Saudi Arabia Fiber Optics Market Size, Share, Trends and Forecast by Cable Type, Optical Fiber Type, Application, and Region, 2026-2034

Saudi Arabia Fiber Optics Market Size, Share, Trends & Forecast (2026-2034)

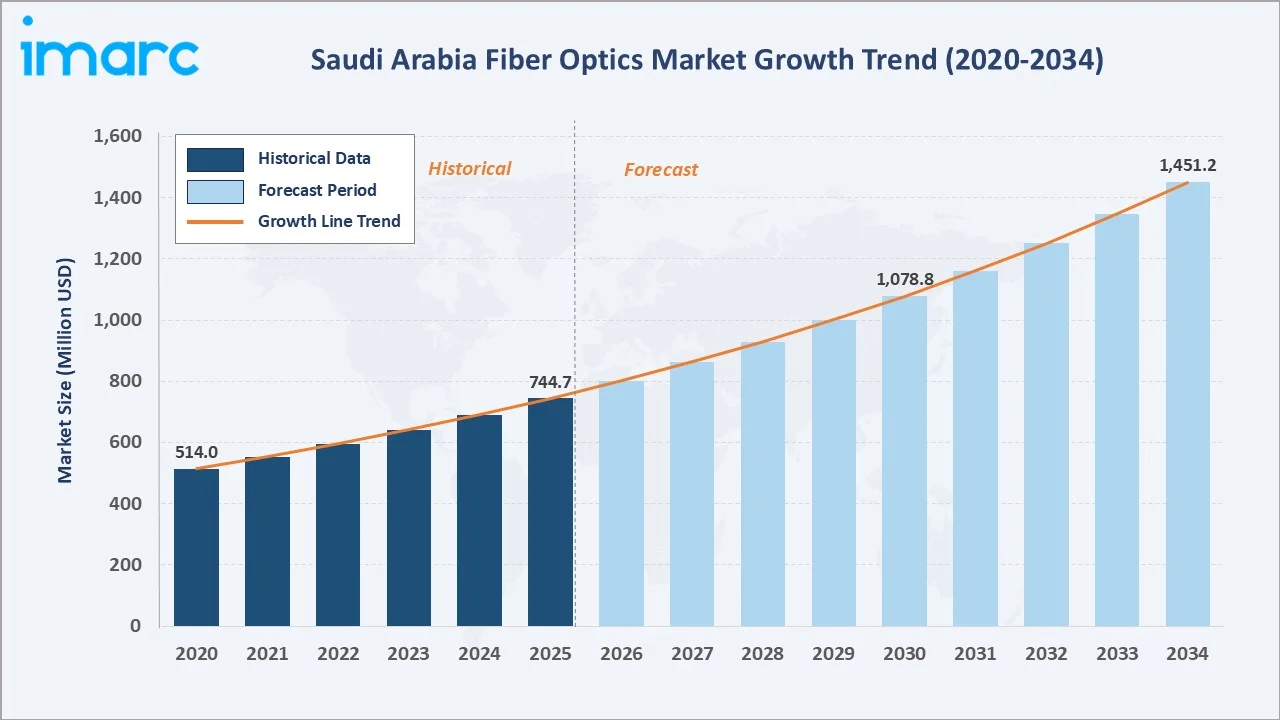

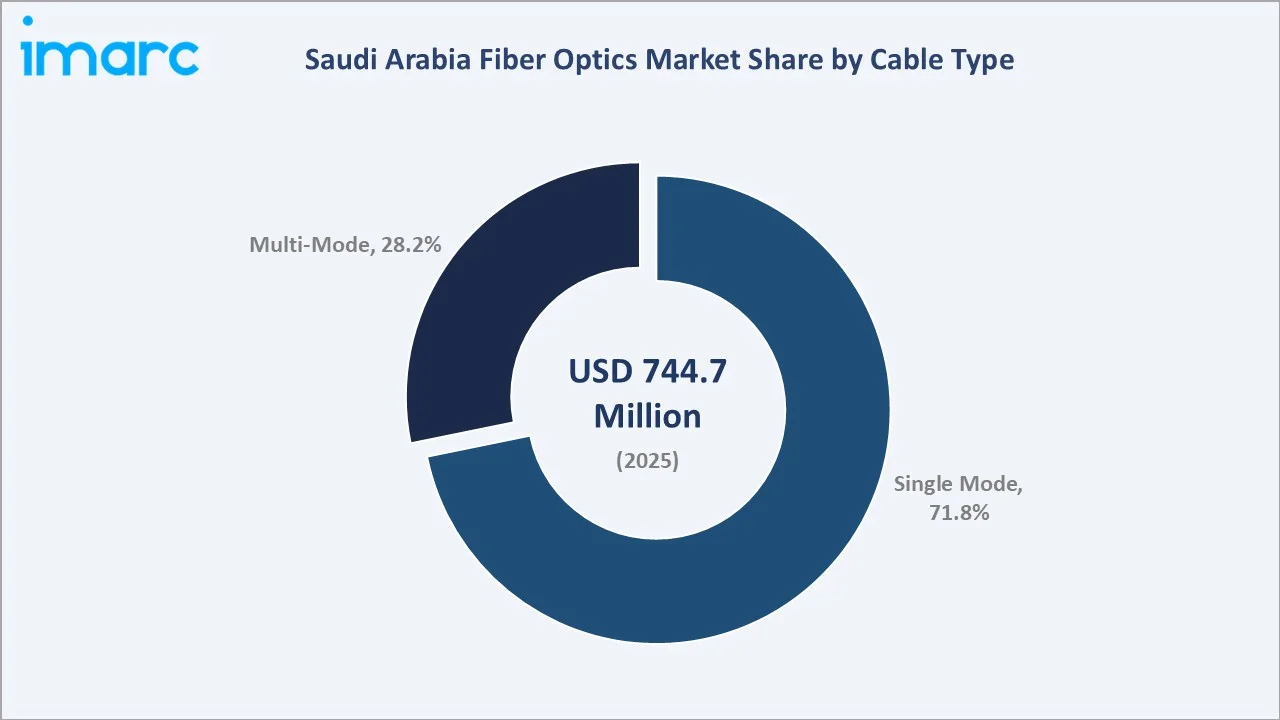

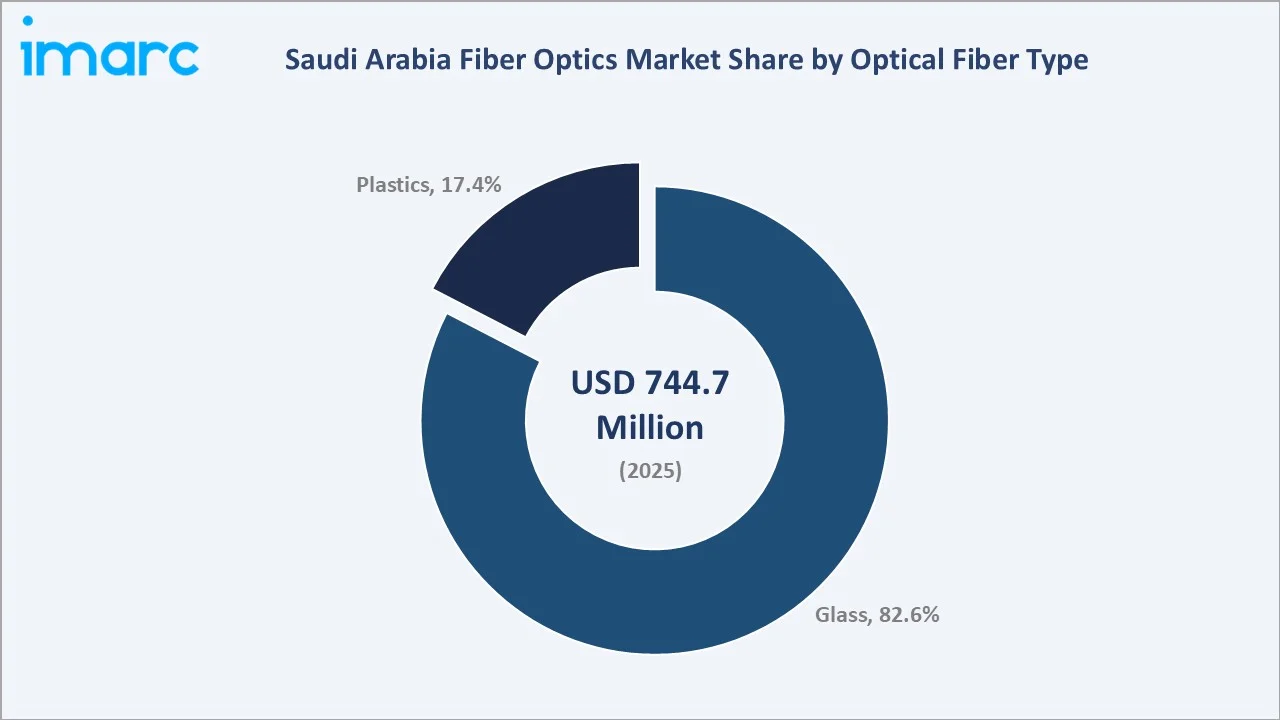

The Saudi Arabia fiber optics market reached USD 744.7 Million in 2025 and is projected to reach USD 1,451.2 Million by 2034, growing at a CAGR of 7.70% during 2026-2034. Growth is driven by high-speed connectivity demand, Vision 2030 digital transformation, and expanding cloud and data center infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 744.7 Million |

|

Forecast Market Size (2034) |

USD 1,451.2 Million |

|

CAGR (2026-2034) |

7.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Cable Type |

Single Mode (71.8%, 2025) |

|

Dominant Optical Fiber Type |

Glass (82.6%, 2025) |

|

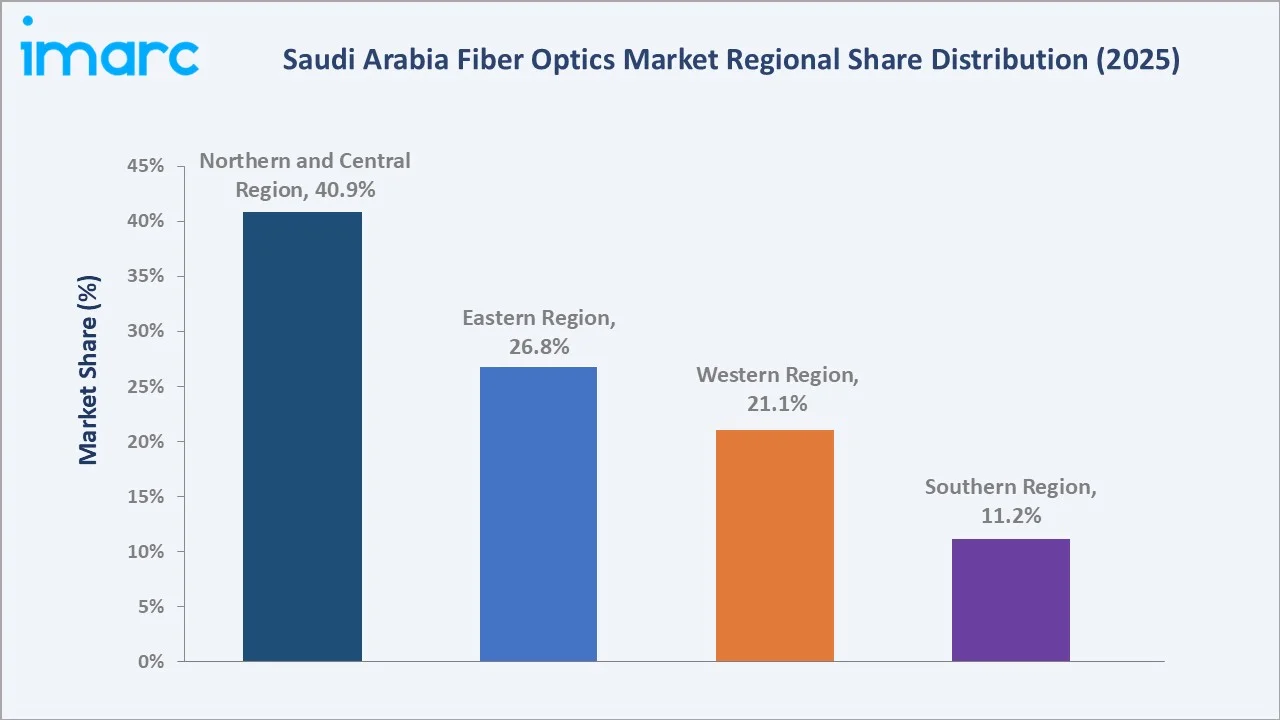

Leading Region |

Northern and Central Region (40.9%, 2025) |

The market expanded from USD 514.0 Million in 2020 to USD 744.7 Million in 2025, anchored at USD 1,078.8 Million by 2030, and is forecast to reach USD 1,451.2 Million by 2034, supported by sustained telecom infrastructure investment and Vision 2030 digital initiatives.

To get more information on this market, Request Sample

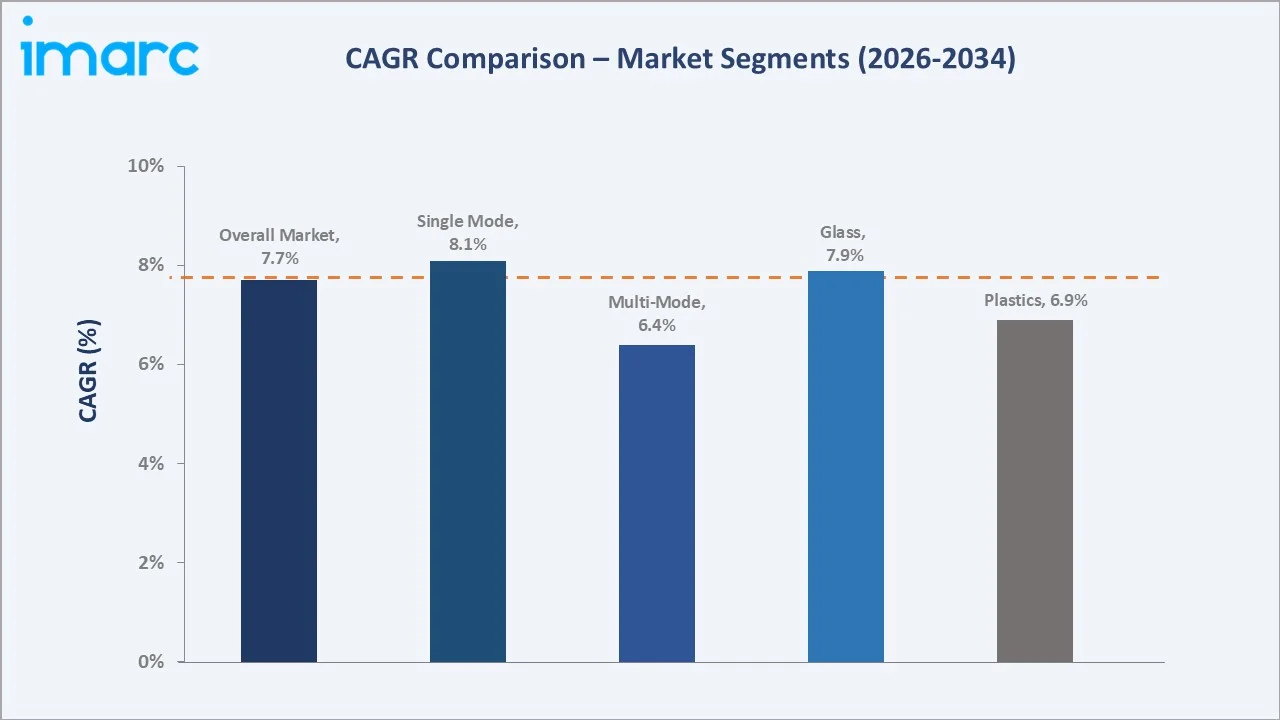

Single Mode cables and glass optical fiber are estimated to grow faster than the overall market, at approximately 8.1% and 7.9% CAGR respectively, as long-haul network expansion and hyperscale data center connectivity continue to favor high-performance fiber technologies through 2034.

Executive Summary

The Saudi Arabia fiber optics market reached USD 744.7 Million in 2025, reflecting sustained investment in national broadband infrastructure aligned with Vision 2030's digital transformation objectives. Fiber networks are increasingly favored over copper systems for their bandwidth, reliability, and energy efficiency.

Single Mode cables lead at 71.8% share through long-haul and metro network deployment, while glass optical fiber dominates at 82.6% owing to superior transmission performance. The Northern and Central Region leads at 40.9%, anchored by Riyadh's telecom infrastructure and data center concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Cable Type |

Single Mode - 71.8% share (2025) |

|

Dominant Optical Fiber Type |

Glass - 82.6% share (2025) |

|

Leading Region |

Northern and Central Region - 40.9% share (2025) |

|

Market Opportunity |

25G PON shared infrastructure; hyperscale data center fiber backbone; terrestrial-satellite network integration |

Key Analytical Observations Supporting The Above Data:

- Single Mode at 71.8%: Dominates due to long-distance, high-bandwidth transmission suited for telecom backbone and metro networks, reinforced by national fiber rollouts such as ACES-NH's 25G PON neutral host network launched in 2025.

- Glass at 82.6%: Leads owing to superior signal transmission, lower attenuation, and durability, making it the preferred choice for telecom, data center, and long-haul network deployments across the Kingdom.

- Northern and Central Region at 40.9%: Leads through Riyadh's concentration of telecom operators, government digital projects, and data center investments supporting Vision 2030 connectivity goals.

Saudi Arabia Fiber Optics Market Overview

The Saudi Arabia fiber optics market encompasses the design, manufacture, and deployment of optical fiber cables used to transmit data as light pulses across telecom, data center, and enterprise networks, offering higher bandwidth and lower signal loss than copper-based systems.

The ecosystem integrates fiber cable manufacturers, optical component suppliers, telecom operators, network integrators, data center operators, and regulatory bodies such as the Communications, Space & Technology Commission (CST) overseeing licensing and infrastructure standards across the Kingdom.

Market Dynamics

To evaluate market opportunities, Request Sample

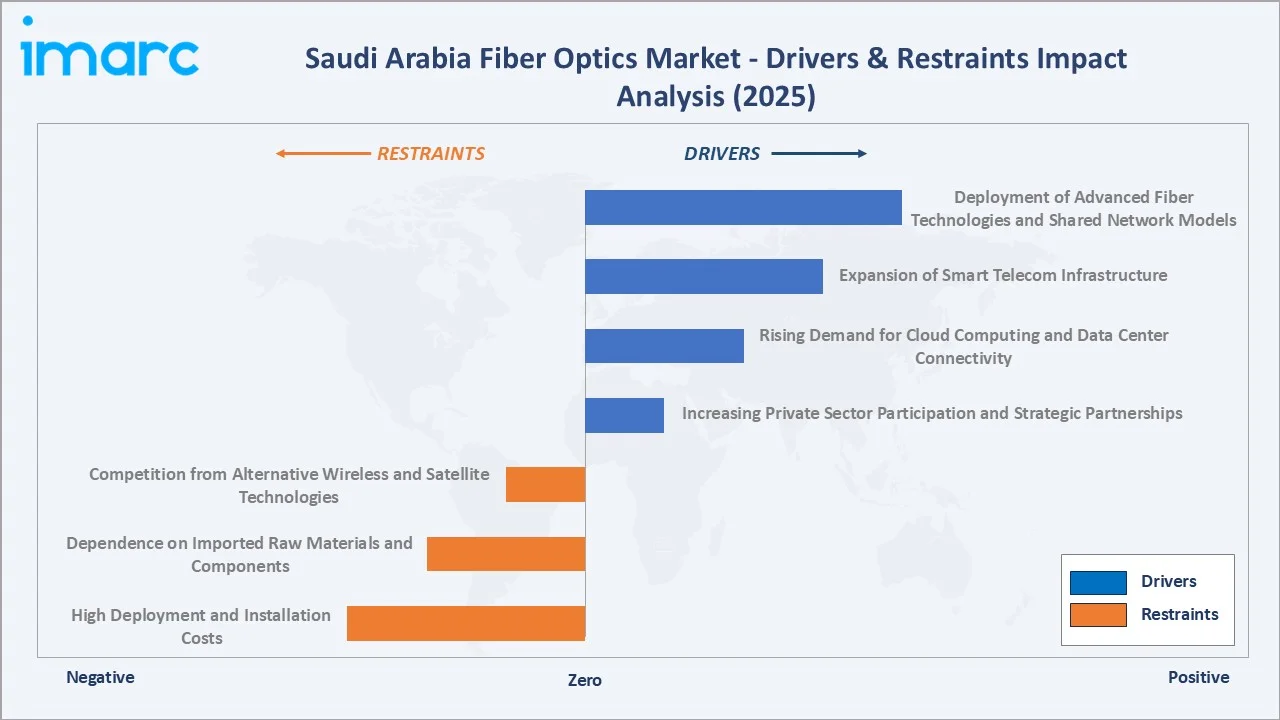

Market Drivers

- Deployment of Advanced Fiber Technologies and Shared Network Models: In February 2025, Nokia enabled Saudi Arabia's first 25G PON-based neutral host network via ACES-NH, allowing multiple operators to share infrastructure for high-capacity, low-latency connectivity, supporting Vision 2030 digital goals. Shared infrastructure models lower per-operator capital expenditure while accelerating nationwide fiber coverage. Wider adoption of such neutral-host models is expected to shorten deployment timelines across both urban and semi-urban markets.

- Expansion of Smart Telecom Infrastructure: The CST announced SR 1 billion in investments and four new licenses at LEAP25 to expand intelligent telecom infrastructure, including fiber-optic and non-terrestrial satellite communication networks. These investments strengthen national broadband resilience and support the Kingdom's transition toward next-generation connectivity standards. Continued regulatory support is expected to further encourage private capital inflows into fiber network expansion.

- Rising Demand for Cloud Computing and Data Center Connectivity: The rapid expansion of cloud computing services, hyperscale data centers, and enterprise digital transformation is driving demand for high-speed, low-latency fiber optic networks across Saudi Arabia. Increasing adoption of artificial intelligence (AI), big data analytics, and cloud-based applications is further accelerating bandwidth requirements, encouraging investments in scalable fiber infrastructure to support reliable data transmission and interconnection.

- Increasing Private Sector Participation and Strategic Partnerships: Growing collaboration between telecommunications operators, infrastructure developers, and private investors is accelerating fiber optic network deployment across the Kingdom. Strategic partnerships are improving project execution, expanding broadband coverage, and supporting the development of next-generation digital infrastructure. These collaborative initiatives are also helping attract investment, enhance operational efficiency, and strengthen nationwide connectivity.

Market Restraints

- High Deployment and Installation Costs: Trenching, right-of-way permissions, and specialized installation equipment raise fiber rollout costs, particularly across remote and low-density areas, limiting nationwide fiber penetration outside major urban centers. Civil works often account for most of the total project expenditure. These cost pressures can delay last-mile connectivity rollouts in lower-density regions.

- Dependence on Imported Raw Materials and Components: Optical fiber cables rely heavily on imported glass fiber, connectors, and specialized manufacturing inputs, exposing the market to global supply chain disruptions and cost fluctuations. Currency movements and international freight costs further add to landed input costs. This dependence also lengthens procurement lead times for large-scale deployment projects.

- Competition from Alternative Wireless and Satellite Technologies: Expanding 5G and low-earth-orbit satellite broadband services offer alternative connectivity options, potentially moderating fiber deployment demand in select remote regions of the Kingdom. Operators may prioritize wireless-first strategies in low-density areas where fiber trenching costs are prohibitive. This can slow the pace of fiber-to-the-home expansion in select geographies.

Market Opportunities

- Hyperscale Data Center Fiber Backbone Expansion: Rising cloud and AI workloads are driving demand for dedicated high-capacity fiber backbones linking hyperscale data centers, creating growth opportunities for fiber infrastructure providers. Operators investing early in scalable backbone capacity are well positioned to capture long-term enterprise contracts. This trend is expected to accelerate as more global cloud providers establish regional data center presence.

- Integration of Terrestrial and Non-Terrestrial Networks: Licensing satellite and terrestrial network integration, as seen with SKYFive Arabia, opens opportunities for fiber providers to support hybrid connectivity architectures. Combined terrestrial-satellite models can extend high-speed connectivity to underserved regions more cost-effectively. This convergence is also creating new service bundling opportunities for telecom operators.

Market Challenges

- Skilled Workforce Shortage in Fiber Installation: Rapid network expansion is outpacing the availability of trained technicians for precision fiber splicing, testing, and maintenance, creating project delays for operators. Training pipelines have not scaled proportionally with deployment volumes. This gap is prompting operators to invest in dedicated technical training academies and certification programs.

- Network Security and Monitoring Complexity: As fiber networks scale, ensuring physical security and real-time threat detection, such as optical sensing against cable tampering, adds operational complexity and cost. Distributed network footprints make continuous monitoring more resource intensive. Operators are increasingly turning to AI-based sensing tools to manage this complexity at scale.

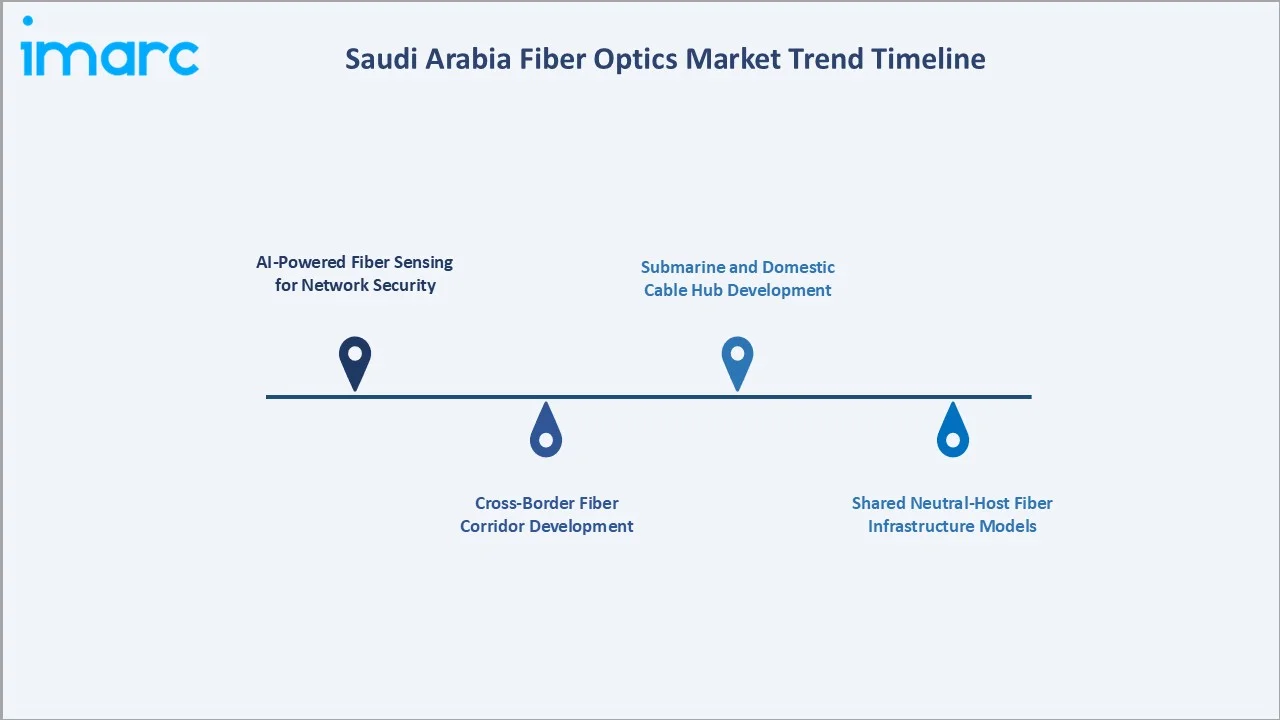

Emerging Market Trends

1. AI-Powered Fiber Sensing for Network Security

Telecom operators are increasingly deploying AI-powered optical fiber sensing solutions to monitor cable integrity and detect physical threats in real time. These systems enhance network security, reduce downtime, and support proactive maintenance across expanding fiber infrastructure.

2. Cross-Border Fiber Corridor Development

Regional telecom operators are developing cross-border terrestrial fiber corridors to strengthen international connectivity and diversify submarine cable access points. Such corridors improve network redundancy and support growing regional data transit demand.

3. Shared Neutral-Host Fiber Infrastructure Models

Neutral-host fiber network models are gaining traction, allowing multiple telecom operators to share infrastructure and reduce redundant capital investment. This approach accelerates nationwide high-speed broadband rollout while lowering deployment costs.

4. Submarine and Domestic Cable Hub Development

Investment in submarine and domestic cable infrastructure is expanding as operators seek to strengthen international connectivity, improve network redundancy, and position the Kingdom as a regional connectivity and data hub.

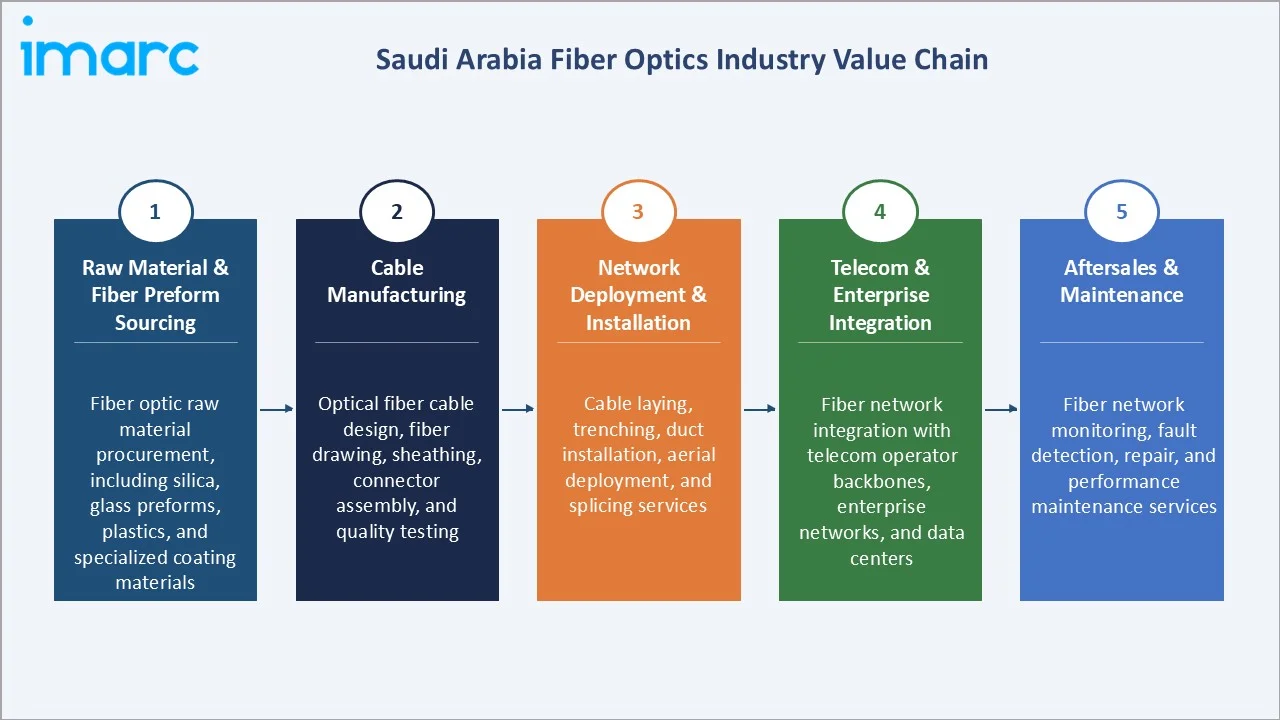

Industry Value Chain Analysis

|

Stage |

Key Participants |

|

Raw Material & Fiber Preform Sourcing |

Fiber optic raw material procurement, including silica, glass preforms, plastics, and specialized coating materials |

|

Cable Manufacturing |

Optical fiber cable design, fiber drawing, sheathing, connector assembly, and quality testing |

|

Network Deployment & Installation |

Cable laying, trenching, duct installation, aerial deployment, and splicing services |

|

Telecom & Enterprise Integration |

Fiber network integration with telecom operator backbones, enterprise networks, and data centers |

|

Aftersales & Maintenance |

Fiber network monitoring, fault detection, repair, and performance maintenance services |

The cable design and manufacturing stage is the value chain's most technically critical tier, while network deployment and installation represent the most labor-intensive segment, given Saudi Arabia's ongoing nationwide fiber rollout under Vision 2030.

Technology Landscape in the Saudi Arabia Fiber Optics Industry

Single Mode Fiber Technology

Single mode fiber technology transmits light through a narrow core, enabling long-distance, high-bandwidth data transmission with minimal signal loss, making it the preferred choice for telecom backbone, metro, and long-haul network deployments.

Multi-Mode Fiber Technology

Multi-mode fiber technology supports shorter-distance, high-bandwidth applications such as data center interconnects and enterprise local area networks, with lower-cost transceivers suited for short-reach, high-density connectivity.

Glass vs Plastic Optical Fiber Technology

Glass optical fiber offers superior transmission distance, lower attenuation, and durability, making it the dominant telecom choice. Plastic optical fiber, though limited in range, offers cost-effective, flexible solutions for short-distance applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Cable Type |

Single Mode |

71.8% |

2025 |

|

Optical Fiber Type |

Glass |

82.6% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Northern and Central Region |

40.9% |

2025 |

By Cable Type

Single Mode cables lead at 71.8% in 2025, driven by their suitability for long-haul, metro, and backbone network deployment across the Kingdom's expanding telecom infrastructure.

To access detailed market analysis, Request Sample

Multi-Mode cables account for the remaining 28.2%, primarily serving data center interconnects and shorter-distance enterprise network applications requiring simplified, cost-effective connectivity.

By Optical Fiber Type

Glass optical fiber leads at 82.6% in 2025, reflecting its dominance across telecom, data center, and long-haul network applications due to superior transmission performance and durability.

Plastic optical fiber holds 17.4% share, serving shorter-distance, cost-sensitive applications including industrial automation and select in-building connectivity use cases.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

Northern and Central Region |

40.9% |

Driven by concentrated telecom infrastructure, strong government digital initiatives, and expanding data center investments |

|

Eastern Region |

26.8% |

Supported by industrial connectivity demand, growing enterprise networks, and expanding broadband infrastructure |

|

Western Region |

21.1% |

Reflects strong commercial and tourism-linked telecom demand, along with expanding port and logistics digitalization |

|

Southern Region |

11.2% |

Driven by emerging connectivity initiatives and growing digital inclusion programs across the region |

The Northern and Central Region, at 40.9%, leads through concentrated telecom infrastructure and government digital initiatives. The Eastern Region, at 26.8%, benefits from industrial connectivity demand, while the Western Region, at 21.1%, reflects strong commercial and tourism-linked telecom demand.

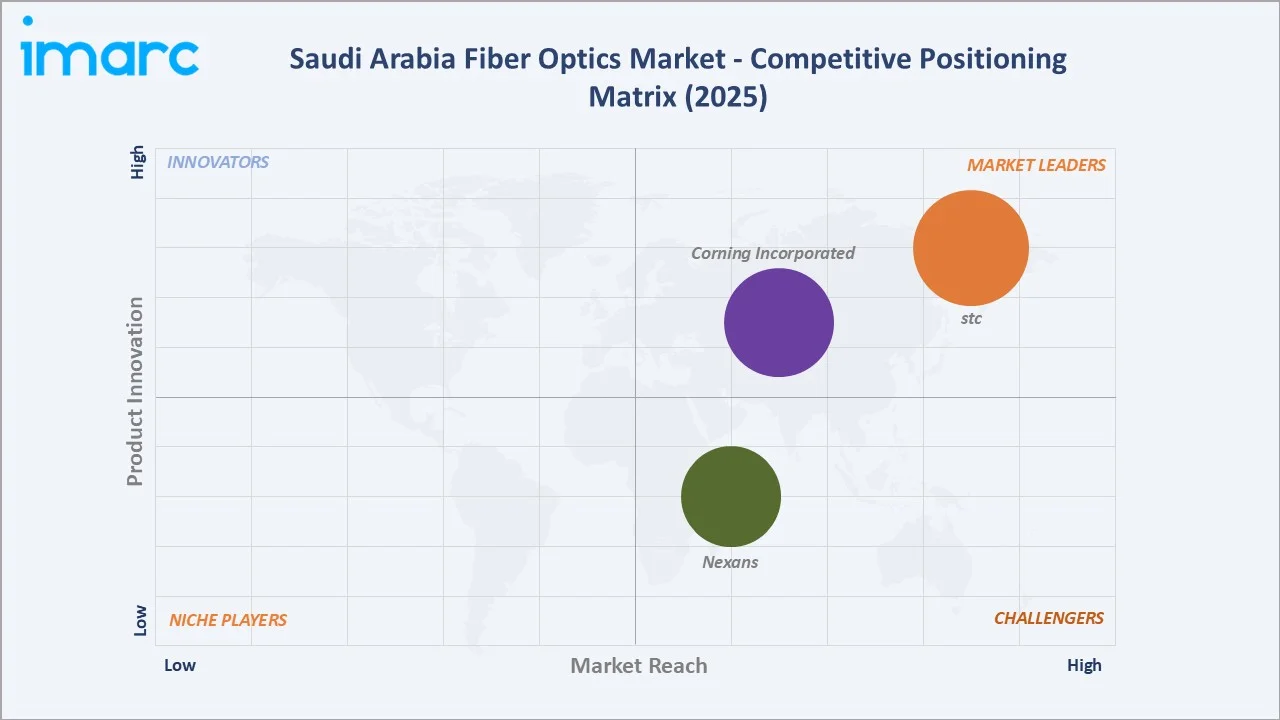

Competitive Landscape

The Saudi Arabia fiber optics market competitive landscape includes global fiber cable manufacturers, telecom operators, and infrastructure contractors. Competition is shaped by technology partnerships, network deployment contracts, and Vision 2030-aligned infrastructure investment programs.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Corning Incorporated |

Optical Fiber Cable, SMF-28 Fiber |

Market Leader |

Corning specializes in advanced optical fiber and cable manufacturing with global telecom deployment expertise. |

|

Nexans |

Optical Fiber Cables, LAN Cabling Systems |

Strong Challenger |

Nexans specializes in cabling systems for telecom, data center, and industrial network applications. |

|

stc |

Fiber Broadband Networks |

Market Leader |

stc leads national fiber broadband deployment and digital infrastructure investment across Saudi Arabia. |

Key players include Corning Incorporated, Nexans, stc, and others.

Key Company Profiles

Corning Incorporated

Corning Incorporated is a US-based global manufacturer of optical fiber and cable, with a strong presence supplying telecom operators and network integrators across Saudi Arabia's fiber optics market.

- Key Products: Optical Fiber Cable, SMF-28 Fiber.

- Strategic Focus: Expanding advanced single-mode fiber production and supporting hyperscale data center and telecom backbone connectivity globally.

Nexans

Nexans is a France-based cabling and connectivity solutions provider supplying optical fiber cables for telecom, data center, and industrial network applications, including projects across the Middle East.

- Key Products: Optical Fiber Cables, LAN Cabling Systems.

- Strategic Focus: Expanding optical fiber cabling systems for telecom, enterprise, and data center connectivity applications across emerging markets.

Market Concentration Analysis

The Saudi Arabia fiber optics market is moderately concentrated, with global cable manufacturers supplying fiber cables alongside domestic telecom operators and infrastructure contractors executing deployment programs.

Investment & Growth Opportunities

Highest Growth Segments

Single Mode cable deployment, glass optical fiber production, hyperscale data center connectivity, and shared neutral-host fiber infrastructure represent the highest-growth investment vectors through 2034, supported by Vision 2030 digital transformation programs.

Emerging Investment Opportunities

Fiber network deployment services represent a high-value emerging opportunity, as nationwide broadband expansion and data center connectivity projects create sustained demand for installation, testing, and maintenance service providers.

Investment Themes

- Shared neutral-host fiber infrastructure investment, reducing redundant capital deployment while accelerating nationwide high-speed broadband coverage across underserved regions.

- Hyperscale data center fiber backbone investment, capturing rising demand from cloud computing, AI workloads, and enterprise digital transformation initiatives across Saudi Arabia.

Future Market Outlook (2026-2034)

The Saudi Arabia fiber optics market is projected to grow from USD 744.7 Million in 2025 to USD 1,451.2 Million by 2034, delivering a 7.70% CAGR, anchored by continued Vision 2030 digital infrastructure investment and expanding data center connectivity.

Single Mode and glass fiber technologies are expected to retain dominance, while shared neutral-host infrastructure and terrestrial-satellite network integration gain wider adoption, supporting the Kingdom's long-term digital transformation and connectivity resilience goals.

Research Methodology

Primary Research

Primary research comprised structured interviews with industry stakeholders, including telecom network engineers, fiber cable manufacturers, infrastructure contractors, and government digital transformation programme representatives across Saudi Arabia.

Secondary Research

Secondary research encompassed company reports, Communications, Space & Technology Commission (CST) publications, Vision 2030 digital infrastructure disclosures, telecom operator announcements, and industry news coverage of fiber network deployment projects.

Forecasting Models

Market revenue forecasts were developed using a bottom-up approach incorporating fiber network deployment volumes, cable type and optical fiber type revenue mix, and regional infrastructure investment trends across the forecast period.

Saudi Arabia Fiber Optics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Cable Types Covered | Single Mode, Multi-Mode |

| Optical Fiber Types Covered | Glass, Plastics |

| Applications Covered | Telecom, Oil and Gas, Military and Aerospace, BFSI, Medical, Railway, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Corning Incorporated, Nexans, stc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia fiber optics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia fiber optics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia fiber optics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Fiber Optics Market Report

The market reached USD 744.7 Million in 2025, driven by Single Mode cable dominance at 71.8%, glass optical fiber leading at 82.6%, and the Northern and Central Region commanding 40.9% share.

The market is projected to grow at a 7.70% CAGR during 2026-2034, reaching USD 1,451.2 Million by 2034, supported by Vision 2030 digital transformation and data center connectivity growth.

Single Mode cables lead at 71.8% share in 2025, driven by their suitability for long-haul, metro, and telecom backbone network deployment across the Kingdom.

Glass optical fiber leads at 82.6% share in 2025, owing to superior transmission performance, lower signal loss, and durability compared to plastic optical fiber.

The Northern and Central Region leads at 40.9%, driven by Riyadh's telecom infrastructure concentration and government digital transformation initiatives.

Leading companies include Corning Incorporated, Nexans, stc, and others.

The market is projected to reach approximately USD 1,078.8 Million by 2030, supported by expanding shared neutral-host infrastructure and hyperscale data center connectivity demand.

Priority opportunities include shared neutral-host fiber infrastructure, hyperscale data center fiber backbone expansion, and fiber network deployment and maintenance services across the Kingdom.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)