Saudi Arabia Industrial Material Handling Robotics Market Size, Share, Trends and Forecast by Type of Robot, Payload Capacity, Operational Environment, Application, End Use Industry, and Region, 2026-2034

Saudi Arabia Industrial Material Handling Robotics Market Overview:

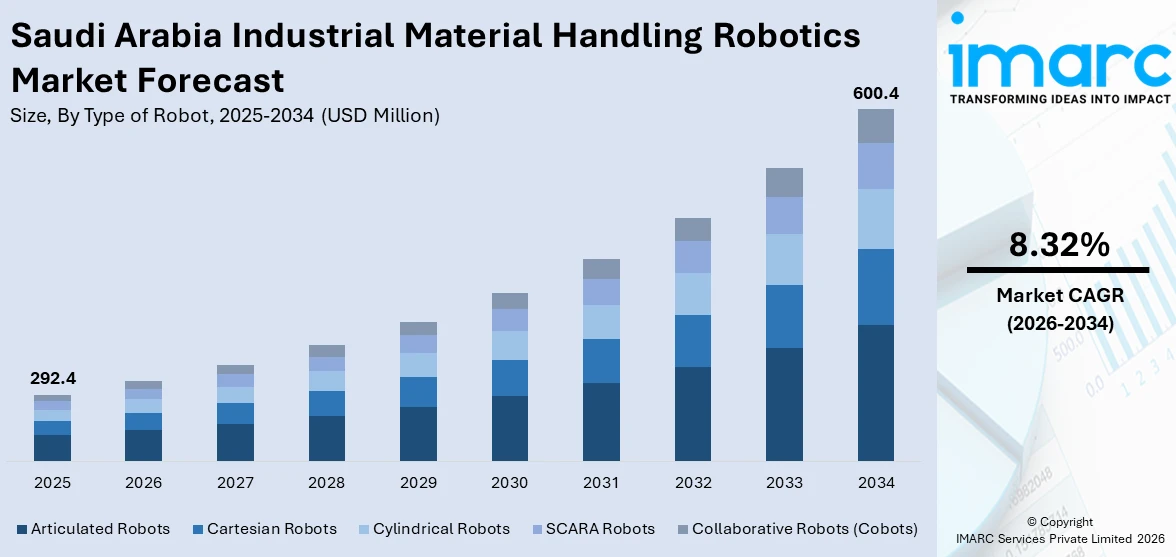

The Saudi Arabia industrial material handling robotics market size reached USD 292.4 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 600.4 Million by 2034, exhibiting a growth rate (CAGR) of 8.32% during 2026-2034. The market is driven by industrial diversification under Vision 2030 and national logistics expansion. Additionally, robotics are integral to mega infrastructural development projects and smart facility design, which is propelling the product demand. Workforce restructuring, automation readiness, and logistics modernization are some of the factors positively impacting the Saudi Arabia industrial material handling robotics market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 292.4 Million |

| Market Forecast in 2034 | USD 600.4 Million |

| Market Growth Rate 2026-2034 | 8.32% |

Saudi Arabia Industrial Material Handling Robotics Market Trends:

Industrial Diversification Under Vision 2030

Saudi Arabia’s Vision 2030 initiative has become a major force behind the transformation of the country’s industrial sector. By focusing on economic diversification and reducing dependence on oil revenues, the government has directed investment into manufacturing, logistics, and infrastructure. These sectors are central to the Kingdom’s industrial strategy and require scalable automation technologies, including robotics for material handling, to meet long-term operational targets. State-owned and private enterprises have received incentives to modernize facilities, adopt advanced machinery, and improve process efficiency. Industrial zones such as King Abdullah Economic City and the Royal Commission for Jubail and Yanbu have attracted significant capital in machinery, warehousing, and high-throughput production systems, areas where robotics now play a central role in streamlining internal transport and reducing turnaround times. On February 6, 2023, Geek+ partnered with Saudi-based Starlinks to launch a 400,000 sq. ft. robotic fulfillment center featuring over 250 autonomous mobile robots with a monthly handling capacity of 3.6 million units. The facility combines P40 Picking, S20C Sorting, and RS8 RoboShuttle systems to optimize e-commerce logistics across Saudi Arabia. This deployment enhances inventory tracking, reduces lead times, and reinforces Saudi Arabia’s logistics infrastructure with high-throughput robotics automation. Moreover, Saudi Arabia’s push to become a regional logistics hub has led to an expansion of seaports, dry ports, and integrated industrial parks. These require automated systems to handle high cargo volumes with minimal downtime. More than 80 words from the heading, this push for transformation is a primary contributor to the Saudi Arabia industrial material handling robotics market growth, especially as large-scale industrial entities look for consistent throughput and digital infrastructure integration.

To get more information on this market Request Sample

Rising Operational Costs and Workforce Nationalization

With labor market reforms and the implementation of Saudization policies, companies are under increasing pressure to limit reliance on expatriate workers and hire locally. This shift has created talent gaps in sectors traditionally dominated by foreign workers, such as warehouse operations and factory-floor logistics. The resulting shortage of skilled labor has accelerated the adoption of robotics in material handling processes. Hiring constraints, combined with cost inflation in recruitment, training, and retention, are compelling companies to reconsider manual workflows. Robotic solutions offer a long-term alternative, reducing the need for continuous staffing and ensuring consistency in repetitive or hazardous tasks. Firms operating in high-risk environments, including petrochemical and metal fabrication, are adopting robotic handling systems to meet both safety standards and productivity goals. This structural labor shift is pushing both multinational firms and domestic manufacturers to invest in automation as part of their workforce optimization strategies wherein the demand is particularly high for systems such as automated guided vehicles (AGVs), robotic arms, and conveyor-based handling solutions. On February 20, 2024, Alat, a PIF-owned entity, and SoftBank Group announced a strategic joint venture to establish a USD 150 million fully automated industrial robot manufacturing and engineering hub in Riyadh, with the first factory set to launch in December 2024. The initiative aims to contribute USD 1 billion to Saudi Arabia’s GDP by 2025 and is supported by Alat’s broader USD 100 billion investment mandate to build carbon-zero manufacturing powered by clean energy. As this workforce transformation continues, the market is being shaped by the necessity to maintain output levels while navigating regulatory labor compliance and cost-efficiency thresholds.

Saudi Arabia Industrial Material Handling Robotics Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on type of robot, payload capacity, operational environment, application, and end use industry.

Type of Robot Insights:

- Articulated Robots

- Cartesian Robots

- Cylindrical Robots

- SCARA Robots

- Collaborative Robots (Cobots)

The report has provided a detailed breakup and analysis of the market based on the type of robot. This includes articulated robots, cartesian robots, cylindrical robots, SCARA robots, and collaborative robots (cobots).

Payload Capacity Insights:

- Low Payload (Up to 50 kg)

- Medium Payload (51 kg to 300 kg)

- High Payload (Above 300 kg)

The report has provided a detailed breakup and analysis of the market based on the payload capacity. This includes low payload (up to 50 kg), medium payload (51 kg to 300 kg), and high payload (above 300 kg).

Operational Environment Insights:

- Indoor

- Outdoor

- Controlled Environment (Clean Rooms)

The report has provided a detailed breakup and analysis of the market based on the operational environment. This includes indoor, outdoor, and controlled environment (clean rooms).

Application Insights:

Access the comprehensive market breakdown Request Sample

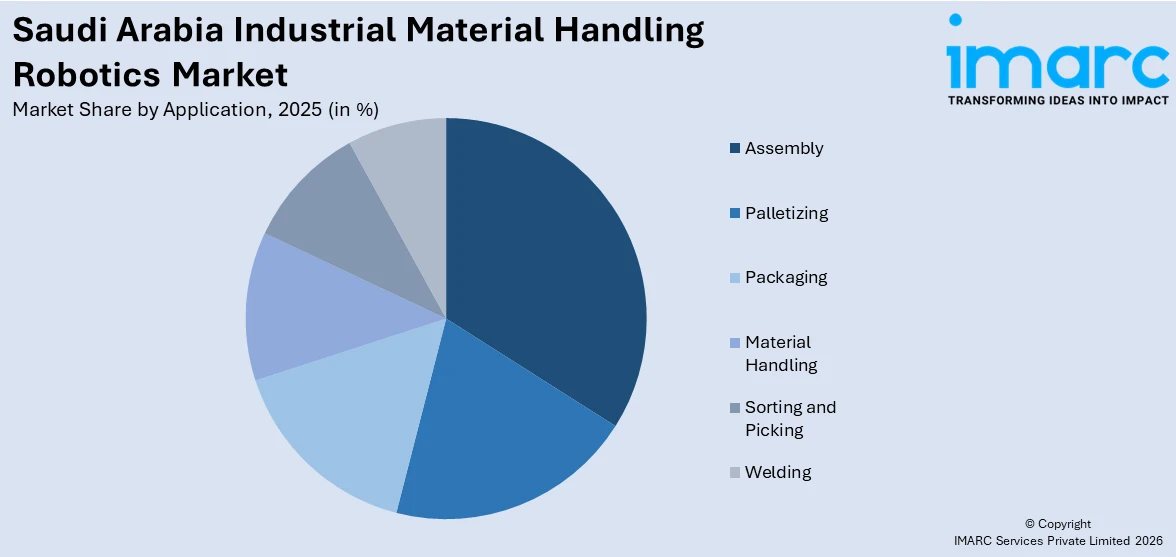

- Assembly

- Palletizing

- Packaging

- Material Handling

- Sorting and Picking

- Welding

The report has provided a detailed breakup and analysis of the market based on the application. This includes assembly, palletizing, packaging, material handling, sorting and picking, and welding.

End Use Industry Insights:

- Automotive

- Food and Beverage

- Electronics

- Aerospace

- Pharmaceuticals

- Logistics and Warehousing

The report has provided a detailed breakup and analysis of the market based on the end use industry. This includes automotive, food and beverage, electronics, aerospace, pharmaceuticals, and logistics and warehousing.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

The report has provided a comprehensive analysis of all major regional markets, including Northern and Central Region, Western Region, Eastern Region, and Southern Region.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Saudi Arabia Industrial Material Handling Robotics Market News:

- On February 12, 2025, Dexory signed a memorandum of understanding with Al Masarat Holdings to deploy AI-powered autonomous mobile robots and digital twin technology at Saudi Arabia’s Masarat Mobility Park in an effort to explore several opportunities related to robotic systems with the manufacturing and logistics applications. The initiative includes setting up a regional R&D and production hub, with robotics-as-a-service (RaaS) platforms for real-time inventory and facility management. Effective through February 2028, the agreement supports Vision 2030 objectives by enhancing logistics automation, operational efficiency, and robotics integration in the Kingdom’s industrial ecosystem.

Saudi Arabia Industrial Material Handling Robotics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types of Robot Covered | Articulated Robots, Cartesian Robots, Cylindrical Robots, SCARA Robots, Collaborative Robots (Cobots) |

| Payload Capacities Covered | Low Payload (Up to 50 kg), Medium Payload (51 kg to 300 kg), High Payload (Above 300 kg) |

| Operational Environments Covered | Indoor, Outdoor, Controlled Environment (Clean Rooms) |

| Applications Covered | Assembly, Palletizing, Packaging, Material Handling, Sorting and Picking, Welding |

| End Use Industries Covered | Automotive, Food and Beverage, Electronics, Aerospace, Pharmaceuticals, Logistics and Warehousing |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Saudi Arabia industrial material handling robotics market performed so far and how will it perform in the coming years?

- What is the breakup of the Saudi Arabia industrial material handling robotics market on the basis of type of robot?

- What is the breakup of the Saudi Arabia industrial material handling robotics market on the basis of payload capacity?

- What is the breakup of the Saudi Arabia industrial material handling robotics market on the basis of operational environment?

- What is the breakup of the Saudi Arabia industrial material handling robotics market on the basis of application?

- What is the breakup of the Saudi Arabia industrial material handling robotics market on the basis of end use industry?

- What is the breakup of the Saudi Arabia industrial material handling robotics market on the basis of region?

- What are the various stages in the value chain of the Saudi Arabia industrial material handling robotics market?

- What are the key driving factors and challenges in the Saudi Arabia industrial material handling robotics?

- What is the structure of the Saudi Arabia industrial material handling robotics market and who are the key players?

- What is the degree of competition in the Saudi Arabia industrial material handling robotics market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia industrial material handling robotics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia industrial material handling robotics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia industrial material handling robotics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)