Qatar Power Transmission and Distribution Market Size, Share, Trends and Forecast by Asset Type, End Use, and Region, 2026-2034

Qatar Power Transmission and Distribution Market Summary:

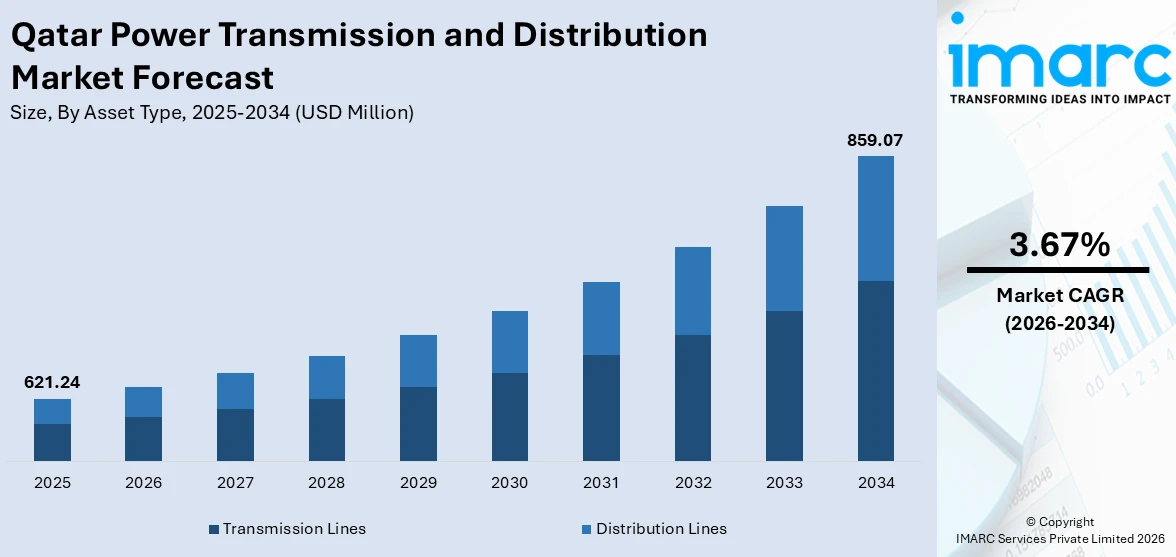

The Qatar power transmission and distribution market size was valued at USD 621.24 Million in 2025 and is projected to reach USD 859.07 Million by 2034, growing at a compound annual growth rate of 3.67% from 2026-2034.

The Qatar power transmission and distribution market is expanding steadily, as the nation undertakes large-scale infrastructure modernization and capacity enhancement programs. Driven by surging electricity consumption, ambitious renewable energy integration targets, and accelerating urban development, demand for transmission lines, substations, and distribution networks is intensifying. The government’s commitment to grid digitization, smart metering deployment, and energy security under Qatar National Vision 2030 is further strengthening the market share.

Key Takeaways and Insights:

- By Asset Type: Transmission lines dominate the market with a share of 53.6% in 2025, owing to extensive high-voltage network expansion programs, new substation construction, and strategic investments in underground cabling to support growing electricity demand and renewable energy evacuation across Qatar.

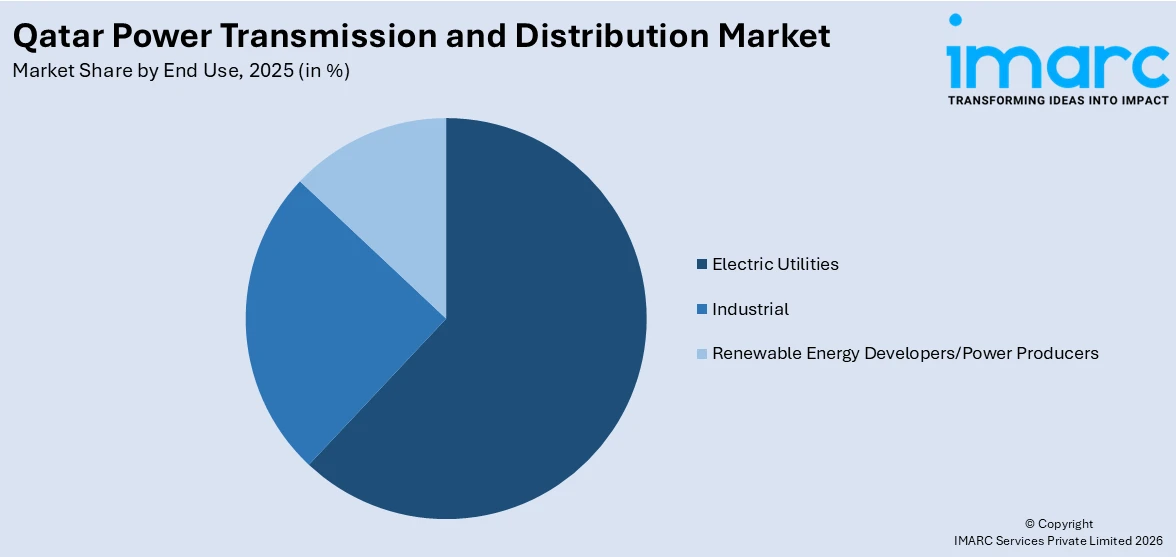

- By End Use: Electric utilities lead the market with a share of 61.9% in 2025, driven by Kahramaa’s position as the sole transmission and distribution system owner and operator, continuous grid modernization, and substantial capital expenditure on high-voltage substations and cable infrastructure.

- By Region: Ad Dawhah represents the largest region with 59.8% share in 2025, driven by the concentration of administrative, commercial, and residential infrastructure in the capital region, necessitating continuous grid reinforcement, substation upgrades, and distribution network expansion.

- Key Players: Key players drive the Qatar power transmission and distribution market by delivering advanced substation solutions, high-voltage cable systems, and smart grid technologies. Their investments in localized manufacturing, engineering partnerships, and digital monitoring capabilities strengthen grid reliability and accelerate infrastructure deployment across the country.

To get more information on this market Request Sample

The Qatar power transmission and distribution market is advancing, as the nation invests heavily in grid modernization, capacity expansion, and renewable energy integration. A key driver underpinning this progress is Qatar’s rapidly growing electricity consumption, which expanded at a rate of 6.5% per year since 2020, reaching 56 TWh in 2024, fueled by rising air conditioning demand and the expanding water desalination industry. The integration of large-scale solar projects necessitates significant transmission infrastructure upgrades. Additionally, ongoing industrial expansion is further amplifying the need for robust power evacuation and distribution systems across the country. Smart metering, grid automation, and GCC interconnection enhancements continue to support sustainable market advancement. Government-led energy efficiency initiatives and long-term national development plans are also reinforcing sustained investments in advanced grid infrastructure.

Qatar Power Transmission and Distribution Market Trends:

Accelerated Smart Grid and Digital Infrastructure Deployment

Qatar is rapidly transforming its power grid through advanced digitization and smart metering technologies. By mid-2025, over 528,000 smart electricity meters and 460,000 smart water meters were deployed throughout Qatar, based on information shared by Kahramaa. The rollout is part of a larger plan to substitute all traditional utility meters with modern digital systems in each Qatari home and business. These digital systems enable real-time consumption monitoring, automated billing, and predictive demand management.

Renewable Energy Integration Driving Transmission Upgrades

The large-scale deployment of solar power capacity is creating substantial demand for new transmission infrastructure across Qatar. In September 2025, Samsung C&T Engineering & Construction (E&C) Group obtained Qatar's largest solar energy project, representing the highest capacity solar undertaking ever carried out by a Korean construction firm. The 2,000MW power plant, valued at KRW 1.46 Trillion, would be constructed at a location in Dukhan, featuring 2.74 Million solar panels, and is set to provide electricity to 750,000 homes by 2030. This mega project, along with existing and upcoming solar facilities, is accelerating investments in high-voltage evacuation infrastructure, grid balancing systems, and substation modernization to accommodate intermittent renewable generation.

Expansion of Regional Grid Interconnection

Qatar is strengthening its cross-border electricity exchange capabilities through the GCC Electrical Interconnection Project. The transmission line connecting Qatar to the GCC network has a capacity of 1,200 MW, enabling power trading with neighboring countries during peak demand periods. Efforts are underway to expand interconnection capacity with additional member states and extend the grid into Iraq and Oman. These regional linkages enhance energy security, reduce the need for excessive domestic reserve capacity, and improve overall grid resilience.

Market Outlook 2026-2034:

The Qatar power transmission and distribution market is positioned for sustained growth, supported by ongoing infrastructure modernization, expanding power generation capacity, and renewable energy integration initiatives. The market generated a revenue of USD 621.24 Million in 2025 and is projected to reach a revenue of USD 859.07 Million by 2034, growing at a compound annual growth rate of 3.67% from 2026-2034. The construction of new high-voltage substations, extensive underground cable networks, and advanced grid management systems are creating significant investment opportunities across the transmission and distribution value chain. The ongoing deployment of smart metering systems, grid automation platforms, and digital monitoring infrastructure will further enhance operational efficiency and support long-term market expansion across the forecast period.

