Saudi Arabia Forklift Market Size, Share, Trends and Forecast by Class, Power Source, Load Capacity, Electric Battery, End User, and Region, 2026-2034

Saudi Arabia Forklift Market Summary:

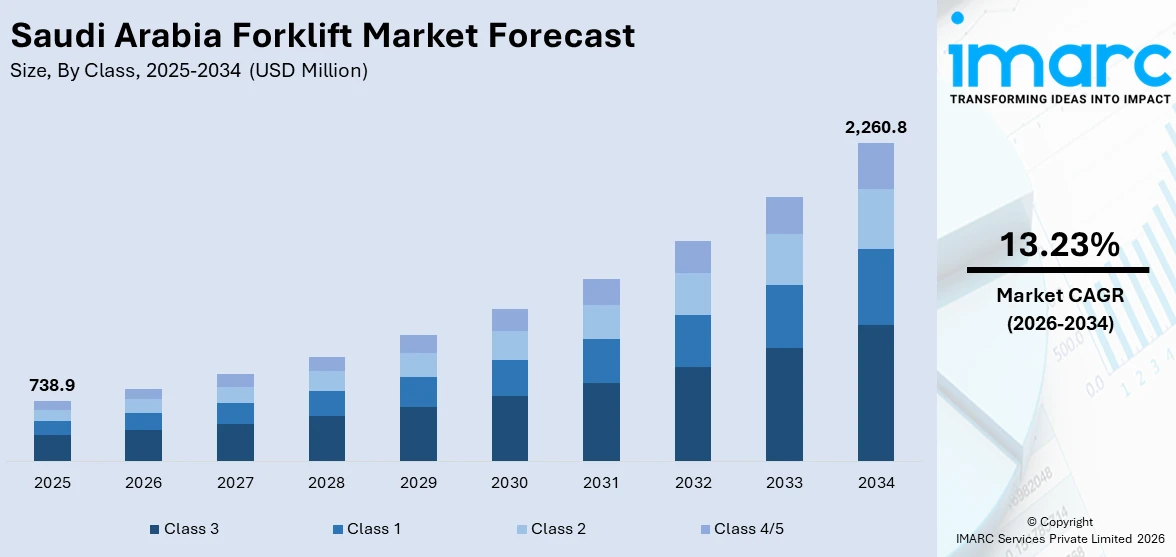

The Saudi Arabia forklift market size was valued at USD 738.9 Million in 2025 and is projected to reach USD 2,260.8 Million by 2034, growing at a compound annual growth rate of 13.23% from 2026-2034.

Saudi Arabia's market is experiencing robust expansion driven by the Kingdom's ambitious Vision 2030 economic diversification program, which prioritizes logistics infrastructure development and industrial growth beyond the oil sector. The National Industrial Development and Logistics Program has catalyzed massive investments in warehouse facilities, ports, and distribution networks, creating sustained demand for material handling equipment. Rising e-commerce penetration and the establishment of specialized logistics zones are further accelerating the shift toward electric and automated forklift systems, thereby expanding the Saudi Arabia forklift market share.

Key Takeaways and Insights:

- By Classes: Class 3 dominates the market with a share of 32% in 2025, driven by electrichand forklift trucks' versatility in warehouse operations.

- By Power Sources: Electric leads the market with a share of 55% in 2025, reflecting the Kingdom's commitment to sustainability and reduced operational costs.

- By Load Capacity: Below 5 ton represents the largest segment with a market share of 40% in 2025, addressing the broad spectrum of material handling requirements across warehouse operations, retail distribution centers, and light manufacturing facilities.

- By Electric Battery: Li-ion holds a market share of 58% in 2025, benefiting from superior energy density and faster charging capabilities.

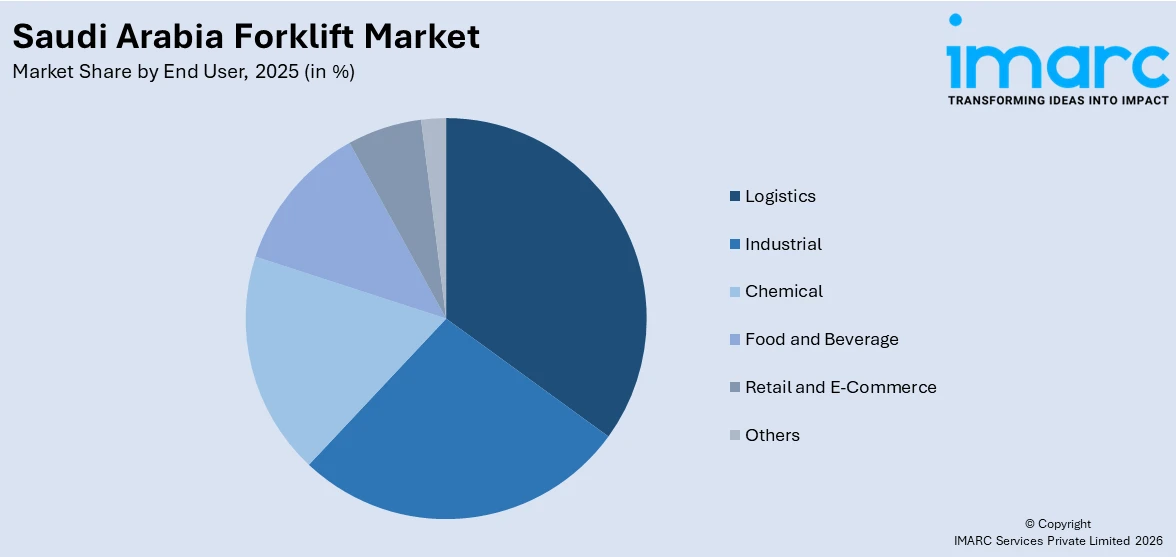

- By End User: Logistics accounts for 29% market share in 2025, driven by rapid e-commerce growth and expanding warehouse infrastructure.

- By Region: Northern and central region represents 30% in 2025, anchored by Riyadh's role as the Kingdom's logistics and e-commerce gateway.

- Key Players: Key players in Saudi Arabia’s forklift market are expanding service networks, improving after-sales support, and introducing more electric and automated models. They are also partnering with logistics firms to reduce downtime, enhance safety, and align with sustainability and efficiency goals.

To get more information on this market Request Sample

The Saudi Arabia forklift market is at a point of significant transformation, driven by unprecedented government-backed industrialization and logistics development. The infrastructure development plans under Vision 2030 have opened up multi-billion dollar opportunities in the petrochemical plants, mega city development projects such as NEOM, and the development of King Abdulaziz Port and King Fahd Industrial Port. In 2024, The Zakat, Tax, and Customs Authority (ZATCA), in collaboration with the National Center for Privatization & PPP (NCP), has announced the launch of the Expression of Interest (EOI) and Request for Qualification (RFQ) phase for the Development and Operations of Customs Warehouses Project at 38 Points of Entry (PoEs) across the Kingdom of Saudi Arabia. The contract for the project will be based on the Design-Build-Finance-Maintain-Operate-Transfer (DBFMOT) model, which will last for 15 years and will include the construction phase. The project includes the design, construction, and maintenance of 13 warehouses, 12 new ones and the renovation of one existing warehouse. The operation phase will include all new and existing warehouses over 38 PoEs. This will cover the loading and unloading of goods into the warehouses, the use of forklifts, cranes, and trucks, as well as providing cleaning services. This project is a clear example of how the government's strategic plans are being directly translated into creating a demand for advanced material handling equipment in the Kingdom's dynamic industrial sector.

Saudi Arabia Forklift Market Trends:

Accelerated Adoption of Electric Forklift Technology

The electric forklift industry has seen an explosive growth rate in Saudi Arabia, because of the government's proposed incentives for companies to move from using internal combustion engines to using electrically-powered equipment. This aligns with the sustainability vision of the Kingdom of Saudi Arabia as seen in its Vision 2030 initiative. The electric forklift has gained dominance in the warehouse and distribution center environment, particularly in temperature-sensitive operations such as refrigeration where strict guidelines are enforced. A recent example of the impact of this shift to electric on logistics infrastructure development was demonstrated when OMODA & JAECOO Automobile Co., Ltd. opened its first designated spare parts distribution center in Dammam, Saudi Arabia in July 2024 which is expected to have the ability to deliver original spare parts to customers’ nearest location within 24 – 48 hours and utilizes battery-powered material handling equipment throughout the facility.

Integration of Automation and Smart Technologies

Forklift operations in Saudi Arabia are increasingly incorporating artificial intelligence, Internet of Things sensors, and autonomous navigation systems to optimize warehouse efficiency and reduce dependence on skilled labor. Companies are deploying intelligent fleet management platforms that enable real-time tracking, predictive maintenance scheduling, and data-driven capacity planning across multiple facilities. This technological evolution responds to both the Kingdom's push for Industry 4.0 adoption and practical challenges related to operator availability in a rapidly expanding market. Advanced electric forklift models tailored specifically for the Middle Eastern climate and operational requirements were launched, featuring enhanced battery cooling systems and smart diagnostics. The integration of GPS and telematics capabilities provides logistics operators with unprecedented visibility into fleet utilization patterns, enabling continuous optimization of material handling processes across Saudi Arabia's extensive warehouse networks. IMARC Group predicts that Saudi Arabia commercial telematics market is projected to attain USD 2,839.3 Million by 2034.

Expansion of Logistics Infrastructure Supporting Vision 2030

Saudi Arabia's logistics sector is undergoing comprehensive transformation through systematic development of specialized zones, ports, and multimodal transport networks that directly drive forklift demand. The government has allocated SAR 40 billion for road development while targeting expansion of port throughput capacity. In 2024, Gulf Warehousing Company Q.P.S.C announced that its subsidiary GWC Energy Services partnered with Saudi Offshore Fabrication Company to develop 100,000 square meters of Grade 'A' logistics facilities at Ras Al-Khair Industrial Port, representing the scale of infrastructure investments creating sustained material handling equipment requirements. These mega-projects span the Eastern Province's petrochemical hub, the Western Province's Red Sea ports, and Riyadh's Special Integrated Logistic Zone, which waives duties on imported parts and positions the capital as a strategic e-commerce gateway requiring extensive warehouse automation and material handling capacity.

How Vision 2030 is Transforming the Saudi Arabia Forklift Market:

Saudi Vision 2030 is playing a major role in transforming the forklift market by accelerating industrial growth, infrastructure development, and logistics expansion across the country. Large-scale projects, including new economic cities, industrial zones, and giga developments, are increasing demand for material handling equipment in construction, manufacturing, and warehousing. Vision 2030’s focus on making Saudi Arabia a regional logistics hub is driving investments in ports, airports, and distribution centers, where forklifts are essential for efficient cargo movement. The rise of e-commerce and supply chain modernization is also boosting the need for advanced warehouse equipment. In addition, sustainability goals under Vision 2030 are encouraging a shift toward electric forklifts and energy-efficient solutions to reduce emissions. Companies are also adopting smart fleet management and automation technologies to improve productivity. Overall, Vision 2030 is creating strong long-term opportunities for forklift market growth.

Market Outlook 2026-2034:

Saudi Arabia's forklift market is positioned for sustained double-digit growth as Vision 2030 initiatives enter their implementation peak, with major infrastructure projects transitioning from planning to active construction and operational phases. The market generated a revenue of USD 738.9 Million in 2025 and is projected to reach a revenue of USD 2,260.8 Million by 2034, growing at a compound annual growth rate of 13.23% from 2026-2034. The convergence of rising e-commerce penetration, expanding petrochemical production capacity, and the Kingdom's strategic positioning as a global logistics hub creates multi-layered demand drivers across industrial and commercial sectors. Electric forklift adoption will accelerate beyond current levels as lithium-ion battery costs continue declining and charging infrastructure becomes ubiquitous across Saudi Arabia's expanding warehouse networks.

Saudi Arabia Forklift Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Class |

Class 3 |

32% |

|

Power Source |

Electric |

55% |

|

Load Capacity |

Below 5 Ton |

40% |

|

Electric Battery |

Li-ion |

58% |

|

End User |

Logistics |

29% |

|

Region |

Northern and Central Region |

30% |

Class Insights:

- Class 1

- Class 2

- Class 3

- Class 4/5

Class 3 dominates with a market share of 32% of the total Saudi Arabia forklift market in 2025.

Class 3 electric hand forklift trucks have established commanding market leadership through their optimal balance of maneuverability, operational efficiency, and zero-emission performance in warehouse environments. These battery-powered units excel in high-density storage facilities where aisle widths are constrained and indoor air quality regulations necessitate emission-free operation. Their compact design enables navigation through narrow corridors while maintaining substantial load-carrying capacity, making them indispensable for order picking, inventory replenishment, and cross-docking activities across Saudi Arabia's expanding logistics infrastructure.

The sustained preference for Class 3 forklifts reflects broader market maturation as Saudi companies prioritize total cost of ownership over initial capital expenditure. Electric hand trucks deliver significantly lower maintenance requirements compared to internal combustion alternatives, eliminate fuel costs entirely, and operate with minimal noise, critical advantages in facilities running extended shifts or 24/7 operations. Saudi Arabia's Vision 2030 emphasis on environmental sustainability has accelerated adoption curves, with government procurement increasingly specifying electric models for logistics and warehousing applications. The segment benefits from continuous technological enhancements including lithium-ion battery integration, regenerative braking systems, and smart fleet management capabilities that optimize charging schedules and extend operational uptime across multi-shift deployments throughout the Kingdom's diverse industrial sectors.

Power Source Insights:

- ICE

- Electric

Electric leads with a share of 55% of the total Saudi Arabia forklift market in 2025.

Electric forklifts have captured market dominance through compelling advantages in operational cost efficiency, environmental compliance, and alignment with Saudi Arabia's sustainability commitments under Vision 2030. Battery-powered units eliminate recurring fuel expenditures while delivering substantially reduced maintenance requirements compared to internal combustion alternatives, creating favorable total cost of ownership economics over multi-year deployment periods. Their zero-emission operation proves essential for indoor warehousing, cold storage, and food processing facilities where air quality regulations and worker safety standards prohibit combustion engine usage.

The electric segment's growth trajectory extends beyond existing market leadership as lithium-ion battery technology continues advancing in energy density, charging speed, and operational lifespan. Modern electric forklifts equipped with fast-charging capabilities and opportunity charging systems minimize downtime previously associated with battery swapping or extended recharging periods, enabling continuous multi-shift operations matching internal combustion performance benchmarks. Saudi Arabia's expanding renewable energy capacity, including massive solar installations at projects like NEOM, creates synergies with electric forklift deployment by providing clean electricity sources that reinforce sustainability credentials throughout the logistics value chain. The convergence of improving battery economics, supportive government policies, and operational advantages positions electric forklifts to further expand market share as Saudi Arabia's industrial and logistics sectors scale their material handling capacity.

Load Capacity Insights:

- Below 5 Ton

- 5-15 Ton

- Above 16 Ton

Below 5 ton exhibits a clear dominance with a 40% share of the total Saudi Arabia forklift market in 2025.

The below 5-ton capacity segment dominates the Saudi Arabian market by. These versatile units handle standard pallet loads, packaged goods, and containerized materials that represent the majority of logistics activities in e-commerce fulfilment, FMCG distribution, and general warehousing operations. Their relatively compact dimensions enable operation in facilities with standard ceiling heights and aisle configurations, making them suitable for the diverse warehouse infrastructure being developed across Saudi Arabia's expanding logistics zones.

Below 5-ton forklifts benefit from advantageous economics including lower initial capital costs, reduced operational expenses, and broader operator skill requirements compared to larger capacity units, facilitating widespread adoption by companies scaling their logistics capabilities. Electric models in this capacity range deliver particularly compelling value propositions through minimal maintenance needs and zero fuel costs, aligning with cost-conscious deployment strategies prevalent among Saudi Arabia's growing small and medium enterprise logistics sector.

Electric Battery Insights:

- Li-ion

- Lead Acid

Li-ion leads with a share of 58% of the total Saudi Arabia forklift market in 2025.

Lithium-ion battery technology has achieved market leadership in Saudi Arabia's electric forklift segment through compelling advantages in performance, operational efficiency, and total cost of ownership over multi-year deployment periods. Li-ion systems deliver substantially higher energy density compared to traditional lead-acid alternatives, enabling longer operational runtime between charges while occupying less physical space and reducing overall vehicle weight. This translates directly into enhanced productivity through extended shift capabilities and faster opportunity charging during break periods, eliminating the downtime and infrastructure requirements associated with battery swapping or prolonged recharging cycles.

Saudi Arabia's harsh climate conditions further favor lithium-ion adoption, as these batteries demonstrate superior temperature tolerance and consistent performance across the Kingdom's extreme heat variations without the accelerated degradation patterns that compromise lead-acid battery lifespan in regional operating environments. The economic calculus increasingly favors lithium-ion despite higher upfront costs, as companies recognize the substantial lifecycle savings from reduced maintenance requirements, extended useful life spanning thousands of charge cycles, and improved energy efficiency that lowers electricity consumption per operational hour. Saudi Arabia's rapid industrial expansion has attracted global battery manufacturers and technology providers establishing regional supply chains, progressively reducing lithium-ion cost premiums while improving local technical support infrastructure.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Industrial

- Logistics

- Chemical

- Food and Beverage

- Retail and E-Commerce

- Others

Logistics exhibits a clear dominance with a 29% share of the total Saudi Arabia forklift market in 2025.

Logistics is one of the largest end-user segments driving demand in the Saudi Arabia forklift market. Growth in warehousing, distribution centers, and freight handling is increasing the need for efficient material movement across supply chains. Forklifts are widely used in ports, airports, and large logistics hubs to support loading, unloading, and pallet handling operations. The expansion of e-commerce and retail distribution has further increased the requirement for modern warehouse equipment, as companies focus on faster delivery timelines and higher inventory turnover. Logistics operators are also investing in forklifts with higher lifting capacities and better maneuverability to manage diverse cargo types, ranging from consumer goods to industrial materials. Demand is especially strong in regions with major infrastructure projects and industrial zones, where logistics activity is expanding rapidly.

The segment is also seeing a shift toward advanced and sustainable forklift solutions. Many logistics providers are adopting electric forklifts to reduce emissions and comply with cleaner operational practices, particularly in indoor warehouse environments. Automation is becoming an important trend, with increased interest in smart forklifts equipped with telematics, fleet management systems, and safety-enhancing technologies. These features help logistics companies monitor equipment performance, reduce downtime, and optimize fleet utilization. With Saudi Arabia strengthening its role as a regional trade and logistics hub under Vision 2030, investments in transport infrastructure and supply chain modernization are expected to sustain long-term forklift demand in the logistics sector.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

Northern and central region leads with a share of 30% of the total Saudi Arabia forklift market in 2025.

The Northern and Central Region's market leadership stems from Riyadh's role as the Kingdom's political capital, largest consumer market, and emerging logistics hub benefiting from Vision 2030's Special Integrated Logistic Zone designation. The capital city concentrates extensive warehouse development, distribution infrastructure, and e-commerce fulfillment operations serving Saudi Arabia's densest population center and surrounding regions. Riyadh's strategic positioning enables efficient distribution to all corners of the Kingdom while its economic diversification initiatives have attracted substantial foreign direct investment in logistics infrastructure, manufacturing facilities, and commercial developments requiring comprehensive material handling capabilities. The region's forklift demand encompasses diverse applications across government procurement, private sector logistics operations, and construction projects supporting the capital's ongoing expansion.

Beyond Riyadh's dominance, the Northern and Central Region includes developing industrial zones and planned mega-cities that will generate additional material handling equipment requirements throughout the forecast period. The region benefits from superior road connectivity, established supply chains for forklift maintenance and parts distribution, and concentration of skilled operators and technical personnel supporting equipment utilization. Government initiatives including the National Housing Program and extensive infrastructure modernization projects create sustained construction-related demand complementing the region's logistics sector growth. The convergence of population density, economic activity concentration, and strategic infrastructure investments ensures the Northern and Central Region's continued leadership in Saudi Arabia's forklift market as the Kingdom implements its ambitious economic transformation agenda.

Market Dynamics:

Growth Drivers:

Why is the Saudi Arabia Forklift Market Growing?

Vision 2030 Infrastructure Development and National Industrial Development and Logistics Program

Saudi Arabia's comprehensive Vision 2030 economic diversification initiative has unleashed unprecedented infrastructure investment that directly drives sustained forklift demand across industrial, logistics, and construction sectors. The National Industrial Development and Logistics Program targets positioning the Kingdom as a global logistics hub through systematic development of specialized zones, port expansions, and multimodal transport networks requiring extensive material handling equipment deployments. The program has catalyzed SR 240 billion (USD 63.95 billion) worth of projects offered to the private sector, spanning privatized ports, airports, and cargo terminals that necessitate sophisticated forklift infrastructure. In March 2025, The Saudi Ports Authority (Mawani), in partnership with DP World, launched a USD 800 million expansion of the South Container Terminal at Jeddah Islamic Port to enhance operational capabilities and increase its capacity from 1.8 million to 4 million TEUs, exemplifying mega-scale port developments that generate massive material handling equipment requirements across operational commissioning and sustained cargo handling activities.

E-Commerce Expansion and Warehouse Infrastructure Development

Saudi Arabia's e-commerce sector is experiencing exponential growth, creating unprecedented demand for automated warehouse facilities equipped with efficient material handling systems. This digital commerce revolution necessitates rapid expansion of fulfillment center capacity across major population centers to meet consumer expectations for rapid delivery while maintaining inventory accuracy and operational efficiency. The Kingdom processed 101 million delivery orders in Q2 2025 alone, with Riyadh accounting for 45% of volume, demonstrating the scale of logistics infrastructure required to support sustained e-commerce penetration. Companies are establishing distributed warehouse networks equipped with electric forklifts, automated storage systems, and smart inventory management platforms to optimize last-mile delivery capabilities throughout Saudi Arabia's increasingly connected consumer market.

Transition to Sustainable and Electric Forklift Technology

Saudi Arabia's commitment to achieving net-zero carbon emissions by 2060 has accelerated the shift from internal combustion engines to electric forklift systems, creating both replacement demand from existing fleets and greenfield adoption in new facilities designed for sustainable operations from inception. Government incentives announced for companies adopting electric and automated material handling equipment provide direct financial support for technology transition while aligning with broader environmental objectives under Vision 2030. Saudi Arabia's expanding renewable energy capacity, including massive solar installations at projects like NEOM, creates additional synergies with electric forklift deployment by providing clean electricity sources that reinforce sustainability credentials throughout industrial operations, positioning the Kingdom as a regional leader in green logistics infrastructure as companies systematically transition their material handling fleets. IMARC Group predicts that the Saudi Arabia renewable energy market is projected to attain 40.8 Gigawatt by 2034.

Market Restraints:

What Challenges the Saudi Arabia Forklift Market is Facing?

Skilled Operator Shortage and Saudization Policy Implementation

The Saudization policy's 2025 updates create skilled operator shortages that constrain forklift market expansion, as companies struggle to meet mandatory Saudi national employment quotas while maintaining operational efficiency. Saudi Arabia faces a projected skilled worker shortage of 663,000 by 2030, potentially leading to USD 206.77 billion in unrealized revenue across construction and industrial sectors. The Nitaqat classification system's increased stringency affects equipment rental and operations companies' costs, as higher Saudi national employment requirements increase labor expenses. Skills gaps between available candidates and job requirements persist, particularly in technical specializations requiring hands-on equipment operation experience and safety certification maintenance.

High Initial Investment Costs for Electric Forklift Technology

Despite favorable lifecycle economics, the higher upfront capital costs of electric forklifts and particularly lithium-ion battery systems create adoption barriers for small and medium enterprises and companies operating under capital expenditure constraints. Electric forklift acquisition costs can exceed internal combustion alternatives by 30 to 50%, with premium lithium-ion battery packs requiring substantial initial investments that strain budgets for companies establishing new operations or expanding existing fleets. While operational savings eventually offset these premiums, the immediate cash flow impact influences purchasing decisions, particularly among cost-sensitive operators.

Rising Construction and Operational Costs

Construction costs in Saudi Arabia rose between 3.4% and 4.2% in 2024, with mega-projects like NEOM and Qiddiya driving up expenses through heavy demand for skilled labor, building materials, and specialized services. The ongoing Red Sea crisis has significantly disrupted maritime supply chains, leading to increases in building material costs that affect forklift deployment timelines and project economics. Oil price volatility creates periodic investment timing uncertainties that affect capital equipment procurement decisions across industrial and logistics sectors dependent on stable commodity revenues for expansion financing.

Competitive Landscape:

Key market players in the Saudi Arabia forklift market are focusing on expanding their dealership and service networks to ensure faster maintenance and better customer support across industrial and logistics hubs. They are introducing advanced models with improved fuel efficiency, higher load capacity, and enhanced safety features to meet the needs of warehouses, ports, and construction sites. A strong shift is also seen toward electric forklifts as companies respond to sustainability goals and the growing demand for cleaner indoor operations. Many players are investing in automation and smart technologies, including telematics, fleet tracking, and predictive maintenance systems, helping customers reduce downtime and optimize equipment usage. Partnerships with logistics providers and large industrial operators are increasing, along with flexible rental and leasing options to attract cost-sensitive buyers. These strategies help strengthen competitiveness in a rapidly developing market.

Saudi Arabia Forklift Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Classes Covered | Class 1, Class 2, Class 3, Class 4/5 |

| Power Sources Covered | ICE, Electric |

| Load Capacities Covered | Below 5 Ton, 5-15 Ton, Above 16 Ton |

| Electric Batteries | Li-ion, Lead Acid |

| End Users Covered | Industrial, Logistics, Chemical, Food and Beverage, Retail and E-Commerce, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Forklift Market Report

The Saudi Arabia forklift market size was valued at USD 738.9 Million in 2025.

The Saudi Arabia forklift market is expected to grow at a compound annual growth rate of 13.23% from 2026-2034 to reach USD 2,260.8 Million by 2034.

Class 3 held the largest market share at 32% in 2025 in 2025, driven by electric hand forklift trucks' versatility in warehouse operations, optimal balance of maneuverability and efficiency, and zero-emission performance suitable for indoor facilities. Their compact design enables navigation through narrow corridors while maintaining substantial load-carrying capacity, making them indispensable for order picking and inventory management across Saudi Arabia's expanding logistics infrastructure

Key factors driving the Saudi Arabia forklift market include Vision 2030 infrastructure development and the National Industrial Development and Logistics Program creating systematic demand across ports, logistics zones, and industrial facilities; exponential e-commerce expansion necessitating rapid warehouse capacity scaling; and accelerated transition to sustainable electric forklift technology supported by government incentives and improving lithium-ion battery economics delivering favorable total cost of ownership.

Major challenges include skilled operator shortages exacerbated by Saudization policy requirements creating a projected deficit of skilled workers by 2030, high initial investment costs for electric forklift technology and lithium-ion battery systems that can exceed internal combustion alternatives , and rising construction and operational costs driven by mega-project demand pressures and ongoing Red Sea supply chain disruptions affecting equipment procurement timelines and project economics.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)