Sales Intelligence Market Size, Share, Trends and Forecast by Component, Deployment Mode, Enterprise Size, Application, Industry Vertical, and Region, 2026-2034

Sales Intelligence Market Size and Share:

The global sales intelligence market size was valued at USD 4.06 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 9.53 Billion by 2034, exhibiting a CAGR of 9.95% from 2026-2034. North America currently dominates the market, holding a market share of 35%. The market encompasses advanced technologies and platforms that enable organizations to gather, analyze, and leverage comprehensive data insights for optimizing sales strategies and customer engagement. These solutions integrate artificial intelligence, machine learning, and analytics capabilities to provide real-time intelligence on prospects, competitors, and market dynamics. Organizations utilize these platforms to enhance lead generation, improve conversion rates, and accelerate revenue growth through data-driven decision making, thereby strengthening their competitive positioning and sales intelligence market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 4.06 Billion |

| Market Forecast in 2034 | USD 9.53 Billion |

| Market Growth Rate (2026-2034) | 9.95% |

The global expansion of digital transformation initiatives across industries represents a fundamental catalyst propelling market advancement. Organizations worldwide increasingly recognize the imperative of leveraging data-driven insights to navigate complex competitive landscapes and achieve sustainable growth. For instance, Salesforce rolled out its new AI platform Agentforce 360 for global availability — connecting humans, AI agents and data on one trusted system, thereby enabling modern sales teams to operate with unprecedented intelligence and speed.The proliferation of big data analytics, cloud computing infrastructure, and advanced artificial intelligence capabilities has democratized access to sophisticated sales intelligence tools previously available only to enterprise-level organizations. Furthermore, the intensification of global competition compels businesses to adopt proactive approaches in identifying opportunities, understanding customer behavior patterns, and anticipating market shifts. The convergence of social media platforms, professional networking sites, and digital communication channels generates unprecedented volumes of actionable intelligence. Modern sales teams require comprehensive visibility into prospect activities, engagement patterns, and decision-making processes to effectively personalize outreach strategies and maximize conversion potential, thereby transforming traditional sales methodologies into data-centric, precision-targeted operations that deliver measurable business outcomes.

To get more information on this market Request Sample

The United States maintains a commanding position accounting for 86% of market adoption, driven by the concentration of technology innovation hubs and early adopter organizations. American enterprises demonstrate exceptional receptivity to emerging sales technologies, supported by robust venture capital funding, entrepreneurial ecosystems, and progressive business cultures that prioritize innovation. The maturity of digital infrastructure across metropolitan and regional markets facilitates seamless deployment and integration of advanced intelligence platforms. Additionally, the competitive intensity characterizing American business environments necessitates continuous optimization of sales operations and customer acquisition strategies. Organizations face mounting pressure to demonstrate measurable returns on marketing investments while simultaneously reducing customer acquisition costs and accelerating sales cycles. The abundance of skilled technology professionals established software development capabilities, and sophisticated go-to-market strategies position American enterprises at the forefront of sales intelligence adoption. This technological leadership reinforces feedback loops that drive continuous platform enhancements, feature innovations, and integration capabilities that benefit the broader market ecosystem.

Sales Intelligence Market Trends:

Artificial Intelligence Integration

The integration of artificial intelligence and machine learning algorithms represents a transformative development reshaping how organizations approach sales operations. Advanced natural language processing capabilities enable automated analysis of communication patterns, sentiment detection, and predictive scoring of lead quality based on historical conversion data. Intelligent recommendation engines provide sales professionals with contextually relevant insights, suggested talking points, and optimal engagement timing to maximize interaction effectiveness. Furthermore, AI-powered automation handles routine administrative tasks, data entry operations, and preliminary prospect research, liberating sales teams to focus on relationship building and strategic engagement activities. Predictive analytics models identify patterns indicating purchase intent, enabling proactive outreach before competitors recognize opportunities. For example, Microsoft Corporation has introduced two new AI “Sales Agent” tools under its Microsoft 365 Copilot suite—designed to autonomously convert contacts into qualified leads and provide real‑time deal risk assessments—marking a significant move toward embedding AI deeply in sales workflows. The continuous learning capabilities of modern AI systems ensure ongoing performance optimization as platforms accumulate additional data points and refine algorithmic accuracy. Organizations leveraging these capabilities achieve substantial improvements in sales productivity, forecast accuracy, and revenue generation efficiency.

