Satellite Communication (SATCOM) Market Size, Share, Trends and Forecast by Component, Application, End Use Industry, and Region, 2026-2034

Global Satellite Communication (SATCOM) Market Size, Share, Trends & Forecast (2026-2034)

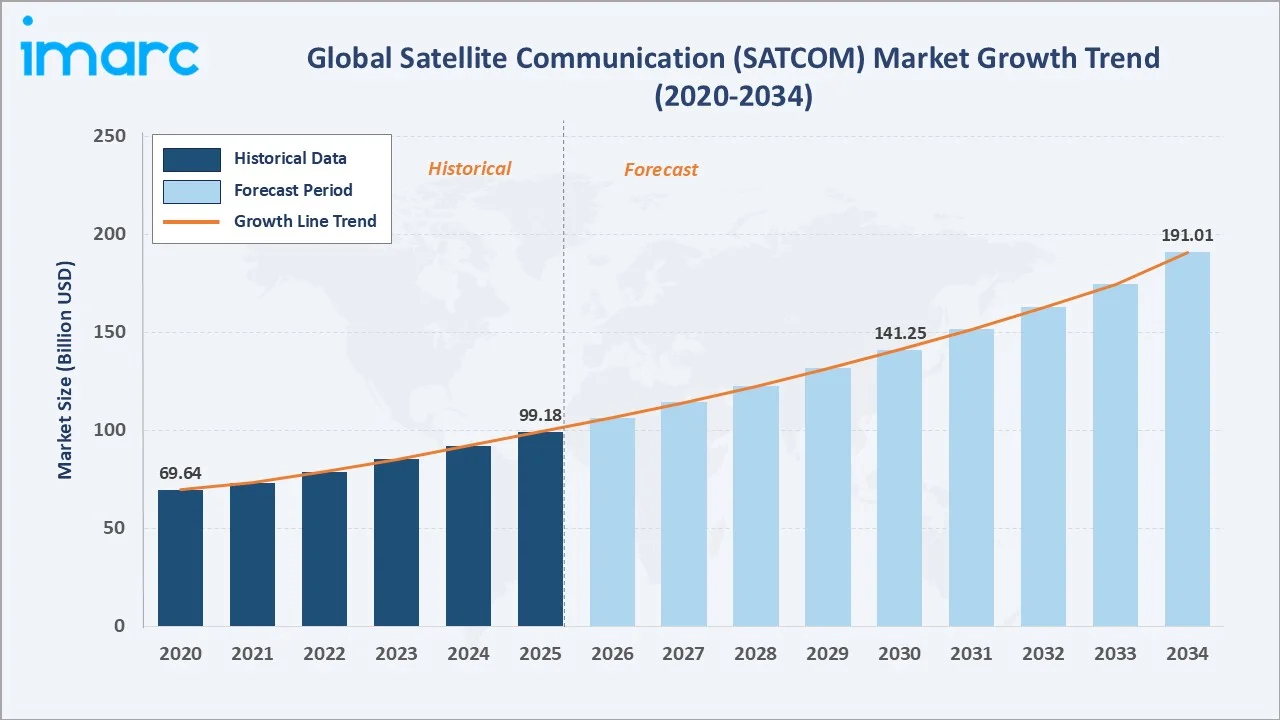

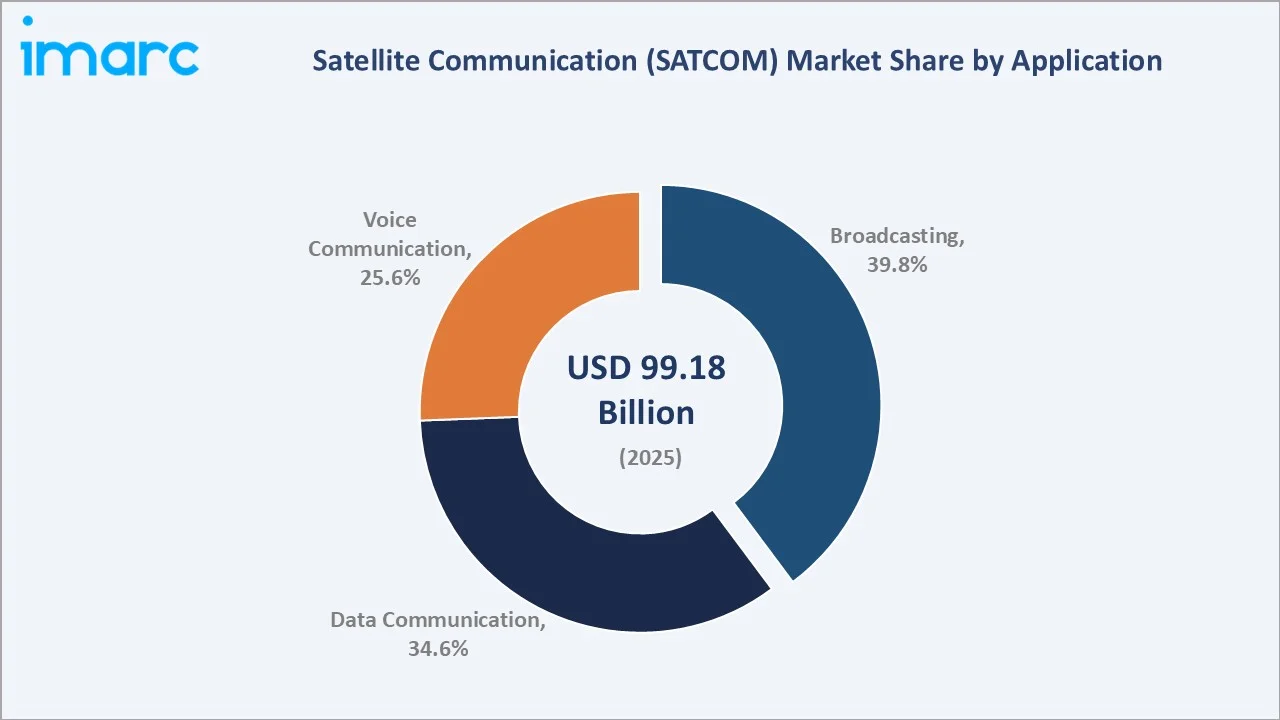

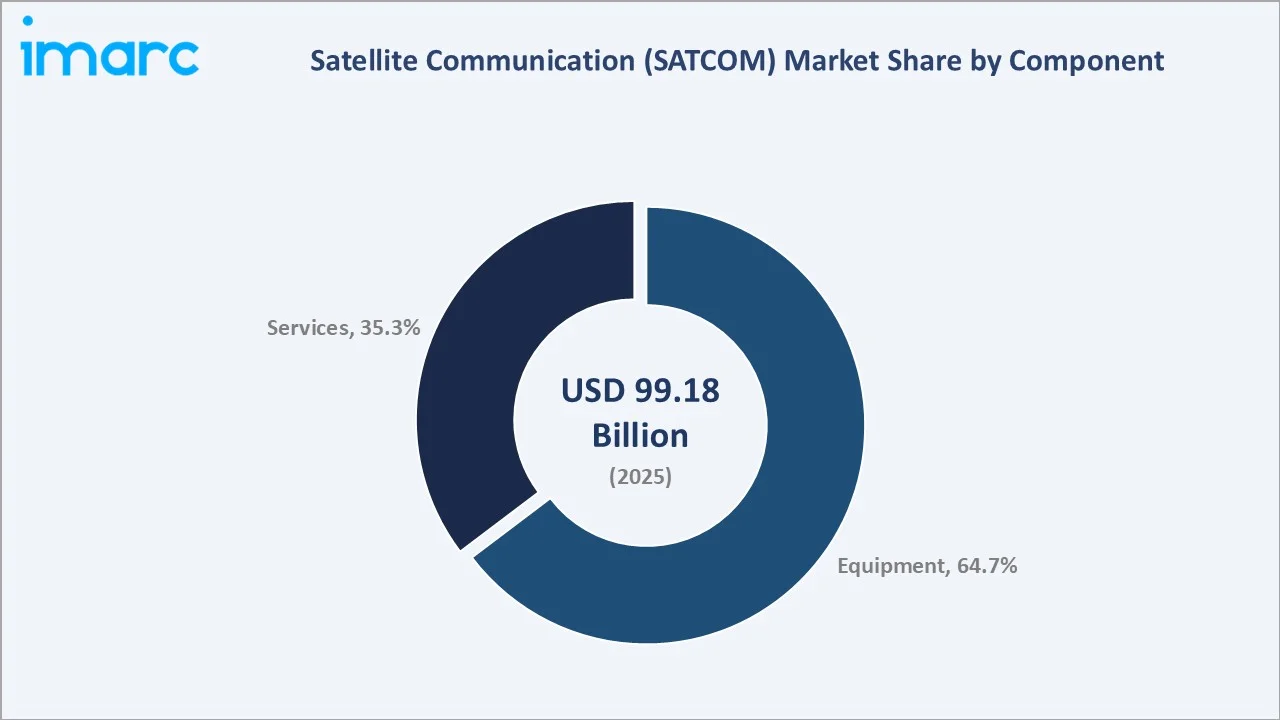

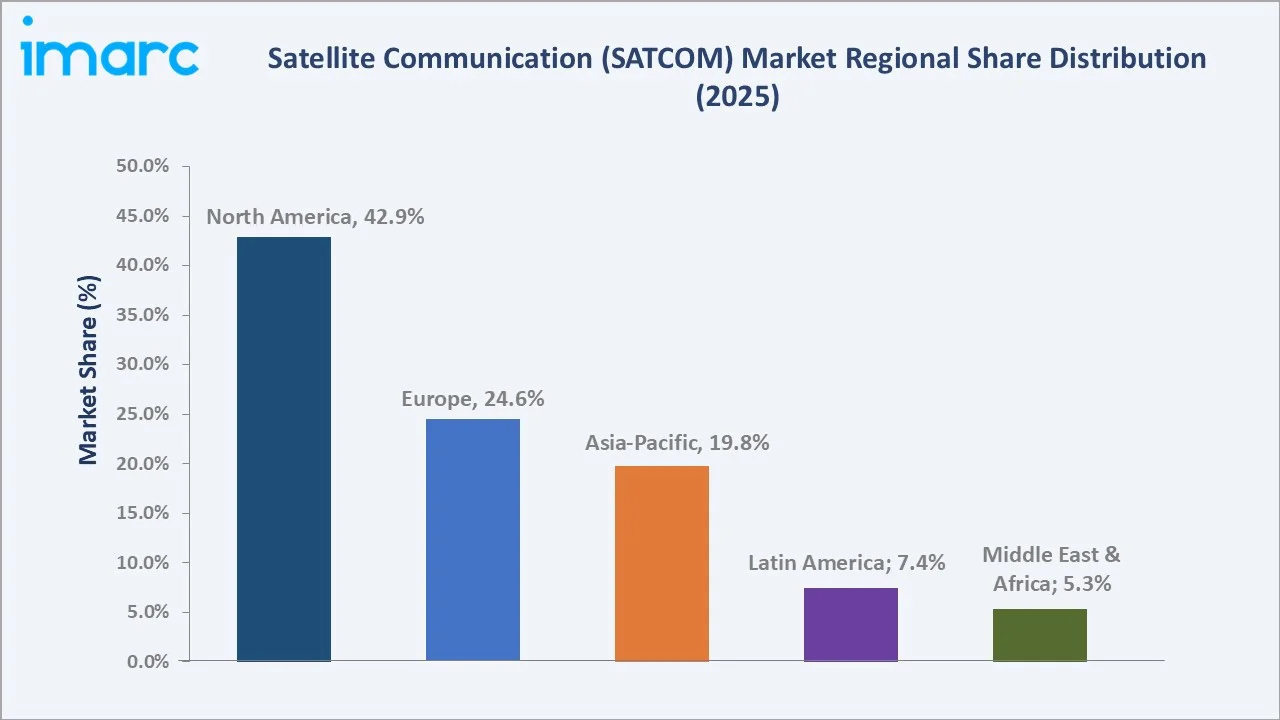

The global satellite communication (SATCOM) market size was valued at USD 99.18 Billion in 2025 and is projected to reach USD 191.01 Billion by 2034, exhibiting a CAGR of 7.33% during 2026-2034. Rapid deployment of low-earth-orbit (LEO) constellations, accelerating in-flight and maritime broadband adoption, defense modernization budgets, and IoT-driven connectivity needs are fueling SATCOM market growth. Broadcasting leads applications with a 39.8% share in 2025, while Equipment captures 64.7% of revenue by component. North America commands a 42.9% share, anchored by Starlink scale, dense defense procurement, and high-throughput satellite (HTS) capacity additions.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 99.18 Billion |

|

Forecast Market Size (2034) |

USD 191.01 Billion |

|

CAGR (2026-2034) |

7.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (42.9% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Application |

Broadcasting (39.8%, 2025) |

|

Leading Component |

Equipment (64.7%, 2025) |

The chart below presents SATCOM market growth from 2020-2034, separating historical recovery from the accelerating forecast curve, with the 7.33% CAGR called out for the forecast period.

To get more information on this market, Request Sample

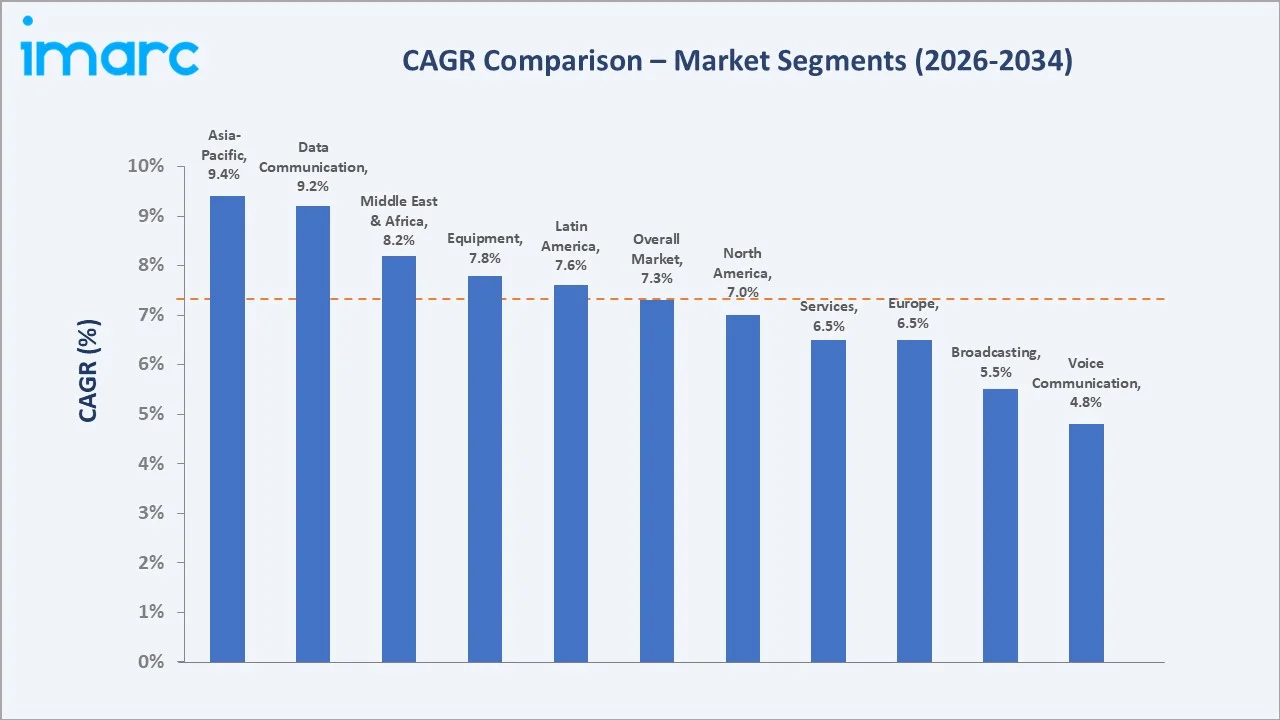

CAGR analysis benchmarks segment- and region-level growth against the 7.33% overall trajectory. Data Communication leads applications, while Asia-Pacific outpaces all regions through 2034.

Executive Summary

The global satellite communication (SATCOM) market is undergoing a structural shift driven by mega-constellations, software-defined payloads, and falling launch economics. Valued at USD 99.18 Billion in 2025, the market is forecast to reach USD 191.01 Billion by 2034, expanding at a 7.33% CAGR. Connectivity needs across aviation, shipping, defense, and rural broadband are pulling commercial demand higher every year.

Equipment dominates the market with 64.7% share in 2025, reflecting heavy spending on user terminals, ground gateways, antennas, and modems tied to constellation rollouts. Services account for 35.3%, anchored by managed bandwidth, broadcasting feeds, mobility services, and government leases. Broadcasting leads applications at 39.8%, followed by data communication at 34.6% and voice communication at 25.6%.

North America accounts for 42.9% of the market in 2025, supported by SpaceX, Viasat, EchoStar, and a deep U.S. Department of Defense customer base. Europe holds 24.6% via SES, Eutelsat-OneWeb, and Inmarsat heritage. Asia-Pacific (19.8%) is the fastest-growing region, fueled by India, China, Japan, and Southeast Asian sovereign satellite programs and rising consumer broadband demand.

Key Market Insights

|

Insight |

Data |

|

Largest Application Segment |

Broadcasting – 39.8% share (2025) |

|

Second Application Segment |

Data Communication – 34.6% share (2025) |

|

Leading Component |

Equipment – 64.7% share (2025) |

|

Leading Region |

North America – 42.9% (2025) |

|

Fastest-Growing Region |

Asia-Pacific – 19.8% share, highest forecast CAGR |

|

Top Companies |

SpaceX, Viasat Inc., SES S.A., EchoStar Corporation, and Eutelsat Communications SA |

Key Analytical Observations Supporting the Table Above:

- Broadcasting's 39.8% lead in 2025 reflects entrenched DTH platforms, satellite radio, and contribution feeds, even as IP-based delivery expands; geostationary capacity for broadcast remains capacity-anchored revenue.

- Data communication at 34.6% is the fastest-rising application, propelled by LEO broadband, in-flight Wi-Fi, maritime VSAT, and machine-to-machine IoT links across logistics and energy assets globally.

- Equipment's 64.7% share in 2025 is tied to mass-scale user terminal shipments tied to Starlink, OneWeb, and military SATCOM-on-the-move modernization, where each subscriber adds hardware revenue.

- North America's 42.9% dominance is driven by major U.S. operators like SpaceX, Viasat, and EchoStar, alongside multi-billion-dollar annual U.S. defense SATCOM spending via Defense Information Systems Agency and United States Space Force.

- Asia-Pacific at 19.8% is the fastest-growing region, driven by India's BharatNet, Indonesia's SATRIA-1, Japan's IGS program, and active LEO partnerships across South Korea and Australia.

- SpaceX-Starlink crossed 10 million subscribers in 2025, while Viasat-Inmarsat merger and SES S.A. completed Intelsat acquisition in July 2025 are reshaping operator concentration at the top tier.

Global Satellite Communication Market Overview

Satellite communication delivers voice, video, and data through orbiting spacecraft (GEO, MEO, LEO) connected to ground stations and end-user terminals. The ecosystem covers satellite manufacturers, launch providers, network operators, ground infrastructure vendors, integrators, equipment OEMs, and service distributors.

Applications span broadcasting, defense and government, in-flight and maritime broadband, enterprise VSAT, IoT, and consumer rural connectivity. Macro drivers include falling launch costs (SpaceX Falcon 9 at roughly USD 2,700 per kg LEO), expanding spectrum allocation, and rising digital infrastructure investment across emerging economies through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

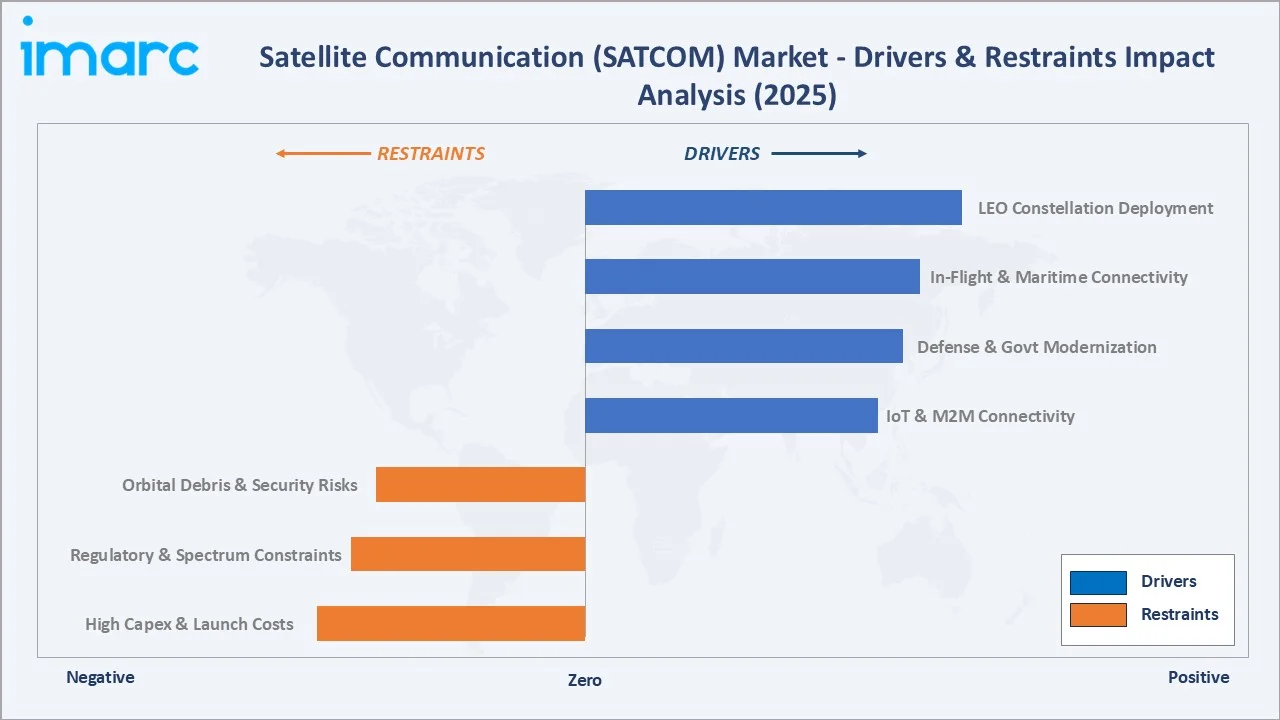

Market Drivers

- LEO Constellation Deployment: Mega-constellations from Swarm Technologies (SpaceX), Eutelsat–OneWeb, Amazon, and China’s Guowang are scaling large LEO fleets, significantly expanding global broadband coverage and supporting sustained SATCOM market growth.

- In-Flight & Maritime Broadband Demand: Commercial aviation is rapidly equipping aircraft with Ka-band and LEO connectivity, while merchant shipping VSAT installations are climbing as cruise lines, ferries, and offshore vessels demand always-on broadband.

- Defense and Government Modernization: U.S. Space Force, NATO members, and Asian defense ministries are accelerating SATCOM-on-the-move, protected tactical waveform, and proliferated LEO architectures, lifting government SATCOM spending each fiscal year.

- IoT and M2M Connectivity Expansion: Satellite IoT operators including Iridium, Globalstar, Astrocast, and Swarm (SpaceX) are scaling sensor connectivity for logistics, agriculture, energy, and asset tracking across regions without terrestrial coverage.

Market Restraints

- High Capex and Launch Costs: Building and launching a constellation often runs into the multi-billion-dollar range, and despite SpaceX's reusability, capex intensity continues to limit new entrants and concentrate market power among well-funded operators.

- Spectrum and Regulatory Constraints: ITU coordination, national licensing delays, and Ku/Ka-band interference rules slow market entry. Operators face years of approval cycles before commercial service launches in many jurisdictions globally.

- Orbital Debris and Space Sustainability Risks: Roughly 14,000-plus tracked debris objects in low-earth orbit raise collision risks, insurance premiums, and end-of-life de-orbit obligations, creating financial overhead for constellation operators.

Market Opportunities

- Direct-to-Device (D2D) Satellite Services: Companies such as Apple Inc.–Globalstar, AST SpaceMobile, T-Mobile–SpaceX Starlink, and Lynk Global are advancing direct-to-smartphone satellite connectivity, enabling messaging and broadband services without terrestrial networks, positioning D2D as a high-growth consumer SATCOM segment.

- 5G–Satellite Network Integration: 3GPP Release 17/18 non-terrestrial network (NTN) standards are enabling hybrid satellite-cellular roaming, creating a clear pathway for telcos to offer ubiquitous coverage with SATCOM partners.

- Earth Observation & Communication Convergence: Combined EO-comms platforms support real-time downlink for defense ISR, climate monitoring, and disaster response, opening dual-use mission service revenue across government clients.

Market Challenges

- Cybersecurity Threats: The 2022 Viasat KA-SAT breach during the Ukraine conflict highlighted SATCOM's vulnerability to nation-state attacks, pushing operators to invest heavily in encryption, ground-network hardening, and zero-trust architectures.

- Geopolitical Fragmentation: U.S.-China-Russia rivalry is splitting SATCOM into competing technology blocs, with export controls (ITAR, EAR) restricting cross-border supply chains and operator partnerships across rival jurisdictions.

- Skilled Talent Shortage: The global SATCOM and space sector faces a shortage of RF engineers and satellite specialists, with significant workforce gaps across aerospace industries and tens of thousands of unfilled roles in the U.S., driven by rising demand for advanced satellite and communication expertise.

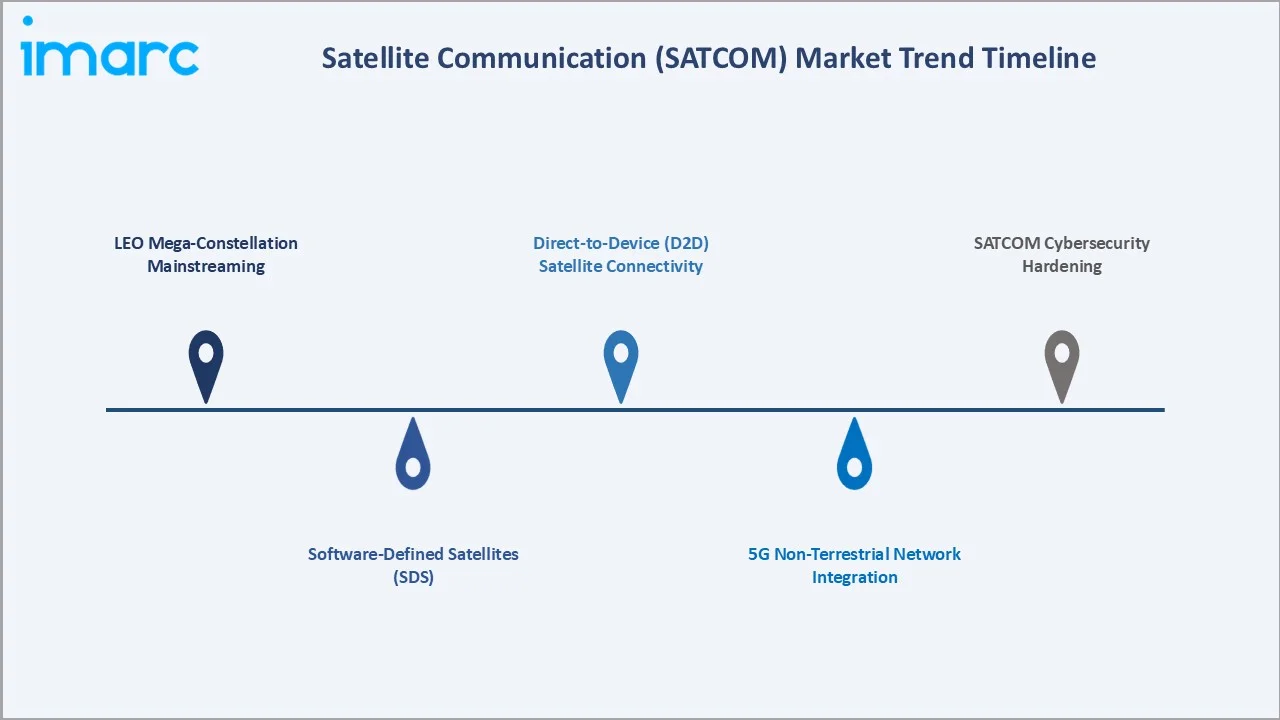

Emerging Market Trends

1. LEO Mega-Constellation Mainstreaming

Low Earth Orbit (LEO) constellations are becoming central to commercial SATCOM due to lower latency. SpaceX’s Starlink surpassed 8 million users globally, while projects like Amazon Kuiper and China’s Guowang continue expanding LEO deployments.

2. Software-Defined Satellites (SDS)

Operators are deploying reconfigurable satellites with flexible payloads. Platforms such as Eutelsat Quantum, SES S.A. O3b mPOWER, and Airbus OneSat enable dynamic beam shaping and capacity allocation, improving operational efficiency and utilization compared to traditional fixed satellites.

3. Direct-to-Device (D2D) Satellite Connectivity

Satellite-to-smartphone connectivity is expanding, enabling messaging without terrestrial networks. AST SpaceMobile launched BlueBird satellites, T-Mobile-Starlink beta tested text-from-space service in late 2024, and Apple-Globalstar continues expanding emergency SOS coverage.

4. 5G Non-Terrestrial Network Integration

Hybrid satellite-cellular networks are becoming a commercial reality. 3GPP Release 17 (2022) and Release 18 (2024) standardized NTN integration, with telcos including KDDI, Optus, Airtel, and Verizon piloting satellite roaming with LEO operators.

5. SATCOM Cybersecurity Hardening

After the Viasat KA-SAT incident, defense SATCOM customers are mandating quantum-resistant encryption, ground-station segmentation, and multi-orbit resilience. Governments and defense agencies are prioritizing secure satellite communications, driving increased investment in cybersecurity solutions across satellite networks.

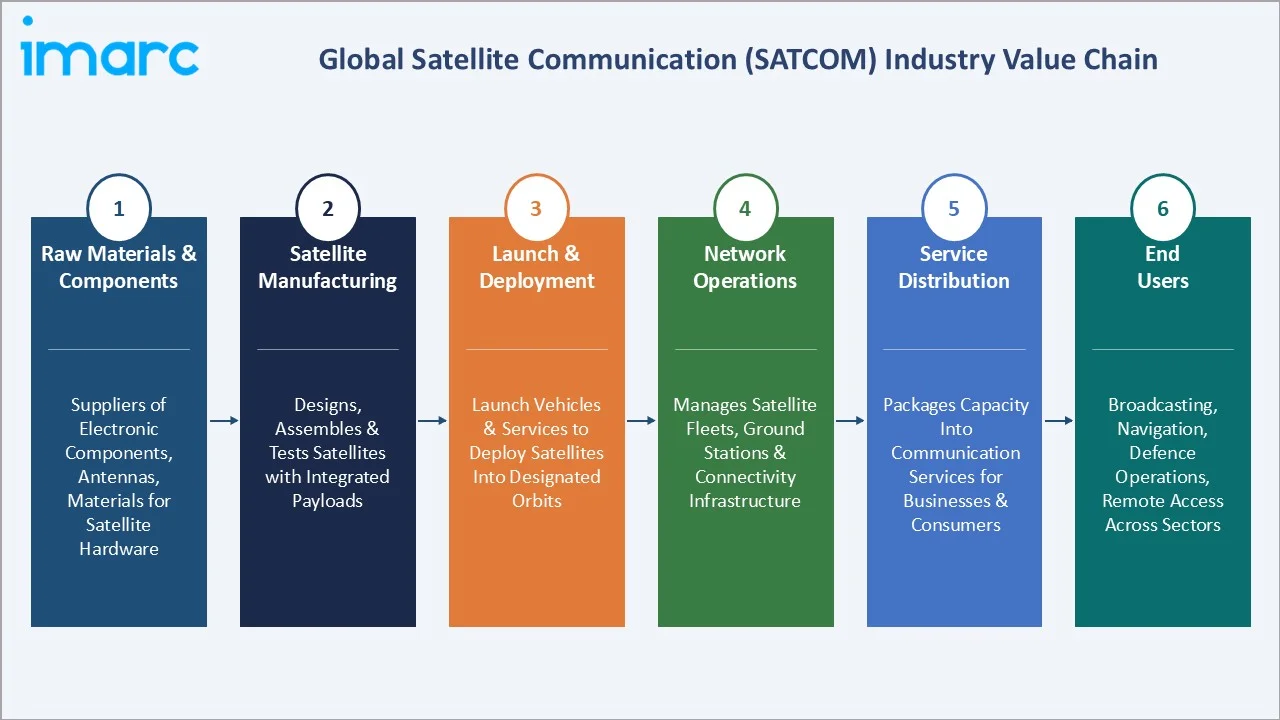

Industry Value Chain Analysis

The SATCOM value chain spans six interconnected stages, each capturing distinct margin pools - from precision RF components through end-user broadband subscriptions.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Supplies essential electronic components, antennas, and materials required for building reliable satellite communication hardware systems |

|

Satellite Manufacturing |

Designs, assembles, and tests satellites with integrated payloads, ensuring performance, durability, and mission readiness standards |

|

Launch & Deployment |

Provides launch vehicles and services to deploy satellites into designated orbits safely and efficiently worldwide |

|

Network Operations |

Manages satellite fleets, ground stations, and connectivity infrastructure to deliver continuous, reliable communication services globally |

|

Service Distribution |

Packages satellite capacity into communication services, distributing connectivity solutions to businesses, governments, and consumers worldwide |

|

End Users |

Utilize satellite services for broadcasting, navigation, connectivity, defence operations, and remote access across diverse sectors |

Tier-1 operators capture the highest value by integrating space, ground, and service layers. Vertical integration trends - led by SpaceX manufacturing rockets, satellites, and terminals in-house - are reshaping margin distribution across the chain through 2034.

Technology Landscape in the SATCOM Industry

Multi-Orbit and High-Throughput Satellite (HTS) Architectures

Satellite operators are deploying multi-orbit networks across GEO, MEO, and LEO to optimize coverage, latency, and capacity. Systems such as SES S.A. O3b mPOWER and Viasat ViaSat-3 deliver high-throughput capacity supporting flexible, scalable broadband services.

Phased-Array and Electronically Steered Antennas (ESAs)

Electronically steered antennas are replacing traditional dishes with flat, low-profile terminals for aviation and maritime use, enabling seamless LEO satellite tracking, improving connectivity on moving platforms, and accelerating adoption of satellite broadband services.

Optical Inter-Satellite Links (OISL)

Laser links between satellites bypass ground gateways and reduce latency. Starlink (V2 satellites), Kuiper, and Telesat Lightspeed all use OISL, enabling global low-latency mesh networks for defense, financial trading, and enterprise applications.

Software-Defined Networking (SDN) and AI-Driven Capacity Management

SATCOM operators are integrating software-defined networking and AI-based analytics to dynamically manage bandwidth and traffic. These technologies improve network efficiency, enable flexible capacity allocation, and support real-time optimization of satellite resources across diverse applications..

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Equipment |

🔒 |

2025 |

|

Application |

Broadcasting |

39.8% |

2025 |

|

End Use Industry |

Government and Military |

40.2% |

2025 |

|

Region |

North America |

42.9% |

2025 |

By Application

Broadcasting holds a 39.8% share in 2025, anchored by direct-to-home (DTH) television, satellite radio (Sirius XM), and live event contribution feeds. Although IP-based streaming is eroding consumer DTH subscribers in mature markets, broadcasting remains the largest revenue pool through committed multi-year capacity contracts.

To access detailed market analysis, Request Sample

Data Communication accounts for 34.6% in 2025 and is the fastest-growing application. LEO broadband, in-flight Wi-Fi, maritime VSAT, IoT, and enterprise networks are driving this segment, supported by falling per-megabit pricing and expanding terminal availability. Voice Communication holds 25.6% in 2025, sustained by Iridium and Inmarsat L-band services serving aviation, maritime safety (GMDSS), defense, and remote workforce voice connectivity. While narrowband by nature, the segment retains durable government and safety-critical demand globally.

By Component

Equipment dominates with a 64.7% share in 2025, driven by user terminals, antennas, transponders, modems, gateway equipment, and amplifiers. Starlink's terminal shipments alone exceeded 6 million units cumulatively by 2025, while military SATCOM-on-the-move terminal procurement continues expanding.

Services account for 35.3% in 2025, including managed bandwidth, broadcasting capacity leases, mobility connectivity (aviation/maritime), broadband subscriptions, and government managed services. Recurring service revenue is structurally attractive, with operator average ARPU rising as LEO consumer broadband scales globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

42.9% |

Starlink scale, Viasat-Inmarsat capacity, U.S. Space Force budgets, dense HTS deployment |

|

Europe |

24.6% |

SES, Eutelsat-OneWeb, Airbus & Thales manufacturing, EU IRIS² constellation program |

|

Asia-Pacific |

19.8% |

India BharatNet, China Guowang, Japan IGS, Indonesia SATRIA, Australia LEO partnerships |

|

Latin America |

7.4% |

Brazil rural broadband, Mexico LEO rollout, Argentina ARSAT, broadcasting capacity demand |

|

Middle East & Africa |

5.3% |

GCC defense SATCOM, Yahsat & Arabsat fleets, sub-Saharan rural broadband expansion |

North America commands a 42.9% global in 2025, supported by SpaceX's Starlink (over 10 million subscribers in 2026), Viasat-Inmarsat's mobility footprint, EchoStar/Hughes consumer broadband, and roughly U.S. Space Force awarded five companies spots on the PTS-G contract, valued at about $4 billion.

Europe holds 24.6% in 2025, anchored by SES (Luxembourg), Eutelsat-OneWeb (France-UK), and the EU's IRIS² sovereign multi-orbit constellation, awarded in late 2024 for roughly EUR 10.6 billion. Asia-Pacific at 19.8% is the fastest-growing region, with India's IN-SPACe reforms, China's Guowang and SatNet constellations, Japan's regional satellites, and active LEO partnerships across Australia, South Korea, and Southeast Asia driving strong forecast growth through 2034.

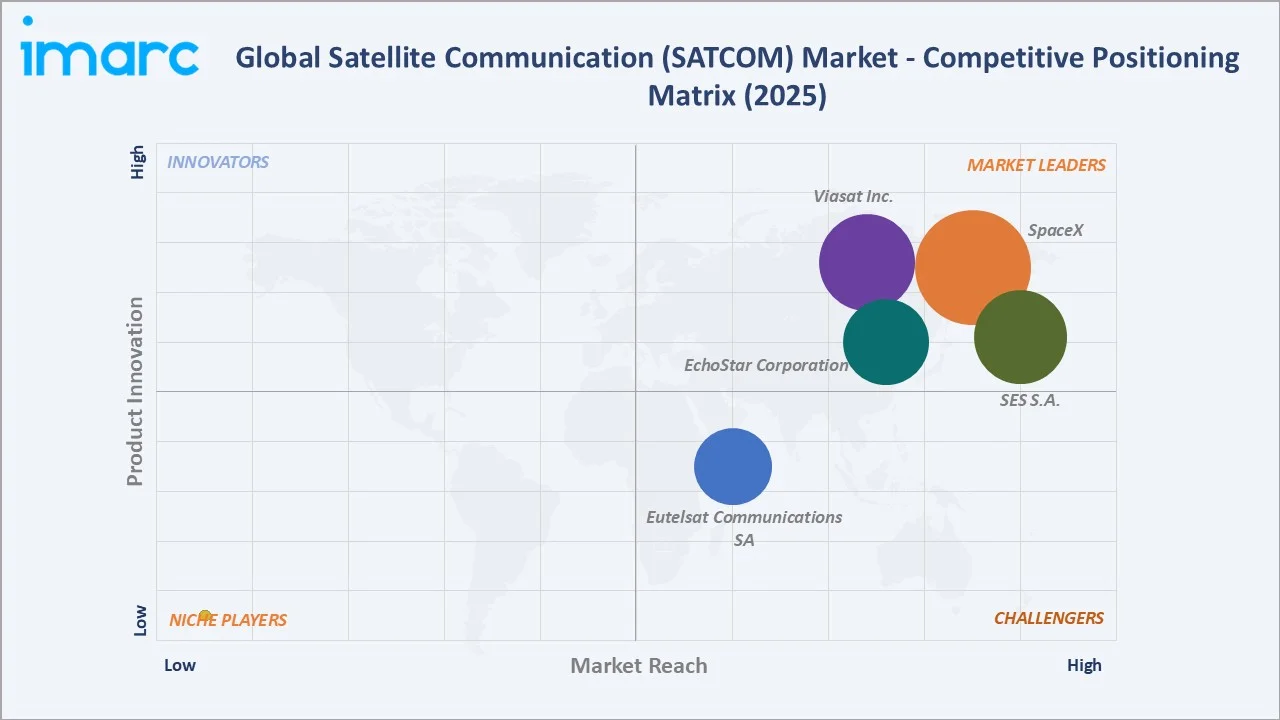

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

SpaceX |

Starlink |

Leader |

LEO scale, vertical integration, lowest launch costs |

|

Viasat Inc. |

ViaSat-3 |

Leader |

GEO-HTS capacity, mobility, government services |

|

SES S.A. |

O3b mPOWER |

Leader |

Multi-orbit GEO+MEO, video, government |

|

EchoStar Corporation |

Hughes JUPITER 3 |

Leader |

Consumer broadband, enterprise VSAT, 5G NTN |

|

Eutelsat Communications SA |

OneWeb LEO |

Challenger |

GEO+LEO multi-orbit, European sovereignty |

The SATCOM market is led by integrated global operators alongside specialized regional and niche players. SpaceX's Starlink generated USD 11 billion in revenue in 2024, while SES reported €2,001 million and Viasat reported USD 4.5 billion in FY2024.

Key Company Profiles

SpaceX (Starlink)

SpaceX, based in Hawthorne, operates the Starlink low-Earth-orbit (LEO) satellite network, the world’s largest broadband constellation. By 2025, it had several thousand active satellites and millions of subscribers globally, generating multi-billion-dollar revenue and positioning itself as the leading commercial SATCOM provider by capacity and user base.

- Product & Service Portfolio: Starlink provides satellite broadband services across residential, enterprise, maritime, aviation, mobility, and government/defense segments, including Direct-to-Cell connectivity and Starshield secure communications.

- Recent Developments: In May 2025, SpaceX launched its largest batch of 29 Starlink V2 Mini Optimized satellites aboard a Falcon 9 rocket from Kennedy Space Center, enhancing network capacity and efficiency. The mission also successfully landed the reusable booster, reinforcing SpaceX’s rapid deployment strategy for global broadband expansion.

- Strategic Focus: SpaceX focuses on scaling Starlink’s global broadband dominance through vertical integration, expanding defense-oriented Starshield capabilities, and advancing Direct-to-Device satellite connectivity for mass-market mobile users.

Viasat, Inc.

Viasat, headquartered in Carlsbad, California, became a leading global SATCOM provider after acquiring Inmarsat in 2023 for USD 7.3 billion. The combined entity delivers broadband and mobility services across aviation, maritime, government, and defense sectors, supported by multi-band satellite assets and multi-orbit capabilities.

- Product & Service Portfolio: Viasat offers satellite broadband and mobility solutions through Viasat-3 GEO satellites, Global Xpress (Ka-band), ELERA (L-band), in-flight connectivity, maritime Fleet Xpress, and secure government communication services.

- Recent Developments: In April 2026, Viasat successfully launched ViaSat-3 F3 aboard a SpaceX Falcon Heavy, achieving initial signal acquisition. The high-capacity satellite, designed for ~1 Tbps throughput, will expand Asia-Pacific connectivity and complete Viasat’s global ViaSat-3 constellation, strengthening its multi-orbit network and mobility-focused SATCOM capabilities.

- Strategic Focus: Viasat focuses on strengthening global mobility and defense communications through integrated multi-band satellite networks, Viasat-3 constellation deployment, and strategic partnerships across commercial and government SATCOM markets.

SES S.A.

SES, headquartered in Betzdorf, Luxembourg, is a leading multi-orbit satellite operator combining GEO and MEO systems. Following its announced acquisition of Intelsat, SES is expanding global coverage across video, government, and mobility markets, serving hundreds of millions of households and strengthening capacity-driven connectivity services worldwide.

- Product & Service Portfolio: SES delivers satellite-enabled video broadcasting (ASTRA), O3b mPOWER MEO broadband, government and defense connectivity, aviation (SES Open Orbits/Signature), and global mobility and network services.

- Recent Developments: In June 2025, SES activated its seventh and eighth O3b mPOWER satellites, launched in December 2024, to deliver global high-throughput, low-latency connectivity. Featuring upgraded payload power modules, the satellites enhance network capacity and efficiency, supporting mobility, government, enterprise, and cloud customers while advancing SES’s scalable MEO broadband strategy.

- Strategic Focus: SES focuses on integrating GEO-MEO multi-orbit capabilities, expanding government and mobility services, leveraging IRIS² participation for European sovereignty, and capturing synergies from the Intelsat combination to scale global connectivity.

Market Concentration Analysis

The global SATCOM market is moderately concentrated at the top tier. SpaceX, Viasat Inc., SES S.A., EchoStar Corporation collectively account for roughly 55-60% of global revenue in 2025, with SpaceX alone capturing an estimated 12-14% share through Starlink's rapid subscriber expansion across consumer and enterprise markets.

Below the top tier, the market becomes more fragmented across regional operators (Yahsat, Arabsat, ARSAT, Telesat), niche IoT specialists (Iridium, Globalstar), and equipment vendors (Hughes, Gilat, Cobham SATCOM, KVH Industries). LEO new entrants such as Amazon Kuiper, China Guowang, and AST SpaceMobile are reshaping the competitive landscape through 2030.

Consolidation is accelerating. Viasat acquired Inmarsat in 2023 (USD 7.3 billion), SES closed Intelsat in 2025 (USD 3.1 billion), and Eutelsat merged with OneWeb in 2023, all creating multi-orbit competitors capable of challenging SpaceX. Further consolidation is widely expected as capex pressure and LEO competition intensify through 2030.

Investment & Growth Opportunities

Fastest-Growing Segments

LEO broadband and Direct-to-Device (D2D) services are among the fastest-growing SATCOM segments, driven by demand for low-latency connectivity and smartphone integration. While exact forecasts vary, industry reports highlight strong double-digit growth for LEO constellations and increasing telecom-satellite partnerships enabling early-stage D2D expansion.

Emerging Market Expansion

Asia-Pacific and Middle East & Africa are key SATCOM growth regions due to digital inclusion and sovereign space investments. India’s IN-SPACe is promoting private participation, while Saudi Arabia’s Vision 2030 supports satellite infrastructure and connectivity initiatives across smart cities and national communications programs.

Venture and Strategic Investment Trends

Global space investments remain strong, with billions deployed annually into LEO constellations, satellite connectivity, and related technologies. Strategic backing from companies like Amazon (Project Kuiper) and Apple (satellite connectivity via Globalstar) reflects sustained long-term capital interest.

Future Market Outlook (2026-2034)

The global SATCOM market forecast projects expansion from USD 99.18 Billion in 2025 to USD 191.01 Billion by 2034 at a 7.33% CAGR, representing roughly USD 92 Billion of incremental value created over the forecast period. Growth will be led by LEO broadband, mobility connectivity, defense modernization, and Direct-to-Device service mass adoption.

Three transformational shifts will reshape SATCOM through 2034. First, multi-orbit operator integration will replace single-fleet competition. Second, satellite-cellular convergence under 5G NTN standards will blur the line between mobile and SATCOM operators. Third, sovereign constellation programs (EU IRIS², China Guowang, India sovereign LEO) will fragment the global market into multiple capability blocs.

By 2034, SATCOM is expected to be a software-defined, multi-orbit, AI-orchestrated service layer integrated with terrestrial 5G/6G networks. Operators investing in vertical integration, Direct-to-Device capability, and defense services are best positioned to capture premium growth across consumer, enterprise, and government segments.

Research Methodology

Primary Research

Primary research included structured interviews and surveys conducted in 2024-2025 with SATCOM industry stakeholders, including senior executives at Tier-1 operators, defense procurement officers, satellite manufacturers, ground systems integrators, mobility connectivity buyers in aviation and maritime, and regulatory specialists at national spectrum authorities.

Secondary Research

Secondary sources include company annual reports (SpaceX, Viasat Inc., SES S.A., EchoStar Corporation, and Eutelsat Communications SA), regulatory filings with the FCC, ITU, and national authorities, government procurement disclosures (DISA, U.S. Space Force, ESA), trade association publications (SIA, GVF, ESOA), and industry trade media including SpaceNews, Via Satellite, and Advanced Television.

Forecasting Models

Market sizing and growth projections were derived using top-down and bottom-up forecasting models, incorporating fleet capacity additions, subscriber projections, defense budget trajectories, mobility traffic forecasts, and scenario analysis under base, optimistic, and conservative LEO deployment and macroeconomic assumptions through 2034.

Satellite Communication (SATCOM) Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Applications Covered | Voice Communication, Broadcasting, Data Communication |

| End Use Industries Covered | Aerospace and Defense, Transportation and Logistics, Agriculture, Government and Military, Media and Entertainment, Others |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | SpaceX, Viasat Inc., SES S.A., EchoStar Corporation, Eutelsat Communications SA, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the satellite communication (SATCOM) market from 2020-2034.

- The satellite communication (SATCOM) market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the satellite communication (SATCOM) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Satellite Communication (SATCOM) Market Report

The global SATCOM market was valued at USD 99.18 Billion in 2025, driven by LEO constellation deployment, defense modernization, mobility broadband demand, and rising IoT connectivity adoption.

The market is projected to reach USD 191.01 Billion by 2034, growing at a 7.33% CAGR, fueled by Direct-to-Device services, in-flight broadband, and 5G–satellite integration.

Broadcasting leads with a 39.8% share in 2025, supported by direct-to-home television, satellite radio, and live event contribution feeds across both mature and emerging markets.

Equipment commands a 64.7% share in 2025, driven by user terminals, antennas, gateway hardware, modems, and amplifiers tied to constellation rollouts and defense modernization.

North America leads with a 42.9% share in 2025, anchored by Starlink scale, Viasat-Inmarsat capacity, EchoStar/Hughes broadband, and dense U.S. defense SATCOM procurement.

Key drivers include LEO mega-constellations, in-flight and maritime broadband demand, defense modernization, IoT connectivity, and falling launch costs led by reusable rockets.

Asia-Pacific is the fastest-growing region, driven by India's IN-SPACe reforms, China's Guowang constellation, Japan's IGS program, and Southeast Asian sovereign satellite investments.

Leading companies include SpaceX, Viasat Inc., SES S.A., EchoStar Corporation, and Eutelsat Communications SA.

Data Communication holds a 34.6% share in 2025 and is the fastest-growing application, driven by LEO broadband, in-flight Wi-Fi, maritime VSAT, and global IoT connectivity.

LEO constellations deliver 20-40 ms latency and high throughput, enabling broadband, IoT, and direct-to-device services previously impossible with traditional GEO satellites.

Software-defined satellites, optical inter-satellite links, phased-array antennas, and AI-driven capacity management are improving fleet flexibility, throughput, and service economics through 2030.

D2D enables standard smartphones to connect directly with satellites for messaging, voice, and broadband, with services from Apple-Globalstar, T-Mobile-Starlink, and AST SpaceMobile scaling rapidly.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)