Qatar Power Transmission and Distribution Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Asset Type |

Transmission Lines |

53.6% |

|

End Use |

Electric Utilities |

61.9% |

|

Region |

Ad Dawhah |

59.8% |

Asset Type Insights:

- Transmission Lines

- Distribution Lines

Transmission lines dominate with a market share of 53.6% of the total Qatar power transmission and distribution market in 2025.

Transmission lines dominate the Qatar power transmission and distribution market, due to the country’s centralized power generation structure and rapidly rising electricity demand. Qatar relies on large, gas-fired power plants and utility-scale renewable projects located away from major load centers. This requires extensive high-voltage transmission networks to evacuate bulk power efficiently over long distances while minimizing technical losses. As electricity consumption continues to grow due to population expansion, cooling demand, and desalination activity, investments in high-capacity overhead and underground transmission lines remain a priority.

Qatar's emphasis on regional power integration, redundancy, and grid dependability is another important element propelling transmission lines dominance. Transmission lines are essential for maintaining grid stability during times of high demand and guaranteeing a steady supply of electricity to urban areas and energy-intensive industrial zones. The demand for new transmission corridors and grid strengthening is further increased by the ongoing integration of renewable energy, especially large-scale solar installations. Furthermore, strong transmission infrastructure is essential to interconnection projects with GCC power networks, enhancing this segment's long-term dominance.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Electric Utilities

- Industrial

- Renewable Energy Developers/Power Producers

Electric utilities lead with a share of 61.9% of the total Qatar power transmission and distribution market in 2025.

Electric utilities command the largest share, driven primarily by Kahramaa’s role as the sole transmission and distribution system owner and operator in Qatar. Kahramaa manages the entire national grid infrastructure, from high-voltage transmission to last-mile distribution, and is responsible for all capital expenditure on grid expansion and modernization. In November 2025, Kahramaa launched the Umm Al Houl 3 primary substation, a 132/11 kV facility with a total capacity of 80 MVA, to supply electricity to Qatar Free Zones Authority and support the growing energy demands of industrial investors.

Electric utilities continue to dominate due to their central role in implementing national energy strategies and ensuring long-term supply reliability. Large-scale expenditures in transmission corridors, substations, and smart grid technologies are mostly utility-led, indicative of the sector's capital-intensive character. Along with regulating the growth of peak loads and preserving system resilience, utilities are also in charge of integrating renewable energy potential. Their dominant position in the Qatar power transmission and distribution industry is further cemented by their ability to design network upgrades at the national level.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah exhibits a clear dominance with a 59.8% share of the total Qatar power transmission and distribution market in 2025.

Ad Dawhah, encompassing Qatar’s capital city Doha and its surrounding areas, commands the largest share of the power transmission and distribution market due to the concentration of government institutions, commercial establishments, and high-density residential developments. The capital region hosts the majority of Qatar’s super substations and high-voltage distribution infrastructure, serving critical loads across diplomatic zones, business districts, and rapidly expanding urban corridors. The ongoing development of major projects, such as Lusail City, Msheireb Downtown Doha, and expanding free trade zones, continues to drive demand for new substations, distribution lines, and grid reinforcement in the Ad Dawhah region.

Reliability, redundancy, and smart grid deployment are given top priority in the region's grid upgrades in order to serve large-scale mixed-use developments, transportation systems, and mission-critical facilities. Advanced distribution networks and underground cabling are being deployed more quickly due to the increased demand for energy from public infrastructure, commercial towers, and hospitality projects. All of these elements work together to establish Ad Dawhah as the hub for ongoing transmission and distribution expenditures in Qatar.

Market Dynamics:

Growth Drivers:

Why is the Qatar Power Transmission and Distribution Market Growing?

Surging Electricity Demand and Generation Capacity Expansion

Qatar’s electricity consumption has been growing rapidly, driven by population expansion, industrial development, and increasing cooling and desalination requirements. The country’s expanding power generation portfolio necessitates proportional growth in transmission and distribution infrastructure to deliver electricity from generation sources to end-users. New generation projects are further intensifying the need for transmission infrastructure. In May 2025, Kahramaa signed a strategic agreement for the development of the Ras Abu Fontas Power and Water Facility, with a production capacity of 2400 MW and 110 Million gallons per day, at a total cost of 13.5 Billion Qatari Riyals. This facility alone is expected to provide approximately 23% of Qatar’s total power output, requiring substantial transmission network expansion to integrate this capacity into the national grid. The continued deployment of combined-cycle gas turbine plants and independent water and power projects is reinforcing the need for upgraded and expanded high-voltage networks across the country.