Integration with Customer Relationship Management Systems

The seamless integration between sales intelligence platforms and customer relationship management systems emerges as a critical capability addressing organizational needs for unified data ecosystems. Modern enterprises demand comprehensive visibility across entire customer lifecycles, from initial prospecting through post-sale relationship management. Integration eliminates data silos that historically impeded information flow between marketing, sales, and customer success functions. Automated data synchronization ensures sales professionals access current intelligence without manual data entry or system switching, thereby maintaining engagement momentum and reducing administrative overhead. For example, S&P Global launched its “Capital IQ Pro Document Intelligence” tool on Salesforce AgentExchange — enabling real‑time document analysis and sentiment insights directly within the CRM platform, thereby enriching CRM records with external intelligence while simultaneously feeding interaction history back into intelligence workflows. Advanced integration capabilities enable bi-directional data flow, enriching CRM records with external intelligence while simultaneously feeding interaction history back into intelligence platforms for enhanced context. The Sales Intelligence Market trends indicate growing emphasis on workflow automation that triggers specific actions based on intelligence signals, prospect behaviors, or predetermined criteria. Organizations implementing integrated solutions report improved data quality, enhanced collaboration across revenue teams, and accelerated decision-making processes that translate directly into competitive advantages.

Mobile-First Platform Development

The evolution toward mobile-first platform architectures reflects fundamental shifts in how sales professionals conduct business activities and consume intelligence. Modern sales teams operate increasingly from distributed locations, requiring immediate access to prospect information, company insights, and engagement recommendations regardless of physical location or device. Mobile applications delivering full-featured functionality enable real-time intelligence access during client meetings, networking events, and travel scenarios where desktop access proves impractical. Progressive web technologies provide responsive experiences that adapt seamlessly across smartphones, tablets, and desktop environments without compromising functionality or user experience. Offline synchronization capabilities ensure uninterrupted access to critical intelligence even in connectivity-challenged environments, with automatic updates occurring upon network restoration. Voice-activated interfaces and conversational AI integration enable hands-free information retrieval while driving or multitasking. The mobile-first approach democratizes access to enterprise-grade intelligence capabilities, empowering field sales representatives, remote workers, and distributed teams with equivalent resources regardless of location, thereby maximizing organizational sales capacity and responsiveness.

Sales Intelligence Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global sales intelligence market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on component, deployment mode, enterprise size, application, and industry vertical.

Analysis by Component:

To get detailed segment analysis of this market Request Sample

- Software

- Services

Software solutions dominate the component landscape, commanding 72% of market allocation driven by the inherent flexibility, scalability, and continuous enhancement capabilities that cloud-native architectures provide. Organizations increasingly favor subscription-based software models that eliminate substantial upfront capital expenditures while providing predictable operational expenses and automatic access to feature updates and security patches. The software-centric approach enables rapid deployment cycles, seamless integration with existing technology stacks, and customization capabilities that address industry-specific requirements. Advanced software platforms incorporate modular architectures allowing organizations to activate specific features aligned with business priorities while maintaining options for expansion as needs evolve. Furthermore, software solutions benefit from network effects where platform improvements, enhanced data coverage, and refined algorithms benefit entire user communities simultaneously. The convergence of artificial intelligence, natural language processing, and predictive analytics within unified software frameworks delivers comprehensive capabilities that would require multiple disparate tools in traditional technology environments, thereby simplifying vendor management and reducing integration complexity.

Analysis by Deployment Mode:

- On-premises

- Cloud-based

Cloud-based deployment architectures represent 68% of implementations, reflecting fundamental shifts in enterprise technology preferences toward agile, scalable infrastructure models. Organizations embrace cloud platforms for their ability to eliminate hardware maintenance responsibilities, reduce total cost of ownership, and provide instant scalability to accommodate fluctuating user populations and data volumes. Cloud deployments facilitate remote workforce enablement, delivering consistent user experiences across geographies and devices without complex virtual private network configurations or security concerns. The subscription-based pricing models characteristic of cloud services align expenses directly with utilization patterns, enabling organizations to optimize spending based on actual requirements rather than projected capacity needs. Additionally, cloud providers assume responsibility for security updates, compliance certifications, disaster recovery, and business continuity planning, thereby reducing internal IT workloads and risk exposure. The sales intelligence market growth trajectory emphasizes cloud-native architectures that leverage containerization, microservices, and API-first designs enabling rapid feature deployment and integration ecosystem expansion that accelerates organizational innovation velocity.

Analysis by Enterprise Size:

- Large Enterprises

- Small and Medium-sized Enterprises

Large enterprises constitute 65% of adoption, driven by sophisticated sales operations, complex organizational structures, and substantial budgets allocated toward technology modernization initiatives. These organizations manage extensive customer portfolios spanning multiple geographies, industries, and market segments, necessitating comprehensive intelligence capabilities that provide visibility across diverse sales motions. Large enterprises possess dedicated revenue operations teams responsible for technology stack optimization, data governance, and performance analytics that smaller organizations often lack. The scale of operations justifies substantial investments in advanced platforms offering enterprise-grade features including single sign-on authentication, role-based access controls, audit logging, and compliance certifications required by regulated industries. Furthermore, large enterprises demonstrate greater willingness to invest in change management, training programs, and process redesign initiatives essential for maximizing platform value realization. Their established vendor relationships, procurement processes, and technology evaluation frameworks facilitate sophisticated solution assessments that evaluate total cost of ownership, integration requirements, and long-term strategic alignment beyond initial licensing costs.

Analysis by Application:

- Lead Management

- Data Management

- Analytics and Reporting

- Others

Lead management applications capture 34% of utilization, addressing fundamental business requirements for systematic prospect identification, qualification, and progression through sales funnels. Organizations recognize lead management as the foundation upon which revenue generation depends, driving investment in capabilities that optimize lead sources, scoring methodologies, and routing algorithms. Effective lead management platforms aggregate prospect information from multiple channels including website interactions, content downloads, event participation, and social media engagement into unified profiles that provide comprehensive context for sales outreach. Advanced scoring models evaluate behavioral signals, demographic attributes, and firmographic characteristics to prioritize opportunities demonstrating highest conversion probability. Automated nurturing workflows maintain engagement with prospects not yet ready for direct sales contact, delivering personalized content that educates, builds trust, and advances buying journeys. Integration with marketing automation platforms creates closed-loop feedback mechanisms that inform campaign optimization and budget allocation decisions. Organizations implementing sophisticated lead management capabilities report substantial improvements in conversion rates, sales cycle duration, and cost per acquisition metrics that directly impact profitability.

Analysis by Industry Vertical:

- BFSI

- IT and Telecom

- Retail and E-Commerce

- Healthcare

- Media and Entertainment

- Others

The Banking, Financial Services, and Insurance sector accounts for 22% of adoption, reflecting the industry's sophisticated sales operations, complex product portfolios, and stringent regulatory requirements that demand comprehensive intelligence capabilities. Financial institutions manage intricate customer relationships spanning multiple product lines, service offerings, and lifecycle stages that benefit substantially from unified intelligence platforms. The competitive intensity characterizing financial services markets compels organizations to identify cross-sell opportunities, anticipate customer needs, and deliver personalized experiences that strengthen retention and lifetime value. Furthermore, regulatory compliance obligations necessitate detailed documentation of customer interactions, decision rationales, and advisory processes that intelligence platforms facilitate through automated tracking and reporting capabilities. The wealth management and insurance sectors particularly benefit from intelligence tools that identify life events, wealth transitions, and risk profile changes triggering product needs. Financial services organizations demonstrate willingness to invest premium amounts for industry-specific features, compliance certifications, and data security standards that protect sensitive financial information and maintain customer trust.

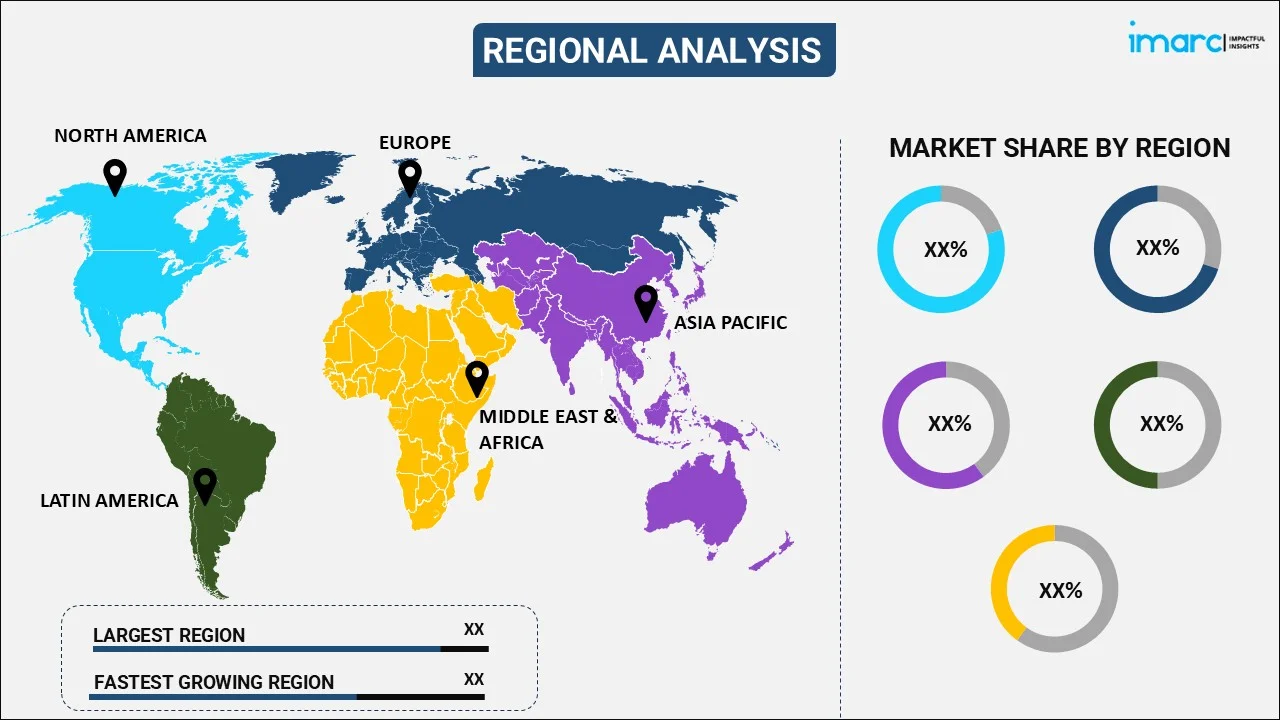

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America maintains market leadership across the global landscape, benefiting from technology-forward business environments, substantial investment in sales enablement initiatives, and mature digital infrastructure supporting advanced platform deployment. The market holds a total share of 35%. North American enterprises benefit from proximity to leading technology vendors, access to specialized implementation partners, and established communities of practice that accelerate knowledge transfer and best practice adoption. The regulatory environment generally favors business innovation while maintaining data protection standards that build customer confidence in platform security. Additionally, North American markets demonstrate strong preferences for subscription-based software models that align with sales intelligence delivery mechanisms. The concentration of multinational corporations headquartered within the region drives demand for global deployment capabilities, multi-language support, and regional data compliance features. Furthermore, the robust venture capital ecosystem funds continuous platform innovation, emerging vendor competition, and technology advancement that benefits organizational buyers through expanding feature sets and competitive pricing dynamics.

Key Regional Takeaways:

United States Sales Intelligence Market Analysis

The United States demonstrates exceptional market maturity characterized by widespread adoption across enterprises of all sizes, robust technology infrastructure, and established vendor ecosystems providing comprehensive solution portfolios. American organizations exhibit sophisticated understanding of sales intelligence value propositions, supported by extensive case studies, industry research, and peer validation demonstrating measurable returns on investment. The concentration of technology companies, venture capital funding, and innovation hubs within major metropolitan areas fosters continuous platform enhancement and feature development. Additionally, American business culture emphasizes data-driven decision making, performance optimization, and technology-enabled productivity gains that align naturally with sales intelligence capabilities. The competitive intensity across industries compels organizations to maintain technological parity with market leaders, driving accelerated adoption cycles. Furthermore, the maturity of integration ecosystems enables seamless connectivity between sales intelligence platforms and complementary technologies including marketing automation, customer success management, and business intelligence tools. The combination of favorable economic conditions, technology literacy, and established best practices positions the United States as the global epicenter for sales intelligence innovation and adoption.

Asia Pacific Sales Intelligence Market Analysis

Asia Pacific emerges as a high-growth region characterized by rapid digital transformation, expanding middle-class consumer populations, and increasing technology investment by enterprises seeking competitive differentiation. The sales intelligence market outlook for this geography indicates substantial expansion potential driven by economic development, urbanization trends, and growing recognition of data-driven sales methodologies. Countries including India, China, Australia, Singapore, and Japan demonstrate varying adoption patterns reflecting diverse economic development stages, regulatory environments, and technology maturity levels. Multinational corporations operating within the region drive initial adoption as they extend enterprise platforms from headquarters to regional operations. Additionally, indigenous technology companies emerge as regional vendors offering localized solutions addressing language requirements, cultural considerations, and market-specific business practices. The mobile-first orientation of Asian markets aligns naturally with modern platform architectures designed for smartphone access and distributed workforce support. Furthermore, government initiatives promoting digital economy development and technology adoption create favorable environments for sales intelligence deployment across industries.

Europe Sales Intelligence Market Analysis

Europe demonstrates sophisticated market characteristics influenced by stringent data protection regulations, diverse linguistic requirements, and established business cultures valuing relationship-driven sales approaches balanced with technological innovation. The General Data Protection Regulation framework significantly impacts platform capabilities, requiring comprehensive consent management, data portability features, and transparent processing documentation that vendors must accommodate to serve European customers. Organizations across the United Kingdom, Germany, France, and Benelux countries lead regional adoption, driven by competitive pressures and digital transformation initiatives. The linguistic diversity characterizing European markets necessitates multi-language platform support, localized user interfaces, and culturally appropriate content that respects regional business customs. Furthermore, European enterprises demonstrate measured technology adoption patterns emphasizing thorough evaluation processes, proof-of-concept implementations, and gradual rollout strategies that differ from more aggressive American deployment approaches. The presence of established industry sectors including automotive manufacturing, pharmaceutical development, and financial services creates demand for vertical-specific intelligence capabilities addressing unique sales motion requirements.

Latin America Sales Intelligence Market Analysis

Latin America represents an emerging market characterized by growing technology adoption, expanding digital infrastructure, and increasing recognition of sales intelligence benefits among progressive enterprises. Countries including Brazil, Mexico, Argentina, and Chile lead regional development, supported by economic growth, urbanization trends, and government initiatives promoting digital transformation across public and private sectors. The region exhibits substantial growth potential as organizations modernize legacy sales processes and adopt contemporary best practices observed in more mature markets. Challenges including economic volatility, currency fluctuations, and varying regulatory frameworks across countries influence adoption patterns and investment priorities. Nevertheless, multinational corporations operating within Latin America drive platform deployment as they extend global technology standards to regional operations. Additionally, the growing presence of technology service providers, implementation partners, and localized support resources reduces barriers to adoption. The demographic trends characterizing Latin American markets, including large youth populations comfortable with digital technologies and mobile-first internet access patterns, create favorable conditions for sales intelligence adoption as these cohorts advance into business decision-making roles.

Middle East and Africa Sales Intelligence Market Analysis

The Middle East and Africa region demonstrates nascent but accelerating adoption driven by economic diversification initiatives, technology infrastructure investments, and growing recognition of digital transformation imperatives. Gulf Cooperation Council countries including United Arab Emirates, Saudi Arabia, and Qatar lead regional development, supported by substantial government spending on technology initiatives, smart city projects, and economic diversification programs reducing dependence on natural resource revenues. These countries demonstrate willingness to invest in advanced technologies as they develop knowledge-based economies and attract international business operations. Additionally, South Africa represents a mature market within the African continent, characterized by established financial services, telecommunications, and retail sectors demonstrating progressive technology adoption patterns. The region faces unique challenges including infrastructure limitations in certain areas, regulatory complexity, and economic disparities between countries that influence market development trajectories. Nevertheless, mobile technology proliferation, young demographic profiles, and entrepreneurial energy create opportunities for leapfrog adoption patterns where organizations bypass legacy systems and implement contemporary cloud-based platforms directly.

Competitive Landscape:

The competitive environment exhibits substantial dynamism characterized by continuous innovation, strategic partnerships, and evolving customer requirements that reshape market positioning and vendor strategies. Organizations differentiate through proprietary data assets, artificial intelligence capabilities, integration ecosystem breadth, and vertical-specific features addressing industry requirements. The market accommodates both established enterprise software vendors leveraging existing customer relationships and specialized pure-play providers focusing exclusively on sales intelligence capabilities. Strategic acquisitions consolidate market share as larger platforms acquire specialized vendors to enhance feature portfolios and accelerate development roadmaps. Furthermore, partnerships between intelligence providers and customer relationship management platforms create integrated solutions delivering enhanced value propositions. The sales intelligence market forecast indicates continued vendor consolidation alongside emergence of innovative entrants introducing disruptive capabilities. Organizations evaluate vendors based on data quality, platform usability, integration capabilities, pricing models, and customer success resources. The competitive intensity drives continuous enhancement, ensuring customers benefit from expanding capabilities and improving economics.

The report provides a comprehensive analysis of the competitive landscape in the sales intelligence market with detailed profiles of all major companies, including:

- Clearbit

- Data Axle

- Demandbase Inc.

- Dun & Bradstreet Corporation

- LinkedIn Corporation (Microsoft Corporation)

- ZoomInfo Technologies Inc.

Latest News and Developments:

- In October 2025: S&P Global launched S&P Capital IQ Pro Document Intelligence on Salesforce’s AgentExchange. The tool integrates earnings call transcripts, regulatory filings, and other document data with generative AI, enabling sales teams to extract insights, sentiment, and actionable next steps directly within the CRM.

- In January 2025: Oracle Corporation launched AI agents to assist sales professionals with tasks such as updating records and generating multilingual customer‑intelligence reports, enhancing workflow efficiency and enabling more actionable sales insights.

Sales Intelligence Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software, Services |

| Deployment Modes Covered | On-Premises, Cloud Based |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium-Sized Enterprises |

| Applications Covered | Lead Management, Data Management, Analytics and Reporting, Others |

| Industry Verticals Covered | BFSI, IT and Telecom, Retail and E-Commerce, Healthcare, Media and Entertainment, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Clearbit, Data Axle, Demandbase Inc., Dun & Bradstreet Corporation, LinkedIn Corporation (Microsoft Corporation), ZoomInfo Technologies Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the sales intelligence market from 2020-2034.

- The research reports provide the latest information on the market drivers, challenges, and opportunities in the global sales intelligence market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the sales intelligence industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Sales Intelligence Market Report

The sales intelligence market was valued at USD 4.06 Billion in 2025.

The sales intelligence market is projected to exhibit a CAGR of 9.95% during 2026-2034, reaching a value of USD 9.53 Billion by 2034.

Primary drivers include accelerating digital transformation initiatives across industries, increasing competitive intensity requiring data-driven sales approaches, and widespread adoption of artificial intelligence technologies. Organizations recognize the imperative of leveraging comprehensive prospect intelligence to optimize conversion rates and reduce customer acquisition costs. Additionally, the proliferation of cloud computing infrastructure democratizes access to enterprise-grade capabilities previously restricted to large corporations. The convergence of big data analytics, machine learning, and predictive modeling enables unprecedented sales effectiveness improvements.

North America currently dominates the sales intelligence market, accounting for a share of 35%. The region benefits from technology-forward business environments, substantial investment in sales enablement initiatives, and mature digital infrastructure supporting advanced platform deployment. United States organizations particularly demonstrate sophisticated understanding of sales intelligence value propositions, supported by extensive case studies demonstrating measurable returns. The concentration of technology vendors, implementation partners, and innovation ecosystems within North America reinforces market leadership and drives continuous platform enhancement benefiting global customers.

Some of the major players in the sales intelligence market include Clearbit, Data Axle, Demandbase Inc., Dun & Bradstreet Corporation, LinkedIn Corporation (Microsoft Corporation), ZoomInfo Technologies Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)