Robotic Welding Market Share, Trends, and Forecast by Type, Payload, End User, and Region, 2026-2034

Robotic Welding Market Size and Share:

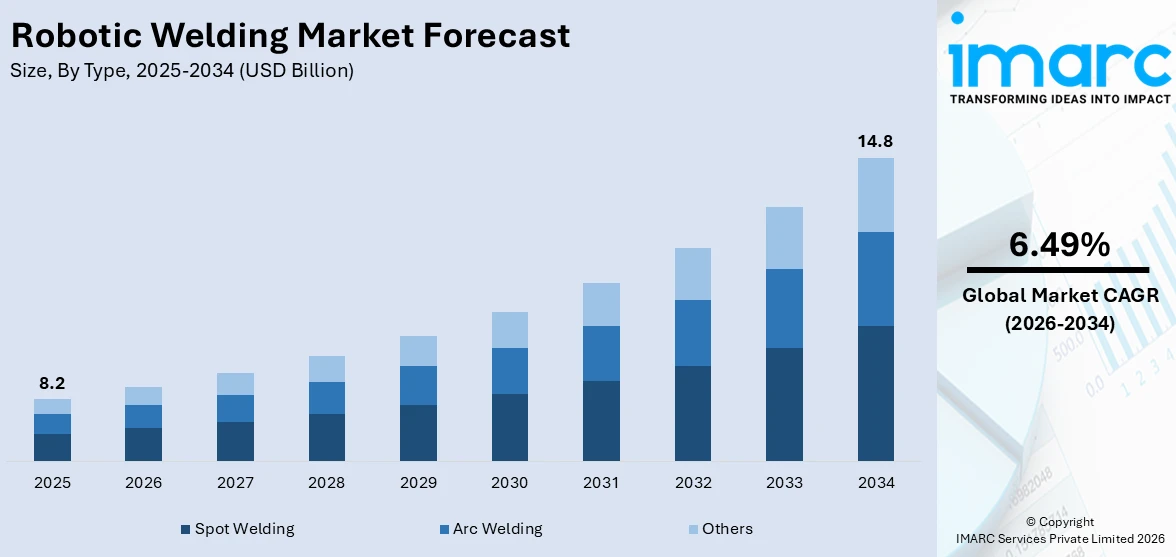

The global robotic welding market size was valued at USD 8.2 Billion in 2025. Looking forward, the market is expected to reach USD 14.8 Billion by 2034, exhibiting a CAGR of 6.49% during 2026-2034. Asia-Pacific currently dominates the market, holding 29% market share in 2025. The market is driven by rising automation in manufacturing, the growing need for efficiency and precision in welding operations, and the increasing adoption of robotics in automotive and transportation industries, which enhances the overall robotic welding market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 8.2 Billion |

|

Market Forecast in 2034

|

USD 14.8 Billion |

| Market Growth Rate (2026-2034) | 6.49% |

The market is driven by factors such as the rising adoption of automation in industries, technological advancements in robotic welding systems, and the need for higher efficiency in large-scale manufacturing. Automotive and transportation industries remain at the forefront of demand as they require faster, precise, and consistent welding solutions. Continuous advancements in robotic payload capacities and spot-welding applications are shaping the robotic welding market outlook. Moreover, industrial robotics is increasingly used to reduce errors and production costs while improving workplace safety, making robotic welding indispensable in high-volume manufacturing.

To get more information on this market Request Sample

The robotic welding market growth in the United States is driven by the growing adoption of automation across automotive, aerospace, and heavy machinery industries to enhance productivity and reduce operational costs. Rising demand for precision welding, improved efficiency, and consistent quality is fueling the shift toward advanced robotic systems. Shortages of skilled welders and rising labor expenses further encourage manufacturers to invest in automated welding solutions. Technological advancements, including AI-integrated robots and collaborative welding systems, support flexible, high-speed production. Additionally, strong infrastructure development, expanding electric vehicle manufacturing, and government incentives promoting smart manufacturing practices are creating significant opportunities for robotic welding market growth nationwide. For instance, in December 2024, Spartan Robotics, a branch of BlueBay Automation, introduced an advanced collaborative robot (cobot) welding cell born from a global partnership. Working alongside Kassow Robots, a Bosch Rexroth subsidiary, and welding technology specialist Fronius, the company developed a flexible seven-axis system engineered to address the intricate welding requirements of US metalworking and fabrication industries.

Robotic Welding Market Trends:

Enhanced Efficiency and Cost Savings

The global robotic welding market is expanding as industries seek solutions that reduce labor injuries, improve order fulfillment speed, and cut operational costs. Notably, some robotic systems have improved weld quality and lowered rework rates by 18%, leading to substantial cost savings and higher productivity. Robotic welding optimizes workspace utilization, streamlines processes, and strengthens supply chain performance for end-user industries. By minimizing downtime and ensuring precise operations, these systems help manufacturers achieve consistent, high-quality output while lowering maintenance expenses. This efficiency-driven adoption highlights how robotic welding is becoming an essential tool for companies aiming to remain competitive, reduce manual intervention, and achieve sustainable growth in today’s fast-paced industrial environments.

Technological Advancements and Customization

Continuous investments in research and development (R&D) by key market players are significantly enhancing robotic welding’s capabilities and appeal. According to the robotic welding market trends, customization trends such as cloud-based operations, remote monitoring, and improved physical design for better collaboration with human workers are accelerating adoption. For example, 72% of organizations are already utilizing generative AI services from public cloud providers in some capacity in 2025, reflecting growing confidence in advanced, connected technologies. These innovations ensure that robotic welding systems can be tailored to specific production needs, providing greater flexibility and adaptability across industries. Such advancements enable improved precision, simplified operation, and seamless integration into existing workflows, driving further demand for these intelligent automation solutions.

Expanding Automotive Applications

Robotic welding is gaining strong traction in the automotive sector, where resistance spot welding and arc welding are essential for high-volume production. Automotive manufacturers increasingly deploy these systems to achieve consistent weld quality, enhance safety, and reduce production cycle times. According to SIAM, India produced a total of 76,60,225 passenger vehicles, commercial vehicles, three wheelers, two wheelers, and quadricycles between April and June 2025, reflecting substantial demand for efficient welding processes. The reprogrammable nature of robotic welding, which requires minimal hard tooling, adds to its appeal by enabling rapid adaptation to design changes or new product lines. This flexibility and scalability make robotic welding indispensable for automotive growth and innovation worldwide.

Robotic Welding Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global robotic welding market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, payload, and end user.

Analysis by Type:

- Spot Welding

- Arc Welding

- Others

Spot welding leads the market with 40% of market share in 2025, driven by its extensive use in automotive manufacturing. It is primarily employed in body-in-white assemblies where sheet metal joining requires high precision and repeatability. Spot welding offers durability, speed, and efficiency, making it indispensable in large-scale vehicle production. The technique’s integration with robotic systems ensures error reduction and cost savings in high-volume manufacturing. As electric vehicle (EV) production grows, spot welding is increasingly used in battery assembly and lightweight design applications. These factors reinforce its leadership position in the robotic welding market, ensuring its continued demand across automotive and industrial applications.

Analysis by Payload:

- Less than 50 Kg

- 50-150 Kg

- More than 150 Kg

50–150 kg payload leads the market with 50% of market share in 2025, because it offers the most versatile balance between strength, efficiency, and flexibility. These robots are powerful enough to handle a wide range of medium to heavy welding tasks, including automotive components, metal fabrication, and industrial equipment, yet compact enough to operate efficiently in diverse manufacturing environments. According to the robotic welding market forecast, their adaptability makes them suitable for small and large enterprises alike, enabling cost-effective automation without the need for extremely high-capacity or oversized systems. Additionally, their precision, reach, and ability to manage complex weld paths make them ideal for industries seeking improved productivity and quality. This combination of performance and practicality positions 50–150 kg robots as the preferred choice across multiple applications.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Automotive and Transportation

- Electrical and Electronics

- Metals and Machinery

- Others

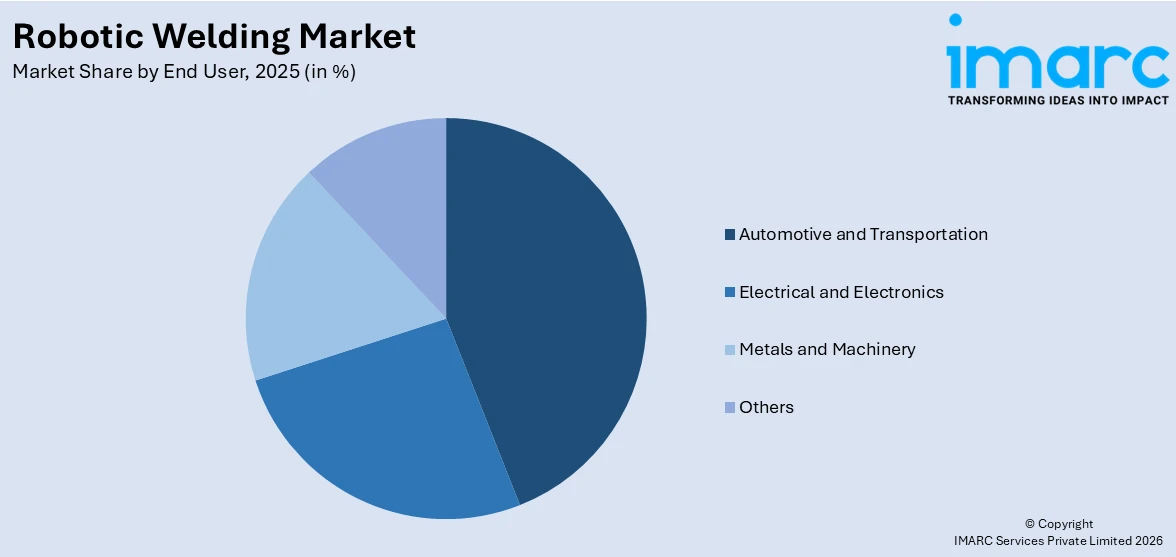

Automotive and transportation leads the market with 44% of market share in 2025. The sector relies heavily on robotic welding for vehicle body structures, chassis, and other critical components requiring high durability and precision. With rising vehicle production and a strong shift toward electric mobility, automotive manufacturers are accelerating robotic welding adoption to meet quality standards and efficiency targets. EV battery and frame assembly further enhances the segment’s reliance on robotic welding, thus creating a positive robotic welding market outlook. By reducing costs and improving consistency, robotic welding has become a cornerstone of the automotive manufacturing process, making this sector the leading consumer of robotic welding technologies worldwide.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

