Saudi Arabia Construction Market Size, Share, Trends and Forecast by Sector and Region, 2026-2034

Saudi Arabia Construction Market Size, Share, Trends & Forecast (2026-2034)

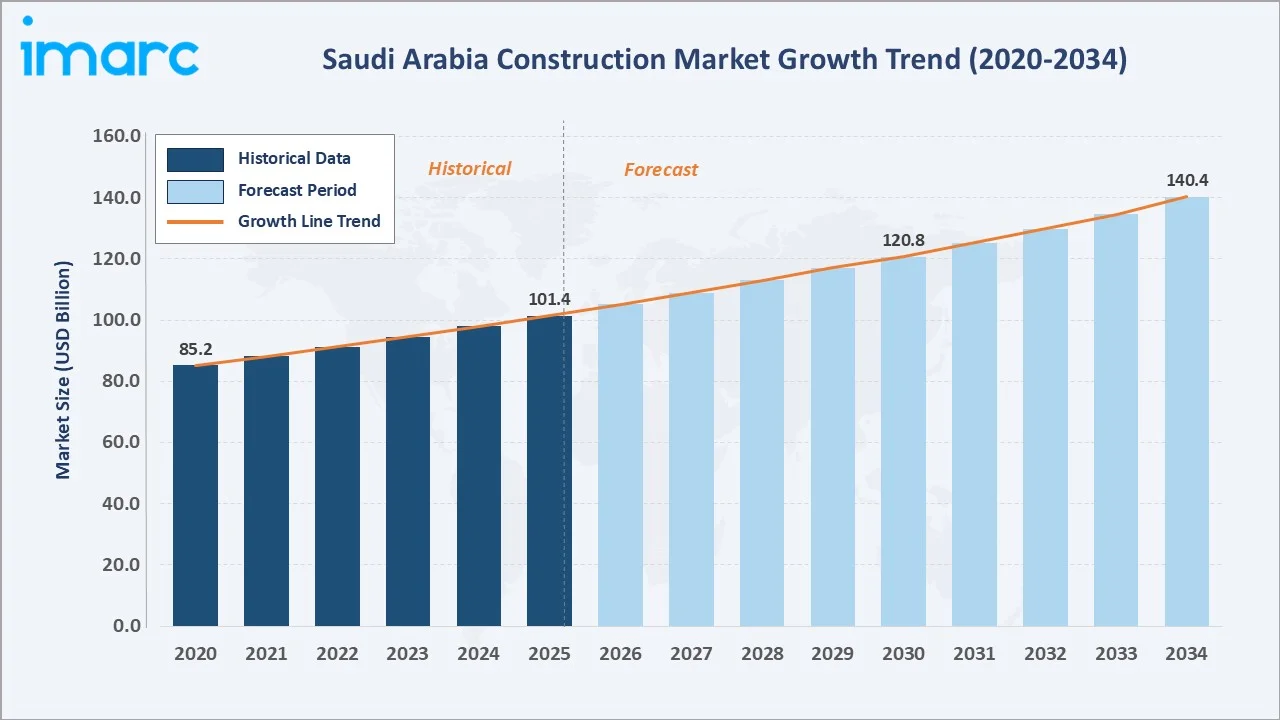

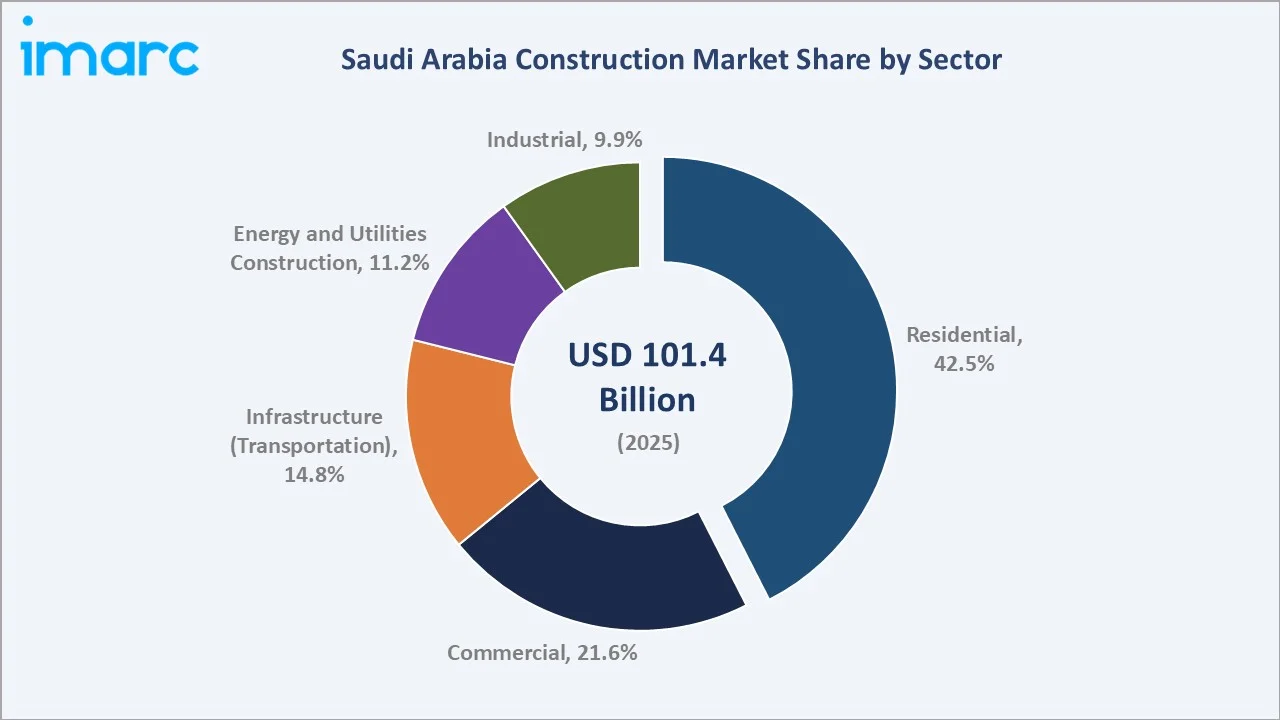

The Saudi Arabia construction market reached USD 101.4 Billion in 2025 and is projected to reach USD 140.4 Billion by 2034, exhibiting a CAGR of 3.6% during 2026-2034. The market is driven by Vision 2030 giga-projects, robust government investment in housing and infrastructure, expanding tourism infrastructure, and a growing private sector role in commercial development.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 101.4 Billion |

|

Forecast Market Size (2034) |

USD 140.4 Billion |

|

CAGR (2026-2034) |

3.6% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Sector |

Residential – 42.5% (2025) |

|

Largest Region |

Western Region – 38.6% (2025) |

|

Fastest Growing Segment |

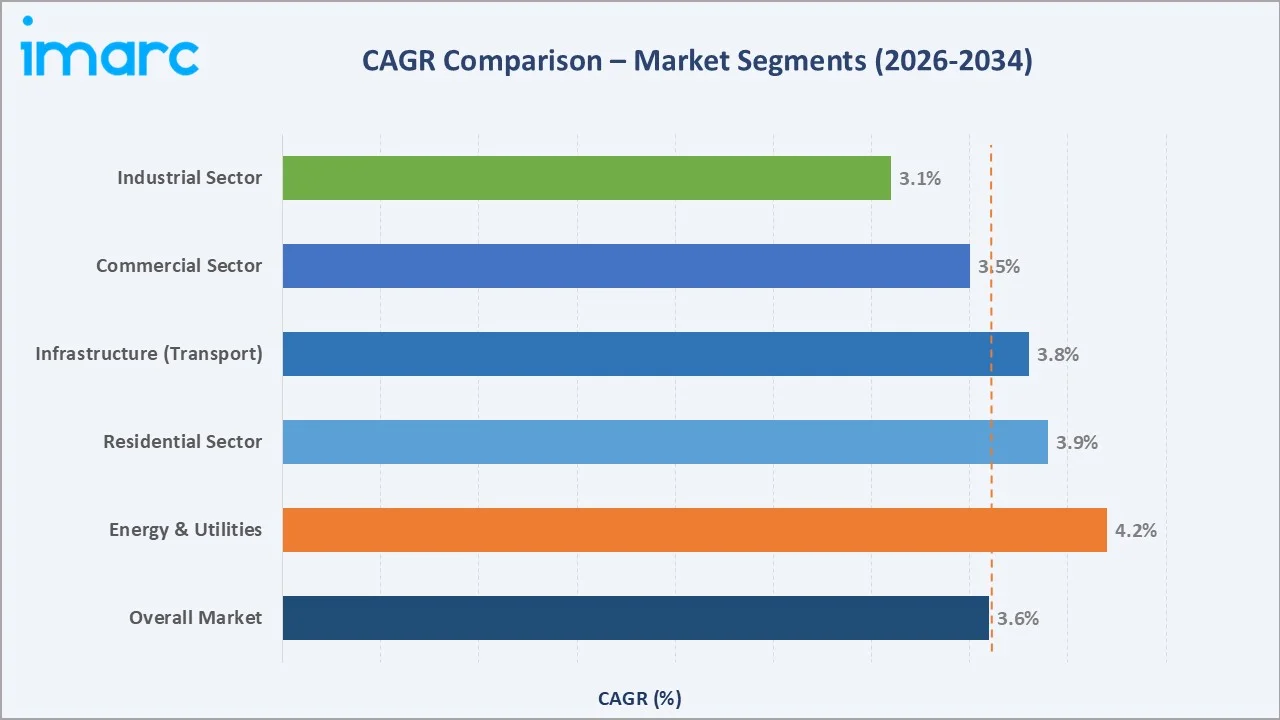

Energy & Utilities – est. CAGR ~4.2% (2026-2034) |

To get more information on this market, Request Sample

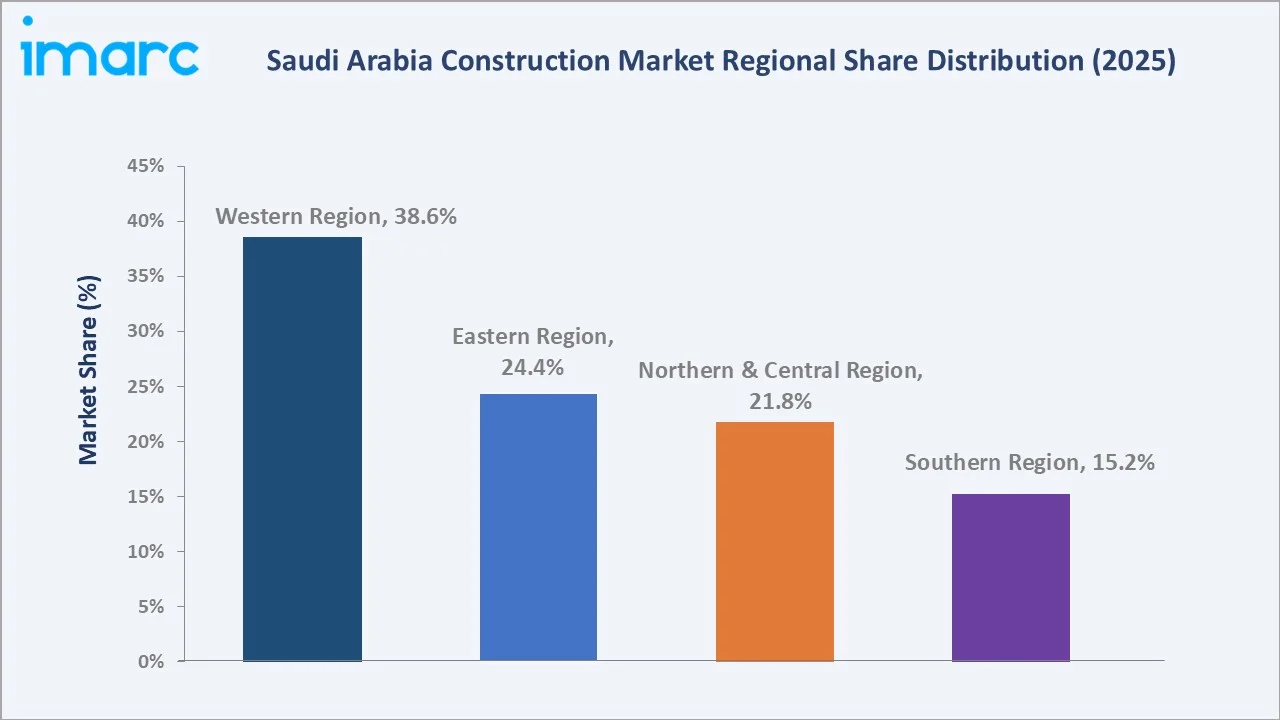

Saudi Arabia’s construction market is led by the Western Region, accounting for 38.6% of revenues, driven by large-scale urban and tourism projects. By sector, residential construction dominates with a 42.5% share, supported by rising housing demand, population growth, and government-led initiatives to expand affordable and urban housing infrastructure.

From USD 85.2 Billion in 2020 to USD 101.4 Billion in 2025 and a projected USD 140.4 Billion by 2034 the market has expanded at a consistent pace. The 2030 checkpoint at USD 120.8 Billion underscores the steady compound growth trajectory. The post-2025 acceleration is primarily attributed to giga-project execution ramp-ups and Energy & Utilities construction spending tied to Saudi Arabia's renewable energy targets.

Executive Summary

The Saudi Arabia construction market stands as one of the most dynamic construction economies in the Middle East, supported by the government's ambitious Vision 2030 transformation agenda. Valued at USD 101.4 Billion in 2025, the market is forecast to reach USD 140.4 Billion by 2034, growing at a steady 3.6% CAGR.

The Residential sector remains the dominant driver at 42.5% share in 2025. ROSHN plans to invest over SAR 350 billion ($93.3 billion) over the next decade, creating communities housing over 1.5 million people from all income groups.

The Western Region leads geographically at 38.6%, supported by grand mosque expansion projects, Jeddah's commercial development pipeline, and ROSHN's western cluster. The Northern & Central Region home to NEOM, Qiddiya, and the Diriyah Gate Authority is the most strategically significant growth zone for the 2026–2034 period.

