Saudi Arabia Centrifugal Pumps Market Size, Share, Trends and Forecast by Type, Stage, Flow Type, Capacity, End User, and Region, 2026-2034

Saudi Arabia Centrifugal Pumps Market Summary:

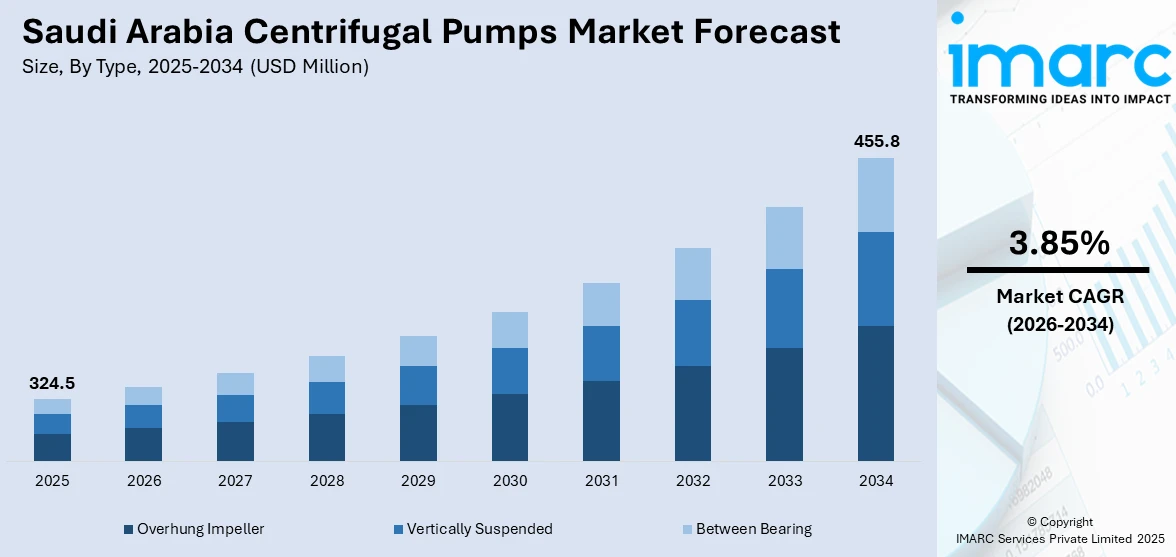

The Saudi Arabia centrifugal pumps market size was valued at USD 324.5 Million in 2025 and is projected to reach USD 455.8 Million by 2034, growing at a compound annual growth rate of 3.85% from 2026-2034.

The Saudi Arabia centrifugal pumps market is being driven by rising demand for water and wastewater management solutions, fueled by rapid urbanization and industrial expansion aligned with Vision 2030. Growth in the oil and gas sector, along with large-scale infrastructure and megaproject developments, is increasing the need for efficient pumping systems. Additionally, government support for desalination plants and water treatment facilities is further boosting market adoption, as these initiatives require reliable, high-performance pumps to ensure effective water management and operational efficiency across industrial and municipal applications.

Key Takeaways and Insights:

- By Type: Overhung impeller dominates the market with a share of 47% in 2025, driven by its widespread adoption in oil and gas applications, desalination facilities, and general industrial processes where reliability and ease of maintenance are prioritized.

- By Stage: Single stage pump leads the market with a share of 50% in 2025, owing to its cost-effectiveness, simple design, and suitability for low to medium pressure applications across water distribution and irrigation systems.

- By Flow Type: Radial flow pumps represent the largest segment with a market share of 62% in 2025, driven by their wide-ranging versatility in managing different types of fluids and their suitability for applications such as water treatment, chemical manufacturing, and petroleum refining.

- By Capacity: Medium capacity dominates the market with a share of 38% in 2025, reflecting balanced demand across municipal water supply systems, industrial processes, and commercial building applications requiring moderate flow rates.

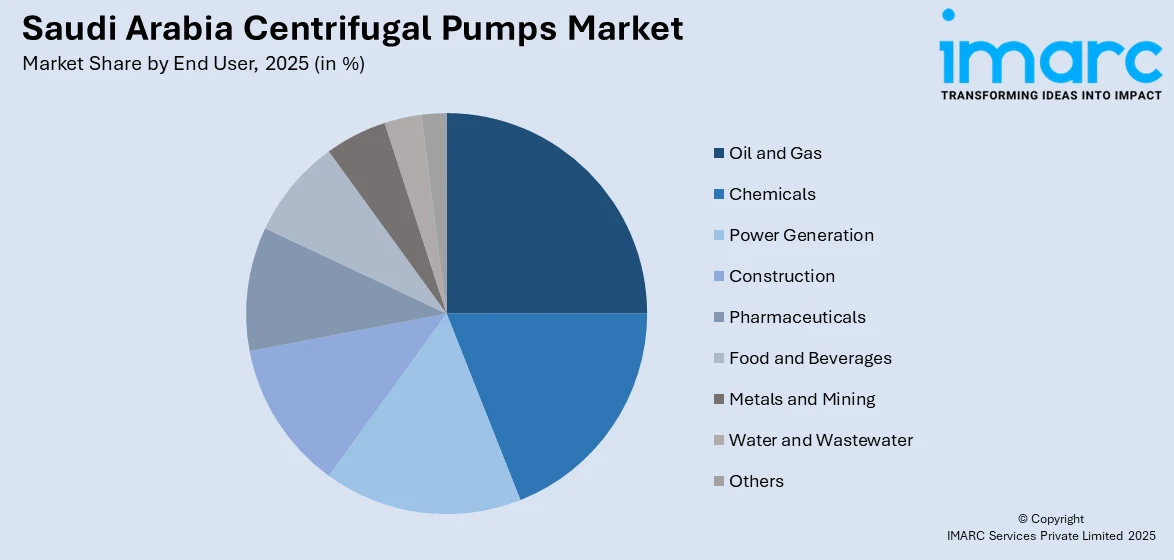

- By End User: Oil and gas lead the market with a share of 22% in 2025, supported by Saudi Arabia's position as a leading global oil producer and substantial investments in upstream and downstream petroleum operations.

- By Region: Northern and Central Region represents the largest segment with a market share of 29% in 2025, driven by expanding urban infrastructure, water distribution and wastewater projects, and industrial growth. Infrastructure modernization, housing and commercial developments, and the need for efficient fluid handling systems boost centrifugal pump adoption across municipal and industrial applications.

- Key Players: The Saudi Arabia centrifugal pumps market demonstrates moderate competitive intensity, with both multinational engineering firms and regional manufacturers actively competing. The landscape is characterized by a mix of established global companies and local producers, driving innovation, efficiency improvements, and a focus on meeting the growing demand for reliable pumping solutions across industrial and municipal applications.

To get more information on this market Request Sample

The Saudi Arabia centrifugal pumps market is experiencing robust growth driven by industrial expansion, infrastructure development, and water management initiatives aligned with Vision 2030. The Kingdom's strategic investments in desalination capacity, targeting over 20 million cubic meters per day by 2030, create substantial demand for high-efficiency pumping solutions. The oil and gas sector remains a cornerstone of market demand, with Saudi Aramco's extensive upstream and downstream operations requiring reliable fluid transfer systems. For instance, in January 2025, the National Water Company confirmed plans to spend SAR 607 Million on 20 water and sanitation schemes throughout the Jazan area, incorporating advanced water supply networks and wastewater treatment plants that require centrifugal pumps as critical components.

Saudi Arabia Centrifugal Pumps Market Trends:

Rising Investment in Desalination Infrastructure

Saudi Arabia is accelerating its desalination capacity expansion to address water scarcity challenges across the Kingdom. The country currently relies on desalination for over 70 percent of its drinking water supply, with plans to double capacity to approximately 17.8 million cubic meters per day by 2030. New large-scale plants are being developed across strategic areas such as the Eastern Province, Makkah, Jazan, and the Madinah region. This infrastructure expansion creates sustained demand for high-pressure centrifugal pumps essential for reverse osmosis and thermal desalination processes.

Adoption of Smart Pump Technologies and IoT Integration

The market is witnessing growing adoption of intelligent pumping systems equipped with real-time monitoring capabilities and predictive maintenance features. Industrial operators are integrating IoT-enabled sensors and cloud-based analytics platforms to optimize pump performance, reduce unplanned downtime, and enhance operational efficiency. Major manufacturers are deploying vibration monitoring and edge analytics solutions that can forecast bearing failures weeks in advance, significantly improving asset reliability across critical water, oil, and gas infrastructure applications.

Energy Efficiency Mandates Driving Equipment Upgrades

Stringent energy efficiency regulations and sustainability initiatives are reshaping pump procurement decisions across the Kingdom. The implementation of technical regulations for water consumption devices and industrial efficiency standards is pushing facility operators to retrofit existing installations with variable frequency drive pumps that can reduce energy consumption by up to 35 percent. This regulatory environment favors premium, high-efficiency centrifugal pump designs that deliver lower total cost of ownership despite higher initial investment.

How Vision 2030 is Transforming the Saudi Arabia Centrifugal Pumps Market

Vision 2030 is significantly transforming the Saudi Arabia centrifugal pumps market by driving large-scale infrastructure, industrial, and urban development projects that require advanced pumping solutions. Megaprojects such as NEOM, the Red Sea development, and Qiddiya are generating extensive demand for reliable pumps across construction, water management, and industrial applications. Simultaneously, initiatives to expand water and wastewater treatment facilities, along with the growth of the oil and gas sector, are increasing the need for high-efficiency, durable pumping systems. By prioritizing sustainable infrastructure and technological modernization, Vision 2030 is accelerating adoption of innovative centrifugal pump solutions, boosting market growth, and enhancing operational efficiency across multiple sectors in the Kingdom.

Market Outlook 2026-2034:

The outlook for the Saudi Arabia centrifugal pumps market remains positive, supported by ongoing government investment in water infrastructure, urban development, and the expansion of the oil and gas sector. Large-scale megaprojects under Vision 2030 are creating significant demand for pumping solutions across construction, industrial, and utility applications. These initiatives are driving the need for efficient, reliable, and high-performance pumps to support water management, energy operations, and infrastructure development, positioning the market for steady growth as the country continues to modernize its industrial and urban landscapes. The market generated a revenue of USD 324.5 Million in 2025 and is projected to reach a revenue of USD 455.8 Million by 2034, growing at a compound annual growth rate of 3.85% from 2026-2034.

Saudi Arabia Centrifugal Pumps Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Overhung Impeller |

47% |

|

Stage |

Single Stage Pump |

50% |

|

Flow Type |

Radial Flow Pumps |

62% |

|

Capacity |

Medium Capacity |

38% |

|

End User |

Oil and Gas |

22% |

|

Region |

Northern and Central Region |

29% |

Type Insights:

- Overhung Impeller

- Vertically Suspended

- Between Bearing

Overhung impeller dominates with a market share of 47% of the total Saudi Arabia centrifugal pumps market in 2025.

Overhung impeller centrifugal pumps maintain market leadership due to their compact design, lower maintenance requirements, and versatility across multiple industrial applications. These pumps feature the impeller mounted on the shaft extension beyond the bearing housing, enabling efficient fluid handling in petrochemical processing, water treatment, and HVAC systems. The configuration provides excellent accessibility for maintenance and impeller replacement, reducing downtime in critical operations.

The increasing preference for overhung impeller designs in Saudi Arabia highlights their suitability for the country’s varied industrial sectors. Facilities such as oil refineries, chemical plants, and desalination units favor these pumps for their dependable performance, efficiency, and cost-effectiveness. The adoption of specialized pump configurations in complex industrial environments underscores the importance of tailored solutions capable of handling demanding operational conditions while ensuring reliability, safety, and optimal performance across diverse applications.

Stage Insights:

- Single Stage Pump

- Two Stage Pump

- Multi-Stage Pump

Single stage pump leads with a share of 50% of the total Saudi Arabia centrifugal pumps market in 2025.

Single stage pumps command the largest market share owing to their operational simplicity, cost-efficiency, and suitability for applications requiring low to medium pressure with high flow rates. These pumps utilize a single impeller to move fluids, making them ideal for water circulation, drainage systems, and general industrial transfer operations. The straightforward design translates to reduced manufacturing costs and simplified maintenance procedures.

The segment's dominance in Saudi Arabia stems from extensive deployment across municipal water supply networks, agricultural irrigation systems, and building services applications. The National Water Company's extensive water distribution infrastructure across major cities including Riyadh, Jeddah, and Dammam relies heavily on single stage centrifugal pumps for efficient water transmission. Multi-stage configurations are gaining traction in specialized applications such as high-pressure desalination systems and boiler feed water services.

Flow Type Insights:

- Axial Flow Pumps

- Radial Flow Pumps

- Mixed Flow Pumps

Radial flow pumps exhibit clear dominance with a 62% share of the total Saudi Arabia centrifugal pumps market in 2025.

Radial flow pumps maintain significant market leadership attributed to their exceptional versatility and compatibility across diverse industrial applications. These pumps discharge fluid perpendicular to the pump shaft, generating high pressure suitable for water treatment, chemical processing, and petroleum refining operations. The design enables efficient handling of clean and mildly contaminated fluids at varying viscosities and temperatures.

The Saudi Arabia radial flow pump market is experiencing growth driven by the expansion of desalination plants, water treatment facilities, and oil and gas operations. Demand is concentrated in major industrial and infrastructure hubs, reflecting the strategic importance of these regions for economic and developmental activities. The segment is also benefiting from the increasing adoption of smart, IoT-enabled pumping systems, which enhance operational efficiency, enable real-time monitoring, and support sustainability goals, aligning with the broader objectives of Vision 2030 to modernize infrastructure and promote efficient resource management across the Kingdom.

Capacity Insights:

- Small Capacity

- Medium Capacity

- High Capacity

Medium capacity represents the largest share at 38% of the total Saudi Arabia centrifugal pumps market in 2025.

Medium capacity centrifugal pumps represent the largest market segment, reflecting balanced demand across commercial buildings, municipal infrastructure, and mid-scale industrial applications. These pumps offer optimal flow rates and pressure capabilities suitable for water distribution networks, HVAC systems, and process industries requiring moderate throughput. The segment bridges the gap between compact residential units and large industrial equipment.

Market demand for medium capacity pumps is driven by extensive commercial construction activities and the expansion of urban infrastructure across Saudi Arabia. The Kingdom's construction sector, valued at USD 70.33 billion in 2024 and projected to reach USD 91.36 billion by 2029, creates sustained procurement opportunities for medium-range pumping equipment. High capacity segments are experiencing accelerated growth to support mega desalination projects and industrial expansion initiatives.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Chemicals

- Oil and Gas

- Power Generation

- Construction

- Pharmaceuticals

- Food and Beverages

- Metals and Mining

- Water and Wastewater

- Others

Oil and gas dominate with a market share of 22% of the total Saudi Arabia centrifugal pumps market in 2025.

The oil and gas sector maintains market leadership as Saudi Arabia's position as the world's largest oil producer drives substantial demand for centrifugal pumping equipment. Centrifugal pumps are extensively deployed across upstream extraction operations, midstream transportation, and downstream refining processes. Saudi Aramco's operations, managing hydrocarbon reserves of 250 billion barrels of oil equivalent, require reliable pumping systems for fluid transfer, drilling operations, and process applications.

The sector's expansion continues with Saudi Aramco planning over 110 projects between 2024 and 2026, including 67 oil, gas, and petrochemical developments. Major initiatives such as the Jafurah Gas Development, projected to exceed USD 100 billion in total investment, and the Marjan oil field expansion valued at USD 18 billion, generate significant demand for specialized centrifugal pumps. These projects also require high-reliability pumping solutions for upstream processing, fluid transfer, and utilities, further supporting sustained equipment demand across the value chain.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

Northern and Central Region leads with a share of 29% of the total Saudi Arabia centrifugal pumps market in 2025.

The Saudi Arabia centrifugal pumps market in the northern region is primarily driven by the concentration of industrial and petrochemical facilities, which demand high-performance pumps for processes such as chemical handling, oil refining, and water management. Rapid urbanization and infrastructure development in key cities are further boosting demand for reliable pumping solutions in construction, utilities, and municipal water systems. Additionally, the adoption of advanced, energy-efficient, and IoT-enabled pumps is enhancing operational efficiency, reducing maintenance requirements, and supporting sustainability initiatives across industrial and commercial applications in the region.

In the central region, centrifugal pump demand is fueled by extensive water and wastewater management projects, including desalination, treatment, and distribution systems. The growth of the oil and gas sector, along with large-scale industrial and urban development, is creating a need for durable and high-capacity pumping solutions. Government-led initiatives under Vision 2030 are promoting modernization of infrastructure, adoption of smart pumping technologies, and energy-efficient systems, driving market expansion while ensuring reliable performance and sustainability across municipal, industrial, and construction applications.

Market Dynamics:

Growth Drivers:

Why is the Saudi Arabia Centrifugal Pumps Market Growing?

Expanding Water Infrastructure and Desalination Capacity

Saudi Arabia's strategic commitment to water security is generating substantial demand for centrifugal pumps across desalination, treatment, and distribution infrastructure. The Kingdom currently produces over 12 million cubic meters of desalinated water daily and plans to double capacity to approximately 20 million cubic meters per day by 2030. The Ministry of Environment, Water, and Agriculture intends to meet 90 percent of national water demand using desalinated water by the end of the decade. These infrastructure developments are driving demand for high-efficiency pumping solutions to support seawater intake, reverse osmosis processes, and the distribution of treated water. Expanding water and sanitation projects across the country are creating significant opportunities for advanced pumping systems, enabling efficient water management, reliable operation, and improved sustainability in desalination, transmission, and wastewater treatment applications.

Oil and Gas Sector Expansion and Modernization

The oil and gas sector continues to be a key source of demand for centrifugal pumps, supported by ongoing investments in expanding production capacity and upgrading processing infrastructure. Significant capital is being directed toward large-scale energy projects, including gas field developments and oil field expansions. These projects involve offshore and onshore facilities, subsea networks, and processing units, all of which require advanced and reliable pumping systems to support complex operations and ensure efficient handling of fluids across upstream and downstream activities. For instance, in April 2024, Saudi Aramco awarded USD 7.7 billion in EPC contracts for the Fadhili Gas Plant expansion, directly elevating demand for specialized pumps across extraction, processing, and distribution applications.

Urbanization and Vision 2030 Megaproject Development

Rapid urbanization and ambitious infrastructure development under Vision 2030 are creating sustained demand for pumping equipment across construction, utilities, and building services sectors. The Saudi Arabia construction market size was valued at USD 101.4 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 138.4 Billion by 2034, exhibiting a CAGR of 3.52% from 2026-2034, driving procurement of centrifugal pumps for water distribution, HVAC systems, and fire protection applications. Population growth in Gulf Cooperation Council cities is expected to increase by 30 percent from 2020 to 2030, with the Kingdom constructing 500,000 additional housing units to address expanding demand. Megaprojects including NEOM, the Red Sea development, and Qiddiya require extensive pumping infrastructure for water supply, wastewater treatment, and industrial processes.

Market Restraints:

What Challenges the Saudi Arabia Centrifugal Pumps Market is Facing?

High Initial Investment and Operational Costs

The substantial capital expenditure required for high-efficiency centrifugal pumps poses procurement challenges for small and medium enterprises. Premium pump systems with advanced features including variable frequency drives, corrosion-resistant materials, and smart monitoring capabilities, command significant price premiums over standard equipment. Energy costs and maintenance requirements further contribute to the total cost of ownership concerns.

Supply Chain Dependencies and Import Reliance

The market's dependence on imported components and finished equipment creates vulnerability to global supply chain disruptions and currency fluctuations. While localization initiatives are expanding domestic manufacturing capacity, critical components including specialized alloys, precision bearings, and electronic controls, remain import-dependent. Extended lead times for specialized pump packages can delay project timelines across infrastructure and industrial sectors.

Technical Expertise and Skilled Workforce Constraints

The installation, operation, and maintenance of sophisticated pumping systems require specialized technical expertise that remains in limited supply domestically. Advanced pump technologies incorporating IoT integration, predictive maintenance algorithms, and complex automation systems demand skilled personnel for optimal performance. Training and capability development programs are essential to address the qualified workforce shortage across industrial sectors.

Competitive Landscape:

The Saudi Arabia centrifugal pumps market exhibits moderate concentration, with multinational engineering corporations maintaining significant market presence through local manufacturing facilities and service networks. Leading players compete through product differentiation, technological innovation, and comprehensive after-sales support. Major manufacturers are expanding regional capacity to serve growing demand, with Flowserve maintaining assembly operations in Dammam and Sulzer operating joint ventures with local partners. Regional challengers are gaining market traction by offering modular designs and rapid service response capabilities. Competition increasingly centers on energy efficiency, digital integration, and predictive maintenance capabilities as operators prioritize total cost of ownership and operational reliability.

Recent Developments:

- November 2025: ITT Inc. completed Phase Two of its approximately USD 25 million project to expand the Industrial Process manufacturing facility in Dammam, Saudi Arabia, doubling the company's capacity. The site secured USD 160 million in orders in 2024 and targets over USD 300 million in annual orders by 2030.

- March 2024: ITT Inc. announced an investment of around $11 million to upgrade testing capabilities across three of its Industrial Process (IP) facilities, aiming to increase capacity for handling large-scale projects in its flow business. This expansion underscores the company’s dedication to delivering superior customer service and ensuring high-quality performance in its industrial solutions.

Saudi Arabia Centrifugal Pumps Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Overhung Impeller, Vertically Suspended, Between Bearing |

| Stages Covered | Single Stage Pump, Two Stage Pump, Multi-Stage Pump |

| Flow Types Covered | Axial Flow Pumps, Radial Flow Pumps, Mixed Flow Pumps |

| Capacities Covered | Small Capacity, Medium Capacity, High Capacity |

| End Users Covered | Chemicals, Oil and Gas, Power Generation, Construction, Pharmaceuticals, Food and Beverages, Metals and Mining, Water and Wastewater, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Centrifugal Pumps Market Report

The Saudi Arabia centrifugal pumps market size was valued at USD 324.5 Million in 2025.

The Saudi Arabia centrifugal pumps market is expected to grow at a compound annual growth rate of 3.85% from 2026-2034 to reach USD 455.8 Million by 2034.

Overhung Impeller dominated the market with a 47% share in 2025, driven by its widespread adoption in oil and gas applications, desalination facilities, and general industrial processes where reliability and ease of maintenance are prioritized.

Key factors driving the Saudi Arabia centrifugal pumps market include expanding water infrastructure and desalination capacity under Vision 2030, sustained oil and gas sector investments by Saudi Aramco, rapid urbanization and megaproject development, and increasing adoption of energy-efficient pumping solutions.

Major challenges include high initial investment and operational costs for premium pump systems, supply chain dependencies and import reliance for critical components, technical expertise and skilled workforce constraints, and stringent energy efficiency regulatory requirements driving equipment upgrade pressures.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)