Qatar Shipping Port Market Size, Share, Trends and Forecast by Cargo Type, Port Type, Ownership, Service, Application, and Region, 2026-2034

Qatar Shipping Port Market Summary:

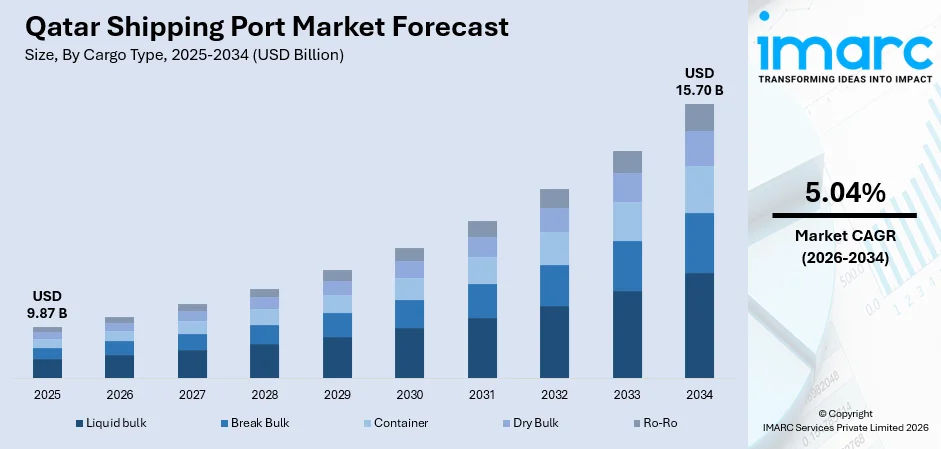

The Qatar shipping port market size was valued at USD 9.87 Billion in 2025 and is projected to reach USD 15.70 Billion by 2034, growing at a compound annual growth rate of 5.04% from 2026-2034.

Qatar’s market is experiencing robust expansion, underpinned by the country’s strategic position along major east-west maritime trade corridors and its ambitious economic diversification agenda under Qatar National Vision 2030. The development of world-class port infrastructure, led by the flagship Hamad Port, has transformed the nation into a prominent regional logistics and transshipment hub. Sustained government investments in port modernization, digital transformation of maritime operations, and the establishment of free economic zones adjacent to port facilities are collectively expanding the Qatar shipping port market.

Key Takeaways and Insights:

- By Cargo Type: Liquid bulk dominates the market with a share of 52.6% in 2025, driven by the country’s position as one of the world’s leading LNG exporters and significant volumes of petroleum product shipments through specialized terminals.

- By Port Type: Artificial leads the market with a share of 88.4% in 2025, reflecting Qatar’s strategic investment in purpose-built deep-water port facilities, primarily Hamad Port, designed to accommodate large-capacity vessels and support diverse cargo handling operations.

- By Ownership: Public represents the largest segment with a market share of 71.3% in 2025, as Qatar’s primary port assets are operated under government-owned entities such as Mwani Qatar and state-affiliated terminal operators aligned with national development objectives.

- By Service: Cargo handling leads the service segment with a share of 47.9% in 2025, supported by advanced automated systems, high-capacity crane infrastructure, and expanding container and bulk cargo throughput volumes at the nation’s key commercial ports.

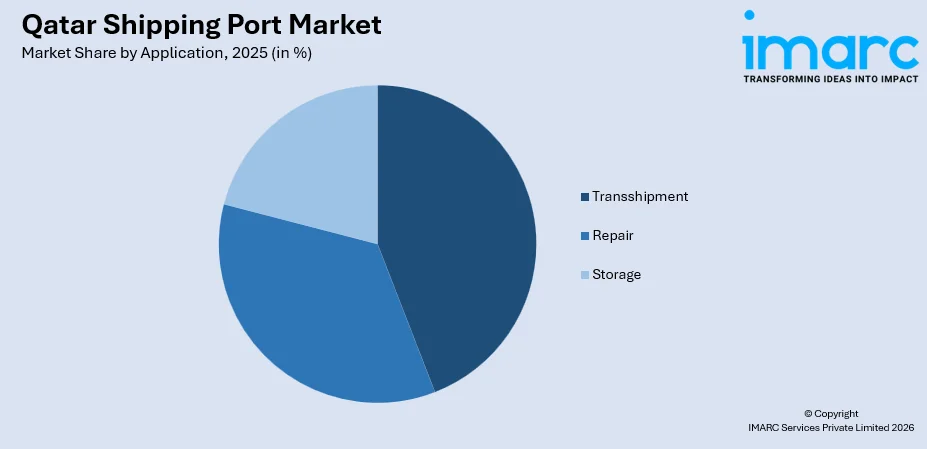

- By Application: Transshipment represents the largest application segment with a share of 44.2% in 2025, reflecting Hamad Port’s growing role as a regional redistribution center, with transshipment volumes accounting for nearly half of total container throughput.

- By Region: Ad Dawhah dominates the regional landscape with a share of 63.7% in 2025, owing to the concentration of Qatar’s principal commercial port infrastructure, logistics zones, and trade facilitation services within and around the capital city.

- Key Players: The Qatar shipping port market features a concentrated competitive landscape characterized by the strong presence of state-backed operators. Key entities are supported by international shipping line partnerships and terminal concession agreements.

To get more information on this market Request Sample

Qatar’s shipping port sector is being shaped by a convergence of infrastructure modernization, expanding trade connectivity, and the country’s strategic positioning as a maritime gateway linking Asian, European, and African markets. The completion of the Hamad Port expansion has enabled the port to connect with over 100 maritime destinations worldwide through 30 direct shipping lines, significantly enhancing Qatar’s capacity to handle containerized, bulk, and specialized cargo. Qatar ports (Hamad, Ruwais, and Doha) experienced a strong increase in December last year, with cargo and container volumes processed during this period showing an annual rise compared to the same time in 2024. The port’s operational excellence was recognized in the 2024 Container Port Performance Index (CPPI) published by the World Bank and S&P Global, which ranked Hamad Port first in the Gulf and eleventh globally. Additionally, the establishment of the Umm Alhoul Free Zone adjacent to Hamad Port in 2025, along with the development of the Marsa maritime cluster, is creating an integrated logistics ecosystem that attracts international freight forwarders, manufacturing firms, and maritime service providers to Qatar’s port network.

Qatar Shipping Port Market Trends:

Rising Transshipment Volumes Reinforcing Qatar’s Regional Hub Status

Qatar’s ports are witnessing a transformative surge in transshipment activity, with cargo redistribution volumes growing substantially as international shipping lines expand their service networks through Hamad Port. Mwani Qatar stated that transshipment activity accounted for nearly 50 percent of total container volumes handled between January and November 2025, underscoring the port’s rapid evolution from a primarily national import-export gateway to a strategic regional redistribution center serving the broader Gulf Cooperation Council and South Asian markets.

Digital Transformation and Smart Port Technologies Enhancing Operational Efficiency

Qatar is accelerating the integration of advanced digital systems into its port operations, with the deployment of the MWANINA Port Community System enabling seamless electronic coordination among exporters, importers, shipping lines, and freight agents. Launched initially as an online platform in November 2022 and subsequently expanded with a mobile application in 2024, the system now supports over 25 digital services and is utilized by 51 shipping lines, 800 freight agents, and 659 transport firms, streamlining vessel berthing, shipment tracking, and electronic payment processes across Qatar’s port network.

Expansion of Free Zones and Integrated Logistics Ecosystems Near Port Facilities

The development of specialized free economic zones adjacent to Qatar’s port infrastructure is attracting significant foreign direct investment in logistics and maritime services. In September 2025, FedEx Logistics inaugurated a new regional logistics facility at Ras Bufontas Free Zone, integrating warehousing and freight forwarding capabilities connected to Hamad Port and Hamad International Airport. The Umm Alhoul Free Zone, located directly beside Hamad Port, continues to grow as a hub for marine industries, heavy manufacturing, and supply chain operations.

Market Outlook 2026-2034:

The Qatar shipping port market is poised for sustained and accelerating expansion over the forecast period, underpinned by a convergence of transformative infrastructure investments, massive hydrocarbon export capacity additions, and the strategic deepening of Qatar’s role as a regional maritime logistics hub. The market generated a revenue of USD 9.87 Billion in 2025 and is projected to reach a revenue of USD 15.70 Billion by 2034, growing at a compound annual growth rate of 5.04% from 2026-2034. The government’s ongoing commitment to expanding free zone ecosystems, enhancing digital port management platforms, and attracting international logistics operators to Qatar’s port-adjacent economic zones is expected to further diversify the market’s revenue base beyond traditional port operations. Additionally, the planned development of the Hamad Port North Logistics Area and the continued maturation of the Marsa maritime cluster within Umm Alhoul Free Zone will create new capacity for ship repair, maritime services, and value-added logistics activities.

Qatar Shipping Port Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Cargo Type |

Liquid Bulk |

52.6% |

|

Port Type |

Artificial |

88.4% |

|

Ownership |

Public |

71.3% |

|

Service |

Cargo Handling |

47.9% |

|

Application |

Transshipment |

44.2% |

|

Region |

Ad Dawhah |

63.7% |

Cargo Type Insights:

- Break Bulk

- Container

- Dry Bulk

- Liquid Bulk

- Ro-Ro

Liquid bulk dominates with a market share of 52.6% of the total Qatar shipping port market in 2025.

Liquid bulk is the leading cargo segment in the Qatar shipping port market, driven largely by the country’s position as one of the world’s top exporters of liquefied natural gas. Ports such as Hamad Port handle substantial volumes of LNG, LPG, condensates, refined petroleum products, and chemicals. This steady flow of energy exports forms the backbone of port activity and revenue. Qatar’s economy is closely tied to hydrocarbons, and liquid bulk movements reflect long term supply contracts with key markets in Asia and Europe.

Dedicated LNG terminals, specialized storage tanks, and advanced loading systems allow for efficient handling of high volumes while meeting strict safety and environmental standards. Continuous investments in port infrastructure and fleet expansion have strengthened capacity and reliability. In addition to exports, liquid bulk imports also play a role. Refined fuels, industrial chemicals, and other petroleum derivatives support domestic industries, power generation, and construction projects. The integration of port facilities with industrial zones further supports smooth cargo flow. With ongoing LNG expansion projects and rising global energy demand, liquid bulk is expected to remain the dominant cargo category in Qatar’s port sector, reinforcing the country’s strategic importance in global energy trade.

Port Type Insights:

- Artificial

- Natural

Artificial leads with a share of 88.4% of the total Qatar shipping port market in 2025.

Artificial ports account for the largest share of the Qatar shipping port market, reflecting the country’s geography and long term infrastructure planning. Qatar’s coastline is relatively shallow in many areas, which limits the development of naturally deep harbors. To overcome this, the country has invested heavily in engineered port facilities designed to handle large cargo volumes and modern vessel sizes. Hamad Port is the most prominent example. Built with advanced dredging, breakwaters, and deep draft berths, it was developed to support container traffic, liquid bulk exports, general cargo, and Ro Ro operations. Its design allows it to accommodate some of the world’s largest ships, including LNG carriers and ultra large container vessels.

Purpose built terminals, automated systems, and integrated logistics zones enhance operational efficiency and reduce turnaround times. Artificial ports also provide greater control over layout and expansion. Authorities can plan berth depth, storage areas, and connectivity to road and industrial networks according to trade needs. This flexibility supports Qatar’s energy exports, construction imports, and growing re export activities. With continued industrial development and LNG expansion projects, artificial port infrastructure remains central to Qatar’s maritime strategy and trade competitiveness.

Ownership Insights:

- Private

- Public

- Public Private Partnership

Public exhibits a clear dominance with a 71.3% share of the total Qatar shipping port market in 2025.

Public ownership represents the largest segment in the Qatar shipping port market, reflecting the strategic importance of maritime infrastructure to the national economy. Major ports, including Hamad Port, operate under government control through entities such as Mwani Qatar. This structure allows the state to align port development with broader economic priorities, particularly energy exports, industrial growth, and trade security. Given Qatar’s reliance on LNG and petroleum exports, public control ensures that port operations support long term national interests rather than short term commercial returns. Investment decisions, capacity expansion, and tariff structures can be coordinated with national development plans. This approach has enabled large scale infrastructure projects, advanced cargo handling systems, and integrated logistics zones to be developed with strong financial backing.

Public ownership also strengthens regulatory oversight and operational stability. Ports handle critical imports such as construction materials, food products, and industrial equipment. Government management helps maintain consistent service levels and supply chain reliability, especially during periods of regional or global disruption. As Qatar continues to expand LNG production and diversify its economy, publicly owned ports remain central to trade facilitation and economic resilience, reinforcing the government’s active role in maritime sector growth.

Service Insights:

- Cargo Handling

- Mooring

- Pilotage

- Towage

Cargo handling leads with a share of 47.9% of the total Qatar shipping port market in 2025.

Cargo handling is the largest service segment in the Qatar shipping port market, reflecting the high volume of trade moving through the country’s ports. With significant exports of LNG, petroleum products, and chemicals, along with steady imports of construction materials, machinery, vehicles, and consumer goods, efficient cargo operations are essential to overall port performance. Advanced cranes, automated yard systems, conveyor networks, and specialized pumping equipment support quick vessel turnaround and high throughput. Dedicated terminals for containers, general cargo, livestock, and liquid bulk allow operations to run in parallel without congestion.

The scale of LNG shipments in particular drives substantial activity in liquid cargo handling. Precision, safety protocols, and technical expertise are critical when dealing with hazardous or temperature controlled products. At the same time, container handling has grown as Qatar strengthens its regional trade links and re export activities. Continuous investment in equipment upgrades, digital tracking systems, and workforce training has improved efficiency and reduced dwell times. As trade volumes expand alongside LNG production capacity, cargo handling will remain the core revenue generating service within Qatar’s port sector.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Repair

- Storage

- Transshipment

Transshipment exhibits a clear dominance with a 44.2% share of the total Qatar shipping port market in 2025.

Transshipment is the largest application segment in the Qatar shipping port market, supported by the country’s strategic position along major east–west maritime routes. Located between Asia, Europe, and Africa, Qatar serves as a convenient redistribution point for cargo moving across the Gulf region and beyond. This geographic advantage allows ports to function not only as origin and destination hubs but also as transfer centers for international shipping lines. Hamad Port plays a central role in transshipment activity. With deep draft berths, modern container terminals, and direct shipping connections to key global ports, it enables efficient transfer of containers between mother vessels and feeder ships. Cargo arriving in large volumes can be consolidated, sorted, and redirected to smaller regional markets such as Oman, Kuwait, Iraq, and parts of East Africa.

Transshipment supports higher vessel traffic and improves port utilization rates. It strengthens Qatar’s position within regional supply chains and reduces reliance on neighboring hub ports. Investments in digital systems, customs facilitation, and logistics zones further enhance turnaround speed and cargo visibility. As trade flows across the Middle East continue to expand and shipping networks adjust to evolving routes, transshipment is expected to remain a primary driver of growth in Qatar’s port operations, reinforcing its ambition to serve as a regional maritime hub.

Region Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah leads with a share of 63.7% of the total Qatar shipping port market in 2025.

Ad Dawhah represents the largest regional segment in the Qatar shipping port market, largely due to its role as the country’s political, commercial, and logistical center. As the capital city, Doha concentrates government institutions, corporate headquarters, financial services, and a significant share of population and industrial demand. This concentration of economic activity drives high volumes of maritime trade linked to construction materials, consumer goods, machinery, and energy related cargo. While Hamad Port is geographically located south of central Doha, its operations are closely tied to the capital’s economic ecosystem. Major importers, exporters, and logistics providers are headquartered in Ad Dawhah, making it the primary coordination hub for port related trade flows. Warehousing, distribution centers, and customs clearance activities are also strongly connected to businesses operating in the capital region.

Infrastructure connectivity further strengthens Ad Dawhah’s dominance. Well developed road networks link the port to industrial zones, commercial districts, and retail markets across the metropolitan area. This ensures efficient inland cargo movement and supports large scale projects and urban development. As Qatar continues infrastructure expansion, energy investments, and commercial diversification, Ad Dawhah is expected to maintain its leading position in maritime trade activity, reinforcing its central role in the national shipping and logistics landscape.

Market Dynamics:

Growth Drivers:

Why is the Qatar Shipping Port Market Growing?

Strategic National Investments in World-Class Port Infrastructure

The Qatar government’s sustained commitment to developing state-of-the-art port infrastructure is a foundational driver of market growth. The multi-billion-dollar Hamad Port project, completed and expanded through successive phases, has provided the country with deep-water berthing capacity, automated container handling systems, and specialized terminals capable of accommodating the largest vessel classes in global shipping. This infrastructure investment extends beyond the ports themselves to encompass the development of adjacent free economic zones, logistics corridors, and industrial cities that create an integrated ecosystem supporting maritime trade expansion. The establishment of the Umm Alhoul Free Zone directly beside Hamad Port exemplifies this approach, offering foreign investors full ownership rights, customs duty exemptions, and direct access to port facilities.

Expansion of LNG and Hydrocarbon Export Capacity Driving Liquid Bulk Volumes

Qatar’s ambitious North Field expansion program represents a transformative growth catalyst for the shipping port market, with planned capacity additions expected to increase. QatarEnergy has finalized exploration and production contracts with multiple nations across different continents and has granted contracts totaling tens of billions of dollars for the North East Field and North South Field expansion projects, aimed at boosting Qatar's LNG production capacity from 77 million tons annually to 126 million tons per year. This unprecedented scaling of gas export capacity will directly increase vessel traffic, liquid bulk cargo volumes, and demand for specialized port services at Ras Laffan Industrial City.

Growing Transshipment Activity and Regional Trade Connectivity

The rapid expansion of transshipment operations at Hamad Port is creating a powerful growth dynamic within Qatar’s shipping port market. The port’s favorable geographic position along east-west trade routes, combined with its high operational efficiency ratings, simplified customs procedures, and expanding network of direct shipping line connections, is attracting increasing volumes of regional cargo redistribution traffic. International shipping lines are progressively incorporating Hamad Port into their hub-and-spoke network configurations, leveraging the facility’s capacity to efficiently transfer containers between feeder vessels serving Gulf markets and mainline vessels operating on intercontinental routes. This structural shift in regional shipping patterns generates compound revenue growth across cargo handling, storage, and ancillary port services. Transshipment activity at Qatar's ports increased by 12 percent in September 2025, highlighting the rising significance of Hamad, Doha, and Al Ruwais ports in both regional and global commerce.

Market Restraints:

What Challenges the Qatar Shipping Port Market is Facing?

Geopolitical Tensions and Maritime Route Vulnerabilities

Qatar’s dependence on the Strait of Hormuz as the primary maritime chokepoint for its hydrocarbon exports and commercial shipping creates inherent vulnerability to regional geopolitical disruptions. Escalating tensions in the broader Middle East, including conflicts affecting Red Sea transit routes, periodically increase shipping insurance costs, redirect vessel traffic, and introduce uncertainty into supply chain planning for Qatar-based port operations.

Intense Regional Competition from Established Hub Ports

Qatar’s shipping port market faces significant competitive pressure from well-established regional maritime hubs, particularly Jebel Ali in Dubai and Salalah in Oman, which benefit from long-standing shipping line relationships, larger throughput capacities, and extensive hinterland connectivity. Attracting and retaining transshipment volumes requires continuous investment in competitive pricing, operational efficiency, and service quality to prevent cargo diversion to rival facilities.

Labor Market Constraints and Skilled Workforce Availability

The specialized nature of modern port operations, including the management of automated systems, digital platforms, and complex logistics coordination, creates demand for technically skilled maritime professionals that Qatar’s relatively small domestic labor market cannot fully satisfy. Reliance on expatriate workers introduces challenges related to workforce retention, knowledge transfer, and the development of sustainable local expertise in port management and maritime services.

Competitive Landscape:

The Qatar shipping port market exhibits a consolidated competitive structure dominated by state-owned and state-affiliated entities that oversee the country’s critical maritime infrastructure. Mwani Qatar (Qatar Ports Management Company) serves as the primary government body responsible for managing and developing the nation’s three main ports, setting operational standards, and coordinating with international maritime organizations. Competition within the market is primarily driven by service quality differentiation, operational efficiency metrics, and the ability to attract international shipping lines through competitive port charges and streamlined customs procedures. The continued expansion of free zone operators, logistics service providers, and specialized maritime firms within port-adjacent economic zones is gradually broadening the competitive landscape beyond traditional port operators.

Recent Developments:

- In November 2025, Old Doha Port revealed the initiation of its maritime transportation service for all future events, building on the significant success it attained during the Qatar Boat Show 2025. In a statement, the port announced that this initiative is part of a range of projects and programs focused on improving the quality of services at the Old Doha Port. The program aims to enhance visitor comfort, ease access to the port, and maintain top efficiency at the events it organizes, all to deliver outstanding experiences for visitors.

Qatar Shipping Port Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Cargo Types Covered |

Break Bulk, Container, Dry Bulk, Liquid Bulk, Ro-Ro |

|

Port Types Covered |

Artificial, Natural |

|

Ownership Covered |

Private, Public, Public Private Partnership |

|

Services Covered |

Cargo Handling, Mooring, Pilotage, Towage |

|

Applications Covered |

Repair, Storage, Transshipment |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Shipping Port Market Report

The Qatar shipping port market size was valued at USD 9.87 Billion in 2025.

The Qatar shipping port market is expected to grow at a compound annual growth rate of 5.04% from 2026-2034 to reach USD 15.70 Billion by 2034.

Liquid bulk held the largest share of the Qatar shipping port market at 52.6% in 2025, driven by the country’s dominant position as one of the world’s leading LNG exporters and significant volumes of petroleum product and petrochemical shipments through specialized terminals.

Key factors driving the Qatar shipping port market include strategic government investments in world-class port infrastructure such as Hamad Port, massive expansion of LNG export capacity through the North Field development projects, growing transshipment volumes reinforcing Qatar’s regional hub status, and the development of integrated free economic zones and digital port management systems.

Major challenges include geopolitical tensions affecting Strait of Hormuz transit security and shipping insurance costs, intense competition from established regional hub ports in the UAE and Oman, labor market constraints in specialized maritime operations, regulatory compliance demands related to evolving international maritime standards, and the capital-intensive nature of port infrastructure maintenance and expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)