Key Market Insights

|

Insight |

Data |

|

Largest Sector Segment |

Residential – 42.5% share (2025) |

|

Second Largest Sector |

Commercial – 21.6% share (2025) |

|

Fastest Growing Segment |

Energy & Utilities – est. CAGR ~4.2% (2026-2034) |

|

Largest Region |

Western Region – 38.6% share (2025) |

|

Top Companies |

Bechtel Corporation, Fluor Corporation, Jacobs, Tekfen Construction, Gilbane Inc., AFRAS, AL Jazirah Engineers & Consultants, and Al-Latifia Trading and Contracting |

Key Analytical Observations Supporting the Above Data:

- Residential sector commands 42.5% share (2025): ROSHN's ambition to deliver 1.5 million homes by 2030 has directly catalyzed residential construction spend. Saudi Arabia aims to raise the home ownership rate to 70% by 2030, in line with the objectives of the Housing Program, one of Vision 2030’s key initiatives.

- Western Region leads at 38.6% revenue share (2025): Ongoing Grand Mosque expansion in Makkah, Madinah's Prophet's Mosque development, and Jeddah's waterfront mega-projects collectively drive the highest construction density in the kingdom.

- Energy & Utilities fastest-growing at ~4.2% CAGR (2026-2034): With a transformative $32 billion investment pipeline, the Kingdom is positioning itself as a global leader in sustainable energy by 2030. Under Vision 2030, Saudi Arabia aims to generate 50% of its electricity from renewable sources, expanding total capacity to 130 gigawatts (GW), including 58.7 GW from solar and 40 GW from wind, reinforcing its clean energy transition.

- NEOM alone represents USD 500 Billion in planned investment: This giga-project in the Northern & Central Region is reshaping the kingdom's construction pipeline, with THE LINE, OXAGON, and SINDALAH components under active development phases.

- Commercial sector at 21.6% driven by tourism target of 150 million visitors annually by 2030: Hotel, resort, and mixed-use construction projects linked to Saudi tourism expansion add significant volume to the commercial construction pipeline through 2034.

Saudi Arabia Construction Market Overview

The Saudi Arabia construction industry encompasses a broad spectrum of activities across the built environment lifecycle from land development, design, and procurement through construction execution, commissioning, and facility management.

The ecosystem involves a layered value chain spanning raw material suppliers (cement, steel, aggregates), engineering consultants, EPC contractors, project developers, logistics providers, and end-user entities comprising government bodies, corporates, and individual consumers. The market recorded USD 85.2 Billion in 2020, growing to USD 101.4 Billion by 2025 a 19% expansion over five years underpinned by government capital expenditure programs.

Macroeconomic tailwinds such as a stable oil-linked fiscal surplus, significant PIF (Public Investment Fund) capital deployment, and the National Transformation Program provide the financial foundation for sustained construction activity. Rising urbanization with over 85% of Saudi Arabia's population already urban continues to drive demand for all categories of built infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

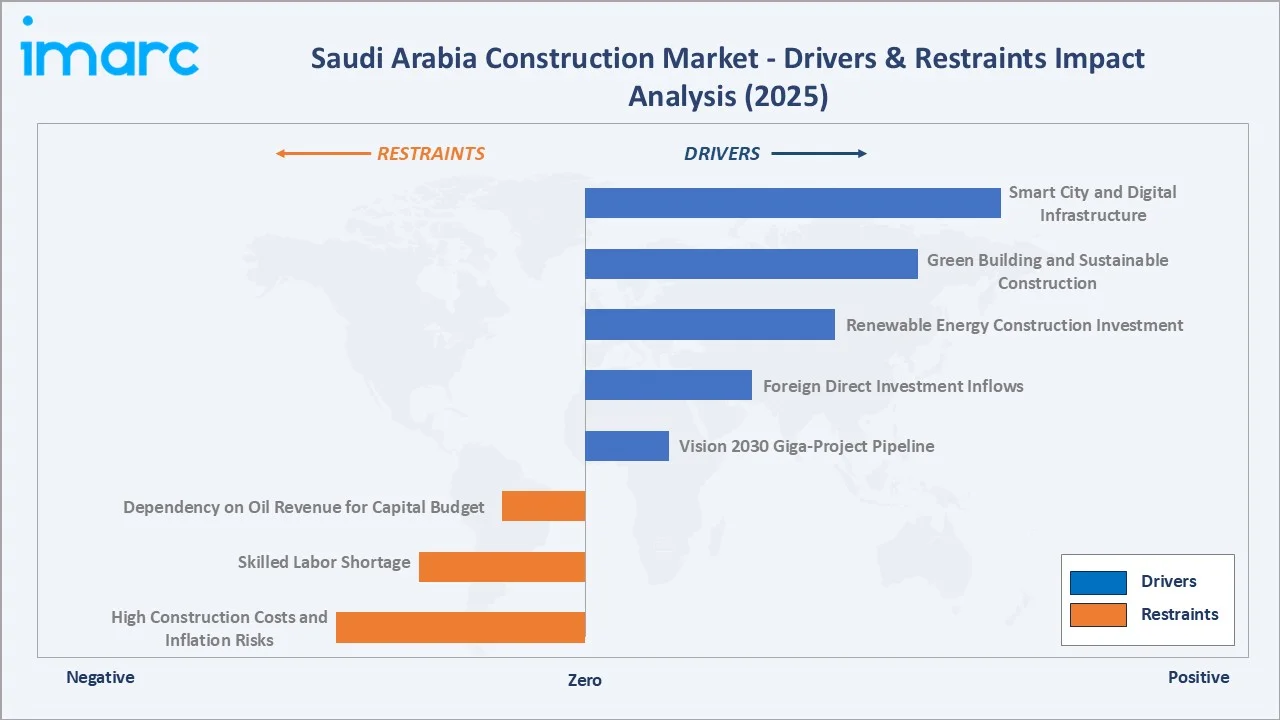

Market Drivers

- Vision 2030 Giga-Project Pipeline: The Saudi government has committed USD 1 Trillion in strategic project investments through 2030, including NEOM (USD 500 Billion), Red Sea Project (USD 15-16 Billion), and Diriyah Gate (USD 20 Billion). These projects are transforming the construction demand landscape.

- Foreign Direct Investment Inflows: Saudi Arabia attracted over USD 31.72 Billion in FDI in 2024. This fuels commercial and industrial construction, particularly in special economic zones such as SPARK (Saudi Arabia Special Economic Zone) and Ras Al-Khair Industrial City.

- Renewable Energy Construction Investment: The Kingdom’s NEOM and National Renewable Energy Program aim to achieve 50% renewable electricity by 2030. Solar, wind, and green hydrogen infrastructure present a significant construction opportunity through 2034, driving strong growth in the Energy and Utilities segment.

Market Restraints

- High Construction Costs and Inflation Risks: Post-2022 commodity price inflation has elevated steel and cement costs significantly. Construction cost inflation impacted project margins and feasibility assessments for smaller developers.

- Skilled Labor Shortage: Saudi Arabia faces a structural shortage of mid-tier construction supervisors and skilled tradespeople. Nationalization targets under Saudization further complicate workforce planning, as the sector remains heavily reliant on foreign labor, creating challenges in balancing localization goals with project execution needs.

Market Opportunities

- Green Building and Sustainable Construction: Saudi Arabia’s Vision 2030 actively promotes LEED and GSAS-certified sustainable construction. The growing focus on green building practices is creating strong premium-segment opportunities for specialized contractors, driven by increasing demand for energy-efficient, environmentally compliant, and sustainable infrastructure development.

- Smart City and Digital Infrastructure: NEOM's digital city requirements and Riyadh Smart City initiatives create demand for construction-integrated ICT infrastructure, smart utilities, and building automation systems a high-growth, high-value construction niche.

Market Challenges

- Dependency on Oil Revenue for Capital Budget: Construction spend is closely linked to government fiscal capacity. Oil price downturns as seen in 2020 risk project deferrals and capital budget contractions, as demonstrated when Saudi Arabia's construction sector contracted % in 2020.

- Supply Chain Bottlenecks: Saudi Arabia imports a significant share of specialty construction materials, mechanical equipment, and finishing products. Global supply chain disruptions as experienced in 2021–2022 extend project timelines and elevate procurement costs.

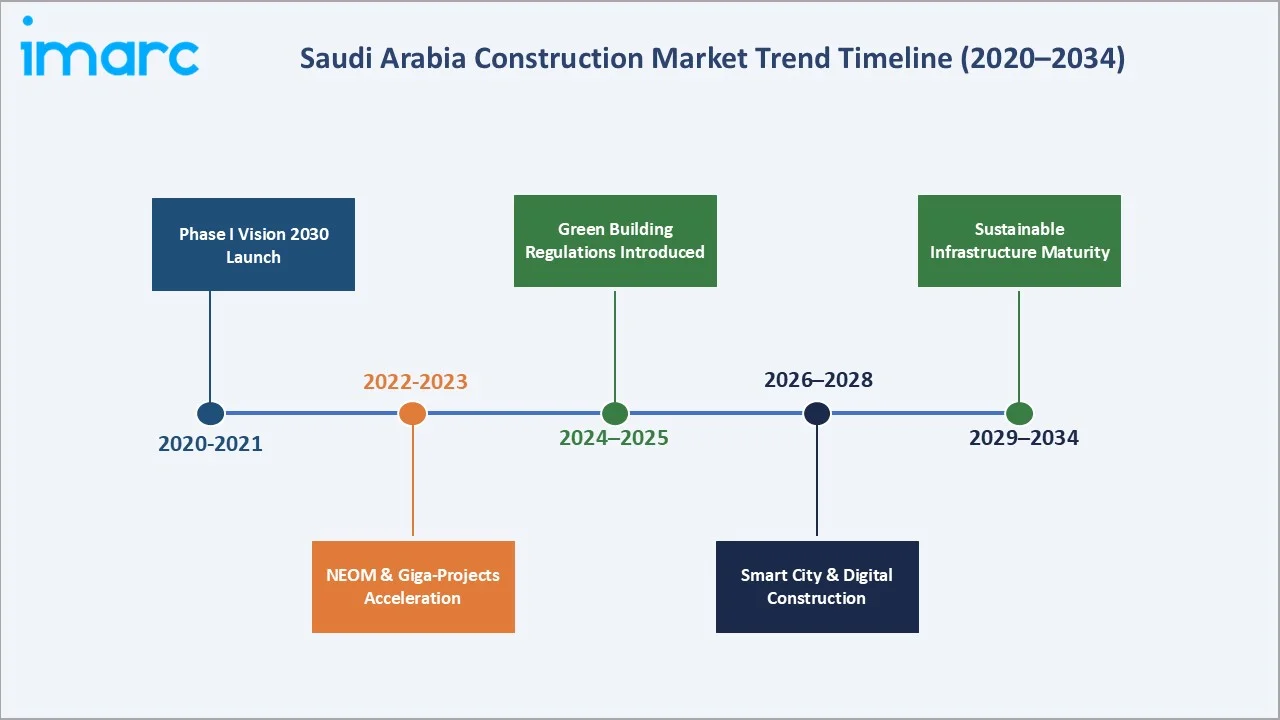

Emerging Market Trends

The following five trends are actively reshaping the Saudi Arabia construction market growth trajectory through 2034:

1. Modular and Off-Site Construction Adoption

Modular construction is gaining traction in Saudi Arabia's housing sector, with ROSHN and several government-backed developers exploring volumetric modular and prefabricated panel systems to accelerate delivery timelines. The National Housing Company (NHC) has piloted prefabricated residential units across multiple regions.

2. Shift Toward Renewable Energy and Green Infrastructure

The national commitment to 50% renewable electricity by 2030 under the National Renewable Energy Program (NREP) is generating significant construction demand for solar parks, wind farms, and green hydrogen facilities. Al-Shuaibah Solar PV Project (2.6 GW) and the NEOM Green Hydrogen Complex are among the flagship energy infrastructure projects reshaping the construction pipeline. This trend directly supports the Energy & Utilities segment.

3. Smart City and Digital Construction Integration

NEOM's THE LINE and SINDALAH developments are pioneering the integration of BIM (Building Information Modeling), AI-powered construction management, and IoT-enabled smart infrastructure within Saudi construction projects. The government's Smart Cities Program covering Riyadh, Jeddah, and NEOM.

4. Tourism Infrastructure Expansion

Saudi Arabia's tourism construction boom driven by the Red Sea Project, AMAALA, Diriyah Gate, and Aseer Development is creating a new high-value commercial construction category. The tourism sector is expected to contribute 10% of GDP by 2030, requiring 320,000 new hotel keys and significant resort, entertainment, and retail infrastructure investment.

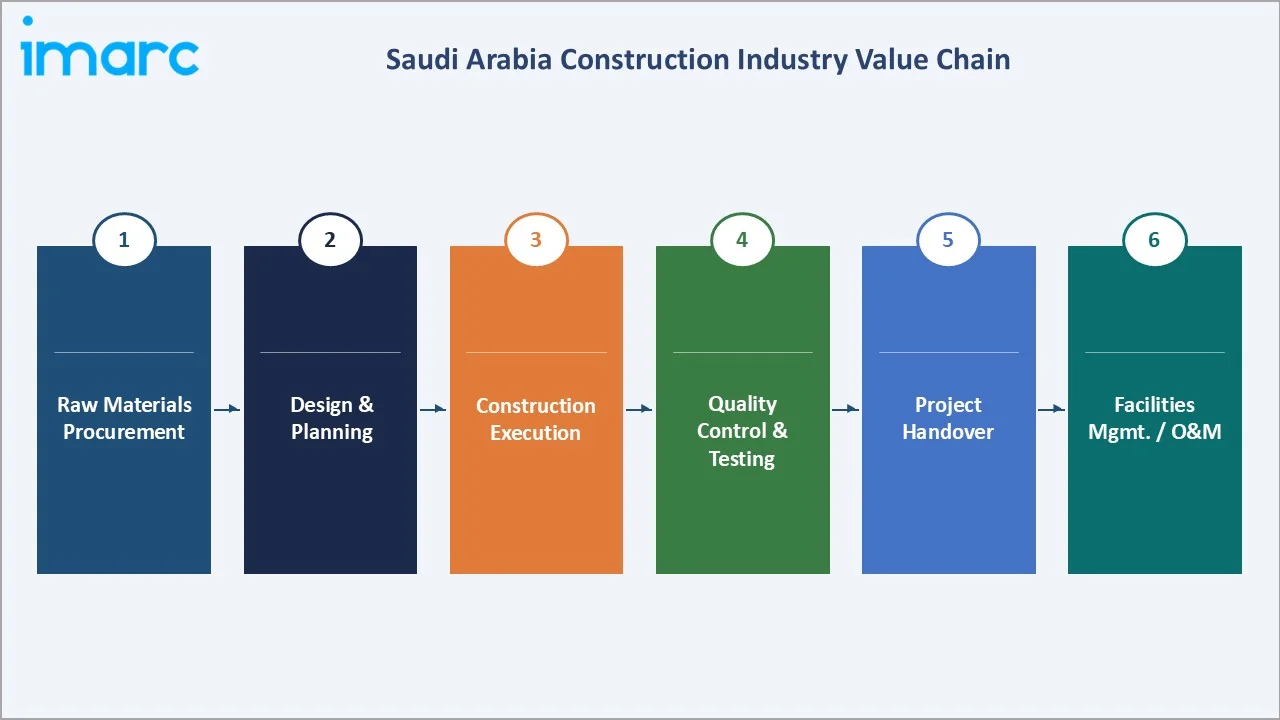

Industry Value Chain Analysis

The Saudi Arabia construction industry value chain encompasses six interconnected stages from raw material procurement through facility management and operations. Each stage involves specialized actors, with increasing integration and consolidation among large EPC contractors.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Saudi Aramco, SABIC, Al Rajhi Cement, ACC, Arabian Cement Company |

|

Design & Engineering |

Dar Al-Handasah, Atkins, Aecom, Parsons, WSP Global |

|

Construction |

Bechtel, Fluor, Tekfen, Saudi Bin Ladin Group, El Seif Engineering |

|

Project Development |

NEOM, ROSHN, PIF, Red Sea Global, Diriyah Gate Authority |

|

Logistics & Equipment |

Al-Futtaim, Al Muhaidib, Arabian Industries, Caterpillar KSA |

|

Operations & Maintenance |

Facilities Management Arms, ENGIE KSA, Emrill, Khidmah |

The value chain is increasingly being consolidated through PPP (Public-Private Partnership) frameworks and integrated project delivery (IPD) contracts, where major EPC contractors such as Bechtel and Fluor manage multiple value chain stages simultaneously.

Technology Landscape in the Saudi Arabia Construction Industry

Building Information Modelling (BIM)

Saudi Arabia’s Ministry of Municipal, Rural Affairs, and Housing mandates BIM Level 2 compliance for major public projects. Adoption is widespread among leading contractors, with flagship developments such as NEOM, Red Sea Global, and PIF projects leveraging advanced BIM for integrated design-to-build workflows, improving coordination and reducing design conflicts and rework costs.

Prefabrication and Modular Construction

Prefabricated and modular construction technologies are gaining momentum, particularly in the Residential sector. ROSHN's partnership with global modular suppliers be delivered via off-site manufacturing by 2027. The NEOM gigafactory concept plans to industrialize construction component manufacturing within the project boundary.

Drone and AI-Powered Site Management

AI-powered project management platforms including Autodesk Construction Cloud and Oracle Primavera – are widely deployed across mega-project sites. Drone-based site surveillance and progress monitoring reduces manual inspection costs with NEOM and Red Sea Project deploying drone fleets across their multi-hundred-kilometre project footprints.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Sector |

Residential |

42.5% |

2025 |

|

Region |

Western Region |

38.6% |

2025 |

By Sector

Residential Sector – 42.5%

To access detailed market analysis, Request Sample

The Residential sector is the largest construction segment, accounting for 42.5% of total market revenue in 2025. Residential construction investment reached approximately USD 43.3 billion in 2023, driven by strong demographic pressure and rising housing demand, with the Kingdom targeting the development of 660,000 residential units by 2030 to support long-term urban expansion.

Regional Market Insights

Saudi Arabia's construction market is geographically segmented into four key regions: Western, Eastern, Northern & Central, and Southern. Each region demonstrates distinct demand drivers, project compositions, and growth trajectories.

|

Region |

Share (2025) |

Growth Driver |

Key Projects |

|

Western Region |

38.6% |

Makkah & Madinah mega-projects |

Grand Mosque expansion, ROSHN Western |

|

Eastern Region |

24.4% |

Oil & industrial infrastructure |

Aramco HQ, SABIC Jubail expansions |

|

Northern & Central Region |

21.8% |

NEOM & Riyadh growth corridor |

NEOM, Qiddiya, Diriyah Gate |

|

Southern Region |

15.2% |

Tourism & military infra |

Aseer region tourism, Jizan port |

The Western Region commands the largest market share at 38.6% (approximately USD 39.1 Billion in 2025). Jeddah, Makkah, and Madinah form the tripartite hub of this region's construction activity. The ongoing Grand Mosque expansion and Prophet's Mosque development are among the world's largest construction projects by value.

Competitive Landscape

The Saudi Arabia construction market features a mixed competitive structure of global EPC leaders, multinational engineering firms, and established regional contractors. The top-tier is dominated by global players with deep project management capabilities and long-standing Saudi government relationships.

|

Company Name |

Brand / Business Focus |

Market Position |

Primary Strength |

|

Bechtel Corporation |

Saudi Arabian Bechtel Company (SABCO) |

Leader |

EPC, mega-infrastructure |

|

Fluor Corporation |

Fluor Arabia |

Leader |

Energy & industrial EPC |

|

Jacobs |

Jacobs KSA |

Leader |

Advisory & program management |

|

Tekfen Construction |

Tekfen Construction & Installation Company |

Challenger |

Industrial & energy projects |

|

Gilbane Inc. |

Gilbane KSA |

Challenger |

Commercial & institutional |

|

AFRAS |

Afras Trading & Contracting Company |

Emerging |

Local contracting, residential |

|

AL Jazirah Engineers & Consultants |

AL Jazirah |

Emerging |

Consulting, urban planning |

|

Al-Latifia Trading and Contracting |

Al Latifa |

Emerging |

Local civil contracting |

Global leaders Bechtel Corporation, Fluor Corporation, Jacobs leverage their EPC expertise and global supply chains to secure the largest government and Aramco contracts. Tekfen Construction, and Gilbane Inc. represent strong mid-tier challengers with proven track records in industrial and institutional construction.

Key Company Profiles

Bechtel Corporation

Bechtel Corporation is one of the world's largest construction and engineering companies, with a century-long operating history and a strong presence across Saudi Arabia's mega-project landscape. Bechtel has been involved in major Saudi projects including the Riyadh Metro, Jubail Industrial City, and components of the Red Sea Project.

- Services Offered: Engineering, Procurement, Construction (EPC); Project Management Consultancy; Program Management.

- Recent Developments: In 2025, Bechtel signed an agreement with the King Salman International Airport Development Company to serve as the delivery partner for three new terminals at King Salman International Airport (KSIA) in Riyadh.

- Strategic Focus: Scaling digital construction capabilities through Bechtel Digital, targeting AI-powered site management and BIM integration across Saudi projects.

Fluor Corporation

Fluor Corporation is a global engineering, procurement, construction, and maintenance (EPCM) company with deep roots in Saudi Arabia's energy and industrial sectors. Fluor has maintained operations in the Kingdom for over four decades, building a strong track record with Saudi Aramco and SABIC project portfolios.

- Services Offered: EPCM for energy, chemicals, and industrial facilities; government infrastructure; advanced technologies.

- Recent Developments: In 2023, Fluor Corporation has won the offsites and utilities package as part of the larger Ras al-Khair crude-oil-to-chemicals complex project.

- Strategic Focus: Renewable energy construction and Net Zero infrastructure, supporting Saudi Arabia's clean energy transition.

Jacobs

Jacobs is a global professional services company providing technical consulting, engineering, and project management services. In Saudi Arabia, Jacobs operates through its advisory and project management arm, serving PIF portfolio projects and government program offices.

- Services Offered: Program Management Consultancy (PMC); advisory services; environmental and sustainability consulting.

- Recent Developments: In 2025, Jacobs confirmed its role in NEOM’s Oxagon project, providing technical and environmental advisory services to DataVolt as part of a $5 billion net-zero data center initiative.

- Strategic Focus: Digital delivery and smart infrastructure advisory, with particular emphasis on NEOM and Saudi Vision 2030 program management.

Market Concentration Analysis

The Saudi Arabia construction market exhibits a moderately fragmented competitive structure. The top 5 players Bechtel Corporation, Fluor Corporation, Jacobs, Tekfen Construction, and Gilbane Inc. collectively account for an estimated 28–32% of total construction value in 2025.

The Residential sector the largest at 42.5% is the most fragmented, with ROSHN, NHC, and thousands of smaller developers and contractors operating across regional markets. The Industrial and Energy & Utilities sectors are the most concentrated, with top 5 players commanding approximately 45–55% of segment revenue due to the specialized nature of EPC contracts.

Investment & Growth Opportunities

Fastest Growing Segments

- Energy & Utilities Construction estimated ~4.2% CAGR (2026–2034), driven by NREP's 130 GW renewable capacity target and green hydrogen infrastructure.

- Hospitality and tourism construction is witnessing strong growth, driven by major developments such as the Red Sea Project, AMAALA, and broader tourism expansion initiatives across Saudi Arabia.

Emerging Markets

- Southern Region: The Aseer Tourism Program and ongoing infrastructure upliftment represent an underserved growth frontier. Market share at 15.2% offers disproportionate growth runway.

- Northern Region: The USD 500 Billion NEOM mega-project is at an early execution stage, with the majority of construction spend expected between 2026–2032.

- Smart City and Digital Infrastructure: Saudi Arabia's Smart Cities Program is creating demand for construction-integrated technology systems, including smart utilities, AI-powered building management, and sensor-embedded infrastructure.

Venture Investment Trends

- PIF's USD 40 Billion annual deployment capacity provides a structural backstop for construction investment across its portfolio of mega-projects and Vision 2030 programs.

- International construction firms are increasingly entering Saudi Arabia through minority stakes in local contractors, enabling compliance with Saudization mandates while securing preferred contractor status.

- Green construction financing through ESG-linked bonds and sustainability-linked loans is gaining traction. The Saudi Green Finance Framework (2023) supports project-level green financing for LEED-certified and net-zero construction.

Future Market Outlook (2026-2034)

The Saudi Arabia construction market is positioned for sustained growth over the 2026–2034 forecast period, projected to expand from USD 101.4 Billion in 2025 to USD 140.4 Billion by 2034 at a 3.6% CAGR. The market trajectory reflects three distinct sub-periods: an acceleration phase (2026–2028); a stabilization phase (2029–2031); and a maturity phase (2032–2034).

Technological disruptions will reshape construction economics over this period. The widespread adoption of modular construction, AI-powered project management, and autonomous equipment is expected to reduce construction delay by 20–30%. This productivity improvement supports margin expansion for leading contractors while enabling faster project delivery timelines critical for Saudi Arabia's ambitious 2030 milestones.

The Energy & Utilities sector's transformation from oil-dependent infrastructure to renewable energy systems represents the most significant structural shift in the Saudi construction market through 2034. Green hydrogen, solar gigafarms, and smart grid infrastructure will constitute a growing share of construction value, reshaping contractor capability requirements and supply chain configurations.

Research Methodology

Primary Research

Primary research comprised structured interviews and surveys with over 80 stakeholders across the Saudi Arabia construction value chain, including senior executives from EPC contractors, project developers, government project offices, materials suppliers, and industry associations. Primary research data was collected during Q3–Q4 2024 and Q1 2025.

Secondary Research

Secondary research incorporated data from Saudi Vision 2030 annual progress reports, Ministry of Municipal & Rural Affairs project registers, MEED Projects database, Saudi Contractors Authority (SCA) publications, NEOM official project filings, PIF annual reports, company financial disclosures (annual reports, investor presentations), and international construction cost databases. Secondary data was triangulated against primary findings to ensure consistency.

Forecasting Models

Market sizing employs a bottom-up approach aggregating sector-level construction value across Residential, Commercial, Industrial, Infrastructure, and Energy & Utilities verticals, using project pipeline data, government capital expenditure budgets, and private sector investment disclosures. Top-down validation uses Saudi Arabia's GDP, government GFCF (Gross Fixed Capital Formation) in construction, and regional GDP growth rates. CAGR projections of 3.6% (2026–2034) are derived through regression-adjusted trend analysis incorporating Vision 2030 project execution milestones.

Saudi Arabia Construction Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sectors Covered | Residential, Commercial, Industrial, Infrastructure (Transportation), Energy and Utilities Construction |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Bechtel Corporation, Fluor Corporation, Jacobs, Tekfen Construction, Gilbane Inc., AFRAS, AL Jazirah Engineers & Consultants, Al-Latifia Trading and Contracting, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia construction market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia construction market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia construction industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Construction Market Report

The Saudi Arabia construction market reached USD 101.4 Billion in 2025, reflecting consistent growth driven by Vision 2030 project execution and government capital investment programs.

The market is projected to reach USD 140.4 Billion by 2034, growing at a CAGR of 3.6% during 2026-2034, supported by giga-projects and renewable energy infrastructure investment.

The Saudi Arabia construction market is forecast to grow at a 3.6% CAGR between 2026 and 2034, driven by residential, commercial, and energy sector construction activities.

The residential sector leads with a 42.5% share in 2025, supported by ROSHN's 1.5 million housing unit target and government mortgage guarantee programs.

The Western Region leads with a 38.6% market share in 2025, anchored by Makkah, Madinah, and Jeddah mega-development projects.

Energy & Utilities Construction is the fastest-growing segment, estimated at ~4.2% CAGR through 2034, driven by Saudi Arabia's 130 GW renewable energy capacity target.

Key players include Bechtel Corporation, Fluor Corporation, Jacobs, Tekfen Construction, Gilbane Inc., AFRAS, AL Jazirah Engineers & Consultants, and Al Latifa Trading and Contracting.

Vision 2030 is the primary demand driver, supporting large-scale strategic projects such as NEOM, the Red Sea Project, Qiddiya, and Diriyah Gate, which are collectively reshaping the Kingdom’s construction pipeline and driving long-term sector growth.

NEOM's USD 500 Billion planned investment is driving significant demand across the Northern & Central Region, spanning residential, commercial, energy, and industrial construction verticals.

Key challenges include high construction cost inflation, skilled labor shortages, oil price volatility affecting government budgets, and mega-project execution complexity.

Renewable energy construction across solar, wind, and green hydrogen represents a significant growth opportunity through 2034, directly supporting the Energy and Utilities segment as the fastest-growing area within the construction market.

The market is moderately fragmented; top 5 players hold ~28–32% share. The residential sub-sector is highly fragmented, while industrial and energy construction is more concentrated among top-tier EPC contractors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)