Russia Diabetes Market Size, Share, Trends and Forecast by Segment and Distribution Channel, 2026-2034

Russia Diabetes Market Size, Share, Trends & Forecast (2026-2034)

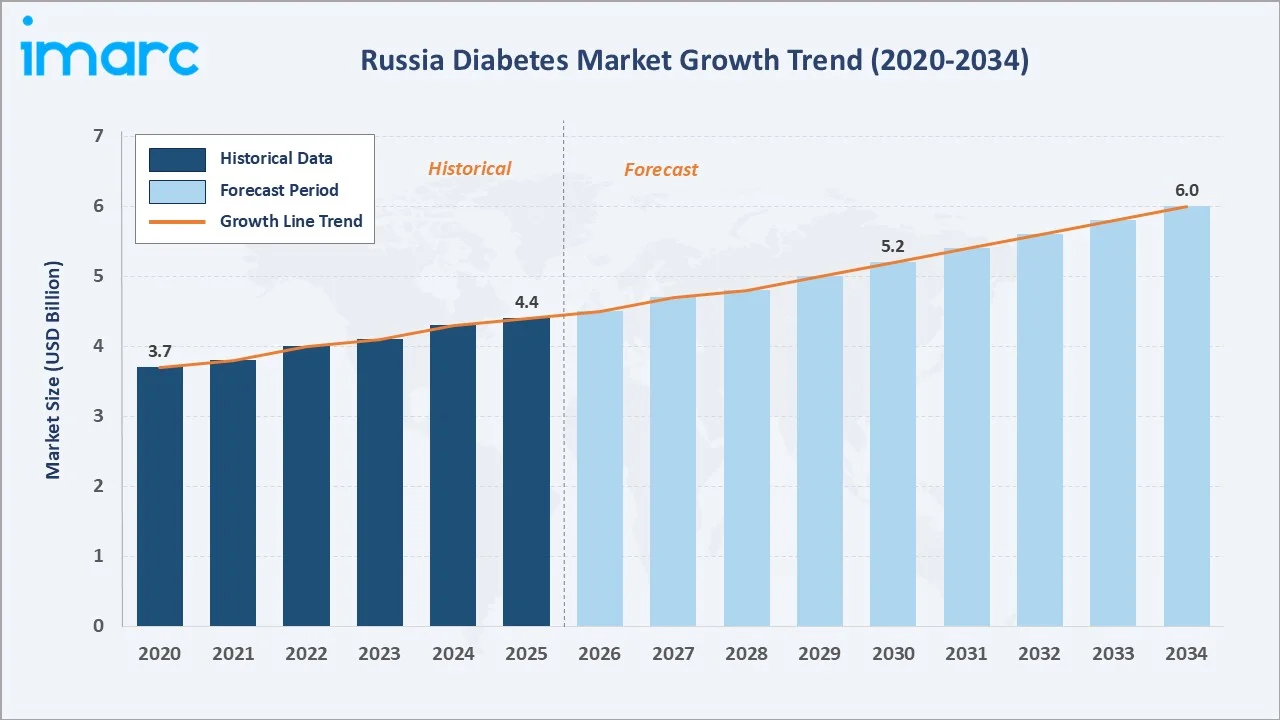

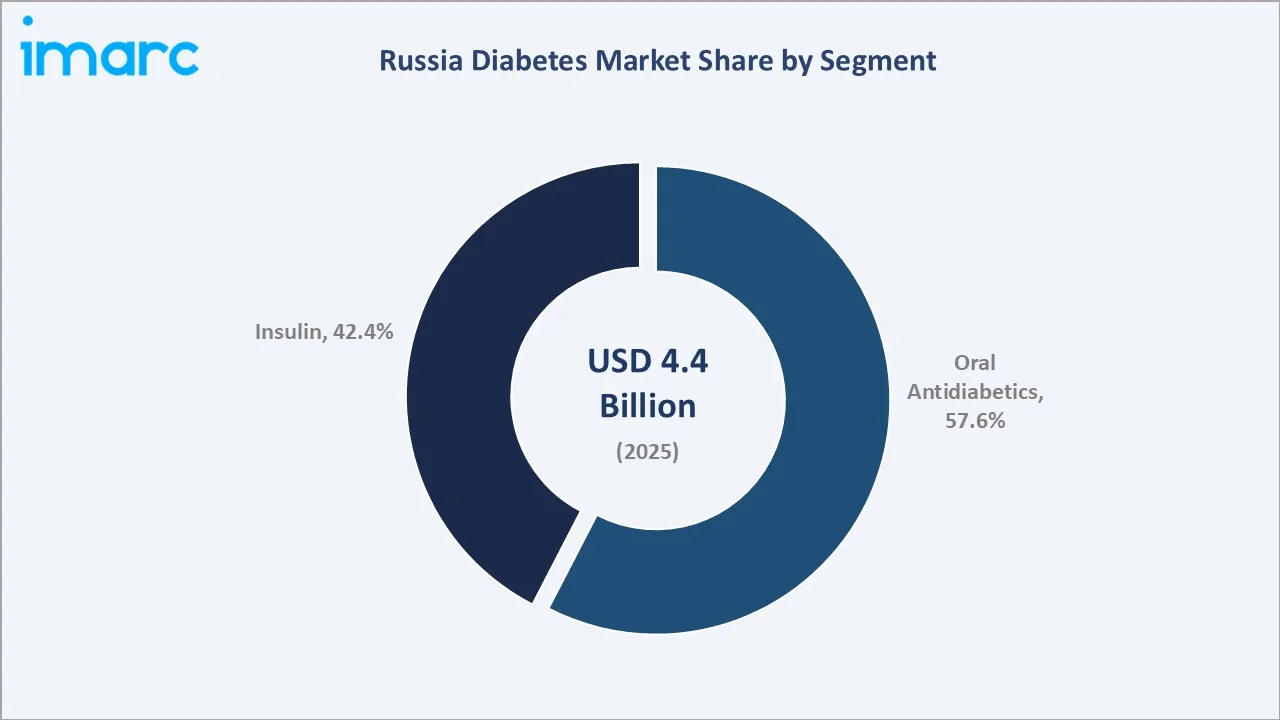

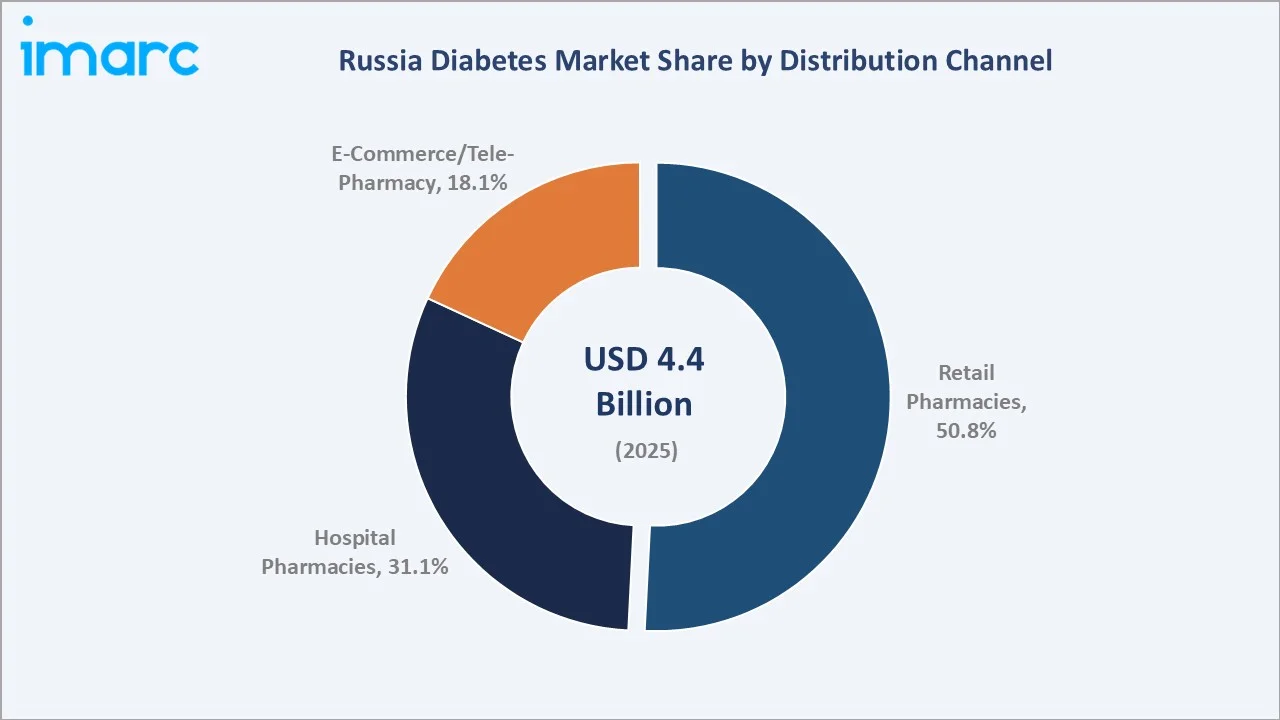

The Russia diabetes market was valued at USD 4.4 Billion in 2025 and is projected to reach USD 6.0 Billion by 2034, growing at a CAGR of 3.50% during 2026-2034. Russia recorded 7.6 million diabetes cases in adults aged 20-79 years in 2024. The market is driven by the rising prevalence of diabetes, aging population, obesity, and sedentary lifestyles, and continues to increase demand for long-term treatment and monitoring solutions. Oral antidiabetics lead at 57.6% segment share, and retail pharmacies dominate distribution at 50.8%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.4 Billion |

|

Forecast Market Size (2034) |

USD 6.0 Billion |

|

CAGR (2026-2034) |

3.50% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

The market grew from USD 3.7 Billion in 2020 to USD 4.4 Billion in 2025, anchored at USD 5.2 Billion in 2030, and forecast to reach USD 6.0 Billion by 2034. Growth is underpinned by Russia's rising diabetes burden, the government's 5.5 billion RUB diabetes funding allocation (November 2024), and the accelerating domestic pharmaceutical import substitution program expanding domestic insulin production.

To get more information on this market, Request Sample

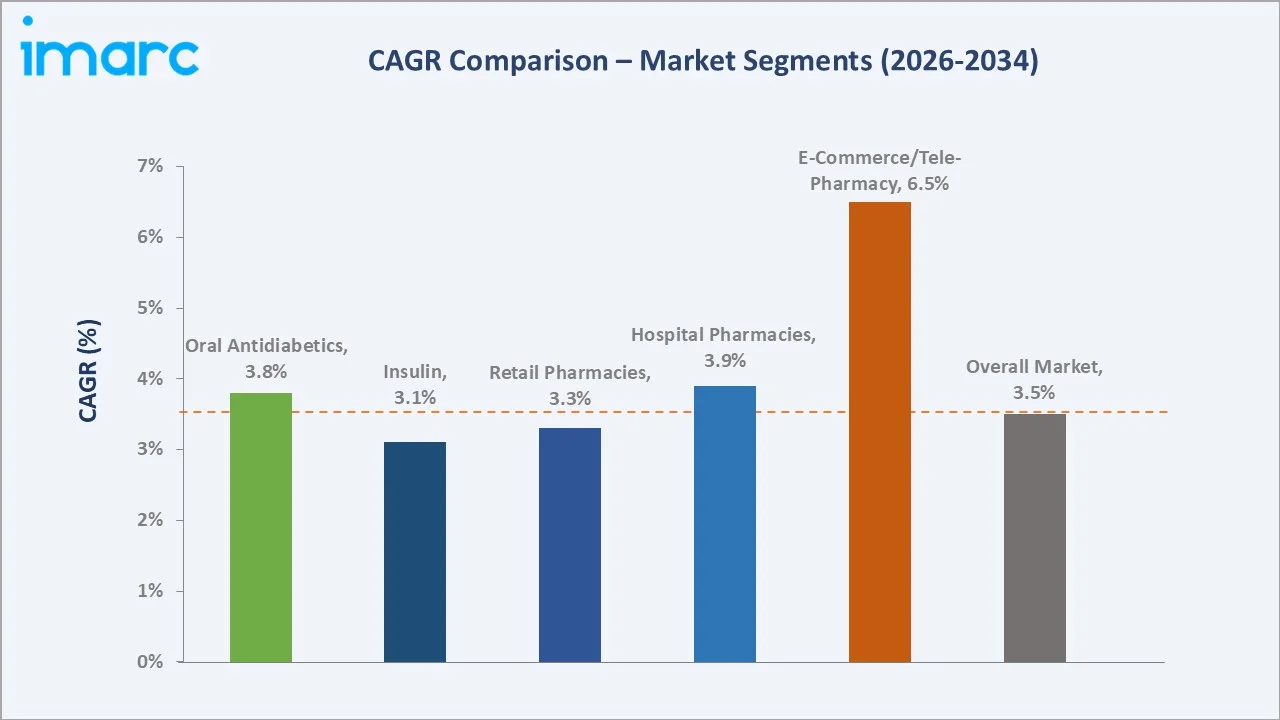

E-commerce/tele-pharmacy grows fastest at ~6.5% CAGR (2026-2034), driven by expanding online prescription fulfillment. Oral antidiabetics grow at ~3.8% CAGR versus Insulin at ~3.1%, supported by Russia's large generic metformin market and expanding SGLT-2 inhibitor prescriptions under VEDL reimbursement frameworks.

Executive Summary

The Russia diabetes market reached USD 4.4 Billion in 2025, operating within a unique geopolitical framework shaped by Western sanctions, government import substitution mandates, and domestic pharmaceutical champions rising to fill gaps left by multinational company withdrawals. Russia's 7.6 million registered diabetes adults (2024) create a structural and growing pharmaceutical demand. Russia's 3.50% CAGR to USD 6.0 Billion by 2034 reflects steady demand growth constrained by ruble depreciation and sanction-related supply disruptions, offset by government healthcare investment, domestic insulin production scaling, and digital pharmacy channel expansion

Oral antidiabetics lead at 57.6% share (2025), anchored by the high-volume metformin generic market, sulfonylureas, and an expanding SGLT-2 inhibitor tier. Insulin at 42.4% is undergoing a structural shift. Retail pharmacies at 50.8% remain dominant.

Key Market Insights

|

Insight |

Data |

|

Largest Segment |

Oral Antidiabetics - 57.6% revenue share (2025) |

|

Leading Distribution Channel |

Retail Pharmacies - 50.8% share (2025) |

Key Analytical Observations Supporting the Above Data:

- Oral antidiabetics at 57.6% (2025): Oral antidiabetics dominate the Russia diabetes market due to their cost-effectiveness, ease of administration, and widespread use as first-line therapy for the large type 2 diabetic population.

- Retail pharmacies at 50.8% anchored by Russia's licensed pharmacy network: Russia's federal pharmacy chains and regional independents form the backbone of commercial diabetes drug dispensing.

Russia Diabetes Market Overview

Russia's diabetes market encompasses pharmaceutical treatments and monitoring devices for type-1, type-2, and gestational diabetes patients. The ecosystem integrates API suppliers, domestic and multinational pharmaceutical manufacturers operating under Russia's import substitution mandate, regulatory framework, and multi-tier distribution serving 7.6 million registered patients.

Russia's pharmaceutical market operates under Roszdravnadzor (Federal Service for Surveillance in Healthcare) oversight. Post-2022 sanction effects have accelerated the government's pharma strategy, prioritizing domestic production of essential diabetes medicines. Macroeconomic influences include ruble volatility, Russia's aging-related type-2 diabetes surge, and healthcare budget resilience supported by hydrocarbon revenues.

Market Dynamics

To evaluate market opportunities, Request Sample

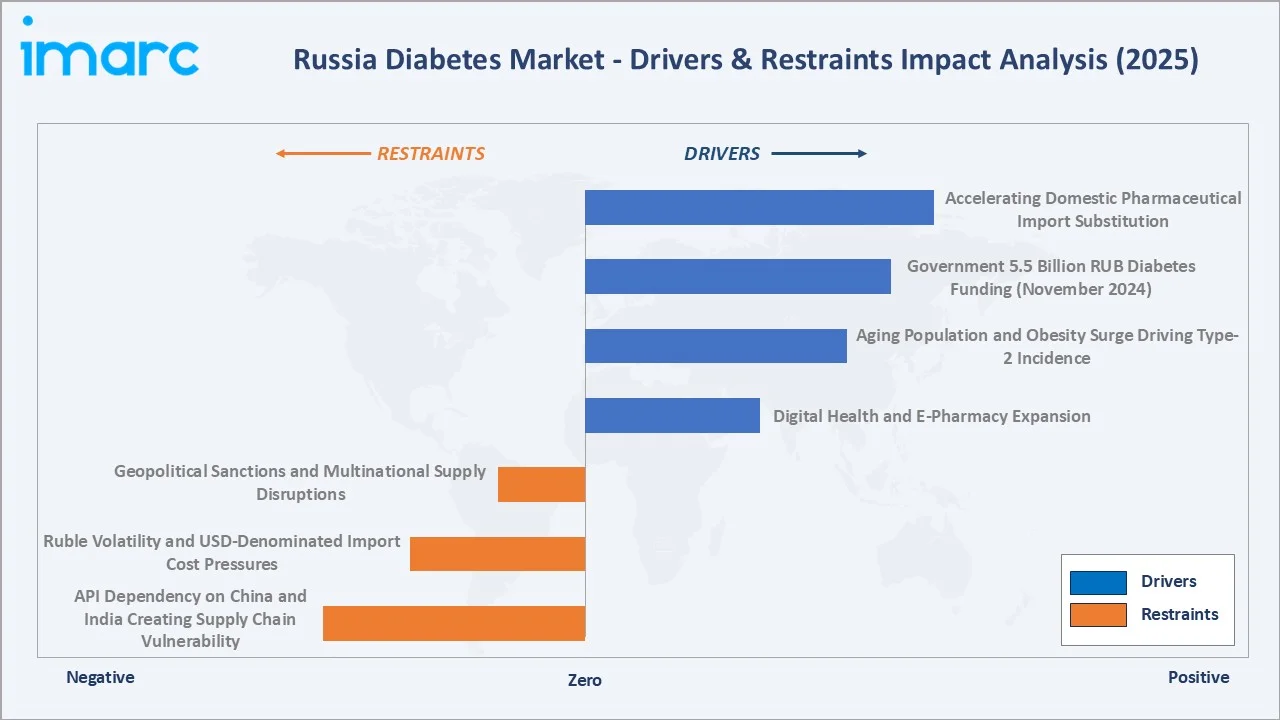

Market Drivers

- Aging Population and Obesity Surge Driving Type-2 Incidence: Russia's aging population is projected to reach 120 million by 2050, and has 2-3x higher type-2 diabetes prevalence versus the national average. Combined with Russia's adult obesity rate, the structural patient base grows predictably, creating compounding pharmaceutical demand for oral antidiabetics and insulin alike.

- Government 5.5 Billion RUB Diabetes Funding (November 2024): Russia's federal government committed 5.5 billion RUB to diabetes management in November 2024, specifically targeting early diagnosis infrastructure, pediatric diabetes detection programs, and regional endocrine center establishment. This creates direct procurement demand expansion for diagnostic devices, insulin, and oral antidiabetic medications in government channels.

Market Restraints

- Geopolitical Sanctions and Multinational Supply Disruptions: Post-2022 Western sanctions have disrupted supply chains for imported pharmaceutical active ingredients, packaging materials, and analytical equipment. Several multinational companies suspended new clinical trials and reduced their commercial activities in Russia, creating supply uncertainties for branded insulin analogs and GLP-1 agonists outside government compulsory license channels.

- Ruble Volatility and USD-Denominated Import Cost Pressures: Russia's pharmaceutical market relies on imported APIs. Ruble depreciation increases the cost of all imported pharmaceutical inputs, squeezing domestic manufacturer margins and creating inflationary pressure on out-of-pocket diabetes medication costs for patients.

Market Opportunities

- Domestic GLP-1 Biosimilar Development - Compulsory License Framework: The Russian Supreme Court has upheld the Russian government's power to issue compulsory licenses for essential medications, including generic versions of Ozempic (active ingredient: semaglutide). These domestically produced products are projected to capture Russia's semaglutide market by 2027, creating a domestic GLP-1 revenue stream without multinational royalty exposure.

- Digital Health and E-Pharmacy Expansion: Russia's digital health programs support telemedicine infrastructure and digital health platform development. AI-driven diabetes monitoring, teleconsultation, and prescription fulfillment platforms are further driving the market growth in the region.

Market Challenges

- API Dependency on China and India Creating Supply Chain Vulnerability: Russia's pharmaceutical manufacturers source most of the active pharmaceutical ingredients from China and India. Any disruption to these supply corridors, such as geopolitical, logistical, or regulatory, creates production vulnerability for domestically manufactured diabetes drugs, undermining the import substitution policy's strategic objectives.

Emerging Market Trends

1. Compulsory Licensing Reshaping GLP-1 Agonist Access

Russia’s Supreme Court upheld the government’s authority to grant compulsory licenses for essential medicines, enabling local production of semaglutide generics without consent from Novo Nordisk. This creates a precedent for compulsory licensing of other premium diabetes drugs, fundamentally reshaping market economics for multinational insulin and GLP-1 companies in Russia.

2. Regional Endocrine Center Infrastructure Buildout

Russia's November 2024 government diabetes funding includes dedicated allocations for the establishment of regional endocrine centers. This infrastructure expansion is creating new institutional pharmacy demand for CGM devices, insulin pumps, and specialty oral antidiabetics in regional capital cities previously served only by Moscow-based specialist referral networks.

3. SGLT-2 Inhibitor Expansion in the Commercial Market Segment

In December 2023, Daewoong Pharmaceutical signed an agreement with Russian firm JSC Pharmasyntez to export its SGLT-2 inhibitor Envlo for diabetes treatment to five Commonwealth of Independent States (CIS) countries, including Russia. Russia's SGLT-2 inhibitor class growth in commercial pharmacy channels, driven by cardiorenal comorbidity evidence translating to expanded cardiologist prescriptions beyond endocrinologists.

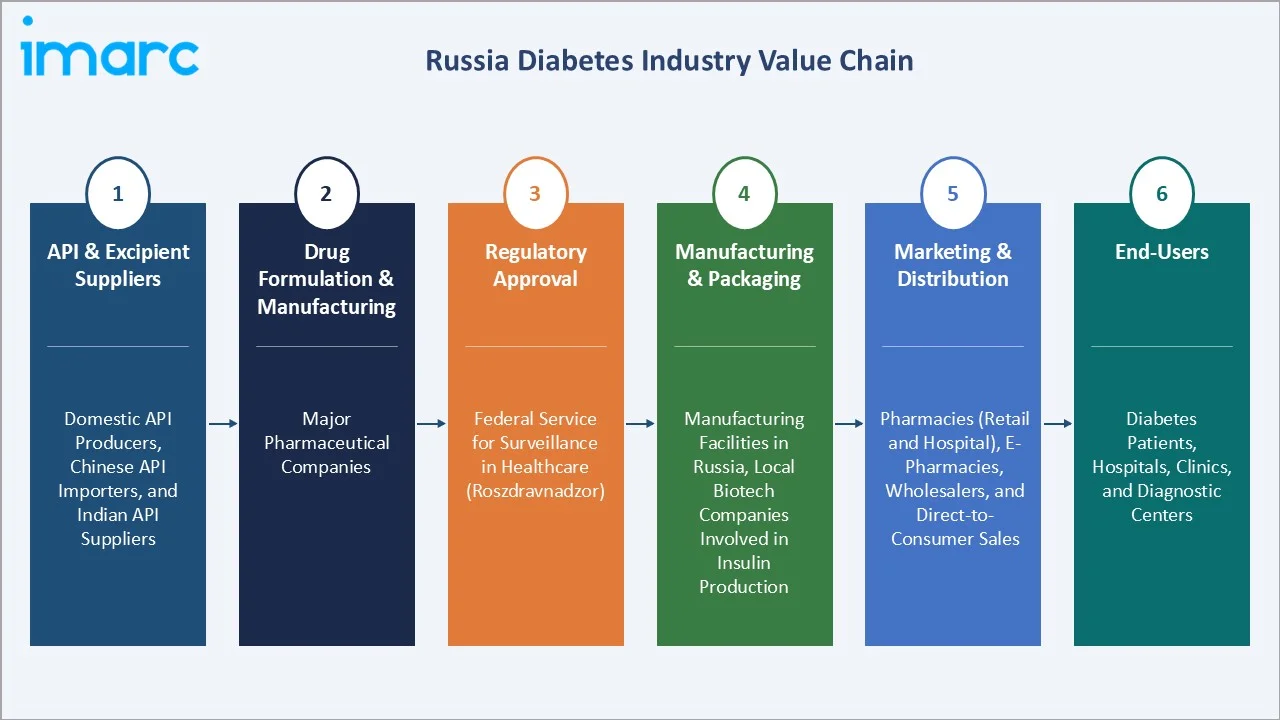

Industry Value Chain Analysis

Russia's diabetes market value chain integrates API supply (predominantly imported), pharmaceutical production under import substitution mandates, Roszdravnadzor regulatory approval, three-tier wholesale distribution, and retail/hospital/e-pharmacy dispensing serving 7.6 million adult patients (2024).

|

Stage |

Key Participants |

|

API & Excipient Suppliers |

Domestic API producers, Chinese API importers, and Indian API suppliers |

|

Drug Formulation & Manufacturing |

Major pharmaceutical companies |

|

Regulatory Approval |

Federal Service for Surveillance in Healthcare (Roszdravnadzor) |

|

Manufacturing & Packaging |

Manufacturing facilities in Russia, local biotech companies involved in insulin production |

|

Marketing & Distribution |

Distribution channels through pharmacies (both retail and hospital), e-pharmacies, wholesalers, and direct-to-consumer sales |

|

End-Users |

Diabetes patients, hospitals, clinics, and diagnostic centers |

Russia's pharmaceutical distribution operates under a three-tier structure: manufacturers to federal distributors to regional sub-distributors to pharmacies. Government procurement represents ~60% of total diabetes drug revenues, with direct tender contracts bypassing retail distribution for hospital and regional endocrine center supply.

Technology Landscape in the Russia Diabetes Industry

Domestic Insulin Production Technology

Geropharm's full-cycle insulin synthesis platform represents Russia's most strategically significant pharmaceutical technology investment. The company synthesizes insulin substance domestically.

Continuous Glucose Monitoring (CGM) and Digital Devices

In December 2025, InnoBioSystems showcased its CGM Fly continuous glucose monitoring system, developed by its R&D engineering center, at Russian Health Care Week 2025, drawing significant attention from industry stakeholders. Although still undergoing certification, the device attracted strong interest from regulatory authorities, businesses, and potential partners, highlighting growing demand and market relevance for advanced glucose monitoring solutions, creating a market opportunity.

Biosimilar Semaglutide and GLP-1 Technology

In August 2024, Russia’s Ministry of Health approved a third domestic generic of Ozempic (semaglutide), originally developed by Novo Nordisk. This is driving the Russia diabetes market by improving affordability and supply of GLP-1 therapies, accelerating adoption amid rising demand and import constraints. The technology transfer from insulin to GLP-1 manufacturing positions Russian domestic companies for next-generation diabetes biologic production through 2034.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Segment | Oral Antidiabetics | 57.6% | 2025 |

| Distribution Channel | Retail Pharmacies | 50.8% | 2025 |

By Segment

Oral antidiabetics lead at 57.6% market share (2025). Russia's type-2 first-line protocol mandates creating a structurally large, price-controlled generic prescription base. SGLT-2 inhibitors are growing at 15-18% annually in the commercial prescription segment, positioning for revenue growth above the generic oral antidiabetic tier.

To access detailed market analysis, Request Sample

Insulin at 42.4% is undergoing structural transformation. Branded insulin analogs retain commercial pharmacy market presence for patients outside the government benefits program. The insulin segment grows at ~3.1% CAGR (2026-2034), constrained by government price controls but supported by patient volume growth.

By Distribution Channel

Retail pharmacies lead at 50.8% share (2025). Russia's licensed pharmacies are the primary diabetes medication dispensing channel for both commercial and reimbursement prescriptions. The channel grows at ~3.3% CAGR through 2034, supported by pharmacy chain consolidation improving operational efficiency.

Hospital pharmacies at 31.1% serve inpatient diabetes management and outpatient specialist clinic prescriptions across Russia's hospitals. E-commerce/tele-pharmacy at 18.1% grows fastest at ~6.5% CAGR, driven by healthcare digital platform collectively processing chronic disease prescriptions.

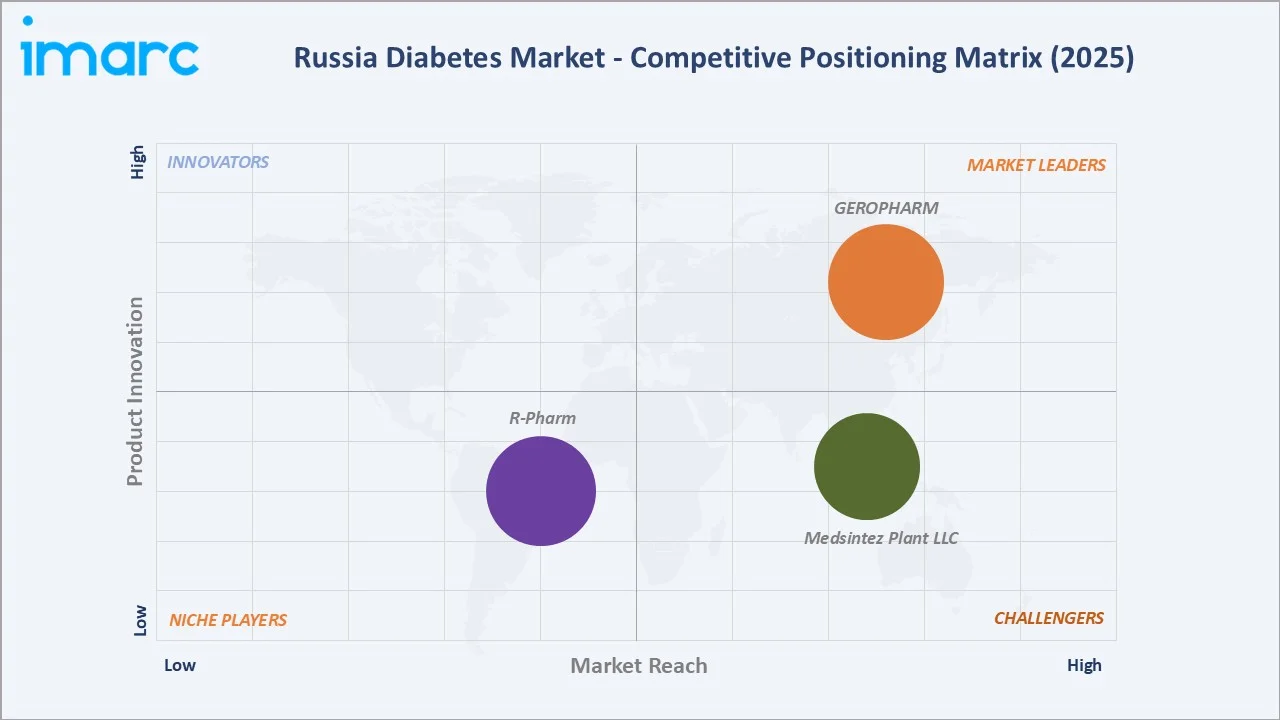

Competitive Landscape

Russia's diabetes pharmaceutical market is moderately concentrated at the government procurement level and increasingly domestic-dominant. Geropharm JSC and Pharmstandard together account for ~30-35% of Russia's government diabetes drug procurement (2025), a share that has grown rapidly from ~12% in 2019. Multinational companies (Novo Nordisk, Sanofi) retain significant commercial market positions but face structural displacement in the government channel.

|

Company Name |

Brand / Product |

Market Position |

Core Strength |

|

GEROPHARM |

Semavic, Sejaro (tirzepatide), Semavic Next, RinLis (insulin lispro), RinGlar (insulin glargine), RinLis Mix 25 |

Market Leader |

GEROPHARM is in the top-3 on the Russian insulin market. The company produces insulins on a full-cycle basis - from substance to finished dosage form. |

|

R-Pharm |

Ravidaglin (Sitagliptin), Vilmitrix (Vildagliptin), Vilmitrix MET (Vildagliptin+Metformin) |

Niche Player |

Domestic diabetes company offering Ravidaglin, Vilmitrix, and Vilmitrix MET for diabetes patients |

|

Medsintez Plant LLC |

ROSINSULIN ASPART R, ROSINSULIN R Medsintez, Prefilled syringe pen ROSINSULIN, Reusable syringe pen ROSINSULIN ComfortPen |

Strong Challenger |

The company offers a wide range of finished dosage forms of genetically engineered and analog human insulin productsTop of FormBottom of Form |

The competitive landscape is uniquely bifurcated, government procurement is increasingly dominated by domestic Russian manufacturers under import substitution policies, while the commercial prescription market retains significant multinational brand presence for premium insulin analogs and SGLT-2 inhibitors among patients. This dual-market structure creates distinct competitive strategies for domestic versus multinational players.

Key Company Profiles

GEROPHARM

GEROPHARM is Russia's leading full-cycle insulin manufacturer and the most strategically significant pharmaceutical company in Russia's diabetes market transformation.

- Product Portfolio: Semavic, Sejaro (tirzepatide), Semavic Next, RinLis (insulin lispro), RinGlar (insulin glargine), RinLis Mix 25, Rinsulin NPH, RinFast, Rinsulin R, Rinsapen II.

- Recent Developments: In October 2023, GEROPHARM relaunched Ozempic in Russia, under the name of Semavic, a semaglutide product, after Novo Nordisk’s withdrawal created a market gap.

- Strategic Focus: Full-cycle insulin synthesis for reduced dependence on imported supply chains.

Medsintez Plant LLC

Medsintez Plant LLC is a key Russia-based biopharmaceutical manufacturer specializing in genetically engineered human insulin and advanced biologics, playing a significant role in strengthening domestic diabetes drug supply and reducing reliance on imports.

- Product Portfolio: ROSINSULIN ASPART R, ROSINSULIN GLARGINE, ROSINSULIN R Medsintez, ROSINSULIN S Medsintez, Prefilled syringe pen ROSINSULIN, Reusable syringe pen ROSINSULIN ComfortPen.

- Recent Developments: In 2023, Medsintez Plant, in partnership with the Promomed Group, initiated full-cycle production of the hypoglycemic drugs Enligria (liraglutide) and Quincenta (semaglutide), used for treating type 2 diabetes, including patients with obesity, overweight, or cardiovascular conditions.

- Strategic Focus: End-to-end insulin production with emphasis on localization and next-generation diabetes therapies to support Russia’s import substitution strategy.

Market Concentration Analysis

Russia's diabetes market exhibits a distinctive dual-tier concentration structure. In the government procurement segment, domestic manufacturers collectively held 44-50% of insulin tender contracts, with this share growing rapidly under import substitution preferences. In the commercial pharmacy market, multinational companies retain 60-65% value share through premium branded insulin analogs, SGLT-2 inhibitors, and GLP-1 agonists accessible only to patients. This dual-market structure creates a high-value commercial niche for multinationals even as government channel share erodes to domestic producers.

Consolidation trends include Russia's pharmacy chain consolidation, Geropharm's inorganic expansion into export markets, and the rapid rise in GLP-1 biosimilars. The compulsory license framework for semaglutide creates a template for potential future consolidation of GLP-1 and other novel diabetes drug markets around domestic Russian producers.

Investment & Growth Opportunities

Fastest Growing Segments

E-commerce/tele-pharmacy channel (~6.5% CAGR), domestic GLP-1 biosimilar market (~20-25% CAGR), CGM device market (~15% CAGR), digital diabetes management platforms (~20% CAGR), and SGLT-2 inhibitor commercial market (~8-10% CAGR) represent Russia's highest-growth investment vectors through 2034. Domestic semaglutide production under compulsory license represents the single highest-value pharmaceutical investment opportunity within Russia's current regulatory framework.

Emerging Market Opportunities

Russia's total number of diabetes patients represents a systematic diagnosis gap opportunity. Government endocrine center expansion programs targeting some regions are designed to systematically increase diagnosed patient registration, potentially adding newly-diagnosed patients to the treatment market by 2030. Each newly-diagnosed patient generates 10-15 years of prescription demand for oral antidiabetics and/or insulin.

Investment Themes

- Domestic API production for insulin and GLP-1: Russia's API import dependency is its pharmaceutical sector's greatest strategic vulnerability. Investment in domestic insulin API synthesis addresses strategic security needs while generating stable, government-backed procurement revenues under the 'Second Extra' preference framework.

- E-pharmacy platform expansion into Tier-2 and Tier-3 cities: Russia's digital pharmacy market penetration outside Moscow and St. Petersburg remains low in terms of prescriptions.

Future Market Outlook (2026-2034)

The Russia diabetes market is projected to grow from USD 4.4 Billion in 2025 to USD 6.0 Billion by 2034, at a 3.50% CAGR reflecting steady patient volume growth moderated by geopolitical constraints on premium drug access and systematic government price controls. Russia's USD 5.2 Billion market in 2030 will reflect a fundamentally transformed competitive structure versus 2020, with domestic manufacturers holding majority government procurement positions across both insulin and oral antidiabetic segments.

Three structural forces define Russia's diabetes market trajectory through 2034 with distinct visibility: irreversible demographic aging continuously expanding the Type-2 patient base; the import substitution policy creating a permanent domestic manufacturer advantage in government procurement that compounds as Geropharm and Medsintez expand their biosimilar portfolios; and the compulsory license framework establishing a regulatory template for domestic GLP-1 and future novel diabetes drug production at scale.

Research Methodology

Primary Research

Primary research comprised structured interviews with 75+ industry stakeholders, including Russian endocrinologists from the Endocrinology Research Centre (Moscow) and regional diabetes centers, pharmaceutical company Russia general managers, Roszdravnadzor regulatory and pricing specialists, federal distributor executives, and retail pharmacy chain directors.

Secondary Research

Secondary research encompassed Russia's State Diabetes Register 2024, Ministry of Health drug pricing, Roszdravnadzor registration database, Federal State Statistics Service (Rosstat) health expenditure data, Russia government budget allocation documents (November 2024 diabetes funding announcement), DSM Group pharmaceutical market reports, and company filings. Over 130 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using bottom-up patient population x treatment penetration x government/commercial revenue per patient models, validated against DSM Group prescription audit data and VEDL procurement statistics. Key inputs include Russia's State Diabetes Register growth trends, import substitution policy escalation scenarios, ruble/USD exchange rate projections, e-pharmacy adoption curves by city tier, and Rosstat demographic aging projections for Russia's federal districts through 2034.

Russia Diabetes Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Oral Antidiabetics, Insulin |

| Distribution Channels Covered | Online Pharmacies, Hospital Pharmacies, Retail Pharmacies |

| Companies Covered | GEROPHARM, R-Pharm, Medsintez Plant LLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Russia diabetes market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Russia diabetes market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Russia diabetes industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Russia Diabetes Market Report

The Russia diabetes market was valued at USD 4.4 Billion in 2025, covering oral antidiabetics, insulin therapies, monitoring devices, and digital health solutions for approximately 7.6 million registered diabetes patients.

The Russia diabetes market is projected to grow at a CAGR of 3.50% during 2026-2034, reaching USD 6.0 Billion by 2034, driven by rising diabetes prevalence, government healthcare investment, domestic pharmaceutical expansion, and e-pharmacy growth.

Oral antidiabetics lead at 57.6% market share (2025), anchored by metformin first-line protocol and expanding SGLT-2 inhibitor prescriptions in the commercial specialist channel.

Retail pharmacies hold the largest share at 50.8% (2025), anchored by Russia's licensed pharmacy network.

E-commerce/tele-pharmacy grows fastest at ~6.5% CAGR (2026-2034), driven by healthcare digital platform processing chronic disease prescriptions digitally under expanded online pharmacy legislation.

Leading companies include GEROPHARM, R-Pharm, and Medsintez Plant LLC, among others.

In November 2024, Russia's government allocated 5.5 billion RUB to combat diabetes, targeting early diagnosis, regional endocrine center establishment, essential medication supply, and pediatric diabetes detection programs across Russia's federal regions.

Insulin holds 42.4% of Russia's diabetes market (2025), undergoing structural transformation as Geropharm and Medsintez capture government procurement share, while multinational brands retain commercial channel positions.

Russia's diabetes market is projected to reach approximately USD 5.2 Billion by 2030, driven by domestic insulin expansion to government procurement and e-pharmacy capturing high distribution share.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade