Railroad Market Size, Share, Trends and Forecast by Type, Distance, End Use, and Region, 2026-2034

Railroad Market Size, Share, Trends & Forecast (2026-2034)

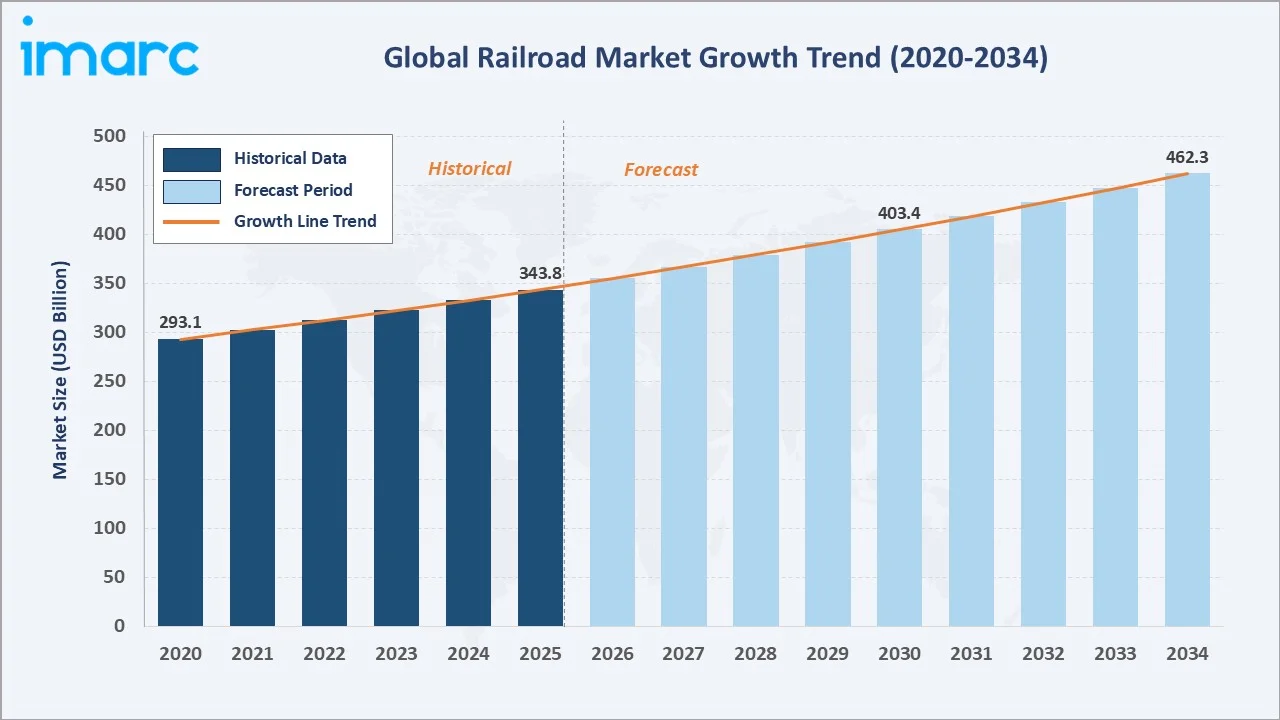

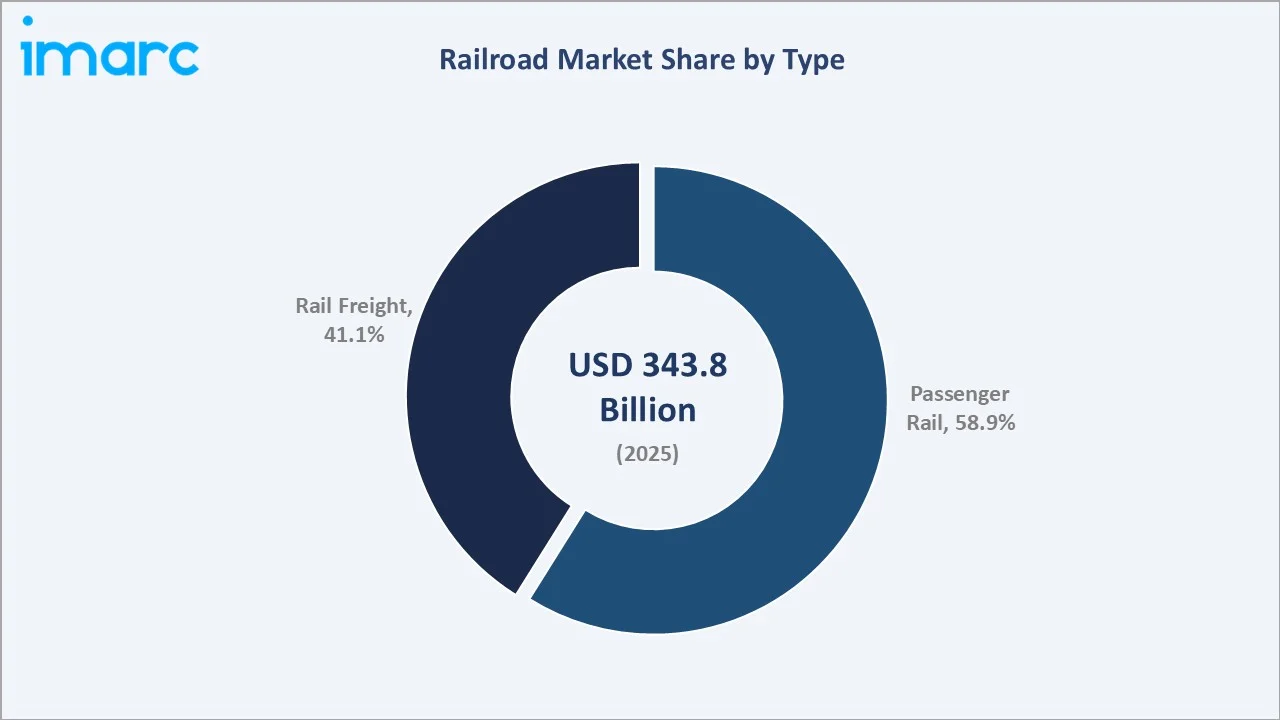

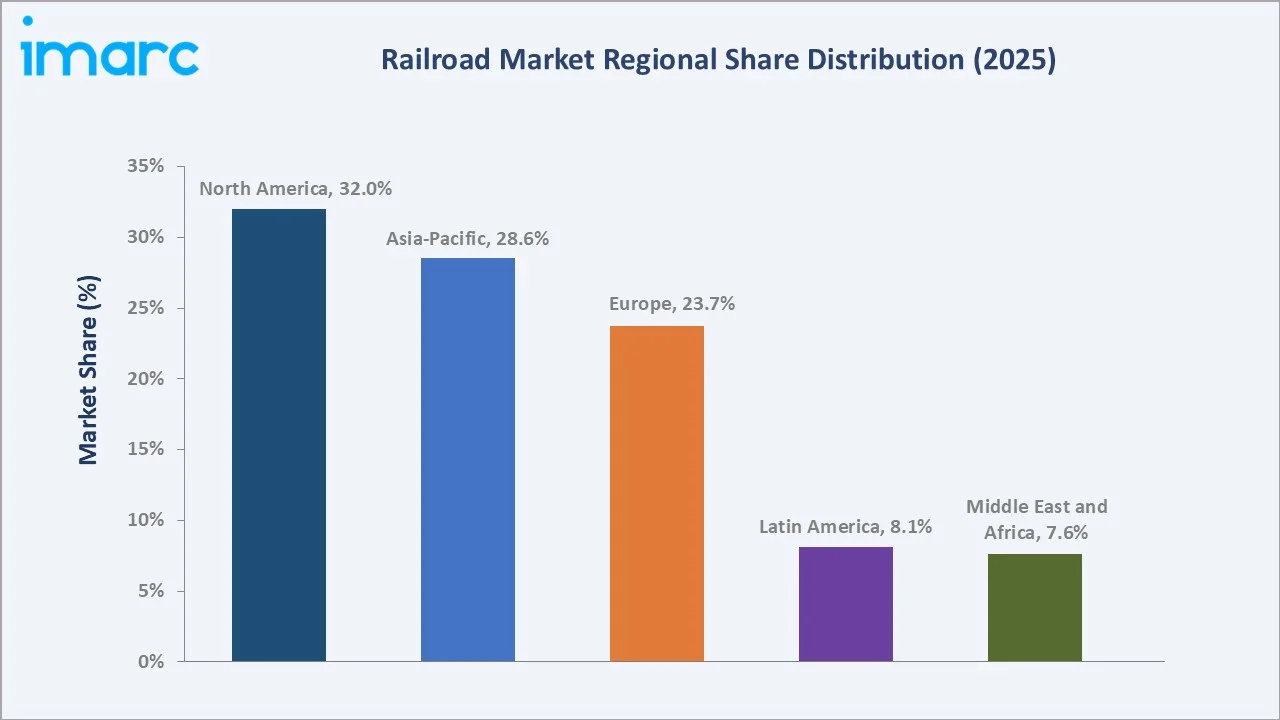

The global railroad market reached USD 343.8 Billion in 2025 and is projected to reach USD 462.3 Billion by 2034, growing at a CAGR of 3.24% during 2026-2034. The market is driven by rising investments in rail infrastructure modernization, urban transit expansion, freight transportation growth, and government initiatives promoting sustainable and efficient mobility solutions. China's high-speed rail network is targeting to extend to 70,000 km by 2035, driving the railroad market demand. Passenger rail dominates at 58.9%. Long distance leads at 54.6%. North America commands 32.0% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 343.8 Billion |

|

Forecast Market Size (2034) |

USD 462.3 Billion |

|

CAGR (2026-2034) |

3.24% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Passenger Rail (58.9%, 2025) |

|

Dominant Distance |

Long Distance (54.6%, 2025) |

|

Leading Region |

North America (32.0%, 2025) |

The market expanded from USD 293.1 Billion in 2020 to USD 343.8 Billion in 2025, anchored at USD 403.4 Billion in 2030, and forecast to reach USD 462.3 Billion by 2034. COVID-19 created the most severe passenger rail revenue disruption in modern history. The post-pandemic recovery has been structural rather than merely cyclical, with governments globally using rail investment as a cornerstone of both economic recovery and decarbonization policy.

To get more information on this market, Request Sample

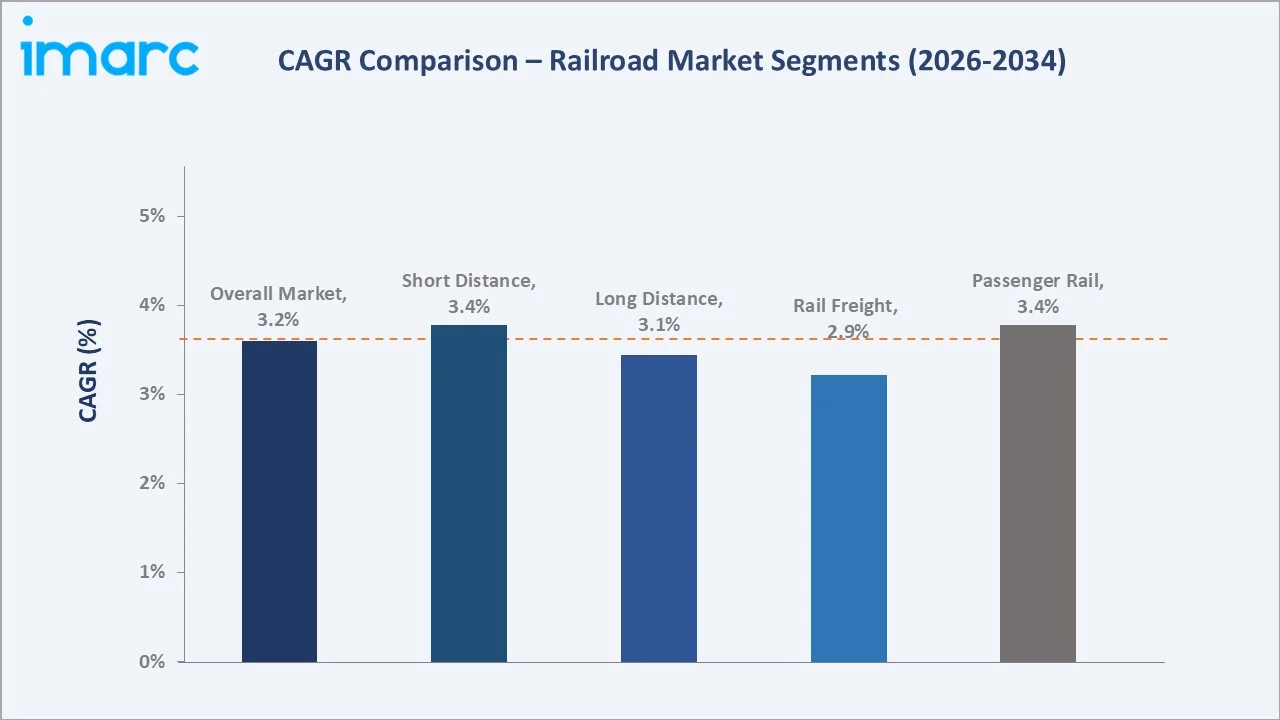

Passenger rail grows at ~3.4% CAGR as urban and HSR capacity expansion compounds post-pandemic ridership recovery. Short-distance rail grows at ~3.4% CAGR driven by urbanization-driven transit investment in Asia Pacific, Europe, and emerging markets, while long-distance rail grows at ~3.1% CAGR through HSR network expansion and decarbonization-driven modal shift from aviation.

Executive Summary

The global railroad market reached USD 343.8 Billion in 2025, representing the world's most environmentally efficient large-scale transportation system and a sector at the intersection of climate policy, urbanization economics, and infrastructure investment cycles. Rail is uniquely positioned as both the world's most carbon-efficient passenger transport mode per km and the most fuel-efficient commercial freight mode, making railroad investment a central pillar of virtually every national climate strategy and transport decarbonization plan. The market is projected to reach USD 462.3 Billion by 2034.

Passenger rail at 58.9% dominates through the structural growth of urban mass transit, high-speed rail adoption displacing domestic aviation on routes under 600 km, and government commitments to passenger rail expansion under climate and mobility frameworks. Long distance at 54.6% reflects both the revenue concentration of HSR premium services and North America's long-haul freight rail dominance as primary revenue generators within their respective categories. North America, at 32.0%, leads through its freight railroad revenue dominance.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Passenger Rail - 58.9% share (2025) |

|

Dominant Distance |

Long Distance - 54.6% market share (2025) |

|

Leading Region |

North America - 32.0% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Passenger Rail at 58.9% reflecting the global investment renaissance in urban transit and high-speed rail driven by climate commitments and urbanization: Passenger rail's dominant market share reflects both the political and commercial momentum behind global rail investment. China's HSR investment is the single largest infrastructure investment program in human history, adding new HSR annually.

- Long Distance at 54.6% anchored by North America's freight rail and global HSR intercity premium services: Long Distance rail's 54.6% share reflects the revenue concentration of two distinct but commercially significant categories. First, North America's Class I railroad freight model is structurally long-distance. Second, high-speed rail's intercity passenger revenue generates premium yields.

- North America at 32.0% through the world's highest-revenue freight railroad system: North America's 32.0% market share reflects the extraordinary commercial success of the US and Canadian Class I freight railroad model.

Railroad Market Overview

The global railroad market encompasses passenger rail services (high-speed intercity, conventional intercity, regional, commuter, urban metro, light rail, and tram operations), freight rail services (intermodal container, bulk commodity, carload, automotive, and specialized freight), and supporting rail infrastructure (track, signaling, electrification, stations, maintenance facilities). The market is served by a combination of government-owned national operators, regulated private operators, and concession operators.

The ecosystem integrates rolling stock manufacturers, infrastructure operators, signaling and technology providers, rail track and component suppliers, passengers and freight shippers as end users, and government bodies setting policy, funding, and regulatory frameworks that define rail market structure in each country. Macroeconomic factors include rapid urbanization, population growth, industrial expansion, and increasing public infrastructure spending.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

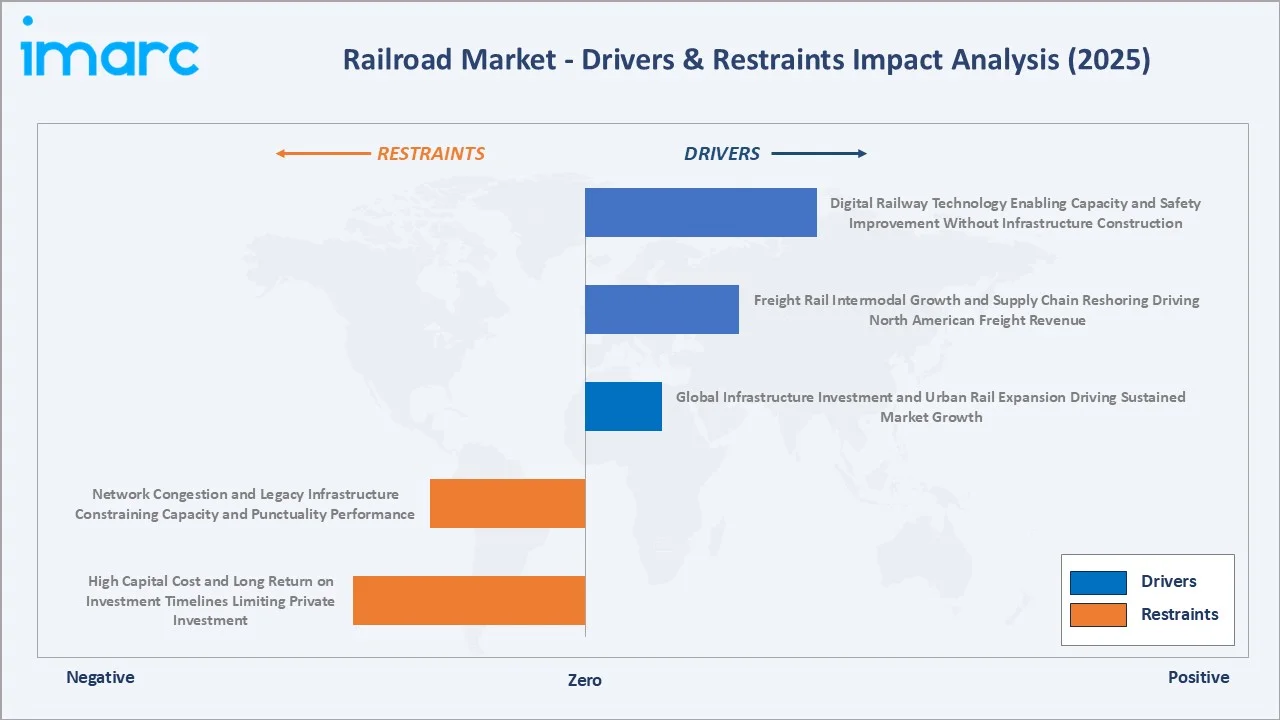

- Global Infrastructure Investment and Urban Rail Expansion Driving Sustained Market Growth: The global rail infrastructure investment pipeline represents one of the largest committed public and private capital programs in human history. Indian Railways developed the National Rail Plan 2030 to build a future-ready railway network by 2030. The plan focuses on strengthening operational capacity and implementing commercial policy strategies to increase the railway sector’s share in freight transportation to 45%. This plan is driving the railroad market by accelerating investments in rail infrastructure, freight corridors, signaling systems, rolling stock, and logistics modernization.

- Freight Rail Intermodal Growth and Supply Chain Reshoring Driving North American Freight Revenue: North American freight rail is experiencing its most structurally favorable demand environment in decades. The US manufacturing reshoring and nearshoring trend is creating new rail freight demand from industrial facilities locating near rail-served corridors.

- Digital Railway Technology Enabling Capacity and Safety Improvement Without Infrastructure Construction: The adoption of digital railway technologies improves network capacity, operational efficiency, and passenger safety without requiring extensive new infrastructure construction. In February 2026, Greece launched the railway.gov.gr platform, an advanced digital system that allows passengers to monitor train movements in real time across the national rail network. These digital solutions are also helping railway authorities lower operational costs while supporting safer and more reliable rail transportation services.

Market Restraints

- High Capital Cost and Long Return on Investment Timelines Limiting Private Investment: Rail infrastructure is among the most capital-intensive investments in the global economy. These capital costs, combined with 30-50 year project lifetimes and rail's inherent public service characteristics, create returns on invested capital of 3-6% that are below commercial investors' typical hurdle rates of 8-12%. This creates a structural dependence on government funding and viability gap support that makes rail investment highly sensitive to political commitment, national fiscal capacity, and interest rate cycles.

- Network Congestion and Legacy Infrastructure Constraining Capacity and Punctuality Performance: Network congestion and aging railway infrastructure limit operational capacity, reducing service reliability and increasing delays across passenger and freight networks. Legacy signaling systems, outdated tracks, and insufficient maintenance investments restrict train frequency and efficient traffic management, particularly in densely utilized rail corridors. These challenges also increase operational costs and negatively impact punctuality, customer satisfaction, and overall network efficiency.

Market Opportunities

- Night Train Renaissance as Low-Carbon Long-Distance Travel Alternative to Aviation: The revival of night trains is creating significant opportunities as travelers increasingly seek low-carbon alternatives to short- and medium-haul air travel. Governments and rail operators are expanding overnight rail services to support sustainable mobility goals, reduce transportation emissions, and improve cross-border connectivity. Rising demand for comfortable long-distance travel, combined with investments in modern sleeper coaches and digital booking systems, is further strengthening the market potential for night rail transportation.

- Hydrogen and Battery-Electric Trains Enabling Decarbonization of Non-Electrified Rail Networks: Hydrogen and battery-electric trains enabling low-emission rail operations on non-electrified routes without the need for extensive overhead electrification infrastructure. Rail operators and governments are increasingly investing in alternative propulsion technologies to meet decarbonization targets, reduce diesel dependency, and lower operating emissions. This transition is driving demand for advanced rolling stock, charging systems, hydrogen refueling infrastructure, and next-generation rail technologies across regional and freight networks.

Market Challenges

- Political Governance and Funding Continuity Risk for Long-Duration Rail Projects: Political uncertainty and inconsistent funding support delay long-duration rail infrastructure and modernization projects. Changes in government priorities, regulatory policies, budget allocations, and public investment strategies can disrupt project execution timelines and reduce investor confidence. These risks often lead to cost overruns, stalled developments, and slower adoption of advanced rail technologies and network expansion initiatives.

- Chinese Rolling Stock Procurement Restrictions in Western Markets Creating Market Fragmentation: Restrictions on Chinese rolling stock procurement in several Western markets are creating fragmentation within the global railroad industry by limiting supplier access and reducing cross-border equipment standardization. Trade tensions, national security concerns, and localization requirements are increasing procurement complexities and project costs for rail operators and manufacturers. These restrictions are also disrupting supply chains and slowing the adoption of cost-competitive rail technologies in international markets.

Emerging Market Trends

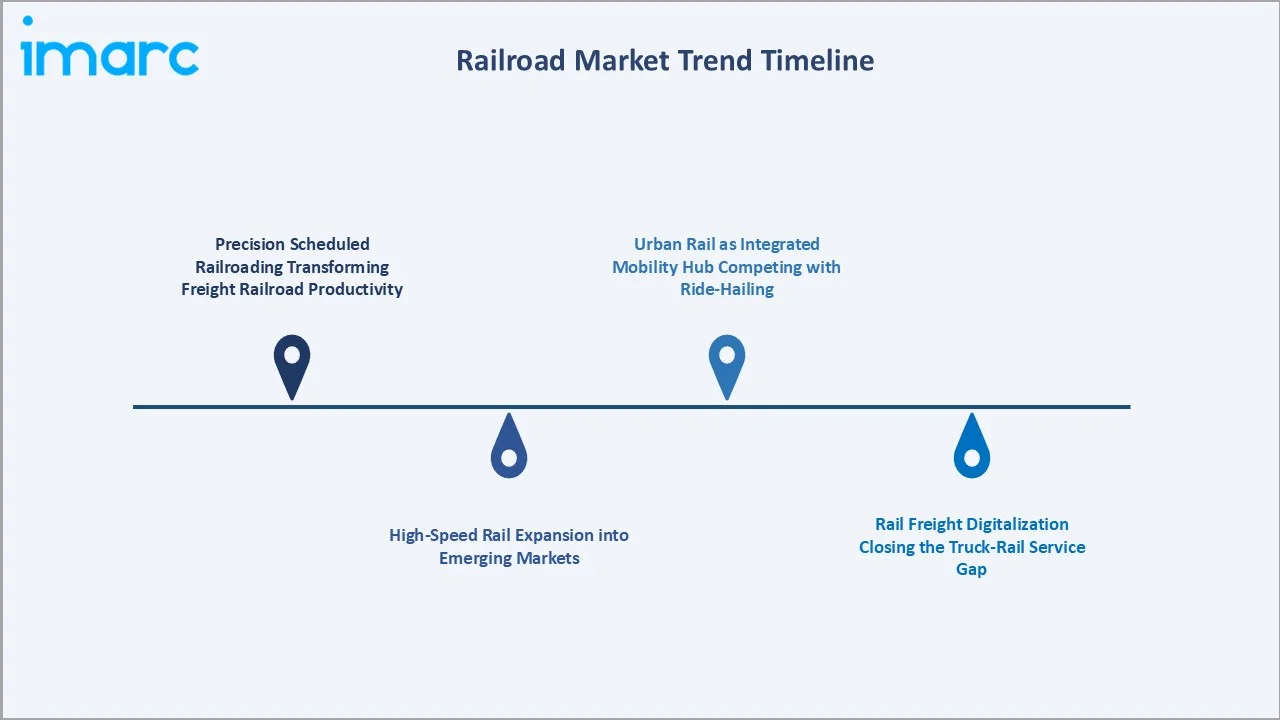

1. Precision Scheduled Railroading Transforming Freight Railroad Productivity

Precision Scheduled Railroading (PSR) is improving freight network efficiency, asset utilization, and operational productivity through fixed scheduling and optimized train movements. Rail operators are increasingly adopting PSR strategies to reduce transit times, lower fuel consumption, minimize idle assets, and enhance service reliability across freight transportation networks.

2. High-Speed Rail Expansion into Emerging Markets

The expansion of high-speed rail networks into emerging markets is becoming a significant trend as governments invest in faster, energy-efficient, and sustainable transportation infrastructure. Countries across Asia, the Middle East, Latin America, and parts of Africa are increasingly developing high-speed rail corridors to improve intercity connectivity, support economic growth, and reduce dependence on road and air transportation. India Union Budget 2026–27 announced 7 new high-speed rail corridors, signalling expansion beyond the Mumbai–Ahmedabad corridor.

3. Rail Freight Digitalization Closing the Truck-Rail Service Gap

Rail freight digitalization is improving shipment visibility, scheduling accuracy, and real-time cargo tracking, helping rail operators compete more effectively with road transportation services. Technologies such as AI-driven logistics platforms, predictive analytics, automated yard management, and digital freight booking systems are enhancing operational efficiency, reducing transit delays, and improving customer experience across rail freight networks.

4. Urban Rail as Integrated Mobility Hub Competing with Ride-Hailing

Urban rail systems are increasingly evolving into integrated mobility hubs by combining metro, bus, bike-sharing, and last-mile connectivity services within unified transportation ecosystems. This trend is helping rail operators compete with ride-hailing platforms by offering seamless multimodal travel, digital ticketing, improved convenience, and lower transportation costs for daily commuters in densely populated cities.

Industry Value Chain Analysis

The global railroad industry value chain integrates infrastructure planning and construction, rolling stock manufacturing and procurement, track and signaling systems installation, train operations and dispatch, passenger and freight service delivery, and maintenance, overhaul, and digital operations. Infrastructure represents the highest capital intensity and the longest asset lifetime.

|

Stage |

Key Participants |

|

Infrastructure Planning & Construction |

National railway authorities, transport ministries, civil engineering contractors, and rail infrastructure developers. |

|

Rolling Stock Manufacturing & Procurement |

Rolling stock manufacturers producing locomotives, metro trains, passenger coaches, freight wagons, and high-speed rail systems. |

|

Track & Signaling Systems Installation |

Rail signaling companies, electrification equipment suppliers, track laying contractors, communication and train control system providers. |

|

Train Operations & Network Management |

Passenger rail operators, freight rail companies, dispatch and traffic management centers. |

|

Passenger & Freight Service Delivery |

Railway service providers offering passenger transportation, intercity transit, urban metro services, freight logistics, ticketing platforms, and multimodal mobility integration solutions. |

|

Maintenance, Overhaul & Digital Operations |

Rail maintenance depots, predictive maintenance technology providers, refurbishment and overhaul facilities, providers of AI-based traffic management, IoT-enabled monitoring systems, automated fare collection, cybersecurity, and predictive analytics. |

The maintenance, overhaul, and digital operations tier is the railroad value chain's highest-margin segment for equipment manufacturers, creating revenue recurrence. Rolling stock manufacturers have progressively transitioned from one-time equipment sales toward long-term service contracts that generate 15-25 year recurring revenue equal to 2-3x the original equipment value over the contract lifetime.

Technology Landscape in the Railroad Industry

Train Control and Signaling Technology

Advanced train control and signaling technologies are improving network safety, operational efficiency, and traffic management capabilities. In February 2023, Delhi Metro launched India's first-ever indigenously developed Train Control & Supervision System, jointly developed by Navratna Defence PSU Bharat Electronics Limited (BEL) & Delhi Metro Rail Corporation (DMRC), the i-ATS (Indigenous - Automatic Train Supervision) for operations on its first corridor, Red Line. These technologies are also supporting real-time monitoring, automated operations, predictive maintenance, and safer high-speed and urban rail transportation networks.

Rolling Stock Traction Technology

Advancements in rolling stock traction technology are improving train efficiency, acceleration, energy consumption, and operational reliability. Modern electric propulsion systems, regenerative braking, lightweight traction motors, battery-electric systems, and hydrogen-powered traction technologies are enabling cleaner and more energy-efficient rail transportation. These innovations are also supporting high-speed rail expansion, lower maintenance costs, and the decarbonization of passenger and freight rail networks.

Predictive Maintenance and AI-Enabled Operations

Predictive maintenance and AI-enabled operations are improving asset reliability, operational efficiency, and network safety through real-time data analytics and automated monitoring systems. AI-driven platforms can identify potential equipment failures in tracks, locomotives, signaling systems, and rolling stock before breakdowns occur, reducing unplanned downtime and maintenance costs. These technologies are also enhancing train scheduling, traffic management, energy optimization, and overall rail network performance.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Passenger Rail |

58.9% |

2025 |

|

Distance |

Long Distance |

54.6% |

2025 |

|

End Use |

🔒 |

🔒 |

2025 |

|

Region |

North America |

32.0% |

2025 |

By Type

Passenger rail leads at 58.9% market share (2025). Passenger rail revenue encompasses ticket sales across urban metro, commuter rail, regional rail, intercity conventional, and high-speed rail. High-speed rail generates the highest revenue per seat-km, making it the most commercially valuable passenger segment despite serving fewer total passengers than urban metro. Urban metro generates the highest passenger volume globally and forms the financial foundation for the Asia Pacific.

To access detailed market analysis, Request Sample

Rail freight at 41.1% is dominated by North America's Class I railroad system, supplemented by European freight rail, Russian Railways freight, and Chinese freight rail.

By Distance

Long distance leads at 54.6% market share (2025). Long-distance rail encompasses freight haul operations above 500 miles, intercity passenger rail on routes above 300 km, and overnight sleeper train services. Long-distance revenue majority reflects the higher per-journey revenue of each trip type. These per-trip revenue levels dwarf short-distance commuter and urban rail trip values, creating a long-distance revenue majority despite potentially lower passenger journey volumes.

Short distance at 45.4% is growing at ~3.4% CAGR through urban transit investment and commuter network expansion. Short distance rail's near-parity with long-distance reflects the enormous volume of urban transit journeys in Asia Pacific's megacities that, despite low per-trip fares, aggregate to significant total revenues through passenger journeys in major systems.

Regional Market Insights

|

Region |

Share (2025) |

Key Railroad Market Drivers & Characteristics |

|

North America |

32.0% |

Supported by extensive freight rail networks, strong intermodal transportation demand, rail infrastructure modernization programs, and increasing investments in digital signaling and operational efficiency technologies. |

|

Asia-Pacific |

28.6% |

Driven by high-speed rail expansion, urban metro development, rising freight transportation demand, and large-scale government investments in rail infrastructure. |

|

Europe |

23.7% |

Characterized by strong policy support for sustainable transportation, cross-border rail connectivity, electrification projects, and increasing investments in low-emission passenger and freight rail systems. |

|

Latin America |

8.1% |

Supported by freight rail modernization, mining and agricultural commodity transportation, metro rail expansion, and infrastructure improvement initiatives across key regional economies. |

|

Middle East and Africa |

7.6% |

Witnessing growth through investments in urban transit systems, high-speed rail corridors, freight connectivity projects, and economic diversification initiatives aimed at strengthening regional transportation infrastructure. |

North America's 32.0% market share is structurally sustained by the Class I freight railroad system's commercial excellence. The IIJA includes $102 billion in total rail funding, including $66 billion from advanced appropriations, and $36 billion in authorized funding is progressively adds passenger rail revenue while leaving freight rail's commercial success unchanged.

Asia-Pacific at 28.6% is the investment growth leader, with China's HSR investment, India's modernization program, and Southeast Asia's metro development collectively representing high annual rail capital spending. Europe, at 23.7%, is the policy leadership region. Latin America, at 8.1%, is led by Brazil's world-class freight rail concessions and growing urban metro investment. The Middle East and Africa, at 7.6%, is the fastest-growing region from a smaller base, driven by GCC transit development and Africa's urbanization-driven metro investment.

Competitive Landscape

The global railroad competitive landscape is uniquely segmented by operator type, geography, and commercial model. National passenger operators compete within their domestic markets for ridership and government funding. North American Class I freight railroads compete for freight traffic in regulated but market-based North American freight rail duopolies and triopolies. Rolling stock manufacturers compete globally for rolling stock contracts that are among the largest single-item public procurement contracts in the world.

|

Company Name |

Operating Region |

Market Position |

Core Strength |

|

Union Pacific |

23 western states of the US |

Market Leader |

Union Pacific's goal is to be the safest railroad in North America. |

|

Deutsche Bahn AG |

Germany and 14 other European Countries |

Strong Challenger |

Deutsche Bahn AG, through its DB Long-Distance, provides passengers with fast, comfortable, and eco-friendly travel within Germany and 14 other European countries. |

|

CSX Corporation |

Eastern United States and two Canadian provinces |

Established Player |

CSX is a leading supplier of rail-based freight transportation in North America. |

|

National Railroad Passenger Corporation |

United States and Canada |

Established Player |

The National Railroad Passenger Corporation, Amtrak, is a corporation striving to deliver a high-quality, safe, on-time rail passenger service that exceeds customer expectations. |

The competitive landscape's defining tension is between cost leadership and Western governments' growing hesitancy about critical infrastructure dependence on Chinese state-owned suppliers.

Key Company Profiles

Union Pacific

Union Pacific is one of the largest railroad companies by revenue and one of the world's most commercially efficient freight railroad operations. The company’s goal is to be the safest railroad in North America.

- Operating Regions: 23 western states of the US.

- Recent Developments: In August 2025, Union Pacific Railroad launched a new, truck-competitive domestic intermodal service connecting Southern California’s Inland Empire to the heart of Chicago, significantly boosting intermodal capacity.

- Strategic Focus: Focused on expanding freight network efficiency, intermodal transportation capabilities, digital rail operations, and infrastructure modernization to strengthen logistics and supply chain connectivity across North America.

Deutsche Bahn AG

Deutsche Bahn AG is Germany's national integrated rail operator and one of Europe's largest railroad companies by revenue.

- Operating Regions: Germany and 14 Other European Countries.

- Recent Developments: In January 2026, Deutsche Bahn launched an immediate action programme aimed at improving safety and cleanliness at train stations across Germany.

- Strategic Focus: Focused on sustainable rail transportation, digital network modernization, high-speed passenger connectivity, and the expansion of low-emission freight and mobility solutions across Europe.

Market Concentration Analysis

The global railroad market exhibits distinctive concentration patterns by segment. North American Class I freight railroad operations are highly concentrated. European passenger rail is increasingly competitive, with national incumbents facing growing open-access competition. Rolling stock manufacturing is moderately concentrated globally. Market concentration in rolling stock supply is politically contested in Western markets, and growing EU concerns about Chinese rolling stock create artificial market segmentation. The protectionist trend is instead sustaining Western rolling stock manufacturers at a higher cost per unit but preserving domestic industrial capacity and supply chain independence that governments consider strategically valuable.

Investment & Growth Opportunities

Highest Growth Segments

Passenger Rail (~3.4% CAGR), short distance urban transit (~3.4% CAGR), hydrogen and battery train rolling stock (~20-25% CAGR from small base), digital signaling systems (ETCS/ERTMS deployment ~8-12% CAGR), and rail maintenance services and predictive maintenance subscription platforms (~6-8% CAGR) represent the global railroad market's highest-growth investment vectors.

Emerging Investment Opportunities

The African rail market represents the largest greenfield rail investment opportunity globally for 2026-2034. Africa has the world's lowest rail penetration relative to population, and its projected high urban population growth by 2034 will create transit demand for metro and commuter rail systems in cities that currently have no rail transit.

Investment Themes

- High-speed rail corridor development in emerging markets creating rolling stock and systems market through 2034: First-mover technology partnerships create long-term supply relationships that generate fleet expansion, spare parts, and maintenance contract revenue streams 2-5x original procurement value over 30-year operational lifetimes.

- Rail freight intermodal network investment for North American and European modal shift to decarbonize supply chains: Each new intermodal terminal in North America enables high annual TEU to shift from truck to rail, reducing transport emissions 75% and transport cost 15-25% for shippers with appropriate origin-destination pairs.

Future Market Outlook (2026-2034)

The global railroad market is projected to grow from USD 343.8 Billion in 2025 to USD 462.3 Billion by 2034, delivering a 3.24% CAGR over the forecast period. The market's anchor value of USD 403.4 Billion in 2030 represents a global railroad industry where China's HSR network has crossed 70,000 km making it twice the length of all other national HSR networks combined, India's Vande Bharat network has established semi-high-speed passenger rail as the standard for Indian intercity travel on electrified routes, North America's IIJA-funded Amtrak expansion has added new US city pairs to the national passenger rail network, and spanning freight railroad is demonstrating the commercial potential of cross-border integrated freight rail operations. Three structural forces define global railroad market growth through 2034 with high confidence: climate policy irreversibility, urbanization-driven transit demand, and energy and freight economics.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including VP of Strategy and Commercial directors; Chief Operating Officers and Network Planning directors; rail infrastructure directors; signaling technology directors; and rail policy and regulatory specialists.

Secondary Research

Secondary research encompassed UIC (International Union of Railways) World Rail Statistics 2025; AAR (Association of American Railroads) Railroad Facts 2025; European Commission Rail Market Monitoring (RMMS) 2024; individual company annual reports and investor presentations; UITP Global Metro Ridership Statistics; European Commission Connecting Europe Facility rail investment data; IEA Transport and Energy 2025; Infrastructure Investor Rail Sector Review 2025; Railway Gazette International market data. Over 70 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using top-down and bottom-up models calibrated against World Rail Statistics historical revenue data series, AAR Class I railroad freight revenue tracking, European rail market monitoring data, regional rail investment pipeline data, and GDP-linked rail demand elasticity models. Key inputs include World Economic Outlook GDP projections by country, urban population growth by region, rail modal share targets by policy jurisdiction, rolling stock fleet age and replacement cycle data, and infrastructure investment program commitment data from national transport ministries.

Railroad Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Rail Freight, Passenger Rail |

| Distances Covered | Long Distance, Short Distance |

| End Uses Covered | Mining, Construction, Agriculture, and Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Union Pacific, Deutsche Bahn AG, CSX Corporation, National Railroad Passenger Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the railroad market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global railroad market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the railroad industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Railroad Market Report

The global railroad market reached USD 343.8 Billion in 2025, driven by North America's world-leading Class I freight railroad revenues, China's expanding HSR network, India's National Rail Plan investment, European Green Deal passenger rail expansion, and Asia Pacific's urban metro and commuter rail capital investment programs.

The market grows at 3.24% CAGR during 2026-2034, reaching USD 462.3 Billion by 2034, driven by Asia Pacific's urban transit investment, European HSR and commuter rail capacity expansion under the Green Deal, North American IIJA-funded service growth, India's Vande Bharat and HSR programs, digital signaling capacity enhancement, and hydrogen and battery train fleet growth enabling rail expansion on non-electrified networks.

Passenger rail leads at 58.9% through urban metro, regional, and high-speed rail services, collectively generating higher total revenues than freight despite freight's dominance in North America.

Long distance leads at 54.6% through North America's Class I railroad long-haul freight dominance, global HSR premium intercity revenue, and overnight sleeper train revenues.

North America leads at 32.0% through the unique commercial model of privately-owned Class I freight railroads generating high freight revenues without government subsidy, supplemented by IIJA-funded Amtrak passenger rail renaissance.

Leading companies include Union Pacific, Deutsche Bahn AG, CSX Corporation, and National Railroad Passenger Corporation, among others.

The market is projected to reach approximately USD 403.4 Billion by 2030, with China's HSR network growth, India's Mumbai-Ahmedabad HSR approaching commercial operation, US IIJA-funded expansion adding new city pairs, and hydrogen train deployments growth.

Precision Scheduled Railroading (PSR) is the operating methodology that transformed North American freight railroad economics, running fixed-schedule trains with reduced locomotive and car inventory, eliminating excess classification yards, and requiring strict customer placement/pull times.

Three priority opportunities: HSR corridor development in emerging markets, creating high rolling stock and systems procurement through 2034, first-mover technology partnerships generate 30-year supply relationships valued at 3-5x initial procurement; ETCS digital signaling deployment; and rail freight intermodal terminal investment and DAC European freight wagon digitalization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)