Qatar Offshore Wind Energy Market Size, Share, Trends and Forecast by Component, Foundation Type, Capacity, Location, and Region, 2026-2034

Qatar Offshore Wind Energy Market Summary:

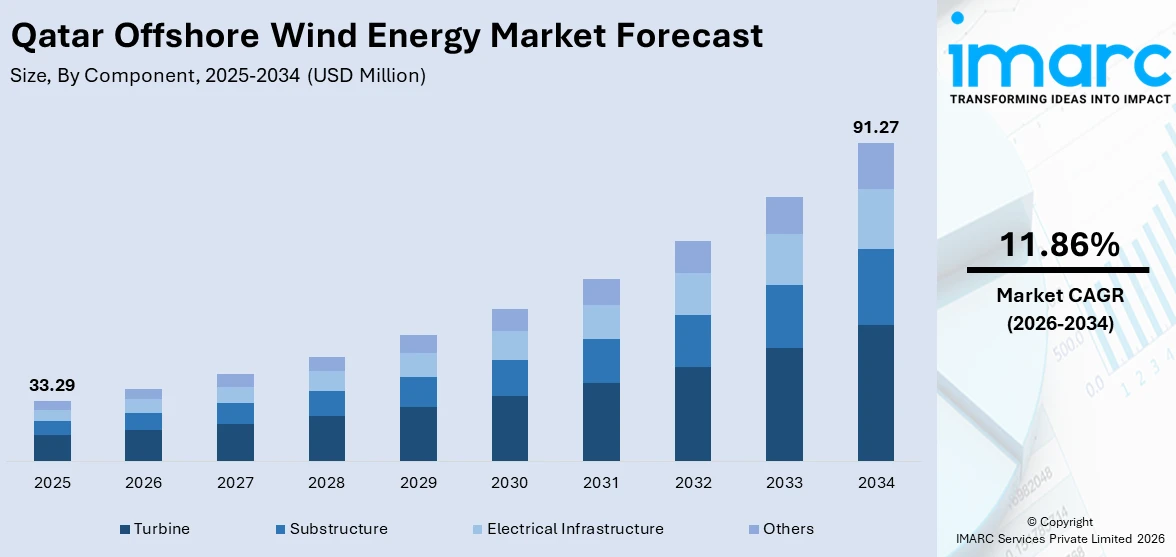

The Qatar offshore wind energy market size was valued at USD 33.29 Million in 2025 and is projected to reach USD 91.27 Million by 2034, growing at a compound annual growth rate of 11.86% from 2026-2034.

The Qatar offshore wind energy market is gaining momentum as the country accelerates its clean energy transition and diversifies beyond hydrocarbon-dependent power generation. The growing government commitment to renewable energy targets, favorable offshore wind conditions along the Arabian Gulf coastline, and advancing turbine technologies are strengthening the foundation for offshore wind development. Strategic investments in grid modernization, emerging green hydrogen integration opportunities, and regional cooperation frameworks are collectively reshaping Qatar's energy landscape, positioning offshore wind as a critical contributor to the nation's long-term sustainability objectives.

Key Takeaways and Insights:

- By Component: Turbine dominates the market with a share of 34% in 2025, owing to high capital intensity, rapid efficiency gains, large rotor adoption, localized assembly prospects, and strong alignment with Qatar’s offshore decarbonization and energy diversification priorities goals.

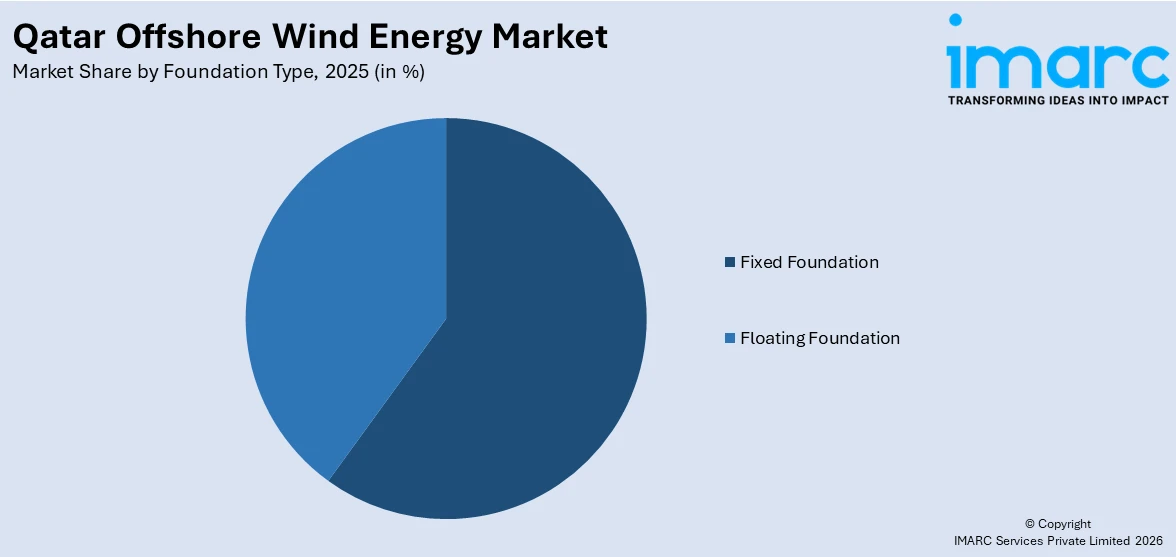

- By Foundation Type: Fixed foundation represents the largest segment with a market share of 60% in 2025, driven by shallow seabed conditions, lower installation complexity, proven engineering designs, cost predictability, and compatibility with Qatar’s nearshore offshore wind development plans.

- By Capacity: Greater than or equal to 5 MW leads the market with a share of 76% in 2025, reflecting the preference for utility scale projects, higher energy yield, efficiency, reduced unit costs, and long-term capacity optimization strategies.

- By Location: Shallow water dominates the market with a share of 51% in 2025, supported by favorable bathymetry, easier access for installation vessels, lower construction risk, faster project timelines, and reduced capital and operational expenditure requirements for offshore developments.

- By Region: Ad Dawhah represents the largest segment with a market share of 40% in 2025, due to strong grid infrastructure, proximity to demand centers, port readiness, policy focus, and concentration of planned offshore renewable energy investments in region.

- Key Players: The Qatar offshore wind energy market features a developing competitive landscape with international turbine manufacturers, engineering firms, and energy developers positioning strategically to capture emerging opportunities as the country advances its offshore wind ambitions.

To get more information on this market Request Sample

The Qatar offshore wind energy market is advancing as the country pursues an ambitious energy diversification agenda aligned with its National Vision 2030 framework. A major catalyst shaping this progress is the government's comprehensive renewable energy strategy, which provides a structured roadmap for scaling clean power generation. In 2024, KAHRAMAA launched the Qatar National Renewable Energy Strategy targeting 4 GW of renewable capacity by 2030, increasing the renewable share of the power mix from 5% to 18%. This strategic initiative encompasses feasibility studies for wind energy projects alongside large-scale solar deployments, creating a supportive policy environment for offshore wind development. The convergence of national decarbonization imperatives, declining offshore wind technology costs, and Qatar's strategic positioning along the Arabian Gulf coastline is establishing a robust foundation for sustained offshore wind market expansion. The growing interest in hybrid renewable-hydrogen energy systems further amplifies long-term investment potential throughout the forecast period.

Qatar Offshore Wind Energy Market Trends:

Decarbonization and Climate Commitments

International climate commitments and domestic emissions reduction targets are increasingly shaping Qatar’s energy planning across sectors, strengthening the role of offshore wind as a low carbon power option. Offshore wind supports electricity demand growth while reducing lifecycle emissions, aligning environmental objectives with industrial policy needs. This shift is reflected in private sector initiatives, including Ooredoo Qatar’s 2024 “Clean Energy – Super Hybrid” program, which integrated solar with renewable backup sources such as wind and was expected to save around 140 tons of CO2 per site over 25 years. Such efforts reinforce regulatory acceptance, policy consistency, and long-term demand visibility for cleaner electricity, improving the investment outlook for offshore wind projects.

Rising Domestic Power Demand

Sustained growth in electricity usage driven by urban development, industrial expansion, and intensive cooling requirements is catalyzing the demand for additional power generation capacity in Qatar. Offshore wind supports future demand growth without increasing reliance on gas fired generation, while complementing existing power system planning and enhancing long term supply security. This demand pressure is underscored by the 2024 Qatar energy report, which indicates total energy usage per capita exceeding 20 toe and electricity employment of 20.7 MWh, both ranking second globally. Such high usage levels strengthen the case for diversifying generation sources, supporting early offshore wind investments, phased capacity additions, and proactive grid integration planning.

Access to Capital and State Backing

Qatar’s strong fiscal position and access to long term capital play a critical role in advancing offshore wind prospects and supporting large scale renewable investments. State backed entities and sovereign investment capacity significantly reduce the financing constraints typically associated with capital intensive offshore projects. This financial strength enables early-stage development, effective risk absorption, and the availability of patient capital structures aligned with offshore wind economics. The participation of government linked investors also enhances lender confidence, improving access to favorable financing terms. With stable funding availability, project developers can prioritize technical optimization, efficient execution, and timely delivery rather than being constrained by short term financial pressures.

Market Outlook 2026-2034:

The Qatar offshore wind energy market is positioned for sustained growth throughout the forecast period, underpinned by strengthening policy frameworks and advancing technology readiness. Increasing government investment in offshore infrastructure and the growing integration with green hydrogen initiatives are expected to drive higher revenue streams and accelerate Qatar's sustainable energy transition. The market generated a revenue of USD 33.29 Million in 2025 and is projected to reach a revenue of USD 91.27 Million by 2034, growing at a compound annual growth rate of 11.86% from 2026-2034.

Qatar Offshore Wind Energy Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Component |

Turbine |

34% |

|

Foundation Type |

Fixed Foundation |

60% |

|

Capacity |

Greater Than or Equal to 5 MW |

76% |

|

Location |

Shallow Water |

51% |

|

Region |

Ad Dawhah |

40% |

Component Insights:

- Turbine

- Substructure

- Electrical Infrastructure

- Others

Turbine dominates with a market share of 34% of the total Qatar offshore wind energy market in 2025.

Turbine represents the largest segment due to its high share of total project cost and direct impact on power generation efficiency. Large scale offshore turbine is central to converting wind resources into usable electricity, making it the most value intensive component. Advancements in blade design, rotor diameter, and generator technology improve output under moderate wind conditions typical of the region. Project developers prioritize turbine performance and reliability to maximize capacity factors, reduce downtime, and ensure long term returns on offshore wind investments.

The dominance of the turbine segment is further reinforced by the growing number of projects planned and the emphasis on large utility scale installations. Offshore developments typically require fewer but highly specialized turbines, which increases the per unit value contribution and strengthens procurement demand. This trend is supported by the growing supplier engagement, as seen in 2026 when TESUP expanded into Qatar through the launch of an official local website, enabling direct access to renewable energy products, including wind turbines. By positioning wind turbines as scalable solutions for businesses and sustainability needs, such developments further raise spending on advanced turbine technologies.

Foundation Type Insights:

Access the comprehensive market breakdown Request Sample

- Fixed Foundation

- Floating Foundation

Fixed foundation leads with a market share of 60% of the total Qatar offshore wind energy market in 2025.

Fixed foundation dominates the market owing to favorable seabed conditions and relatively shallow offshore waters. Large areas along Qatar’s coastline support monopile and jacket foundation, which is proven, cost effective, and widely deployed in global offshore wind projects. This foundation offers structural stability, lower engineering complexity, and predictable installation timelines. Developers favor fixed foundation because of established supply chains, reduced construction risk, and compatibility with conventional installation vessels. Its reliability supports early-stage market development and helps limit capital costs during initial offshore wind deployment.

The dominance of fixed foundation is further reinforced by Qatar’s focus on nearshore offshore wind sites to optimize project feasibility. Shorter distances from shore reduce installation, operation, and maintenance costs, making fixed structure more economical than floating alternatives. Fixed foundation also allows easier integration with existing grid infrastructure and marine logistics. Regulatory clarity and environmental assessment processes favor well understood foundation technologies. Combined with regional experience from oil and gas offshore structures, fixed foundation aligns well with local engineering capabilities, reinforcing their leading position in the market.

Capacity Insights:

- Less Than 5 MW

- Greater Than or Equal to 5 MW

Greater than or equal to 5 MW exhibits a clear dominance with a 76% share of the total Qatar offshore wind energy market in 2025.

Greater than or equal to 5 MW holds the biggest share, driven by the focus on maximizing power output from a limited number of offshore installations. Larger capacity turbines deliver higher energy generation per unit, improving project economics and reducing the number of foundations and cables required. This approach lowers installation and maintenance costs on a per megawatt basis. Utility scale projects favor higher rated turbines to achieve commercial viability and meet national renewable energy targets, making large capacity installations the preferred choice for planned offshore developments.

Adoption of turbines with capacities of 5 MW or higher is also supported by advances in offshore wind technology and supplier readiness. Proven turbine platforms offer improved reliability, longer service intervals, and better performance under varying wind conditions. Larger units align with grid integration strategies by delivering stable power output. International developers bring experience from mature offshore markets where high-capacity turbines are standard. These factors, combined with Qatar’s emphasis on efficient clean energy expansion, reinforce the dominance of the segment in the market.

Location Insights:

- Shallow Water

- Transitional Water

- Deep Water

Shallow water dominates with a market share of 51% of the total Qatar offshore wind energy market in 2025.

Shallow water leads the market because of favorable coastal bathymetry and accessible nearshore zones. Large stretches of shallow water allow simpler foundation design, lower installation complexity, and reduced project costs. Developers benefit from easier transport of equipment, shorter installation timelines, and safer working conditions. Shallow site supports use of conventional fixed foundations, which is well established and widely available. Proximity to shore also simplifies grid connection and maintenance activities, making shallow water attractive for early-stage offshore wind development in Qatar.

Dominance of shallow water is further supported by environmental and regulatory considerations. Nearshore project allows better monitoring, controlled marine impact, and streamlined permitting processes. Lower water depths reduce reliance on specialized vessels, lowering capital and operational expenditure. Shallow site also aligns with Qatar’s infrastructure planning, enabling integration with existing ports and logistics facilities. Experience gained from offshore oil and gas operations in similar water depths strengthens technical confidence. These advantages collectively position shallow water as the primary focus for offshore wind projects within Qatar’s emerging renewable energy market.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah leads with a market share of 40% of the total Qatar offshore wind energy market in 2025.

Ad Dawhah account for the majority of the market share attributed to its strong infrastructure base, energy demand concentration, and strategic coastal positioning. The region hosts key government institutions, utilities, and major urban centers that drive electricity usage and renewable energy planning. Proximity to ports, grid infrastructure, and industrial facilities supports efficient project development and power evacuation. Ad Dawhah also benefits from advanced regulatory oversight and planning capabilities, enabling smoother project coordination. These advantages make the region a focal point for early offshore wind initiatives and pilot scale developments.

Regional dominance is reinforced by established maritime logistics, a skilled workforce, and experienced service providers concentrated in Ad Dawhah. Engineering expertise developed through the oil and gas sector supports offshore construction efficiency and reliable operations. The coastal waters near the capital offer favorable conditions for nearshore wind installations, lowering technical and development risks. This leadership is further supported by continued offshore investment activity, including in 2025, when QatarEnergy LNG launched the next expansion phase of its USD 5 billion North Field Production Sustainability offshore project, reflecting strong capital commitment. Government backed diversification priorities and proximity to major demand hubs strengthen Ad Dawhah’s position as Qatar’s leading offshore wind market.

Market Dynamics:

Growth Drivers:

Why is the Qatar Offshore Wind Energy Market Growing?

National Energy Diversification Objectives

The Qatar offshore wind energy market growth is driven by the national objective to broaden the energy base beyond hydrocarbons while maintaining long term economic stability. Policy direction emphasizes reduced exposure to fossil fuel price cycles and stronger alignment with global energy transition trends. Offshore wind fits this direction due to its scalability and compatibility with existing energy infrastructure planning. Furthermore, government level commitment to cleaner energy sources supports early-stage market development through strategic vision, planning clarity, and institutional backing. These factors collectively improve confidence for long duration capital deployment and encourage structured progress toward utility scale offshore wind adoption.

Grid Modernization and System Integration Planning

Offshore wind development in Qatar is reinforced by the need to strengthen grid resilience and improve long term system flexibility as renewable capacity increases. The integration of variable power sources drives investment in transmission upgrades, digital monitoring, and advanced dispatch mechanisms that support stable system operations. This direction is evident in Qatar’s broader grid readiness efforts, including the 2025 power purchase agreement between KAHRAMAA and QEWC for peak generation units at the Ras Abu Fontas Plant, which will add 511 MW of capacity at an estimated cost of 1.6 billion Qatari Riyals with operations expected in January 2027. Such initiatives create a more adaptive power network, supporting offshore wind integration and sustained market growth.

Technology Cost Improvements and Operational Efficiency Gains

Advancements in offshore wind turbine design, modern installation techniques, and improved operations management are steadily lowering cost barriers and enhancing project feasibility. The deployment of larger, more efficient turbines, higher capacity factors, and advanced maintenance strategies is strengthening overall project economics and boosting long term competitiveness. Qatar stands to benefit from entering the offshore wind sector at a time when global technology maturity is well established, helping reduce early-stage development risks. Greater operational reliability and more predictable generation output are also building confidence among stakeholders, supporting offshore wind’s role in Qatar’s future energy capacity planning.

Market Restraints:

What Challenges the Qatar Offshore Wind Energy Market is Facing?

High Initial Capital Investment Requirements

Offshore wind projects demand substantial upfront capital for turbine procurement, foundation installation, subsea cable networks, and grid integration infrastructure. Limited local manufacturing capacity and dependency on imported specialized equipment increase project costs. Establishing offshore infrastructure in Qatar's challenging marine environment, characterized by high temperatures and elevated salinity, requires additional engineering adaptations that further elevate capital expenditure requirements.

Limited Offshore Wind Resource Assessment Data

Qatar's offshore wind energy potential remains comparatively under-studied relative to its well-documented solar resources. Historical wind assessments have relied on relatively short measurement campaigns that lack comprehensive long-term variability analysis. Moderate average offshore wind speeds present lower capacity factors compared to leading global offshore wind markets, creating uncertainty around project economics and energy yield projections.

Nascent Regulatory Framework for Offshore Wind Development

The regulatory environment for offshore wind energy in Qatar remains in early development stages compared to the more established frameworks governing solar energy projects. Specific offshore wind permitting processes, environmental impact assessment protocols, marine spatial planning guidelines, and grid interconnection standards require further formalization. Skilled workforce shortages for specialized offshore installation and maintenance operations present additional operational challenges.

Competitive Landscape:

The Qatar offshore wind energy market features a developing competitive landscape characterized by international energy companies and turbine manufacturers positioning strategically to capture emerging opportunities. Market dynamics reflect a transitional phase as the country moves from feasibility assessments toward commercial-scale project planning. Competition is shaped by technology leadership, regional project experience, and capabilities in adapting offshore wind solutions to Gulf environmental conditions. Strategic partnerships between international developers and local energy entities are increasingly defining competitive positioning, with emphasis on technology transfer, local content development, and integrated renewable energy solutions spanning wind, solar, and hydrogen production.

Recent Developments:

- October 2025: Offshore Oil Engineering Co. (COOEC) officially launched the USD 4 Billion Qatar BH EPIC offshore energy project developed by QatarEnergy. The project was located in the Bul Hanine oilfield and represents the largest international offshore EPC contract ever awarded to a Chinese company. The development includes dozens of offshore facilities and subsea pipelines, strengthening China–Qatar energy cooperation under the Belt and Road Initiative.

Qatar Offshore Wind Energy Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Turbine, Substructure, Electrical Infrastructure, Others |

| Foundation Types Covered | Fixed Foundation, Floating Foundation |

| Capacities Covered | Less Than 5 MW, Greater than or Equal to 5 MW |

| Locations Covered | Shallow Water, Transitional Water, Deep Water |

| Regions Covered | Ad Dawhah, Al Rayyan, Al Wakrah, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Offshore Wind Energy Market Report

The Qatar offshore wind energy market size was valued at USD 33.29 Million in 2025.

The Qatar offshore wind energy market is expected to grow at a compound annual growth rate of 11.86% from 2026-2034 to reach USD 91.27 Million by 2034.

Turbine, holding the largest revenue share of 34% in the 2025, because of high capital intensity, rapid efficiency gains, large rotor adoption, localized assembly prospects, and strong alignment with Qatar’s offshore decarbonization and energy diversification priorities goals.

Key factors driving the Qatar offshore wind energy market include international climate commitments and domestic emissions reduction targets, which support offshore wind as a low carbon solution. Private initiatives such as Ooredoo Qatar’s 2024 “Clean Energy – Super Hybrid” program, saving about 140 tons of CO2 per site over 25 years, further reinforce demand for cleaner electricity.

Major challenges include high initial capital investment requirements, limited offshore wind resource assessment data, nascent regulatory frameworks for offshore-specific permitting, moderate average wind speeds compared to global hotspots, dependency on imported equipment, and skilled workforce shortages for specialized offshore operations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)