Saudi Arabia Logistics Market Size, Share, Trends and Forecast by Model Type, Transportation Mode, End Use, and Region, 2026-2034

Saudi Arabia Logistics Market Size, Share, Trends & Forecast (2026-2034)

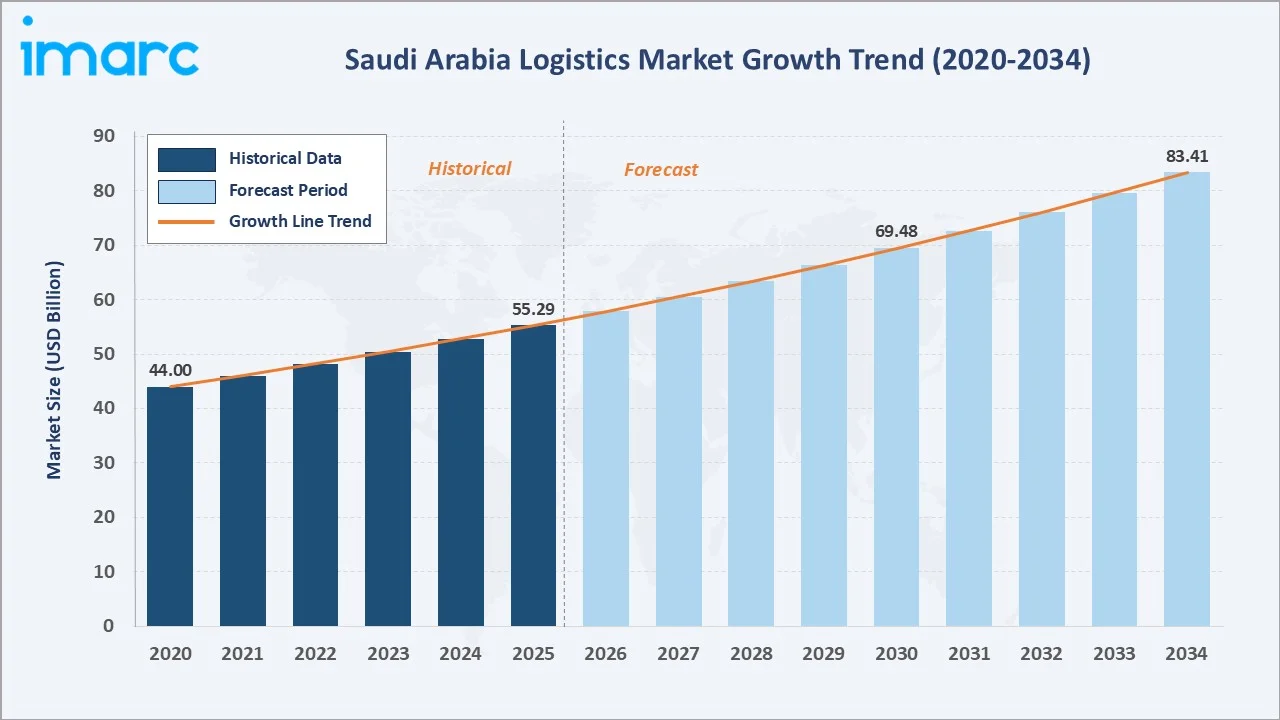

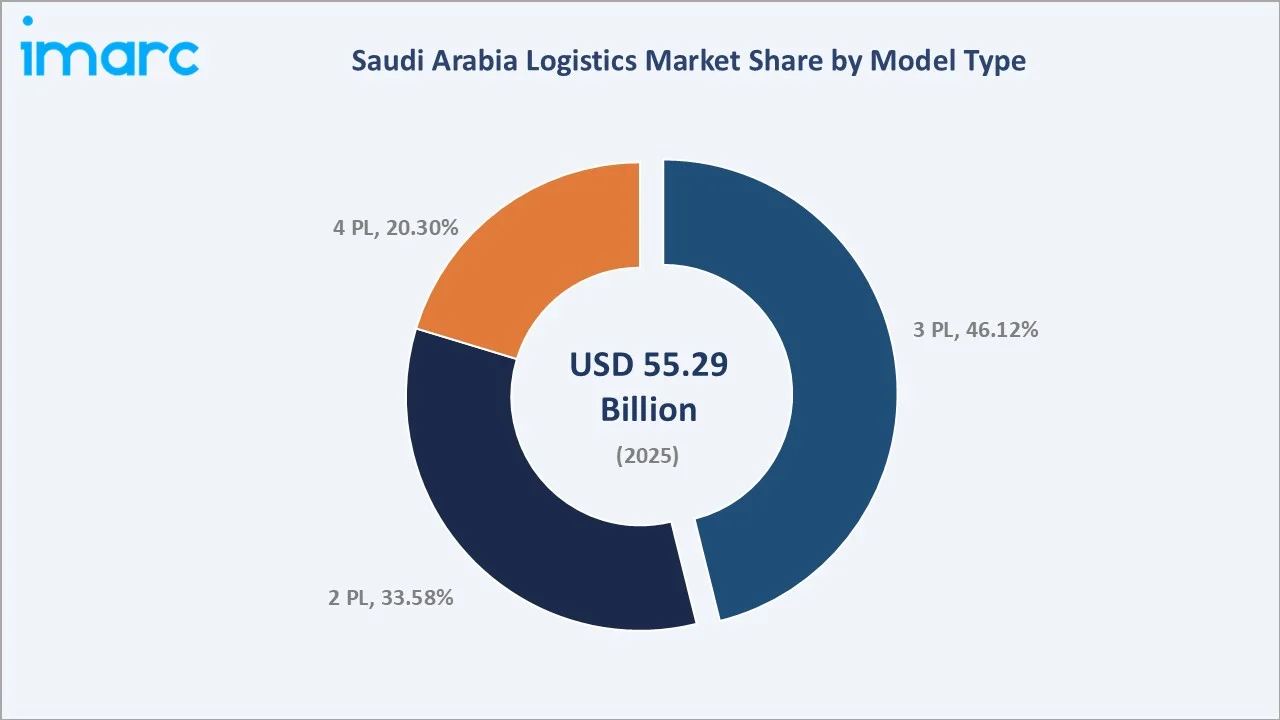

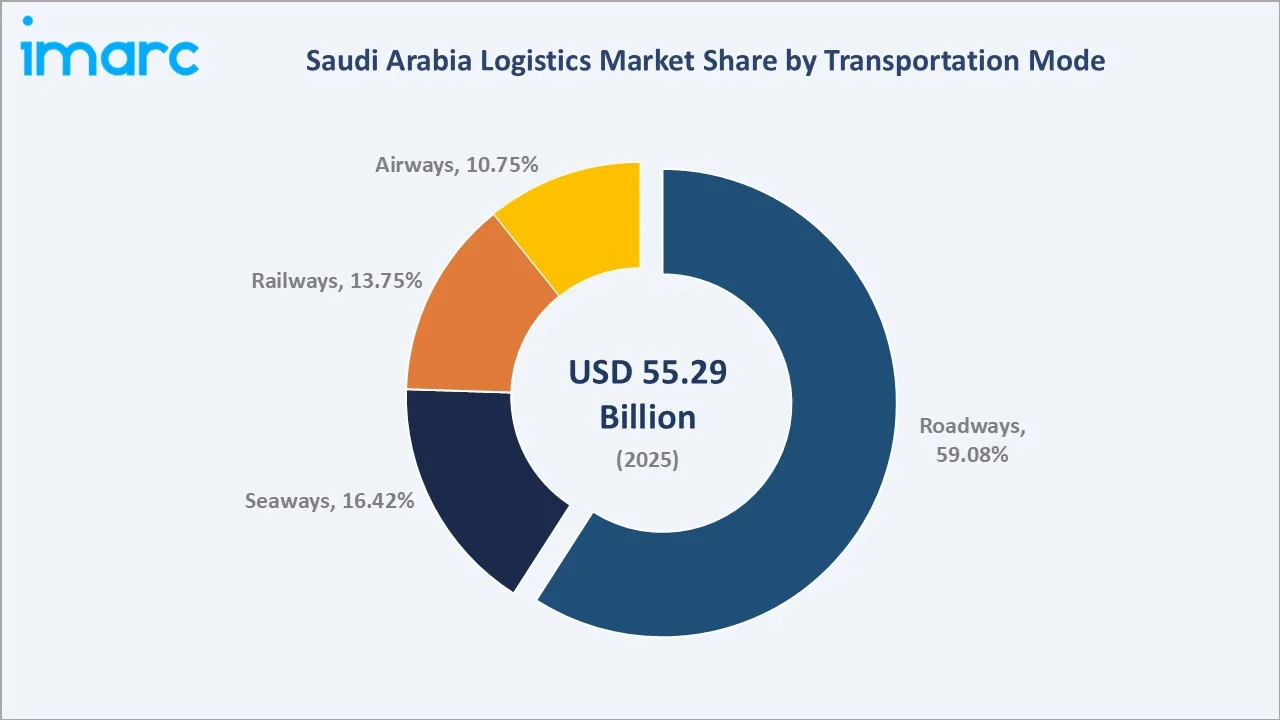

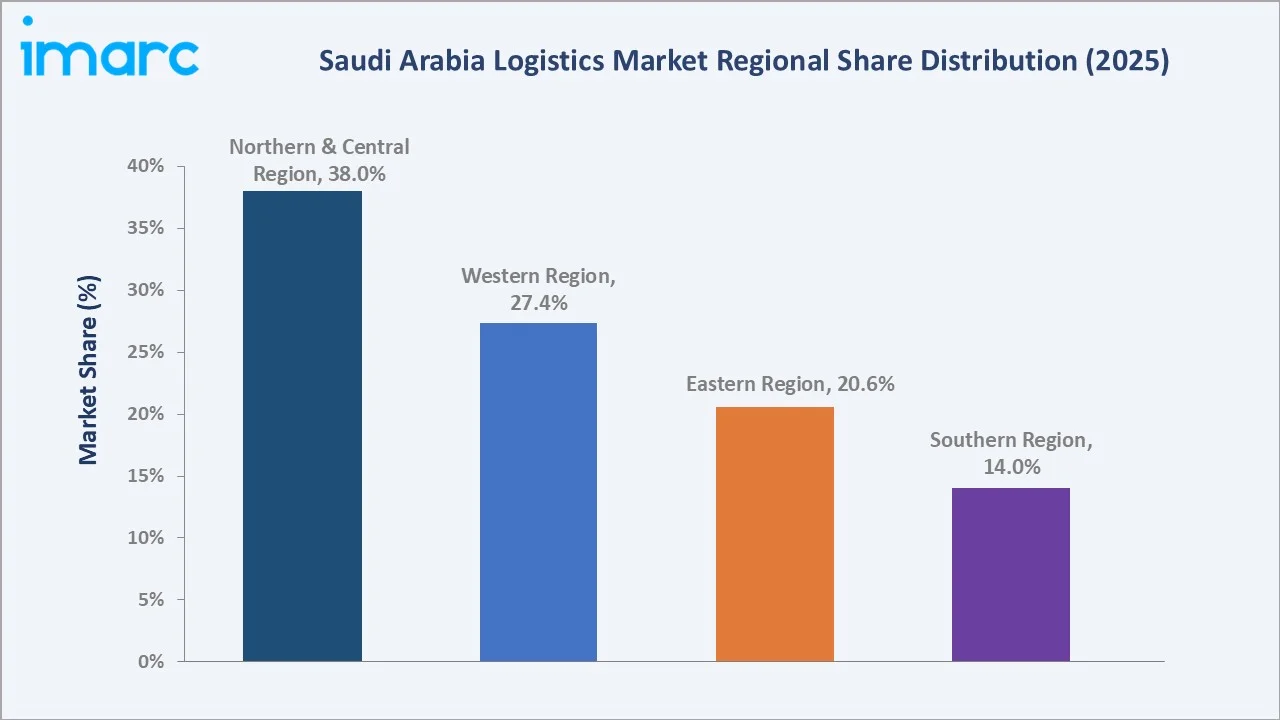

The Saudi Arabia logistics market size reached USD 55.29 Billion in 2025 and is projected to reach USD 83.41 Billion by 2034, exhibiting a CAGR of 4.67% during 2026-2034. Vision 2030 infrastructure investments, e-commerce expansion, and the Kingdom's strategic positioning as a trade corridor connecting Asia, Europe, and Africa are the primary forces driving market growth.

3 PL dominates the model type mix at 46.12% in 2025, while roadways lead the transportation segment at 59.08%. Northern and Central Region commands a dominant 38.0% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 55.29 Billion |

|

Forecast Market Size (2034) |

USD 83.41 Billion |

|

CAGR (2026-2034) |

4.67% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Northern and Central Region (38.0% share, 2025) |

|

Second Largest Region |

Western Region (27.4% share, 2025) |

|

Leading Model Type |

3 PL (46.12%, 2025) |

|

Leading Transportation Mode |

Roadways (59.08%, 2025) |

The Saudi Arabia logistics market trajectory from 2020 through 2034, with expansion to USD 55.29 Billion in 2025, reflects sustained Vision 2030 momentum, while the forecast to USD 83.41 Billion captures accelerating e-commerce demand, industrial diversification, and multimodal connectivity investments across the Kingdom.

To get more information on this market, Request Sample

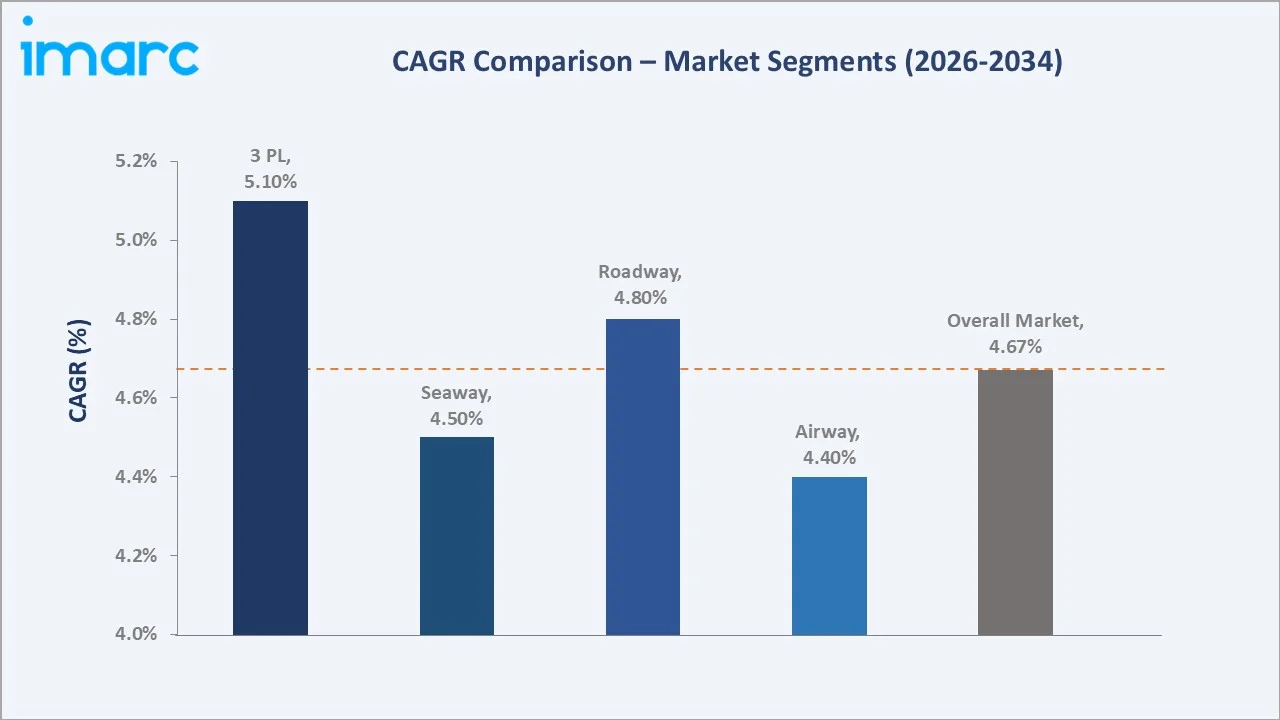

The CAGR trajectories across key model type, transportation mode, and regional sub-segments, with 3 PL at ~5.1% CAGR and Roadways at ~4.8% CAGR, represent the fastest-growing categories within the Saudi Arabia logistics industry analysis through 2034.

Executive Summary

The Saudi Arabia logistics market is on a sustained growth trajectory from USD 55.29 Billion in 2025 to USD 83.41 Billion by 2034. Logistics services, spanning freight forwarding, warehousing, distribution, and last-mile delivery across manufacturing, retail, and energy sectors, benefit from the Kingdom's strategic repositioning as a regional trade hub.

3 PL dominates the model type segment at 46.12% in 2025, driven by enterprise outsourcing of supply chain operations and rising demand for integrated transportation, warehousing, and value-added services. 2 PL (33.58%) commands traditional asset-based freight flows, while 4 PL (20.30%) serves premium supply chain orchestration mandates for complex multi-vendor operations.

Roadways lead transportation mode at 59.08% in 2025, reflecting the Kingdom's 73,000-kilometer highway network and trucking flexibility. Seaways (16.42%) capture bulk import-export flows through Jeddah, Dammam, and King Abdullah Ports. Railways (13.75%) and airways (10.75%) support heavy industrial freight and high-value time-sensitive cargo respectively.

Northern and Central Region dominates at 38.0% in 2025, led by Riyadh's economic centrality and the Special Integrated Logistics Zone (SILZ). Western region (27.4%) leverages Jeddah Islamic Port, while Eastern region (20.6%) serves oil and gas corridors. Southern region (14.0%) emerges through industrial diversification programs.

Key Market Insights

|

Insight |

Data |

|

Largest Model Type |

3 PL - 46.12% share (2025) |

|

Leading Transportation Mode |

Roadways - 59.08% share (2025) |

|

Leading Region |

Northern and Central Region - 38.0% share (2025) |

|

Second Largest Region |

Western Region - 27.4% share (2025) |

|

Top Companies |

DHL Group, Bahri, AJEX, Agility, Kuehne+Nagel, Saudi Post | SPL, SAL, GWC |

Key Analytical Observations Expanding on the Above Data:

- 3 PL, with 46.12% in 2025, dominates because enterprises increasingly outsource non-core supply chain operations to specialized providers offering integrated transportation, warehousing, and last-mile capabilities. E-commerce scale demands and just-in-time manufacturing accelerate 3 PL adoption across sectors.

- Roadways, with 59.08% in 2025, dominate transportation mode due to the Kingdom's extensive 73,000-kilometer highway network, trucking flexibility for door-to-door delivery, and infrastructure upgrades like the Eastern Expressway connecting Riyadh to Dammam that reduce transit times.

- Northern and Central Region's 38.0% dominance reflects Riyadh's role as the Kingdom's economic and administrative capital, hosting major corporate headquarters, the SILZ offering 50-year tax holiday, and a population of nearly 7.95 million driving e-commerce fulfillment demand.

- Western Region, with 27.4% in 2025, benefits from Jeddah Islamic Port as the Kingdom's largest seaport, handling over 65% of imports, plus King Abdullah Economic City's manufacturing clusters generating sustained freight forwarding and warehousing demand.

Saudi Arabia Logistics Market Overview

Logistics in Saudi Arabia encompasses freight forwarding, road, sea, rail, and air transportation, warehousing, distribution, and last-mile delivery supporting industrial, commercial, and e-commerce flows, integrating customs brokerage, cold chain handling, and technology-enabled tracking across multimodal corridors.

The ecosystem integrates shippers, freight forwarders, 3PL operators, transportation carriers, warehousing providers, technology enablers, and end-use industries spanning manufacturing, retail, e-commerce, oil and gas, automotive, and healthcare across the Kingdom.

Market Dynamics

To evaluate market opportunities, Request Sample

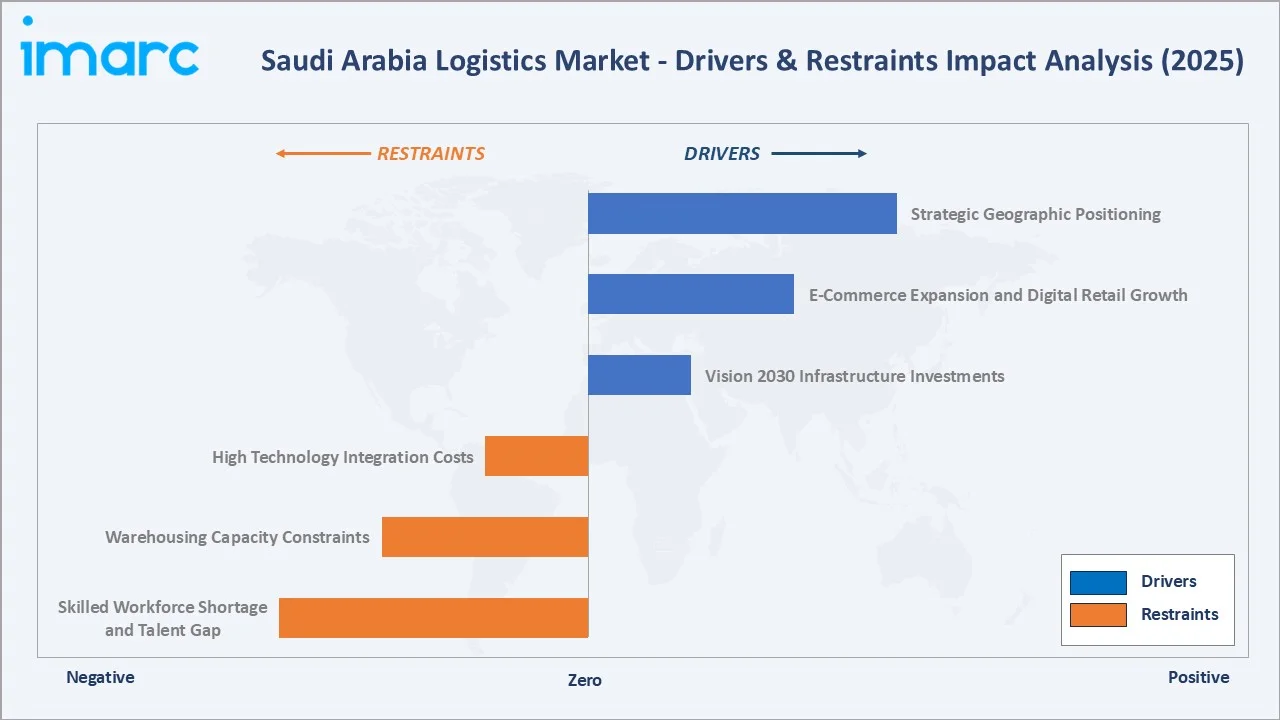

Market Drivers

- Vision 2030 Infrastructure Investments: The government targets increasing transport and logistics sector GDP contribution from 6% to 10% by 2030. Large-scale investments in port expansion, airport cargo capacity, and rail corridor extension create integrated multimodal transport networks.

- E-Commerce Expansion and Digital Retail Growth: Online retail penetration has accelerated with 33.6 million internet users by end of 2024, driving requirements for micro-fulfilment centers, optimized distribution networks, and expanded last-mile delivery fleets across urban centers.

- Strategic Geographic Positioning: Saudi Arabia's location at the crossroads of three continents positions it as a natural logistics hub for Asia-Europe-Africa trade flows. Red Sea, Arabian Gulf, and Indian Ocean shipping lane access drives regional distribution opportunities.

Market Restraints

- Skilled Workforce Shortage and Talent Gap: The industry faces a supply-demand gap for workers qualified in warehouse management, logistics technology, and digital platform operations. Saudization requirements mandating domestic employment quotas increase recruitment and training costs for operators.

- Warehousing Capacity Constraints: High warehouse utilization levels in major urban centers pressure storage availability, leading to rising rental costs and limited expansion options. This shortage creates operational challenges for importers, distributors, and e-commerce players in time-sensitive segments.

- High Technology Integration Costs: Automation, blockchain-based tracking, and advanced material handling systems require substantial upfront capital plus recurring maintenance and skilled workforce training, slowing adoption among SMEs and widening the efficiency gap versus large operators.

Market Opportunities

- Free Trade Zones and Special Economic Areas: SILZ near Riyadh's King Khalid International Airport offers 50-year tax holiday and 4-hour customs clearance. These specialized zones attract multinational operators seeking streamlined import-export operations and regional distribution platforms.

- Green Logistics and Sustainability: Operators aligning with the Kingdom's 2060 net-zero targets are integrating electric delivery vehicles, solar-powered warehouses, and carbon-neutral fleets. Saudi Green Initiative funding creates commercial opportunities for low-emission logistics service providers.

Market Challenges

- Regulatory Compliance and Saudization: Localization mandates, evolving customs protocols, and cross-border documentation requirements add complexity and cost, particularly for SMEs lacking scale to absorb compliance overhead and invest in specialized training programs.

- Last-Mile Urban Density and Delivery Cost: Rapid e-commerce growth strains urban delivery infrastructure as congestion, parking restrictions, and addressing inconsistencies increase per-parcel delivery costs and reduce driver productivity across metropolitan Riyadh, Jeddah, and Dammam.

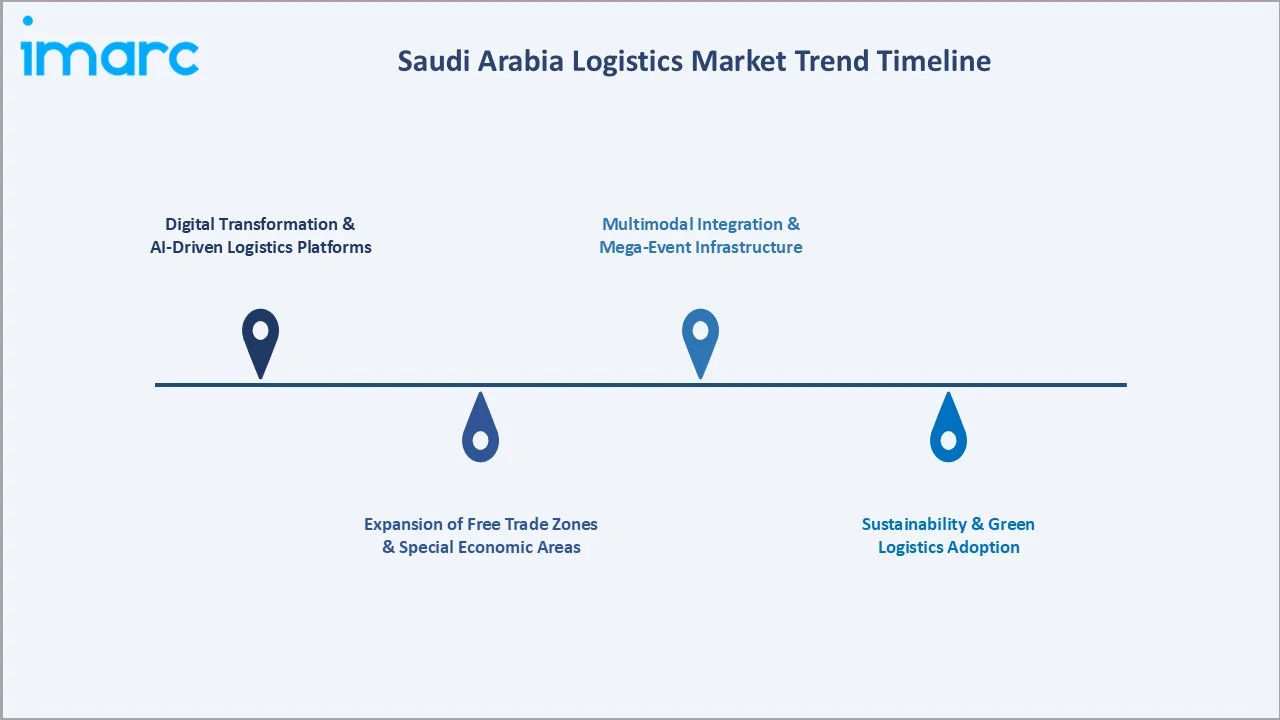

Emerging Market Trends

1. Digital Transformation and AI-Driven Logistics Platforms

The Saudi Arabia logistics market is witnessing accelerated adoption of artificial intelligence, IoT sensors, and blockchain-based tracking. Providers are deploying AI-driven route optimization, predictive analytics, and real-time inventory visibility to improve delivery accuracy and reduce operational costs.

2. Expansion of Free Trade Zones and Special Economic Areas

The proliferation of specialized logistics zones is reshaping the market landscape as the Kingdom develops integrated facilities offering streamlined customs and tax incentives. SILZ attracts global operators through 50-year tax holidays, enabling faster import-export operations and reducing costs for multinational distribution hubs.

3. Sustainability and Green Logistics Adoption

Environmental sustainability is becoming central as operators align with the Kingdom's 2060 net-zero targets. Companies are integrating electric delivery vehicles, solar-powered warehouses, and carbon-neutral fleet operations. The Saudi Green Initiative drives investments in green logistics solutions across transport and storage.

4. Multimodal Integration and Mega-Event Infrastructure

The upcoming Expo 2030 and FIFA World Cup 2034 accelerate infrastructure buildout across ports, airports, and rail corridors. In November 2024, Alstom signed an SAR 300 million agreement with Saudi Railway Company enhancing the east-west freight corridor, demonstrating continued multimodal connectivity commitment.

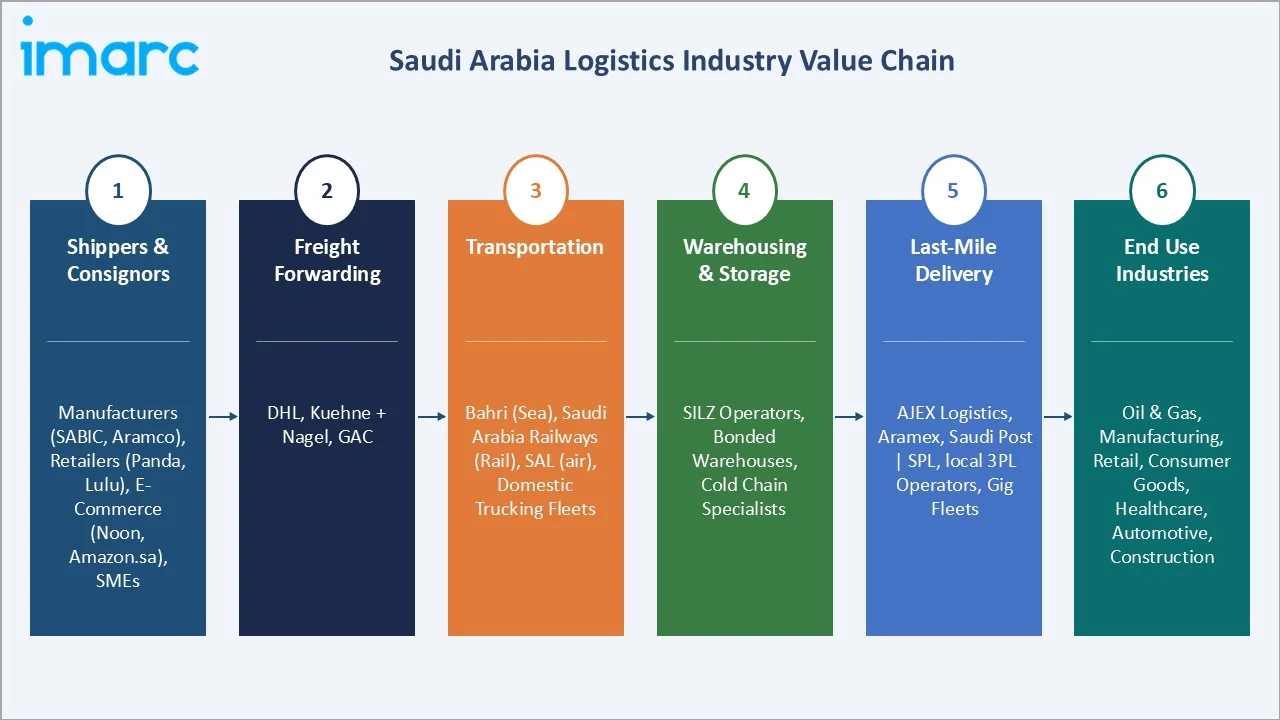

Industry Value Chain Analysis

The Saudi Arabia logistics value chain spans six stages from shipper demand through end-use delivery. Freight forwarding and last-mile delivery capture the highest value-add margins, while transportation and warehousing generate significant working capital requirements favoring well-capitalized integrated operators.

|

Stage |

Key Players / Examples |

|

Shippers & Consignors |

Manufacturers (SABIC, Aramco), Retailers (Panda, Lulu), E-commerce (Noon, Amazon.sa), SMEs |

|

Freight Forwarding |

DHL, Kuehne + Nagel, GAC |

|

Transportation |

Bahri (sea), Saudi Arabia Railways (rail), SAL (air), domestic trucking fleets |

|

Warehousing & Storage |

SILZ operators, bonded warehouses, cold chain specialists |

|

Last-Mile Delivery |

AJEX Logistics, Aramex, Saudi Post | SPL, local 3PL operators, gig fleets |

|

End Use Industries |

Oil & Gas, Manufacturing, Retail, Consumer Goods, Healthcare, Automotive, Construction |

Integrated operators with captive fleets, owned warehouse networks, and in-house technology platforms, such as DHL Supply Chain's 78,000 square meter SILZ hub, achieve cost structures below providers relying on spot capacity procurement. This vertical integration delivers meaningful competitive advantage in commoditized freight and warehousing segments.

Technology Landscape in the Saudi Arabia Logistics Industry

Warehouse Management Systems and Automation

Operators are deploying advanced Warehouse Management Systems (WMS) with automated sortation, robotic picking, and goods-to-person workflows. DHL's SILZ facility features 53,000 square meters of advanced multi-user warehouse space integrating conveyor automation, dimensioning scanners, and cloud-based inventory visibility for technology, retail, and automotive clients.

AI-Powered Route Optimization and Predictive Analytics

Logistics providers leverage AI-driven Transportation Management Systems (TMS) for dynamic routing, demand forecasting, and fleet utilization optimization. Machine learning models process real-time traffic, weather, and delivery window data to reduce fuel consumption, improve on-time delivery rates, and lower per-kilometer operating costs across nationwide fleets.

IoT Sensors and Blockchain-Based Cargo Tracking

IoT-enabled containers, GPS trackers, and temperature sensors provide end-to-end visibility across multimodal shipments. Blockchain platforms enable tamper-proof documentation for customs, proof-of-delivery, and multi-party supply chain coordination, reducing paperwork cycles and disputes across cross-border corridors.

Digital Freight Platforms and Last-Mile Apps

Digital freight-matching platforms connect shippers with trucking capacity through mobile apps, reducing empty miles and improving asset utilization. Consumer-facing delivery apps enable same-day and next-day delivery windows across Riyadh, Jeddah, and Dammam, reshaping e-commerce fulfilment economics.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Model Type | 3 PL | 46.12% | 2025 |

| Transportation Mode | Roadways | 59.08% | 2025 |

| End Use | Manufacturing | 18.07% | 2025 |

| Region | Northern and Central Region | 38.0% | 2025 |

By Model Type

3 PL commands a 46.12% majority share in 2025 owing to enterprise-wide outsourcing of non-core supply chain operations and rising demand for integrated transportation, warehousing, and last-mile solutions.

To access detailed market analysis, Request Sample

2 PL, with 33.58% in 2025, represents traditional asset-based freight carriers handling dedicated point-to-point transportation with limited value-added services. This segment serves bulk shippers, oil and gas operators, and construction materials flows prioritizing carrier reliability and cost over integrated coordination.

4 PL, with 20.30% in 2025, serves premium supply chain orchestration mandates coordinating multiple service providers under a single strategic partner. 4 PL operators deliver end-to-end visibility, network design, and performance management for complex multinational clients with globally distributed manufacturing and distribution footprints.

By Transportation Mode

Roadways dominate transportation mode at 59.08% in 2025, reflecting the Kingdom's 73,000-kilometer highway network enabling flexible door-to-door delivery. The Eastern Expressway connecting Riyadh to Dammam and upgraded bypass highways reduce transit times, supporting faster, reliable road-based supply chain operations across industrial zones.

Seaways, with 16.42% in 2025, capture bulk import-export flows through Jeddah Islamic Port, King Abdulaziz Port at Dammam, and King Abdullah Port. These ports handle container, bulk, and Ro-Ro traffic supporting oil exports, petrochemical shipments, and consumer goods imports from Asian and European gateways.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Northern and Central Region |

38.0% |

Riyadh economic hub; SILZ; e-commerce fulfillment; corporate HQs |

|

Western Region |

27.4% |

Jeddah Islamic Port; King Abdullah Economic City; religious tourism logistics |

|

Eastern Region |

20.6% |

Oil & gas corridor; Dammam port; petrochemical complexes; industrial freight |

|

Southern Region |

14.0% |

Industrial diversification; Jazan Economic City |

Northern and Central region's 38.0% dominance in 2025 is anchored by Riyadh's role as the Kingdom's economic and administrative capital. Riyadh's 2025 population reached 7,952,860, creating substantial consumer demand that supports e-commerce fulfilment and last-mile delivery networks alongside corporate headquarters and manufacturing clusters.

Western region, with 27.4% in 2025, leverages Jeddah Islamic Port handling most Saudi imports, plus King Abdullah Economic City's manufacturing and logistics infrastructure. Religious tourism logistics serving Makkah and Madinah pilgrim flows generate specialized freight, catering, and distribution demand during Hajj and Umrah seasons.

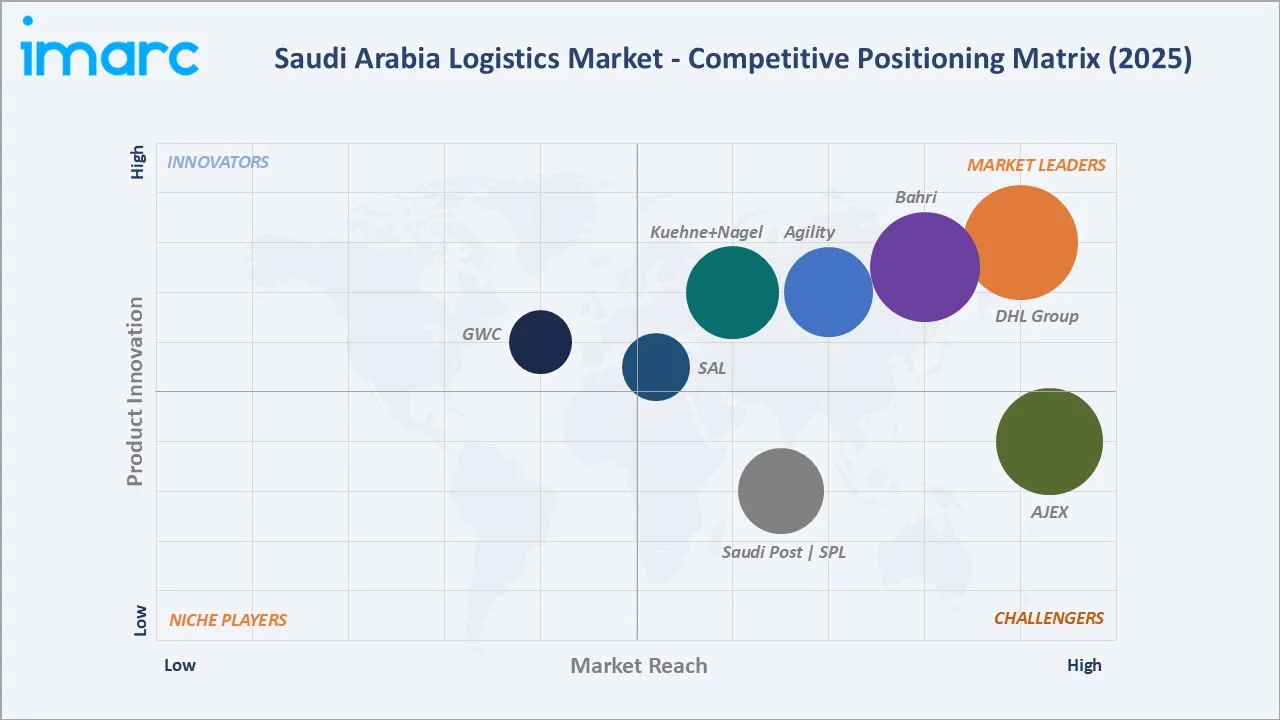

Competitive Landscape

The Saudi Arabia logistics market exhibits a fragmented competitive structure with international integrators and regional operators contesting specialized service segments. Global players expand through strategic acquisitions and joint ventures, while local companies leverage domestic market knowledge and regulatory familiarity to serve traditional industries.

|

Company Name |

Key Services |

Market Position |

Strategic Focus |

|

DHL Group |

Contract logistics, warehousing, e-commerce fulfillment, freight forwarding |

Leader |

SILZ regional distribution hub (under construction, completion Q2 2027); technology & retail; multi-sector |

|

Bahri |

Oil tankers, chemical shipping, dry bulk, logistics solutions |

Leader |

National shipping; energy exports; maritime dominance |

|

AJEX |

Parcel delivery, e-commerce logistics, cross-border shipping, express |

Challenger |

E-commerce specialist; DHL eCommerce partnership |

|

Agility |

Contract logistics, fairs & events, project logistics, freight forwarding |

Leader |

Warehousing scale; Kuwaiti regional leader; GCC network |

|

Kuehne+Nagel |

Sea freight, air freight, road logistics, contract logistics |

Leader |

Global forwarder; Vision 2030 industrial clients |

|

Saudi Post | SPL |

Parcel delivery, e-commerce last-mile, domestic & international post |

Challenger |

National infrastructure; e-commerce enablement |

|

SAL |

Air cargo, ground handling, logistics services |

Leader |

Air cargo specialist; Saudia Group affiliate |

|

GWC |

Logistics, warehousing, freight forwarding, records management |

Emerging |

Qatari player; regional expansion; multi-modal |

Key players DHL Group, Bahri, AJEX, Agility, Kuehne+Nagel, Saudi Post | SPL, SAL, GWC, and others.

Key Company Profiles

DHL Group

DHL group is a leading global contract logistics operator with a major Saudi presence anchored by its SILZ regional hub. The company serves technology, retail, automotive, energy, and e-commerce sectors through integrated warehousing, transportation, and value-added services.

- Services Offered: Contract logistics, 78,000 square meter SILZ hub, e-commerce fulfillment, freight forwarding, cold chain, returns management, technology-enabled supply chain.

- Recent Developments: In November 2025, DHL Supply Chain announced a EUR 130 million investment to establish a 78,000 square meter regional logistics hub at SILZ under a 26-year lease agreement.

- Strategic Focus: DHL's strategy centers on scale advantages from the SILZ mega-hub, multi-sector vertical capabilities, and digital supply chain platforms enabling global clients to consolidate regional distribution through Saudi Arabia, capturing Asia-Europe-Africa transit flows with rapid customs clearance and advanced warehouse automation.

Bahri

Bahri is the Kingdom's national shipping champion, operating one of the world's largest Very Large Crude Carrier (VLCC) fleets. The company delivers oil transportation, chemical shipping, dry bulk, and integrated logistics solutions supporting Saudi Aramco's energy export flows and industrial clients.

- Services Offered: Crude oil shipping, chemical tankers, dry bulk carriers, Ro-Ro liner services, integrated logistics, ship management, and offshore services.

- Recent Developments: In January 2026, Bahri and Hadeed signed a Letter of Intent (LOI) to explore collaboration in maritime transport, with a focus on supporting Hadeed’s iron ore shipping requirements. The agreement outlines plans for both companies to assess how Bahri’s shipping capabilities can be leveraged to meet Hadeed’s logistics needs, while also identifying potential joint opportunities.

- Strategic Focus: Bahri's strategy emphasizes scale in crude and chemical shipping supporting Saudi Aramco and SABIC exports, while investing in liner services and integrated logistics to diversify beyond bulk commodity transport. Fleet renewal and LNG bunkering capabilities position Bahri for energy transition and multimodal growth.

AJEX

AJEX Logistics is a fast-growing Saudi parcel delivery and e-commerce logistics specialist serving domestic and cross-border shipments across the Kingdom and wider Middle East. The company operates integrated sortation hubs, last-mile fleets, and regional express networks.

- Services Offered: Express parcel delivery, e-commerce fulfillment, cross-border shipping, last-mile delivery, returns handling, temperature-controlled express.

- Recent Developments: In October 2025, AJEX Logistics Services has launched Saudi Arabia’s first GMP-GxP compliant logistics facility in Riyadh, marking a major step forward in the Kingdom’s healthcare and life sciences supply chain infrastructure. The purpose-built 3,000-square-meter facility is designed to meet the growing demand for temperature-controlled storage and distribution of pharmaceutical products, positioning AJEX as a pioneer in compliant logistics within the Saudi market.

- Strategic Focus: AJEX focuses on e-commerce-native express delivery, leveraging the DHL eCommerce partnership to combine global network reach with Saudi operational density. Strategic investment in sortation automation, last-mile capacity, and digital customer experience targets share gains as online retail penetration deepens across the Kingdom.

Market Concentration Analysis

The Saudi Arabia logistics market is moderately fragmented with no single operator holding more than 8-10% of total revenue. International integrators compete with national champions across contract logistics, freight forwarding, and express delivery, while regional specialists dominate specific corridors and vertical niches.

Consolidation is accelerating through strategic partnerships and minority acquisitions, such as DHL eCommerce's stake in AJEX Logistics. Private equity and sovereign wealth fund interest in logistics platforms, combined with Vision 2030 PIF-led investments, are reshaping competitive dynamics and driving scale-building across 3PL, warehousing, and last-mile segments.

Investment & Growth Opportunities

Fastest-Growing Segments

3 PL at ~5.1% CAGR through 2034 leads model type growth, driven by e-commerce scale and manufacturing complexity. Roadways at ~4.8% CAGR remains the highest-volume transportation growth engine, supported by highway network upgrades and trucking fleet modernization programs.

Emerging Opportunities

The Southern Region at ~4.5% CAGR is the fastest-growing region through 2034, supported by Jazan Economic City, mining diversification, and regional trade normalization. The Eastern Region benefits from petrochemical expansion and Aramco's downstream investments generating specialized industrial logistics demand.

Venture & Investment Trends

PIF-backed investments in logistics infrastructure, SILZ expansion, and multimodal corridors create platform investment opportunities. Private equity interest in consolidating fragmented 3PL and last-mile operators, plus green logistics funding aligned with the Saudi Green Initiative, generate sustained capital inflows across the sector.

Future Market Outlook (2026-2034)

The Saudi Arabia logistics market is forecast to expand from USD 55.29 Billion in 2025 to USD 83.41 Billion by 2034 at a CAGR of 4.67%, adding USD 28.1 Billion in incremental annual market value. This sustained growth reflects Vision 2030 infrastructure momentum and demographic-driven consumption expansion.

Three forces will most significantly shape the landscape through 2034. Mega-event infrastructure for Expo 2030 and FIFA World Cup 2034 accelerates multimodal buildout. E-commerce penetration drives last-mile densification. AI and automation adoption reshapes warehouse economics, creating scale advantages for technology-enabled 3PL leaders.

Research Methodology

Primary Research

Primary research encompassed structured interviews in 2024-2025 with Saudi Arabia logistics industry stakeholders, including senior commercial managers at international integrators, local fleet operators, SILZ tenants, customs brokers, and end-user supply chain executives across manufacturing, retail, e-commerce, and oil and gas verticals.

Secondary Research

Key secondary sources include Vision 2030 program publications, Transport General Authority (TGA) reports, Saudi Ports Authority data, Saudi Railway Company disclosures, General Authority of Civil Aviation statistics, World Bank Logistics Performance Index, and trade publications covering GCC logistics and Middle East transportation.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models, incorporating GDP growth rates, trade volume data, e-commerce penetration, and infrastructure investment flows. Scenario analysis (base, optimistic, conservative) accounts for macroeconomic uncertainty and Vision 2030 execution risks.

Saudi Arabia Logistics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Model Types Covered | 2 PL, 3 PL, 4 PL |

| Transportation Modes Covered | Roadways, Seaways, Railways, Airways |

| End Uses Covered | Manufacturing, Consumer Goods, Retail, Food and Beverages, IT Hardware, Healthcare, Chemicals, Construction, Automotive, Telecom, Oil and Gas, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | DHL Group, Bahri, AJEX, Agility, Kuehne+Nagel, Saudi Post | SPL, SAL, GWC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Logistics Market Report

The Saudi Arabia logistics market reached USD 55.29 Billion in 2025, reflecting Vision 2030 momentum, e-commerce growth, and strategic trade hub positioning.

The market is projected to reach USD 83.41 Billion by 2034, growing at a CAGR of 4.67% during 2026-2034, driven by infrastructure and mega-event investments.

3 PL leads with 46.12% share in 2025, driven by enterprise outsourcing and demand for integrated transportation, warehousing, and last-mile solutions.

Roadways lead at 59.08% in 2025, reflecting the 73,000-kilometer highway network enabling flexible door-to-door delivery across industrial and urban centers.

Northern and Central Region commands 38.0% share in 2025, driven by Riyadh's hub status, SILZ, and major distribution centers serving nationwide demand.

3 PL at ~5.1% CAGR and the Southern Region at ~4.5% CAGR are the fastest growing through 2034, driven by e-commerce scale and industrial diversification.

Leading companies include DHL Group, Bahri, AJEX, Agility, Kuehne+Nagel, Saudi Post | SPL, SAL, GWC, and others.

Key drivers include Vision 2030 infrastructure investments, e-commerce expansion, strategic geographic positioning, manufacturing growth, and free trade zone proliferation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)