Saudi Arabia Industrial Air Blowers Market Size, Share, Trends and Forecast by Type, Business Type, End User, and Region, 2026-2034

Saudi Arabia Industrial Air Blowers Market Summary:

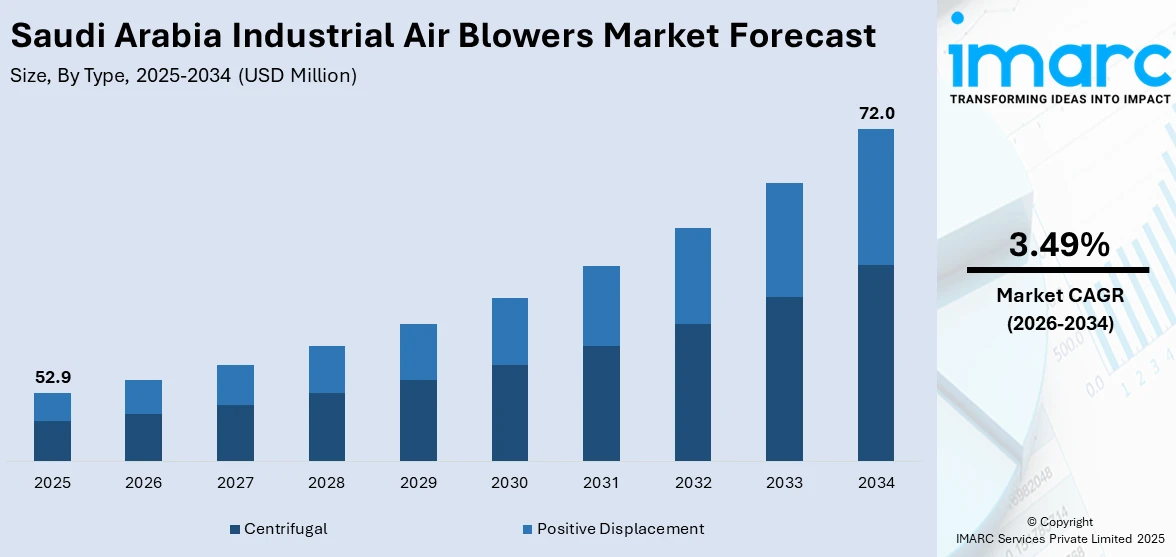

The Saudi Arabia industrial air blowers market size was valued at USD 52.9 Million in 2025 and is projected to reach USD 72.0 Million by 2034, growing at a compound annual growth rate of 3.49% from 2026-2034.

The Saudi Arabia industrial air blowers market is gaining momentum as the Kingdom accelerates industrial diversification under Vision 2030. Expanding petrochemical production, growing wastewater treatment infrastructure, and rising energy efficiency mandates are bolstering demand for advanced air handling solutions. Ongoing investments in manufacturing capacity, coupled with government-led sustainability frameworks, are strengthening adoption of industrial blowers across key sectors, reinforcing Saudi Arabia industrial air blowers market share.

Key Takeaways and Insights:

- By Type: Centrifugal dominates the market with a share of 59% in 2025, owing to its superior airflow efficiency, consistent pressure output, and widespread adoption across petrochemical, wastewater treatment, and manufacturing applications in the Kingdom.

- By Business Type: Equipment sales lead the market with a share of 70% in 2025. This dominance is driven by ongoing industrial expansion, new facility commissioning, and strong demand for initial equipment procurement across Saudi Arabia’s growing manufacturing and processing sectors.

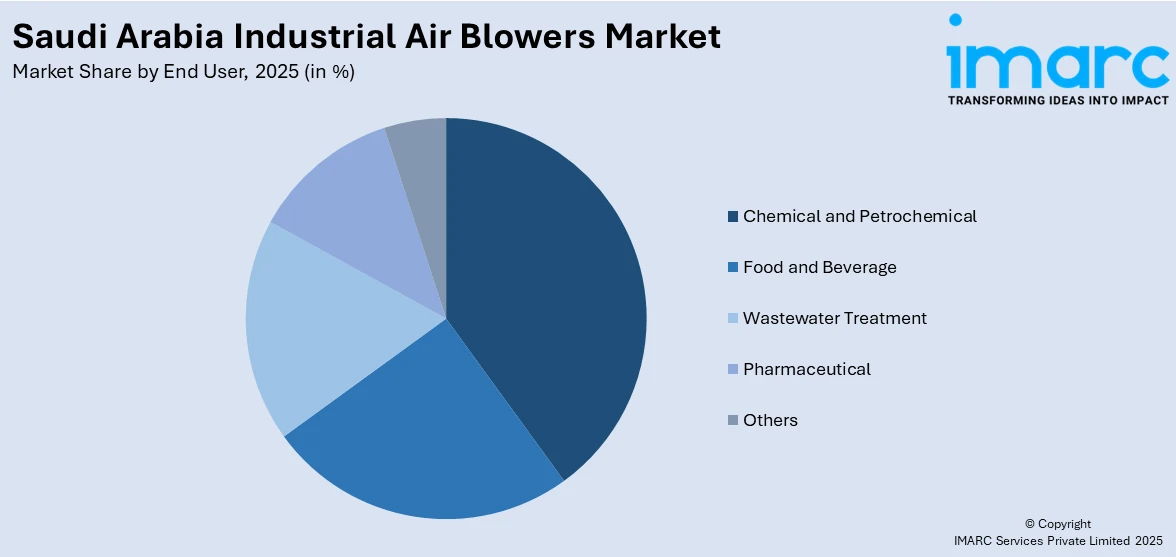

- By End User: Chemical and petrochemical holds the largest segment with a market share of 32% in 2025, reflecting the critical role of air blowers in process gas handling, combustion air supply, and ventilation across the Kingdom’s extensive refining and petrochemical complexes.

- By Region: Northern and Central Region represents the largest region with 29% share in 2025, driven by the concentration of industrial cities, petrochemical hubs in Jubail, government-led infrastructure projects, and Riyadh’s expanding industrial and municipal development activity.

- Key Players: Key players drive the Saudi Arabia industrial air blowers market by expanding service networks, strengthening after-sales capabilities, introducing energy-efficient blower technologies, and leveraging strategic partnerships with regional distributors to enhance product availability and market penetration across the Kingdom.

To get more information on this market Request Sample

The Saudi Arabia industrial air blowers market is advancing as the Kingdom pursues large-scale industrial transformation under its Vision 2030 strategy. Rapid expansion of manufacturing zones, petrochemical complexes, and wastewater treatment infrastructure is creating sustained demand for reliable air handling equipment. The government’s National Industrial Strategy, which targets increasing the number of factories from 12,000 at end-2024 to 36,000 by 2035, is a major catalyst for market expansion. Growing emphasis on energy-efficient technologies is encouraging the adoption of advanced centrifugal and positive displacement blowers that reduce operational costs and meet evolving regulatory standards. The chemical and petrochemical sector remains a primary consumer, supported by substantial investments in new refining and processing facilities across Jubail and Yanbu industrial cities. Additionally, the expansion of water and wastewater treatment plants under public-private partnership models is creating new demand channels. Strengthening after-sales service networks and rental solutions are further enabling market participants to address diverse operational requirements across the Kingdom’s expanding industrial landscape.

Saudi Arabia Industrial Air Blowers Market Trends:

Accelerating Localization of Pharmaceutical and Food Manufacturing

Saudi Arabia is rapidly expanding domestic pharmaceutical and food production capacity, creating new demand channels for industrial air blowers used in cleanroom ventilation, process air supply, and controlled-environment manufacturing. The Kingdom is commissioning new pharmaceutical plants focused on complex oncology and injectable medications, while dedicated food industry clusters such as the Jeddah Food Industry Cluster are attracting significant investment and hosting numerous processing facilities. Government initiatives promoting local production and reduced import dependency are broadening the end-user base for industrial air handling equipment across these high-growth manufacturing sectors.

Rising Adoption of Energy-Efficient Blower Technologies

The Kingdom is prioritizing energy conservation across industrial operations, with the government targeting a 30% reduction in national energy consumption. The energy efficiency market is valued at approximately SAR 1.6 Billion, reflecting growing preference for sustainable industrial technologies. This shift is driving adoption of variable-speed centrifugal blowers and high-efficiency positive displacement systems that minimize power consumption while maintaining consistent airflow performance across demanding industrial environments.

Expanding Wastewater Treatment Infrastructure

Saudi Arabia is significantly scaling its wastewater treatment capacity through major public-private partnership projects. In 2024, three independent sewage treatment plants in Madinah, Tabuk, and Buraydah were commissioned with a combined capacity of 440,000 cubic meters per day. These facilities generate over half of their energy internally through biogas and solar integration, setting new benchmarks for sustainability in the Kingdom's water infrastructure and creating sustained demand for industrial air blowers in aeration and process ventilation applications.

How Vision 2030 is Transforming the Saudi Arabia Industrial Air Blowers Market:

Saudi Arabia's Vision 2030 is reshaping the industrial air blowers market by accelerating economic diversification and driving large-scale industrial expansion across the Kingdom. Mega-projects such as the Amiral petrochemical complex, NEOM's advanced manufacturing zones, and the Jeddah Food Industry Cluster are generating unprecedented demand for air handling and ventilation equipment across petrochemical, food processing, and pharmaceutical sectors. Regulatory reforms under the National Industrial Development and Logistics Program, including localization incentives, streamlined licensing frameworks, and public-private partnership models, have strengthened investor confidence and expanded the industrial project pipeline. The Kingdom's ambitious factory expansion targets and continued development of industrial cities such as Jubail and Yanbu are accelerating equipment procurement, while growing emphasis on energy efficiency standards and sustainability mandates is driving adoption of advanced centrifugal and positive displacement blower technologies across diverse end-user applications.

Market Outlook 2026-2034:

Saudi Arabia's industrial air blowers market is positioned for steady expansion, driven by accelerating industrial diversification, growing petrochemical capacity, and continued infrastructure development under Vision 2030. Increasing domestic manufacturing capabilities, rising demand for energy-efficient air handling solutions, and expanding wastewater treatment networks are expected to drive higher equipment procurement volumes. The government's commitment to significantly expanding the national factory base and ongoing investments in petrochemical mega-projects across Jubail and Yanbu are anticipated to create significant long-term demand. Additionally, the strengthening of after-sales service infrastructure and the introduction of rental solutions by leading blower manufacturers are enabling broader market accessibility and fostering a more competitive, innovation-driven industrial air blowers landscape across the Kingdom. The market generated a revenue of USD 52.9 Million in 2025 and is projected to reach a revenue of USD 72.0 Million by 2034, growing at a compound annual growth rate of 3.49% from 2026-2034.

Saudi Arabia Industrial Air Blowers Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Centrifugal |

59% |

|

Business Type |

Equipment Sales |

70% |

|

End User |

Chemical and Petrochemical |

32% |

|

Region |

Northern and Central Region |

29% |

Type Insights:

- Positive Displacement

- Centrifugal

Centrifugal dominates with a market share of 59% of the total Saudi Arabia industrial air blowers market in 2025.

Centrifugal blowers are the preferred choice across Saudi Arabia’s heavy industries due to their ability to deliver high-volume airflow at consistent pressures, making them essential for petrochemical processing, combustion air supply, and industrial ventilation. The Middle East and Africa region is emerging as a key market for centrifugal blowers, driven by infrastructure development and economic diversification efforts, with Saudi Arabia and the United Arab Emirates leading regional growth. Vision 2030-aligned industrial expansion across several operational industrial cities is generating significant procurement demand for centrifugal air handling equipment.

The growing emphasis on operational efficiency and reduced energy consumption is further reinforcing centrifugal blower adoption. Leading manufacturers maintain strong market positioning through extensive distributor networks, localized after-sales support, and dedicated service centers across the Kingdom. The increasing commissioning of new processing facilities, wastewater treatment plants, and industrial complexes continues to sustain robust demand for centrifugal blower systems. Advancements in variable-speed drive technologies and smart monitoring capabilities are enabling end users to optimize airflow performance while minimizing operational costs across diverse industrial applications.

Business Type Insights:

- Equipment Sales

- Services

Equipment sales leads with a share of 70% of the total Saudi Arabia industrial air blowers market in 2025.

Equipment sales dominate the Saudi Arabia industrial air blowers market as the Kingdom’s rapid industrial expansion drives sustained procurement of new blower systems. The ongoing commissioning of manufacturing facilities, petrochemical complexes, and wastewater treatment plants requires significant upfront equipment acquisition. Expansive distributor networks and specialized industrial equipment suppliers play a critical role in market delivery, with indirect sales channels accounting for a substantial portion of overall transactions.

The strong equipment sales segment reflects the capital-intensive nature of Saudi Arabia’s industrialization trajectory, where new project development necessitates complete air handling system installations. Industrial processes across chemical manufacturing, food production, and pharmaceutical operations require purpose-built blower configurations, driving customized equipment procurement. The Kingdom’s goal of increasing factory count ensures a sustained long-term demand pipeline for new industrial air blower equipment. Manufacturers are strengthening regional warehousing and technical support capabilities to capture this growing demand.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Food and Beverage

- Wastewater Treatment

- Pharmaceutical

- Chemical and Petrochemical

- Others

The chemical and petrochemical exhibits a clear dominance with a 32% share of the total Saudi Arabia industrial air blowers market in 2025.

The chemical and petrochemical sector represents the primary demand driver for industrial air blowers in Saudi Arabia, utilizing these systems for combustion air supply, process gas handling, catalyst regeneration, and facility ventilation. The Kingdom's petrochemical industry is one of the largest in the Gulf region, contributing significantly to national economic output and industrial diversification. Jubail and Yanbu serve as the Kingdom's principal petrochemical hubs, housing major refining and processing complexes that require continuous and reliable air handling infrastructure to maintain safe and efficient operations.

Ongoing mega-project developments are reinforcing the sector’s position as the largest end-user segment. In February 2025, the Saudi government approved feedstock allocations for major new petrochemical complexes in Jubail, including a 1.5 Million Tons per year ethylene facility by Sipchem-LyondellBasell. These large-scale downstream expansions require extensive industrial air handling infrastructure for combustion air supply, process ventilation, and catalyst regeneration. The continued investment in refining and processing capacity across the Kingdom's established industrial cities is generating sustained procurement demand for high-performance blower systems tailored to demanding petrochemical operating environments.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

Northern and Central Region holds the largest share at 29% of the total Saudi Arabia industrial air blowers market in 2025.

The Northern and Central Region leads the Saudi Arabia industrial air blowers market, anchored by Riyadh’s position as the Kingdom’s administrative and economic capital with a rapidly growing industrial base. The region benefits from proximity to major industrial clusters and government-led smart city initiatives that are driving infrastructure modernization. Riyadh is a hotspot for water infrastructure investment, with its densely urbanized population and high population growth rate necessitating effective water management systems. Government-led schemes and smart city initiatives are accelerating adoption of advanced industrial equipment, including blower systems for municipal and industrial applications.

The Saudi government's substantial financial commitments toward petrochemical development initiatives are further strengthening the region's industrial equipment procurement pipeline. Strategic budget allocations aligned with Vision 2030 are accelerating project commissioning across key industrial zones, driving sustained demand for air handling systems. Additionally, the expansion of wastewater treatment infrastructure across central urban areas, including new independent sewage treatment plants and collection networks, is creating additional demand channels for aeration and ventilation blower systems throughout the Northern and Central Region.

Market Dynamics:

Growth Drivers:

Why is the Saudi Arabia Industrial Air Blowers Market Growing?

Expanding Petrochemical Production Capacity

Saudi Arabia's petrochemical sector is undergoing significant capacity expansion, creating substantial demand for industrial air blowers used in process gas handling, combustion air supply, and facility ventilation. The Kingdom's petrochemical production capacity is expected to grow substantially over the coming years, driven by strategic investments in new refining and downstream processing complexes. Major mega-projects including the Aramco-TotalEnergies Amiral complex in Jubail are advancing toward operational launch, featuring large-scale ethylene crackers and integrated processing units. These developments require extensive industrial air handling infrastructure, directly driving demand for centrifugal and positive displacement blower systems across the Kingdom's expanding petrochemical landscape.

Government-Led Industrial Infrastructure Investment

The Saudi government's commitment to economic diversification under Vision 2030 is channeling massive investments into industrial infrastructure, generating sustained demand for industrial equipment including air blowers. The National Industrial Development and Logistics Program targets attracting significant investments across key sectors, with the goal of substantially increasing the industrial sector's contribution to national GDP. Dedicated allocations for petrochemical-related initiatives and the National Industrial Strategy's ambitious factory expansion targets are further accelerating industrial development. These government-led programs are creating a robust project pipeline across chemical manufacturing, food processing, pharmaceutical production, and wastewater treatment, all of which require industrial air blower systems for ventilation, aeration, and process air applications.

Growing Wastewater Treatment Infrastructure

Saudi Arabia is rapidly expanding its wastewater treatment capacity to address the demands of a growing urban population and industrial base, creating significant opportunities for industrial air blower deployment in aeration and process ventilation applications. The government has announced six new wastewater treatment projects under the public-private partnership model, while three independent sewage treatment plants in Madinah, Tabuk, and Buraydah were commissioned in 2024 with a combined capacity of 440,000 cubic meters per day. In February 2024, VA TECH WABAG secured a USD 33.5 Million contract for an industrial wastewater treatment plant at Ras Tanura Refinery, demonstrating the expanding scope of water treatment infrastructure that drives blower system procurement.

Market Restraints:

What Challenges the Saudi Arabia Industrial Air Blowers Market is Facing?

High Initial Equipment and Installation Costs

Industrial air blowers, particularly high-capacity centrifugal systems, require significant capital investment for procurement, installation, and commissioning. The upfront costs associated with acquiring advanced blower equipment, combined with specialized infrastructure requirements for proper installation, present a barrier for smaller industrial facilities and emerging manufacturing enterprises. While long-term operational savings exist, many price-sensitive operators find it challenging to justify substantial initial expenditure without accessible financing mechanisms or government subsidies.

Specialized Maintenance and Technical Expertise Shortages

Industrial air blowers demand regular specialized maintenance to sustain optimal performance, including vibration analysis, impeller balancing, and bearing replacement. The shortage of trained technicians qualified to service complex blower systems, particularly in remote industrial zones away from major urban centers, creates operational challenges. Extended equipment downtime resulting from delayed maintenance or limited access to certified service providers can significantly impact production efficiency and increase total cost of ownership for industrial operators.

Rising Operational Energy Costs

The Saudi government’s phased reduction of industrial energy subsidies as part of economic restructuring under Vision 2030 has led to increased electricity tariffs for commercial and industrial consumers. Since air blowers are energy-intensive equipment that operate continuously in many industrial processes, rising electricity costs directly impact operational expenses. The transition to higher energy prices, while encouraging efficiency, creates short-term cost pressures for facilities operating legacy blower systems that lack variable-speed drives or modern energy optimization features.

Competitive Landscape:

The Saudi Arabia industrial air blowers market features a dynamic mix of international manufacturers and regional distributors competing through product differentiation, service network expansion, and technological innovation. Competition is driven by investments in energy-efficient blower technologies, comprehensive rental solutions, and digital monitoring capabilities. Regional suppliers are leveraging local expertise and customization capabilities to serve niche applications, while international manufacturers focus on strengthening service infrastructure and expanding spare parts availability across the Kingdom. Strategic partnerships between global equipment producers and local distributors are enhancing market reach and after-sales support. The growing emphasis on variable-speed drive technologies and smart monitoring systems is intensifying competition, encouraging market participants to continuously refine their offerings to meet evolving industrial requirements.

Saudi Arabia Industrial Air Blowers Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Positive Displacement, Centrifugal |

| Business Types Covered | Equipment Sales, Services |

| End Users Covered | Food and Beverage, Wastewater Treatment, Pharmaceutical, Chemical and Petrochemical, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Industrial Air Blowers Market Report

The Saudi Arabia industrial air blowers market size was valued at USD 52.9 Million in 2025.

The Saudi Arabia industrial air blowers market is expected to grow at a compound annual growth rate of 3.49% from 2026-2034 to reach USD 72.0 Million by 2034.

Centrifugal dominated the market with a share of 59%, driven by its superior airflow efficiency, consistent pressure output, and widespread adoption across petrochemical, wastewater treatment, and manufacturing operations throughout the Kingdom.

Key factors driving the Saudi Arabia industrial air blowers market include expanding petrochemical production capacity, government-led industrial infrastructure investment under Vision 2030, growing wastewater treatment infrastructure, and rising demand for energy-efficient air handling solutions.

Major challenges include high initial equipment and installation costs, shortage of specialized maintenance technicians in remote industrial zones, rising operational energy costs due to subsidy reductions, and supply chain dependencies on imported blower components and spare parts.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)