Real Time Location System Market Size, Share, Trends and Forecast by Component, Application, Vertical, and Region 2026-2034

Global Real Time Location System Market Size, Share, Trends & Forecast (2026-2034)

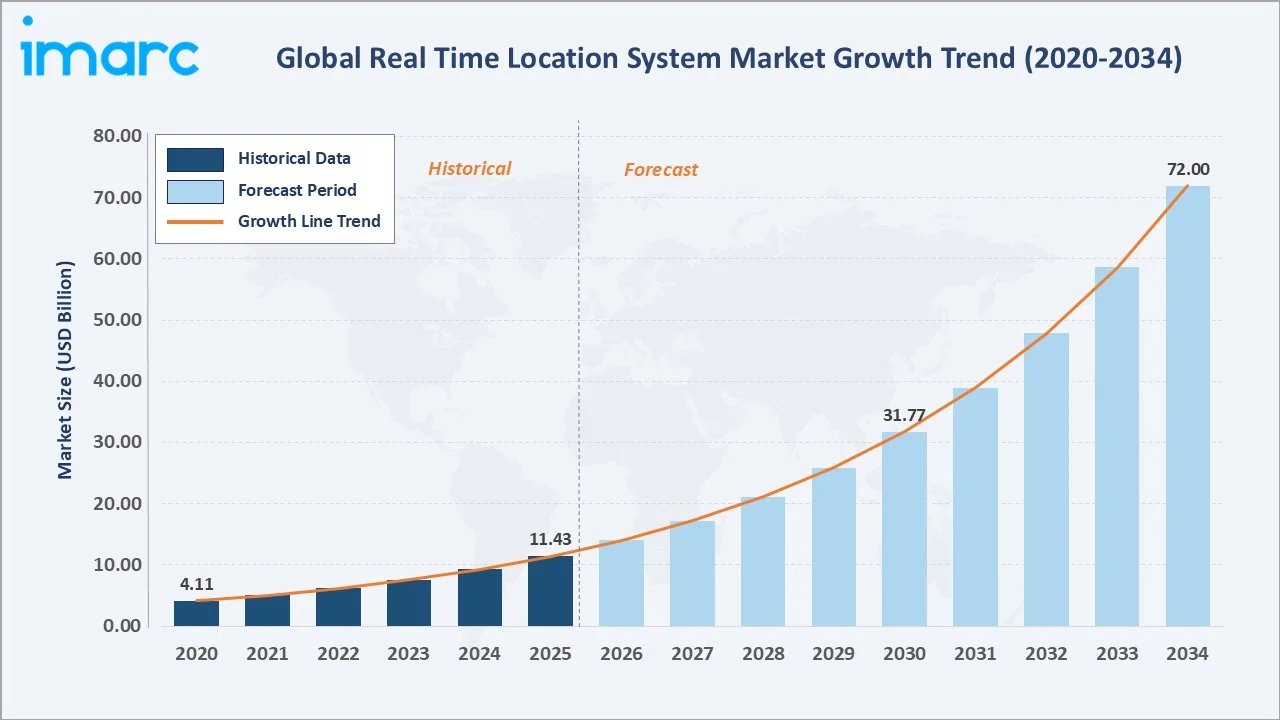

The global real time location system (RTLS) market size was valued at USD 11.4 Billion in 2025 and is projected to reach USD 72.0 Billion by 2034, exhibiting a CAGR of 22.69% during the forecast period 2026-2034. Accelerating IoT adoption, smart-building integration, and heightened demand for real-time asset visibility across healthcare, manufacturing, and logistics are driving RTLS market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.4 Billion |

|

Forecast Market Size (2034) |

USD 72.0 Billion |

|

Market Size (2030) |

USD 31.8 Billion |

|

CAGR (2026-2034) |

22.69% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

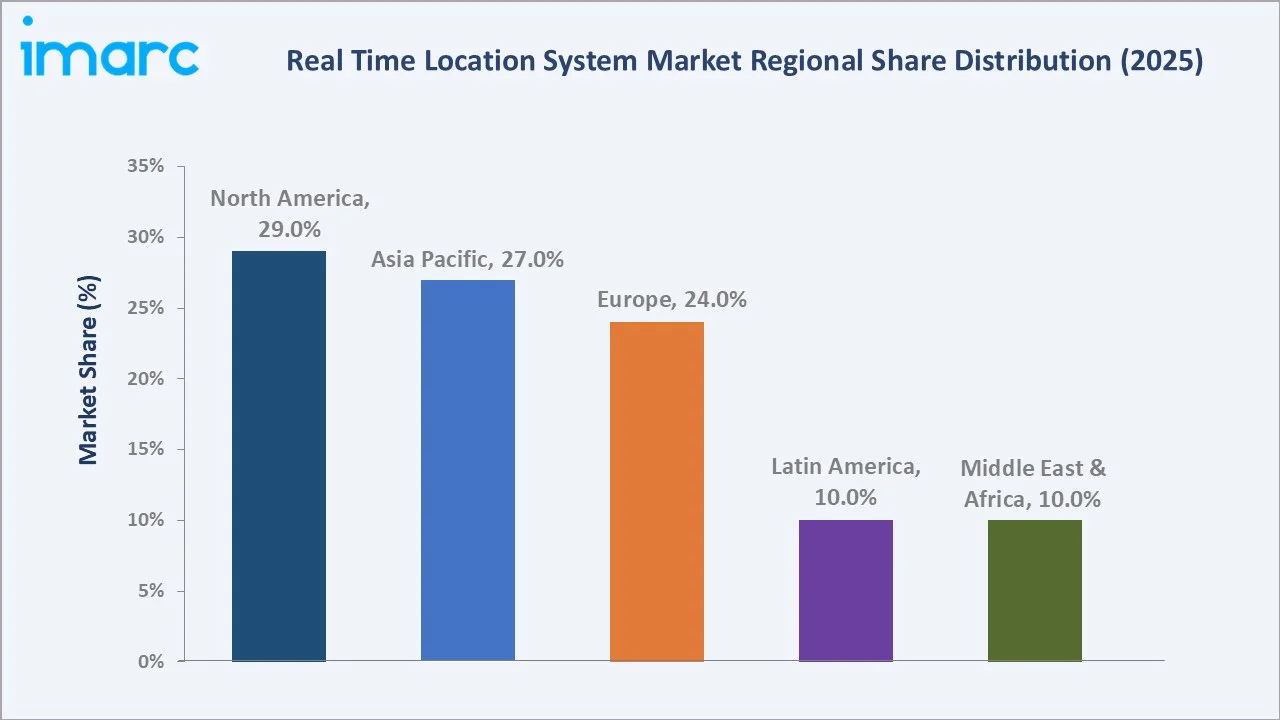

Largest Region (2025) |

North America (29%) |

|

Fastest Growing Region |

Asia Pacific |

|

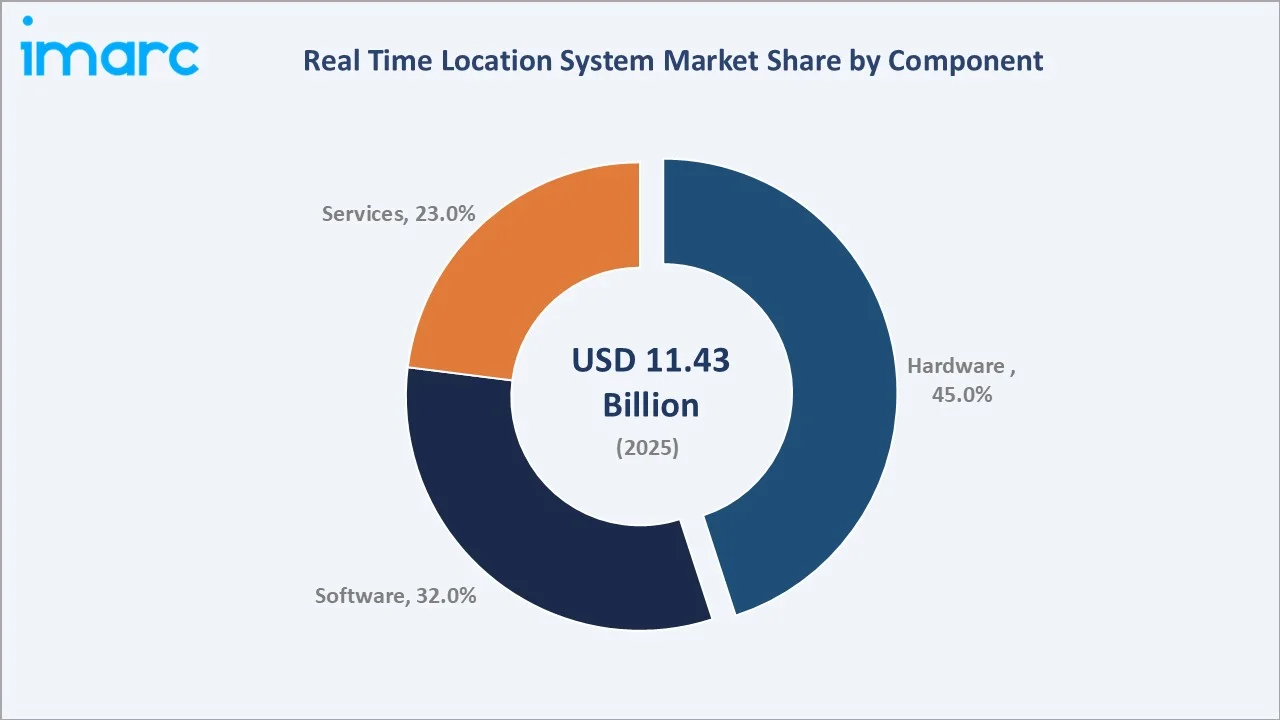

Leading Component (2025) |

Hardware (45%) |

|

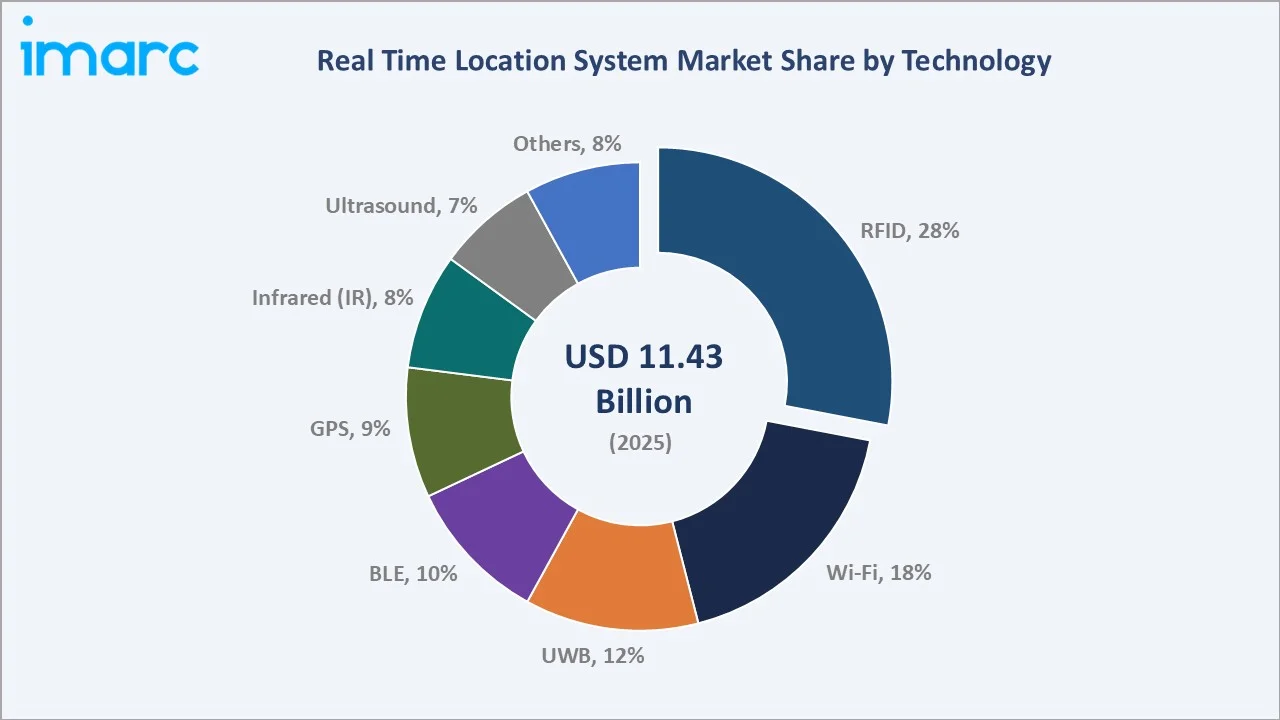

Leading Technology (2025) |

RFID (28%) |

The chart below illustrates the global RTLS market growth trajectory from 2020 through 2034, contrasting historical expansion against a robust forecast curve powered by smart infrastructure, Industry 4.0 adoption, and expanding RTLS use cases across high-growth verticals.

To get more information on this market, Request Sample

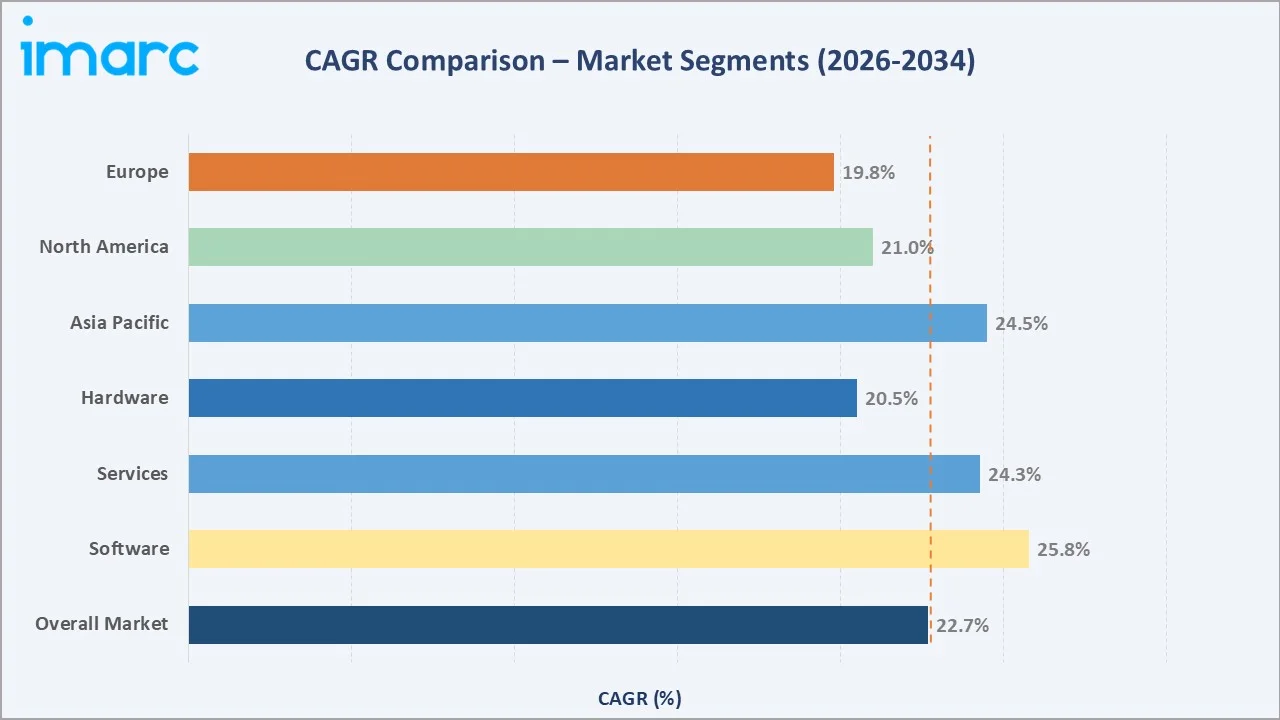

Segment and regional CAGR comparisons below highlight software and Asia Pacific as the fastest-growing sub-categories within the global RTLS market forecast through 2034.

Executive Summary

The global RTLS market is undergoing a structural transformation, driven by Industry 4.0 integration, smart-building expansion, and heightened operational visibility requirements across multiple verticals. Valued at USD 11.4 Billion in 2025, the market is forecast to reach USD 72.0 Billion by 2034, delivering one of the highest CAGRs in the technology sector at 22.69%.

Hardware dominates with a 45% component share in 2025, underpinned by growing demand for RFID readers, UWB anchors, and BLE beacons. Software is the fastest-growing component, advancing at an estimated CAGR of ~25.8% through 2034, as enterprises increasingly invest in analytics dashboards, middleware platforms, and AI-integrated location engines.

North America holds a 29% revenue share in 2025, anchored by high RTLS penetration in U.S. hospitals, distribution centres, and defence installations. Asia Pacific, with a 27% share, is the fastest-growing region, driven by China's smart-factory expansion and India's emerging healthcare and logistics infrastructure.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Hardware – 45% share (2025) |

|

Second Component |

Software – 32% share (2025) |

|

Leading Technology |

RFID – 28% share (2025) |

|

Fastest Growing Technology |

UWB – ~30%+ CAGR (2026-2034) |

|

Dominant Region |

North America – 29% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – ~24.5% CAGR (2026-2034) |

|

Top Companies |

Zebra Technologies, Impinj, Stanley Healthcare, Honeywell, Ubisense, CenTrak, Trimble, Sewio Networks, Quuppa, and Infsoft |

|

Key Application |

Inventory/Asset Tracking & Management |

|

Market Opportunity |

Smart hospital infrastructure |

Key Analytical Observations Supporting The Above Data:

- Hardware's 45% dominance in 2025 reflects expanding deployments of RFID reader infrastructure, UWB positioning anchors, and BLE beacon networks across hospitals, warehouses, and manufacturing plants globally.

- Software's 32% share is growing fastest as enterprises invest in real-time dashboards, AI-powered analytics engines, and middleware solutions that translate location data into actionable operational insight.

- RFID's 28% technology leadership stems from its cost-scalability in large-area tracking environments, including retail stockrooms, distribution centres, and airport baggage systems handling billions of items annually.

- North America’s 29% market dominance is driven by early adoption of RTLS in U.S. healthcare, where approximately 6,100 hospitals had active RTLS infrastructure as of 2024, largely supported by compliance requirements from Joint Commission accreditation.

- Asia Pacific's 27% share and highest growth are underpinned by China's smart-factory expansion under the 'Made in China 2025' initiative and India boosted semiconductor ambitions via Semicon India program (Dec 2021), allocating Rs. 76,000 crore (US$ 8.79 billion).

- UWB's rapid ascent positions it as the precision-tracking technology of choice for applications requiring sub-30 cm accuracy, including surgical equipment tracking in operating theatres and autonomous mobile robot guidance in Industry 4.0 plants.

Global Real Time Location System Market Overview

Real time location systems are technology platforms that continuously determine and communicate the precise geographic position of objects, assets, or personnel in real time within a defined area. RTLS integrates hardware components such as tags, readers, and anchors with software platforms to deliver location data streams used for operational optimization, safety compliance, and supply chain visibility.

The industry spans a broad application ecosystem including inventory and asset tracking in warehouses, patient and staff safety monitoring in hospitals, access control and security in restricted facilities, and autonomous vehicle guidance in smart factories.

Market Dynamics

To evaluate market opportunities, Request Sample

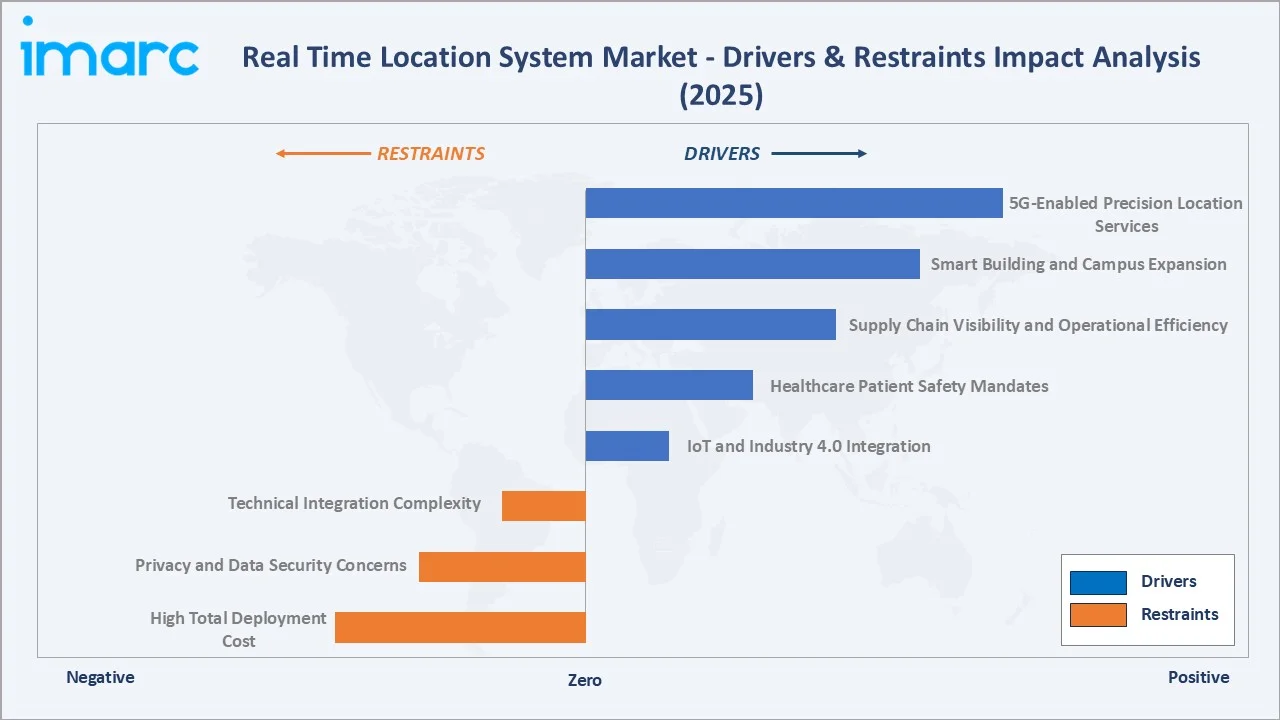

Market Drivers

- IoT and Industry 4.0 Integration: Number of connected IoT devices growing 14% to 21.1 billion globally as of 2025. Smart manufacturing deployments are embedding RTLS as a core visibility layer, enabling autonomous material flow tracking and real-time equipment utilisation dashboards in automated plants.

- Healthcare Patient Safety Mandates: Healthcare represents the single largest RTLS vertical. Over 6,100 U.S. hospitals have deployed active RTLS infrastructure, driven by Joint Commission standards requiring real-time tracking of crash carts, infusion pumps, and ventilators. Patient elopement prevention and infant protection systems are generating recurring upgrade demand across North American and European hospital networks.

- Supply Chain Visibility and Operational Efficiency: Global e-commerce revenue projected to grow from 4.12 trillion USD in 2024 to 6.49 trillion USD by 2029, driving warehouse operators to deploy RTLS for real-time forklift tracking, dock scheduling, and inventory cycle-count automation. Distribution centres report 20-35% reduction in asset search time following RTLS deployment.

- Smart Building and Campus Expansion: Building management systems increasingly integrate RTLS for occupancy-based energy management, space utilization analytics, and emergency evacuation, expanding its application beyond traditional industrial sectors.

Market Restraints

- High Total Deployment Cost: Enterprise-grade RTLS deployments require substantial upfront investment, including infrastructure setup, large-scale tag procurement, and software licensing, which can limit adoption among smaller healthcare facilities and SME manufacturers.

- Privacy and Data Security Concerns: Personnel tracking raises workforce privacy concerns, especially in regions with strict data protection regulations. Organizations must implement consent frameworks and data minimization protocols, increase compliance requirements and slowing internal approval processes for RTLS projects.

- Technical Integration Complexity: Integrating RTLS data with legacy ERP, WMS, and CMMS systems remains complex, as interoperability gaps between vendor ecosystems increase costs and extend deployment timelines.

Market Opportunities

- 5G-Enabled Precision Location Services: 5G's sub-millisecond latency and network slicing capability enable carrier-grade RTLS services at scale. Telecoms including Verizon and Ericsson are commercialising 5G-native positioning solutions targeting smart stadium, campus, and industrial park deployments through 2030.

- Emerging Market Healthcare Infrastructure Build-Out: India’s Ayushman Bharat Digital Mission is driving large-scale healthcare digitisation, while expanding hospital infrastructure across Southeast Asia is creating significant opportunities for RTLS adoption in patient safety and asset management.

- Autonomous Robotics and Industry 4.0 Convergence: Autonomous mobile robots (AMRs) in warehouses and factories require centimetre-level positioning, positioning UWB-based RTLS as a critical navigation backbone and driving strong recurring demand for hardware.

Market Challenges

- Multi-Vendor Ecosystem Fragmentation: The RTLS market lacks a universal interoperability standard. Vendor lock-in concerns delay procurement decisions as enterprises struggle to evaluate total cost of ownership across proprietary hardware and software ecosystems.

- RF Signal Interference in Complex Environments: Dense industrial environments with metallic structures and high electromagnetic interference significantly degrade Wi-Fi and BLE-based RTLS accuracy, requiring expensive signal-mapping and calibration exercises that increase deployment time and cost.

Emerging Market Trends

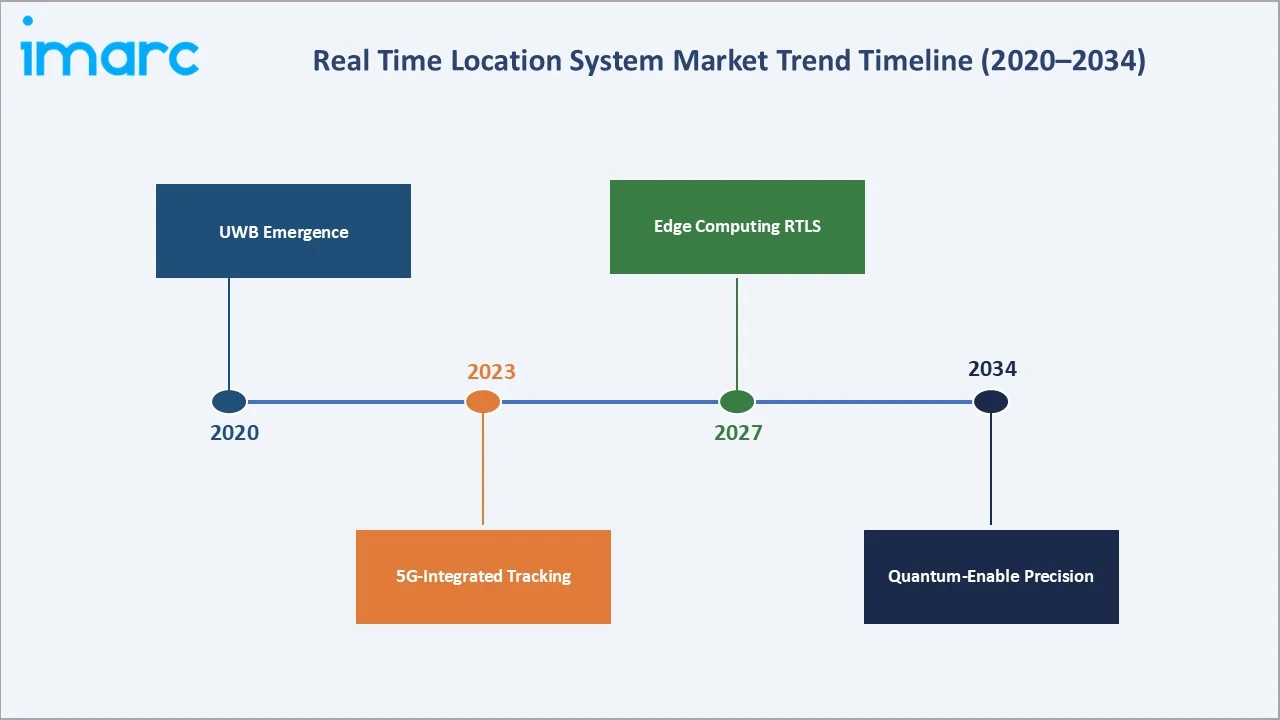

1. Ultra-Wideband (UWB) Technology Adoption Surge

UWB-based RTLS is rapidly gaining adoption due to its ability to deliver sub-30 cm positional accuracy - a tenfold improvement over BLE and Wi-Fi alternatives. Apple's AirTag platform and the global iPhone 11+ installed base have accelerated UWB chip economies of scale. Industrial and healthcare buyers are increasingly standardising on UWB for high-value asset tracking and autonomous robotics guidance.

2. AI and Machine Learning-Augmented Location Analytics

Next-generation RTLS platforms are integrating AI/ML engines to transform raw location data streams into predictive operational insights. Applications include predictive maintenance triggered by unusual equipment location patterns, patient flow optimization in hospital emergency departments, and demand-driven inventory positioning in distribution centres.

3. Digital Twin Integration for Location Intelligence

The integration of RTLS with building information modelling (BIM) and digital twin platforms is emerging as a high-value enterprise capability. Real-time location feeds from RTLS systems animate live digital twins of hospital floors, factory layouts, and airport terminals, enabling simulation-based scenario planning. Siemens, IBM, and Microsoft Azure Digital Twins are actively developing RTLS data connectors for this converging market.

4. Wearable RTLS Tags for Workforce Safety Compliance

Occupational safety regulation is expanding RTLS beyond asset tracking into worker safety. Wearable RTLS tags with SOS alerts, fall detection, and proximity warnings are being mandated in mining, oil & gas, and construction sectors.

5. Cloud-Hosted RTLS-as-a-Service (RTLSaaS) Platforms

Subscription-based RTLS platforms are lowering the entry barrier for SME and mid-market adopters unable to justify large upfront capital expenditures. Cloud-hosted RTLSaaS eliminates on-premise server infrastructure and shifts procurement to OpEx models.

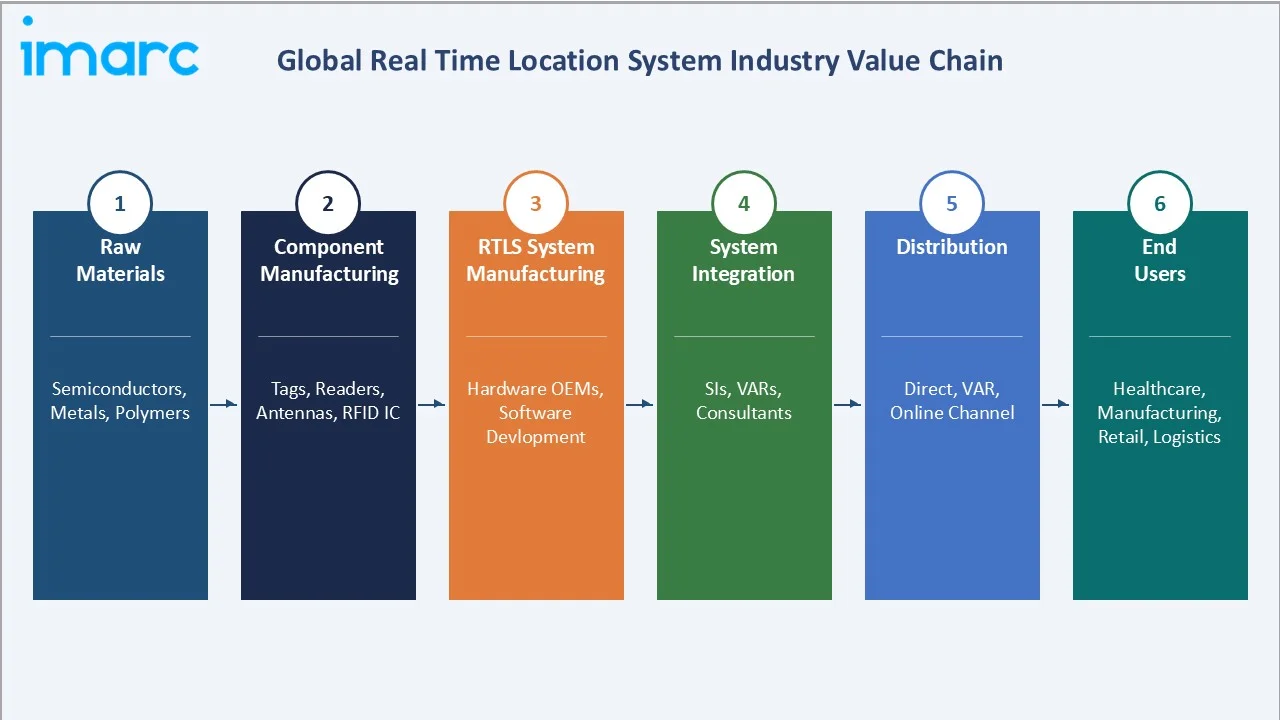

Industry Value Chain Analysis

The global RTLS industry value chain spans six integrated stages, from raw material supply through end-user deployment. Each stage presents distinct competitive dynamics and technology requirements relevant to the overall RTLS market analysis.

|

Stage |

Key Players / Description |

|

Raw Materials |

Semiconductor foundries (TSMC, Samsung), specialty metal suppliers, polymer resin producers |

|

Component Manufacturing |

RFID IC suppliers (NXP, Impinj), UWB chip makers (Decawave/Qorvo), antenna manufacturers |

|

RTLS System Manufacturing |

OEM hardware (Zebra, Honeywell, CenTrak); RTLS software platforms (Ubisense, Sewio, Quuppa) |

|

System Integration |

IT SIs (Accenture, IBM, Deloitte), specialist RTLS integrators, healthcare IT consultants |

|

Distribution & Sales |

VAR networks, direct enterprise sales teams, online B2B channels, RTLS-as-a-Service providers |

|

End Users |

Healthcare systems, manufacturing & automotive OEMs, retail chains, logistics & transport operators, government & defence |

Technology Landscape in the Real Time Location System Industry

RFID and UWB – Dominant Technology Layers

RFID remains the foundational technology with a 28% market share in 2025. Passive UHF RFID delivers cost-efficient area-level tracking at scale, while active RFID provides real-time location updates with greater range. UWB is the fastest-growing technology, offering sub-30 cm accuracy for precision-critical applications including surgical equipment tracking and AMR navigation.

AI and Edge Computing Integration

Edge computing-enabled RTLS gateways are eliminating cloud latency by processing location calculations locally. AI-layer integration adds predictive analytics and anomaly detection to location data streams, expanding RTLS value beyond operational visibility.

5G and Wi-Fi 6/6E Connectivity

Wi-Fi 6E (6 GHz band) significantly improves RTLS accuracy through reduced channel congestion and time-of-flight measurement improvements, bringing sub-metre accuracy to Wi-Fi-based systems. 5G's native positioning services (Rel-16 NR Positioning) will deliver 3-metre accuracy outdoors and integrate seamlessly with carrier-managed smart campus deployments, opening large-venue and campus-wide RTLS at carrier-grade reliability by 2027-2028.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | Hardware | 45% | 2025 |

| Technology | RFID | 28% | 2025 |

| Application | Inventory/Asset-Tracking & Management | 26% | 2025 |

| Vertical | Healthcare | 22% | 2025 |

| Region | North America | 29% | 2025 |

By Component

Hardware dominates the RTLS market with a 45% share in 2025. RFID readers, UWB anchors, BLE gateways, and passive/active tags constitute the core hardware layer, with tag volume being the largest unit-cost driver. Software accounts for 32% of the market, driven by enterprise demand for real-time dashboards, location analytics platforms, workflow automation middleware, and AI-powered location intelligence engines.

To access detailed market analysis, Request Sample

By Technology

RFID leads the technology segment with a 28% share in 2025. Wi-Fi-based RTLS accounts for 18%, benefitting from existing infrastructure in most enterprise environments. UWB holds 12% and is the fastest-growing technology. BLE commands 10%, finding strong adoption in healthcare and retail beacon networks. GPS (9%), Infrared (8%), Ultrasound (7%), and other emerging technologies account for the remaining market share.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Players |

|

North America |

29% |

Hospital RTLS mandates, U.S. DoD asset tracking, warehouse automation, smart campus |

Zebra, Honeywell, Stanley Healthcare, Trimble |

|

Asia Pacific |

27% |

China smart-factory expansion, India healthcare build-out, ASEAN logistics growth |

Zebra APAC, local integrators, Baidu RTLS |

|

Europe |

24% |

GDPR-compliant personnel tracking, Industrie 4.0, smart airport deployments |

Ubisense, Sewio, Infsoft, Quuppa |

|

Latin America |

10% |

Brazil healthcare modernisation, mining sector safety compliance, logistics digitisation |

Regional integrators, Zebra LAT |

|

Middle East & Africa |

10% |

Saudi Vision 2030 smart city projects, UAE smart hospital mandates, African mining safety |

Honeywell, regional SIs |

North America commands the largest regional share at 29% in 2025. The U.S. healthcare sector alone drives significant RTLS demand. Defense infrastructure programs in the U.S. are increasingly incorporating RTLS across military bases and logistics depots, while e-commerce warehouse automation is driving strong demand for real-time forklift and inventory tracking solutions across the region.

Asia Pacific holds a 27% market share and represents the fastest-growing region, driven by China's 'Made in China 2025' smart manufacturing initiative. Japan's high-precision automotive manufacturing and South Korea's semiconductor fab expansion are generating significant UWB and RFID RTLS demand.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Zebra Technologies |

Zebra RTLS, MotionWorks |

Leader |

Broad hardware portfolio, healthcare & logistics depth |

|

Impinj |

Impinj RAIN RFID |

Leader |

RFID reader chip leadership, RAIN ecosystem |

|

Stanley Healthcare |

AeroScout, Hugs |

Leader |

Healthcare-specific RTLS, infant security |

|

Honeywell |

Honeywell Forge RTLS |

Leader |

Industrial IoT integration, global distribution |

|

Ubisense |

SmartSpace, DIMENSION4 |

Challenger |

UWB precision, automotive manufacturing |

|

CenTrak |

CenTrak RTLS |

Challenger |

Clinical-grade healthcare RTLS |

|

Trimble |

Trimble RTLS |

Challenger |

Outdoor & mixed-environment tracking |

|

Sewio Networks |

Sewio UWB RTLS |

Emerging |

European UWB precision, SME-friendly |

|

Quuppa |

Quuppa Intelligent Locating |

Emerging |

BLE angle-of-arrival accuracy, SDK ecosystem |

|

Infsoft |

Infsoft RTLS Platform |

Emerging |

SaaS indoor positioning, flexible integration |

The RTLS competitive landscape is moderately fragmented, with global technology conglomerates competing alongside specialist vendors and emerging SaaS-native platforms. Leading players compete on location accuracy, vertical-specific certifications, cloud platform integration, and total cost of ownership. Strategic acquisitions are reshaping the market.

Key Company Profiles

Zebra Technologies

Zebra Technologies is a global leader in enterprise-grade RTLS hardware and software, headquartered in Lincolnshire, Illinois, USA. The company serves over 10,000 enterprise clients across healthcare, retail, manufacturing, and transportation, with operations in 100+ countries.

- Product & Platform Portfolio: Zebra's RTLS portfolio includes MotionWorks Enterprise for real-time asset location, RFID readers and UHF RAIN RFID infrastructure, wearable worker safety tags, and the Zebra Savanna cloud data intelligence platform that processes over 100 billion data reads annually.

- Recent Developments: In 2022, Zebra Technologies expanded its autonomous mobile robotics integration capabilities through its Fetch Robotics subsidiary, enabling simultaneous AMR guidance and RTLS asset tracking within shared warehouse environments.

- Strategic Focus: Zebra's strategy centres on deepening vertical software capabilities, expanding its SaaS recurring revenue base, and integrating RTLS with autonomous robotics to provide end-to-end warehouse intelligence solutions.

Impinj

Impinj, headquartered in Seattle, Washington, is the global leader in RAIN RFID technology. The company's platform connects billions of physical items to the internet, enabling real-time inventory visibility across retail, healthcare, and supply chain environments.

- Product & Platform Portfolio: Impinj's product ecosystem includes the Impinj M700 and M800 endpoint IC series (the world's best-selling RFID chips), Speedway and xSpan fixed-infrastructure RFID readers, and the Impinj platform cloud connectivity layer enabling enterprise-scale item intelligence.

- Recent Developments: In 2025, Impinj has introduced three new Gen2X innovations aimed at enhancing RFID performance. The company has also integrated Gen2X support into its M770 and M780 endpoint ICs, expanding applications across logistics, manufacturing, automotive, and healthcare.

- Strategic Focus: Impinj's strategic focus is expanding the RAIN RFID ecosystem through semiconductor innovation, cloud platform monetisation, and growing enterprise software revenue from its Impinj platform as recurring ARR.

Honeywell

Honeywell is a diversified technology and manufacturing company headquartered in the U.S., operating across aerospace, building technologies, performance materials, and safety & productivity solutions. The company is a key player in industrial digitalization, automation, and connected enterprise platforms.

- Product & Platform Portfolio: Honeywell Forge RTLS integrates with building management systems, industrial IoT platforms, and ERP systems to deliver unified operational visibility. Products span BLE and Wi-Fi RTLS hardware, cloud analytics, and AI-powered operational dashboards targeting manufacturing, airports, and commercial buildings.

- Recent Developments: In 2023, Honeywell announced the expansion of its Honeywell Forge for Buildings platform to include native RTLS capabilities for space utilisation and emergency management across its global smart building customer base of commercial facilities.

- Strategic Focus: Honeywell's RTLS strategy is anchored in enterprise software integration, leveraging its global industrial IoT platform to position RTLS as an embedded capability within broader operational intelligence solutions for manufacturing and facility management clients.

Market Concentration Analysis

The global RTLS market exhibits moderate fragmentation. The top five players include Zebra Technologies, Impinj, Stanley Healthcare, Honeywell, Ubisense, CenTrak, collectively account for approximately 35-42% of global RTLS market revenue in 2025. The remaining market share is distributed across specialist vendors, regional systems integrators, and technology conglomerates with RTLS as an embedded capability.

The market is experiencing bifurcated concentration dynamics. At the premium enterprise tier, consolidation is accelerating around vertically specialised platforms, AI integration capability, and SaaS recurring revenue models. Healthcare and automotive verticals exhibit higher concentration given clinical certification and precision accuracy requirements that create significant barriers to entry.

Investment & Growth Opportunities

Fastest-Growing Segments

Software is the highest-growth component sub-segment at approximately 25.8% CAGR through 2034, driven by AI platform adoption, digital twin integration, and RTLSaaS subscription model expansion. UWB is the fastest-growing technology at an estimated 30%+ CAGR, as precision applications in autonomous robotics and healthcare proliferate.

Emerging Market Expansion

India represents a high-potential emerging market, driven by government-led logistics modernization and healthcare digitization initiatives. Meanwhile, expanding hospital infrastructure in Southeast Asia, large-scale smart city developments in the Middle East, and increasing safety compliance requirements in Sub-Saharan Africa are collectively creating strong growth opportunities for RTLS adoption.

Venture and Strategic Investment Trends

Investment in RTLS platforms has accelerated significantly, with strong funding directed toward UWB-focused startups, AI-driven analytics, and RTLS-as-a-service solutions. Key innovation areas include edge-enabled gateways, worker safety wearables, digital twin integration, and 5G-based positioning, while M&A activity continues as major technology players acquire specialized vendors to strengthen capabilities and recurring revenue streams.

Future Market Outlook (2026-2034)

The global RTLS market forecast projects sustained value expansion from USD 11.4 Billion in 2025 to USD 72.0 Billion by 2034 at a CAGR of 22.69%. North America will retain regional leadership while Asia Pacific accelerates structurally. Healthcare and manufacturing verticals will anchor demand, while smart-building and retail sectors represent the highest incremental growth opportunity.

Three key shifts will reshape the RTLS market through 2034. First, UWB will displace RFID as the dominant precision-tracking technology in high-value applications by approximately 2029,

Second, AI-native RTLS platforms will commoditise basic location tracking and shift competition toward predictive operational intelligence. Third, 5G-native positioning services will open massive new RTLS addressable markets in outdoor campuses, smart cities, and carrier-managed industrial parks, potentially doubling the serviceable market by 2032-2034.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with RTLS industry stakeholders, including product directors at RTLS OEM manufacturers, CIOs at large hospital systems, procurement managers at automotive assembly plants, logistics operations directors, and institutional investors in industrial IoT platforms. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and pricing benchmarks.

Secondary Research

Secondary sources include IoT Analytics annual IoT market tracker, Ericsson Mobility Reports, WHO Global Health Infrastructure database, U.S. Department of Defense asset management publications, IEEE 802.15.4z UWB standardisation documentation, company annual reports, trade publications including RFID Journal, Healthcare IT News, and Logistics Management, and regional construction association databases covering hospital and smart-factory project pipelines.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating enterprise IoT spending indices, vertical-sector GDP correlators, RTLS hardware unit pricing curves, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for technology adoption uncertainty and macroeconomic variability.

Real Time Location System Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Coverage | Hardware, Software, Services |

| Technologies Coverage | RFID, Wi-Fi, UWB, BLE, Infrared (IR), Ultrasound, GPS, Others |

| Applications Coverage | Inventory/Asset-Tracking and Management, Personnel/Staff-Locating And Monitoring, Access Control/Security, Environmental Monitoring, Yard, Dock, Fleet Warehouse-Management And Monitoring, Supply Chain Management And Operational Automation/ Visibility, Others |

| Verticals Coverage | Healthcare, Manufacturing and Automotive, Retail, Transportation and Logistics, Government and Defense, Education, Oil and Gas, Mining, Sports and Entertainment, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Argentina, Colombia, Chile, Peru, Turkey, Saudi Arabia, Iran, United Arab Emirates |

| Companies Covered | Zebra Technologies, Impinj, Stanley Healthcare, Honeywell, Ubisense, CenTrak, Trimble, Sewio Networks, Quuppa, Infsoft, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the real time location system market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global real time location system market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the real time location system industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Real Time Location System Market Report

The global real time location system market was valued at USD 11.4 Billion in 2025, driven by IoT adoption, healthcare asset tracking mandates, and expanding smart manufacturing deployments worldwide.

The market is projected to reach USD 72.0 Billion by 2034, growing at a CAGR of 22.69% during 2026-2034, supported by UWB adoption, AI-integrated platforms, and 5G-enabled positioning services.

Hardware leads with a 45% share in 2025, driven by RFID reader infrastructure, UWB anchor deployments, and growing BLE beacon network installations across healthcare and industrial verticals.

UWB is the fastest-growing technology, estimated to advance at over 30% CAGR through 2034, driven by sub-30 cm accuracy requirements in autonomous robotics, healthcare, and automotive manufacturing.

North America holds the largest regional share at 29% in 2025, anchored by U.S. hospital RTLS deployments, defence asset tracking, and e-commerce warehouse automation investments.

The global RTLS market is projected to reach USD 31.8 Billion in 2030, representing a near-tripling from 2025 levels, driven by sustained enterprise digitisation and expanding vertical adoption.

Key drivers include IoT and Industry 4.0 adoption, healthcare patient safety regulations, supply chain visibility mandates, smart building expansion, and UWB technology maturation reducing deployment costs.

Major players include Zebra Technologies, Impinj, Stanley Healthcare, Honeywell, Ubisense, CenTrak, Trimble, Sewio Networks, Quuppa, and Infsoft.

RFID leads at 28%, followed by Wi-Fi at 18%, UWB at 12%, BLE at 10%, GPS at 9%, Infrared at 8%, Ultrasound at 7%, and other technologies accounting for 8% collectively.

Asia Pacific is the fastest-growing region, driven by China's smart-factory expansion, India's logistics policy investments, and rapid healthcare infrastructure growth across Southeast Asia.

Key opportunities include AI-native RTLS platform development, UWB-based autonomous robotics integration, healthcare RTLS in emerging markets, RTLSaaS subscription platforms, and 5G-enabled campus positioning services.

RTLS-as-a-Service is a subscription-based delivery model eliminating upfront capital barriers, estimated to grow at approximately 28% CAGR through 2030, expanding adoption among SMEs and mid-market enterprises.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)