Ambitious Renewable Energy Targets Necessitating Grid Upgrades

Qatar’s pursuit of renewable energy diversification is creating significant demand for new transmission and distribution infrastructure. The country aims to achieve 4 GW of new renewable energy capacity by 2030 through multiple large-scale projects, each requiring dedicated grid connection and power evacuation systems. The integration of utility-scale solar plants into the national grid requires upgrades to high-voltage transmission lines, substations, and grid balancing systems to manage variability in power generation. Existing infrastructure, originally designed for centralized gas-fired power plants, must be reinforced to accommodate bidirectional power flows and intermittent renewable output. As a result, investments in grid flexibility, advanced protection systems, and real-time monitoring technologies are accelerating, strengthening long-term demand for transmission and distribution upgrades across the country.

Industrial Expansion and Infrastructure-Led Economic Development

Rapid industrial growth and infrastructure-led economic development are further strengthening demand for power transmission and distribution infrastructure in Qatar. The expansion of energy-intensive industries, logistics hubs, free zones, and manufacturing clusters is increasing the need for reliable, high-capacity power supply networks. Large industrial consumers require dedicated substations, redundant transmission lines, and robust distribution systems to ensure uninterrupted operations. Ongoing investments in ports, metro systems, commercial real estate, and public infrastructure are also adding to electricity load growth, particularly in urban and industrial corridors. To support these developments, utilities are expanding high-voltage transmission networks and reinforcing distribution systems near industrial zones and economic clusters. Additionally, long-term national development strategies emphasize economic diversification beyond hydrocarbons, which further accelerates infrastructure construction and power demand. These factors collectively position industrial expansion as a key structural driver of sustained growth in the Qatar power transmission and distribution market.

Market Restraints:

What Challenges the Qatar Power Transmission and Distribution Market is Facing?

State Monopoly Limiting Private Sector Investment in Transmission and Distribution

The transmission and distribution sector in Qatar is entirely owned and operated by Kahramaa, with no private investment permitted in grid infrastructure. While this ensures centralized planning and consistent standards, it restricts the entry of private capital and innovative business models that could accelerate grid expansion and modernization. The absence of competitive market dynamics may limit cost optimization opportunities and slow the adoption of emerging technologies in grid management.

Extreme Climatic Conditions Increasing Infrastructure Maintenance Requirements

Qatar’s harsh desert climate, characterized by extreme summer temperatures exceeding 50 degrees Celsius, heavy dust accumulation, and high humidity levels, poses significant challenges for outdoor transmission and distribution equipment. These conditions accelerate the degradation of transformers, cables, switchgear, and overhead line components, increasing maintenance costs and requiring specialized equipment designed to withstand severe thermal stress. Underground cable installations, while preferred for aesthetic and reliability reasons, face additional challenges related to soil conditions and thermal dissipation in the arid environment.

Dependence on Imported Equipment and Technology

Qatar relies almost entirely on imported technologies and equipment for its power transmission and distribution infrastructure, as the country lacks significant domestic manufacturing capabilities for high-voltage components. This dependency creates supply chain vulnerabilities, extends procurement timelines, and exposes the market to global logistics disruptions and price fluctuations. While local partnerships and joint ventures are being encouraged, the specialized nature of transmission equipment manufacturing continues to necessitate reliance on international suppliers for critical grid components.

Competitive Landscape:

The Qatar power transmission and distribution market operates within a framework where Kahramaa serves as the sole system owner and operator, with international engineering and manufacturing firms competing for contracts across multiple phases of the national grid expansion program. Competition is driven by technological capabilities, project execution track records, and the ability to deliver turnkey solutions that meet stringent quality and timeline requirements. Companies are differentiating through localized manufacturing partnerships, advanced digital grid solutions, and comprehensive after-sales support capabilities. Strategic joint ventures with Qatari entities are becoming increasingly important as Kahramaa prioritizes local content and capacity building.

Qatar Power Transmission and Distribution Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Asset Types Covered |

Transmission Lines, Distribution Lines |

|

End Uses Covered |

Electric Utilities, Industrial, Renewable Energy Developers/Power Producers |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Power Transmission and Distribution Market Report

The Qatar power transmission and distribution market size was valued at USD 621.24 Million in 2025.

The Qatar power transmission and distribution market is expected to grow at a compound annual growth rate of 3.67% from 2026-2034 to reach USD 859.07 Million by 2034.

Transmission lines dominated the market with a share of 53.6%, driven by extensive high-voltage network expansion programs, new substation construction, and strategic underground cabling investments to support growing electricity demand and renewable energy integration.

Key factors driving the Qatar power transmission and distribution market include surging electricity consumption, ambitious renewable energy integration targets, government-led infrastructure modernization under Qatar National Vision 2030, and large-scale generation capacity additions requiring grid expansion.

Major challenges include state monopoly restricting private investment in grid infrastructure, extreme climatic conditions increasing equipment maintenance requirements, dependence on imported transmission equipment, supply chain vulnerabilities, and the technical complexity of integrating intermittent renewable energy sources.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)