Qatar Steel Market Size, Share, Trends and Forecast by Type, Product, Application, and Region, 2026-2034

Qatar Steel Market Summary:

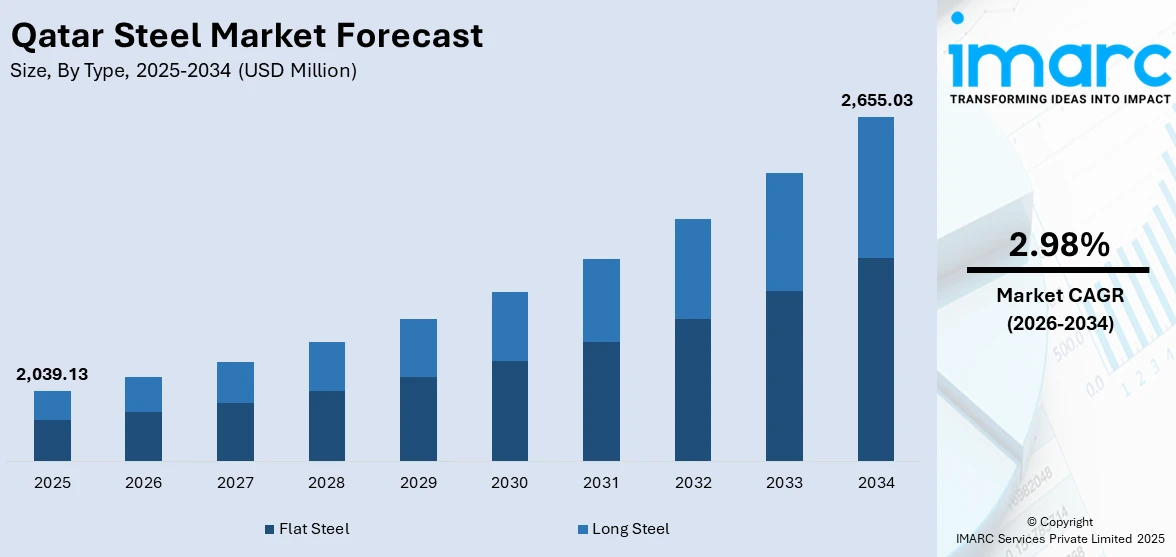

The Qatar steel market size was valued at USD 2,039.13 Million in 2025 and is projected to reach USD 2,655.03 Million by 2034, growing at a compound annual growth rate of 2.98% from 2026-2034.

The Qatar steel market is experiencing steady growth driven by robust construction activities, infrastructure development projects, and the nation's ongoing economic diversification initiatives. Government investments in mega-projects, including transportation networks and renewable energy facilities, continue to fuel steel demand across various sectors. Industrial expansion and manufacturing growth further support market development, while technological advancements in steel production enhance operational efficiency and product quality. Qatar steel market share reflects strong domestic production capabilities.

Key Takeaways and Insights:

- By Type: Flat steel dominates the market with a share of 55% in 2025, driven by strong demand from construction and manufacturing sectors requiring sheet and plate products for structural applications.

- By Product: Structural steel leads the market with a share of 26% in 2025, owing to its essential role in building construction, infrastructure projects, and industrial facility development.

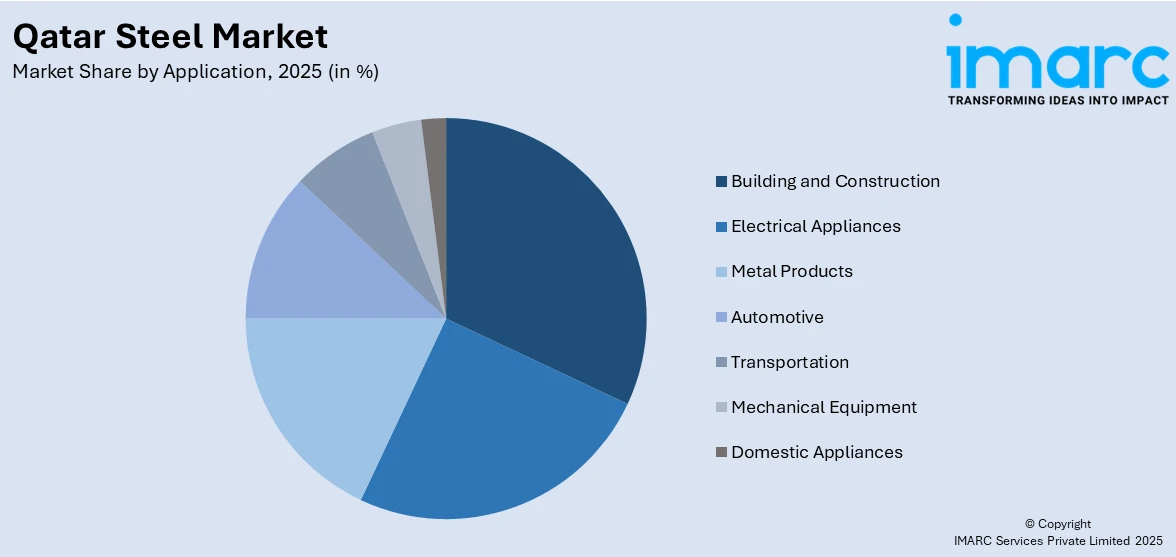

- By Application: Building and construction represent the largest segment with a market share of 32% in 2025, fueled by ongoing residential, commercial, and infrastructure development projects across the nation.

- By Region: Ad Dawhah leads the market with a share of 40% in 2025, as the capital city serves as the economic hub with concentrated commercial construction and infrastructure investments.

- Key Players: The Qatar steel market exhibits a moderately competitive landscape, with established domestic producers and regional suppliers competing across product segments. Market participants focus on technological innovation, sustainable production practices, and strategic partnerships to strengthen their competitive positioning and expand market reach.

To get more information on this market Request Sample

The Qatar steel market continues to benefit from substantial government investments in infrastructure modernization and economic diversification under the Qatar National Vision 2030 framework. The Third National Development Strategy 2024-2030 outlines ambitious industrial development targets, with the manufacturing sector aiming to achieve QR 70.5 billion in added value by 2030. For instance, Qatar Steel has long been a cornerstone of the country’s steel industry and continues to serve as the leading domestic producer. The company operates integrated steelmaking facilities, including direct reduced iron units and electric arc furnaces, supporting a stable and efficient production base. Its strategy emphasizes regional cooperation to strengthen supply chain reliability and operational efficiency. By fostering cross-border partnerships for raw material sourcing, Qatar Steel enhances resilience, supports consistent production, and reinforces its role in meeting domestic demand while maintaining competitiveness within the broader Gulf steel market.

Qatar Steel Market Trends:

Infrastructure Development and Construction Boom

The Qatar steel market is witnessing robust growth driven by significant infrastructure investments and an expanding construction pipeline. The Public Works Authority (Ashghal) announced a five-year infrastructure plan valued at USD 22.2 billion for 2025-2029, representing the largest infrastructure investment program in the authority's history. Major government-led initiatives in transport networks, renewable energy facilities, and large-scale commercial projects are fueling steel demand, while preparations for the Asian Games 2030 continue to drive structural steel requirements across residential, commercial, and industrial sectors.

Technological Advancement and Production Efficiency

Innovation and sustainable practices are transforming the Qatar steel market, with advanced production technologies enhancing operational efficiency and product quality. Qatar Steel's DRI/HBI sales reached approximately 1.4 million tons in 2024, representing a remarkable 167% year-on-year increase. Advanced production methods, including electric arc furnaces and direct reduced iron processes, deliver higher-quality steel while reducing environmental impact. The company's decision to restart its DR-1 plant in Q4 2024 reflects strong demand and commitment to expanding production capacities through cleaner manufacturing technologies.

Industrial Diversification and Manufacturing Expansion

Qatar's economic diversification strategy beyond oil and gas is opening strong new avenues for steel demand across emerging industrial sectors. The Qatar National Manufacturing Strategy 2024-2030 targets raising the manufacturing sector's added value to QR 70.5 billion and increasing non-hydrocarbon exports to approximately QR 49.1 billion. New manufacturing hubs, petrochemical facilities, and technology parks are emerging, requiring specialized steel for equipment, machinery, and structural applications. Government support through industrial zone development and favorable investment policies ensures sustained steel market growth.

Market Outlook 2026-2034:

The Qatar steel market outlook remains positive, supported by sustained government infrastructure investments and industrial diversification initiatives aligned with Qatar National Vision 2030. The construction sector is expected to grow approximately 2% in 2025, with the North Field East LNG expansion projects and government-led investments serving as primary growth drivers. Strategic regional partnerships, including Qatar's participation in the Integrated Industrial Partnership for Sustainable Economic Development with Bahrain, Egypt, Jordan, Morocco, Turkey, and the UAE, will strengthen supply chains and enhance market competitiveness. The market generated a revenue of USD 2,039.13 Million in 2025 and is projected to reach a revenue of USD 2,655.03 Million by 2034, growing at a compound annual growth rate of 2.98% from 2026-2034.

Qatar Steel Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Flat Steel |

55% |

|

Product |

Structural Steel |

26% |

|

Application |

Building and Construction |

32% |

|

Region |

Ad Dawhah |

40% |

Type Insights:

- Flat Steel

- Long Steel

Flat steel dominates with a market share of 55% of the total Qatar steel market in 2025.

Flat steel products command the largest share of Qatar's steel market, driven by extensive applications across construction, manufacturing, and industrial sectors. The segment includes plates, sheets, and coils essential for building facades, roofing systems, and structural components in commercial and residential developments. Qatar's flat steel market is expected to grow steadily, with plates representing the largest revenue-generating product subsegment. Growing demand from the automotive sector and electrical appliances manufacturing further supports flat steel consumption across the nation.

The robust infrastructure development pipeline, including smart city projects in Lusail and urban modernization initiatives in Doha, continues to drive flat steel demand. The Qatar National Manufacturing Strategy 2024-2030 emphasizes the development of downstream steel processing capabilities, creating additional opportunities for flat steel product applications in value-added manufacturing. Strategic investments in production technology and quality enhancement have positioned domestic suppliers to meet increasingly sophisticated specifications demanded by major construction and industrial projects.

Product Insights:

- Structural Steel

- Prestressing Steel

- Bright Steel

- Welding Wire and Rod

- Iron Steel Wire

- Ropes

- Braids

Structural steel leads with a share of 26% of the total Qatar steel market in 2025.

Structural steel products maintain market leadership driven by their critical role in building construction, infrastructure development, and industrial facility projects. The segment benefits from Qatar's extensive construction pipeline, including high-rise commercial buildings, transportation infrastructure, and industrial warehousing facilities. Structural steel fabrication and pre-engineered building segments are expected to lead market growth, reflecting significant construction activity across the nation's urban development zones.

The adoption of pre-fabricated and pre-engineered buildings continues to drive structural steel demand, reflecting trends toward faster and more cost-effective construction methods. Qatar's preparations for hosting major international events, combined with ongoing urbanization and population growth, support sustained structural steel consumption. Advanced manufacturing technologies adopted by domestic fabricators enhance product quality and production efficiency, enabling suppliers to meet stringent specifications for complex architectural and engineering applications.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Building and Construction

- Electrical Appliances

- Metal Products

- Automotive

- Transportation

- Mechanical Equipment

- Domestic Appliances

Building and construction represent the highest revenue with a 32% share of the total Qatar steel market in 2025.

Building and construction applications dominate Qatar's steel consumption, driven by ambitious infrastructure development and urbanization initiatives. The Qatar construction market size reached USD 70.1 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 167.5 Billion by 2034, exhibiting a growth rate (CAGR) of 10.17% during 2026-2034. It continues to generate substantial steel demand for residential, commercial, and public facility projects. The Qatari government has allocated over QAR 210 billion toward infrastructure projects as part of its National Development Strategy 2030, supporting sustained construction sector growth and steel consumption.

Large-scale urban development and infrastructure projects continue to drive strong demand for steel across structural, reinforcement, and finishing applications. Ongoing investments in transport networks, planned cities, and smart urban developments are sustaining activity in the construction sector as it transitions from earlier market adjustments. At the same time, increasing emphasis on sustainable construction and green building practices is encouraging the use of advanced steel products that offer improved durability, efficiency, and environmental performance, supporting long-term demand within the construction industry.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah exhibits a clear dominance with a 40% share of the total Qatar steel market in 2025.

Ad Dawhah (Doha) maintains its position as the primary steel consumption hub, driven by its status as Qatar's capital and economic center. The metropolitan area concentrates significant commercial construction activity, including high-rise office developments, retail complexes, and hospitality facilities. Government ministries and infrastructure authorities headquartered in Doha coordinate major public works projects that generate substantial structural steel demand. The city's established infrastructure and logistics capabilities provide efficient distribution channels for steel products across the nation.

Lusail, developed as a smart city near Doha, continues to draw substantial steel-intensive construction activity with a strong emphasis on sustainability and modern urban design. Ongoing expansion across the greater Doha area is supporting residential projects and community infrastructure that require a wide range of steel applications. At the same time, Al Rayyan and Al Wakrah are accounting for a growing share of steel demand as urban development spreads beyond the capital’s central zones, reflecting a broader geographic distribution of construction-driven steel consumption.

Market Dynamics:

Growth Drivers:

Why is the Qatar Steel Market Growing?

Government Infrastructure Investments and Development Projects

The infrastructure development by the government is among the main growth factors in the Qatar steel market. The steel demand is being maintained in the various uses due to long-term government programmes of urban development, transportation systems, and civic infrastructure. Road projects, road networks, government buildings, and drainage systems are some of the projects that involve huge amounts of structural and reinforcement steel. Meanwhile, procurement is becoming more tailored to local suppliers and local steel manufacturers, and empowering supply chains. This continued emphasis on large-scale infrastructure and local sourcing underpins stable steel demand and reinforces the sector’s role in national development.

Economic Diversification and Industrial Expansion

Qatar’s economic diversification efforts under the National Vision 2030 framework are creating strong demand for steel across emerging industrial sectors. The national manufacturing strategy emphasizes expanding domestic production capacity and strengthening non-hydrocarbon industries, which supports increased use of steel in industrial facilities, machinery, and export-oriented manufacturing. This focus on industrial development reinforces steel’s role as a critical input in Qatar’s long-term economic transformation. The Ministry of Commerce and Industry aims to achieve a 3.4% compound annual growth rate in non-oil sectors by 2030 while targeting USD 100 billion in foreign direct investment. Industrial zone development and free trade area expansions create backbone infrastructure requiring extensive steel utilization for manufacturing facilities, warehousing, and logistics operations supporting the nation's economic transformation objectives.

Energy Sector Expansion and LNG Projects

The growing energy industry in Qatar has remained in high demand for steel with the development of large-scale LNG projects and the related industrial infrastructure. Continuous investments in processing plants, pipelines, and storage systems demand large quantities of structural and special steel. The recovery in the construction activity has been closely associated with the energy projects and the infrastructure programs headed by the government. Simultaneously, the shift to renewable energy in the country is also aiding the steel consumption, with solar energy being dependent on steel to construct the mounting structures, utility supports, and other infrastructures, which underpin the significance of steel in the changing energy environment in Qatar.

Market Restraints:

What Challenges the Qatar Steel Market is Facing?

Global Price Volatility and Raw Material Cost Fluctuations

The Qatar steel market faces challenges from global steel price fluctuations and volatile raw material costs. Dependence on imported iron ore and scrap metal exposes the market to international supply chain vulnerabilities and geopolitical tensions affecting commodity pricing. Rising input costs place pressure on manufacturer margins and can lead to higher steel prices for end users across construction and industrial sectors.

Limited Local Manufacturing Capacity and Import Dependence

Qatar's steel market remains vulnerable to international market dynamics due to reliance on imports for a portion of steel requirements and raw material supplies. Global shipping costs remain elevated, impacting tender costs due to minimal local manufacturing of certain steel products. Limited domestic production capacity for specialized steel grades necessitates import dependence, creating supply chain risks and pricing uncertainties.

Post-World Cup Market Adjustment and Project Pipeline Changes

After the completion of major event-driven developments, Qatar’s construction sector has moved into a consolidation phase marked by softer demand for large projects. As the market stabilizes, growth has moderated compared with earlier expansionary periods. Parts of the construction supply chain have adjusted capacity to align with changing requirements, leading to cost pressures and higher overheads. This transition reflects a shift from rapid build-out toward a more balanced and sustainable construction environment.

Competitive Landscape:

The Qatar steel market exhibits a moderately concentrated competitive landscape with established domestic producers and regional suppliers competing across multiple product segments. Market participants differentiate through product quality, technological capabilities, sustainable production practices, and strategic partnerships. The industry structure features a combination of integrated steel producers, steel fabricators, and specialized product manufacturers serving construction, industrial, and manufacturing end-use sectors. Companies focus on operational efficiency, production capacity optimization, and customer service excellence to strengthen competitive positioning. Strategic investments in advanced manufacturing technologies and sustainability initiatives enhance market participants' ability to meet evolving customer specifications and regulatory requirements. Regional cooperation agreements and cross-border partnerships are increasingly important for securing raw material supplies and expanding market reach across GCC countries.

Recent Developments:

- February 2025: Qatar Steel and Bahrain Steel signed a supply agreement valued at USD 1.266 billion, covering 5 million metric tons of raw materials over five years. The partnership strengthens regional industrial cooperation and ensures stable supply of essential raw materials for Qatar Steel's operations, enhancing production efficiency and supporting long-term economic growth.

- January 2025: Egypt and Qatar announced a partnership to build a USD 100 million iron and steel plant in Qena, Egypt, with operations scheduled to begin in 2026. Egypt will hold a 51% stake while Qatar finances production lines and raw materials with a 49% share. Approximately 80% of the plant's rebar output will be exported to regional markets.

Qatar Steel Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Flat Steel, Long Steel |

| Products Covered | Structural Steel, Prestressing Steel, Bright Steel, Welding Wire and Rod, Iron Steel Wire, Ropes, Braids |

| Applications Covered | Building and Construction, Electrical Appliances, Metal Products, Automotive, Transportation, Mechanical Equipment, Domestic Appliances |

| Regions Covered | Ad Dawhah, Al Rayyan, Al Wakrah, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Steel Market Report

The Qatar steel market size was valued at USD 2,039.13 Million in 2025.

The Qatar steel market is expected to grow at a compound annual growth rate of 2.98% from 2026-2034 to reach USD 2,655.03 Million by 2034.

Flat Steel dominated the Qatar steel market with a 55% share in 2025, driven by strong demand from construction and manufacturing sectors requiring sheet and plate products for structural and industrial applications.

Key factors driving the Qatar steel market include substantial government infrastructure investments under the National Development Strategy, economic diversification initiatives aligned with Qatar National Vision 2030, energy sector expansion including North Field East LNG projects, and growing construction activity across residential, commercial, and industrial sectors.

Major challenges include global steel price volatility and raw material cost fluctuations, dependence on imported iron ore and scrap metal, elevated shipping costs affecting tender prices, competition from regional suppliers, and post-World Cup market adjustments with reduced large-scale project demand compared to previous years.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade