital literacy, combined with strong internet connectivity and reliable mobile networks, supports seamless use of mobile wallets, QR code payments, and NFC-enabled transactions, encouraging broader acceptance of digital financial services and fostering growth in the city’s mobile payments ecosystem.

The city’s advanced retail and service landscape further propels mobile payment adoption. Supermarkets, shopping malls, hospitality venues, and e-commerce platforms are integrating digital wallets to offer faster, contactless payment options. Government-backed initiatives and collaborations with global payment networks enhance convenience and security, while loyalty programs and promotional campaigns encourage frequent usage. These factors, coupled with a tech-savvy urban population, position Ad Dawhah as the leading hub for mobile payment growth in Qatar.

Market Dynamics:

Growth Drivers:

Why is the Qatar Mobile Payments Market Growing?

Government Initiatives and Regulatory Support for Digital Transformation

The Qatar Central Bank's proactive regulatory approach represents a primary growth driver, with the Third Financial Sector Strategy establishing clear frameworks for digital payment innovation. For instance, the December 2024 launch of QA-RTGS aligned Qatar's settlement backbone with ISO 20022 standards, providing banks with immediate and irrevocable gross settlement capabilities alongside richer data fields. The Fawran instant payment service has processed millions of transactions, demonstrating strong demand for seamless peer-to-peer transfers using phone numbers rather than traditional banking identifiers. Regulatory decisions to open API-based direct integration for fintechs have reduced friction and promoted product diversity. The Qatar Central Bank reduced and unified merchant discount rates for electronic payments, implementing favorable fee structures that encourage small business adoption and advance cashless economy objectives aligned with Qatar National Vision 2030.

High Smartphone Penetration and Advanced Digital Infrastructure

Qatar benefits from widespread smartphone usage and strong mobile connectivity, making mobile payments a natural choice for everyday transactions across consumer groups. Easy access to smart devices and reliable internet services supports seamless digital purchases, bill payments, and peer-to-peer transfers. Ongoing government focus on strengthening digital infrastructure, cloud capabilities, and smart city initiatives is enhancing the scalability and security of payment platforms. High-quality connectivity also enables integrated digital experiences, creating a supportive ecosystem for the continued expansion of mobile and digital financial services.

Rising E-Commerce Adoption and Changing Consumer Preferences

Qatar's e-commerce market continues experiencing robust growth, reflecting changing consumer behaviors with substantial portions of the population now shopping online. The Qatar e-commerce market size reached USD 3.8 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 10.1 Billion by 2033, exhibiting a growth rate (CAGR) of 10.27% during 2025-2033. The move to online shopping has highlighted the need to have an efficient and secure way of payment, which has prompted companies to incorporate high-level digital payment systems in their system. The Qatar digital average transaction amounts are much higher than regional averages, which indicates that the level of purchasing power and the inclination toward high-quality products among the population is high. Most of the e-commerce revenue is made through mobile commerce, which is complemented by biometrics, instant-pay rails, and live-stream shopping to make mobile devices the primary channel of choice when it comes to buying fashion, beauty, and on-demand food. Responsive design and data-light experiences are of interest to retailers as their goal is to reap the benefits of maximum reach, and the integration of app-based loyalty programs and mobile wallets strengthens the mobile-first profile of the market.

Market Restraints:

What Challenges the Qatar Mobile Payments Market is Facing?

Cybersecurity Concerns and Fraud Prevention Requirements

The mobile payments industry has a great deal to do with cybersecurity, which is reported to be escalating with the volume of digital transactions. Both consumers and businesses need to be assured that their money and transactions are secured against the changing threats. Multi-factor authentication requirements on high-risk transfers and investments in behavioural biometrics help to ease these concerns, but create complexity in the implementation of these services by service providers.

Limited Consumer Awareness in Underserved Segments

Despite high overall digital adoption rates, limited awareness about mobile payment benefits persists among certain consumer segments including older demographics and populations in areas outside major urban centers. Financial literacy gaps regarding digital wallet functionality, security features, and available services restrict broader adoption. Competition from traditional banking services and established cash transaction habits continues to influence consumer behavior in specific market segments.

Fragmented QR Code Standards Among Small Merchants

Many small retailers continue relying on proprietary QR codes rather than the standardized Qatar Mobile Payment system infrastructure, leading to inconsistent consumer experiences. Despite regulatory subsidies for merchant onboarding and integration efforts, costs and training requirements temper immediate adoption among small and medium enterprises. This fragmentation moderates the short-term growth trajectory and creates complexity for consumers navigating different payment acceptance methods across merchants.

Competitive Landscape:

The Qatar mobile payments market exhibits a dynamic competitive structure with major banking institutions, telecommunications providers, and emerging fintech companies competing across multiple segments. Universal banks lead in merchant acquiring and wallet-linkage innovations, with dominant players expanding digital payment service offerings and enhancing customer engagement through technology investments. Telecommunications operators leverage extensive subscriber networks and airtime channels to deliver peer-to-peer transfer services while expanding into adjacent financial services including micro-lending. Fintech entrants are introducing competitive fee structures and innovative solutions in buy-now-pay-later and small-merchant payment gateways, compressing traditional interchange margins. Strategic partnerships between local and international players are reshaping competitive dynamics, with collaborations enabling cross-border payment capabilities and expanded merchant networks. Companies are continuously refining their strategies through technology investments, improved user experiences, and expanded service portfolios to strengthen market positioning.

Recent Developments:

- October 2025: Ooredoo Fintech partnered with PayPal to join PayPal World, enabling seamless global payments for consumers and merchants. The collaboration enhances cross-border transactions, expands wallet accessibility, and strengthens Qatar's digital financial ecosystem by connecting Ooredoo Money users with millions of merchants worldwide who accept PayPal.

- March 2025: Doha Bank and Ooredoo Money, a subsidiary of Ooredoo Fintech, signed a memorandum of understanding at Web Summit Qatar 2025 to collaborate on fintech initiatives. The partnership aims to enhance digital banking services, promote financial inclusion, and accelerate the growth of Qatar's fintech ecosystem through advanced, secure, and innovative solutions.

Qatar Mobile Payments Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Payment Types Covered |

|

|

Applications Covered |

Entertainment, Energy and Utilities, Healthcare, Retail, Hospitality and Transportation, Others |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Mobile Payments Market Report

The Qatar mobile payments market size was valued at USD 6,296.06 Million in 2025.

The Qatar mobile payments market is expected to grow at a compound annual growth rate of 15.72% from 2026-2034 to reach USD 23,419.76 Million by 2034.

Proximity payment, representing the largest revenue share of 55% in 2025, remains the dominant payment type in Qatar's mobile payments market, driven by extensive NFC terminal coverage, QR code standardization efforts, and consumer preference for quick, secure contactless transactions across retail and service establishments.

Key factors driving the Qatar mobile payments market include supportive government initiatives promoting digital transformation, high smartphone penetration and advanced digital infrastructure, rising e-commerce adoption, strategic fintech partnerships, and growing consumer preference for contactless payment methods.

Major challenges include cybersecurity concerns requiring robust fraud prevention measures, limited consumer awareness among certain demographic segments, fragmented QR code standards among small merchants, regulatory compliance complexities, and competition from traditional banking services and cash transaction habits.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)