Saudi Arabia Furniture Market Size, Share, Trends and Forecast by Material, Application, Distribution Channel, and Region 2026-2034

Saudi Arabia Furniture Market Size, Share, Trends & Forecast (2026-2034)

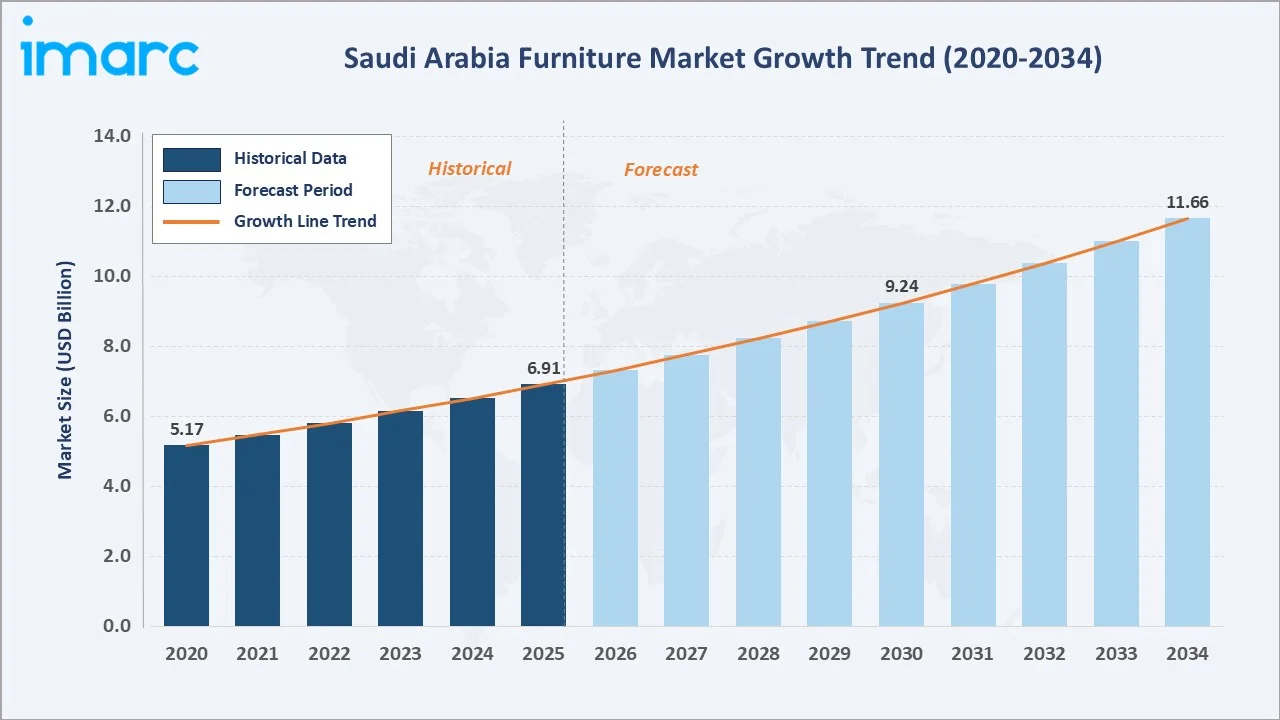

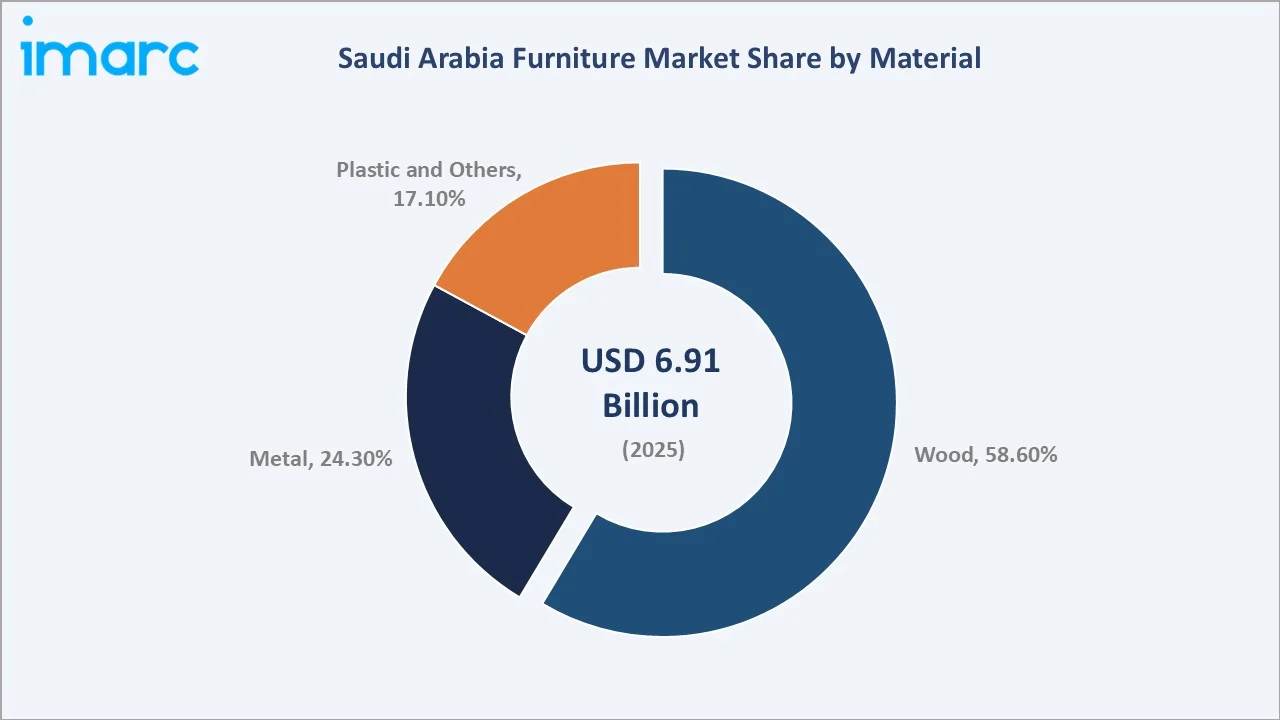

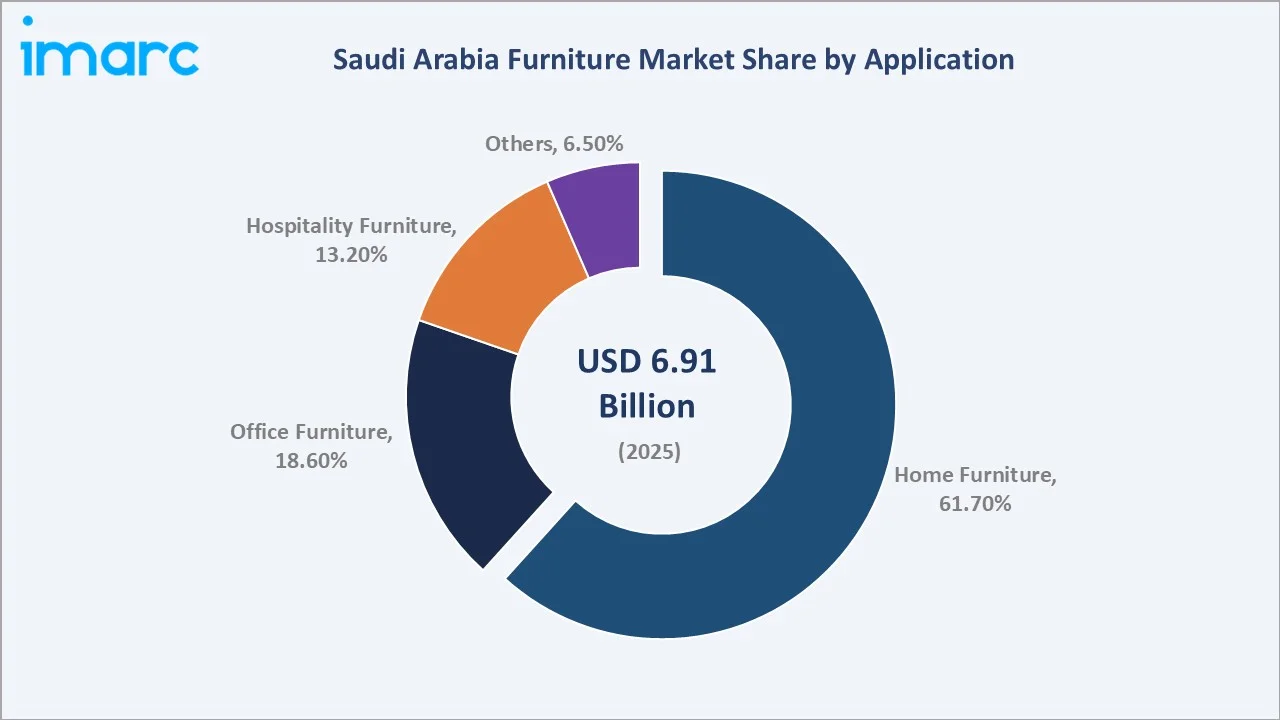

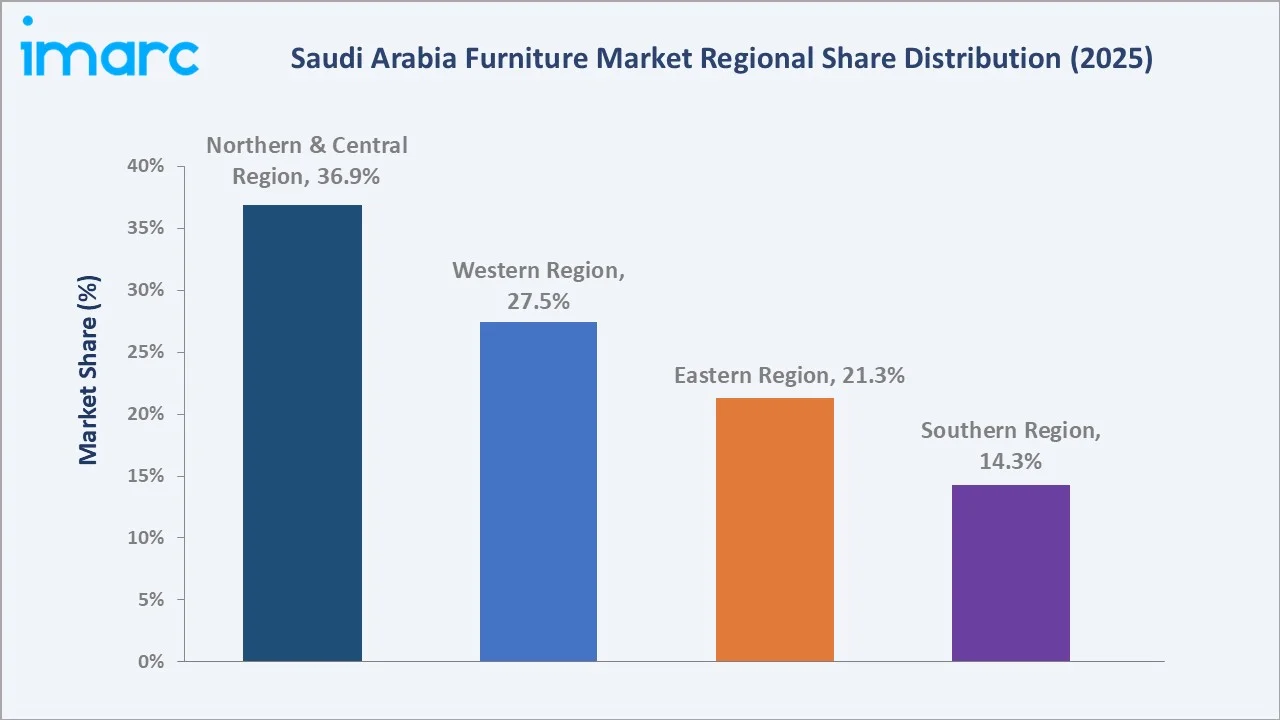

The Saudi Arabia furniture market size reached USD 6.91 Billion in 2025 and is projected to reach USD 11.66 Billion by 2034, exhibiting a CAGR of 5.99% during 2026-2034. Vision 2030 housing and hospitality investments, rising urbanization, and surging e-commerce adoption are the primary forces driving market growth. Wood dominates the material mix at 58.6% in 2025, while Home Furniture leads the application segment at 61.7%. The Northern and Central Region commands a dominant 36.9% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.91 Billion |

|

Forecast Market Size (2034) |

USD 11.66 Billion |

|

CAGR (2026-2034) |

5.99% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Material |

Wood (58.6%, 2025) |

|

Leading Application |

Home Furniture (61.7%, 2025) |

|

Largest Region |

Northern and Central Region (36.9%, 2025) |

The Saudi Arabia furniture market growth trajectory from 2020 through 2034, with the historical expansion to USD 6.91 Billion in 2025, reflects consistent infrastructure-driven demand, while the forecast to USD 11.66 Billion captures accelerating Vision 2030 investments, hospitality expansion, and rising expatriate-driven residential furnishing demand.

To get more information on this market, Request Sample

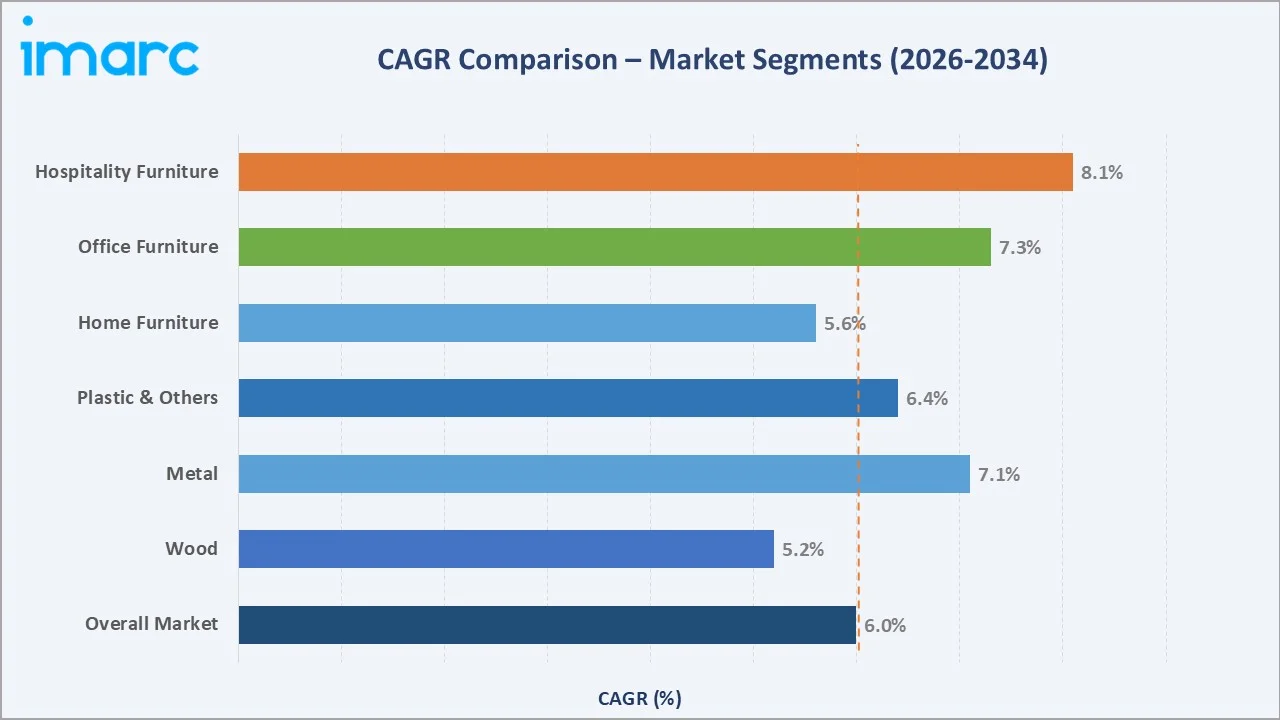

The CAGR trajectories across key material, application, and regional sub-segments, with Hospitality Furniture at ~8.1% CAGR and Office Furniture at ~7.3% CAGR, are the fastest-growing categories within the Saudi Arabia furniture industry analysis through 2034.

Executive Summary

The Saudi Arabia furniture market is on a sustained growth trajectory from USD 6.91 Billion in 2025 to USD 11.66 Billion by 2034. Furniture, an essential component across residential, commercial, and hospitality environments, benefits from the non-discretionary nature of housing and infrastructure investment demand in Saudi Arabia.

Wood dominates material at 58.6% in 2025, owing to its aesthetic versatility, durability, and strong consumer preference for traditional and modern wooden pieces. Metal furniture (24.3%) commands a significant share in commercial and office environments, valued for its robustness and contemporary design. Plastic and Others (17.1%) serve budget-sensitive and outdoor applications.

Home Furniture leads application at 61.7% in 2025, driven by new residential construction from Vision 2030 housing programs and rising urbanization. Office Furniture (18.6%) benefits from corporate workspace expansion, while Hospitality Furniture (13.2%) grows fastest, driven by hotel and tourism project development across the Kingdom.

The Northern and Central Region dominates at 36.9% in 2025, anchored by Riyadh's concentration of residential and commercial development. The Western Region (27.5%) and Eastern Region (21.3%) follow, sustained by Jeddah's retail and tourism market and Dammam's industrial base, respectively.

Key Market Insights

|

Insight |

Data |

|

Largest Material |

Wood - 58.6% share (2025) |

|

Leading Application |

Home Furniture - 61.7% share (2025) |

|

Fastest-Growing Application |

Hospitality Furniture - ~8.1% CAGR |

|

Leading Region |

Northern and Central Region - 36.9% (2025) |

|

Second Region |

Western Region - 27.5% (2025) |

|

Top Companies |

IKEA, Almutlaq Furniture, Al Rugaib Furniture, Home Centre (Landmark Group), National Furniture Manufacturing Company (Athath) |

Key Analytical Observations Expanding On The Above Data:

- Wood's 58.6% material dominance in 2025 reflects the deep cultural preference for high-quality wooden furniture in Saudi homes. Teak, oak, and engineered wood products are widely used for bedroom, dining, and living room furniture, balancing aesthetics with structural durability.

- Home Furniture's 61.7% application share is anchored by Saudi Arabia's residential construction boom under Vision 2030. The government's target to raise homeownership from 47% to 70% by 2030 underpins consistent demand for complete home furnishing packages.

- The Northern and Central Region's 36.9% dominance reflects Riyadh's role as the economic hub. Mega-projects such as NEOM planning offices and King Salman Park urban development are generating substantial procurement of residential and commercial furniture.

- The Western Region's 27.5% share is sustained by Jeddah's position as a premier commercial and tourism destination. The city's hotel pipeline expansion and retail corridor development are consistently driving hospitality and retail furniture demand.

Saudi Arabia Furniture Market Overview

Furniture encompasses a broad range of manufactured products used to support human activity in residential, commercial, and hospitality environments. Product categories span bedroom sets, dining suites, living room collections, office workstations, and bespoke hospitality furnishings. Materials include solid wood, engineered wood, metal alloys, polymer composites, and upholstered textiles.

The Saudi Arabia ecosystem integrates timber and raw material importers, domestic and international furniture manufacturers, surface treatment and upholstery specialists, specialty and mass-market retailers, e-commerce platforms, EPC contractors furnishing commercial projects, and diverse end-use sectors spanning residential, corporate, hospitality, and government applications.

Market Dynamics

To evaluate market opportunities, Request Sample

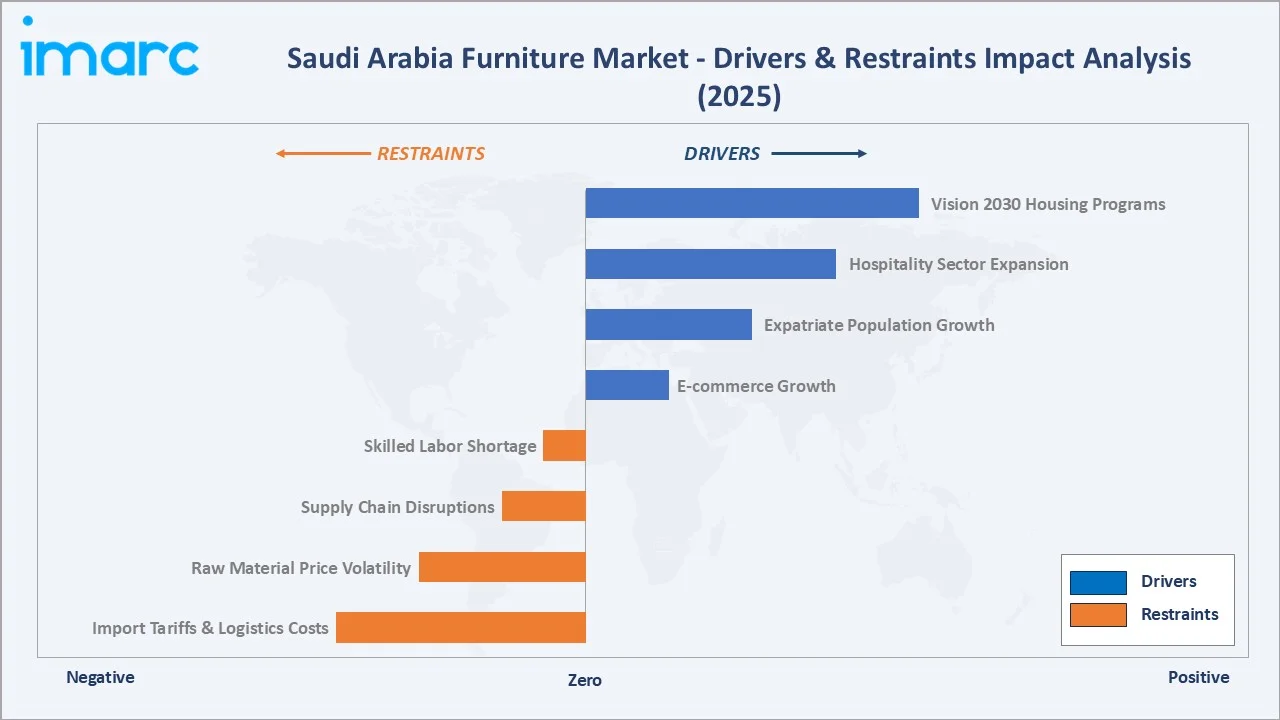

Market Drivers

- Vision 2030 Housing and Infrastructure Programs: The Saudi Housing Program targets raising homeownership to 70% by 2030, generating continuous procurement demand for residential furniture across newly constructed units, villas, and apartment complexes across major urban centers.

- Expanding Expatriate Population and Urbanization: Saudi Arabia's growing expatriate workforce drives demand for essential home furniture including beds, sofas, and dining sets. Urban population growth requires comprehensive furnishing of newly constructed residential properties throughout the Kingdom.

- Hospitality Sector Expansion via Tourism Initiatives: Saudi Arabia plans over 362,000 additional hotel keys by 2030, underpinning more than USD 110 Billion in hospitality investment. Each property requires complete furnishing packages, generating large-scale contract furniture procurement.

Market Restraints

- High Import Tariffs and Logistics Costs: International furniture brands face significant challenges from import tariffs and elevated logistics costs in Saudi Arabia. These factors limit competitive pricing and constrain market penetration, particularly in mid-range consumer segments.

- Raw Material Price Volatility: Dependence on imported timber, steel, and polymer resins exposes Saudi furniture manufacturers to global commodity price fluctuations, increasing production costs and complicating long-term pricing strategies.

Market Opportunities

- Eco-Friendly and Sustainable Furniture Demand: Growing consumer awareness of environmental sustainability is creating demand for FSC-certified wood, recycled material furniture, and low-VOC finishes. Manufacturers incorporating sustainability credentials gain preference in government procurement and premium consumer segments.

- AR/VR-Enhanced Digital Shopping Experience: Augmented reality and virtual reality technologies are revolutionizing online furniture purchasing. Platforms enabling consumers to visualize furniture in their homes before purchase are significantly reducing return rates and increasing online conversion rates.

Market Challenges

- Competition from Low-Cost International Imports: Affordable furniture imports, particularly from Asian manufacturers, intensify price competition in mass-market segments. Domestic producers face pressure to maintain cost competitiveness while investing in quality and design innovation.

- Supply Chain Complexity and Lead Times: Custom furniture projects requiring non-standard dimensions, specialized materials, or unique finishes generate extended production lead times of 6-14 weeks, challenging project timelines for hospitality and commercial construction applications.

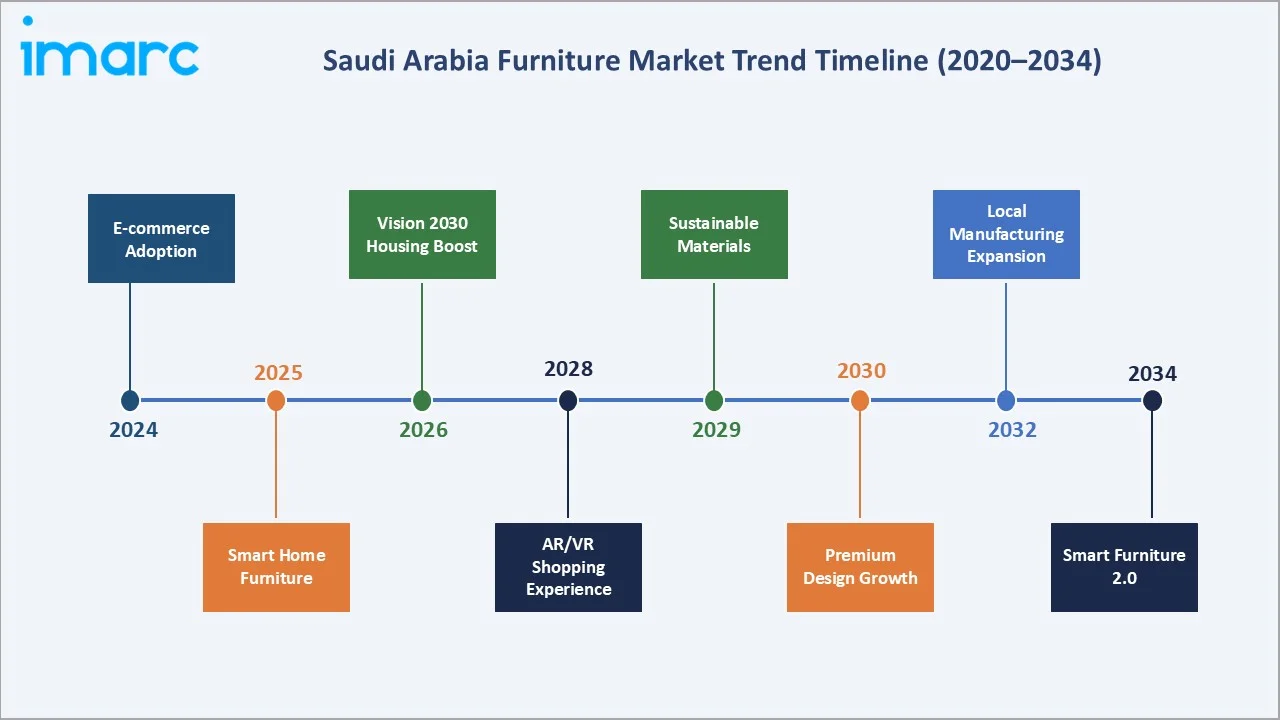

Emerging Market Trends

1. E-commerce and Digital Transformation Reshaping Furniture Retail

E-commerce adoption in Saudi Arabia's furniture market has accelerated significantly, driven by 99% internet penetration and widespread smartphone usage. Online furniture platforms offer diverse product ranges, competitive pricing, and home delivery services, attracting consumers seeking convenient shopping experiences.

2. Modular and Space-Efficient Furniture for Urban Apartments

Rapid urbanization and growing demand for compact living spaces in Riyadh, Jeddah, and Dammam are driving adoption of modular, multi-functional furniture. Manufacturers are developing adaptable designs featuring storage-integrated beds, foldable dining sets, and sofa-bed combinations catering to urban lifestyle needs.

3. Premium and Luxury Furniture Growth Driven by Affluent Consumers

Rising disposable incomes among affluent Saudi households are fueling demand for premium and luxury furniture segments. Bespoke designs, high-quality imported materials, and customized finishes are gaining traction, particularly among high-net-worth individuals investing in villa and premium apartment interiors.

4. Smart Furniture Integration with IoT and Technology

The integration of technology into furniture products, including smart beds with health monitoring, desks with integrated charging stations, and connected storage solutions, is an emerging trend capturing consumer interest among tech-savvy younger Saudi demographics.

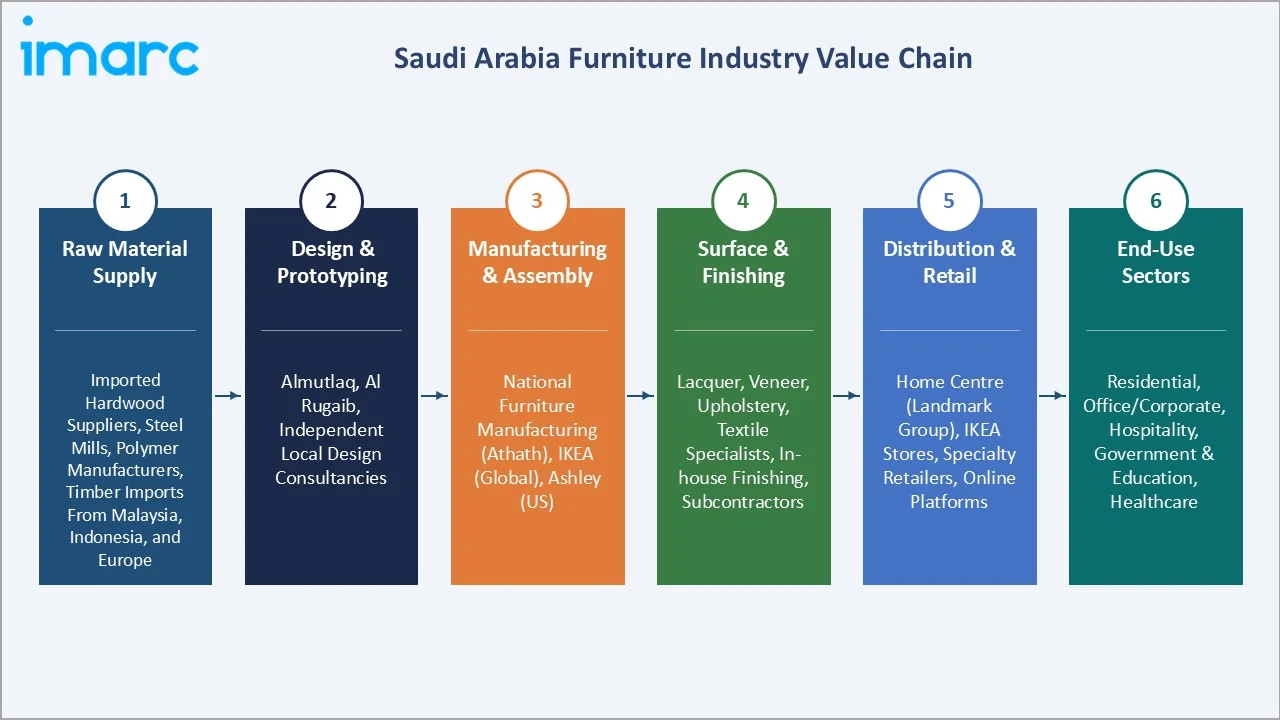

Industry Value Chain Analysis

The Saudi Arabia furniture value chain spans six stages from raw material sourcing through end-use delivery. Manufacturing and design capture the highest value-add margins, while retail distribution and project-specific customization generate significant competitive differentiation among market participants.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Imported hardwood suppliers, steel mills, polymer manufacturers; Timber imports from Malaysia, Indonesia, and Europe |

|

Design & Prototyping |

Almutlaq, Al Rugaib; Independent local design consultancies catering to bespoke residential projects |

|

Manufacturing & Assembly |

National Furniture Manufacturing (Athath), IKEA (global), Ashley (US) |

|

Surface & Finishing |

Lacquer, veneer, upholstery, and textile specialists; In-house finishing at major manufacturers and specialized subcontractors |

|

Distribution & Retail |

Home Centre (Landmark Group), IKEA stores; Specialty retailers, online platforms, and project sales teams |

|

End-Use Sectors |

Residential, Office/Corporate, Hospitality, Government & Education, Healthcare |

Vertically integrated furniture companies with captive manufacturing and in-house retail operations achieve lower cost structures than importers relying on third-party manufacturing. IKEA's global supply chain and local store network exemplifies this advantage in the Saudi market.

Technology Landscape in the Saudi Arabia Furniture Industry

CNC Manufacturing and Automated Production Lines

Computer Numerical Control (CNC) routing, cutting, and drilling systems have become standard in Saudi Arabia's larger furniture manufacturing facilities. CNC automation enables consistent dimensional precision, reduces material waste, and accelerates production cycles for high-volume residential and commercial furniture orders.

Material Innovation: Engineered Wood and Advanced Composites

Medium-density fiberboard (MDF), high-density fiberboard (HDF), and particleboard are widely adopted as cost-effective alternatives to solid wood. These engineered materials offer dimensional stability, consistent surface quality, and reduced susceptibility to moisture-related warping in Saudi Arabia's climate.

Sustainability Technology and Eco-Material Adoption

Water-based lacquers, low-formaldehyde adhesives, and FSC-certified timber are gaining specification in Saudi Arabia's premium furniture segment. Government green building requirements and increasing consumer awareness are accelerating adoption of environmentally compliant materials and production processes.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Material |

Wood |

58.6% |

2025 |

|

Application |

Home Furniture |

61.7% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

Northern and Central Region |

36.9% |

2025 |

By Material

Wood commands a 58.6% majority share in 2025, reflecting its deep cultural resonance in Saudi interiors and its unmatched versatility across traditional and contemporary design styles. Solid teak, oak, and engineered wood products are consistently specified across bedroom, dining, and living room furniture collections, from mass-market to premium tiers.

To access detailed market analysis, Request Sample

Metal furniture at 24.3% in 2025 is irreplaceable in commercial, office, and outdoor applications where structural durability is paramount. Steel and aluminum furniture dominate office workstation systems, shelving, and commercial seating, growing at ~7.1% CAGR. Plastic and Others (17.1%) serve light-duty indoor and outdoor applications where affordability and ease of maintenance are prioritized.

By Application

Home Furniture dominates at 61.7% in 2025, representing the largest and most consistent demand category in Saudi Arabia's furniture market. Rising residential construction under Vision 2030, the government's homeownership target, and a young population seeking stylish home interiors are collectively sustaining robust home furniture procurement.

Office Furniture at 18.6% in 2025 benefits from growing corporate workspace investment, Vision 2030 business diversification attracting multinational tenants, and increasing demand for ergonomic solutions. Hospitality Furniture (13.2%) is the fastest-growing application, driven by Saudi Arabia's unprecedented hotel pipeline development targeting over 362,000 new hotel keys by 2030.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Northern and Central Region |

36.9% |

Riyadh mega-projects; Vision 2030 housing; NEOM admin demand; corporate workspace expansion |

|

Western Region |

27.5% |

Jeddah tourism and hospitality boom; Red Sea Project; Makkah & Madinah pilgrimage infrastructure |

|

Eastern Region |

21.3% |

Dammam-Khobar-Dhahran industrial and residential growth; petrochemical sector; ARAMCO infrastructure |

|

Southern Region |

14.3% |

Abha tourism development; Aseer Vision projects; residential construction in Najran and Jizan |

The Northern and Central Region's 36.9% market dominance in 2025 is driven by Riyadh's status as both the political and economic capital of Saudi Arabia. Riyadh's urban population of over 7 million, combined with massive residential and commercial construction activity, creates the Kingdom's deepest furniture procurement market.

The Western Region, with 27.5% in 2025, benefits from Jeddah's dual role as Saudi Arabia's premier commercial port and tourism gateway. The region's rapidly expanding hospitality sector, anchored by the Red Sea Project development and Makkah's annual pilgrimage tourism, creates significant hospitality and retail furniture procurement cycles.

Competitive Landscape

The Saudi Arabia furniture market is moderately fragmented, with international retail giants competing alongside regional manufacturers and specialty local brands. IKEA dominates in organized retail through its global sourcing model and store network, while domestic manufacturers such as Almutlaq and Al Rugaib maintain strong regional loyalty and custom capabilities.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

IKEA |

Complete home furniture range; modular systems; beds, sofas, dining, storage |

Leader |

Volume leadership; digital/omnichannel; sustainability |

|

Almutlaq Furniture |

Luxury and mid-range residential furniture; branded international collections |

Leader |

Premium positioning; KSA heritage; loyalty programs |

|

Al Rugaib Furniture |

Sofas, bedroom, dining, and kids' furniture collections |

Leader |

Strong local brand; KSA-wide retail network |

|

Home Centre (Landmark Group) |

Home furniture, decor, and furnishing accessories |

Leader |

Multi-category retail; affordable mid-range positioning |

|

Ashley Homestore Furniture |

Sofas, beds, dining, home office |

Challenger |

US brand expansion; premium showroom format |

|

AthathCo. (National Furniture Manufacturing Company) |

Domestic mass-market furniture; government and institutional supply |

Challenger |

Local manufacturing; government procurement |

|

Pan Home |

Full-range home furniture and home decor accessories |

Emerging |

Gulf-wide footprint; competitive mid-market pricing |

The key players include IKEA, Almutlaq Furniture, Al Rugaib Furniture, Home Centre (Landmark Group), Ashley Homestore Furniture, AthathCo. (National Furniture Manufacturing Company), Pan Home, and others.

Key Company Profiles

IKEA

IKEA is the world's largest furniture retailer, operating through a global supply chain. In Saudi Arabia, IKEA is operated by the Alsulaiman Group, which handles multiple large-format stores and has invested in e-commerce capabilities to serve the Kingdom's digitally engaged consumers.

- Product Portfolio: Complete home furnishing range including bedroom, living room, kitchen, dining, storage, and home office solutions, offered at accessible price points with iconic flat-pack assembly.

- Recent Developments: In November 2024, IKEA Alsulaiman opened a new store in Madinah as part of its broader expansion strategy in Saudi Arabia, reinforcing its commitment to strengthening its retail presence in the Kingdom. The large-format store offers a comprehensive shopping experience with a wide range of home furnishing products and customer amenities, while also contributing to local economic development through job creation and sustainable infrastructure initiatives.

- Strategic Focus: IKEA's strategy in Saudi Arabia leverages its global supply chain scale to maintain competitive pricing, while investing in digital channels and sustainability credentials to align with Vision 2030's eco-friendly development goals.

Almutlaq Furniture

Almutlaq Furniture is one of Saudi Arabia's most established and recognized domestic furniture brands, operating a network of premium showrooms across the Kingdom. The company offers an extensive range of locally relevant and internationally sourced furniture collections.

- Product Portfolio: Luxury and mid-range residential furniture collections including international branded lines, bespoke furniture services, and full interior design consultation for residential and commercial clients.

- Strategic Focus: Almutlaq differentiates on brand heritage, premium positioning, and comprehensive customer service, targeting affluent Saudi consumers and hospitality clients requiring bespoke high-quality furnishing solutions.

Al Rugaib Furniture

Al Rugaib Furniture is a leading Saudi Arabian furniture retail chain with a strong presence across the Kingdom. Known for offering contemporary and traditional furniture collections at competitive prices, the company serves a broad consumer base across residential segments.

- Product Portfolio: Diverse range of sofas, bedroom sets, dining furniture, children's furniture, and home accessories, combining imported collections with domestically manufactured pieces.

- Recent Developments: In January 2026, Hamad M. Al Rugaib & Sons Trading Co. inaugurated a new Ashley furniture showroom in Dammam, Saudi Arabia, marking a continued expansion of the brand’s retail footprint in the region. The large-format store introduces a modern retail concept with curated lifestyle displays and a broad range of home furnishing products, while also contributing to local employment and enhancing customer access to globally recognized furniture offerings.

- Strategic Focus: Al Rugaib focuses on broad geographic retail coverage, competitive pricing in the mid-market segment, and regular collection refreshes aligned with seasonal demand cycles and consumer design trends.

Home Centre (Landmark Group)

Home Centre, a division of the UAE-based Landmark Group, is one of the largest home furnishing retail chains in the Middle East and South Asia. In Saudi Arabia, Home Centre operates an extensive retail network offering furniture, home décor, and furnishing accessories.

- Product Portfolio: Multi-category home furnishing products spanning furniture, lighting, rugs, bedding, and home accessories, positioned at accessible mid-range price points.

- Strategic Focus: Home Centre leverages the Landmark Group's regional scale to maintain competitive sourcing costs, focusing on a broad mid-market consumer base seeking one-stop home furnishing solutions across Saudi Arabia's major cities.

Market Concentration Analysis

The Saudi Arabia furniture market is moderately fragmented at the national level, with international brands like IKEA holding strong urban positions while domestic manufacturers and regional chains maintain significant shares in their respective home markets. No single company commands more than 15-20% of total market revenue.

Consolidation trends are emerging as domestic developers increasingly seek single-source furnishing partners capable of supplying complete fit-out packages for large-scale residential and hospitality projects. International companies entering the Saudi market through franchise or direct investment are increasing competitive intensity in premium segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Hospitality Furniture at ~8.1% CAGR through 2034 is the highest-growth application segment, driven by Saudi Arabia's unprecedented hotel and resort development pipeline targeting 362,000 new hotel keys by 2030. Office Furniture at ~7.3% CAGR represents the broadest corporate workspace investment opportunity.

Emerging Markets

The Southern Region at ~6.8% CAGR is the fastest-growing region for furniture through 2034. Abha's emergence as a domestic tourism destination, Aseer Vision development projects, and increasing residential construction in Najran and Jizan are creating new furniture demand from a region with historically low market penetration.

Venture & Investment Trends

Private investment interest in Saudi Arabia's furniture manufacturing sector is growing, incentivized by government local content requirements under Vision 2030 that favor domestically produced goods in government procurement. E-commerce furniture platform investments are attracting venture funding as digital penetration accelerates across the Kingdom.

Future Market Outlook (2026-2034)

The Saudi Arabia furniture market is forecast to expand from USD 6.91 Billion in 2025 to USD 11.66 Billion by 2034 at a CAGR of 5.99%, adding USD 4.75 Billion in incremental annual market value over the forecast period. This sustained growth reflects the market's infrastructure-linked, non-discretionary demand characteristics.

Three structural forces will most significantly shape the Saudi Arabia furniture market landscape through 2034. Vision 2030 housing and commercial development will sustain residential and office furniture demand at scale. Tourism and hospitality mega-project delivery will generate the largest contract furniture procurement cycles in the Kingdom's history. Digital transformation of furniture retail will shift an increasing share of sales to e-commerce channels, reshaping distribution economics.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Saudi Arabia furniture industry stakeholders, including retail chain procurement managers, domestic manufacturer executives, real estate developers, hospitality project directors, and furniture industry association representatives. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption trends.

Secondary Research

Key secondary sources include Saudi Vision 2030 housing program publications, Ministry of Housing investment data, GASTAT census and urbanization statistics, Saudi Tourism Authority hotel pipeline reports, SASO furniture product standards documentation, Euromonitor International furniture market data, and trade publications covering Middle East retail and manufacturing sectors.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, housing construction indices, urbanization data, consumer expenditure patterns, and historical market evolution. Scenario analysis covering base, optimistic, and conservative cases was performed to account for oil price and macroeconomic uncertainty.

Saudi Arabia Furniture Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Materials Covered | Wood, Metal, Plastic and Others |

| Applications Covered | Home Furniture, Office Furniture, Hospitality Furniture, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | IKEA, Almutlaq Furniture, Al Rugaib Furniture, Home Centre (Landmark Group), Ashley Homestore Furniture, AthathCo. (National Furniture Manufacturing Company), Pan Home, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia furniture market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia furniture market.

- The study maps the leading, as well as the fastest-growing, markets. It further enables stakeholders to identify the key country-level markets within the region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia furniture industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Furniture Market Report

The Saudi Arabia furniture market reached USD 6.91 Billion in 2025, reflecting consistent demand from Vision 2030 housing programs, expanding expatriate population, and a growing hospitality sector.

The market is projected to reach USD 11.66 Billion by 2034, growing at a CAGR of 5.99% during 2026-2034, driven by residential construction, hospitality project development, and e-commerce channel expansion.

Wood leads with a 58.6% material share in 2025, valued for its aesthetic versatility, durability, and alignment with Saudi cultural preferences for high-quality residential furniture.

Home Furniture leads at 61.7% in 2025, driven by Vision 2030 residential construction, rising homeownership targets, and young Saudi consumers seeking contemporary interior designs.

The Northern and Central Region commands a dominant 36.9% market share in 2025, driven by Riyadh's concentration of residential, commercial, and government infrastructure development.

Hospitality Furniture is the fastest-growing application at ~8.1% CAGR through 2034, driven by Saudi Arabia's unprecedented hotel and resort development pipeline under Vision 2030 tourism initiatives.

Leading companies include IKEA, Almutlaq Furniture, Al Rugaib Furniture, Home Centre (Landmark Group), Ashley Homestore Furniture, AthathCo. (National Furniture Manufacturing Company), Pan Home, and others.

Key drivers include Vision 2030 housing and infrastructure programs, expanding expatriate population, rapid hospitality sector development, rising disposable incomes, and accelerating e-commerce adoption across the Kingdom.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)