Qatar Warehousing Market Size, Share, Trends and Forecast by Warehouse Type, End Use, and Region, 2026-2034

Qatar Warehousing Market Summary:

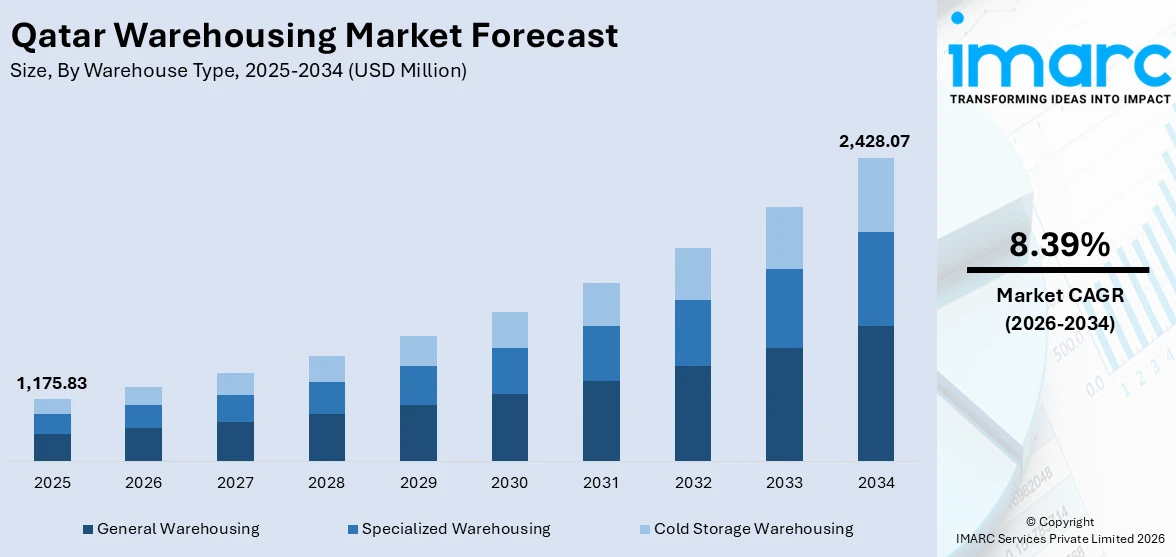

The Qatar warehousing market size was valued at USD 1,175.83 Million in 2025 and is projected to reach USD 2,428.07 Million by 2034, growing at a compound annual growth rate of 8.39% from 2026-2034.

The Qatar warehousing market is experiencing robust growth driven by the nation’s economic diversification efforts under Qatar National Vision 2030, expanding free zone infrastructure, and rising import dependency for consumer goods and industrial materials. The rapid expansion of e-commerce, growing retail activity, and increased investment in cold chain and specialized storage solutions are further strengthening warehousing demand, positioning the country as a key logistics hub and bolstering Qatar warehousing market share.

Key Takeaways and Insights:

- By Warehouse Type: General warehousing dominates the market with a share of 46.2% in 2025, driven by the increasing demand for large-scale storage facilities to support import-heavy supply chains, retail distribution operations, and the growing volume of consumer goods across the country.

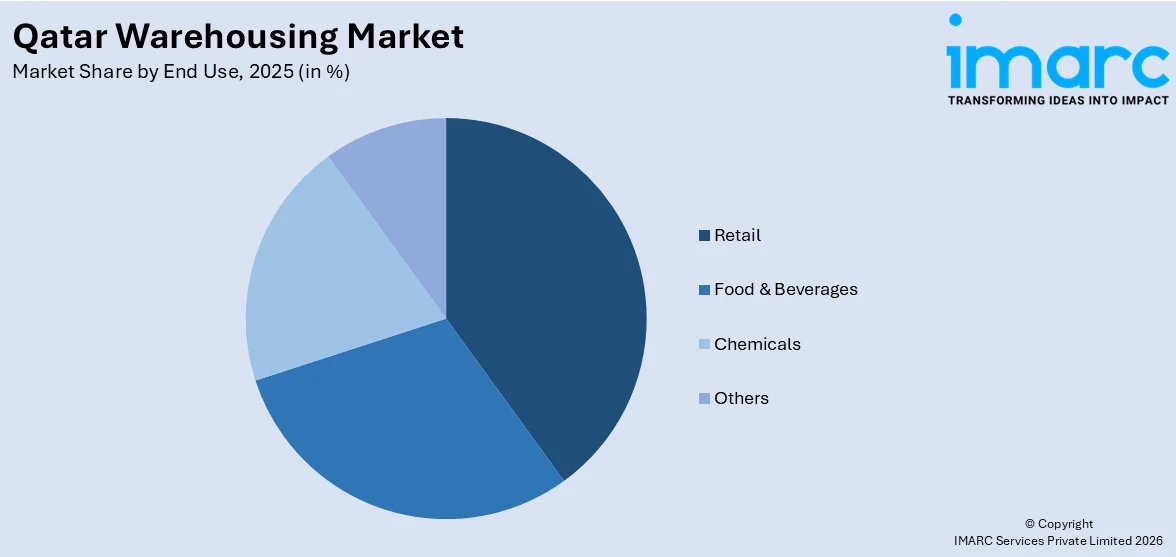

- By End Use: Retail leads the market with a share of 36.8% in 2025, reflecting the expansion of organized retail formats, rising consumer spending power fueled by high GDP per capita, and the accelerating shift toward omnichannel fulfillment strategies.

- By Region: Ad Dawhah represents the largest region with 58.1% share in 2025, supported by the concentration of major logistics hubs, port infrastructure, commercial centers, and the presence of leading warehousing operators within the capital municipality.

- Key Players: Leading companies in the Qatar warehousing market are expanding their service portfolios, investing in automation and sustainability initiatives, developing specialized storage solutions, and forming strategic partnerships to strengthen market positioning and address the growing demand for integrated logistics services.

To get more information on this market Request Sample

The Qatar warehousing market is presently undergoing a major shift as the country is gearing up to become a leading logistics gateway between Asia, Africa, and Europe. The government’s focus on diversifying the economy has triggered the establishment of two large free trade zones at Ras Bufontas and Umm Alhoul, which aim to maximize logistics efficiency through the adoption of advanced warehousing and manufacturing facilities. The growing demand from the retail and food and beverages industries, along with the emergence of e-commerce platforms and refrigerated storage needs, is continuously fueling the development of modern warehousing infrastructure in the Qatar warehousing market. Major players are now adopting automation solutions, digital warehouse management systems, and energy-efficient solutions to maximize logistics efficiency and cater to the evolving needs of clients in the Qatar warehousing market.

Qatar Warehousing Market Trends:

Accelerating Digital Transformation and Warehouse Automation

The adoption of advanced technologies including artificial intelligence, augmented reality, and automated storage and retrieval systems is reshaping warehouse operations across Qatar. Operators are implementing cloud-based warehouse management systems, IoT-enabled tracking, and predictive maintenance tools to improve real-time visibility and asset utilization. In April 2024, Gulf Warehousing Company became the first logistics provider in Qatar to introduce vision-picking technology using augmented reality to enhance warehouse efficiency and accuracy, while also deploying AI-powered records management and automated storage and retrieval systems for e-commerce fulfillment operations.

Expansion of Free Zone Logistics Infrastructure

Qatar’s free zone ecosystem is emerging as a significant catalyst for warehousing expansion, with both Ras Bufontas and Umm Alhoul free zones attracting global logistics operators. These zones offer streamlined customs processing, proximity to world-class transport infrastructure, and a business-friendly regulatory environment. In October 2025, Qatar Free Zones Authority and Alfardan Automotive inaugurated a 67,000-square-meter automotive and spare parts logistics hub at Umm Alhoul Free Zone, featuring temperature-controlled bays for luxury vehicles, a 24-bay pre-delivery inspection center, and advanced inventory management systems.

Integration of Green and Sustainable Warehousing Practices

Sustainability is becoming a strategic priority for warehousing operators in Qatar, driven by the nation’s commitment to achieving net-zero emissions by 2050 under Qatar National Vision 2030. Logistics providers are adopting renewable energy solutions, water recycling programs, and environmentally responsible operational practices. In April 2025, Gulf Warehousing Company partnered with Yellow Door Energy to develop solar power plants across three logistics hubs, including Logistics Village Qatar, Bu Sulba Warehousing Park, and Al Wukair Logistics Park, generating approximately 50,000 megawatt-hours of clean energy annually.

Market Outlook 2026-2034:

The Qatar warehousing market is set to register positive growth during the forecast period, driven by the government’s continued focus on infrastructure development, diversification of the economy, and enhancement of logistics capabilities in key free zones. The growing penetration of e-commerce, demand for temperature-controlled and specialty storage facilities, and the enhanced role of Qatar as a regional transshipment point are expected to generate positive momentum for the warehousing market. Automation, digital supply chain solutions, and sustainable logistics practices will continue to enhance the market’s trajectory. The market generated a revenue of USD 1,175.83 Million in 2025 and is projected to reach a revenue of USD 2,428.07 Million by 2034, growing at a compound annual growth rate of 8.39% from 2026-2034.

Qatar Warehousing Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Warehouse Type |

General Warehousing |

46.2% |

|

End Use |

Retail |

36.8% |

|

Region |

Ad Dawhah |

58.1% |

Warehouse Type Insights:

- General Warehousing

- Specialized Warehousing

- Cold Storage Warehousing

General warehousing dominates with a market share of 46.2% of the total Qatar warehousing market in 2025.

General warehousing represents the largest portion of the Qatar warehousing market, owing to the country’s large dependence on imports for consumer, food, and industrial goods. The market for general warehousing is also supported by the growing logistics infrastructure and the growing preference among companies to subcontract their storage and distribution functions to specialized third-party logistics service providers. The Gulf Warehousing Company, the largest logistics company in Qatar, operates large warehousing capacities through its regional operations, including large facilities at Logistics Village Qatar, Bu Sulba Warehousing Park, and Al Wukair Logistics Park.

The general warehousing market remains supported by the continued growth of Qatar’s non-hydrocarbon economy, especially the manufacturing, construction, and wholesale trade sectors. The increasing need for efficient inventory management, cross-dock services, and centralized distribution solutions is encouraging companies to invest in the development of larger and more complex warehouse facilities with advanced material handling systems and computerized inventory management systems. The development of logistics parks and free zones is also contributing to the growth of general warehousing capacity.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Retail

- Food & Beverages

- Chemicals

- Others

Retail leads with a share of 36.8% of the total Qatar warehousing market in 2025.

The retail industry is the biggest end-use industry for the warehousing market in Qatar, driven by the growing consumer economy and the emergence of modern retail formats such as hypermarkets, supermarkets, and specialty stores. The retail industry in Qatar is expected to continue growing with the support of high disposable incomes, a large and heavily urbanized population, and the development of large-scale shopping destinations, which will drive the demand for efficient warehousing and distribution infrastructure to support the retail supply chain.

The growing e-commerce industry in Qatar is also expected to drive the demand for warehousing in the retail industry. Online shopping platforms are increasingly investing in fulfillment centers, dark stores, and last-mile delivery facilities to support consumer demand for faster delivery. The trend towards omnichannel retailing, which involves the integration of physical and online retailing, is also driving the demand for more flexible and technology-driven warehousing solutions that can support both traditional bulk distribution and individual order fulfillment with high accuracy and speed.

Regional Insights:

- Ad Dawhah

- Al Rayyan

- Al Wakrah

- Others

Ad Dawhah represents the leading region with a 58.1% share of the total Qatar warehousing market in 2025.

Ad Dawhah has the strongest presence in the Qatar warehousing market, driven by the region’s focus on the logistics infrastructure, commercial, and port sectors. The region is home to Hamad Port, which was one of the top-performing container ports in the World Bank’s Container Port Performance Index, with transshipment containers contributing a substantial volume to the overall container handled, as stated by Mwani Qatar, thus establishing the region as the main gateway for Qatar’s trade and warehousing activities.

The presence of large logistics parks such as Logistics Village Qatar and the surrounding industrial zones provides a strong foundation for warehousing and distribution services in Ad Dawhah. The region is also home to the headquarters and main operations of the main logistics players, ensuring that the region is close to the main customers in the retail, manufacturing, and energy sectors. Port automation, smart customs, and free zone projects are some of the factors that continue to attract logistics players to the region.

Market Dynamics:

Growth Drivers:

Why is the Qatar Warehousing Market Growing?

Government-Led Infrastructure Development and Economic Diversification

Qatar’s sustained government investment in logistics infrastructure under the Qatar National Vision 2030 framework is a primary catalyst for warehousing market expansion. The nation has committed substantial resources to developing world-class port facilities, airport expansions, road networks, and dedicated logistics zones that directly increase the capacity and efficiency of warehousing operations. The establishment and ongoing expansion of the Ras Bufontas and Umm Alhoul free trade zones have created purpose-built environments for warehousing, distribution, and value-added logistics activities with streamlined customs processes and regulatory incentives for both local and international investors. The broader economic diversification strategy is driving the growth of non-hydrocarbon sectors including manufacturing, pharmaceuticals, food processing, and technology, all of which require sophisticated storage and distribution infrastructure. The government’s Third National Development Strategy for 2024 to 2030 continues to prioritize logistics sector development, and in mid-2025 Qatar announced a USD 1 Billion incentive program designed to stimulate new joint ventures and foreign business setups, further reinforcing the warehousing sector’s long-term growth outlook.

Rapid E-Commerce Expansion and Evolving Consumer Fulfillment Expectations

The rapid expansion of e-commerce in Qatar is generating significant new demand for warehousing and fulfillment infrastructure. The country’s near-universal internet penetration, combined with one of the highest smartphone adoption rates in the region, has established a mobile-first shopping culture that continues to reshape retail logistics requirements. E-commerce transactions in Qatar recorded year-over-year growth, underscoring the accelerating shift toward digital commerce and the corresponding need for modern fulfillment centers, last-mile delivery hubs, and automated warehousing solutions. The growing demand for faster delivery times, including same-day and sub-sixty-minute grocery delivery, is pushing logistics providers to develop micro-fulfillment centers and dark stores in strategic urban locations, thereby expanding the overall warehousing footprint.

Strategic Geographic Positioning as a Regional Transshipment and Logistics Hub

Qatar’s strategic geographic location at the crossroads of major east-west trade routes positions the country as a natural logistics hub connecting Asia, Africa, and Europe. This geographic advantage is being actively leveraged through world-class infrastructure investments in Hamad Port and Hamad International Airport, which provide deep-water maritime access and global air cargo connectivity respectively. The growth in transshipment volumes at Hamad Port, which accounted for nearly half of total container volumes handled between January and November 2025, demonstrates the port’s expanding role beyond a national gateway into a regional logistics platform. This increasing transshipment activity directly drives demand for warehouse space for consolidation, deconsolidation, and value-added logistics services. The ongoing development of integrated logistics corridors that connect port, airport, and free zone infrastructure is further strengthening Qatar’s competitive position, attracting global logistics operators who require strategic warehousing facilities to service broader regional distribution networks.

Market Restraints:

What Challenges the Qatar Warehousing Market is Facing?

Limited Land Availability and Elevated Warehousing Costs

The scarcity of available industrial land in prime logistics locations, particularly within and around the Doha metropolitan area, poses a significant constraint on warehousing expansion. High land costs and rising rental rates for warehouse facilities increase operational expenses for logistics providers, limiting the ability of smaller operators to scale and potentially deterring new market entrants. This supply-demand imbalance in warehouse real estate puts upward pressure on storage costs across the sector.

Shortage of Skilled Logistics and Warehousing Workforce

Qatar’s warehousing sector faces a persistent challenge in recruiting and retaining skilled professionals with expertise in modern warehouse management, automation technologies, and supply chain operations. The country’s reliance on expatriate labor, combined with evolving visa regulations and labor market dynamics, creates workforce availability constraints. As warehousing facilities become increasingly technology-driven, the demand for personnel trained in robotics, data analytics, and digital systems management continues to outpace supply.

Fluctuating Trade Volumes and Demand Cyclicality

The Qatar warehousing market remains susceptible to fluctuations in trade volumes driven by global economic conditions, geopolitical developments, and commodity price volatility. Project-based demand from the energy and construction sectors can lead to uneven warehouse utilization rates, creating challenges for operators in maintaining consistent occupancy and revenue levels. Balancing service quality with cost efficiency during periods of reduced demand remains an ongoing concern for market participants.

Competitive Landscape:

The Qatar warehousing market has a moderately consolidated competitive environment, which is dominated by well-established local players and an increasing presence of global logistics firms. The major players are differentiating themselves based on infrastructure, diversified services, and technology. The players are focusing on enhancing their storage capacity, implementing automation and digital management systems, and developing dedicated facilities for temperature-controlled storage, handling hazardous materials, and e-commerce fulfillment. Collaborations, mergers, and free zone investments are increasing competition and innovation in the market. The market is experiencing a trend of integrated logistics services, where warehousing companies are providing end-to-end supply chain services that include storage, transportation, customs brokerage, and last-mile delivery to engage and retain customers from various industry sectors.

Recent Developments:

- In January 2026, Gulf Warehousing Company reported QR 120 million in net profit for the financial year 2025, reflecting the company’s strong operational performance and continued portfolio diversification through integration and expansion across the region.

- In October 2025, Gulf Warehousing Company acquired a strategic, non-controlling stake in European technology and logistics scale-up Quivo to expand its footprint across three continents. The partnership integrates Quivo’s omnichannel software into GWC warehouses in Qatar, with additional rollouts planned in the UAE and Saudi Arabia.

Qatar Warehousing Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Warehouse Types Covered |

General Warehousing, Specialized Warehousing, Cold Storage Warehousing |

|

End Uses Covered |

Retail, Food & Beverages, Chemicals, Others |

|

Regions Covered |

Ad Dawhah, Al Rayyan, Al Wakrah, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Qatar Warehousing Market Report

The Qatar warehousing market size was valued at USD 1,175.83 Million in 2025.

The Qatar warehousing market is expected to grow at a compound annual growth rate of 8.39% from 2026-2034 to reach USD 2,428.07 Million by 2034.

General warehousing dominated the market with a share of 46.2%, driven by the country’s high import dependency for consumer goods and industrial materials, expanding logistics parks, and the growing preference for outsourced storage and distribution services.

Key factors driving the Qatar warehousing market include government-led infrastructure development under Qatar National Vision 2030, rapid e-commerce expansion, increasing import volumes, free zone development, growing retail activity, and the country’s strategic positioning as a regional logistics hub.

Major challenges include limited land availability and high warehousing rents in prime locations, shortage of skilled logistics workforce, fluctuating trade volumes tied to global economic conditions, demand cyclicality from project-based energy and construction sectors, and rising operational costs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade