Japan Lubricants Market Size, Share, Trends and Forecast by Product Type, End User, and Region, 2026-2034

Japan Lubricants Market Size, Share, Trends & Forecast (2026-2034)

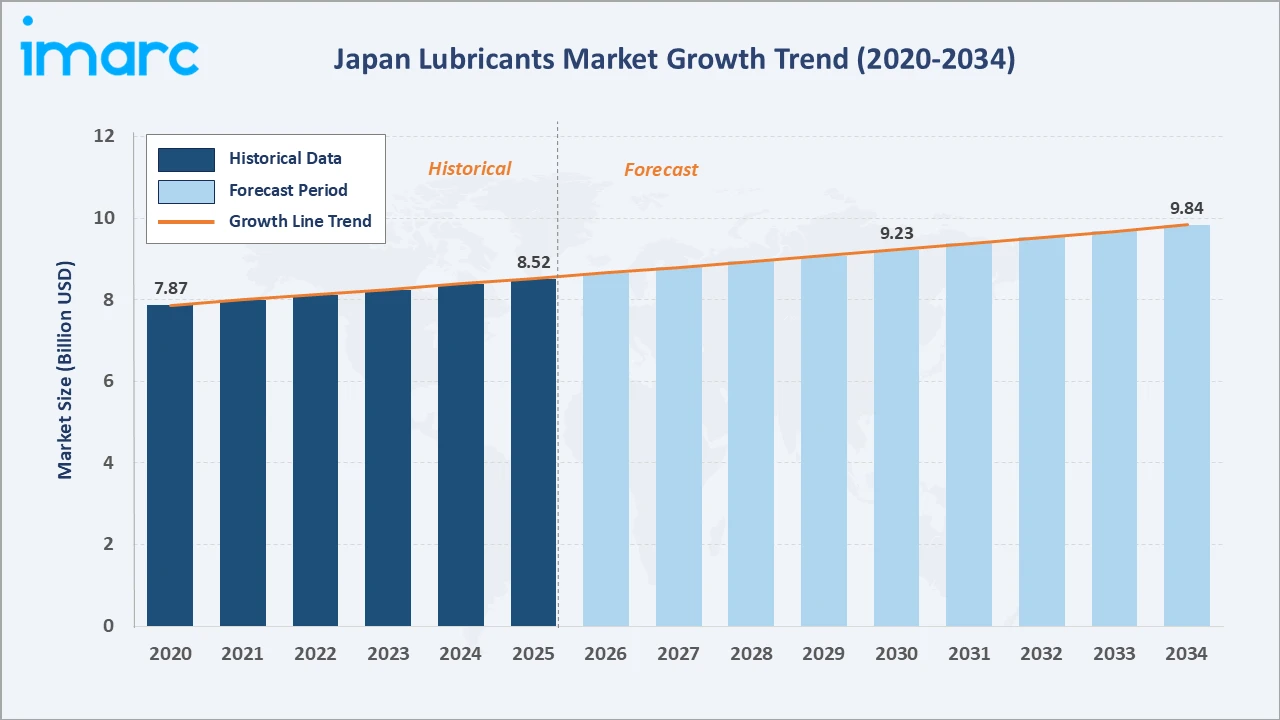

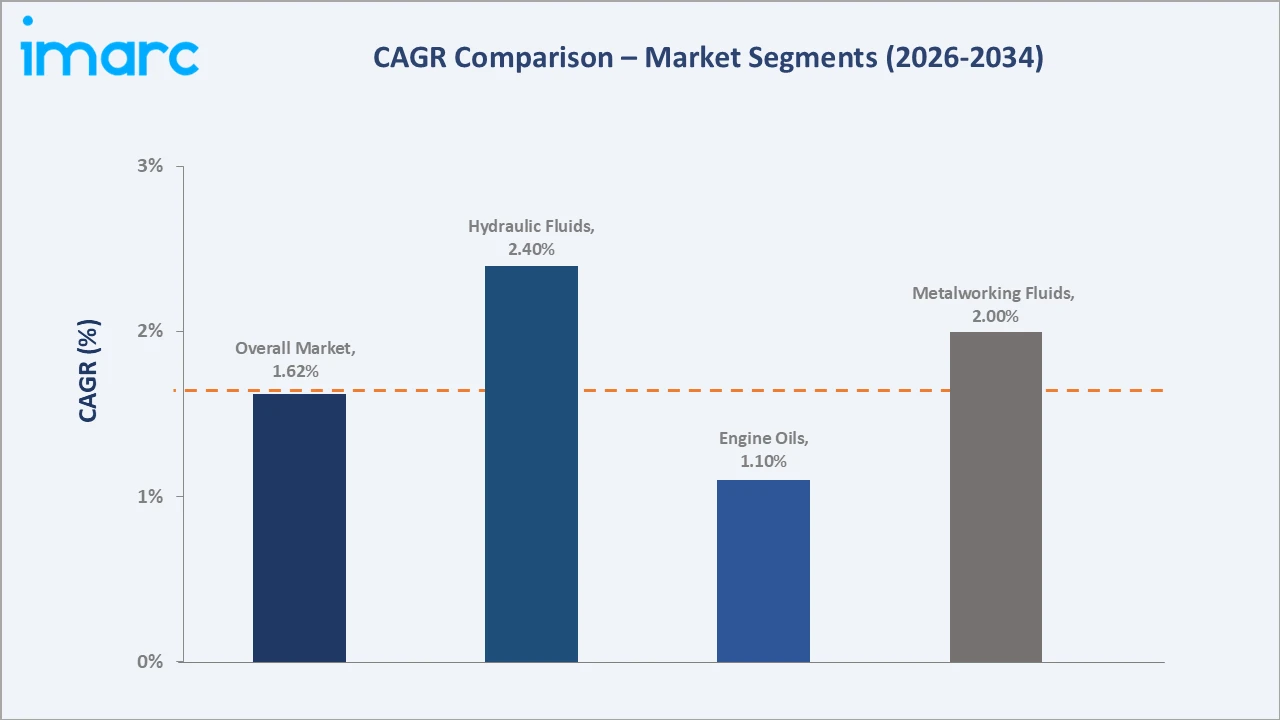

The Japan lubricants market reached USD 8.52 Billion in 2025 and is projected to reach USD 9.84 Billion by 2034, growing at a CAGR of 1.62% during 2026-2034.

Growth is driven by wind energy expansion, rising EV adoption, and increasing preference for biodegradable lubricants. Engine oils lead product types at 41.8% share, while automotive dominates end-user demand at 46.7%. Kanto Region leads regionally at 35.2% share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.52 Billion |

|

Forecast Market Size (2034) |

USD 9.84 Billion |

|

CAGR (2026-2034) |

1.62% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Engine Oils (41.8%, 2025) |

|

Dominant End User |

Automotive (46.7%, 2025) |

|

Leading Region |

Kanto Region (35.2%, 2025) |

The market grew from an estimated USD 7.87 Billion in 2020 to USD 8.52 Billion in 2025, reflecting steady but modest expansion typical of Japan's mature industrial and automotive lubricant base. This growth trajectory is anchored at USD 9.23 Billion by 2030 before reaching USD 9.84 Billion by 2034, as consistent low-single-digit annual growth across the historical and forecast periods reflects market stability, supported by steady industrial output, an established vehicle servicing culture, and gradually expanding renewable energy and specialty fluid applications.

To get more information on this market, Request Sample

Hydraulic fluids grow fastest among product types at an estimated 2.4% CAGR, supported by industrial automation and manufacturing equipment upgrades. Heavy equipment end-use is expanding on infrastructure and construction machinery demand, while engine oil growth remains modest amid Japan's shrinking combustion vehicle parc.

Executive Summary

The Japan lubricants market reached USD 8.52 Billion in 2025, reflecting a mature, technologically advanced industrial and automotive base. Lubricants remain essential across automotive, heavy equipment, metalworking, and power generation applications, reducing friction, wear, and energy losses while extending machinery lifespan and improving overall operational efficiency across end-use sectors.

Engine oils dominate product type at 41.8%, reflecting Japan's large vehicle parc and stringent maintenance culture. Automotive leads end-user demand at 46.7% through passenger and commercial vehicle servicing. Kanto Region leads regionally at 35.2%, anchored by its industrial density and automotive manufacturing concentration, which together sustain the region's position as the market's largest single demand center.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Engine Oils - 41.8% share (2025) |

|

Dominant End User |

Automotive - 46.7% market share (2025) |

|

Leading Region |

Kanto Region - 35.2% market share (2025) |

|

Market Opportunity |

Bio-based lubricants; EV thermal fluids; wind turbine gear oils; synthetic metalworking fluids; re-refined base oils |

Key Analytical Observations Supporting the Above Data:

- Engine Oils at 41.8%: Engine oils dominate as Japan's large passenger and commercial vehicle fleet requires frequent oil changes and stringent maintenance standards, sustaining steady replacement demand despite gradual electrification of the vehicle parc.

- Automotive at 46.7%: The automotive segment leads due to Japan's high vehicle ownership density and rigorous servicing culture, with continuous demand from passenger cars, commercial vehicles, and two-wheelers for engine, transmission, and gear oils.

- Kanto Region at 35.2%: Kanto dominates through Tokyo's concentrated industrial base, automotive manufacturing clusters, and major port logistics hubs, generating the highest regional demand for automotive and industrial lubricant products.

Japan Lubricants Market Overview

The Japan lubricants market encompasses the formulation, blending, distribution, and application of engine oils, greases, hydraulic fluids, metalworking fluids, transmission and gear oils, and other specialty lubricants used across automotive, industrial, and power generation sectors nationwide, supporting a wide range of machinery and vehicle operating conditions.

The ecosystem integrates base oil refiners, additive manufacturers, blenders and formulators, distributors, automotive OEMs, industrial equipment operators, and regulatory bodies enforcing environmental standards. Rising industrial automation and Japan's shift toward sustainable, biodegradable lubricant formulations continue to reshape supply chain priorities, encouraging closer collaboration between formulators and end users on performance requirements.

Market Dynamics

To evaluate market opportunities, Request Sample

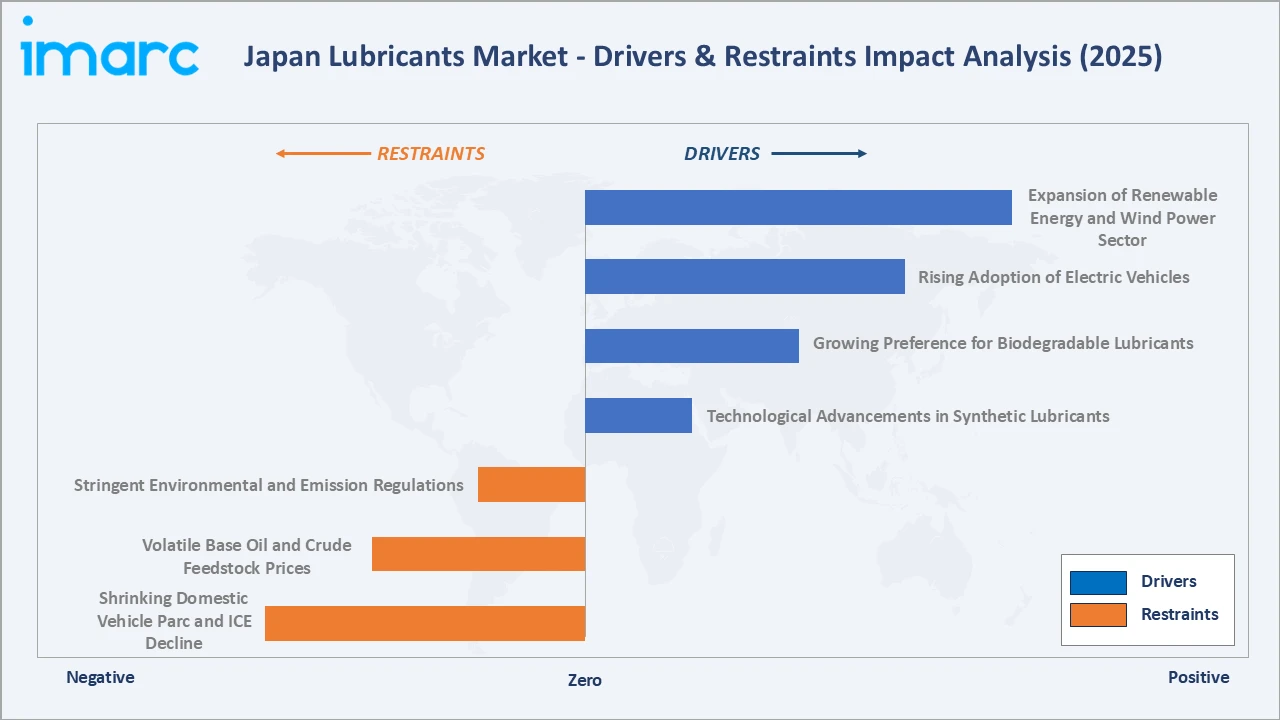

Market Drivers

- Expansion of Renewable Energy and Wind Power Sector: Japan's growing wind energy capacity requires specialized turbine gear oils and hydraulic fluids for reliable operation. Expanding offshore and onshore wind installations are increasing demand for high-performance lubricants engineered for extended service intervals and harsh conditions. This is justified by national policy support for renewable capacity additions, which requires dependable long-life fluids to minimize turbine downtime and maintenance costs across remote installations. As more wind farms reach commercial operation, recurring maintenance cycles are expected to sustain steady lubricant demand over the forecast period.

- Rising Adoption of Electric Vehicles: Growing EV adoption is increasing demand for specialized thermal management and dielectric fluids used in battery cooling and e-axle lubrication, as automakers expand EV production and develop drivetrain-specific formulations. This trend is justified by Japan's automotive OEMs accelerating hybrid and battery-electric model launches to meet emission targets and consumer demand. Each new EV platform requires tailored fluid chemistries, creating a distinct and growing product category for lubricant formulators supplying domestic and export-oriented automakers.

- Growing Preference for Biodegradable Lubricants: Stricter environmental regulations and sustainability commitments are driving demand for biodegradable, low-toxicity lubricants across industrial and marine applications, encouraging manufacturers to invest in bio-based formulations without compromising performance. This shift is justified by tightening discharge and disposal standards that raise compliance risk for conventional mineral-oil-based products. Corporate sustainability commitments among industrial buyers further reinforce procurement preferences for certified biodegradable lubricant alternatives across sensitive operating environments.

- Technological Advancements in Synthetic Lubricants: Continuous innovation in synthetic lubricant technology is improving thermal stability, oxidation resistance, and service intervals, enhancing machinery efficiency and encouraging wider adoption across automotive and industrial applications. This is justified by rising equipment operating temperatures and extended maintenance interval requirements in modern machinery, which conventional mineral oils increasingly struggle to satisfy. Manufacturers investing in synthetic formulation research are consequently well positioned to capture premium-tier demand from performance-sensitive industrial and automotive customers.

Market Restraints

- Shrinking Domestic Vehicle Parc and ICE Decline: Japan's aging population and gradual shift toward electric vehicles are slowing growth in the internal combustion vehicle parc, limiting long-term demand growth for conventional engine oils despite steady replacement demand. This is justified by demographic contraction reducing the total addressable driver base, combined with electrification policy support that gradually displaces conventional powertrains. Lubricant manufacturers reliant on conventional engine oil volumes may consequently face a structurally slower long-term demand base.

- Volatile Base Oil and Crude Feedstock Prices: Fluctuating crude oil and base oil prices increase production cost uncertainty for lubricant manufacturers, squeezing margins and complicating pricing strategies, particularly for smaller blenders without integrated refining capacity. This volatility is justified by Japan's near-total dependence on imported crude and base oil feedstock, which exposes domestic blenders directly to global energy price swings. Smaller regional players without hedging capabilities or refining integration face disproportionate margin pressure during periods of elevated feedstock cost volatility.

- Stringent Environmental and Emission Regulations: Increasingly strict environmental compliance requirements raise reformulation and testing costs for manufacturers, particularly as Japan tightens standards for biodegradability, toxicity, and industrial waste oil disposal. This restraint is justified by the rising capital and R&D expenditure required to reformulate legacy product lines to meet evolving standards. Smaller manufacturers with limited testing infrastructure may find compliance costs proportionally more burdensome than larger, vertically integrated competitors.

Market Opportunities

- Bio-Based and Recycled Lubricant Formulations: Growing demand for circular-economy solutions is creating opportunities for re-refined base oils and bio-based formulations that reduce reliance on virgin crude feedstock while meeting sustainability targets. This opportunity is justified by national circular-economy policy direction and corporate procurement preferences increasingly favoring recycled-content products. Manufacturers that establish re-refining and bio-based production capacity early stand to gain durable cost and sustainability positioning advantages.

- EV and Wind Turbine Specialty Fluids: Expanding EV production and offshore wind capacity present growth opportunities for manufacturers developing specialized dielectric, thermal, and turbine gear fluids tailored to these emerging applications. This opportunity is justified by the limited number of qualified suppliers currently serving these technically demanding niches, which allows early movers to secure long-term OEM qualification and premium pricing before broader competitive entry occurs.

Market Challenges

- Intensifying Competition from Global Majors: Domestic lubricant blenders face intensifying competition from global energy majors expanding their specialty and synthetic lubricant portfolios in Japan, pressuring pricing and market share for smaller regional players. This challenge is justified by global majors' greater R&D scale and brand recognition, which allow them to introduce premium synthetic products more rapidly than smaller domestic competitors can match, gradually eroding share in higher-margin product categories.

- Used Oil Collection and Recycling Infrastructure Gaps: Inconsistent used-oil collection infrastructure across Japan's regions complicates compliance with recycling mandates, raising operational costs for manufacturers expanding re-refined base oil supply chains. This challenge is justified by uneven investment in regional collection logistics, which creates supply variability for re-refiners and limits the scalability of circular-economy lubricant production outside major industrial corridors.

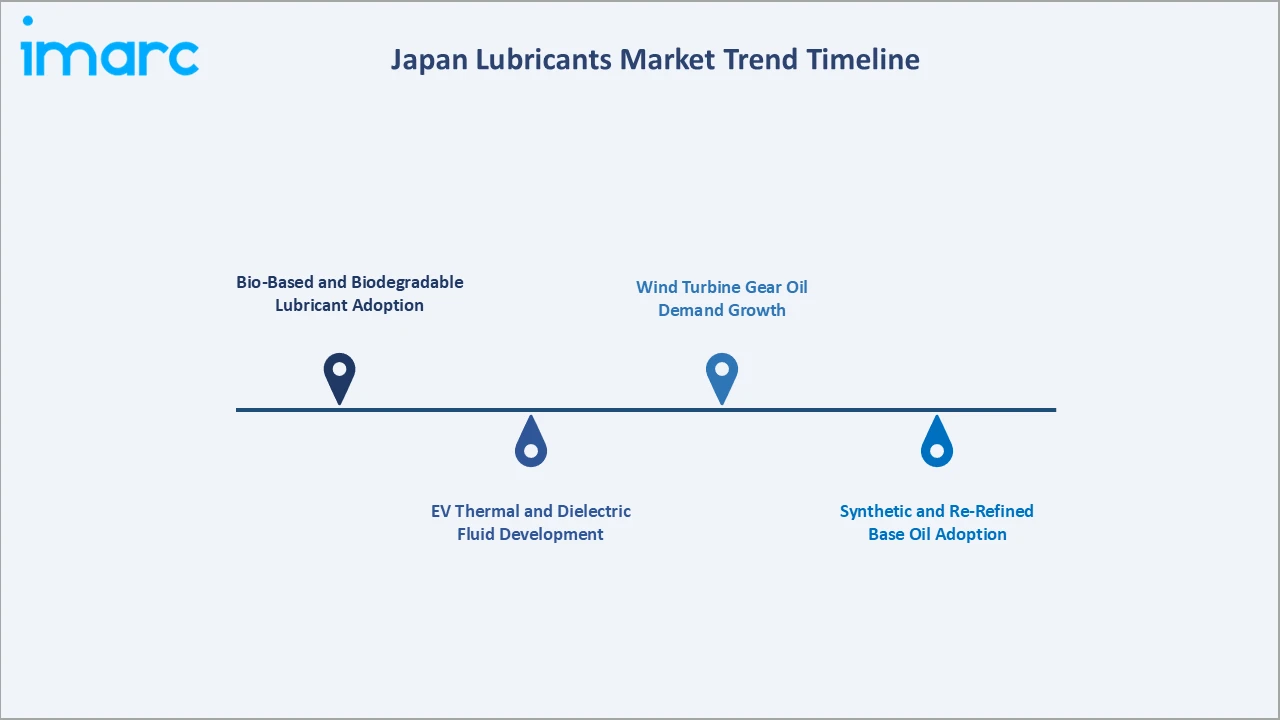

Emerging Market Trends

1. Bio-Based and Biodegradable Lubricant Adoption

Japanese manufacturers are increasingly formulating biodegradable and low-toxicity lubricants to meet tightening environmental regulations and sustainability commitments, particularly for marine, forestry, and industrial applications where spillage risk is high.

2. EV Thermal and Dielectric Fluid Development

Automakers and lubricant suppliers are jointly developing specialized thermal management and dielectric fluids for battery cooling and e-axle lubrication, reflecting Japan's steady transition toward hybrid and battery electric vehicle platforms.

3. Wind Turbine Gear Oil Demand Growth

Japan's offshore and onshore wind capacity expansion is driving demand for high-performance turbine gear oils engineered for extended service intervals and reduced maintenance downtime in remote wind farm installations.

4. Synthetic and Re-Refined Base Oil Adoption

Growing preference for synthetic and re-refined base oils reflects Japan's dual focus on lubricant performance and circular-economy sustainability, reducing virgin crude dependence while meeting efficiency and emission standards.

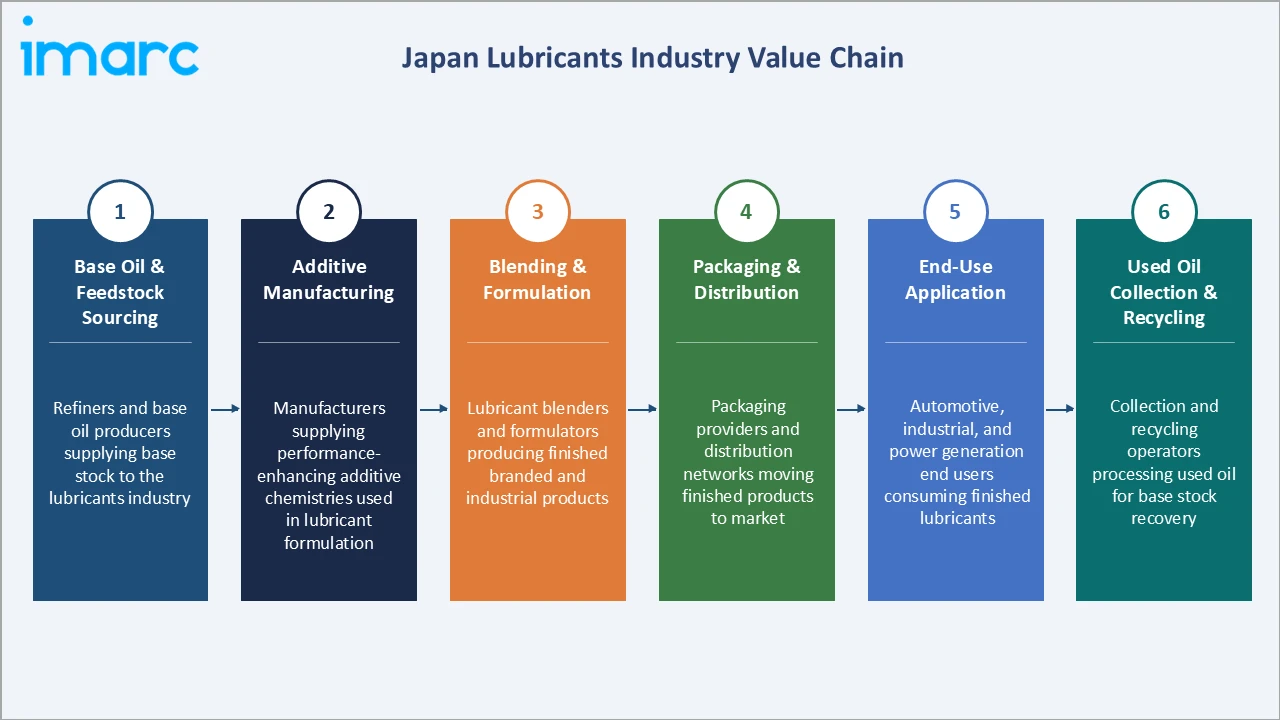

Industry Value Chain Analysis

The Japan lubricants value chain integrates base oil and feedstock sourcing, additive manufacturing, blending and formulation, packaging and distribution, end-use application, and used oil collection and recycling, forming an increasingly circular supply chain structure.

|

Stage |

Key Participants |

|

Base Oil & Feedstock Sourcing |

Refiners and base oil producers supplying base stock to the lubricants industry |

|

Additive Manufacturing |

Manufacturers supplying performance-enhancing additive chemistries used in lubricant formulation |

|

Blending & Formulation |

Lubricant blenders and formulators producing finished branded and industrial products |

|

Packaging & Distribution |

Packaging providers and distribution networks moving finished products to market |

|

End-Use Application |

Automotive, industrial, and power generation end users consuming finished lubricants |

|

Used Oil Collection & Recycling |

Collection and recycling operators processing used oil for base stock recovery |

The blending and formulation stage remains the value chain's most commercially competitive tier, where domestic players and global majors compete on product performance, brand trust, and distribution reach across automotive and industrial channels. This is justified by formulation being the primary point of product differentiation, where proprietary additive packages and performance testing determine competitive positioning more than upstream feedstock sourcing.

Technology Landscape in the Japan Lubricants Industry

Synthetic Lubricant Technology

Synthetic lubricant technology offers superior thermal stability, oxidation resistance, and extended drain intervals compared with conventional mineral oils. Its adoption is justified by rising demand from high-performance automotive engines and industrial machinery operating under increasingly demanding temperature and load conditions, supporting wider uptake across premium product tiers.

Bio-Based and Biodegradable Lubricant Technology

Bio-based and biodegradable lubricant technology reduces environmental impact through improved biodegradability and lower toxicity while maintaining functional performance. This technology's growing relevance is justified by tightening discharge regulations and corporate sustainability commitments, particularly across marine, forestry, and other environmentally sensitive industrial applications nationwide.

Advanced Additive Technology

Advanced additive technology, including next-generation anti-wear, dispersant, and friction-modifier chemistries, enhances lubricant performance and service life. Its increasing importance is justified by original equipment manufacturers specifying tighter performance standards, requiring formulators to continuously upgrade additive packages to remain qualified suppliers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Engine Oils |

41.8% |

2025 |

|

End User |

Automotive |

46.7% |

2025 |

|

Region |

Kanto Region |

35.2% |

2025 |

By Product Type

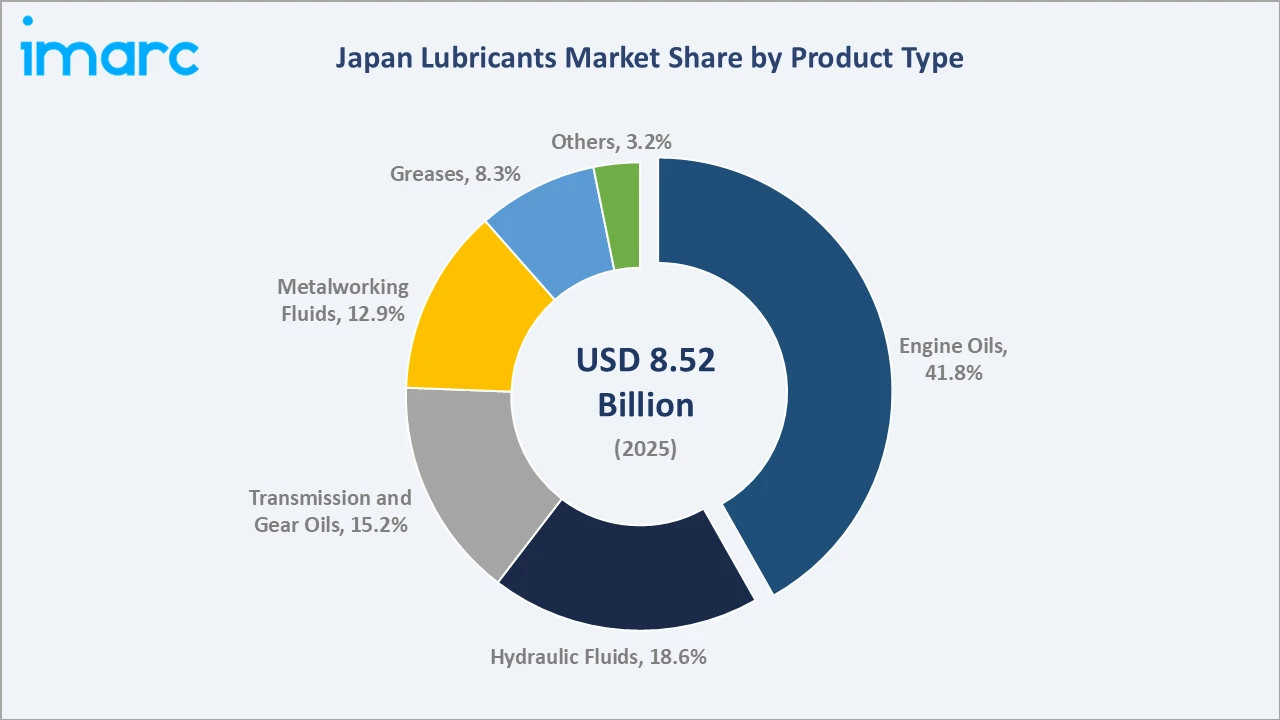

Engine oils lead product type segmentation at 41.8% in 2025, reflecting Japan's large vehicle parc and frequent maintenance cycles across passenger cars, commercial vehicles, and two-wheelers requiring regular oil replacement.

To access detailed market analysis, Request Sample

Hydraulic fluids follow at 18.6%, driven by industrial automation and construction machinery, and represent the fastest-growing product category. Transmission and gear oils hold 15.2%, while metalworking fluids at 12.9% serve precision manufacturing. Greases at 8.3% and other specialty products at 3.2% complete the segment, together forming a diversified product base.

By End User

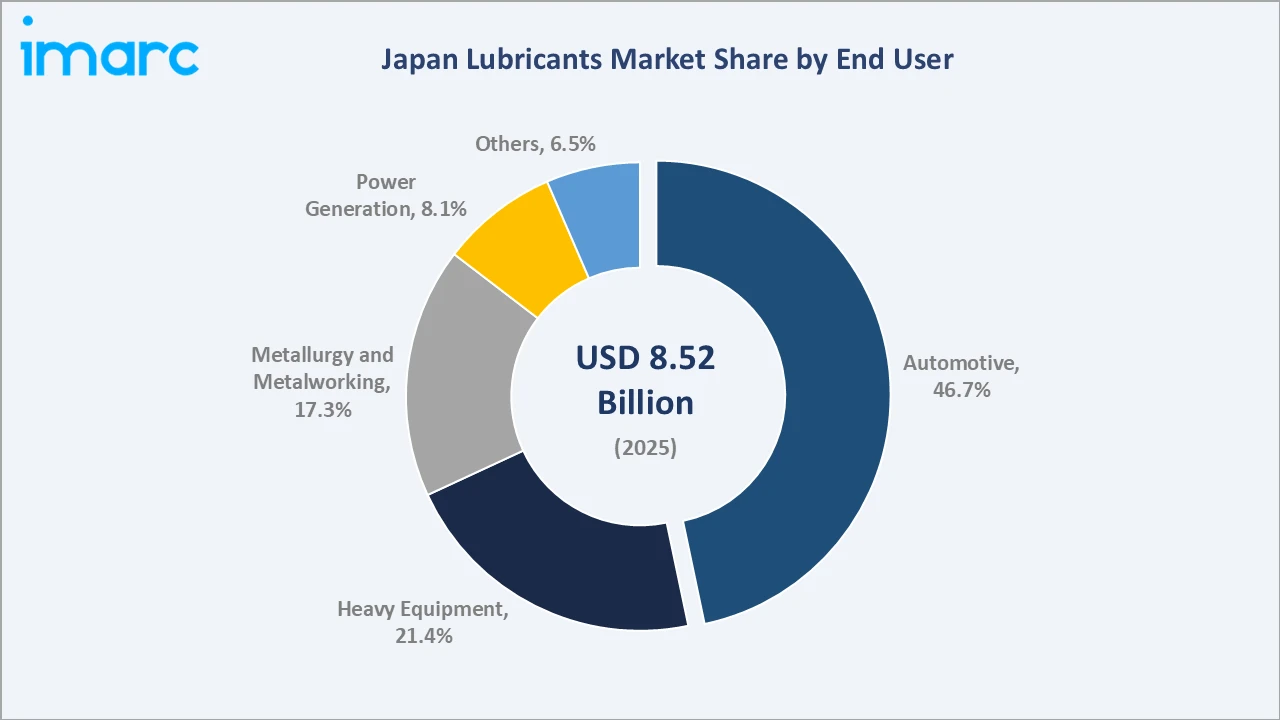

Automotive leads end-user segmentation at 46.7%, driven by Japan's high vehicle density and rigorous servicing standards across dealerships and independent service centers nationwide, sustaining steady demand for engine, transmission, and gear oils.

Heavy equipment follows at 21.4%, supported by construction and infrastructure activity across the country. Metallurgy and metalworking hold 17.3%, power generation accounts for 8.1%, and other applications, including marine and aerospace, represent 6.5% of end-user demand, reflecting the market's broad industrial reach.

Regional Market Insights

|

Region |

Share (2025) |

Key Lubricants Market Drivers & Characteristics |

|

Kanto Region |

35.2% |

Driven by a dense industrial base, strong automotive manufacturing presence, and major logistics infrastructure |

|

Kansai/Kinki Region |

19.4% |

Supported by a diversified manufacturing and heavy industry base alongside steady aftermarket activity |

|

Central/Chubu Region |

15.8% |

Anchored by a significant automotive manufacturing presence and related parts production activity |

|

Kyushu-Okinawa Region |

9.6% |

Growing on expanding manufacturing investment supporting rising industrial lubricant demand |

|

Tohoku Region |

7.1% |

Supported by growing renewable energy installations and agricultural and industrial machinery needs |

|

Chugoku Region |

5.6% |

Driven by shipbuilding, steel, and heavy industrial manufacturing activity |

|

Hokkaido Region |

4.3% |

Reflects agricultural machinery, forestry equipment, and regional industrial lubricant consumption |

|

Shikoku Region |

3.0% |

Smallest regional market, supported by paper, chemical, and marine industry lubricant demand |

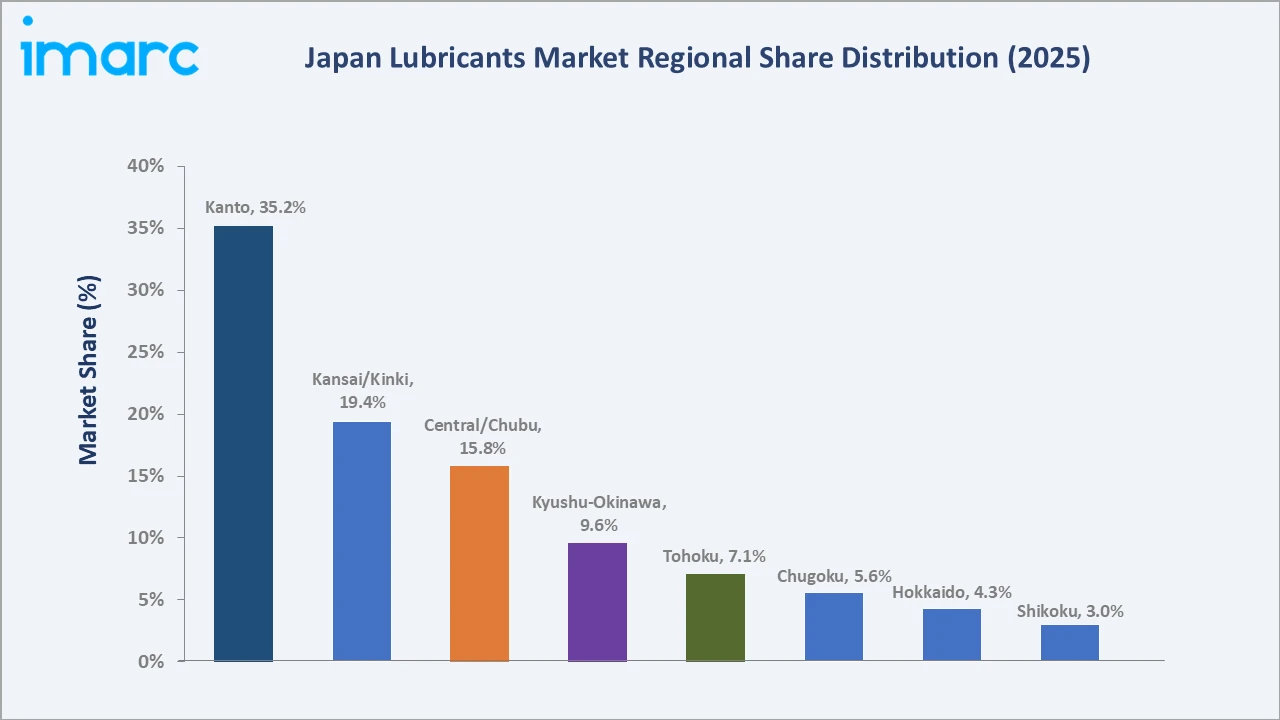

Kanto Region, at 35.2%, leads through its industrial concentration and automotive manufacturing scale. Kansai/Kinki, at 19.4%, reflects a diversified chemical and heavy industry base, while Central/Chubu, at 15.8%, benefits from a strong automotive OEM manufacturing presence, together forming the market's three largest regional demand centers.

Kyushu-Okinawa, at 9.6%, and Tohoku, at 7.1%, reflect growing manufacturing and renewable energy investment. Chugoku, Hokkaido, and Shikoku collectively hold 12.9%, representing smaller but steady industrial and agricultural lubricant demand pools across Japan's remaining regions, each supported by localized manufacturing and maintenance activity.

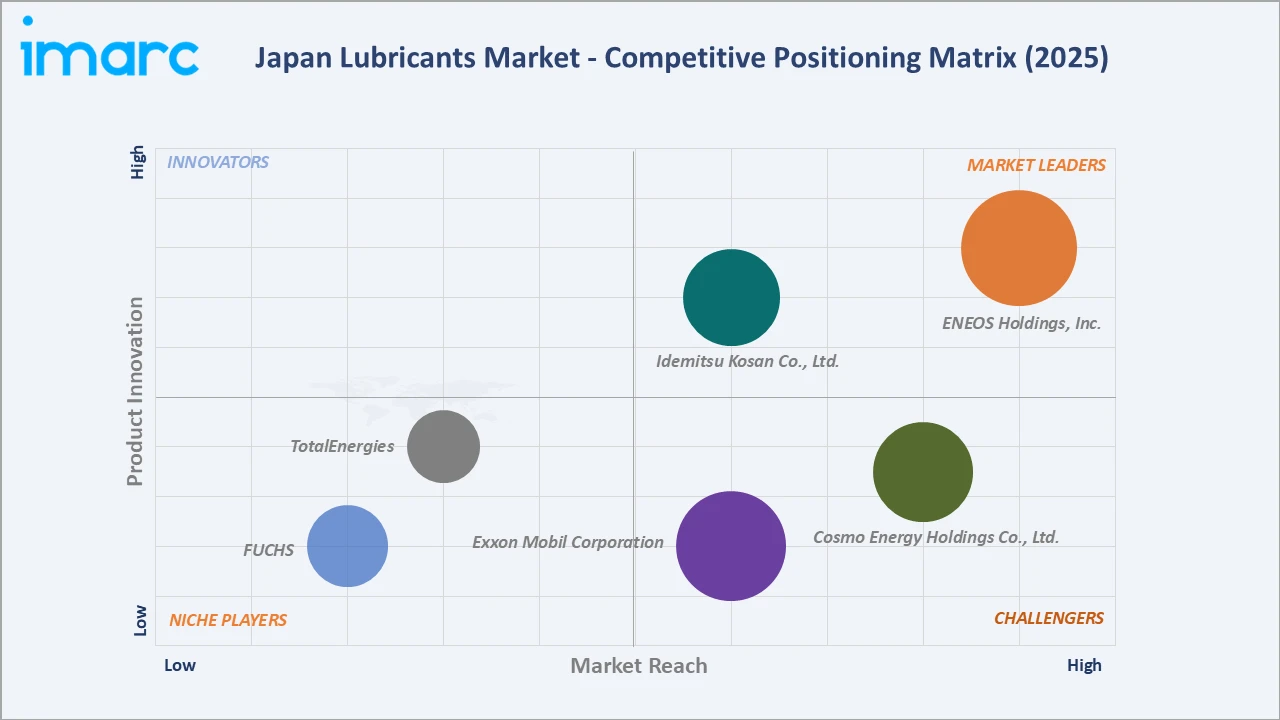

Competitive Landscape

The Japan lubricants market competitive landscape is moderately concentrated, comprising established domestic refiners with strong retail and industrial distribution networks alongside global energy majors competing through premium synthetic and specialty lubricant portfolios across automotive, industrial, and marine applications nationwide.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

ENEOS Holdings, Inc. |

Engine oils, industrial lubricants, greases, Automotive Lubricants, Marine Lubricants, Industrial & Private-use Engine Oils |

Market Leader |

Japan's largest integrated energy company with extensive refining capacity and nationwide retail distribution network |

|

Idemitsu Kosan Co., Ltd. |

Engine oils, hydraulic fluids, gear oils |

Market Leader |

Leading domestic refiner with strong automotive OEM partnerships and diversified industrial lubricant portfolio |

|

Cosmo Energy Holdings Co., Ltd. |

Engine oils, greases, Industrial Lubricants, Metalworking Fluids |

Strong Challenger |

Established Japanese lubricant specialist focused on automotive aftermarket and industrial applications |

|

Exxon Mobil Corporation |

Automotive lubricants, Industrial lubricants, Greases |

Strong Challenger |

Global lubricant major with premium synthetic product portfolio and strong brand recognition in Japan |

|

FUCHS |

Automotive lubricants, Industrial lubricants, Lubricating Greases, Metal processing lubricants, Special application lubricants |

Niche Player |

German specialty lubricant manufacturer focused on high-performance industrial and metalworking applications |

|

TotalEnergies |

Total Quartz, industrial and marine lubricants |

Niche Player |

Global energy company with growing specialty lubricant presence across automotive and marine segments |

Key players include ENEOS Holdings, Inc., Idemitsu Kosan Co., Ltd., Cosmo Energy Holdings Co., Ltd., Exxon Mobil Corporation, FUCHS, TotalEnergies, and others.

Key Company Profiles

ENEOS Holdings, Inc.

ENEOS Holdings, Inc. operating through ENEOS Corporation, is Japan's largest integrated energy company, maintaining a dominant presence in the domestic lubricants market through extensive refining capacity, nationwide retail distribution, and a broad portfolio of automotive and industrial lubricant products serving both consumer and industrial customers.

- Key Products: Engine oils, industrial lubricants, greases, Automotive Lubricants, Marine Lubricants, Industrial & Private-use Engine Oils

- Strategic Focus: Strengthening synthetic and bio-based lubricant portfolios while expanding retail and industrial distribution reach across Japan and select export markets.

Idemitsu Kosan Co., Ltd.

Idemitsu Kosan Co., Ltd. is a leading Japanese energy and petrochemical company with a strong lubricants business built on extensive refining infrastructure and long-standing partnerships with domestic automotive OEMs across passenger and commercial vehicle segments.

- Key Products: Engine oils, hydraulic fluids, gear oils

- Strategic Focus: Deepening OEM partnerships while expanding synthetic and specialty lubricant production capacity to serve evolving automotive and industrial performance requirements.

Market Concentration Analysis

The Japan lubricants market is moderately concentrated, with the top two key players collectively holding a leading share of domestic engine oil and industrial lubricant sales, while global majors and specialty players compete across premium and niche segments.

Investment & Growth Opportunities

Highest Growth Segments

Hydraulic fluids (~2.4% CAGR), greases (~1.9% CAGR), and metalworking fluids (~2.0% CAGR) represent the highest-growth product segments, while heavy equipment end-use and EV thermal fluid applications offer above-market growth potential through 2034. This ranking is justified by these categories' closer alignment with industrial automation, construction activity, and electrification trends than with the slower-growing conventional automotive engine oil base.

Emerging Investment Opportunities

Bio-based and re-refined lubricant production represents Japan's most significant emerging investment opportunity, as sustainability mandates and circular-economy targets drive demand for environmentally responsible formulations across automotive and industrial applications. Early investment is justified by the relatively limited domestic re-refining capacity currently available to meet this rising demand.

Investment Themes

- Bio-Based Lubricant Manufacturing Capacity Expansion: Investment in bio-based and biodegradable lubricant production capacity positions manufacturers to capture growing demand from environmentally conscious industrial and marine customers while meeting tightening regulatory requirements.

- EV and Renewable Energy Specialty Fluid Development: Investment in dielectric, thermal management, and wind turbine gear fluid development creates opportunities to capture demand from Japan's expanding EV and renewable energy infrastructure base.

Future Market Outlook (2026-2034)

The Japan lubricants market is projected to grow from USD 8.52 Billion in 2025 to USD 9.84 Billion by 2034, delivering a 1.62% CAGR, with an anchor value of USD 9.23 Billion by 2030. Growth will be shaped by gradual electrification, renewable energy expansion, and rising demand for sustainable lubricant formulations.

Bio-based and synthetic lubricants are expected to gain further share as environmental regulations tighten, while EV thermal fluids and wind turbine gear oils emerge as high-growth specialty categories supporting Japan's broader energy transition through 2034. Manufacturers that invest early in these specialty categories are best positioned to capture disproportionate long-term value as conventional product growth remains comparatively modest.

Research Methodology

Primary Research

Primary research comprised structured interviews with industry stakeholders, including procurement managers, technical formulation specialists, distribution partners, and industry association representatives across Japan's automotive and industrial lubricant sectors, providing qualitative context for observed market trends.

Secondary Research

Secondary research encompassed company annual reports, industry association publications, government regulatory filings, trade association data, and international energy and lubricant market databases covering Japan's historical and forecast market trends across all major product and end-user categories.

Forecasting Models

Market revenue forecasts were developed using a bottom-up approach incorporating product type and end-user consumption patterns, regional industrial activity levels, and historical growth trends adjusted for regulatory and technology transition factors expected to influence demand through the forecast period.

Japan Lubricants Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Engine Oils, Greases, Hydraulic Fluids, Metalworking Fluids, Transmission and Gear Oils, Others |

| End Users Covered | Automotive, Heavy Equipment, Metallurgy and Metalworking, Power Generation, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | ENEOS Holdings, Inc., Idemitsu Kosan Co., Ltd., Cosmo Energy Holdings Co., Ltd., Exxon Mobil Corporation, FUCHS, TotalEnergies, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan lubricants market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan lubricants market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan lubricants industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Lubricants Market Report

The Japan lubricants market reached USD 8.52 Billion in 2025, driven by engine oils leading at 41.8% share, automotive end-use dominant at 46.7%, and Kanto Region leading regionally at 35.2% through its industrial and automotive manufacturing concentration and logistics infrastructure.

The market grows at a 1.62% CAGR during 2026-2034, reaching USD 9.84 Billion by 2034 from USD 8.52 Billion in 2025, reflecting steady demand from Japan's mature automotive and industrial base alongside emerging EV and renewable energy applications.

Engine oils lead at 41.8%, reflecting Japan's large vehicle parc and frequent maintenance cycles. Hydraulic fluids grow fastest at an estimated 2.4% CAGR, supported by industrial automation and construction machinery demand.

Automotive leads at 46.7% through high vehicle ownership density and rigorous servicing standards. Heavy equipment follows at 21.4%, supported by construction and infrastructure activity across the country.

Kanto Region leads at 35.2% through Tokyo's industrial concentration, automotive manufacturing clusters, and major port logistics infrastructure generating the highest regional lubricant demand nationwide.

Leading companies include ENEOS Holdings, Inc., Idemitsu Kosan Co., Ltd., Cosmo Energy Holdings Co., Ltd., Exxon Mobil Corporation, FUCHS, TotalEnergies, and others.

The market is projected to reach approximately USD 9.23 Billion by 2030, with growing adoption of bio-based formulations, EV thermal fluids, and wind turbine gear oils shaping the mid-forecast period as Japan's energy transition steadily accelerates.

Priority opportunities include bio-based and re-refined lubricant manufacturing, EV thermal and dielectric fluid development, and wind turbine gear oil production supporting Japan's renewable energy expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)