Saudi Arabia Construction Demolition Waste Recycling Market Size, Share, Trends and Forecast by Material, Source, Service, and Region, 2026-2034

Saudi Arabia Construction Demolition Waste Recycling Market Overview:

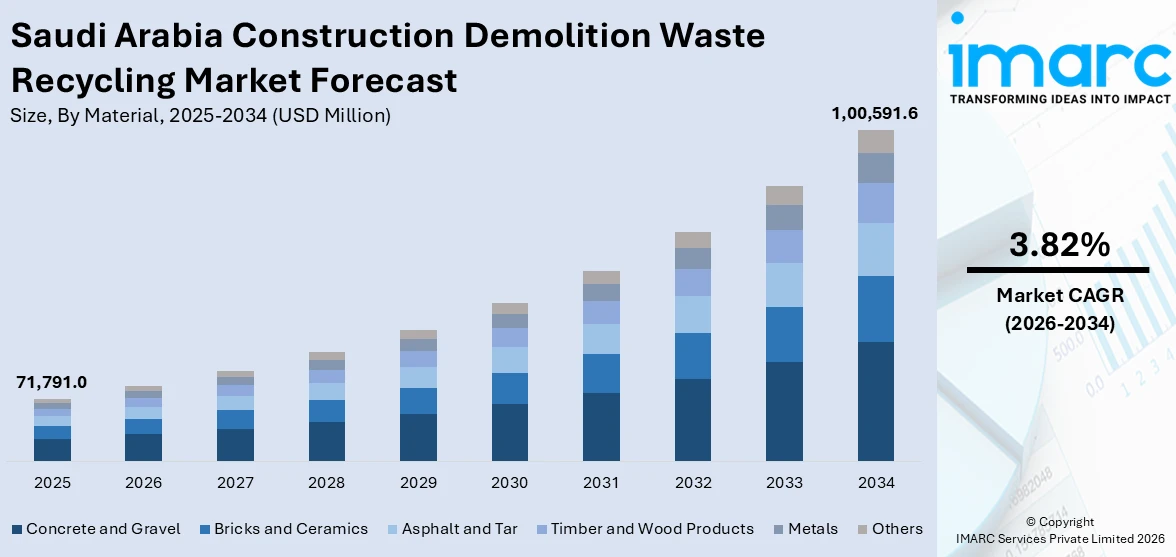

The Saudi Arabia construction demolition waste recycling market size reached USD 71,791.0 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 1,00,591.6 Million by 2034, exhibiting a growth rate (CAGR) of 3.82% during 2026-2034. The market is driven by regulatory mandates under Vision 2030 enforcing recycling targets, infrastructure upgrades introducing advanced processing capabilities, and mega projects generating sustained demand for large-scale material recovery. Contractors are adapting workflows to meet compliance and efficiency standards. These trends are expected to further augment the Saudi Arabia construction demolition waste recycling market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 71,791.0 Million |

| Market Forecast in 2034 | USD 1,00,591.6 Million |

| Market Growth Rate 2026-2034 | 3.82% |

Saudi Arabia Construction Demolition Waste Recycling Market Trends:

Government Regulations and Sustainability Initiatives

Officials are enforcing more stringent waste management regulations to reduce pressure on landfills and protect the ecosystem. These policies are in accordance with Saudi Arabia's long-term development vision, which highlights efficient resource use and sustainable building methods. Through the implementation of regulations regarding appropriate disposal and recycling, the governing authority motivates contractors and developers to embrace environmentally sustainable waste management practices. Moreover, environmental guidelines seek to lower carbon emissions and promote sustainable utilization of natural resources. This drive for adherence opens avenues for the recycling sector to grow, as businesses look for options that satisfy regulatory standards while staying competitive. In addition, government-driven efforts to encourage green building certifications and recycling-oriented practices strengthen the need for effective demolition waste recycling methods, contributing to the market growth.

To get more information on this market Request Sample

Rising Construction and Infrastructure Development

The rapid expansion of construction and infrastructure projects in Saudi Arabia is a crucial factor catalyzing the demand for demolition waste recycling. Urban development, modernization programs, and large-scale initiatives generate vast quantities of debris that must be managed sustainably. Recycling provides a critical solution, enabling the diversion of waste from landfills while reducing reliance on virgin raw materials. In 2025, the Asian Infrastructure Investment Bank (AIIB) and Saudi Arabia signed a joint declaration to advance sustainable infrastructure investments. This partnership emphasizes energy, transport, water, urban development, and renewable energy, underscoring the need for efficient waste management systems to support long-term sustainability. By mobilizing financing and fostering public-private partnerships (PPP), such agreement highlights recycling as a core element of environmentally responsible infrastructure. Contractors and developers increasingly view recycling as essential not only for compliance but also for cost efficiency and future competitiveness.

Integration of Smart City Projects

Saudi Arabia’s commitment to developing smart cities, guided by advanced technologies and sustainable planning, is driving the demand for construction demolition waste recycling. In 2024, A Saudi company, Tilal Real Estates, launched the $1.6 billion "Heart of Khobar" smart city project, located in the eastern port of Khobar. These urban initiatives prioritize resource efficiency, circular practices, and reduced environmental impact, making recycling integral to achieving sustainability goals. Recycling facilities are being incorporated into city designs to ensure proper waste diversion and compliance with international benchmarks. By embedding waste recycling systems into smart city frameworks, the Kingdom ensures that construction and demolition materials are responsibly managed, supporting both economic and environmental objectives. Such high-profile projects showcase Saudi Arabia’s alignment with global green city standards, reinforcing recycling as a symbol of innovation and forward-looking urban transformation.

Saudi Arabia Construction Demolition Waste Recycling Market Growth Drivers:

Technological Advancements in Recycling Processes

Contemporary sorting, crushing, and processing machinery enhances efficiency, minimizes contamination, and allows for greater recovery rates of precious materials. These advancements enhance recycling's feasibility for extensive projects where time and precision are essential. Automation, digital surveillance systems, and intelligent waste tracking solutions are also transforming how businesses manage and enhance demolition waste. Through the integration of technology, companies can optimize operations, improve material quality, and comply with international standards for recycling efficiency. The introduction of new techniques, including mobile recycling units and modular systems, improves operational flexibility, allowing for easier waste recycling directly at project locations. These innovations not only lower logistical expenses but also enhance confidence in recycled products, promoting wider acceptance throughout the sector. Additionally, the shift towards more sustainable and efficient practices is helping businesses align with international environmental goals, fostering a circular economy and reducing reliance on virgin materials.

Educational and Awareness Campaigns

Educational programs and awareness efforts are crucial in advancing the recycling market for construction demolition waste in Saudi Arabia. Government bodies, trade groups, and ecological organizations are funding initiatives to emphasize the advantages of recycling and the dangers of unregulated waste. These initiatives focus on contractors, engineers, laborers, and the broader community, emphasizing that recycling is recognized as an effective and socially responsible option. Workshops, seminars, and technical certifications enhance skill development, allowing construction professionals to implement recycling practices more efficiently. Through raising awareness, these initiatives also aid in addressing resistance to change, fostering trust in the quality and dependability of recycled materials. As time progresses, this cultural and professional transition fosters a more open market landscape, in which recycling is recognized as a typical industry norm. Educational initiatives promote lasting adoption by integrating sustainability into the principles and practices of Saudi Arabia's construction industry.

Development of Waste Management Infrastructure

The development of a robust national waste management infrastructure is a crucial factors impelling the Saudi Arabia construction demolition waste recycling market. Significant investments in collection systems, transfer stations, and modern recycling facilities are improving efficiency and making recycling a practical choice for contractors across the Kingdom. These advancements reduce logistical barriers and enable scalable solutions for mega-projects and expanding urban centers. A key milestone in this effort was reached in 2025, when the Saudi Investment Recycling Company (SIRC) signed a MoU with US-based EIG Management Company, LLC. The agreement focuses on enhancing collaboration in funding and managing infrastructure projects tied to the circular economy and waste management. This initiative not only strengthens financial resources but also accelerates the creation of advanced recycling systems within Saudi Arabia. By expanding infrastructure through such partnerships, recycling is positioned as a core component of project planning and sustainable development nationwide.

Saudi Arabia Construction Demolition Waste Recycling Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on material, source, and service.

Material Insights:

- Concrete and Gravel

- Bricks and Ceramics

- Asphalt and Tar

- Timber and Wood Products

- Metals

- Others

The report has provided a detailed breakup and analysis of the market based on the material. This includes concrete and gravel, bricks and ceramics, asphalt and tar, timber and wood products, metals, and others.

Source Insights:

Access the comprehensive market breakdown Request Sample

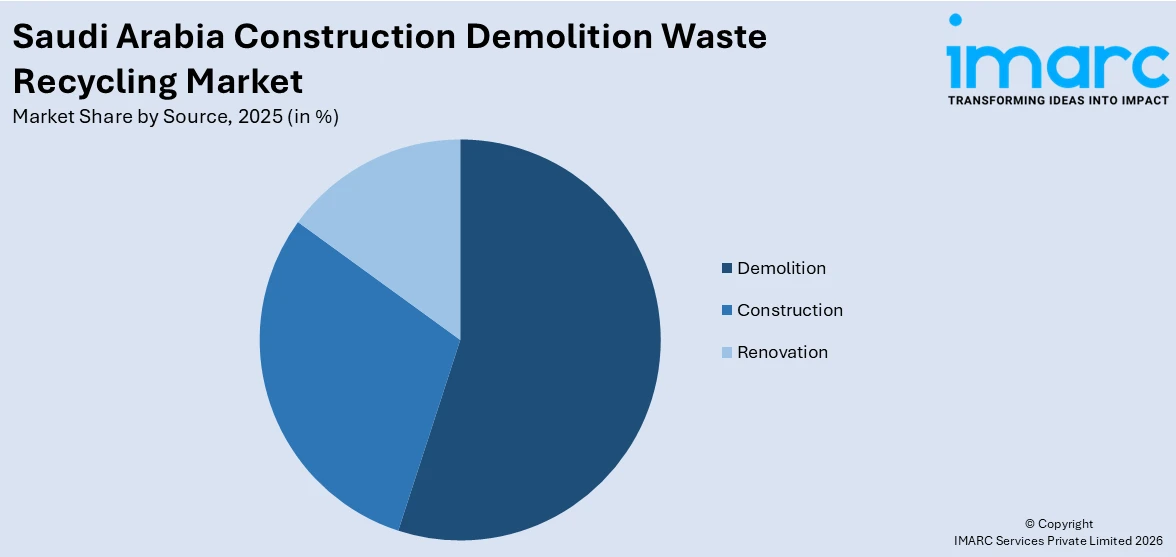

- Demolition

- Construction

- Renovation

The report has provided a detailed breakup and analysis of the market based on the source. This includes demolition, construction, and renovation.

Service Insights:

- Disposal

- Collection

The report has provided a detailed breakup and analysis of the market based on the service. This includes disposal and collection.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

The report has also provided a comprehensive analysis of all major regional markets. This includes Northern and Central Region, Western Region, Eastern Region, and Southern Region.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Saudi Arabia Construction Demolition Waste Recycling Market News:

- In August 2025, the Saudi Roads General Authority (RGA) met with the National Center for Waste Management (MWAN) to explore expanding the use of demolition waste in asphalt mixes. This initiative aims to reduce environmental waste, improve resource efficiency, and enhance the Kingdom's road infrastructure. It aligns with Saudi Arabia's broader goals to improve logistics and road safety by 2030.

- In January 2025, Saudi Arabia's Roads General Authority completed the country's first road using recycled construction and demolition (C&D) waste in the asphalt mixture. This sustainable project, developed in partnership with Al Ahsa Municipality and MWAN, supports Saudi Arabia's Vision 2030 goals, aiming for a 60% C&D waste recycling rate by 2035. The initiative reduces environmental impact and promotes resource efficiency in road construction.

- On 15 May 2023, EDGE Innovate announced its role in equipping Saudi Arabia’s first construction waste recycling facility in Al Khair, Riyadh, operated by SIRC. The 1.3 million m² plant, launched in July 2021, processes 600 tons of waste per hour with a targeted recycling rate above 90%, aiming to recover 20 million tons of legacy debris and 5 million tons of annual CDW by 2035. The facility supports Vision 2030 goals by supplying recycled materials for major projects, including a 35,000-unit housing development.

- On 15 May 2023, Akam, a subsidiary of the Saudi Investment Recycling Company (SIRC Group), signed a memorandum of cooperation with Qatar’s Alawalya for Primary Materials to advance joint efforts in construction and demolition waste recycling. The agreement covers technical reviews of sorting lines, reuse solutions for soil and powder residues in fertilization and roadworks, and the exchange of Qatari specifications and studies for recycled materials.

Saudi Arabia Construction Demolition Waste Recycling Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Materials Covered | Concrete and Gravel, Bricks and Ceramics, Asphalt and Tar, Timber and Wood Products, Metals, Others |

| Sources Covered | Demolition, Construction, Renovation |

| Services Covered | Disposal, Collection |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia construction demolition waste recycling market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia construction demolition waste recycling market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia construction demolition waste recycling industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Construction Demolition Waste Recycling Market Report

The construction demolition waste recycling market in Saudi Arabia was valued at USD 71,791.0 Million in 2025.

The Saudi Arabia construction demolition waste recycling market is projected to exhibit a CAGR of 3.82% during 2026-2034, reaching a value of USD 1,00,591.6 Million by 2034.

The Saudi Arabia construction demolition waste recycling market is driven by rising construction activities, government regulations promoting sustainability, and increasing pressure to reduce landfill usage. The growing demand for recycled materials, cost efficiency in waste management, and national initiatives supporting circular economy practices further influence the market, aligning with environmental conservation and resource optimization goals.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)