Saudi Arabia Home Healthcare Market Size, Share, Trends and Forecast by Product and Service, Indication, and Region 2026-2034

Saudi Arabia Home Healthcare Market Size, Share, Trends & Forecast (2026-2034)

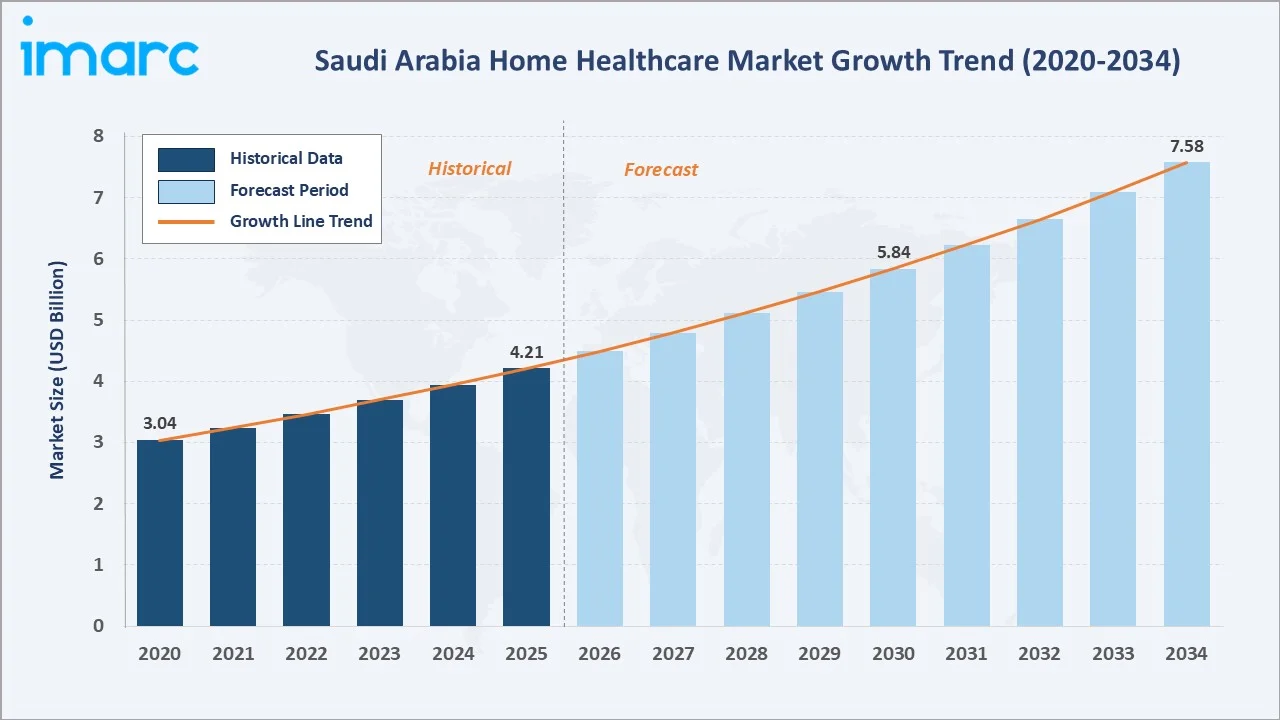

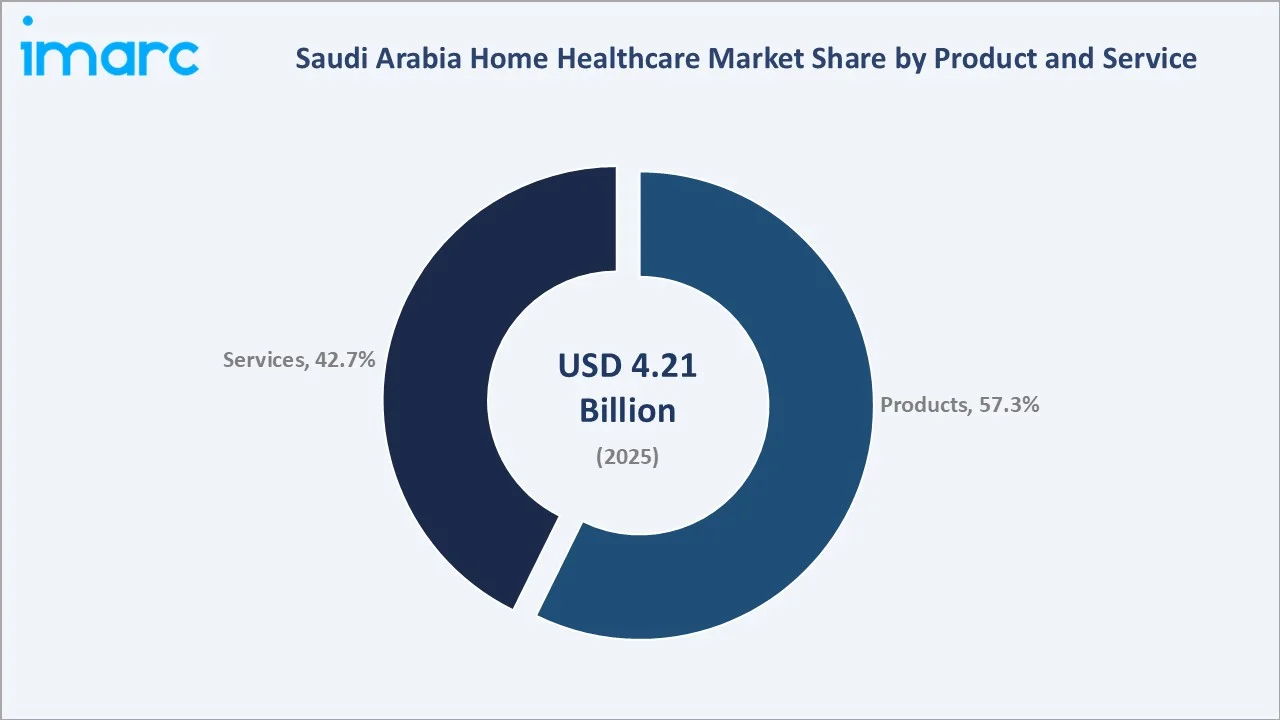

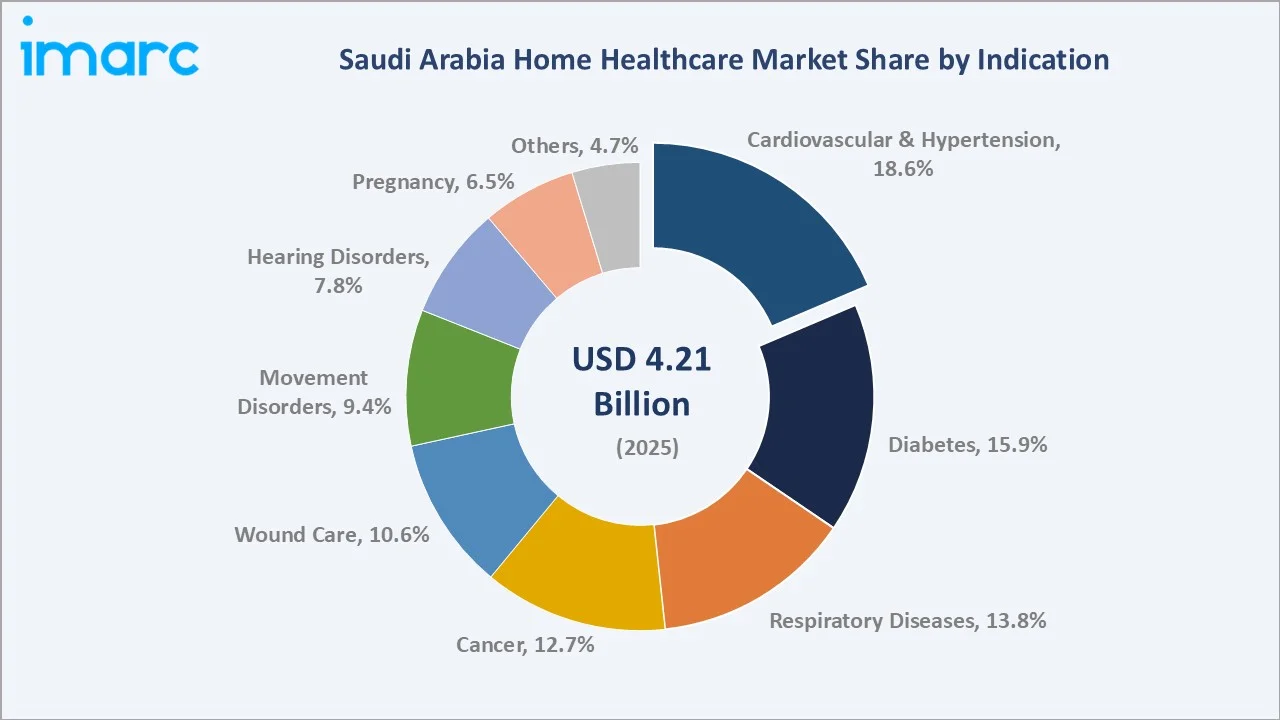

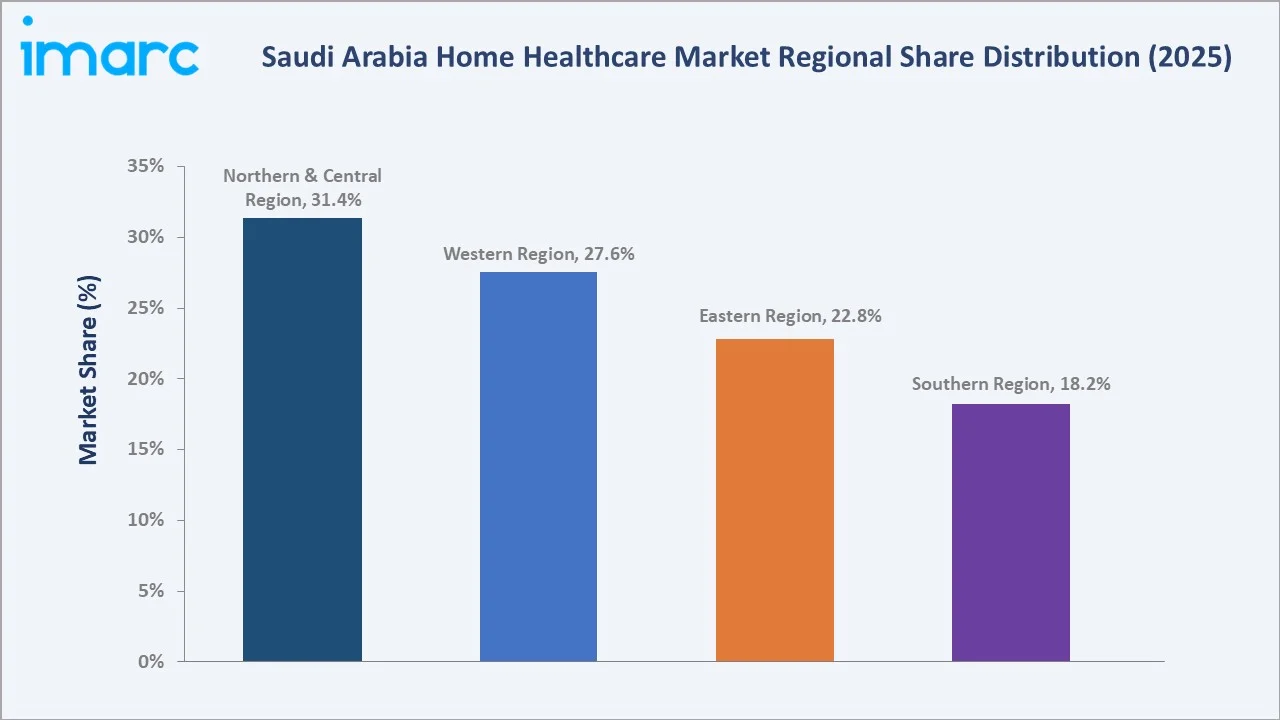

The Saudi Arabia home healthcare market was valued at USD 4.21 Billion in 2025 and is projected to reach USD 7.58 Billion by 2034, expanding at a CAGR of 6.75% during 2026-2034. Growth is anchored by Vision 2030’s healthcare privatization mandate, Saudi Arabia’s world-leading chronic disease burden with 5.3 million diabetes cases in 2024 and projected to 9.5 million cases by 2050, mandatory health insurance expansion, and the government’s objective to shift 30% of healthcare delivery from hospital to community settings. Products lead with 57.3% share, cardiovascular diseases and hypertension are the largest indications at 18.6%, and the Northern & Central Region dominates at 31.4%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.21 Billion |

|

Forecast Market Size (2034) |

USD 7.58 Billion |

|

CAGR (2026-2034) |

6.75% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

Northern & Central Region (31.4%, 2025) |

|

Fastest Growing Region |

Western Region (CAGR ~7.2%, 2026-2034) |

The Saudi Arabia home healthcare market grew from USD 3.04 Billion in 2020 to USD 4.21 Billion in 2025, underpinned by COVID-19-driven acceleration in remote care adoption, post-pandemic normalization of telehealth consultations, and the Saudi Ministry of Health's systematic push to shift non-critical care from overburdened hospitals to home settings under the National Transformation Program. Anchored at USD 5.84 Billion in 2030, the market is forecast to reach USD 7.58 Billion by 2034, driven by Vision 2030 healthcare privatization, an expanding elderly population, and increasing household investment in chronic disease management.

To get more information on this market, Request Sample

The 6.75% CAGR reflects structural demand fundamentals: Saudi Arabia's diabetes prevalence at 23.1% of the adult population, cardiovascular disease burden driving sustained home monitoring adoption, and the government's Vision 2030 commitment to increase private sector healthcare participation by 2030, creating favorable conditions for private home healthcare operators to scale service delivery.

Executive Summary

The Saudi Arabia home healthcare market grew from USD 3.04 Billion in 2020 to USD 4.21 Billion in 2025, driven by COVID-19’s permanent restructuring of Saudi care delivery preferences, Vision 2030 Health Sector Transformation Program’s systematic hospital bed decongestion strategy, and mandatory health insurance expansion under CCHI that brought home healthcare reimbursement coverage to previously uninsured workers.

Saudi Arabia’s chronic disease epidemiological crisis creates the world’s most compelling home healthcare demand case among upper-middle-income markets: a 23.1% adult diabetes prevalence rate, hypertension prevalence requiring continuous blood pressure monitoring and medication management, and adult obesity rate creating a complex comorbidity burden that makes long-term hospital-based chronic disease management both clinically suboptimal and financially unsustainable. The market’s forecast path to USD 7.58 Billion by 2034 at 6.75% CAGR reflects Vision 2030’s target of private sector healthcare delivery by 2030, the National Health Insurance Scheme (NHIS) expansion mandating home healthcare benefit inclusion, and Saudi Arabia’s rapidly digitalizing healthcare system.

Products lead at 57.3%, encompassing home medical devices (glucometers, continuous glucose monitors, blood pressure monitors, home oxygen concentrators, CPAP/BiPAP machines), wound care products, mobility aids, and pharmaceutical home delivery. Cardiovascular diseases and hypertension lead indication share at 18.6%, reflecting Saudi Arabia’s hypertensive adults, while diabetes at 15.9% represents the fastest-growing indication as Saudi Arabia’s diabetics require continuous glucose monitoring, insulin management, and foot care that are systematically transitioning from clinic-based to home-based delivery. The Northern & Central Region’s 31.4% dominance reflects Riyadh’s 8.2 million population concentration and Vision 2030’s health investment prioritization of the capital.

Key Market Insights

|

Insight |

Data |

|

Dominant Product and Services Segment |

Product – 57.3% revenue share (2025) |

|

Dominant Indication |

Cardiovascular Diseases & Hypertension – 18.6% (2025) |

|

Leading Region |

Northern & Central Region – 31.4% share (2025) |

|

Fastest Growing Region |

Western Region (CAGR ~7.2%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Product segment at 57.3% driven by Saudi Arabia’s home medical device adoption: Saudi Arabia’s mandatory health insurance under CCHI covers home medical devices, including blood glucose monitors, continuous glucose monitoring systems, home blood pressure monitors, and nebulizers for covered insured patients.

- Cardiovascular diseases at 18.6% reflecting Saudi Arabia’s hypertension and heart disease burden: Saudi Arabia with over 5.1 million adults aged 30–79 years with hypertension places it among the world’s highest-prevalence countries for cardiovascular risk, requiring systematic home blood pressure monitoring, antihypertensive medication adherence programs, and cardiac rehabilitation home visits for post-MI and post-CABG patients.

- Northern & Central at 31.4% anchored by Riyadh’s healthcare infrastructure and Vision 2030: Riyadh’s 8.2 million population, served by hospitals, generates Saudi Arabia’s largest hospital discharge volume, with Vision 2030’s target of reducing average length of hospital stay systematically increasing home healthcare referral volumes per discharge.

Saudi Arabia Home Healthcare Market Overview

Saudi Arabia’s home healthcare market encompasses the full spectrum of professional healthcare products and services delivered to patients in their home environments, ranging from home medical devices and pharmaceutical products to skilled nursing visits, rehabilitation therapy, and complex clinical services such as home infusion therapy and palliative care. The ecosystem integrates global medical device manufacturers, licensed home healthcare service providers, digital health and telehealth platforms, and insurance payers under regulatory oversight from the Ministry of Health (MoH), Saudi Food and Drug Authority (SFDA), and Council of Cooperative Health Insurance (CCHI).

Applications span chronic disease management (diabetes, cardiovascular disease, COPD), post-acute hospital discharge care (surgical wound care, rehabilitation, IV antibiotics), palliative and hospice care, maternal and neonatal home care, and preventive health monitoring for high-risk populations. Saudi Arabia’s macroeconomic context, Vision 2030’s public and private healthcare expenditures in 2025 are SAR 250 billion, representing 6% of national GDP, mandatory health insurance, an expanding private healthcare sector, and Saudi Arabia’s population with one of the chronic disease burdens, creates the structural demand environment for sustained home healthcare market growth.

Market Dynamics

To evaluate market opportunities, Request Sample

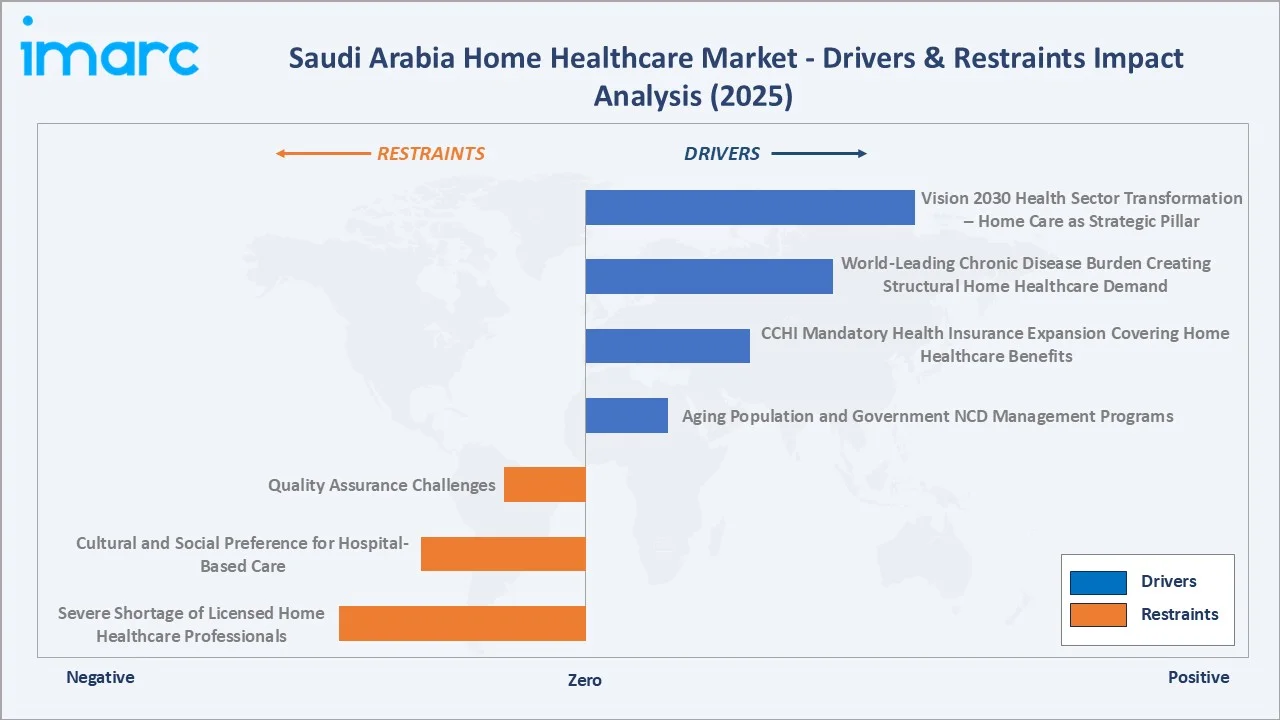

Market Drivers

- Vision 2030 Health Sector Transformation: Home Care as Strategic Pillar: Saudi Arabia’s Vision 2030 Health Sector Transformation Program (HSTP) has identified home healthcare as a critical component of its hospital bed decongestion and healthcare cost sustainability strategy.

- World-Leading Chronic Disease Burden Creating Structural Home Healthcare Demand: Saudi Arabia’s chronic disease epidemiology with 5.3 million diabetes cases in 2024 and projected 9.5 million diabetes cases by 2050, over 5.1 million adults aged 30–79 years with hypertension, and 23.5% women and 22.8% men with obesity, creates a patient population where adults require systematic ongoing disease management that is more efficiently delivered at home than in hospital outpatient clinics.

- CCHI Mandatory Health Insurance Expansion Covering Home Healthcare Benefits: CCHI’s progressive mandatory health insurance expansion, including expatriate workers under employer-mandated policies, has created the financial infrastructure for home healthcare market growth.

- Aging Population and Government NCD Management Programs: Saudi Arabia’s population ages 65 and above was reported at 2.9508 % in 2024, the fastest demographic segment in the kingdom, creating an expanding elderly home healthcare demand base for skilled nursing, physiotherapy, dementia care, and fall prevention programs.

Market Restraints

- Severe Shortage of Licensed Home Healthcare Professionals: Saudi Arabia’s home healthcare sector faces a critical clinical workforce constraint. Saudi Arabia’s healthcare workforce is predominantly expatriate, creating visa processing delays, Saudization pressure, and workforce turnover rates that constrain home healthcare provider expansion capacity.

- Cultural and Social Preference for Hospital-Based Care: Saudi Arabia’s healthcare culture historically equates quality care with hospital-based inpatient treatment, a preference reinforced by decades of government-funded free inpatient care and high hospital bed availability ratios.

Market Opportunities

- Vision 2030 Mega Projects Generating Premium Home Healthcare Demand: NEOM’s The Line and Diriyah Gate Authority’s luxury residential development will create new premium home healthcare demand clusters in Saudi Arabia’s planned smart city environments. NEOM’s health sector plan includes a comprehensive home healthcare program as standard residential service for The Line’s residents, creating a greenfield high-income home healthcare market.

- Saudization of Home Healthcare Workforce Creating Local Talent Pipeline: Saudi Arabia’s Vision 2030 Saudization of healthcare target is creating a domestic clinical workforce pipeline that reduces home healthcare’s dependence on volatile expatriate recruitment.

Market Challenges

- Quality Assurance Across Geographically Dispersed Home Settings: Home healthcare quality assurance is inherently more complex than hospital-based care: clinical supervisors cannot directly observe home nurses’ and therapists’ patient interactions, infection control compliance in home settings varies dramatically between patient households, and family caregiver training completion rates for care plan compliance in Saudi home healthcare programs.

- Limited Home Healthcare-Specific Clinical Training Programs: Saudi Arabia lacks dedicated home healthcare clinical training programs at the undergraduate and continuing education levels, with nursing graduates being trained for hospital environments rather than home settings.

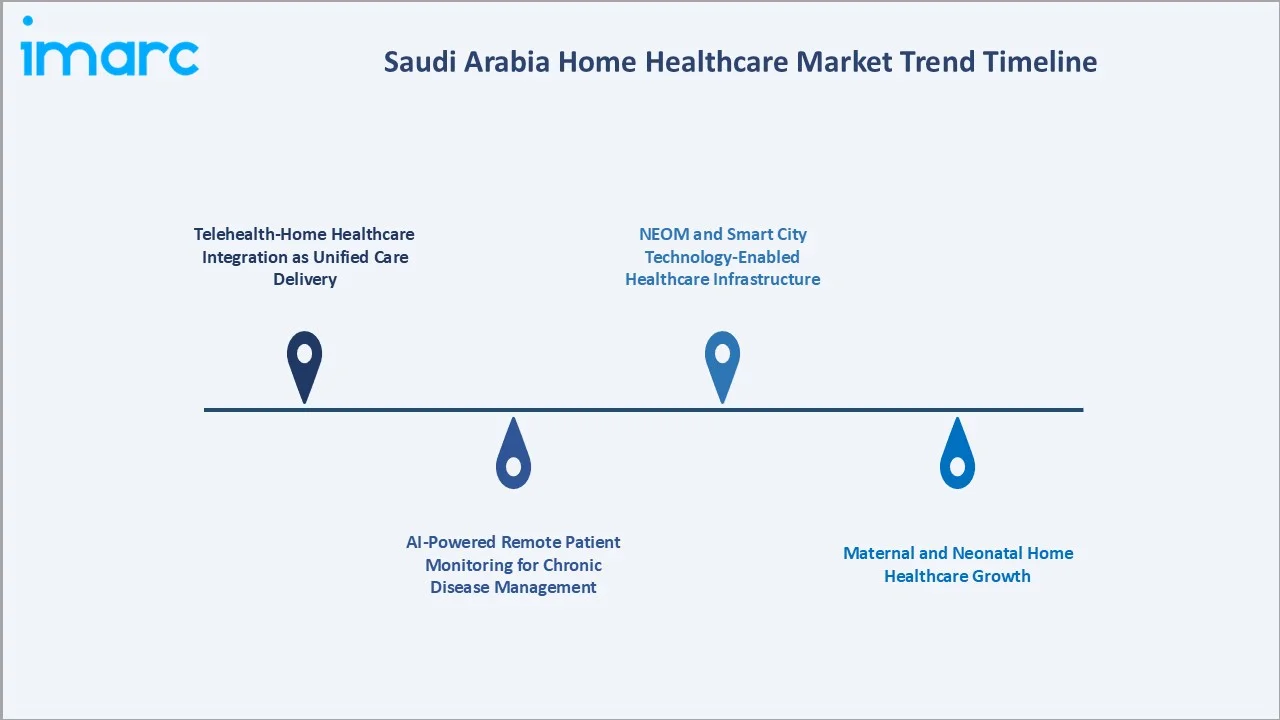

Emerging Market Trends

1. Telehealth-Home Healthcare Integration as Unified Care Delivery

Saudi Arabia’s Seha Virtual Hospital is being integrated with licensed home healthcare providers to create a digitally-supervised home care model. Under this model, home nurses and therapists conduct physical care while connected via video consultation to specialist physicians, enabling physician-level clinical supervision during home nursing visits without requiring physical physician travel.

2. AI-Powered Remote Patient Monitoring for Chronic Disease Management

Saudi Arabia’s massive chronic disease burden is driving rapid adoption of AI-powered remote patient monitoring (RPM) systems that collect continuous home health data and generate automated care alerts for clinical teams.

3. Maternal and Neonatal Home Healthcare Growth Under Vision 2030 Family Policy

Saudi Arabia’s national fertility rate of 2.15 in 2024, combined with Vision 2030’s family support policy, is driving demand for professional home maternal and neonatal care.

4. NEOM and Smart City Projects Creating Technology-Enabled Home Healthcare Infrastructure

NEOM’s digital-first health system design, incorporating IoT-enabled smart home health monitoring as standard residential infrastructure, will create Saudi Arabia’s first purpose-built technology-integrated home healthcare environment.

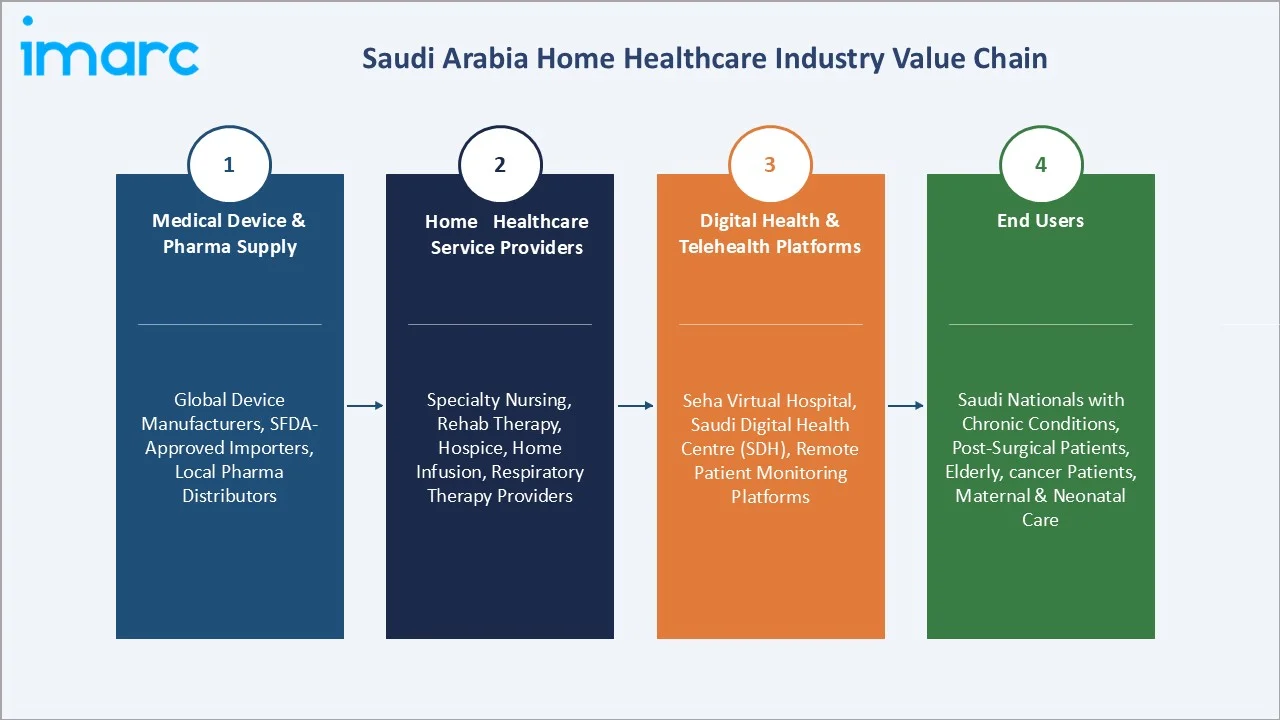

Industry Value Chain Analysis

Saudi Arabia’s home healthcare value chain spans global medical device and pharmaceutical supply through licensed home healthcare service delivery, digital health platforms, insurance payers, and patient end users, under regulatory governance from MoH, SFDA, CCHI, and CBAHI.

|

Stage |

Key Participants |

|

Medical Device & Pharmaceutical Supply |

Global medical device manufacturers with Saudi operations, local pharmaceutical distributors, and Saudi Food and Drug Authority (SFDA)-approved home medical device importers |

|

Home Healthcare Service Providers |

Specialty home nursing providers; rehabilitation therapy agencies; hospice and palliative care providers; physiotherapy and occupational therapy home visit agencies; home infusion therapy providers; respiratory therapy home service companies |

|

Digital Health & Telehealth Platforms |

Seha Virtual Hospital; Saudi Digital Health Center (SDH) national EHR integration; remote patient monitoring platforms integrating wearables with home healthcare nurse dashboards |

|

End Users |

Saudi nationals with chronic conditions, post-surgical home recovery patients discharged from public and private hospitals; elderly population; cancer patients receiving home chemotherapy or palliative care; maternal and neonatal care at home; COPD and asthma patients on home oxygen and nebulizer therapy; expatriate community requiring home healthcare covered by employer insurance |

Home healthcare service providers capture the highest per-patient-episode revenue: they generate significantly higher per-service revenue than comparable hospital outpatient visits. The most strategically valuable position in Saudi Arabia’s home healthcare value chain is the integrated provider that combines product supply with clinical service delivery, as demonstrated by HHC and Bayader’s model of pairing durable medical equipment provision with clinical nursing services per patient episode.

Technology Landscape in the Saudi Arabia Home Healthcare Industry

Telehealth and AI-Assisted Clinical Decision Support

AI triage systems use machine learning severity scoring to prioritize acute home patient consultations with appropriate specialist physicians within less time. Integrating with home healthcare providers’ care management systems, enabling home nurses to consult supervising physicians via secure video during complex home wound care or IV therapy procedures.

Home Infusion and Clinical Therapy Technology

Spectrum infusion pumps enable safe IV drug administration by trained nurses in home settings with integrated drug library guardrails preventing dosing errors. The home infusion system with RFID medication traceability tracks the IV medication preparation-to-administration chain in home settings to international pharmacy practice standards.

Digital Care Management and EHR Integration

Saudi Arabia’s NHIC (National Health Information Center)’s Unified National Health System (UNHS) is progressively integrating licensed home healthcare providers as data contributors and consumers. When fully integrated, home healthcare nurses will access patients’ complete inpatient discharge summaries, medication histories, imaging results, and laboratory data in real time, eliminating the clinical information gaps that currently create patient safety risks in home settings.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Product and Service | Product | 57.3% |

2025 |

| Indication | Cardiovascular Diseases and Hypertension | 18.6% |

2025 |

| Region | Northern and Central Region | 31.4% |

2025 |

By Product and Service

Products lead at 57.3% market share (2025). The product category encompasses three primary sub-segments: Therapeutic Products (home medical devices for treatment delivery-insulin pumps, nebulizers, CPAP/BiPAP machines, home oxygen concentrators, IV infusion pumps); Testing, Screening, and Monitoring Products (diagnostic and monitoring devices for home use- glucometers, CGM systems, blood pressure monitors, pulse oximeters, cardiac monitors); and Mobility Care Products (wheelchairs, walking aids, patient lifts, hospital beds, bathroom safety equipment for home use).

To access detailed market analysis, Request Sample

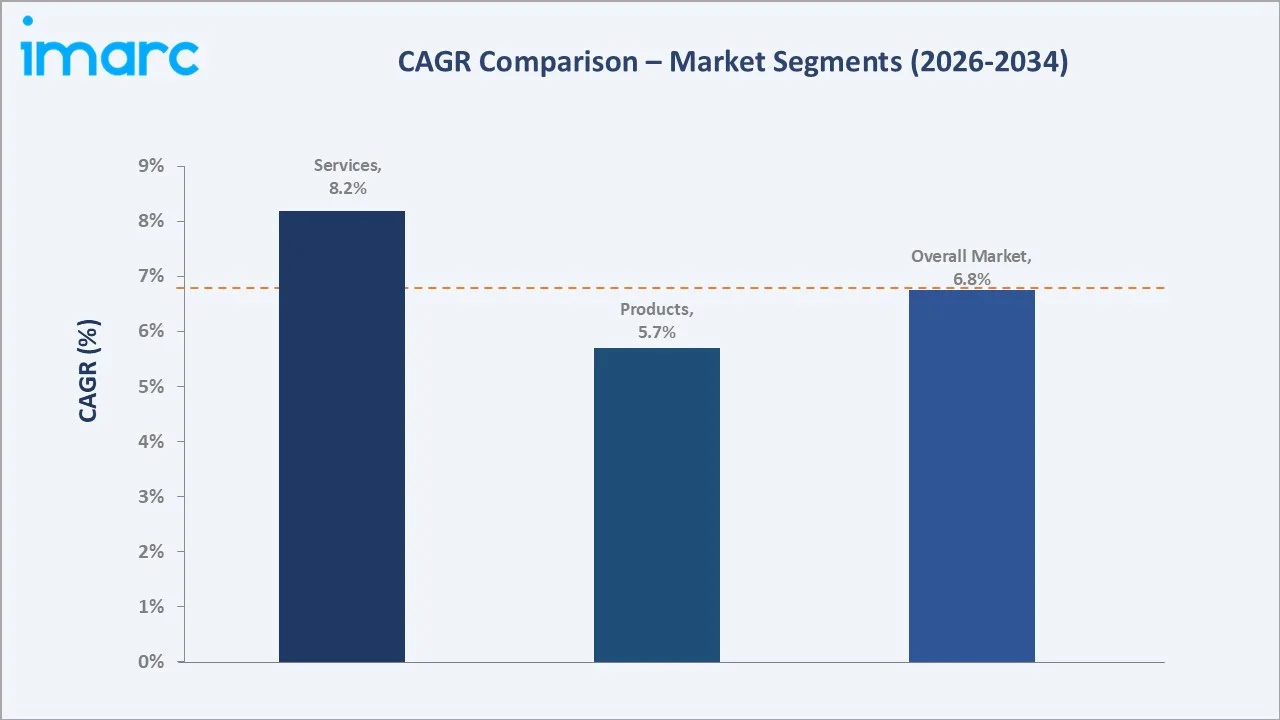

Services at 42.7% (USD 1.80 billion) are growing at ~8.2% CAGR, the fastest market segment, as CCHI benefits expansion progressively converts home service delivery from private-pay to insurance-reimbursed. Skilled nursing is the dominant service sub-segment, followed by rehabilitation therapy, home infusion therapy, and hospice and palliative care.

By Indication

Cardiovascular diseases and hypertension lead at 18.6%, reflecting Saudi Arabia’s 5.1 million adults aged 30–79 years with hypertension, 1.6% overall prevalence of CVDs, with 1.9% among males and 1.4 among females, constituting the largest home product category.

Cancer at 12.7% is growing at 9‑10% CAGR as KFSH&RC and the Saudi Oncology Society’s home chemotherapy and palliative care programs expand nationally. Wound care at 10.6%, movement disorders at 9.4%, hearing disorders at 7.8%, pregnancy at 6.5%, and others at 4.7% collectively represent the market’s remaining indication distribution, with movement disorder home physiotherapy and maternal home care growing above the market CAGR as Vision 2030’s family health programs and elderly care strategies accelerate their respective demand categories.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Northern & Central Region |

31.4% |

Riyadh city’s 8.2 million population is Saudi Arabia’s largest urban concentration, driving the highest absolute home healthcare demand nationally |

|

Western Region |

27.6% |

Jeddah and Makkah-Madinah’s religious tourism economy is creating permanent resident and seasonal home healthcare demand |

|

Eastern Region |

22.8% |

Dammam-Al Khobar-Dhahran metropolitan cluster with Saudi Aramco’s world-class employee health insurance program covering comprehensive home healthcare for ARAMCO employees and dependents |

|

Southern Region |

18.2% |

Asir, Jizan, Najran, and Al Baha regions’ rapidly expanding government healthcare infrastructure under Vision 2030 rural health development program |

The Northern & Central Region’s 31.4% dominance is structural: Riyadh’s 8.2 million population generates the nation’s highest discharge-to-home-healthcare referral volume. Vision 2030’s capital city investment concentration is driving population growth, systematically expanding the region’s addressable home healthcare market.

The Western Region’s 27.6% with the fastest regional CAGR (~7.2%) reflects Jeddah’s position as Saudi Arabia’s commercial capital and the Holy Cities’ permanent resident community’s home healthcare demand. The Eastern Region’s 22.8% is anchored by Saudi Aramco’s comprehensive employee health insurance program covering employees and dependents with some of Saudi Arabia’s most generous home healthcare benefits.

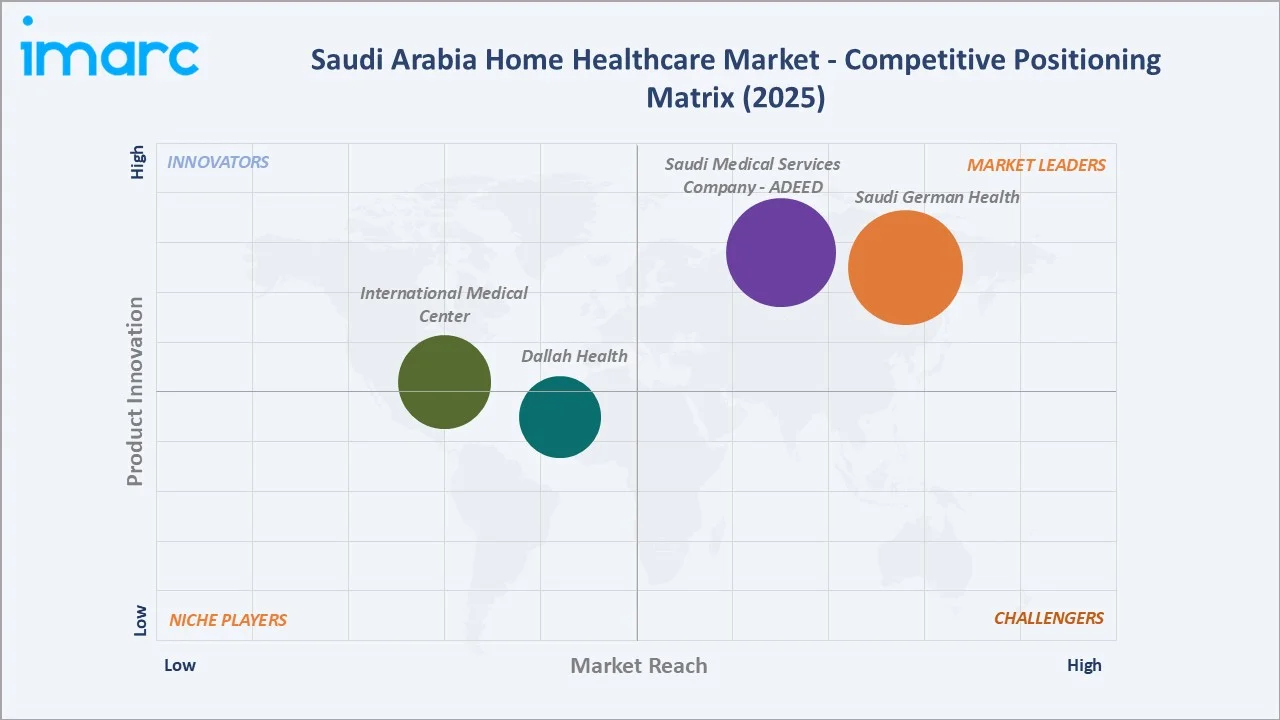

Competitive Landscape

Saudi Arabia’s home healthcare market is moderately concentrated among CBAHI-accredited licensed providers and highly fragmented among the broader universe of registered home healthcare agencies.

|

Company Name |

Services |

Market Position |

Core Strength |

|

Saudi German Health |

Elderly Care, Pediatric Care, Alzheimer's Care, Post-Surgery Care, Chronic Condition Care, Pre- and Postnatal Care, Care for All Ages |

Market Leader |

Saudi German Health’s bed hospitals generate continuous post-discharge home healthcare referrals across the Saudi market |

|

Saudi Medical Services Company - ADEED |

Nursing Services, Care Assistant, Doctor Visit at Home, Physiotherapy at Home, Dietician Services, Lab Test at home, Medical Transfer Services |

Market Leader |

ADEED is recognised as a modern business model within the Saudi Arabian home healthcare market, offering a wide range of at-home medical services. |

|

Dallah Health |

Physical Therapy, Nursing Services, Lab Services, Home Hemodialysis, Vaccinations, Mother and Child Care, Radiology, and Care Giver |

Established |

Riyadh-headquartered listed Saudi healthcare company operating Dallah Hospital as one of Riyadh’s largest private hospitals with dedicated home healthcare subsidiary |

|

International Medical Center |

Home Nursing Services, Geriatric assessment Package, Home Hemodialysis, Urinary Catheterization, Home care for Tracheostomy Change/Care, Home care for Wound Dressing and Suture Removal |

Established |

Jeddah-headquartered JCI-accredited hospital group with a home healthcare division serving the Western Region’s expatriate and Saudi national community |

The top four providers collectively represent an estimated 35–40% of the organized home healthcare service market. This moderate concentration reflects the market’s geographic distribution across Saudi Arabia’s administrative regions and the licensed provider requirement that prevents unregistered operators from participating in CCHI-reimbursed care, creating barriers to informal market entry while allowing regional specialists to thrive.

Key Company Profiles

Saudi German Health

Saudi German Health is the Saudi operations, operating around seven Saudi German Hospitals across the region with dedicated home healthcare service arms in Jeddah, Riyadh, Aseer, Dammam, Madinah, Makkah, and Hail. Saudi German Health’s multi-city hospital network generates consistent home healthcare referral volumes across its Saudi hospital system.

- Service Portfolio: Elderly Care, Pediatric Care, Alzheimer's Care, Post-Surgery Care, Chronic Condition Care, Pre- and Postnatal Care, Care for All Ages.

- Recent Developments: Saudi German Health Riyadh launched hospital-to-home oncology care pathway for cancer patients receiving oral chemotherapy, enabling home monitoring by oncology-trained nurses with weekly telehealth check-ins with SGH Riyadh oncologists.

- Strategic Focus: Hospital-home care integration as core competitive advantage, SGH home care teams embedded within hospital discharge planning processes, creating seamless patient transitions; digital health platform as family engagement and clinical quality monitoring tool.

Saudi Medical Services Company - ADEED

ADEED (Saudi Medical Services Company) is a Riyadh-based home healthcare provider operating as a modern home medical services model in the Saudi market. Licensed by the Ministry of Health and aligned with Vision 2030's goal of reducing hospital bed occupancy by shifting suitable cases to home-based care, ADEED delivers integrated at-home medical services 24/7, supported by qualified clinical staff held to the same quality standards as hospital and healthcare facilities.

- Service Portfolio: Nursing Services, Care Assistant, Doctor Visit at Home, Physiotherapy at Home, Dietician Services, Lab Test at home, Medical Transfer Services.

- Recent Developments: In March 2025, ADEED Medical Services Company announced its achievement of the Joint Commission International (JCI) accreditation for Excellence in Home Healthcare.

- Strategic Focus: Vision 2030-aligned hospital-to-home care transition as core value proposition; JCI and CBAHI dual accreditation as key quality differentiator; digital platform as patient engagement and operational efficiency driver; comprehensive service bundling, spanning clinical, rehabilitative, diagnostic, and personal care, to serve as a single-provider home health solution for families across all age groups.

Market Concentration Analysis

Saudi Arabia’s home healthcare market is moderately concentrated at the service provider tier and fragmented at the product distribution level. CBAHI-accredited home healthcare service providers account for approximately 70‑75% of the insurance-reimbursable home service market, with the top four providers representing 35‑40% of this organized market. The remaining 25‑30% is distributed across registered home healthcare agencies with varying service scopes, accreditation levels, and geographic coverage.

The product distribution tier is more fragmented: SFDA-licensed home medical device distributors number nationally, with no single distributor controlling more than 15% of total home device volume. International brands command market share through exclusive Saudi agency agreements rather than direct distribution, creating a layer of Saudi distributor intermediaries whose market position depends on exclusive supply agreement renewals rather than operational competitiveness.

Investment & Growth Opportunities

Fastest Growing Segments

Service segment (~8.2% CAGR), Western Region (~7.2% CAGR), home infusion therapy sub-segment (~12‑15% CAGR), telehealth-integrated remote patient monitoring (~25‑30% CAGR from 2025 base), and cancer indication (~9‑10% CAGR) represent Saudi Arabia’s highest-growth home healthcare investment vectors.

Emerging Market Opportunities

NEOM’s resident target by 2030 creates a greenfield premium home healthcare market requiring smart home health monitoring infrastructure, concierge physician home visit programs, and AI-assisted remote disease management. Southern Region’s below-average home healthcare penetration represents a structural expansion opportunity as Vision 2030’s rural health equity investments improve Southern Region infrastructure and insurance coverage.

Investment Themes

Vision 2030’s Healthcare Transformation Fund, Saudi Aramco’s Wa’ed venture arm, Sanabil Investments, and international healthcare PE are actively seeking Saudi home healthcare investment opportunities as the regulatory environment matures.

- Key technology investment areas: AI-powered remote patient monitoring platforms, SFDA-compliant connected home medical devices for CGM and cardiac monitoring, telehealth-home care integrated platforms meeting NHIC interoperability standards, CBAHI accreditation support software, and Arabic-language care management applications for home healthcare workflows.

- Workforce development investment: HRDF-supported home healthcare training centers, Saudi nursing school curriculum development for home care specialty, home healthcare aide Saudization programs, physiotherapy and occupational therapy home care specialty certification, and Arabic-language online continuing education for home healthcare professionals.

Future Market Outlook (2026-2034)

Saudi Arabia’s home healthcare market is entering its most consequential transformation phase, not merely growing in volume, but structurally repositioning from a supplementary care option for wealthy Saudis to an integral component of the national healthcare delivery architecture. From USD 4.21 Billion in 2025, the market will reach USD 7.58 Billion by 2034, at a steady 6.75% CAGR that reflects the controlled, policy-anchored pace of a healthcare sector transformation program rather than the volatile demand cycles of technology-driven markets.

Vision 2030’s healthcare transformation creates three non-negotiable demand drivers that guarantee this growth: the hospital average length of stay target creates structural demand for post-acute home care that cannot be met within hospital walls; CCHI’s progressive benefit expansion mandates create the insurance reimbursement infrastructure that makes home healthcare financially accessible to Saudi Arabia’s insured lives; and the National Health Insurance Scheme’s planned expansion to Saudi nationals will add additional covered lives to the home healthcare reimbursement ecosystem by 2027.

Research Methodology

Primary Research

Primary research included structured interviews with 120+ industry stakeholders in 2025, comprising home healthcare company executives, CBAHI accreditation officers, CCHI home healthcare benefit policy teams, Saudi MoH Health Sector Transformation Program representatives, SFDA medical device division officials, hospital discharge coordinators at King Faisal Specialist Hospital and King Fahd Medical City, and insurance medical directors at Bupa Arabia and Tawuniya.

Secondary Research

Secondary research encompassed the Saudi Ministry of Health Health Yearbook 2024, CCHI Annual Reports and benefit circulars, SFDA Medical Device Market Reports, CBAHI home healthcare accreditation database, Saudi Commission for Health Specialties (SCFHS) workforce statistics, Saudi Center for Disease Prevention and Control (SCDC) NCD prevalence data, Vision 2030 Health Sector Transformation Program progress reports, company financial disclosures, and IMARC healthcare industry databases. Over 160 secondary sources were reviewed.

Forecasting Models

Forecasts were developed using a bottom-up patient population × service utilization rate × average episode cost model, segmented by indication, product/service type, and region, validated against top-down healthcare expenditure models. Key inputs include Vision 2030 hospital length of stay targets, CCHI benefit expansion timelines, NHIS implementation schedule, Saudi population and disease prevalence projections, and licensed home healthcare provider capacity expansion plans.

Saudi Arabia Home Healthcare Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product and Services Covered |

|

| Indications Covered | Cancer, Respiratory Diseases, Movement Disorders, Cardiovascular Diseases and Hypertension, Pregnancy, Wound Care, Diabetes, Hearing Disorders, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Saudi German Health, Saudi Medical Services Company - ADEED, Dallah Health, International Medical Center, etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia home healthcare market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia home healthcare market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia home healthcare industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Home Healthcare Market Report

The Saudi Arabia home healthcare market was valued at USD 4.21 Billion in 2025 and is projected to reach USD 7.58 Billion by 2034.

The Saudi Arabia home healthcare market is forecast to grow at a CAGR of 6.75% during 2026-2034, driven by Vision 2030 healthcare privatization, chronic disease burden, and CCHI mandatory insurance expansion.

Products lead with 57.3% revenue share (2025), driven by CCHI-reimbursed home medical devices for Saudi Arabia’s diabetics, hypertensives, and COPD/sleep apnea patients.

Cardiovascular diseases and hypertension leads with 18.6% share (2025), reflecting Saudi Arabia’s hypertensive adults, heart failure patients, and large post-cardiac surgical home rehabilitation volume.

The Northern & Central Region leads with 31.4% share (2025), driven by Riyadh’s 8.2 million population, three major medical cities generating hospital discharges, and Vision 2030’s Riyadh investment concentration.

Key companies include Saudi German Health, Saudi Medical Services Company - ADEED, Dallah Health, and International Medical Center, among others.

Key drivers include Vision 2030 HSTP’s hospital LOS reduction targets, Saudi Arabia’s world-leading chronic disease burden, CCHI mandatory insurance home benefit expansion, aging population, and Seha Virtual Hospital’s telehealth integration.

Key trends include telehealth-home care integration (Seha Virtual Hospital), AI-powered remote patient monitoring, home infusion therapy CCHI benefit expansion, NEOM smart home health infrastructure, maternal home care growth, and Saudization of the clinical workforce.

Key challenges include a lower licensed professional shortage, cultural preference for hospital-based care, CCHI claim settlement delays, NHRA licensing compliance burden, and limited home healthcare-specific clinical training programs.

Top opportunities include NEOM smart home health infrastructure, home infusion therapy CCHI-reimbursed scale-up, Arabic-language remote patient monitoring platforms, Southern Region market entry, Saudization workforce development programs, and CBAHI-compliant digital care management systems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)