Saudi Arabia Grid Energy Storage Solutions Market Size, Share, Trends and Forecast by Technology, Application, End User, and Region, 2026-2034

Saudi Arabia Grid Energy Storage Solutions Market Overview:

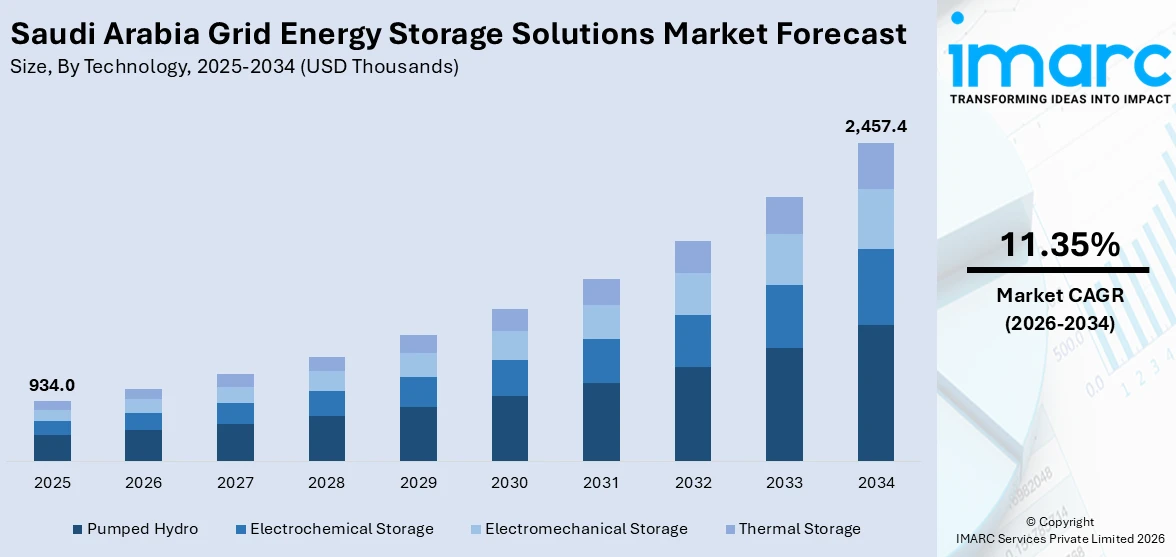

The Saudi Arabia grid energy storage solutions market size reached USD 934.0 Thousands in 2025. Looking forward, IMARC Group expects the market to reach USD 2,457.4 Thousands by 2034, exhibiting a growth rate (CAGR) of 11.35% during 2026-2034. The market is driven by Saudi Arabia’s long-term energy transition policies and regulatory frameworks. Additionally, commercial sector resilience and industrial applications enhance grid reliability. Government investment, energy diversification plans, and smart infrastructure rollouts are some of the factors positively impacting the Saudi Arabia grid energy storage solutions market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 934.0 Thousands |

| Market Forecast in 2034 | USD 2,457.4 Thousands |

| Market Growth Rate 2026-2034 | 11.35% |

Saudi Arabia Grid Energy Storage Solutions Market Trends:

Government Initiatives and Strategic Vision

Saudi Arabia’s national development policies are a significant driver for the adoption of advanced electricity storage infrastructure. Under Vision 2030, the Kingdom is committed to transforming its power generation profile by increasing the share of renewable energy while modernizing its grid system. This transition has placed considerable emphasis on decentralized storage systems to ensure grid stability, reliability, and reduced dependency on hydrocarbons. Additionally, the Public Investment Fund (PIF) is increasingly channeling capital toward infrastructure that supports clean energy deployment, further aligning investment flows with long-term energy storage capabilities. Beyond domestic policy, Saudi Arabia’s efforts to position itself as a leader in sustainable energy across the GCC and MENA regions have pushed regulators to create favorable policies for private sector involvement. This includes auction-based tenders and technology-neutral grid codes that encourage competitive bidding for energy storage deployment. On March 12, 2025, Siemens Energy secured a USD 1.6 Billion contract to supply core technologies for the 3.6 GW Rumah 2 and Nairyah 2 gas-fired power plants in Saudi Arabia, which will serve around 1.5 million homes and replace aging oil-based plants. The plants, designed with CO₂ capture compatibility, are expected to cut emissions by up to 60% and will be supported by long-term maintenance agreements spanning 25 years. Siemens will manufacture key components at its expanding Dammam Hub, aligning with Saudi Arabia’s strategy to localize energy sector capabilities and stabilize its power grid as it scales renewable integration. The Saudi Arabia grid energy solutions market growth is largely underpinned by these regulatory reforms and capital investments facilitating grid flexibility and decarbonization.

To get more information on this market Request Sample

Increasing Penetration of Renewable Energy

Saudi Arabia’s solar potential is among the highest globally, with irradiation levels exceeding 2,200 kWh/m² annually in most regions. As large-scale solar photovoltaic (PV) projects move toward commercial operation, there is an immediate need to address grid intermittency and frequency regulation. Grid-connected storage systems, particularly battery energy storage systems (BESS), have become vital in bridging the gap between generation and consumption. On January 20, 2025, Saudi Arabia commissioned its largest battery energy storage system (BESS), a 500 MW/2,000 MWh project in Bisha, developed by Saudi Electric Company using 122 prefabricated units from China’s BYD. The system integrates 6 MW power conversion systems and lithium iron phosphate batteries, aiming to enhance grid flexibility and renewable energy integration under the kingdom’s Vision 2030 target of 50% clean energy. The declining cost of lithium-ion batteries and the emergence of alternative chemistries such as sodium-ion and flow batteries are improving project economics. This has accelerated private sector participation in both utility-scale and distributed storage projects. As storage becomes central to the reliability of Saudi Arabia’s future energy mix, project developers and energy utilities are focusing on modular systems with longer life cycles and scalable capacity. The keyword market growth continues to benefit from these developments in renewable integration and technological cost curves.

Saudi Arabia Grid Energy Storage Solutions Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on technology, application, and end user.

Technology Insights:

- Pumped Hydro

- Electrochemical Storage

- Electromechanical Storage

- Thermal Storage

The report has provided a detailed breakup and analysis of the market based on the technology. This includes pumped hydro, electrochemical storage, electromechanical storage, and thermal storage.

Application Insights:

Access the comprehensive market breakdown Request Sample

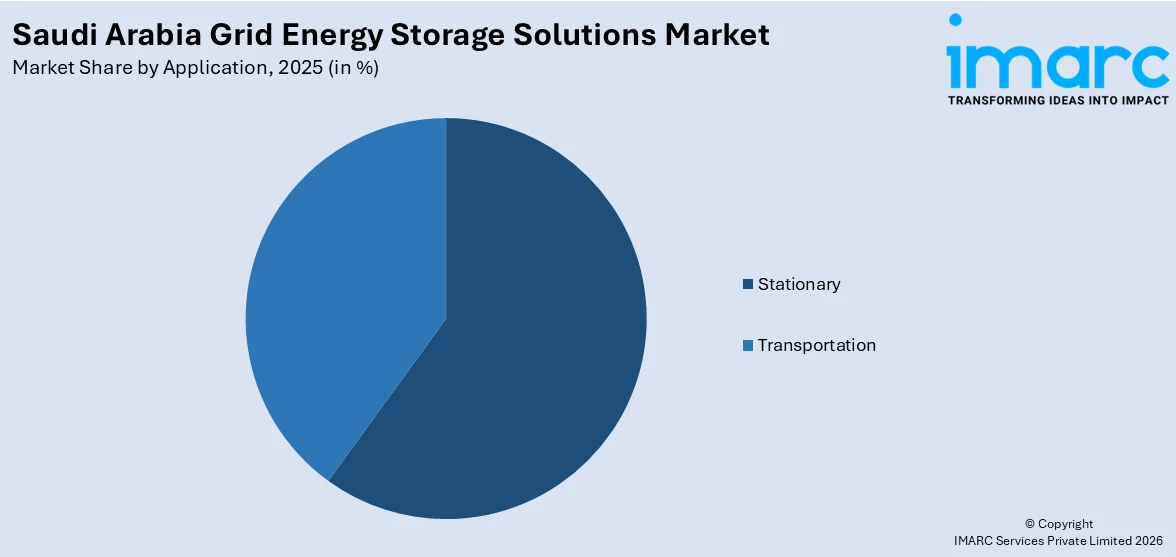

- Stationary

- Transportation

The report has provided a detailed breakup and analysis of the market based on the application. This includes stationary and transportation.

End User Insights:

- Residential

- Non-Residential

- Utilities

The report has provided a detailed breakup and analysis of the market based on the end user. This includes residential, non-residential, and utilities.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

The report has provided a comprehensive analysis of all major regional markets, including Northern and Central Region, Western Region, Eastern Region, and Southern Region.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Saudi Arabia Grid Energy Storage Solutions Market News:

- On September 11, 2024, Huawei announced the completion of the world’s largest microgrid power station in Saudi Arabia to support the Red Sea New City project, with a generation capacity of 400 MW photovoltaic power and 1.3 GWh of energy storage. The microgrid is expected to deliver one billion kWh annually and has been supplying green power since September 2023, positioning it as a critical infrastructure for what aims to be the world’s first fully renewable-energy-powered city. This project is part of Saudi Arabia's Vision 2030, which includes transforming 50 islands into sustainable luxury destinations, and is backed by USD 500 Billion in development funding.

Saudi Arabia Grid Energy Storage Solutions Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Thousands USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Pumped Hydro, Electrochemical Storage, Electromechanical Storage, Thermal Storage |

| Applications Covered | Stationary, Transportation |

| End Users Covered | Residential, Non-Residential, Utilities |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Saudi Arabia grid energy storage solutions market performed so far and how will it perform in the coming years?

- What is the breakup of the Saudi Arabia grid energy storage solutions market on the basis of technology?

- What is the breakup of the Saudi Arabia grid energy storage solutions market on the basis of application?

- What is the breakup of the Saudi Arabia grid energy storage solutions market on the basis of end user?

- What is the breakup of the Saudi Arabia grid energy storage solutions market on the basis of region?

- What are the various stages in the value chain of the Saudi Arabia grid energy storage solutions market?

- What are the key driving factors and challenges in the Saudi Arabia grid energy storage solutions market?

- What is the structure of the Saudi Arabia grid energy storage solutions market and who are the key players?

- What is the degree of competition in the Saudi Arabia grid energy storage solutions market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia grid energy storage solutions market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia grid energy storage solutions market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia grid energy storage solutions industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)