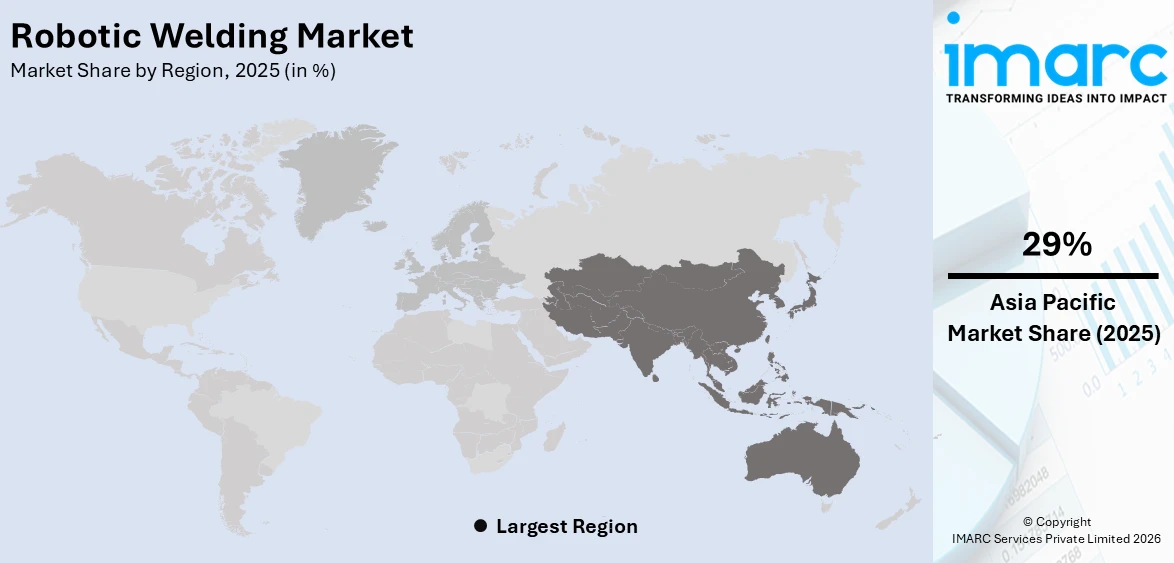

In 2025, Asia Pacific accounted for the largest market share of 29%. Asia-Pacific represents the dominant region in 2025, supported by strong automotive production bases in China, Japan, and South Korea. Asia-Pacific is experiencing significant robotic welding market demand driven by growing construction activities such as smart cities and large-scale infrastructure development. For instance, as of May 9, 2025, a total of 7,555 smart city projects, 94% of the total 8,067 projects, have been completed in India. Expanding urbanization and the need for sustainable, efficient building methods are encouraging the use of robotic welding for structural steel, pipelines, and complex frameworks. Rising government-backed infrastructure projects and private investments are creating a surge in demand for automated welding processes to ensure the timely completion of massive construction undertakings. Enhanced productivity, safety, and reduced project costs are positioning robotic welding as a key enabler for future-ready infrastructure, strengthening its role in addressing construction industry requirements across the region.

Key Regional Takeaways:

North America Robotic Welding Market Analysis

The North America robotic welding market is driven by rising automation adoption to reduce labor costs, enhance productivity, and improve worker safety. Manufacturers increasingly deploy robotic systems to achieve precise weld quality, lower rework rates, and minimize downtime, supporting lean manufacturing goals. Strong demand from automotive, aerospace, and heavy machinery sectors accelerates the need for high-volume, consistent welding operations. Technological advancements such as cloud-connected monitoring, generative AI integration, and customizable robotic arms further boost efficiency and flexibility. Additionally, government incentives for smart manufacturing and the region’s focus on reshoring production strengthen market growth. The availability of skilled robotics integrators and continuous research and development (R&D) investments from key players also fosters innovation, making robotic welding a strategic choice for North American industries.

United States Robotic Welding Market Analysis

In 2025, the United States accounted for 85.04% of the robotic welding market in North America. The United States is witnessing strong momentum in robotic welding adoption due to growing investment in the automotive sector, where increased demand for higher production efficiency and advanced automation is driving deployment across assembly lines. For instance, GM is planning to invest USD 4 Billion in its US manufacturing plants. Rising emphasis on precision, speed, and safety in manufacturing operations is creating greater reliance on robotic welding systems to handle complex welding tasks. In addition, workforce challenges and the need to reduce labor-intensive processes are strengthening the case for automation. Increasing competitiveness in vehicle manufacturing and the push for consistent product quality are further boosting integration of robotic welding technologies, supporting long-term adoption trends across the sector.

Europe Robotic Welding Market Analysis

Europe is registering rising robotic welding adoption owing to growing industrialization and increasing production across key manufacturing segments. For instance, industrial production in the Euro Area increased 3.70 percent in May of 2025 over the same month in the previous year. Expanding industrial bases and the demand for higher throughput are pushing enterprises toward automation in welding operations. The focus on operational efficiency, reduced downtime, and superior weld accuracy is making robotic welding systems vital in meeting production demands. Rising competitiveness in industrial output and emphasis on maintaining product consistency are also encouraging deployment. Furthermore, the need to address workforce shortages and improve workplace safety is propelling wider integration of robotic welding solutions, ensuring scalability and long-term growth across multiple European industries.

Latin America Robotic Welding Market Analysis

Latin America is advancing robotic welding adoption supported by growing mining industries where efficiency and durability are vital in equipment manufacturing and repair. According to International Energy Agency, Latin America, rich in critical minerals, is projected to reach USD 154 Billion in mining and refining value amid regulatory reforms to attract foreign capital. Expanding extraction activities and rising demand for heavy machinery production are encouraging automated welding processes to reduce downtime and ensure reliability. The push for stronger weld quality, enhanced safety, and faster operations is driving industries to rely on robotic welding solutions, aligning with increasing mining activities and production capacity expansion across the region.

Middle East and Africa Robotic Welding Market Analysis

Middle East and Africa are experiencing growing robotic welding adoption driven by the expansion of the electrical and electronics sector. For instance, the Middle East’s smartphone market grew 15% to 13.2 Million Units in Q2 2025. Rising demand for consumer electronics, semiconductors, and electrical equipment manufacturing is creating opportunities for precision-driven welding automation. The need for accuracy, miniaturization, and consistent quality in production lines is accelerating reliance on robotic welding systems. Increasing focus on technological advancements, combined with growing manufacturing capacity, is reinforcing the role of robotic welding as a core enabler for the electrical and electronics sector in the region.

Competitive Landscape:

The global robotic welding market is characterized by a mix of established robotics companies and emerging automation solution providers. Competition is driven by technological advancements, product innovations, and strategic partnerships. Industry leaders focus on expanding product portfolios, enhancing robotic payload capacities, and developing software-integrated welding solutions. Key players also pursue mergers, acquisitions, and collaborations to strengthen their global presence and customer base. With rising automation adoption across industries, the competitive landscape continues to evolve, emphasizing both innovation and scalability.

The report provides a comprehensive analysis of the competitive landscape in the global robotic welding market with detailed profiles of all major companies, including:

- ABB Ltd.

- Comau (Stellantis N.V.)

- DAIHEN Corporation

- FANUC Corporation

- Hyundai Robotics Co. Ltd. (Hyundai Heavy Industries Group)

- Kawasaki Heavy Industries Ltd.

- KUKA AG

- Nachi-Fujikoshi Corp.

- Panasonic Corporation

- Siasun Robot & Automation Co. Ltd.

- Yaskawa Electric Corporation

Latest News and Developments:

- July 2025: FBR Limited officially introduced its new Mantis™ robotic welding system with an 8-meter range and a capacity of welding up to 25 kilograms per hour, marking the company’s second major step into large-scale automation for industries such as mining, shipbuilding, and defense.

- May 2025: Novarc Technologies Inc. introduced its AI-powered NovAI™ system at Automate 2025, which transformed robotic welding by integrating real-time vision and cognition to improve weld quality, reduce defects, and minimize overwelding while enabling cobots and robots to handle complex welding tasks with greater efficiency and traceability.

- April 2025: Path Robotics and ALM Positioners announced a strategic partnership to integrate robotic welding with advanced positioning systems, creating fully autonomous AI-powered solutions that transformed automation in manufacturing by enhancing accuracy, reducing complexity, and addressing skilled labor shortages.

- March 2025: Vention Inc. unveiled its Click & Customize family of robotic work cells, including a robotic welding solution released in January 2025, which enabled manufacturers to quickly design and deploy customizable welding cells to address labor shortages and boost productivity in manufacturing.

- February 2025: Delta showcased its newly launched D-Bot series Collaborative Robots at ELECRAMA 2025, highlighting their applications in smart manufacturing processes such as packaging, electronics assembly, materials handling, and robotic welding, while also unveiling a 240kW DC fast EV charger to support India’s sustainable cities.

Robotic Welding Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Spot Welding, Arc Welding, Others |

| Payloads Covered | Less than 50 Kg, 50-150 Kg, More than 150 Kg |

| End Users Covered | Automotive and Transportation, Electrical and Electronics, Metals and Machinery, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ABB Ltd., Comau (Stellantis N.V.), DAIHEN Corporation, FANUC Corporation, Hyundai Robotics Co. Ltd. (Hyundai Heavy Industries Group), Kawasaki Heavy Industries Ltd., KUKA AG, Nachi-Fujikoshi Corp., Panasonic Corporation, Siasun Robot & Automation Co. Ltd. and Yaskawa Electric Corporation. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the robotic welding market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global robotic welding market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the robotic welding industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Robotic Welding Market Report

The robotic welding market was valued at USD 8.2 Billion in 2025.

The robotic welding market is projected to exhibit a CAGR of 6.49% during 2026-2034, reaching a value of USD 14.8 Billion by 2034.

The market is driven by increasing industrial automation, growing automotive production, demand for efficiency and precision, and the adoption of robotic welders with high payload capacities. Spot welding and the automotive industries remain major contributors.

Asia Pacific dominates the robotic welding market due to rapid industrial automation, expanding automotive and electronics manufacturing, rising labor costs, and increasing demand for precision, productivity, and high-quality welding solutions.

Leading companies in the robotic welding market include ABB Ltd., Comau (Stellantis N.V.), DAIHEN Corporation, FANUC Corporation, Hyundai Robotics Co. Ltd. (Hyundai Heavy Industries Group), Kawasaki Heavy Industries Ltd., KUKA AG, Nachi-Fujikoshi Corp., Panasonic Corporation, Siasun Robot & Automation Co. Ltd., Yaskawa Electric Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade