Saudi Arabia Heat Exchanger Tubes Market Size, Share, Trends and Forecast by Material Type, Product Type, Tube Configuration, Distribution Channel, End Use Industry, and Region, 2026-2034

Saudi Arabia Heat Exchanger Tubes Market Summary:

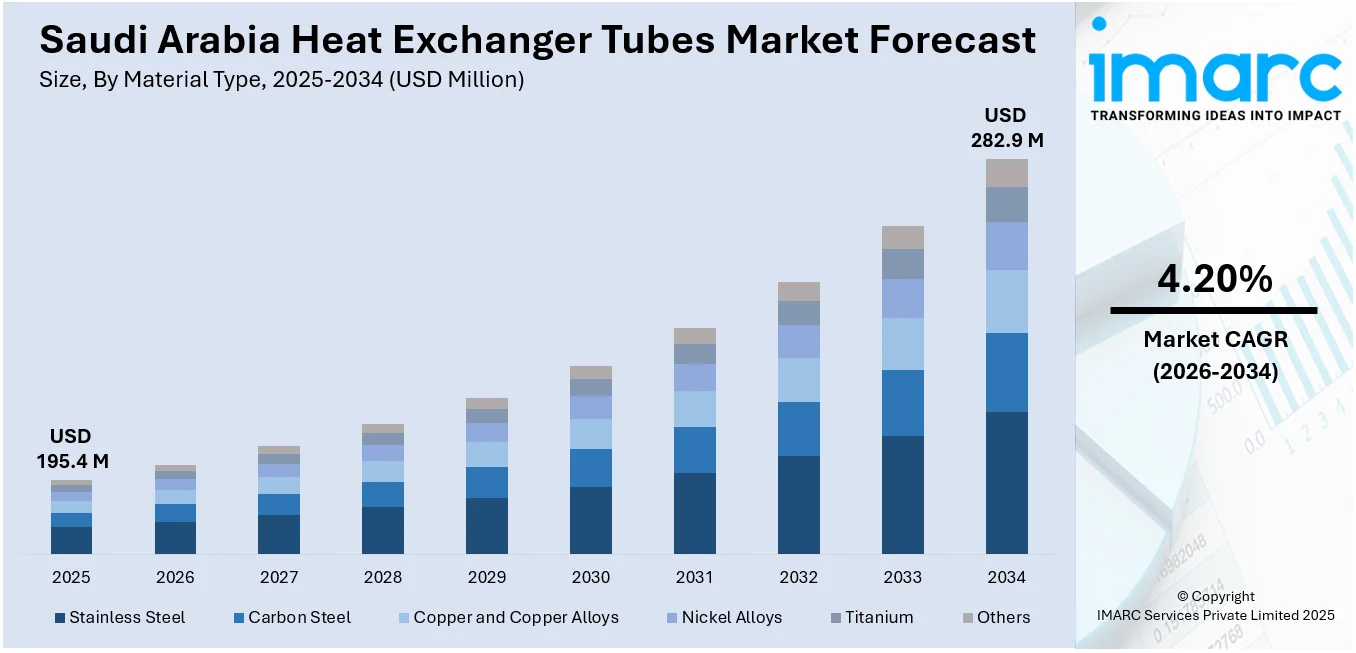

The Saudi Arabia heat exchanger tubes market size was valued at USD 195.4 Million in 2025 and is projected to reach USD 282.9 Million by 2034, growing at a compound annual growth rate of 4.20% from 2026-2034.

The Saudi Arabia heat exchanger tubes market is growing as large-scale industrial diversification programs accelerate demand across petrochemical, desalination, and power generation sectors. The growing investments in energy infrastructure, coupled with rising adoption of advanced thermal management solutions, are strengthening procurement activity. Ongoing localization initiatives and the commissioning of mega projects across multiple industrial verticals are further reinforcing the demand for high-performance heat exchanger tubing, contributing to the Saudi Arabia heat exchanger tubes market share.

Key Takeaways and Insights:

- By Material Type: Stainless steel represents the largest segment with a market share of 35% in 2025, due to its superior corrosion resistance and suitability for demanding petrochemical and desalination operating environments.

- By Product Type: Seamless heat exchanger tubes lead the market with a share of 58% in 2025, owing to their enhanced structural integrity and capacity to withstand high-pressure industrial applications.

- By Tube Configuration: U-tubes dominate the market with a share of 40% in 2025, supported by widespread adoption in shell-and-tube heat exchangers used across refining and petrochemical processing facilities.

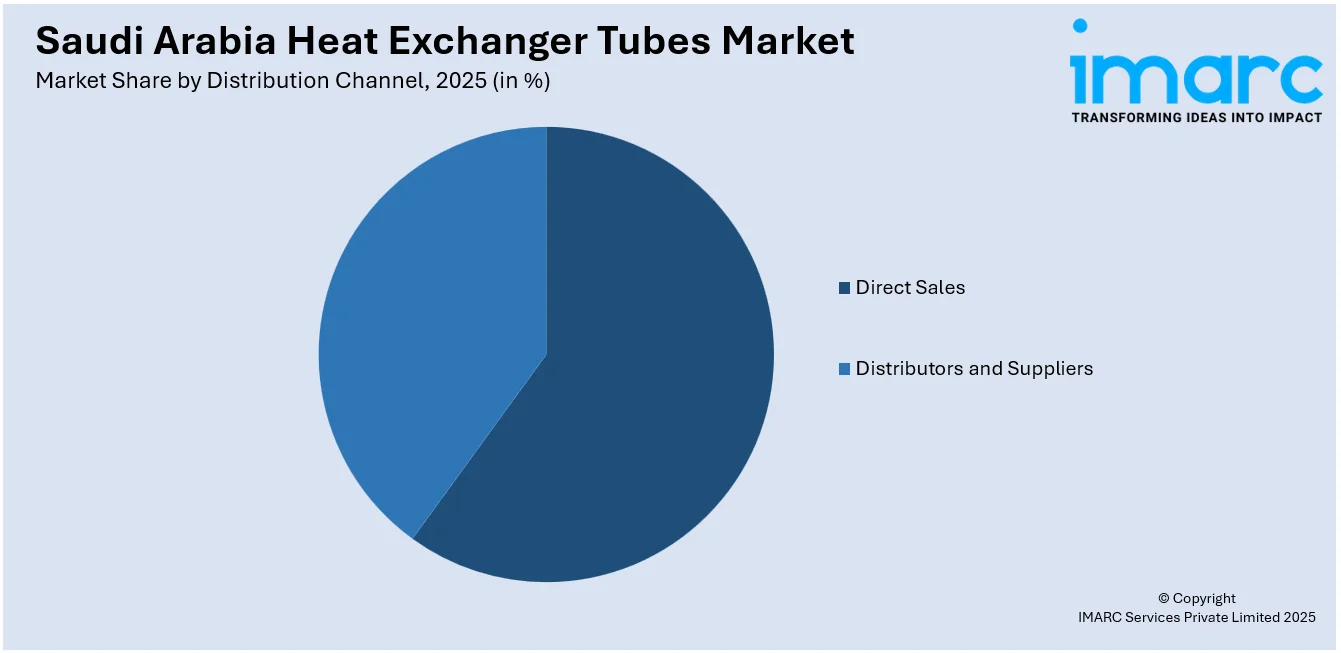

- By Distribution Channel: Direct sales represent the largest segment with a market share of 56% in 2025, reflecting the preference for integrated procurement in large-scale industrial and infrastructure projects.

- By End Use Industry: Oil and gas lead the market with a share of 24% in 2025, underpinned by extensive upstream, midstream, and downstream expansion programs across the kingdom.

- By Region: Northern and Central Region dominates the market with a share of 30% in 2025, driven by concentrated petrochemical infrastructure in Jubail and rapid urban development in Riyadh.

- Key Players: The Saudi Arabia heat exchanger tubes market features a competitive mix of global manufacturers and regional producers, with companies focusing on product innovation, localization strategies, and capacity expansion to strengthen their market positioning.

To get more information on this market Request Sample

The Saudi Arabia heat exchanger tubes market is driven by strong industrial growth, robust energy sector, and rising demand for efficient thermal management systems. Continued investments in oil and gas refining, petrochemical processing, and heavy manufacturing are generating substantial requirements for durable and corrosion-resistant tubing solutions. This momentum is reflected in recent developments, as in 2025 Saudi Arabia approved feedstock allocations for two new petrochemical complexes in Jubail, advancing major capacity additions and reinforcing demand for heat transfer equipment. Power generation expansion and energy efficiency initiatives are further supporting adoption of advanced exchanger systems. The Kingdom’s dependence on desalination for freshwater supply also contributes significantly, requiring specialized tubes for high salinity environments. In addition, infrastructure development and district cooling projects are increasing heating, ventilation, and air conditioning (HVAC)-related demand. Emerging sectors such as mining, renewable energy, and localization efforts under Vision 2030 are broadening market applications, ensuring sustained growth across diverse industries.

Saudi Arabia Heat Exchanger Tubes Market Trends:

Localization of Heat Exchanger Component Manufacturing

Saudi Arabia is increasingly promoting domestic manufacturing of industrial components to reduce reliance on imports and improve supply chain resilience. This focus is catalyzing the demand for locally produced heat transfer equipment and tubing. This localization drive gained momentum in 2024, when Alfa Laval Arabia for Maintenance began assembling its first plate heat exchanger units in the Kingdom after securing industrial license approval. The initial production included four AHRI-certified AQ10T-BFM units for a district cooling HVAC project at its Jubail facility. Such initiatives expand the local manufacturing ecosystem, shorten lead times, and encourage broader adoption of domestically sourced heat exchanger tubes, aligning with Saudi Vision 2030 industrial development goals.

Infrastructure Development and Large-Scale Construction Projects

Ongoing infrastructure investment and large-scale construction activity in Saudi Arabia are increasing the need for HVAC systems, district cooling networks, and industrial utilities that rely on heat exchangers. Heat exchanger tubes are essential for maintaining stable temperature control in residential complexes, commercial buildings, and mixed-use developments. This trend is reflected in continued housing expansion, as in 2024 Saudi Arabia announced a SAR 800 million housing project in Jeddah by the National Housing Company, delivering over 1,000 units within the Al-Sadan Community. As new cities, transport corridors, and tourism infrastructure advance toward completion, there is a higher need for efficient thermal management systems, thus supporting higher usage of heat exchanger tubing products.

Rising Investments in Renewable and Clean Energy Projects

The increasing number of renewable energy and clean power initiatives in Saudi Arabia is driving the need for heat exchanger tubes across emerging applications. Solar thermal systems, hydrogen production facilities, and energy storage projects rely on efficient heat transfer equipment to maintain temperature stability and operational reliability. This trend is evident in ongoing project development, as in 2024 GlassPoint reported progress on its USD 1.5 billion solar thermal project in Saudi Arabia supporting Ma’aden’s aluminum operations, including a new solar-to-steam manufacturing facility. As clean energy investments advance, there is a rise in the demand for specialized heat exchanger tubes designed to perform under varied and demanding operating conditions.

How Vision 2030 is Transforming the Saudi Arabia Heat Exchanger Tubes Market:

Saudi Arabia’s Vision 2030 is significantly transforming the heat exchanger tubes market by accelerating industrial diversification, infrastructure expansion, and energy sector modernization. Large-scale investments in petrochemicals, power generation, desalination, and district cooling projects are catalyzing the demand for high-performance heat exchanger tubing solutions. The Vision’s focus on local manufacturing and industrial localization is also encouraging domestic production and attracting foreign partnerships in advanced materials and engineering services. Growth in renewable energy, hydrogen development, and sustainable industrial processes is further supporting adoption of efficient heat transfer technologies. Overall, Vision 2030 is strengthening market opportunities by driving industrial growth, technology upgrades, and long-term capacity expansion.

Market Outlook 2026-2034:

The Saudi Arabia heat exchanger tubes market is positioned for growth, supported by ongoing mega project developments, energy infrastructure modernization, and industrial localization initiatives. The market generated a revenue of USD 195.4 Million in 2025 and is projected to reach a revenue of USD 282.9 Million by 2034, growing at a compound annual growth rate of 4.20% from 2026-2034. Continued investments in petrochemical processing, desalination capacity expansion, and power generation infrastructure are expected to drive higher revenue streams, while sustainability-focused efficiency mandates create additional demand for advanced heat exchanger tubing solutions.

Saudi Arabia Heat Exchanger Tubes Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Material Type |

Stainless Steel |

35% |

|

Product Type |

Seamless Heat Exchanger Tubes |

58% |

|

Tube Configuration |

U-Tubes |

40% |

|

Distribution Channel |

Direct Sales |

56% |

|

End Use Industry |

Oil and Gas |

24% |

|

Region |

Northern and Central Region |

30% |

Material Type Insights:

- Stainless Steel

- Carbon Steel

- Copper and Copper Alloys

- Nickel Alloys

- Titanium

- Others

Stainless steel dominates with a market share of 35% of the total Saudi Arabia heat exchanger tubes market in 2025.

Stainless steel leads the market due to its superior corrosion resistance, durability, and suitability for harsh operating environments. Heat exchangers in industries, such as oil and gas, petrochemicals, power generation, and desalination, require materials that can withstand high temperatures, pressure variations, and aggressive fluids. Stainless steel tube provides long service life, reduced maintenance needs, and reliable thermal performance. Its ability to resist scaling and chemical degradation makes it the preferred choice for critical industrial applications across the Kingdom.

The dominance of stainless steel is reinforced by expanding industrial infrastructure and sustained investment in energy and water projects. Stainless steel tube is widely preferred in refinery operations, cooling systems, and seawater-based heat exchange applications where high corrosion resistance is essential. Industrial operators prioritize stainless steel for its durability, operational safety, and compliance with strict quality standards. This demand is supported by major water initiatives, as in 2025 Veolia signed an agreement with SATORP to develop the Middle East’s largest industrial water recycling project in Jubail Industrial City, strengthening requirements for reliable heat transfer materials.

Product Type Insights:

- Seamless Heat Exchanger Tubes

- Welded Heat Exchanger Tubes

Seamless heat exchanger tubes lead with a market share of 58% of the total Saudi Arabia heat exchanger tubes market in 2025.

Seamless heat exchanger tubes account for the majority of the market share owing to their superior mechanical strength, uniform structure, and ability to withstand high pressure and temperature conditions. These tubes are widely preferred in critical applications across oil and gas, petrochemicals, power generation, and desalination facilities. The absence of welded joints reduces the risk of leaks and structural failures, ensuring higher reliability and longer service life. This performance advantage makes seamless tubes essential for demanding industrial operations.

The dominance of seamless tubes is further supported by Saudi Arabia’s extensive use of heat exchangers in energy intensive industries. Operators prioritize seamless products for enhanced safety, reduced maintenance requirements, and consistent thermal efficiency. These tubes also perform well in corrosive and high stress environments, aligning with the Kingdom’s harsh operating conditions. As large-scale industrial projects continue to expand, there is a higher demand for high quality and reliable heat exchanger components, reinforcing the leading position of seamless tubes in the market.

Tube Configuration Insights:

- U-Tubes

- Straight Tubes

- Finned Tubes

U-tubes exhibits a clear dominance with a 40% share of the total Saudi Arabia heat exchanger tubes market in 2025.

U-tubes represent the largest segment attributed to their efficiency in handling thermal expansion and high temperature variations. This design allows the tubes to expand and contract without causing excessive stress, making them suitable for demanding industrial environments. U-tube heat exchangers are widely used in oil and gas processing, petrochemical plants, and power generation facilities where reliability and durability are critical. Their compact structure and ability to accommodate pressure changes support strong adoption across the Kingdom.

The dominance of U-tubes is further reinforced by their cost effectiveness and ease of maintenance compared to more complex configurations. The design enables simpler tube bundle replacement and improved cleaning access on the shell side, which is important in industries dealing with fouling fluids. Saudi Arabia’s large scale industrial base requires efficient heat transfer systems with long operational life, and U-tube configurations provide a practical solution. As energy and industrial investments continue, demand for U-tube heat exchanger components remains strong.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Direct Sales

- Distributors and Suppliers

Direct sales dominate with a market share of 56% of the total Saudi Arabia heat exchanger tubes market in 2025.

Direct sales dominate the market because of the highly specialized nature of industrial procurement and the need for customized engineering solutions. Major end users, such as oil and gas companies, petrochemical plants, power utilities, and desalination operators, require heat exchanger tubes that meet strict technical specifications and regulatory standards. Direct engagement with manufacturers ensures quality assurance, accurate material selection, and timely delivery for large scale projects. This channel also supports long term supply contracts and reliable after sales service.

The dominance of direct sales is further influenced by the complexity and critical importance of heat exchanger systems in Saudi Arabia’s industrial operations. Buyers prioritize direct sourcing to reduce procurement risks, ensure compliance with performance standards, and secure technical support during installation and maintenance. Direct sales channels also enable manufacturers to provide tailored solutions, pricing transparency, and project specific documentation. As industrial investments expand and demand for high performance heat exchanger tubes grows, direct sales remain the preferred distribution channel in the market.

End Use Industry Insights:

- Power Generation

- Oil and Gas

- Chemical and Petrochemical

- HVAC and Refrigeration

- Food and Beverage Processing

- Automotive and Aerospace

- Marine and Shipbuilding

- Pharmaceuticals

- Others

Oil and gas lead with a market share of 24% of the total Saudi Arabia heat exchanger tubes market in 2025.

Oil and gas hold the biggest market share driven by the Kingdom’s dominant position as a global energy producer and the extensive use of heat exchange systems across upstream, midstream, and downstream operations. Refineries, gas processing plants, and petrochemical complexes require high performance tubes to manage heating, cooling, and condensation processes under extreme pressure and temperature conditions. Heat exchanger tubes are essential for ensuring process efficiency, operational safety, and continuous production in energy facilities, making oil and gas the largest contributor.

The dominance of the oil and gas sector is further supported by continuous investments in refinery expansion, downstream diversification, and gas development projects. Heat exchangers are essential for controlling thermal processes in crude distillation, LNG processing, and chemical conversion units, where operational reliability is critical. This demand is reinforced by major upstream progress, as in 2025 Saudi Arabia brought the first phase of the Jafurah gas project onstream, marking a significant milestone in its gas expansion strategy. Such developments increase the need for durable stainless steel and seamless tube solutions capable of withstanding harsh operating conditions.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

Northern and Central Region exhibits a clear dominance with a 30% share of the total Saudi Arabia heat exchanger tubes market in 2025.

Northern and Central Region lead the market due to their high concentration of industrial activity, energy infrastructure, and large-scale processing facilities. These regions host major oil and gas operations, petrochemical complexes, power generation plants, and industrial cities that require extensive heat exchange systems. The presence of refineries, manufacturing clusters, and utility projects drives consistent demand for high performance heat exchanger tubes. Strong industrial investment and proximity to key demand centers further support the regional dominance.

The leadership of Northern and Central Region is reinforced by ongoing expansion of industrial zones and national infrastructure development under Vision 2030. Large projects in these regions require reliable thermal management solutions for energy, water treatment, and manufacturing processes. Buyers in these areas prioritize durable materials and advanced tube configurations to meet harsh operating conditions. Established supply networks and direct procurement channels also strengthen market activity, positioning the segment as the primary hubs for heat exchanger tube demand.

Market Dynamics:

Growth Drivers:

Why is the Saudi Arabia Heat Exchanger Tubes Market Growing?

Water Desalination and Treatment Sector Requirements

Saudi Arabia’s strong reliance on desalination for freshwater supply is catalyzing the demand for heat exchanger tubes in thermal desalination facilities. Processes such as multi-stage flash and multi-effect distillation require efficient heat exchange systems to ensure reliable water production under high salinity and elevated temperature conditions. This demand is reinforced by ongoing infrastructure expansion, as in 2025 the National Water Company began pumping desalinated drinking water to the Al-Murouj District in Al-Qurayyat, extending networks by over 7,000 meters and supplying around 1,000 cubic meters per day to benefit more than 1,600 residents. As desalination capacity continues to grow, there is a higher demand for corrosion-resistant tubing solutions.

Expansion of Mining and Mineral Processing Activities

The robust mining sector in Saudi Arabia is increasingly contributing to demand for heat exchanger tubes, as mineral extraction and processing activities rely heavily on effective thermal regulation. Mining operations require robust heating and cooling systems to support extraction, refining, and material handling under harsh operating conditions, where equipment reliability is critical. This momentum is reinforced by policy support, as in 2026 Saudi Arabia launched the third round of its Mining Exploration Enablement Program to accelerate mineral exploration and attract both local and international investors. As mining projects scale up and downstream processing capacity grows, there is a rise in the demand for heavy-duty, corrosion-resistant heat exchanger tubes that ensure operational efficiency, equipment protection, and long service life.

Technological Advancements in Materials and Tube Manufacturing

Innovation in tube manufacturing and material science is significantly driving the adoption of advanced heat exchanger tubes in Saudi Arabia. Industrial sectors increasingly require tubing solutions that offer superior resistance to corrosion, high pressure, and extreme operating temperatures. The growing use of improved alloys, advanced welding methods, and precision-engineered production techniques enhances tube durability, thermal efficiency, and long-term performance. As industrial operators place greater emphasis on reliability, reduced downtime, and lower maintenance expenditure, demand for high-quality heat exchanger tubes continues to rise. This trend is particularly evident across energy, petrochemical, desalination, and heavy industrial applications, supporting the market growth.

Market Restraints:

What Challenges the Saudi Arabia Heat Exchanger Tubes Market is Facing?

High Capital Investment Requirements for Large-Scale Projects

The substantial upfront costs associated with procuring specialized heat exchanger tubes for mega infrastructure projects create financial barriers, particularly for smaller industrial operators and municipalities. High-specification materials, such as nickel alloys and titanium, command significant price premiums, limiting their adoption to critical applications and constraining broader market penetration across cost-sensitive segments.

Import Dependency and Supply Chain Vulnerabilities

Despite the growing localization efforts, Saudi Arabia continues to rely heavily on imported heat exchanger tubes for specialized grades and configurations not yet manufactured domestically. This dependency exposes procurement timelines to international supply chain disruptions, shipping delays, and currency fluctuations, creating uncertainty for project planning and potentially increasing overall equipment costs for end users.

Limited Availability of Specialized Technical Workforce

The installation, maintenance, and inspection of heat exchanger systems require highly trained technical personnel with expertise in metallurgy, welding, and non-destructive testing. The limited availability of specialized workforce within the kingdom creates operational challenges, increases project execution timelines, and drives up labor costs for industrial operators managing complex heat exchange infrastructure.

Competitive Landscape:

The Saudi Arabia heat exchanger tubes market exhibits a moderately consolidated competitive structure, with established global manufacturers competing alongside emerging regional producers. Market participants are differentiating through material innovation, production capacity expansion, and alignment with localization mandates under the national industrial development program. Strategic partnerships between international tube manufacturers and local industrial investment entities are reshaping competitive dynamics, enabling technology transfer and domestic production capabilities. Companies are increasingly investing in advanced manufacturing processes, quality certifications, and supply chain integration to secure contracts for mega projects across petrochemical, desalination, and energy infrastructure sectors.

Saudi Arabia Heat Exchanger Tubes Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Material Types Covered | Stainless Steel, Carbon Steel, Copper and Copper Alloys, Nickel Alloys, Titanium, Others |

| Product Types Covered | Seamless Heat Exchanger Tubes, Welded Heat Exchanger Tubes |

| Tube Configurations Covered | U-Tubes, Straight Tubes, Finned Tubes |

| Distribution Channels Covered | Direct Sales, Distributors and Suppliers |

| End Use Industries Covered | Power Generation, Oil and Gas, Chemical and Petrochemical, HVAC and Refrigeration, Food and Beverage Processing, Automotive and Aerospace, Marine and Shipbuilding, Pharmaceuticals, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Heat Exchanger Tubes Market Report

The Saudi Arabia heat exchanger tubes market size was valued at USD 195.4 Million in 2025.

The Saudi Arabia heat exchanger tubes market is expected to grow at a compound annual growth rate of 4.20% from 2026-2034 to reach USD 282.9 Million by 2034.

Stainless steel holds the largest revenue share of 35% in 2025, driven by superior corrosion resistance, high-temperature stability, and extensive application across petrochemical, desalination, and oil and gas sectors.

Key factors driving the Saudi Arabia heat exchanger tubes market include expanding infrastructure and construction activity, which is catalyzing the demand for HVAC, district cooling, and industrial thermal systems. This is reflected in projects such as the SAR 800 million Jeddah housing development announced in 2024, delivering over 1,000 units and requiring efficient heat transfer solutions.

Major challenges include high capital investment requirements for specialized materials, import dependency and supply chain vulnerabilities for advanced tube grades, limited availability of specialized technical workforce, and price volatility of raw materials.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade