Saudi Arabia Medical Imaging Equipment Market Size, Share, Trends and Forecast by Equipment Type, Modality, Application, End User, and Region, 2026-2034

Saudi Arabia Medical Imaging Equipment Market Overview:

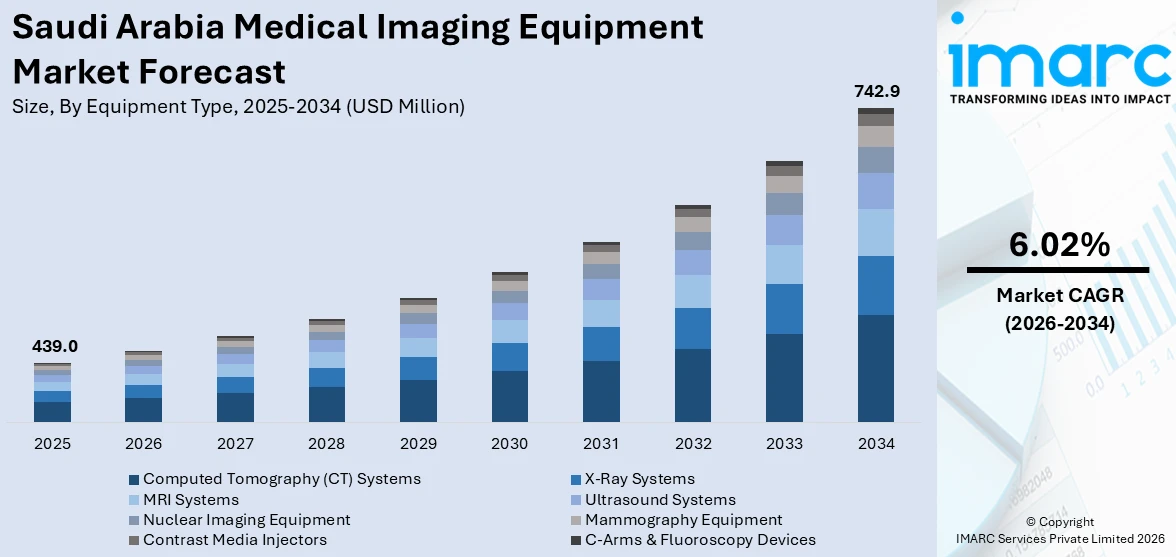

The Saudi Arabia medical imaging equipment market size reached USD 439.0 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 742.9 Million by 2034, exhibiting a growth rate (CAGR) of 6.02% during 2026-2034. Rising healthcare investments, increasing chronic disease prevalence, expanding medical tourism, government initiatives like Vision 2030, technological advancements, growing elderly population, demand for early diagnosis, AI integration, improved healthcare infrastructure, and expanding private sector participation are driving Saudi Arabia's medical imaging equipment market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 439.0 Million |

| Market Forecast in 2034 | USD 742.9 Million |

| Market Growth Rate 2026-2034 | 6.02% |

Saudi Arabia Medical Imaging Equipment Market Trends:

AI-Driven Imaging and Smart Diagnostics

AI is changing how medical imaging works in Saudi Arabia. It's making diagnosis more accurate and faster. AI tools can analyze images and spot problems quickly. This means fewer mistakes when doctors read scans. With the Saudi government prioritizing AI-driven healthcare under Vision 2030, hospitals are rapidly adopting machine learning algorithms for improved radiological interpretations. A 2023 report by the Saudi Ministry of Health says that AI can boost detection rates for serious conditions like lung cancer and heart disease by 30%. That helps lower the chances of misdiagnosis. Also, AI is speeding up how quickly doctors get radiology reports. Some places have seen report times drop by 40%, which is great since patient numbers are rising. Additionally, the commercial sector is making significant investments in AI-enhanced imaging. With the goal of increasing scan interpretation efficiency by 20% by 2025, King Faisal Specialist Hospital & Research Centre stated in 2024 that it will be collaborating with AI companies to include deep learning models for MRI and CT scans. The National Center for AI in the Kingdom has also started projects to hasten the use of AI in medical imaging, which will support market expansion.

To get more information on this market Request Sample

Expansion of Public-Private Partnerships (PPPs) in Healthcare Imaging

The medical imaging industry in Saudi Arabia is growing quickly. This is mostly because of new partnerships between the government and private companies. These partnerships help fund better imaging technology in hospitals and clinics. The Saudi Investment Ministry says that projects in medical imaging could grow by 35% from 2023 to 2025. This will help hospitals buy modern MRI, CT, and PET-CT scanners. The Ministry of Health has initiated a PPP model for radiology services, with private investors financing cutting-edge imaging centers in Riyadh, Jeddah, and Dammam. Initiated in 2023, the Health Holding Company (HHC) is one such project that oversees private investments in imaging infrastructure. This company will manage private imaging investments and aims to outfit over 50 public hospitals with advanced radiology devices by 2024. With this upgrade, the imaging capacity in the country will be boosted by 25%. Moreover, SAR 1.2 billion, or approximately $320 million, is being invested by the Saudi Industrial Development Fund towards domestic imaging gadget production. This will reduce the country's reliance on imports. Saudi hospitals also signed long-term agreements with significant players such as Siemens Healthineers and GE Healthcare. Saudi Arabia, driven by the priorities of the country under its National Industrial Development and Logistics Program (NIDLP), is all set to observe strong growth of locally assembled diagnosis devices in the market by the year 2025.

Saudi Arabia Medical Imaging Equipment Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the region/country level for 2026-2034. Our report has categorized the market based on equipment type, modality, application, and end user.

Equipment Type Insights:

- Computed Tomography (CT) Systems

- X-Ray Systems

- MRI Systems

- Ultrasound Systems

- Nuclear Imaging Equipment

- Mammography Equipment

- Contrast Media Injectors

- C-Arms & Fluoroscopy Devices

The report has provided a detailed breakup and analysis of the market based on the equipment type. This includes computed tomography (CT) systems, X-ray systems, MRI systems, ultrasound systems, nuclear imaging equipment, mammography equipment, contrast media injectors, and C-arms & fluoroscopy devices.

Modality Insights:

- Stand-Alone Devices

- Portable Devices

- Hand-Held Devices

A detailed breakup and analysis of the market based on the modality have also been provided in the report. This includes stand-alone devices, portable devices, and hand-held devices.

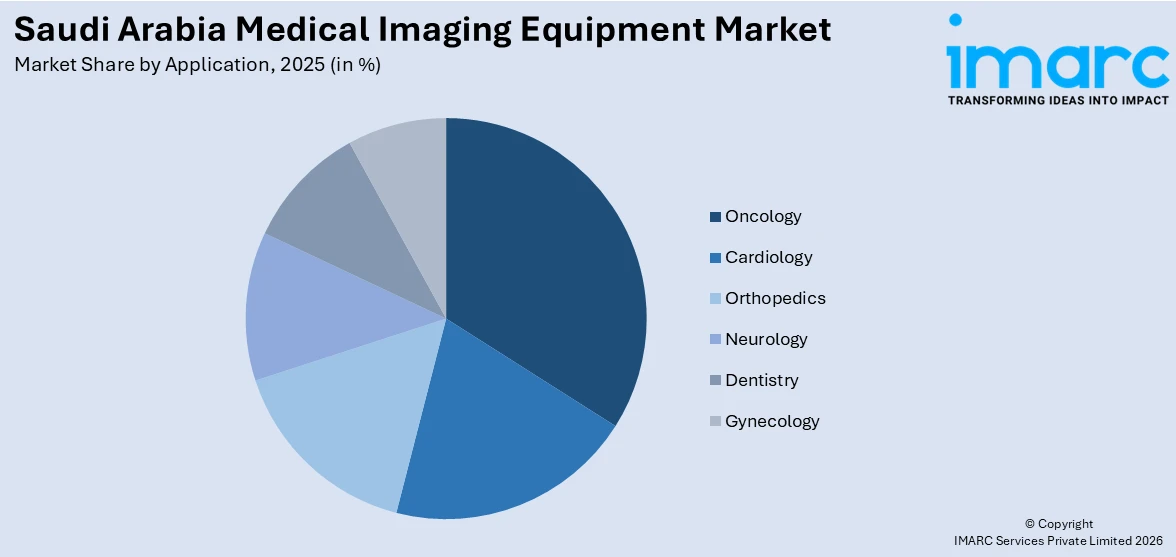

Application Insights:

Access the comprehensive market breakdown Request Sample

- Oncology

- Cardiology

- Orthopedics

- Neurology

- Dentistry

- Gynecology

The report has provided a detailed breakup and analysis of the market based on the application. This includes oncology, cardiology, orthopedics, neurology, dentistry, and gynecology.

End User Insights:

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Surgical Centers

- Specialty Clinics

- Research Institutes

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes hospitals, diagnostic imaging centers, ambulatory surgical centers, specialty clinics, and research institutes.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

The report has also provided a comprehensive analysis of all the major regional markets, which include Northern and Central Region, Western Region, Eastern Region, and Southern Region.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Saudi Arabia Medical Imaging Equipment Market News:

- February 2025: United Imaging, a top company in medical imaging and radiotherapy, has expanded its strategic partnership with Al Mana Group, one of the biggest medical groups in Saudi Arabia. They aim to improve diagnosis and treatment using CT, radiotherapy, molecular imaging, and AI.

- November 2024: GE HealthCare teamed up with Dr. Sulaiman Al-Habib Medical Services Group to bring in new tech for radiology. They were using AI and imaging tools. This partnership supports Vision 2030, making it easier for more people in Saudi Arabia to get high-quality medical care.

Saudi Arabia Medical Imaging Equipment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Equipment Types Covered | Computed Tomography (CT) Systems, X-Ray Systems, MRI Systems, Ultrasound Systems, Nuclear Imaging Equipment, Mammography Equipment, Contrast Media Injectors, C-Arms & Fluoroscopy Devices |

| Modalities Covered | Stand-Alone Devices, Portable Devices, Hand-Held Devices |

| Applications Covered | Oncology, Cardiology, Orthopedics, Neurology, Dentistry, Gynecology |

| End Users Covered | Hospitals, Diagnostic Imaging Centers, Ambulatory Surgical Centers, Specialty Clinics, Research Institutes |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Saudi Arabia medical imaging equipment market performed so far and how will it perform in the coming years?

- What is the breakup of the Saudi Arabia medical imaging equipment market on the basis of equipment type?

- What is the breakup of the Saudi Arabia medical imaging equipment market on the basis of modality?

- What is the breakup of the Saudi Arabia medical imaging equipment market on the basis of application?

- What is the breakup of the Saudi Arabia medical imaging equipment market on the basis of end user?

- What are the various stages in the value chain of the Saudi Arabia medical imaging equipment market?

- What are the key driving factors and challenges in the Saudi Arabia medical imaging equipment market?

- What is the structure of the Saudi Arabia medical imaging equipment market and who are the key players?

- What is the degree of competition in the Saudi Arabia medical imaging equipment market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia medical imaging equipment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia medical imaging equipment market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia medical imaging equipment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)